Superannuation funds are hoping mergers will help buffer them against the challenges intensified by COVID-19, writes Ben Hurley and Narelle Hooper.

Riding the lift at Aware Super’s sharp new Sydney CBD offices, chair Neil Cochrane enthusiastically counts off developments in the year everything stopped.

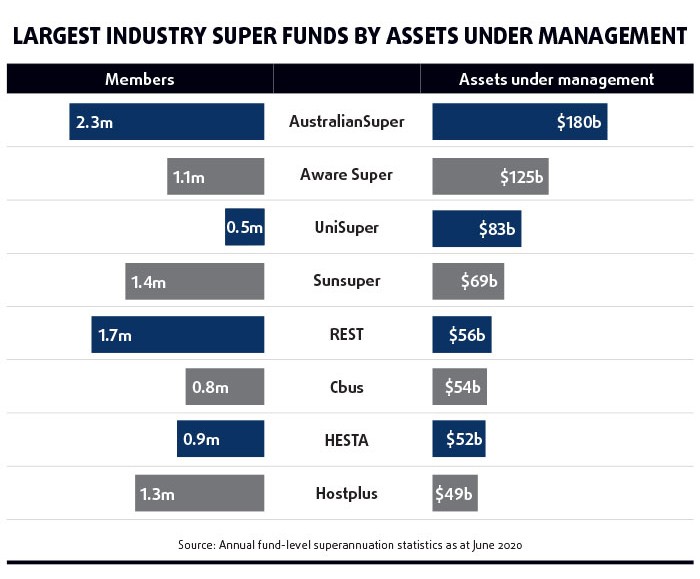

On 30 June, industry funds First State Super and VicSuper completed the biggest merger in Australian superannuation history to become the second-largest fund, with $125b of assets under management and 1.1 million members. The following week, CEO Deanne Stewart GAICD made headlines when she announced the fund’s climate change transition plan, including a time line for exiting investments in thermal coal, reducing emissions in its listed equities portfolio by 2023 and advocating for an economy-wide 45 per cent cut in greenhouse emissions by 2030. Then came plans for a rebrand as Aware Super and confirmation of a merger with WA Super in December, adding 50,000 members and another $4b in funds under management. And somewhere in the middle of the lockdown, the fund moved a third of its 1400 staff into new Green Star-rated, socially distanced offices. The fact that the organisation was able to pull it off in the midst of a once-in-a-century pandemic says much about its alignment and execution capacity.

But to go fast, first you need to go slow, as the saying goes. The rapid progress was the product of lengthy discussion and planning that saw the board and management of both funds test their alignment on values, culture and objectives. “Very early on in the merger discussion, we sat down and agreed how the board was going to look. We agreed on principles first,” says Cochrane (see page 54). The same went for the executive team. Ultimately, he says, it was the sense of purpose — for the organisation to become a force for good — and a focus on member interests that enabled the fund to execute amid extraordinary conditions without any major issues.

After the existential threat of COVID-19, there’s a new sense of urgency to the forces reshaping Australia’s superannuation industry. Aware Super’s advocacy on environmental, social and governance (ESG) issues might have caught the headlines, but plenty more has been happening under the radar.

In September, Queensland’s QSuper and Sunsuper announced they were continuing due diligence and, if combined, would surpass AustralianSuper as the country’s largest fund, with around $160b in assets under management and two million members.

In Tasmania, Tasplan, a $10b fund, is in the throes of merging with $13b fund MTAA Super. Unlike Aware, which made the call to push on with its original deadline despite COVID-19, to avoid prolonging the uncertainty that came with it. Tasplan and MTAA have extended their merger completion deadline to March 2021.

It’s Tasplan’s fourth merger since 2011 and chair Naomi Edwards FAICD, who is also a member of the AICD’s national board, says the pressure on funds to consolidate is only going to rise. “I think we’ll see a rapid acceleration of trends towards a merger.

I believe anything sub-$1b will struggle to survive unless it’s on a strong growth trajectory because of a new and unique value proposition.”

Regulatory burdens, falling revenue, complexity and rising costs were already driving the trend towards fewer, bigger funds when COVID-19 delivered a triple hit to the industry. Investment markets have become more volatile and this is expected to continue well beyond 2020. Massive job losses due to the shutdown have cut off super contributions from hundreds of thousands of Australians. And, as at November, the federal government’s Early Release Scheme has resulted in more than $34b being paid out of super accounts.

Edwards sees the Early Release Scheme, in particular, as a “seismic shift” in how super is perceived in Australia by both politicians and the public. While it may lead members to take greater ownership of their super and make more active decisions about which fund they elect — a positive outcome — it could also lead people to view it “as a slush fund to be accessed whenever it’s needed, which will defeat its purpose”.

