Overview

- The global economy is grappling with a new geopolitical jolt. The war in the Persian Gulf is both another uncertainty shock and an energy shock. Oil and gas prices have already risen, but the ultimate macro consequences will depend on the duration and intensity of the disruption to energy supplies.

- History tells us that energy shocks can have significant macro implications, but that outcomes are not mechanical. Large and persistent energy shocks can boost inflation and depress growth. But the scale of the damage usually depends on a range of factors including pre-existing supply-demand balances, the extent of available buffers and the broader macro environment.

- ‘Chokepoint risk’ is a key factor this time, as prolonged disruption to flows through the Strait of Hormuz would affect a large share of global oil and LNG exports. Significant damage to key regional energy infrastructure is another important risk to supply, given Tehran’s strategy of broadening the conflict.

- For Australia, the prospect of higher energy prices – while good news for our terms of trade and government tax revenues – comes at an awkward time. An increase in the headline rate of inflation would further complicate life for the RBA, given that inflation is already above target and the central bank is contemplating further tightening.

In this edition, we consider some of the potential economic consequences of the escalating war in the Persian Gulf, drawing on the history of previous conflict-driven energy shocks. We also review a busy week for Australian economic data, including the December quarter 2025 national accounts. Next week, I will be at the AICD’s Australian Governance Summit. If you are attending and get the chance, please do say ‘hello.’ It’s always lovely to meet readers. This also means that after two bumper editions, next week’s offering will have to be a much slimmed down version. Which I suspect will be a relief all round…

Last week, we said global economic resilience was being subjected to a series of stress tests, citing ongoing trade policy, geopolitical, technological and financial market uncertainty and referencing the elevated risk of a US-Iran conflict. The day after publication, on Saturday 28 February, Washington launched Operation Epic Fury, triggering a new phase of conflict in the Middle East.

At this stage, it is hard to gauge the overall economic and geoeconomic implications. Instead, analysis has focused on the likely scope of the disruption to energy supplies and consequences for commodity prices, inflation, asset prices and monetary policy. Below, we review historical lessons from conflict-driven energy price shocks and also consider implications for the Global and Australian economic outlooks.

Here in Australia, although inevitably overshadowed by the intensification of conflict in the Persian Gulf, it has been a busy week on the domestic data front. Top of the bill were December quarter 2025 national accounts which showed annual growth beating expectations and accelerating to 2.6 per cent. That was positive news in terms of stronger activity relative to the lacklustre growth performance that preceded it, delivering another lift in GDP per capita. But growth was also uncomfortably above where the RBA thinks the Australian economy’s speed limit is now to be found. There were also new numbers on the housing market, job ads, the current account, government finance and more. We provide a quick roundup below.

Another uncertainty shock…and an energy shock

War in the Persian Gulf is the latest uncertainty shock to hit the global economy.

Although the sequence of the so-called ’12-day war’ in June last year, threats of US Intervention in Iran earlier this year, and the buildup of US forces in recent weeks all meant the outbreak of fighting was far from unexpected, there are still plenty of unknowns. These range from the short term (how long will the conflict last, how many other countries will be drawn in, how will it end) to the longer term (how will this shift the balance of power in the Middle East, how will the new Trump Way of War change geopolitics?). As readers will no doubt be tired of reading by now, uncertainty shocks tend to be negative for economic activity, by encouraging households to delay consumption and firms to delay investment (although last year, the global economy proved surprisingly resilient in the face of elevated levels of uncertainty).

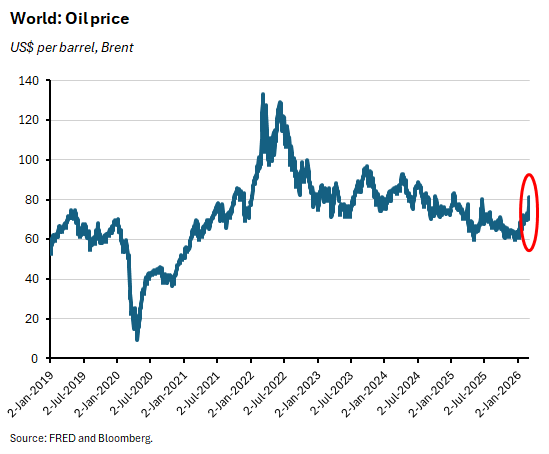

Crucially, as well as an uncertainty shock, the war is also in the process of triggering an energy shock. There have already been marked increases in the price of oil and gas. At the time of writing, Brent had risen by about 25 per cent over the previous month and pushed through US$80/barrel (b) to around US$83/b (after having earlier reached US$85/b). European gas prices as measured by the Dutch TTF futures benchmark had jumped from around 30 euros per Megawatt hour (MWh) before the war to more than 50 euros/MWh and at times had approached 60 euros/MWh during trading.

If they persist, those increases are already large enough to have a material effect on global economic outcomes: The IMF’s helpful rule of thumb is that a sustained 10 per cent increase in oil prices would lower global output by about 0.15 percentage points in the following year and increase global inflation by about 0.4 percentage points. That said, oil and gas prices currently remain well below the kind of levels they reached in 2022, indicating that for now at least, the shock is considerably smaller.

The energy and uncertainty shocks are intertwined, since at this point the size and duration of any spike in energy prices and therefore the ultimate implications for growth and inflation are…you guessed it…highly uncertain.

History lessons on war, energy and economics

This is far from the first time that conflict in the Middle East has threatened global energy markets and the outlook for the world economy. Past examples include the 1956-57 Suez Crisis, the 1973-74 Arab oil embargo in response to the Yom Kippur War, the 1978-79 Iranian Revolution, the 1980-88 Iran-Iraq war, and the 1990 Iraq invasion of Kuwait. More recent disruptions include the 2011 Libyan civil war, the 2019 attacks on Saudi oil facilities and the prolonged imposition of sanctions on the Iranian regime. Another and more recent example of a conflict-driven shock to global commodity markets originated outside the region, when the Russian invasion of Ukraine in 2022 triggered sharp price increases for energy and some food products.

