Overview

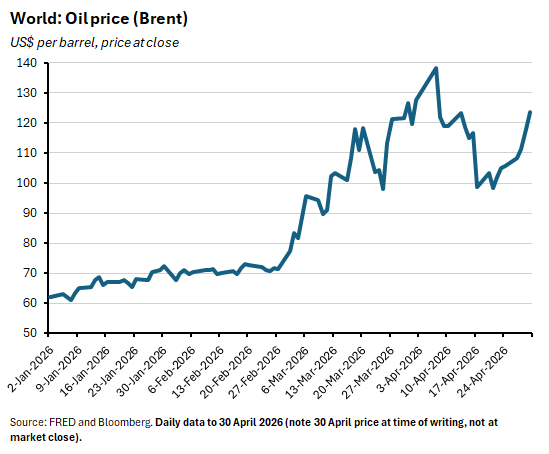

- Disruption to global energy and other markets persists as the world economy remains hostage to chokepoint risk at the Strait of Hormuz. Oil prices have now risen for the past eight days.

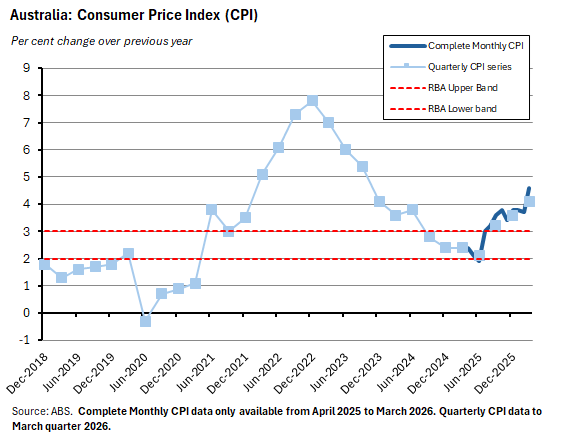

- The first evidence of the inflationary impact of the war appeared in this week’s March 2026 Consumer Price Index data. The annual rate of headline inflation rose to 4.6% last month – the highest reading since September 2023 – after automotive fuel prices jumped by nearly 33% over the month to be up more than 24% over the year.

- The annual rate of underlying inflation on the RBA’s preferred measure (the quarterly trimmed mean series) was 3.5% in the March quarter and hence remained uncomfortably above the top of the RBA’s target band. That will help keep the pressure on the Monetary Policy Board to deliver another rate hike next week. That said, with war uncertainty still high, a likely re-run of the March policy debate over tightening vs waiting means the decision should once again be a close-run thing.

This week we note the persistence of the disruption to global supply conditions arising from the war in the Gulf before considering the initial impact on Australian inflation as seen in the March 2026 Consumer Price Index results. With the Reserve Bank’s Monetary Policy Board (MPB) meeting next week, we judge that the latest inflation data are unlikely to radically change minds from the positions set out in the March MPB meeting. It follows that while a rate hike is marginally the more likely option next week, the decision could again prove to be a close one (although note that market pricing is currently considerably more confidentin predicting another 25bp rate hike on 5 May).

And a reminder that there will be a post-Budget economics webinar on 14 May. As usual, it will be free for ACID members. For more details see: Budget 2026 and the New Economic (dis)Order

An extended disruption to global supply

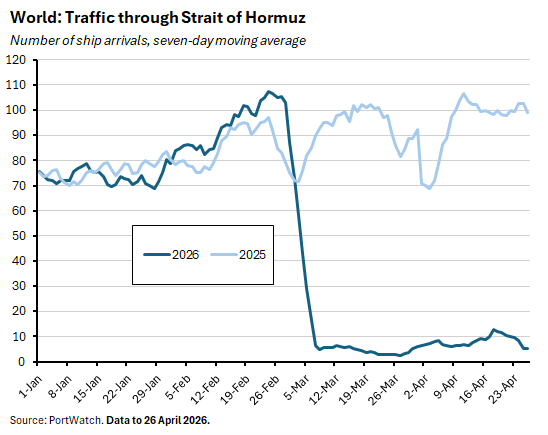

While the intensity of the war in the Middle East has declined, the disruption to the Strait of Hormuz and to global energy and other markets continues, as shipping through the global chokepoint remains heavily restricted.

The absence of any substantial progress in re-opening the Strait has adverse implications for the global outlook. Recall that in the most recent IMF World Economic Outlook, the Fund had sketched out three scenarios for the world economy – a reference scenario, an adverse scenario, and a severe scenario. As of now, the continued interruption to global supply means that relatively more benign economic scenarios such as the Fund’s reference scenario, which were predicated on a quick end to the conflict, are disappearing into the global rear-view mirror. Instead, the question is which of the other two options (adverse vs severe) will now apply. Meanwhile, oil prices have started to head back up, with eight consecutive days of price increases for Brent crude reflecting a shift to market pessimism on the prospects for any swift easing in supply constraints.

