Overview

- A fragile ceasefire has provided some relief on oil prices, although ongoing risks around continued regional violence, energy supply and production, shipping disruption and chokepoint risk mean the near-term outlook remains highly uncertain.

- Regardless of the ceasefire, the war has already generated a range of aftershocks around energy and food security, debt sustainability, market structure, and geopolitical risk.

- Recent Australian data show consumer confidence remains weak while inflation expectations are still elevated. The market anticipates further rate increases from the RBA, even as the latest MPB minutes reinforce the challenges for monetary policy posed by war-driven uncertainty.

After last week’s break (and our Special on Chokepoint risk and supply chains) this week, we look at the ongoing global economic fallout from the conflict in the Middle East against the backdrop of this week’s fragile-seeming ceasefire, consider the latest war-driven readings on Australian consumer sentiment and inflation expectations, and catch up on the domestic economic data released during the Easter period, including the latest Monetary Policy Board (MPB) Minutes.

A fragile ceasefire

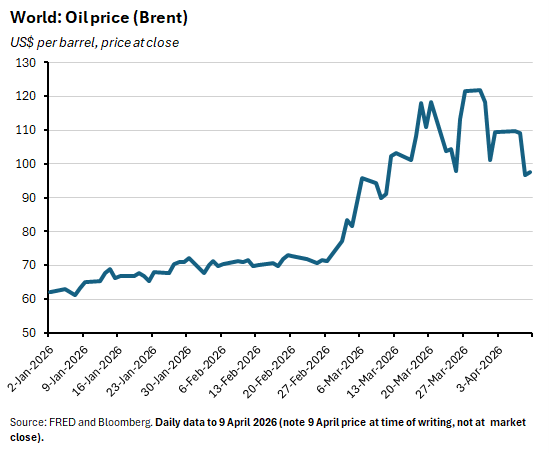

At the time of writing, a ceasefire – of sorts – was just about holding in the Middle East. News of this latest swing in the rapidly fluctuating narrative of the current war had initially sent the oil price back down below US$100/b, although uncertainties related to the ongoing violence in Lebanon and the degree of access Tehran would actually permit through the Strait of Hormuz meant that the supposed two-week long truce was already looking shaky. As a result, oil prices had started to edge higher. All of which left the economic outlook feeling…fragile.

Even if the current ceasefire does manage to hold for the next two weeks, that leaves significant uncertainty as to what comes next, including regarding control over the Strait of Hormuz. Meanwhile, other complicating factors include the large backlog to shipping and the (still ongoing) damage to energy infrastructure, both of which mean that the disruption caused by the conflict will continue long after the last drone has been launched.

Several aftershocks are already visible

The global economy is already feeling the aftershocks from the blow to international trade created by almost forty days of conflict. Exhibit one here is the global wave of energy rationing that has been triggered by the war, with emerging and middle income economies in Asia particularly exposed to date.

The interruption to energy and to fertiliser supplies also saw world food commodity prices rise in March this year for a second consecutive month. Granted, according to the FAO, the overall impact on food prices to date has been relatively modest, thanks in part to the cushion provided by ample supplies of global cereals. Still, a prolonged disruption would threaten crop yields while some African countries that rely on access to seaborne fertilisers from the Gulf are already suffering steep increases in basic food prices. South Asian economies also look exposed.

Then there is the fiscal fallout. Government policy responses have provided emergency consumer support in the form of cuts in fuel excise duty, the roll out of fuel and energy subsidies, and the provision of targeted income support. All of which represent an additional strain on already-stretched public sector balance sheets. More importantly, rising government borrowing costs due to bond market fears as to the likely inflationary consequences of another adverse global supply shock have also added to fiscal brittleness (although note that at times fears about the adverse implications for growth have pushed market sentiment in the opposite direction). As the OECD’s latest global debt report reminds us, central government borrowing in OECD countries reached US$17 trillion last year and pre-war was forecast to rise to US$18 trillion this year. Against that backdrop, investors in sovereign bonds were already worried by projected fiscal deficits, elevated government bond issuance, and a decline in demand for long-term bonds. The result had been rising long-term bond yields, prompting borrowers to shorten the maturity of their new issuance, thereby trading off lower interest rates for increased rollover risk. The war has further complicated this picture.

Looking to the longer term, energy analysts are busy trying to map out how energy markets and policies will adjust to recent events, with the likely possibilities ranging from the construction of new infrastructure to avoid the Strait, further boosts to policy support for electrification and renewables, and a new lease of life for coal.

The global security environment is likewise in transition. As noted last week, the conflict has served as a dramatic illustration of chokepoint risk in the global economy, a lesson that will be magnified should Tehran retain effective control of the Strait. At the same time, the war has further highlighted the deteriorating relationship between Washington and many of its key allies.

