Overview

- Next week’s budget will take place against a backdrop of elevated economic and geopolitical uncertainty due to the continuing conflict in the Middle East. The energy price shock triggered by the war creates both short- and longer-term spending pressures for the fiscal position, although higher energy prices will also provide offsetting revenue gains.

- The war is not the only challenge that Budget 2026 is expected to tackle. Even before the disruption to the Strait of Hormuz, there was a lengthy fiscal to-do list that included budget repair, tax reform, a pressing growth and productivity agenda, and growing calls to tackle housing affordability and intergenerational equity. All to be managed within the constraints imposed by above-target inflation.

- Australia’s central bank responded to the latter with a third consecutive 25bp rate increase this week, taking the cash rate target to 4.35%. That restrictive setting should buy the Monetary Policy Board some time to assess the economic fallout from the war.

- The new RBA forecasts in the May 2026 Statement on Monetary Policy (SMP) highlight the significant uncertainties around the economic outlook.

As next week’s budget draws closer the fog of war persists, complicating life for policymakers. Conflicting signals are still emerging from Washington and Tehran regarding the likelihood of an agreement. The United States has declared that Operation Epic Fury has concluded while Project Freedom (the plan to guide vessels through the Strait of Hormuz) has been suspended. The oil price continues to fluctuate, with Brent around US$100/b at the time of writing.

Closer to home, Australia remains at Level Two (‘Keeping Australia moving’) of the government’s four-level National Fuel Security Plan while Canberra retains its focus on shoring up domestic supply. According to the latest official update on Australian fuel stocks, stocks of petrol (43 days), jet fuel (28 days) and diesel (33 days) are currently little changed from their pre-war (December quarter 2025) levels of 38 days, 29 days, and 32 days, respectively.

The government has announced a new $10 billion Australian Fuel Security and Resilience package in response to the war. The promised funding is to: establish a Fuel and Fertiliser Security Facility to increase the supply and storage; establish a Government-owned Australian Fuel Security Reserve of around a billion litres to increase long-term diesel and aviation fuel supply; support an increase to the Minimum Stockholding Obligation to deliver an additional 10 days of fuel holdings; and support feasibility studies into new or expanded refining capabilities. More details will be announced in Budget 2026.

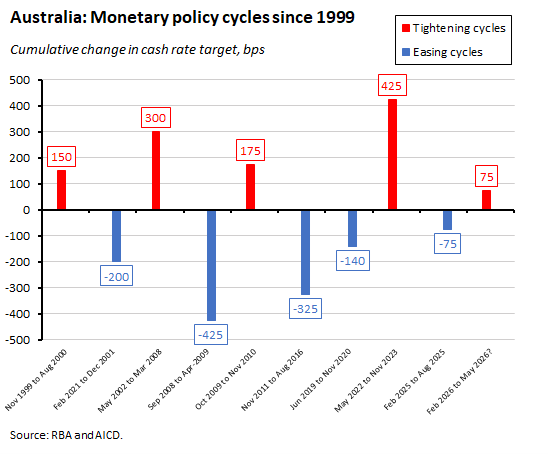

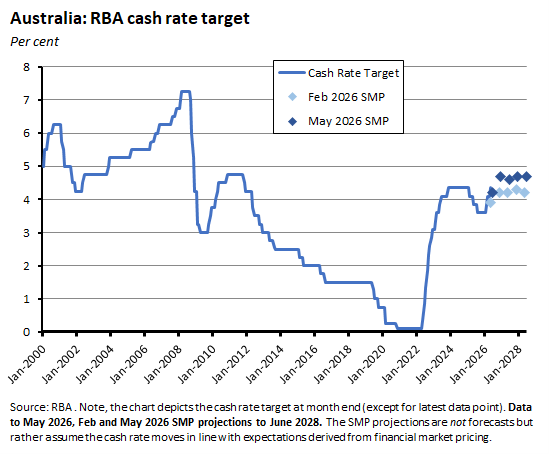

This week the RBA’s Monetary Policy Board (MPB) delivered a third consecutive 25bp rate increase, taking the cash rate target up to 4.35%. The rate hike was widely expected although the MPB vote in favour (8-1) was more decisive than we had anticipated last week. A look back at the history of RBA rate moves tells us that the central bank pushed the policy rate up to 4.35% in November 2023 in a decision marking the 13th and final rate hike in a 425bp policy normalisation process unwinding the pandemic-era’s ultra-low 0.1% cash rate. Policy was then unchanged until February last year, when the central bank announced the first of three 25bp rate cuts, with the final one arriving in August last year. The MPB has now unwound all that policy easing returning the cash rate to its November 2023 setting.