Note that beyond global energy markets, the conflict is also reshaping the economics and geoeconomics of the Middle East in interesting ways, with the UAE recently exiting from OPEC following earlier news that the Emirates along with other US allies in the region had opened talks with Washington about a financial backstop.

Higher fuel prices pushed up March inflation in Australia

The absence of any resolution to the situation in the Gulf is also unwelcome news for Australia’s inflation outlook. This week, the ABS said that Australia’s Consumer Price Index (CPI) rose 1.1% over the month in March 2026 to up 4.6% over the year. The market had expected a slightly higher annual rate of inflation last month, with the consensus forecast anticipating a 4.8% print. Even so, headline inflation is now at its highest rate since September 2023 (when it reached 5.4%) and roughly level with the December quarter 2023 outcome.

In the case of the quarterly CPI, the headline figure was up 1.4% quarter-on-quarter in the March quarter 2026, in line with the consensus forecast. The annual rate rose to 4.1%, up from 3.6% in the December quarter 2025.

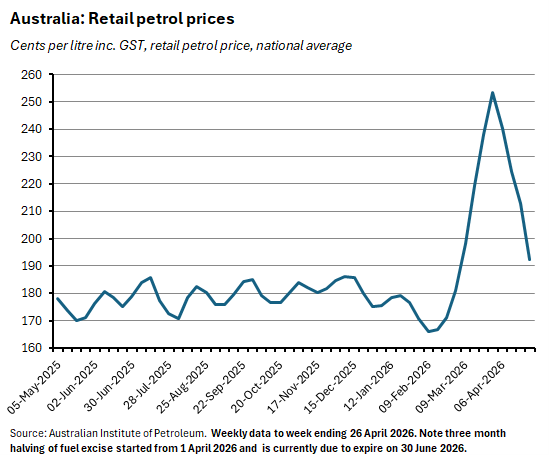

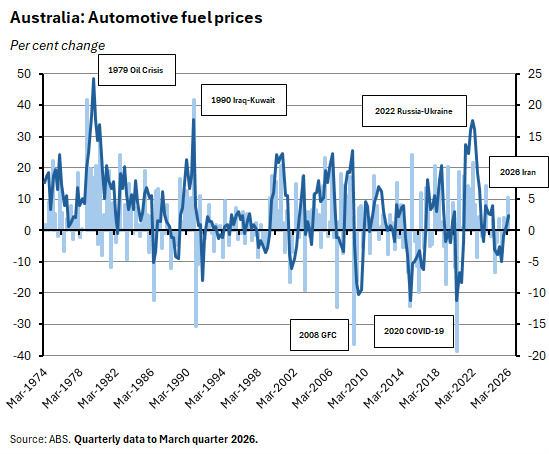

The March monthly and quarterly CPI numbers are the first to capture the implications of the war in the Middle East for Australian inflation outcomes. The latter manifested in a 32.8% monthly jump in automotive fuel prices in March – the largest since the current series began in 2017 – which translated into an annual rise of 24.2%. This in turn produced a sharp 9.2% monthly increase in the Transport Group overall, which rose 8.9% over the year. Note that these increases all arrived before the government halved the fuel excise tax for three months, effective from 1 April this year.

According to the quarterly data on fuel prices, which offer a longer perspective than the new monthly series, although the current spike in prices is already significant, it has yet to reach the scale of past shocks, including most recently the post-COVID inflation spike and the 2022 Russian invasion of Ukraine. In the March quarter this year, the quarter-on-quarter increase in prices was 5.2% compared with nearly 11% in the March quarter 2022, for example. And on a year-on-year basis, the latest result was just 4.8%, compared with rates of more than 30% experienced in 2021 and 2022.