This historical record shows that war has the potential to trigger substantial disruptions to supply and therefore the price of energy. Mostly, this has been an oil price story, but more recently (with the Ukraine war a prominent example), the economic impact has also been felt through the price of natural gas.

Inflation is another key part of the shock transmission mechanism. A recent review of the experience with global inflation between 1970 and 2022 found that global oil price shocks have been the main driver of variations in headline (but not core) inflation over the period, accounting for more than 38 per cent. That compares to around 28 per cent for demand shocks and smaller contributions from global supply shocks and global interest rate shocks. The review finds that oil price and demand shocks have also tended to be the main drivers of movements in global inflation around every global recession since 1970.

Moreover, under some circumstances, large price shocks can have destabilising consequences that extend beyond higher inflation and lower activity, as seen in stagflationary shocks of the 1970s that contributed to large scale economic regime change (the shift from the post-war Keynesian consensus to 1980s neoliberalism).

Importantly, however, (as we’ve noted several times before), analysis of this same historical record also tells us that there is no simple, mechanical relationship between an oil price shock and global economic developments.

At one end of the spectrum, we have those two 1970s oil shocks. The first involved an OPEC embargo which led to the removal of about 4.3 million barrels per day (mbpd) from the market over a five-month period (equivalent to about 7.5 per cent of global supply at the time) while OPEC also quadrupled the official price of oil. That shock generated a jump in global inflation and the onset of the 1975 recession. In the case of the second, up to 5.5mbpd of oil were withdrawn from the market over a six-month period as the disruption triggered by the Iranian Revolution caused oil prices to more than double. Again, there were stagflationary consequences, with a sharp increase in global inflation and a steep downturn in global economic activity.

Then there is the 1980-88 Iran-Iraq war, which removed upwards of four mbpd from global markets and the 1990 Iraq invasion of Kuwait, which again removed more than four mbpd and initially caused prices to double. Both shocks were associated with an increase in global inflation in the late 1980s and early 1990s, but in this case the consequences were much less dramatic than their 1970s counterparts.

Right at the other end of the spectrum, last year’s ‘12-day war’ saw oil prices briefly jump by about US$10/b during the conflict, before retreating equally rapidly once the bombing campaign had concluded.

One key lesson is the economic magnitude of an energy shock will partly be a function of the size and duration of the direct disruption to supply. This in turn will be determined by the duration and intensity of conflict, as well as by strategies pursued by and relative capabilities of, the combatants. But a second key lesson is that the scale of the international economic fallout will also be a function of the broader mix of the supply and demand conditions prevailing at the time of the shock and of the overall macroeconomic environment.

On the supply side, key factors will include the degree of pre-conflict tightness in energy markets, the availability of alternative sources of supply (a product of the degree of geographic and geopolitical diversification in oil suppliers), and the size (plus the ability and willingness to deploy) of strategic energy reserves.

On the demand side, the prevailing level of the global economy’s reliance on oil will be important. This in turn will be driven in part by structural forces such as the current oil intensity of production (that is, the amount of oil that is required to produce one unit of GDP), which has fallen from 0.12 tonnes of oil equivalent (toe) in 1970 to 0.05 toe by 2022. Demand will also be influenced by the prevailing cyclical strength of world economic growth and the consequent pressure on global oil demand.

Scaling potential supply shock: ‘Chokepoint risk’ and Strait of Hormuz

Drawing on this framework, what can we say about the potential size of any supply shock?

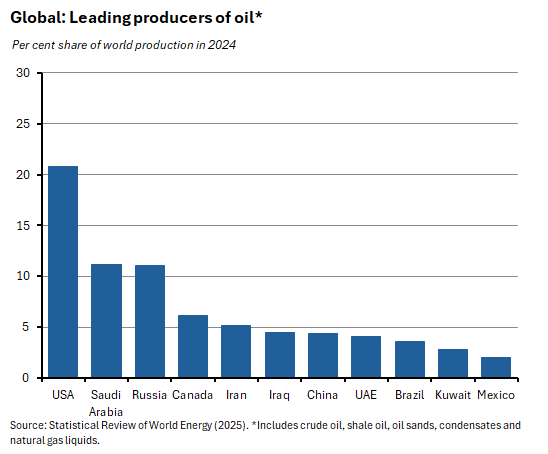

Start with Iran’s share of world oil production, which according to the Energy Institute’s Statistical Review of World Energy was about five mbpd in 2024, or about 5.2 per cent of the world total.

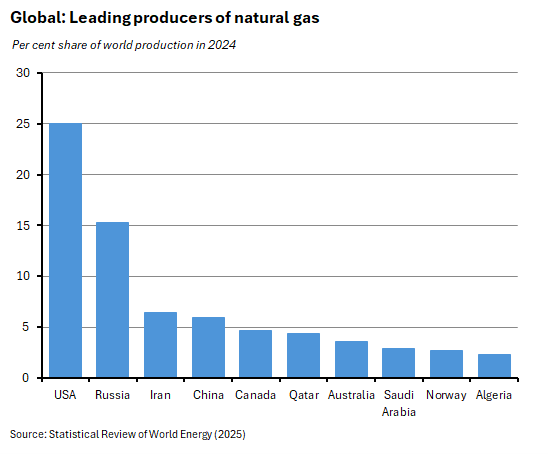

According to the same source, in the same year, Iran’s production of natural gas was about 263 billion cubic metres or 6.4 per cent of the world total.

Iran’s export numbers are considerably lower. The International Energy Agency (IEA) estimates Iranian crude oil exports averaged 1.6mbpd in 2024, nearly all of which ended up in China, for use in independent ‘teapot’ refineries, while the latest OPEC statistical bulletin puts Iranian exports of crude and petroleum products at around 1.98 mbpd. All of which makes Iran a significant player in global energy markets, but not a key exporter.