The long tail

In its annual Industry Super Forces at Work report, strategy consultancy firm Right Lane estimates as many as 60 per cent of all funds could be in negative cash flows by the end of 2020 — which is a strong indicator historically that a fund is going to exit the industry — and suggests the coming years could see even more consolidation than is happening now.

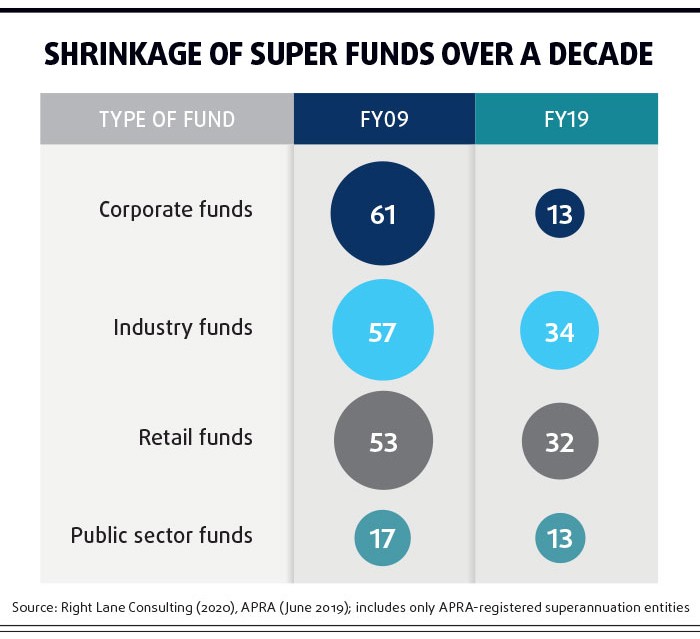

Half of Australian superannuation entities (including corporate, retail, industry and public sector funds) either merged or wound up between 2009 and 2019, says Right Lane associate principal Abhishek Chhikara. Even so, the industry has a long tail of underperforming funds. Analysis by Right Lane found that even before the pandemic, 19 of a total 92 registered super entities were receiving almost all of the net contributions into the system, amounting to $43.5b in the five years from 2015 to 2019. The middle 54 fought it out for a total gain of $6b, while the bottom 19 collectively shrank by $7b.

At the same time, expenses are rising as funds invest in uplifting their technological capabilities to meet member demands and also deal with a raft of regulatory changes directed at the sector in recent years. “We see these jaws of revenue and costs opening up and that really puts funds in a quandary,” says Chhikara. “Is their value proposition defensible enough to raise fees? Can they lower costs without compromising on quality as expenses have risen steadily? Or do they have reserves they can tap into and is this delaying the inevitable? It’s quite challenging and COVID-19 is making it worse.”

In recent years, the banking Royal Commission; legislation such as Protecting Your Super (PYS) and Putting Members’ Interests First (PMIF); and the introduction by the Australian Prudential Regulation Authority (APRA) of a Product Heatmap for the MySuper suite of simple, default super products for Australian workers have increased the pressure on funds to eliminate duplicate fees and exit the industry or merge if they are underperforming.

In the 2020–21 Budget announced in October, the Morrison government further turned up the heat with its Your Future, Your Super package.

Now, superannuation accounts will follow workers rather than being automatically created each time they switch jobs — ending fee gouging through the creation of multiple accounts. Funds will also be required to meet an annual performance test, with poor performers required to notify their members of this fact. An online comparison tool aims to show how funds really stack up on fees and returns.

Whose interests?

In this context, there’s an increasing focus on the governance of funds. Speaking to the Australian Institute of Superannuation Trustees on 12 October, APRA deputy chair Helen Rowell MAICD warned that member interests needed to come before the personal interests of board directors. “Self-interest has no place in the boardroom, and this will continue to be a focus of APRA’s work to lift governance practices across the industry,” she said. “Mergers are not about maintaining jobs for current directors or deals such as ‘you take the chair and I’ll take the deputy’.”

During the banking Royal Commission, Catholic Super attracted criticism for dragging its heels on an ultimately failed merger with the Australian Catholic Superannuation and Retirement Fund over the issue of which fund would be dominant after the merger. “What does it matter a hill of beans which fund merges into which?” Commissioner Kenneth Hayne AC QC asked Catholic Super’s deputy chair, Peter Haysey.

Directors protecting their positions “is the elephant in the room” in merger discussions, but it shouldn’t be given any weight at all, says John Atkin FAICD, chair of Qantas Super and the AICD’s national board. “For many of the people who are directors of trustee companies, it might be the only board position they have, so it may be very important to them personally,” he says. “You should start any review process with the assumption that you won’t be the director at the end of it, otherwise your personal interest will distort the discussions.”