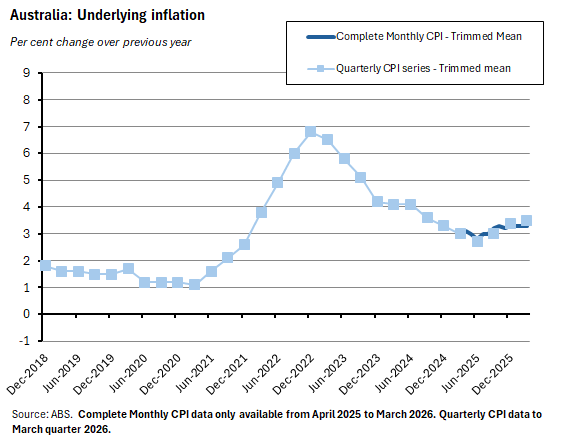

While the RBA’s inflation target is set in terms of the headline rate, when it comes to implementing policy Australia’s central bank pays more attention to underlying inflation in the form of the trimmed mean. And until it is fully comfortable with the properties of the new monthly series, Martin Place has said that it will continue to focus on measures of underlying inflation from the quarterly CPI. For now, the Gulf energy price shock has yet to have a significant impact on measures of underlying inflationary pressures (although this will change over time as higher input costs feed through into other prices and – possibly – wages).

According to this week’s release, for example, the trimmed mean measure of underlying inflation rose by 0.8% over the quarter to be up 3.5% over the year. That outcome was a little softer than the consensus forecast for 0.9% over the quarter but in line with the market expectation for a 3.5% annual rate. It was also little changed compared to a December quarter 2025 outcome of 0.9% quarter-on-quarter and 3.4% year-on-year. The new monthly series meanwhile put the annual rate of increase of the trimmed mean at 3.3%, a rate which has been unchanged for four consecutive months.

An alternative quarterly measure of underlying inflation, the weighted median, sent a similar signal. It too was up 0.8% over the quarter (down from 1% in the December quarter 2025) to be 3.5% higher over the year (up from 3.3% in December).

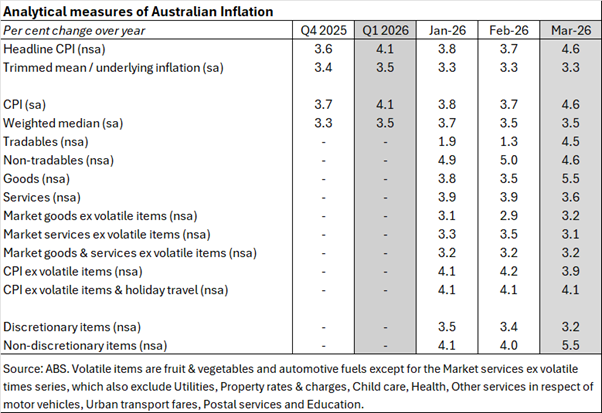

A glance at the other analytical measures of inflation suggests that they are broadly consistent with this story of an initial but limited impact from the conflict in the Middle East. Higher fuel prices were reflected in marked increases in the annual rate of goods and tradables inflation last month and were also visible in a pickup in price rises for non-discretionary items. Meanwhile, the annual rate of increase in some services-based series ticked down.

That said, underlying inflation in March was still stuck above the top of the RBA’s target band according to both the new monthly and the old quarterly measures. And war-driven fuel prices were not the only source of price pressure. While the Transport Group contributed about one percentage point to the 4.6% headline inflation rate in March, for example, the contribution from the Housing Group was even higher, at around 1.4 percentage points. Part of the story here was the ongoing impact from higher electricity costs and the exhaustion of Commonwealth and State Government electricity rebates by households. But there was also continued pressure from new dwellings and rentals prices.

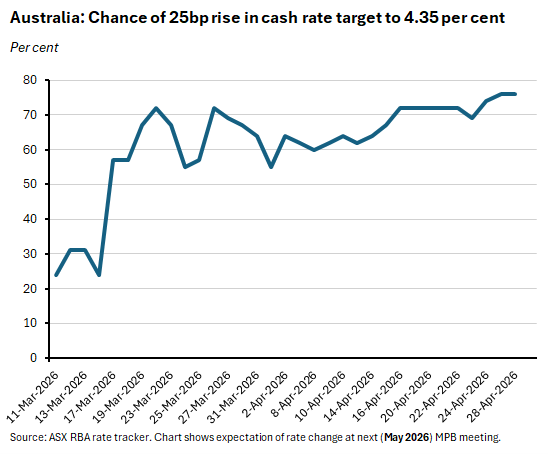

Where does all this leave the RBA and the Monetary Policy Board (MPB) ahead of next week’s MPB meeting? There was probably little in this data release to change the position of either side of the debate. On the one hand, both headline and underlying inflation remain uncomfortably above target, and thanks to the Gulf war are likely to deviate further from target in the June quarter. On the other hand, the uncertainties around the impact of the war remain elevated, the duration of the conflict is now already longer than had been assumed in some of the more optimistic scenarios, and the downside risks to future activity are mounting. All of which points to a re-run of the debate at the March 2026 MPB meeting (covered in our review of the meeting’s minutes) between acting vs waiting. If so, another split decision could be on the cards, probably leading to another close vote to lift the cash rate.