Importantly, however, the potential for a shock to energy supplies in this case goes well beyond a disruption of Iranian production and exports. Markets have been particularly focused on the risk to the transit of energy supplies through the Strait of Hormuz, or on ‘chokepoint risk.’

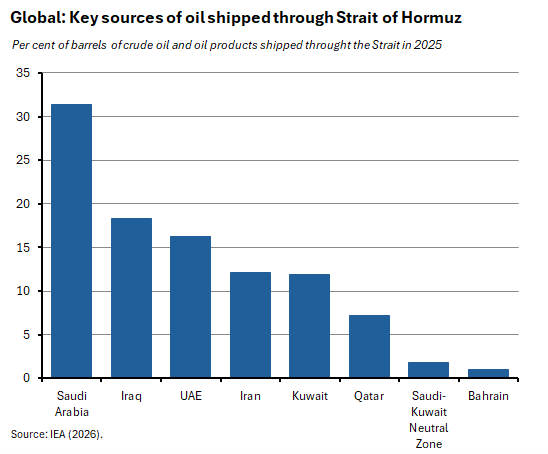

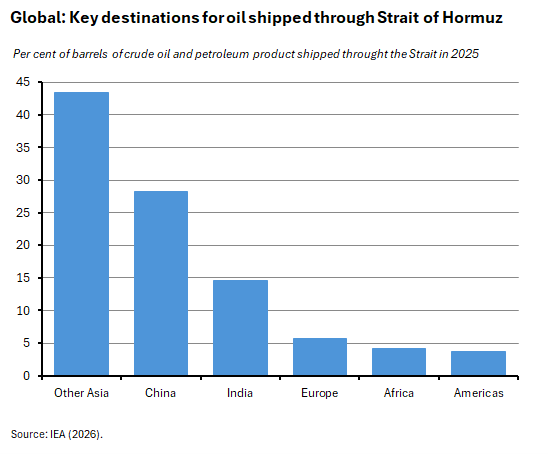

The US Energy Information Administration (EIA) provides a handy summary of world oil transit chokepoints, listing the two most important global chokepoints for crude oil and petroleum liquids as the Strait of Malacca and the Strait of Hormuz. According to later EIA estimates, in 2024, oil flow through the Strait of Hormuz averaged 20 mbpd, or the equivalent of about 27 per cent of world maritime oil trade or around 20 per cent of global petroleum liquids consumption. More recent estimates from the International Energy Agency (IEA) reckon that again nearly 20mbpd of oil and oil condensates were exported via the Strait last year, led by exports from Saudi Arabia, Iraq and the UAE.

Most of this oil went to Asia, with China and India particularly important recipients, as well as Japan, South Korea and other regional economies.

According to the IEA, alternative oil export routes are limited, with only Saudi Arabia (in the form of the Abqaiq-Yanbu pipeline system or the East-West Crude Pipeline) and the UAE (with the Abu Dhabi Crude Oil Pipeline) possessing operational pipelines that would allow flows to avoid the Strait. The IEA thinks they might allow for an additional 3.5 mb/d to 5.5 mb/d of export capacity – well short of the volumes that normally transit the Strait.

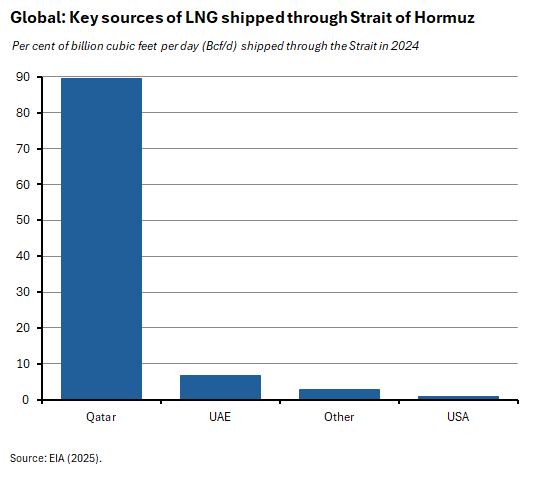

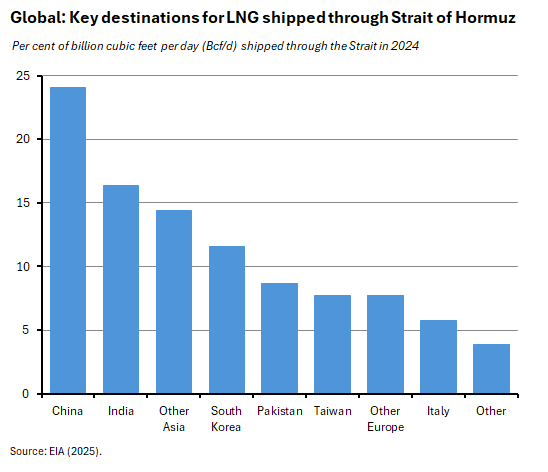

Moreover, one feature that makes this regional energy shock different from its predecessors (but not from the Ukraine-Russia shock of 2022) is the increased role of natural gas in the global energy trade. In this context, the IEA notes that, excluding deliveries to Kuwait, all LNG exports from Qatar and the UAE transit the Strait. It reckons that last year, the total volume of LNG shipped this way comprised almost 20 per cent of global trade in LNG, with almost 90 per cent of that headed for the Asian market.

Earlier estimates from the EIA also highlight the dominant role of Qatar in LNG shipments and of Asian economies as destinations, although note that some significant early price action is also being felt in Europe, where gas prices earlier this week rose to their highest level since 2023.

These ‘chokepoint risks’ are now very much in play. Iranian forces have warned vessels against passing through the Strait and at least six tankers have been hit since the war began. Insurance and shipping rates had soared to record highs by the start of this week, and at the time of writing, shipping through the Strait had reportedly ground to a halt, leading to a collapse in seaborne oil exports. Washington has said the US navy could start escort operations through the Strait at some point and suggested that the US Development Finance Corporation could provide risk insurance and guarantees for tankers. In the meantime, however, the cost of insurance has since jumped more than 12-fold.