Building strength

Many funds are seeking to strengthen their position by seeking greater scale, meaning more funds are set to dive into large and complex mergers in the coming years. They will increasingly influence corporate decision-making, applying their long-term investment horizons to push boards and management towards a greater focus on issues such as social and environmental issues and responding to climate risk.

Edwards, who hopes this upheaval leads to fresh blood and greater diversity on boards, argues that all Australian boards — not just super-fund boards — are at risk of being too long in the tooth. “Diversity needs to be broader than just gender,” she says. “Boards need to have real technology strengths and, in many cases, that will require you to have a younger, fresher balance to your board.”

Analysis by Right Lane contends that funds with fewer than 500,000 members are generally not efficient. According to Chhikara, an ideal structure for the industry would be three to five generalist mega-funds and seven to 10 specialist funds with no fewer than 500,000 members.But a base belief in “bigger is better” is not the answer to everything, and boards will need to weigh up a number of factors before deciding that a merger is in the best interests of their members. “There is definitely a sub-scale point at which being small is bad,” says Edwards. “But there are diseconomies of being ultra-big. You can get locked out of good investment opportunities because they’re just too small for you.”

The benefits of scale also depend on how your size is achieved, she says. A clean, well-integrated merger under a single brand is the best way to realise economies of scale. The 2019 attempt at a three-way merger between Tasplan, Statewide Super and WA Super failed largely because merging three entities at once “just proved to be too complicated”, says Edwards.

“If your bigness is achieved just by mashing everyone together under different systems that you don’t integrate, under different advisory bodies, under different families of brands, then you might be big, but you don’t get the benefits,” she says.

It’s also critical that the board’s chair, CEO and directors all click, she adds, as goodwill between the parties is vital to effectively governing the fund — with the caveat, of course, that they’re all driven by the desire to achieve the best outcome for members and not themselves. “What you need to do is develop a robust business case that shows member benefits in terms of fee savings, lower investment costs, higher service levels and broader product range. If the business case shows those things, it’s very hard not to proceed with a merger.”

Size matters

Aware Super’s Stewart — who was CEO of MetLife Australia from 2014 to 2018 and has more than 25 years’ leadership experience in the super, wealth and insurance sectors — strongly believes that bigger funds bring greater benefits to members. Scale drives down administration, trustee and investment costs, resulting in lower fees for members — a boon before you even look at investment returns. It allows funds to invest in strong administrative systems behind the scenes and have dedicated teams for areas such as regulatory compliance so this doesn’t distract the rest of the team.

Scale also enables funds to build solid internal capabilities and invest directly into significant assets, she says. In 2018, First State Super secured a 40-year concession to run Victoria’s land title registry business for $2.86b and, in 2017, was part of a consortium that purchased the NSW government’s land title registry service. It has invested directly in social housing and renewable energy projects around the world.

“Scale gives you direct access to many more types of investments,” says Stewart. “So instead of having to do that within a pooled fund structure, where you have layers of fees, you can strip those out and have better opportunities and lower fees that you can pass on to members.”

But there may still be room in the future super landscape for smaller players who claim to have an edge over large funds through agility, superior member engagement, tailored insurance products, and the ability to take advantage of niche investment opportunities that are too small to make a material difference to the portfolios of bigger players.

Some smaller funds will look at ways to leverage scale while keeping their distinct offering to members. In 2019, Catholic Super merged with Equip Super using an extended public offer model that allows funds to outsource trusteeship, administration, custody and investment operations while retaining responsibility for strategy, brand development and member and employer relations.

In July, Media Super and Cbus Super, a building and construction industry fund, announced they were doing due diligence for a merger in 2021 that would combine the funds’ investment and admin operations, but maintain individual branding.

BUSSQ, a public offer industry fund for workers in the building, construction and civil industries, has just over 80,000 members and assets under management of around $5b, with 52 staff. Despite its relatively small size, the fund has been one of the top five performers among Balanced Index options over the past year, and also over seven years, according to SuperRatings statistics.

“We see our size as an advantage here,” says BUSSQ board chair Paula Masters MAICD. “We can take opportunities that bigger funds aren’t able to; in particular, we’ve had success with agriculture and small caps. And our size gives us the agility to make quick decisions and act on them.”

The fund has a dedicated risk and governance team to deal with ongoing regulatory change, and there’s a tender process to outsource admin, which Masters expects will lead to a reduction in fees. Outsourcing provides the benefits of scale without being wedded into legacy systems, she explains.

Qantas Super, has around $8b in assets and 30,000 members. Atkin is also an independent director for Commonwealth Bank Group Super, which has more than $12b of assets and 75,000 members. Although among the largest superannuation funds that specialise in single corporate groups, it’s tiny compared to the likes of big industry funds. Atkin says efficiency comes through scale, but only up to a certain point.

Qantas Super met all its early release obligations while maintaining liquidity and, in 2020, signed off on accounts that will have provided members with more than $500m of benefits. Engagement and member satisfaction scores from surveys reached “all-time highs”, he reports.