Next week is Budget week, which as usual means there will be no economic update. Instead, there will be the AICD’s regular budget night overview which will offer our initial views on Budget 2026. And then, after a day to digest a bit more of the detail, there will be a post-Budget economics webinar on 14 May. As usual, it will be free for AICD members. To register, see: Budget 2026 and the New Economic (dis)Order

Budget Preview: Competing crises

Last December, the 2025-26 Mid-Year Economic and Fiscal Outlook predicted that Australia would run a deficit of $36.8 billion (1.3% of GDP) on the underlying cash balance this fiscal year, to be followed by a $34.3 billion (1.1% of GDP) deficit in 2026-27. Add in Canberra’s various off-budget spending measures and this year’s deficit on the headline cash balance was estimated at $58.6 billion (2% of GDP) followed by a shortfall of $62.7 billion (2.1% of GDP) in 2026-27.

The government is likely to do better than the MYEFO numbers for this year. According to the latest General Government Sector Monthly Financial Statement (for March 2026), the year-to-date deficit on the underlying cash balance was $30.4 billion (lower than the MYEFO profile for $47.4 billion) while the deficit on the headline cash balance was $40.2 billion (vs a MYEFO profile of $60 billion).

When the Treasurer delivers Budget 2026 next week, he will be expected to address a range of crises of different size and urgency. Back in 2024, I wrote the Treasurer had to engage in a kind of macro-political juggling act, as he tried to keep multiple balls in the air. Two years on, and the juggling act continues as the same Treasurer faces a mix of familiar challenges and some difficult new ones. Consider:

- The new and obvious crisis is the war in the Middle East, the disruption to energy supplies and the resulting pressures on inflation, the cost-of-living and activity. Canberra is already paying an immediate fiscal cost for its price relief measures (primarily the halving of the fuel excise for three months from 1 April this year). There are political and social pressures to do more on this front, with pre-budget discussion of a tax offset for workers. The increased focus on building domestic economic resilience also comes with a price tag attached – see this week’s announced $10 billion funding for the Fuel Security and Resilience Package. Still, there should also be some good news here for the budget bottom line next year, as higher commodity prices and a larger nominal economy work to boost the tax take.

- The Iran war is just one symptom of a broader security crisis arising from the rapid decay of the international security order. On 16 April this year, the government released the 2026 National Defence Strategy (NDS) and the accompanying 2026 Integrated Investment Program (IIP). This too carries a fiscal cost. For example, the IIP envisions $425 billion in defence spending through to 2035-36, including promises in the 2026 NDS of an additional $14 billion over the next four years and $53 billion over the next decade.

- Australia’s inflation and growth challenges preceded the war but will now be exacerbated by it. As the RBA reminded us this week, Australia has an inflation problem that is in large part derived from a supply-side/growth problem: domestic capacity constraints mean that we struggle to maintain real GDP growth above 2% without driving inflation above target. In the near term, the RBA’s fight against inflation should serve as a constraint on government spending, since each new dollar of government demand injected into the economy is potentially a dollar of private demand that Martin Place will feel compelled to remove via higher interest rates. In the medium term, budget settings from tax to regulatory policy exert an important influence on the economy’s supply side, and business will be watching closely to see if the Treasurer lives up to past promises to materially shift the regulatory environment in a pro-productivity direction. Meanwhile, the Iran war has just worsened Australia’s growth-inflation trade-off. Even on the RBA’s relatively optimistic baseline forecast (discussed in detail below), the near-term growth outlook is looking distinctly anaemic.

- The housing affordability crisis and the associated challenges around intergenerational equity. While there is broad consensus that sustainably fixing the former ultimately requires a difficult-to-deliver increase in the housing stock, there have also been long-standing calls to tackle the demand side via changes to capital gains tax and negative gearing settings. Adjustments to both, along with changes to the taxation of discretionary trusts, are all tipped to be at the heart of Budget 2026, and of the government’s messaging on intergenerational issues.