The longer any closure is assumed to be, the higher the price of energy is expected to go. During last year’s 12-day war, market analyst estimates of the impact of a closure of the Strait had ranged from US$80/b – US$130/b and similar estimates have been doing the rounds over the past week.

It is also worth noting that ‘chokepoint risk’ extends beyond energy. The Strait is also one of the most significant bottlenecks for global fertilisers, with perhaps 30 to 35 per cent of global urea exports (from Qatar, Iran, the UAE, Bahrain and Saudi Arabia) at risk. It also accounts for a significant share of trade flows in phosphates and sulphur. And there are also potentially significant adverse implications for Middle East food imports.

Scaling potential supply shock: Energy infrastructure risk

The risk to energy supply goes beyond ‘chokepoint risk.’

There is also the threat of escalating damage to regional oil and gas infrastructure as the conflict spreads across the Persian Gulf, in line with Tehran’s apparent strategy to broaden the war. Qatar, for example, has already reported that it halted LNG production after intercepting two Iranian drones targeting the critical Ras Laffan energy facility and LNG hub, which is the world’s largest LNG facility. Similarly, the Saudi government said it had intercepted and destroyed two drones that had tried to attack the Ras Tanura refinery – one of the region’s largest refineries and a key export terminal for Saudi crude.

Pre-conflict energy situation offers some comfort

Sticking with the same framework, another important lesson from history is that prevailing demand and supply conditions in global energy markets, along with the presence of alternative suppliers or significant buffer stocks, will also influence outcomes.

In the case of the oil market, the pre-war position looked relatively benign. For example, at the start of this year, the EIA was reporting that across the course of 2025, crude oil prices (measured as the Brent crude oil spot price) had fallen from a monthly average of US$79/b in January to US$63/b by December, despite the June 2025 strikes on Iran and the disruption created by the ongoing Russia-Ukraine war. Overall, the annual average price last year was just US$69/b, the lowest since pandemic-ravaged 2020. The EIA also estimates that global production of crude oil and liquid fuels outpaced consumption across 2025, leading to the largest implied stock build recorded since 2000 (aside from COVID-19-disrupted 2020), with particularly large crude oil inventory increases by China. Consistent with this story, as recently as early February this year, before the outbreak of war in the Persian Gulf, the EIA was forecasting lower oil prices for 2026 and 2027, on the expectation that production of petroleum and other liquids would continue to exceed demand, leading to prices falling to an average of US$58/b this year and US$53/b in 2027.

Likewise, the starting point for the IEA’s recent assessment of global oil market conditions is that the market had been in significant surplus since the start of 2025 and that prior to 28 February 2026, global oil supply was again expected to far exceed demand through this year. For example, according to the February 2026 Oil Market Report, global oil demand was forecast to rise by less than 0.9mbpd this year, versus a projected increase in world oil supply of 2.4mbpd.

In terms of stocks, the IEA says global oil inventories rose to more than 8.2 billion barrels in 2025 - reaching their highest level since 2021 - and reports that IEA members hold more than 1.2 billion barrels of public emergency oil stocks.

What about the scope for alternative oil suppliers? At a 1 March meeting of eight OPEC+ members, the group agreed to increase production by 206kbpd from April this year. An important complication here, however, is that the bulk of this promised increase is expected to come from countries (Saudi Arabia, Iraq, Kuwait, and the UAE) that are exposed to the current conflict and to the ‘chokepoint risk’ analysed above. Beyond OPEC, scope for rapid increases may be limited. Some US shale producers, for example, have said it would likely take months before they would deliver a big increase in output.

Turning to natural gas, the IEA reports that prior to the current conflict, markets were gradually rebalancing following dislocation generated by the February 2022 Russian invasion of Ukraine. In the medium term, the agency had anticipated that a wave of new LNG capacity would come online between this year and the end of this decade and by boosting supply would reshape market dynamics. But in the meantime, it judged that market conditions were ‘tight’ in the first two months of this year. As a result, it now warns for example that an ‘extended loss of output from the Ras Laffan facility in Qatar could significantly exacerbate this market tightness’.

What about global macro risk?

The next piece of the puzzle is the state of the global macroeconomic environment.

Back at the start of this year, the baseline scenario for the world economy was for ‘more of the same,’ with the IMF expecting the rate of world real GDP growth in 2026 to be much like the outcome for 2025. That scenario assumed helpful tailwinds from continued monetary policy easing, as well as from fiscal stimulus plus ongoing resilience in the face of a series of downside risks reflecting the possibility of trade policy shocks, geopolitical tensions, AI-related financial market dislocations, mounting debt burdens (on which see this week’s further reading recommendations, below) and more.

Obviously, current events in the Middle East represent the manifestation of some of that geopolitical risk and – by pushing up prices and thereby threatening progress on disinflation – they also pose some new questions over that assumption of a benign monetary policy environment going forwards.

At the same time, higher energy prices and more uncertainty will also hit consumer disposable income and harm household and business sentiment.

The distribution of the economic fallout will also influence the global picture. At this stage, early losers look likely to be the energy-importing economies of Europe and Asia, while energy exporters with production or trade routes not directly exposed to the Gulf conflict, including the United States and Russia are more insulated and may even benefit, at least in terms of their energy export revenues.

Uncertainties created by the war also add to existing uncertainties and sensitivities around the current level of equity market valuations. Market volatility in recent weeks had already served as one indicator of nervous investors and now there are more negative scenarios for market participants to worry about.

Implications for Australia – inflation, interest rates and activity

Economic implications for Australia are similar to the global macro story, albeit influenced by our different position in the monetary policy cycle and modified by our status as a significant energy exporter.