“If you look at Qantas Super, there was probably no fund in Australia put under more pressure by COVID-19,” says Atkin. “I participated in a few forums where people talked about these concentrated cohort funds and how that might be a weakness of the fund. That’s not how it’s worked out at Qantas at all.”

Anatomy of a merger

How do you get large boards with representative directors to agree to a merger that will do many of them out of a job?

Chair Neil Cochrane has been through a few mergers in his time, but says Aware Super’s has been an entirely different experience. “I think it’s because we literally have a high goal: to be a force for good and to serve our members. First State Super and VicSuper both go back to the early days of compulsory superannuation and have long had a focus on responsible investment and innovation.

Former VicSuper chair Wayne Kayler-Thomson says the organisation learnt from the early stages of potential mergers. “Often you found that boards were focused on their own future and... the CEO looking after their own interests. While members’ interest was the rhetoric, it was often hiding other motivations,” he says.

Merger discussions started with informal meetings of the fund chairs, deputy chairs and CEOs discussing the particular values of the fund and how the board was going to look, with basic principles agreed very early on.

It was decided that the new board would reflect the membership and geographic balance (45 per cent Victoria, 55 per cent NSW); have equal representation of employers and employees; and reflect the membership sectors within the board — nurses, teachers and emergency services workers.

It was also agreed to initially increase the board from 12 members to 14, plus an independent chair. Two seats from NSW-based employers and unions were dropped to make way for four VicSuper directors, and eight board members are female.

Cochrane says it’s the largest of the five boards he’s chaired over his 40-year career, although it will shrink to 10 plus one in 2022. “That was essential, because it’s the structure of the board and who’s on the board that is the Achilles heel. Wayne and I said we were writing it in our own blood — and it’s in the constitution in the merger agreement — that we have to shrink down to 10,” he says.

“It was each of us looking [each other] in the eye and trusting each other,” says Kayler-Thomson, who stepped down at the end of his tenure after serving a decade on VicSuper’s board.

Former First State Super CEO Deanne Stewart retained her position, while former VicSuper CEO Michael Dundon joined the executive of the larger entity. A steering committee was set up with the two chairs, two CEOs and a director from each side. Operationally, Stewart set up a merger team, separating it from business as usual.

Cochrane says respect has been a fundamental element of the process. “The directors all saw that the merger was in the best interests of our members — that we are the custodians of other people’s savings — and it was in the best interests of the business. Ego didn’t play a role.

“I think it’s really important to work through problems together, [including] problems you may have had in the past, because it gives an insight into the way you approach things. If you can talk openly about challenges you have, it can only strengthen the merger.”

Regular checks of the merger’s operational aspects and progress are on the board’s agenda. Stewart says there were many complex matters to be dealt with during integration, successor fund transfer, asset migration and investments allocation. The biggest challenge was bringing together employees from two strong regional teams; however, careful management meant the technical project teams were able to work productively from home.

“You want to make sure people feel really proud to be part of the organisation coming together,” says Stewart. “That’s much harder to do — in terms of building trust, building collaboration, feeling connected, caring for people — through electronic means rather than person to person.”

Although the VicSuper brand is still in use, all staff were brought onto the same communications platform (Microsoft Teams), while regular video calls introduced new leaders, allowed teams to get to know each other as best they could and onboarded new employees. When it came to redundancies, says Cochrane, the organisation worked to give people a long period of notice — the same rule it’s applying in the merger with WA Super. “Make sure you are as generous as you can be,” he advises.

Cochrane says his experience of growing up with socially conscious parents in South Africa laid a strong foundation. His mother was a founding member of the Black Sash women’s resistance movement and his father was a doctor who worked in a black hospital. He came to Australia in 1989 to escape apartheid, returning in 1994 — when Nelson Mandela became president — as CEO of Southern Asset Management, which led socially responsible investment initiatives. He returned to Australia in 2001 to take up the role of CEO of REST Super.

Both Stewart and Cochrane have embraced the notion of Aware Super becoming “a force for good”, noting the rapid shift in investor concerns on environmental, social and governance (ESG) issues and climate risk. “The industry is waking up to the importance of ESG,” says Cochrane. “For years we’ve been talking about good governance in terms of it being beneficial for business. This is what corporate Australia and investors have really understood this year. Our members have jobs that are directly affected by the environment; they’re in emergency services, they’re firefighters, police, nurses, teachers. They see the impact on a daily basis. We’re grateful to be able to lead, knowing that we have the support of our membership.

“Today, someone is joining the fund who will be with us for the next 45 years as a contributing member and then 35 years in retirement. So we are looking for someone who may be with us for 80 years — that makes you think long-term.”

Latest news

Already a member?

Login to view this content