- Finally, budget repair and an overhaul of the tax system are long-running fiscal ambitions. While Australia’s debt and deficit position looks in decent shape relative to many of our peers (as discussed here), we still face a medium-term challenge in reconciling desired spending with expected revenue. Pre-war sources of spending pressure already included the Child Care Subsidy, Medical Benefits, Hospitals, Defence, the NDIS and Interest Payments, for example, all of which were expected to grow faster than nominal GDP over the next decade as of the December 2025 MYEFO. As Budget 2026 approaches, the government has promised a range of measures aimed at limiting spending, including cuts to the public service workforce. The government has again pledged to scale back the growth in spending on the NDIS after having previously aimed at (but struggled to meet) a growth target of 8%. The new ambition is to slash annual growth to an average of around 2% over forward estimates. If met, this would imply a scheme costing around $55 billion by 2030 instead of more than $70 billion. Doing a better job matching spending and revenue is only part of the task, however, given long-standing concerns over the way that budget revenue is collected. The adverse implications for sustainability and incentives arising from our over-reliance on taxing private and general company income is a prominent example here.

Measures designed to help on one front risk creating new challenges on another, with new spending measures in support of national resilience pushing against budget repair, for example. Likewise, depending on the detail, new tax settings could create growth headwinds in terms of changed incentives or increased complexity.

The RBA takes the cash rate target back to 4.35%

Following the MPB meeting on 5 May 2026, the Board voted 8-1 to increase the cash rate target by 25bp to 4.35% (with the sole dissenter voting to leave the policy rate unchanged at 4.1%). According to the accompanying statement from the MPB:

‘Higher fuel prices are adding to inflation and there are indications that this is likely to have second-round effects on prices for goods and services more broadly. This inflation impulse is in addition to the high inflation recorded around the start of 2026, reflecting capacity pressures in the economy.

In light of these considerations, the Board assessed that inflation is likely to remain above target for some time and that the risks remain tilted to the upside, including to inflation expectations. It was therefore judged appropriate to increase the cash rate target.’

The decision to increase the policy rate this week was widely anticipated after last week’s inflation result. But the strength of the vote in favour was more surprising after the March MPB had seen a 5-4 split on an increase, with the minority position back then focused on war-related uncertainty. That uncertainty has hardly dissipated: the likely duration of the conflict remains unknown and likewise, the ultimate impact on activity and inflation is still unclear.

This week’s increase means the RBA has now delivered a cumulative 75bp of tightening via three successive rate hikes across the first three meetings of this year. The market projections that underpin the forecasts in the May 2026 Statement on Monetary Policy (SMP) see the cash rate rising a little further from here, to 4.7% by the end of this year, before remaining around this level until at least June 2028. This is a higher trajectory than assumed in the February 2026 SMP, which had the cash rate peaking at 4.3% in the December quarter 2027.

The RBA’s communications nevertheless sounded slightly less hawkish than they have done for a while. The new view seems to be that by unwinding all the previous policy easing and thereby returning the policy stance to a more restrictive position, the MPB has bought itself some time to assess the incoming data and judge the impact of the Iran war. Granted, the Board statement merely noted that:

‘Having raised the cash rate three times, monetary policy is well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment.’

But in her press conference following the meeting, Governor Bullock told her audience that:

‘The Board now judges the level of the cash rate to be a bit restrictive, which will help to address the risk that inflation will be higher and more persistent once the current shock passes through the economy. This gives the Board space to see how the conflict plays out and the response of Australian households and businesses to the shock.’ [emphasis added]

The next MPB meeting is scheduled for 15-16 June, followed by one on 10-11 August, with meetings in September, November and December to round out the year.

The RBA’s take on Iran war impacts

One important theme of both Governor Bullock’s press briefing and the new SMP was that most of the RBA’s policy response to date has been driven by concerns about the outlook for inflation and the economy’s capacity constraints that pre-dated the Iran war. Subsequently, that war has led to sharp increases in commodity prices, led by energy. As seen in the March inflation numbers, those higher fuel prices have already pushed up the headline inflation rate, with the RBA also detecting ‘indications that [they] are likely to have second-round effects on prices for goods and services more broadly.’ At the same time, consumer sentiment and business confidence are both down sharply, although here the RBA notes that current indicators of consumer spending have yet to suggest any material slowdown in household consumption.

In a special section of the May SMP, the RBA offers its own in-depth assessment of the impact of the war on the Australian economy. The focus is on how higher energy prices will affect output and inflation, which the RBA reckons will be the main channel for any economic consequences. Although it does note that in addition there will be important effects from other price increases (for fertiliser, rural commodities, and aluminium) and from higher global uncertainty. At least four key points are worth highlighting:

- While Australia is a net exporter of energy overall (mainly thermal coal and LNG) we are a net importer of oil, and particularly of refined products such as diesel, petrol, and jet fuel. And while our overall oil intensity of production has fallen over time, an important exception to this trend is diesel, where Australia’s use of diesel per unit of GDP has increased since the 2000s due to strong demand from mining and agriculture, a greater reliance on diesel-powered road freight, and the increased popularity of diesel passenger vehicles. As a result, our per capita diesel consumption is now among the highest in the world.