Higher energy prices and in particular higher oil prices will feed directly into headline inflation via higher transport costs (the Transport group has a weight of 11.45 per cent in the Consumer Price Index including a weight of 3.35 per cent for Automotive fuel) as a rise in fuel prices will directly push up the headline rate (although it will have less influence on the RBA’s preferred measure of underlying inflation, the trimmed mean). There will also be indirect increases via higher input costs.

The resultant increase in prices will complicate life for Martin Place. True, the simple ‘just so’ version of central bank policy here would say that monetary policy should look through a temporary supply shock. But for the RBA, this conventional wisdom is complicated in practice by the broader economic position. After all, both headline and underlying inflation are already above target and have been for some time. The latest inflation reading has just come in relatively hot; the RBA has started to tighten monetary policy anyway and more tightening was anticipated even before the 28 February shock. The Monetary Policy Board (MPB) has pledged to ‘do what it considers necessary’ to return inflation to target; and the latest quarterly GDP growth numbers (discussed below) suggest an economy running well above its speed limit. All of which makes a passive response look tricky.

In this context, in a Q&A session following a speech this week, Governor Michele Bullock first explained that – like everyone else – the RBA was unsure about what would happen next, and that Martin Place would ‘be doing more work on particular scenarios’. She then went on to say:

‘…with a supply shock occurring in a situation where we already have high inflation, I think there is a risk that inflation expectations may start to move. So that will be something, I think, that will be at front of mind for the Board. Are we in a position where it’s difficult to look through, particularly if it’s an elongated shock?...we already have elevated inflation and I think there is a risk that inflation expectations might become a little bit unanchored.’

And with specific reference to the upcoming March MPB meeting, she added:

‘I’m not making a prediction about March, but it will be a live meeting. We have inflation at 3.8 per cent headline and we have unemployment at 4.1…The Board will be actively looking at whether or not it needs to move more quickly.’

Higher energy prices will also exacerbate the current cost of living squeeze on households, hurting consumer sentiment, which tends to respond quite quickly to movements in petrol prices. There is also some risk that war news and the attendant uncertainty could further undermine consumer and business confidence, serving as an additional drag on activity.

At the same time, higher global energy prices are likely to boost Australian export prices. That would lift our terms of trade and via increased resource sector profits, boost corporate tax receipts and thereby help with the budget position. That said, a significant share of any revenue gain will also flow offshore in the form of higher dividend payments to foreign investors, who own around 80 to 85 per cent of the Australian resource sector.

Finally, there are mixed implications for the Australian dollar. All else equal, to the extent that higher uncertainty moves us closer to a ‘risk off’ world, the currency would be expected to weaken. But as just noted, everything else is not equal: the possibility of higher energy prices, higher interest rates and higher terms of trade are all offsetting factors.

Key unknowns: Duration and intensity

Pull all this together and the likely direction of economic outcomes in the short term – upward pressure on prices and downward pressure on activity – seems clear. Less clear is the magnitude of these effects. This will be determined by the duration and intensity of the conflict. The longer and more intense the war, the more likely it is that disruption to energy traffic through the Strait of Hormuz is prolonged and/or that there is greater damage to key regional energy infrastructure.

One initial take on market reactions to date, for example, is that the initial collective view was that the war would look like a re-run of the June 2025 experience and would be over in days. That estimate of the likely duration of conflict now seems to have been revised up to weeks, albeit with a limited degree of confidence.

One way in which analysts think about the potential timing here is in terms of a mechanical race between capabilities. On the one hand, there is a clock running on the supply of US munitions. On the other, there is the ongoing attrition of Iranian launchers and stockpiles. Another approach has stressed the contest between US and Iranian strategies – that is, between the progress with regime destruction on the one hand versus the progress with regional and economic and market destabilisation on the other.

As well as these kinds of calculations, the belief that this is a conflict that is more likely to last weeks than months is also likely based on the assumption that Washington retains the ability to declare victory and move on at a time that suits. This option is aided by a degree of ambiguity as to the ultimate objectives of the attacks launched on 28 February, which seem to have ranged from the destruction of Iranian offensive capabilities through to regime change. If those judgements all prove to be correct, the global economic fallout could prove limited.

But things may not play out this way. Tehran may not cooperate for a start. And at the risk of cliché, it is worth citing Clausewitz here, who reminds us in On War that ‘War is the realm of uncertainty…War is the realm of chance’ and ‘In war more than anywhere else things do not turn out as we expect.’

An expanding arc of instability

One final thought before we turn our attention to this week’s Australian economic news.

For understandable reasons, most of the initial economic and geoeconomic focus on the fallout from the conflict in the Persian Gulf has been on implications for energy supply and prices and what this could mean for the global economy. Yet the longer it goes on, the greater the likelihood that the war will have important implications elsewhere.

For example, those implications could include the impact on a Russian economy that will receive a helpful financial boost from higher oil prices, even as a key regional ally has its military power dismantled. Also an impact on a Ukraine that could see needed arms supplies diverted to the Middle East; plus on a Beijing that will face a higher energy import bill and a search for new suppliers while also bolstering its position as the predictable superpower. And further impacts on Gulf economies that have just been reminded of their vulnerability; and on the future of the ‘Dubai business model’. There could also be consequences for the US midterm elections due later this year.

Step back a bit further and there is also a broader point to be made here about an expanding arc of instability that now reaches from Africa to Afghanistan. The Sahel region of Africa, from Senegal in the West to Eritrea in the East, is marred by violence and disruption, including civil war in Sudan, conflict in Ethiopia and Somalia and rising tensions between Ethiopia and Eritrea. To the North, Libya remains mired in its own civil conflict. In the Middle East there is violence and disruption from Gaza and Lebanon on the shores of the Mediterranean to across the Persian Gulf and Iran. And on 27 February, one day before the launch of Operation Epic Fury, Pakistan’s defence minister declared his country and Afghanistan were now in ‘open war.’