It has also raised questions as to the efficacy of the application of the ‘Trump Doctrine’ beyond Venezuela. For example, in an interesting contribution, Richard Fontaine, CEO of the Center for a New American Security (CNAS) recently suggested that the current US president’s use of force could be seen as the anti-Powell doctrine. The Powell Doctrine (developed during Gulf War 1 by US General Colin Powell) had asserted that war should only be employed as a last resort, in pursuit of a clear objective, with a clear exit strategy, with public support, and utilising overwhelming force. In contrast, according to Fontaine, the Trump Doctrine has involved surprise attacks, limited public buy-in, multiple and often vague objectives that allow for a swift exit, and a focus on the use of air power and special forces. Gulf War 3 and Iran have been proving a tough test for this approach.

An update on the Australian economic fallout

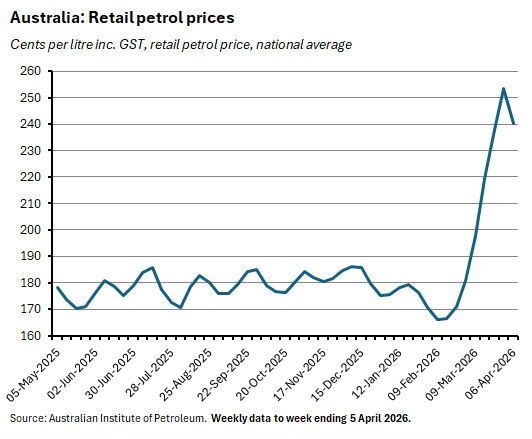

Prior to this week’s ceasefire, Australian households had been offered some local, limited relief from the price consequences of the war in the form of the government’s decisions to halve the Australian fuel excise for three months with effect from 1 April and to effectively remove Australia’s heavy vehicle road user charge over the same period (by cutting it to zero).

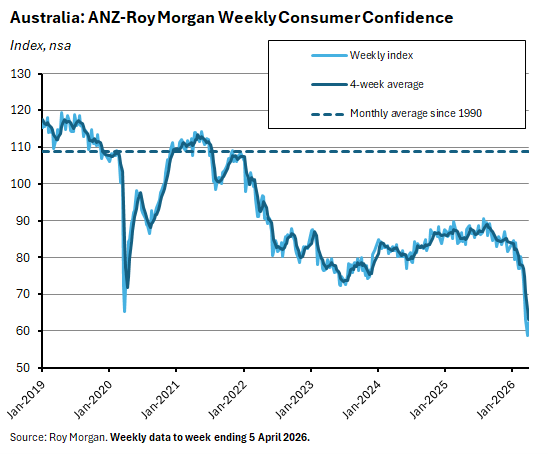

The consequent drop in petrol prices may have contributed to a modest improvement in reported household sentiment. The weekly ANZ-Roy Morgan Consumer Confidence measure said confidence edged up from its recent record low, rising 3.5 points to an index reading of 62.3 for the week-ending 5 April 2026. Although that still left confidence down 24.5 points over the year, languishing at its second-lowest reading in the history of the series.

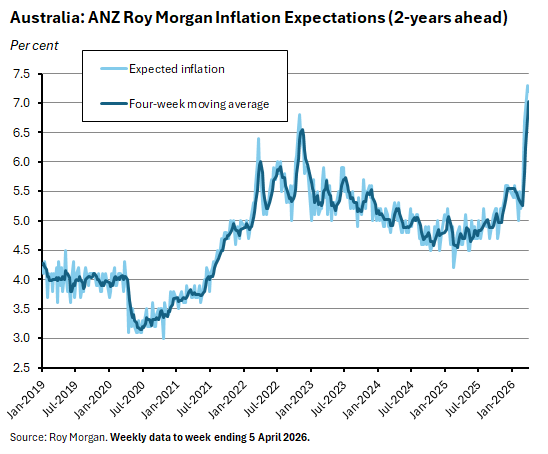

According to the same survey, weekly inflation expectations nudged lower by 0.1 percentage point last week. But at a still-elevated 7.2 per cent they will remain a source of discomfort for Martin Place.

Messages from last week’s MPB Minutes

Sticking with Martin Place, last week’s publication of the Minutes of the 16-17 March 2026 MPB meeting gave us more detail regarding that meeting’s split vote on monetary policy. Recall, it saw five MPB members vote in favour of increasing the cash rate target by 25bp to 4.1 per cent but four vote to leave it unchanged at 3.85 per cent. The Minutes tell us that both camps agreed that ‘further tightening in monetary policy would likely be required in the near term to bring inflation back to target within a reasonable timeframe.’ Their disagreement was over whether that tightening should begin last month, or whether it made sense to wait until the implications of the war in the Persian Gulf became clearer.