- Higher fuel prices will have a direct impact on consumer prices. As a rule of thumb, the direct effect of a 10% increase in fuel prices is an increase in headline CPI inflation of a bit more than 0.3 percentage points over one to two quarters, given that fuel comprises about 3.3% of the CPI basket.

- Higher fuel prices will also have an indirect impact on consumer prices though higher inputs costs, which could include imports, domestic production costs, and transportation costs. The RBA estimates that the indirect domestic cost effects of a 10% domestic fuel price increase would see the price level 0.2-0.25% higher over one to two years, assuming the fuel price increase is persistent enough to be passed on in full.

- Fuel price increases could also have second-round effects via higher inflation expectations and wages growth, although in general the evidence suggests that while oil supply shocks have tended to push up nominal wage growth in Australia, they do so by less than the increase in inflation, such that real wages tend to decline.

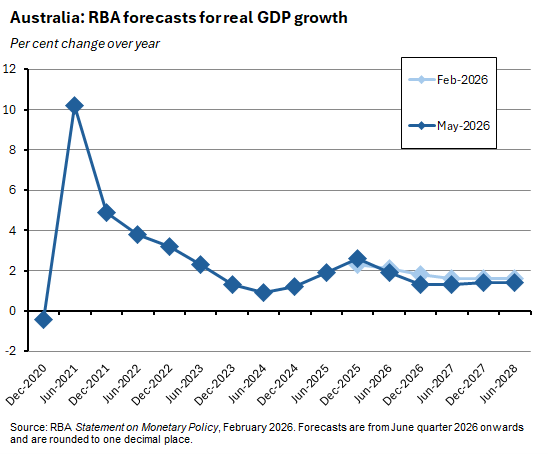

The RBA’s new baseline economic outlook

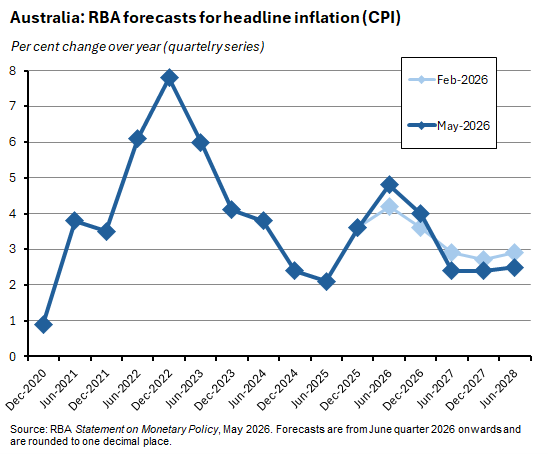

The SMP’s new baseline forecasts for the Australian economy assume that a near-term resolution to the conflict in the Middle East will see oil prices gradually decline over coming quarters. As noted above, they also assume the cash rate increases to 4.7% by the end of this year. Conflict-driven disruptions to global energy supplies mean higher fuel and raw materials costs push up headline inflation relative to the February 2026 projections. Hence headline inflation is now expected to be higher through this year, although it peaks at ‘just’ 4.8% in the June quarter, up from 4.6% in March 2026. After that, inflation is then expected to be lower next year and into 2028, returning to around the mid-point of the target band by as early as the June quarter 2027.

Underlying inflation, as measured by the quarterly trimmed mean, is also forecast to peak in the June quarter of this year at 3.8% (up from 3.5% now) but to then remain above 3% until the middle of next year, before gradually falling to 2.5% by the June quarter 2028.

These higher prices and higher interest rates help deliver a lower trajectory for real economic growth. Previously forecast to run at 2.1% this year, real GDP is now projected to grow at a lacklustre 1.9%. Next year will be worse, with growth expected to be just 1.3%.

Slower expected growth also comes with a slightly softer outlook for the labour market. While Australia’s unemployment rate is still expected to end this year at 4.3%, unchanged from February’s forecast, the RBA then sees it rising to 4.7% by June 2028, up slightly from the previous projection of 4.6%.

Key judgements and risks, plus downside scenarios

That baseline scenario rests on three key judgements.