Australian growth surges past speed limit

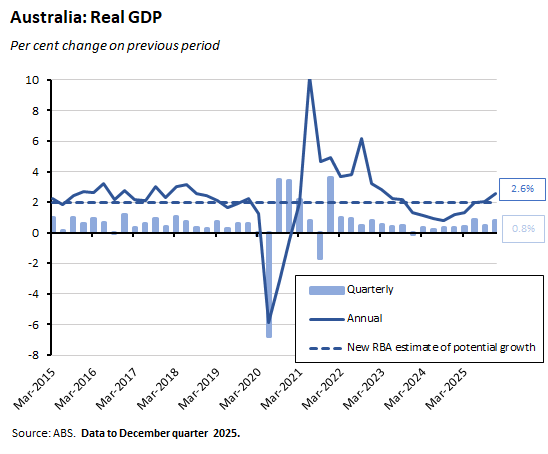

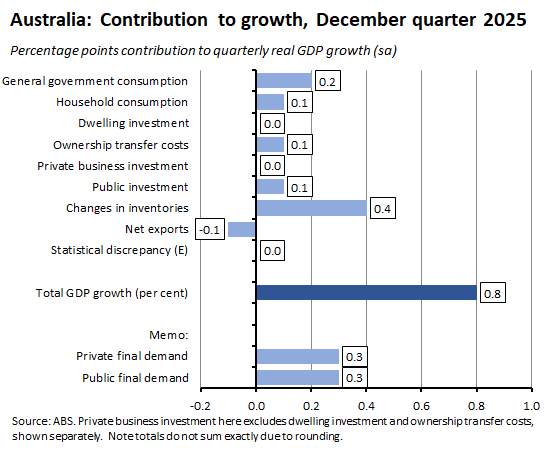

This week the ABS said that Australia’s real GDP grew by a seasonally adjusted 0.8 per cent over the December quarter of last year. That was stronger than an (upwardly revised) 0.5 per cent in the previous September quarter and represented a return to the robust pace of quarterly growth seen in the June quarter 2025. That June quarter result aside, this was the strongest quarterly outcome since December quarter of 2022. On an annual basis, growth ran at 2.6 per cent, its fastest rate since the March quarter 2023.

The results were in line with the market’s expectations for quarterly growth but above the consensus forecast for annual growth of 2.3 per cent. The RBA’s February 2026 Statement on Monetary Policy had likewise pencilled in a 2.3 per cent outcome for the final quarter of last year.

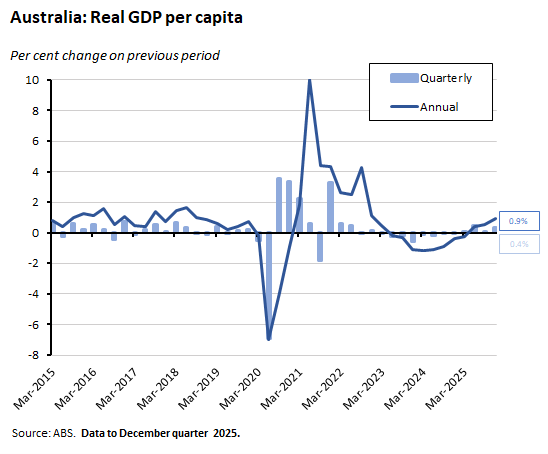

Output growth also ran ahead of population growth again last quarter, with GDP per capita up 0.4 per cent over the quarter – a fourth consecutive rise – and higher by 0.9 per cent over the year. That was the fastest annual pace of growth since the December quarter 2022.

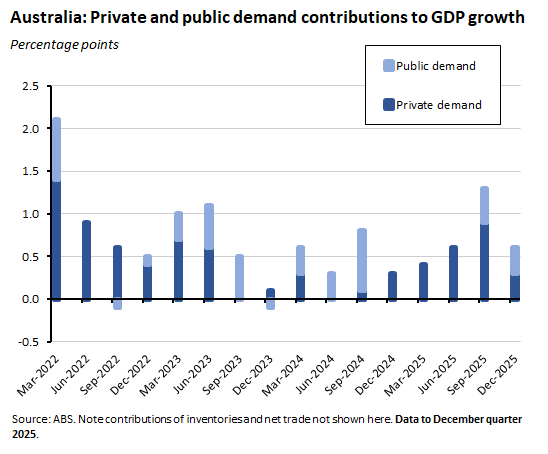

In terms of the drivers of growth, domestic final demand contributed 0.5 percentage points to quarterly GDP growth, with private and public demand each contributing 0.3 percentage points. A rebuild in inventories also contributed 0.4 percentage points to growth while net trade subtracted 0.1 percentage point as the rise in imports outpaced growth in exports.

Digging into the role of private demand shows that household consumption contributed 0.1 percentage point to overall growth last quarter. That reflected a 0.3 per cent quarterly increase in consumption expenditure which translated into 2.4 per cent annual growth. Discretionary spending took the lead, rising by 0.4 per cent quarter-on-quarter and 2.5 per cent year-on-year, which the ABS attributed to consumers taking advantage of Black Friday sales and strong attendance at sporting events and concerts. Spending on essentials was up 0.2 per cent in quarterly terms and 2.4 per cent on an annual basis, with the softer spending in part an artifact of government electricity rebates (which reduce household expenses and appear as government expenditure).

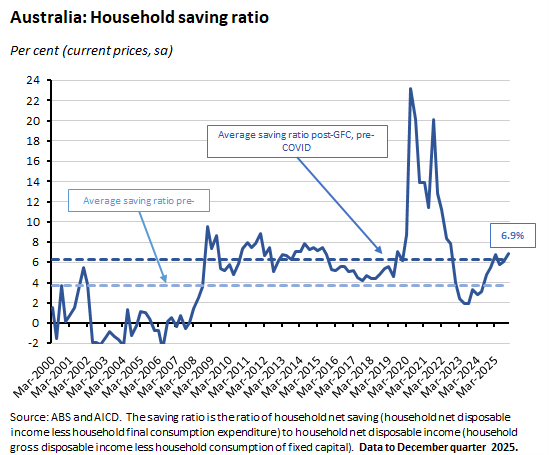

Sticking with households for a moment, the ABS also reported that the rise in nominal gross disposable income over the December quarter was 1.8 per cent, which exceeded growth in nominal spending of 1.1 per cent. As a result, the household saving ratio increased to 6.9 per cent, its highest rate since the September quarter 2022.