According to the Minutes, the case for hiking in March reflected a view that the risk that inflation would not return to target ‘within a reasonable time frame’ had now increased by enough to require an immediate policy response. Supporters of this case pointed to:

- The presence of widespread capacity pressures in the economy;

- The RBA’s pre-war view that there was more excess demand in the economy that it had previously thought;

- The scale of the likely inflationary impact of higher global oil prices and the risk this would add further to those persistent inflationary pressures, given a pre-existing context of excess demand;

- The buffer to war-related risks to activity provided by Australia’s status as a net energy exporter and the ‘generally healthy’ status of household balance sheets;

- A labour market where the RBA reckoned that the balance of risks had shifted away from a potential future loosening to a situation where current conditions were tighter than full employment; and

- A belief that prevailing financial conditions were insufficiently restrictive.

On the other side of the argument, the case for ‘waiting a little longer’ rested on the war-related increases in economic uncertainty, which included:

- Uncertainty about the outlook for domestic economic growth, based in part on weaker-than-expected consumption growth in the final quarter of 2025, plus the possibility that higher petrol prices would further squeeze consumer demand;

- Uncertainty about the tightness of the labour market, especially after the December quarter national accounts had reported a significant slowdown in the growth of average earnings and unit labour costs; and

- Uncertainty about how the conflict in the Middle East would evolve and the impact on demand relative to supply.

As we know, the case for tightening won out. But the uncertainty triggered by the war in the Gulf means that the future trajectory for policy remains highly uncertain. According to the Minutes, MPB members:

‘…agreed that it was not possible to predict the future path for the cash rate target with any confidence, given the high degree of uncertainty around the breadth and duration of the current conflict in the Middle East. A longer conflict could have a material bearing on both inflation and economic activity.’

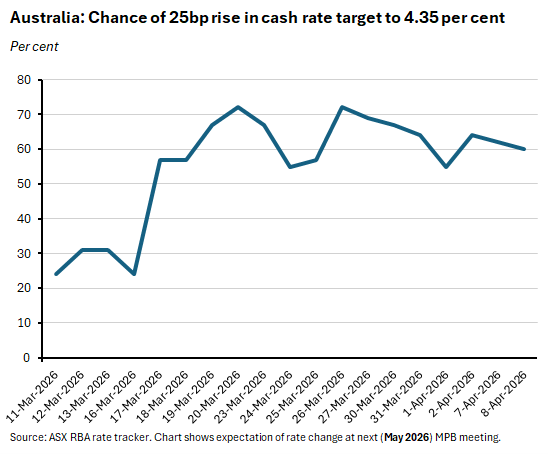

Meanwhile, market pricing continues to anticipate another rate increase at the next MPB meeting (scheduled for 4-5 May). A cut isn’t fully priced in, however. That close 5-4 vote in March, plus ongoing war-driven uncertainty, has been exerting a degree of caution, with the implied probability of a rate cut having fallen from more than 70 per cent in late March to around 60 per cent at the time of writing.

Other Australian data points to note

The ABS Monthly Household Spending Indicator rose 0.3 per cent over the month (seasonally adjusted) to be up 4.6 per cent over the year in February 2026. The Bureau said that discretionary spending was up 0.5 per cent in monthly terms and 4.6 per cent higher on an annual basis, driven by expenditure on concerts and musicals, as well as on air travel and accommodation services. Spending on essential items was flat over the month but 4.6 per cent higher than in February 2025.

ANZ-Indeed Job Ads fell 3.1 per cent over the month in March 2026, reversing much of their 3.2 per cent monthly growth in the previous month. Job Ads were 0.6 per cent lower than in the same month last year.

Total job vacancies stood at 337,900 in February this year, of which 299,000 were in the private sector and 39,000 in the public sector. Total vacancies were up 2.7 per cent from November 2025 (seasonally adjusted) and 3.7 per cent higher than in February 2025. According to the ABS, while private sector vacancies were 3.2 per cent higher over the quarter, public sector vacancies were 0.7 per cent lower. Both numbers were higher (3.6 per cent and 4.7 per cent, respectively) on an annual basis. The Bureau said that February’s 337,900 vacancies were the highest recorded since November 2024.

The Cotality National Home Value Index rose 0.7 per cent in March 2026 to be up 9.9 per cent over the year. The Combined Capitals index was up 0.6 per cent month-on-month and 9.3 per cent year-on-year, with a diverse monthly performance ranging from falls in Sydney (down 0.1 per cent) and Melbourne (down 0.2 per cent) to strong increases in Adelaide (up 1.2 per cent), Darwin (up 1.6 per cent), Brisbane (up 1.8 per cent) and Perth (up 2.5 per cent). Rental growth continued to run at a monthly rate of around 0.7 per cent in March, while the pace of annual growth accelerated to 5.7 per cent, the fastest rate since mid-2025.