- There is a near-term de-escalation in the war leading to a normalisation of trade activity through the Strait. The SMP notes that this assumption is in line with current oil market pricing.

- The spike in fuel prices has a relatively contained and short-lived impact on overall economic growth and the labour market. This judgement rests heavily on the previous judgement such that the price increase proves short-lived. Any hit to activity is also judged to be cushioned by the lower oil-intensity of GDP as well as by the boost to national income provided by higher export revenue from LNG.

- The rise in fuel prices is passed through to underlying inflation quite quickly. The call here is that the pass-through of input cost increases will be accelerated by the presence of capacity constraints, a relatively tight labour market, and already-elevated short-term inflation expectations.

Clearly, some of these judgements are subject to substantial risks and the RBA acknowledges that uncertainty about the duration and severity of the Iran war and its economic fallout mean the outlook is even more uncertain than usual. In particular, the SMP notes that a plausible risk is that the conflict is more prolonged and results in more significant and longer-lasting damage to energy production. In recognition of this, the SMP also presents two adverse scenarios in an echo of the approach taken by the IMF in its April 2026 World Economic Outlook (we discussed the Fund’s reference, adverse and severe scenarios here). In both the RBA’s adverse scenarios, the closure of the Strait of Hormuz is assumed to extend beyond the baseline case, with shipping flows only resuming from the first quarter of next year and normalisation taking even longer. Crucially, both scenarios assume that Australia continues to receive enough imported fuel to meet domestic demand. (Note also that for comparison purposes the RBA assumes the same trajectory for the cash rate in all three scenarios.)

In the first adverse scenario, this prolonged disruption to energy markets sees the Brent oil price peak at around US$145/b in the second quarter of this year and only gradually decline to around US$95/b by the end of the forecast period. Headline inflation now reaches 5.2% in the June quarter 2026 while underlying inflation is about 0.4 percentage points higher than in the baseline forecast by early next year. Output also takes a hit, with the level of domestic GDP around 0.5% lower by mid-2028 compared to baseline. Unemployment is higher.

In the second adverse scenario, the same extended energy supply disruption is now assumed to be associated with a larger hit to both global and Australian economic activity, driven by a large increase in global risk premia. This time, the level of Australian GDP is 0.2% lower than in the first adverse scenario and more than 0.8% below the baseline, while the unemployment rate climbs to 5.1%. As a result, the subsequent disinflation process is quicker, with inflation back in the bottom half of the target band by mid-2028.

Other Australian data points to note

The ABS has published March quarter 2026 estimates for its Selected Living Cost Indexes (LCIs). Living costs for all five household types tracked by the Bureau recorded rises over the March quarter, ranging from 1.1% to 2.5%, while annual increases ranged from 2.6% to 5.2%. At the lower end of the range, the Employee LCI rose 1.4% over the quarter and 2.6% over the year while at the higher end, the Age Pensioner LCI was up 2.5% quarter-on-quarter and 5.2% year-on-year. Housing (due to higher electricity costs following the exhaustion of the Commonwealth Energy Bill Relief Fund rebates), health and transport (due to higher fuel prices) were the main drivers of higher living costs

ANZ-Indeed Australian Job Ads fell 0.8% month-on-month (seasonally adjusted) in April 2026 to be down 1.4% over the year. Last month’s decline follows a downwardly revised 3.2% monthly drop in March this year, but ANZ noted that the index is still 5.2% higher than its December 2025 level.

The ANZ-Roy Morgan Consumer Confidence index fell 0.6 points to 67.2 for the week ending 3 May 2026. That was the seventh lowest reading in the (more than 50-year) history of the series. Weekly inflation expectations rose to 6.7% from 6.6% the previous week.

Last Friday, Cotality said that its national home value index rose 0.3% over the month and 9.8% over the year in April 2026. That marked the slowest monthly pace of growth since January 2025. The combined capitals index rose 0.2% month-on-month and 9.1% year-on-year with monthly price declines in Sydney and Melbourne (both down 0.6%) set against continued albeit slower monthly growth in Adelaide (up 1.1%), Brisbane (up 1.2%) and Perth (up 2.1%). Sydney home values are now 1% below their November 2025 peak while Melbourne values are 2.3% below their March 2022 peak. Cotality also reported a softening in buyer demand, noting that estimates of capital city home sales over the past three months were 5.4% lower than a year ago and 7.4% below their previous five-year average. Likewise, auction clearance rates remain below 55%. Advertised stock levels have also risen above their five-year averages in Sydney and Melbourne. According to Cotality, housing demand is facing ‘a formidable and worsening set of headwinds’ with affordability at record lows, easing population growth, higher interest rates, and more recently the uncertainty brought by the Iran war. In contrast, there is no evidence of any loosening in the rental market for now, with vacancy rates steady at 1.6% across the country compared to the ten-year average of 2.5%. Rents rose 0.6% over the month and 5.7% over the year, the fastest rate of annual growth since October 2024.