Returning to the quarter’s growth drivers, the balance of the contribution from private demand to GDP growth came from private investment, which rose 0.7 per cent over the quarter, five per cent over the year, and contributed 0.1 percentage points to quarterly growth. Private investment has now grown for the past five quarters. Within that total, dwelling investment was up 0.6 per cent quarter-on-quarter and 5.5 per cent year-on-year, while private business investment rose 0.2 per cent quarter-on-quarter and 3.9 per cent year-on-year.

In the case of public demand, government consumption rose 0.9 per cent over the quarter and 3.3 per cent over the year, adding 0.2 percentage points to GDP growth. Public investment grew 0.9 per cent over the quarter, but was down 0.9 per cent over the year, contributing a further 0.1 percentage point to GDP growth.

Speed limits, productivity growth and unit labour costs

The positive news in these December quarter numbers was that the Australian economy accelerated into the final quarter of last year, putting behind it the run of anaemic, sub-two per cent growth that was the norm between the December quarter 2023 and the June quarter 2025. This also pushed the prolonged ‘per capita recession’ further into the rear-view mirror.

The not-so-good news is that at 2.6 per cent, annual growth is running well-ahead of the RBA’s estimate of the economy’s current speed limit, which it thinks is much closer to two per cent. As noted in the previous discussion, put that together with a tight labour market and above-target inflation, and the case for additional monetary policy tightening is apparent.

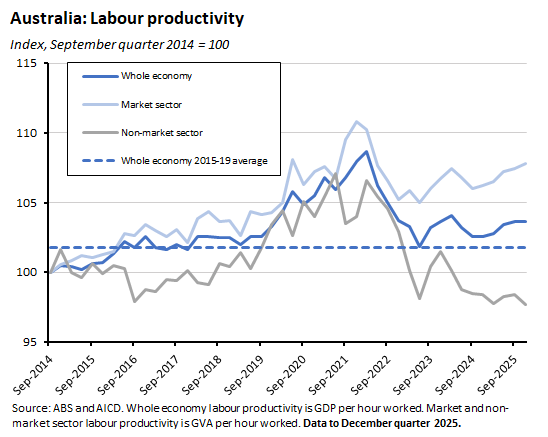

Still, there were also some hopeful signs for Martin Place (and the rest of us) on the economy’s productive potential in the quarterly numbers. Although GDP per hour worked was flat over the December quarter, that still translated into annual growth in labour productivity of one per cent.

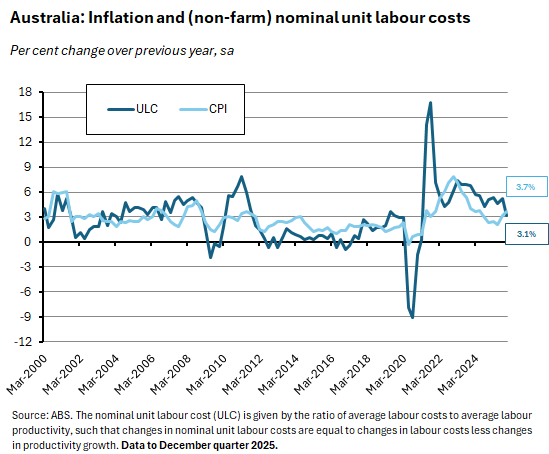

At the same time, annual wage growth in the form of average earnings per employee (non-farm) slowed from more than six per cent in the September quarter 2025 to 4.2 per cent last quarter. And annual growth in nominal non-farm unit labour costs slowed from 5.4 per cent to 3.1 per cent. Indeed, in real terms unit labour costs fell over the year, dropping by 0.1 per cent.

Other Australian data points to note

The Cotality National Home Value Index rose 0.8 per cent over the month in February 2026 to be up 9.9 per cent over the year. Cotality highlighted a divergence across capital cities, with values in Sydney and Melbourne flatlining in the aftermath of last month’s RBA rate hike, even as those in Perth, Brisbane, Adelaide, and Hobart all rose by more than one per cent over the month, reflecting very low levels of listings. Meanwhile, the national Rental Value Index recorded 0.7 per cent monthly growth in February and was 5.5 per cent higher over the year. The latter marks the strongest annual gain since October 2024.

The ABS said the number of total dwelling units approved in January 2026 was 14,564. That was down 7.2 per cent over the month (seasonally adjusted) and 15.7 per cent lower over the year. The fall was driven by a 24.5 per cent monthly drop in approvals for private dwellings excluding houses, which followed a 30.7 per cent decline in December last year. In contrast, approvals for private sector houses were up 1.1 per cent over the month and 7.1 per cent higher than in January 2025. As a quick reminder, the government has set a target of building 1.2 million homes over the five years from July 2024, as part of the National Housing Accord. That implies building around 240,000 new dwellings a year, or roughly 20,000 dwellings a month.

The ANZ-Indeed Index of Australian Job Ads rose 3.2 per cent month-on-month and 2.3 per cent year-on-year in February 2026. February’s increase was the first back-to-back monthly increase since October 2024 and follows an upwardly revised 5.2 per cent monthly jump in January, indicating that hiring has started the year strongly.