At the time of writing, however, market pricing was more confident than this in judging the likelihood of policy tightening. It put a greater than 75% probability on another 25bp rate hike next week.

Other Australian data points to note

The ANZ-Roy Morgan Consumer Confidence Index rose 3.5 points to 68.7 points for the week ending 26 April 2026. While the index remains deep in pessimistic territory, this was the strongest weekly confidence reading since mid-March. ANZ said that all the subindices rose over the week, with the improvement in sentiment led by greater confidence in short-term and medium-term economic confidence. According to the same survey report, weekly inflation expectations eased by half a percentage point to 6.6%, marking their lowest rate since early March and the start of the Middle East conflict.

The ABS said that as of 30 June 2025, Australia’s overseas-born population was 8.8 million people, or about 32% of the estimated resident population of 27.6 million. According to the Bureau, the last time our overseas-born share was this high was back in 1891. Over the two decades since 2005, Australia’s overseas-born population has grown at an average annual rate of 3% while the Australia-born population grew at an average of just 1% over the same period. The four most common countries of birth (comprising more than one-third of all Australians born overseas) are India, England, China, and New Zealand.

New ABS data on international trade for the 2025 calendar year reports that Australia’s trade balance on goods and services was in surplus by $6.9 billion, with a large surplus on goods trade offsetting a deficit of $37.5 billion on services trade.

Further reading and listening

- The ABS gives a brief history of automotive fuel prices in the CPI. Also from the Bureau, seven new insights on Australia’s ecosystems and eight things of interest about Australia’s overseas-born population.

- A McKinnon report on 25 years of false starts in Australian tax reform. The ‘Reform Matrix’ on page eight which starts with the 1999-2000 Ralph Review of Business Taxation and ends with the 2018 Turnbull corporate tax cuts makes for sombre reading with its list of ‘abandoned’, ‘repealed’, ‘not implemented’ and partially implemented measures. See also this AFR story on the new push for tax reform.

- The e61 Institute says indexing tax (and not just CGT) is a good idea.

- On the new $1,000 tax offset.

- The independent Review of the Australian Office of Financial Management.

- The World Bank’s April 2026 Commodity Markets Outlook includes a special focus on the effects of geopolitical oil supply shocks. See also why geopolitical oil shocks hit harder. According to the authors, oil price shocks associated with geopolitical tensions differ from other oil price shocks in several ways: they produce bigger price increases for a given fall in supply; generate a distinctive inventory cycle that is characterised by precautionary stockpiling; lead to more persistent economic downturns; and are bad news for importers and exporters.

- Related, the IMF charts the impact of the Middle East war on oil exporters and importers.

- Also related, the IEA’s latest quarterly gas report covers the impact of the current conflict on gas markets. The Agency reckons that the disruption to shipping through the Strait of Hormuz has removed close to 20% of global LNG supply from the market, while global LNG production fell 8% year-on-year in March. In the longer run, it thinks that the damage to energy infrastructure in Qatar will reduce projected supply growth and delay an anticipated global LNG expansion wave by at least two years, keeping gas markets tight through 2027.

- Also from the IEA, Global Energy Review 2026.

- Another entry into the ‘war and future of the petrodollar’ debate, as this FT essay argues that there’s no such thing as the petrodollar.

- Also from the FT, should your board appoint a bot?

- A new BIS Bulletin examines the de facto currency risk exposure of investment funds.

- Understanding (UK) inequality.

- Lessons from four centuries of Brazilian growth data.

- The WSJ looks at the divided US Fed that will be inherited by incoming Fed Chair Kevin Warsh.

- The Peterson Institute’s Kimberly Clausing on lessons from three global collective action problems – climate change, international trade, and international taxation.

- The MIT Technology Review lists ten things that matter in AI right now, from humanoid data and supercharged scams to agent orchestration and artificial scientists, via weaponized deepfakes and the new war room.

- The 2026 edition of the OECD’s inventory of export restrictions on critical raw materials says that restrictions have increased fivefold since 2009 and remain at historically high levels after sharp increases in 2022-23.

- About a year on from the publication of Abundance, Ezra Klein and co-author Derek Thompson are joined by Marc Dunkelman (author of Why Nothing Works) to discuss what has the abundance movement achieved (in the United States) over the past year.

- The Econoclasts podcast offers an interpretation of the new US dollar swap lines for the Persian Gulf.

- The Trumponomics podcast on regime change at the US Fed.

- The Econtalk podcast ruminates on the battle between Anthropic and the US Department of War

Latest news

Already a member?

Login to view this content