The ABS said that total dwellings approved in March 2026 fell 10.5% over the month (seasonally adjusted) to 17,300 (although that was still nine per cent higher than the number of approvals in March 2025). Approvals for private sector houses edged up 0.9% over the month to stand 12% higher over the year, while approvals for dwellings excluding houses slumped 26% month-on-month while still being up 3.4% year-on-year. According to the Bureau, approvals for private houses are now at their highest level since November 2021.

According to the March 2026 Monthly Household Spending Indicator, household spending was up 1.6% over the month (current prices, seasonally adjusted) and 6.3% higher over the year. The ABS said that the rise in nominal monthly spending in March reflected a 5.1% jump in transport costs due to higher fuel prices driven by the war in the Middle East. Spending on public transport was also strong, suggesting some substitution effects at work. There was also a robust 1.7% rise in food spending, which the Bureau attributed to a combination of higher food prices and some precautionary stockpiling. In volume terms, spending was up 0.7% over the quarter and 2.8% over the year in the March quarter 2026, with the latter marking the strongest annual growth since the June quarter 2023. In this context, the ABS highlighted spending on non-discretionary items including health and food.

New ABS data on Australia’s international investment position as of 31 December 2025 reports a liability of $638.5 billion, with foreign investment in Australia at $5,116.3 billion and Australian investment abroad at $4,477.8 billion. By source country, the top three investors in Australia last year were the United States (27%), the United Kingdom (16%) and Belgium (9%) * while the top three destinations for Australian investors overseas were the United States (37%), the United Kingdom (14%) and New Zealand (5%). *Most investment from Belgium is portfolio investment liabilities in the form of debt securities and reflects Belgium’s status as the host for Euroclear, a major clearing house for euro-denominated bonds and other securities.

The ABS will reinstate its Survey of Business Conditions and Sentiments to ‘better understand the economic impacts of the supply chain disruptions resulting from the closure of the Strait of Hormuz.’

Further reading and listening

- The government has announced a domestic gas reservation scheme that will require gas exporters to supply some of their production - equivalent to 20% of exports – to the Australian market. The scheme will begin on 1 July 2027. The government said the scheme will respect export contracts agreed before the government’s announcement on 22 December last year.

- The latest monthly RBA chart pack.

- The latest Budget Monitor from Deloitte Access Economics.

- Grattan’s Aruna Sathanapally on colliding budget imperatives between responding to short-term shocks while also dealing with long run challenges.

- ABC Business on the tax trio underpinning next week’s budget – changes to capital gains tax, negative gearing, and the taxation of trusts.

- The AFR’s Phillip Coorey reckons Budget 2026 is coming for Generation X (ouch).

- The e61 Institute says the ‘quasi-market’ part of the NDIS is not working.

- From the ABS, a guide to understanding Australia’s productivity statistics.

- The FT reviews Australia’s drive to diversify its trade.

- Two pieces from Goldman Sachs, one tracking the scale of the AI build-out and one on the cracks in the private credit market.

- On the world’s most complex machine.

- The 2026 OECD Economic Survey of New Zealand.

- From the Peterson Institute, via Foreign Policy, are current petrostates a model for our AI future?

- The WSJ explains global economic resilience in the face of the Iran war.

- Are prediction markets good for anything?

- The Economist magazine warns that bad government statistics can cost billions of dollars.

- A new BIS Paper analyses the impact of stablecoins on the international monetary and financial system.

- The Federal Reserve Bank of New York explains the US K-Shaped economy and tracks its drivers.

- Harper’s magazine considers America’s gerontocratic crisis.

- Understanding the rising age of CEOs – a greater demand for accumulated experience in the face of rising uncertainty and economic complexity.

- The Odd Lots podcast explains how Taiwan became the world’s most perilous geopolitical chokepoint.

- The UnHerd podcast asks Odd Arne Westad about the risks of a new WW1.

- Sticking with call backs to history, Unhedged discusses historical analogies for the AI boom.

- Conversations with Tyler talks to Craig Newmark.

Latest news

Already a member?

Login to view this content