The ABS said that total dwellings commenced rose eight per cent (seasonally adjusted) over the December quarter 2025 to be up 26.1 per cent over the year, at 53,567 dwellings. At 28,469, commencements for new private sector houses were down 0.9 per cent in quarterly terms but 7.6 per cent higher on an annual basis. Commencements for ‘new private sector other residential’ were up 23.4 per cent quarter-on-quarter and up 63.7 per cent year-on-year.

The ABS said that the total number of Building Approvals in February 2026 rose 29.7 per cent over the month (seasonally adjusted) and 14 per cent over the year, to reach 19,022. Approvals for private sector houses were up 0.2 per cent month-on-month and 6.1 per cent year-on-year at 9,847 while approvals for private sector dwellings excluding houses jumped 101.2 per cent over the month and 22.4 per cent over the year, to 8,922.

Australia’s balance on international trade in goods was a surplus of $5.7 billion in February 2026 (seasonally adjusted), up $3.4 billion from January’s $2.3 billion surplus. Swings in the export (up $2.1 billion) and import (down $1.3 billion) value of non-monetary gold were key drivers of the monthly result.

New ABS data on Australia’s regional population reported that the country’s capital cities grew by 324,700 people (a 1.8 per cent annual increase) in 2024-25 while regional Australia’s population rose by 94,700 (1.1 per cent). Capital city population growth was down by almost 100,000 people from 2023-24, largely reflecting a 109,400 drop in the contribution made by net overseas migration (which was still the main driver of capital city population growth).

Further reading and listening

- A new ASPI report on Markets as the new front line: Fusing Australia’s economic statecraft.

- The latest issue of Australian Foreign Affairs considers Trade wars and Australia.

- Richard Baldwin has a new CEPR e-book on World War Trade.

- Also from the CEPR, the macro impact of commodity supply shocks and an analysis of China spillovers.

- The FT’s Martin Wolf examines the resilience of global trade in the face of last year’s Trump tariff shocks.

- Also from the FT, a Big Read explains why investors may be wrong to bet on AI disruption of incumbents.

- The Economist magazine on the tug of war in government bond markets between inflation and recession.

- The OECD’s March 2026 Interim Economic Outlook acknowledges that the conflict in the Middle East will test the resilience of the global economy, as higher energy prices and elevated uncertainty boost costs and destroy demand. Based on a technical assumption that the disruption to global energy markets moderates over time, with energy and fertiliser prices projected to begin easing from mid-2026 onwards, the OECD sees global GDP growth running at 2.9 per cent this year and three per cent in 2027. While these numbers are little changed from the growth projections in the OECD’s December 2025 Economic Outlook (which had predicted 2.9 per cent growth for this year and 3.1 per cent for next year), the OECD also notes that in the absence of the war in the Middle East, early readings from the first two months of 2026 would likely have warranted an upgrade to expected growth this year of around 0.3 percentage points. Instead, this potential upgrade has now been fully erased. On the inflation front, the new forecasts expect headline inflation in the G20 to be four per cent this year and 2.7 per cent in 2027. The December projections had anticipated a more subdued outcome, with inflation projected at 2.8 per cent in 2026 and 2.5 per cent in 2027.

- The IMF on how war in the Middle East is affecting Energy, Trade and Finance.

- Also from the IMF, two new analytical chapters from the upcoming World Economic Outlook (WEO), one looking at the macro consequences and trade-offs involved in defence spending, the other on the macro consequences of conflicts and recovery (see this blog post for a summary of both essays). Plus the latest IMF Article IV report on the United States, and lessons from a Scenario Planning Exercise on the Global Economic and Financial Implications of AI.

- From the WSJ, to find Iran’s wealth, look to London property.

- Chokepoints as the true crossroads of history.

- Brad Delong with a quick primer on contango, backwardation and the oil market.

- Understanding recent fluctuations in gold prices.

- The Bank of England considers the rise of dynamic, personalised pricing.

- The McKinsey Global Institute has more thoughts on the next big arenas of competition.

- Why Japan has such good railways.

- Bloomberg’s Trumponomics podcast on the long-term global economic damage from the war with Iran.

- The FT’s Unhedged podcast on Guns, butter and credit asks, are current events echoes of the 1970s, or of the 1960s?

- The ABC’s The Economy, Stupid podcast on Australia’s baby bust.

Latest news

Already a member?

Login to view this content