Australia ran a current account deficit of $21.1 billion in the December quarter of last year (seasonally adjusted). The ABS said the deficit was $2.8 billion larger than in the September quarter 2025, largely on the back of a $2.5 billion increase in the primary income deficit as Australian firms paid larger dividends to overseas investors. There was also a $0.9 billion fall in the income Australians received from their overseas investments. In contrast, the trade surplus on goods and services was little changed at $1.3 billion, down only slightly from the September quarter’s $1.4 billion result. The Bureau highlighted record highs for imports and exports of gold, as prices rose to new highs. Also notable was a 16.6 per cent jump in imports of telecommunications equipment following record imports of smartphones and a 9.1 per cent rise in imports of parts for transport equipment powered by higher demand for lithium batteries in response to the federal government's home battery rebate scheme.

The ABS said Australia’s merchandise trade balance recorded a surplus of $2.6 billion (seasonally adjusted) in January this year. That was down $0.7 billion from the December 2025 result, as exports dipped by $0.4 billion and imports rose by $0.3 billion.

According to the latest edition of the ABS Business Indicators Australia, company gross operating profits rose 5.8 per cent over the quarter (seasonally adjusted) and 3.8 per cent over the year in the final quarter of last year. Wages and salaries were up 0.9 per cent quarter-on-quarter and 5.6 per cent year-on-year.

The ABS Monthly Household Spending Indicator rose by just 0.3 per cent over the month (current prices, seasonally adjusted) in January 2026 to be 4.6 per cent higher over the year. The result followed a 0.5 per cent monthly decline in December 2025. The market consensus forecast had expected a slightly stronger outcome at 0.5 per cent. The Bureau said spending on services drove the increase, lifted by expenditure on digital streaming services, travel agency and tour services and dental services.

The December quarter 2025 release of Government Finance Statistics reported that the general government net operating balance was in deficit by $0.4 billion – an improvement of $33.4 billion from the September quarter. The ABS said general government expenses fell 1.5 per cent in quarterly terms, while total revenue was up 11.9 per cent as tax revenue rose by 15.6 per cent.

Further reading and listening

- From the RBA, Governor Michele Bullock’s recent speech on Listening to Australians, interpreting the data and setting monetary policy. Among other topics, Bullock’s speech touched on the role of uncertainty, noting that recent events in the Middle East were ‘a timely reminder that in this world of geopolitical uncertainty, things can change quickly. It’s too early to say what the economic impact will be, events are moving rapidly and there are different ways this can play out…A supply shock could, for example, add to inflation pressures. And the potential implications for inflation expectations are something we are very alert to. But at the same time, a prolonged impact on energy markets could have adverse effects on global economic activity and result in downward pressure on inflation…So as much as I know the public would like more certainty about the direction of interest rates, it would be wrong for us to pretend to have greater certainty than we do’.

- Also from the RBA, Assistant Governor (Economic) Sarah Hunter’s speech on Recent refinements to the RBA’s dual mandate and navigating back to target. Hunter explains that prior to the 2022/23 Review into the RBA, ‘the legislation governing the RBA spelled out three distinct objectives for monetary policy – price stability, full employment and the economic welfare and prosperity of the Australian people.’ Post-review, this was amended such that the ‘legislation now explains that the RBA’s overarching goal is to promote the economic prosperity and welfare of the Australian people, both now and into the future. And for the Board, this means setting policy in a way that best achieves both price stability and full employment.’ Hunter’s interpretation of what this means in practice is that ‘recent changes have made the dual mandate more explicit and have fed into the enhancements in communicating the Board’s view of the economy and its strategy. But the fundamental components of the mandate remain the same and the continuity of the monetary policy strategy enacted by the Board before and after the legislative change suggest the clarification of the mandate is unlikely to mark a fundamental shift in how monetary policy is formulated in Australia.’ Another interesting part of the speech was its discussion of a counterfactual modelling exercise that examined the possible consequences of the RBA having gone harder and faster on inflation, in the form of a tightening path that followed the average peer central bank. The results suggest that the outcome would have been a lower inflation peak and a faster rate of disinflation, at the cost of a higher unemployment rate.

- The Productivity Commission’s submission to the Select Committee on Productivity in Australia canvasses selected policy options for a more prosperous future.

- Paul Krugman compares the current vulnerability of the world economy to an Iranian oil shock to the state of play during the second 1970’s oil shock and the Iranian revolution.

- The WSJ charts how the early days of the Middle East conflict reshaped market bets (oil prices up a bit, European natural gas prices up a lot, a rally in the shares of defence companies, and shifts in gold and government bond prices) and triggered some unusual trading patterns as the market rewarded ‘oil winners’ from the United States to Norway and punished ‘oil losers’ (much of Europe and Japan).

- While most eyes were on events in the Gulf, China said that it was cutting its growth target. The Economist magazine reckons it is now too low.

- Some thoughts on The 2026 Global Intelligence Crisis.

- Related, Greg Ip in the WSJ says don’t bet on tech causing a job apocalypse.

- Researchers at the NY Fed reckon global r* (the common trend in real interest rates across countries) may have risen by about one percentage point since the pandemic. About one-third of that rise could be due to a decline in the convenience yield for government bonds (this is the idea that for one or more reasons, possibly including the surge in government debt across advanced economies, there has been a fall in the appeal of government bonds in terms of safety and liquidity).

- Visualising the global geopolitical axis.

- Debt is the theme of the March 2026 edition of the IMF’s Finance & Development magazine, with pieces on high debt, hard choices, risks of debt distress for advanced economies, and the Debt-inequality cycle.

- Related, the OECD Global Debt Report 2026.

- From the same source, a new OECD survey of the Mexican economy.

- On betting against DOGE (WSJ).

- The Trumponomics podcast counts down to a global energy shock.

- The Past, Present, Future podcast has been talking to Luke Kemp about Societal Collapse. After covering origins and ancient empires in the first episode, subsequent episodes moved the discussion on to the modern age and then the present day. An upcoming episode will tackle the future.

- Somewhat related, the Prospect podcast in conversation with David Aaronovitch on the return of the Gilded Age.

Latest news

Already a member?

Login to view this content