Overview

- The onset of the US blockade on Iranian shipments will further tighten an already-squeezed oil market, which according to the IEA had suffered a net lossof oil exports of more than 13 million barrels per day last month.

- The latest IMF projections for the world economy illustrate the dilemma facing all forecasters right now - outcomes remain conditional on the ultimate size of the global energy shock and therefore on the duration and intensity of the war in the Middle East. That means the Fund’s three scenarios for the international economic outlook range from a manageable hit to growth through to the risk of the world economy succumbing to what would be a fifth global recession since 1980.

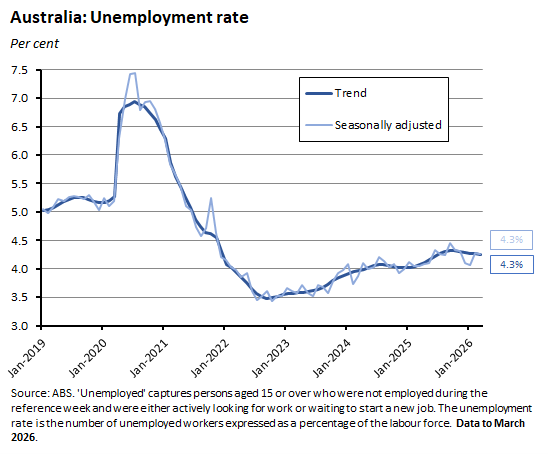

- The global energy shock has yet to be felt in the Australian labour market. Hours worked and the number of employed persons were both up last month while the unemployment rate held steady at 4.3 per cent. In contrast, while activity has been resilient to date, both consumer and business sentiment have deteriorated markedly.

- The AICD’s latest DSI survey shows that directors were already feeling wary about economic prospects even before 28 February and Operation Epic Fury. Pre-war, productivity growth was at the top of their policy to-do list for Canberra.

This week brought another example of Murphy’s Law – anything that can go wrong will go wrong – in action. As we discussed in some detail previously, Australia’s fuel security now depends in part on our two remaining domestic refineries, the Viva Energy Geelong Refinery in Victoria and the Ampol Lytton Refinery in Brisbane, Queensland. And now a major fire has damaged the Geelong refinery. The timing is unfortunate to say the least, suggesting that in this case it is actually Finagle’s Law that is applicable: Anything that can go wrong will – and do so atthe worst possible time.

With that insight into risk management in mind, this week we review new IEA data on the scale of the unfolding disruption to global oil supplies, consider the IMF’s latest projections for the global economy, and assess the March 2026 Australian labour market numbers. We also examine the messages from the AICD’s H1:2026 Director Sentiment Index and summarise this week’s updates on the state of domestic consumer and business sentiment.

Updating the scale of the oil shock

This week saw a US naval blockade on shipping from Iranian ports go into effect. By restricting Iranian oil shipments, the blockade will squeeze not just Tehran but also place additional pressure on an already-tight global oil market.

The timing is tricky. On some estimates, the final pre-war oil shipments to leave the Persian Gulf are due to arrive in Asia and Australia within the next week, after which physical shortages could start to appear. Meanwhile, European, and Asian refineries are reportedly engaged in bidding wars for supplies of crude, leading to record highs in physical spot (as opposed to futures) prices.

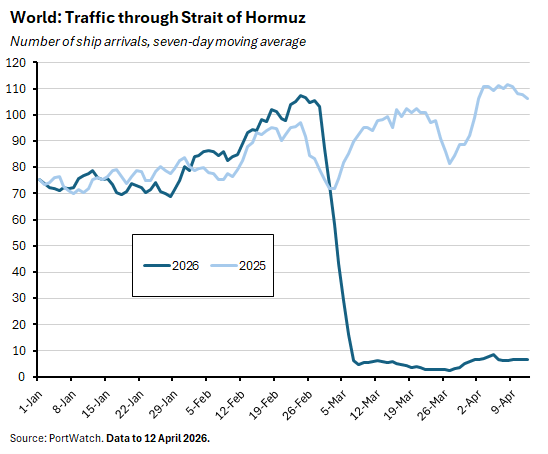

In this context, the International Energy Agency (IEA) has revisited the numbers on global oil exports and oil supply in the April 2026 edition of its monthly Oil Market Report. According to the IEA, in the month prior to the war, more than 20 million barrels per day (mb/d) of crude, natural gas liquids and refined products were moving through the Strait of Hormuz. As of early April, before the current US blockade took effect, Gulf loadings had fallen to around 3.8 mb/d. At the same time, exports through alternative routes – including via pipeline to the west coast of Saudi Arabia and to Fujairah on the east coast of the UAE – had risen from less than 4 mb/d pre-war to 7.2 mb/d. The net impact of those shifts created an overall loss in oil exports of more than 13 mb/d. Add in associated production restrictions and damage to regional energy infrastructure, and the IEA estimates cumulative supply losses of more than 360 mb in March and predicts a shortfall of 440 mb this month.

The IEA also calculates that global oil supply plummeted by 10.1 mb/d in March, making it the largest disruption on record. OPEC+ oil production fell 9.4 mb/d last month while non-OPEC+ supply fell by 770 thousand barrels per day (kb/d) as lower output from Qatar offset increases in oil production by Brazil and the United States.

Part of the resulting gap between demand and supply has been filled by a decline in oil inventories, with the IEA reporting a fall of 85 mb in global observed oil stocks in March. That surprisingly small drop in global reserves disguises a big fall in stocks outside the Gulf, with the latter drawn down by a considerably larger 205 mb, equivalent to about 6.6 mb/d. But in the Middle East, stranded oil production meant that floating storage of crude and oil products in the region rose by 100 mb while onshore crude stocks were up a further 20 mb.

The remaining demand-supply gap has been closed by demand destruction from higher prices. The IEA reckons that, in year-on-year terms, global oil demand contracted by 800 kb/d in March and it predicts a further 2.3 mb/d fall in April. All up, on its latest numbers, global oil demand is projected to be down by 80 kb/d on average across the whole of this year. In last month’s report, it was still predicting demand growth of around 730 kb/d.

Finally, note that the IEA does say that if the war ended soon and the Strait was then reopened, the world would still return to a position of excess oil supply. But that surplus would now be much narrower than the one projected before the conflict, at less than 500 kb/d.

The IMF flags global recession risk

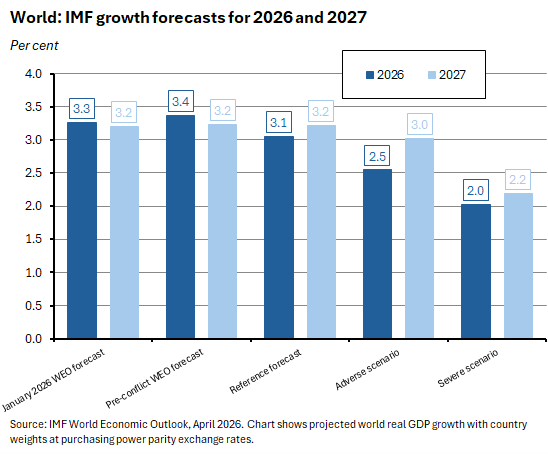

This week also saw the IMF release updated economic forecasts in the April 2026 edition of the World Economic Outlook, which considers the global economy in the shadow of war. Reflecting the uncertainty as to where things go from here, the Fund presents three alternative scenarios:

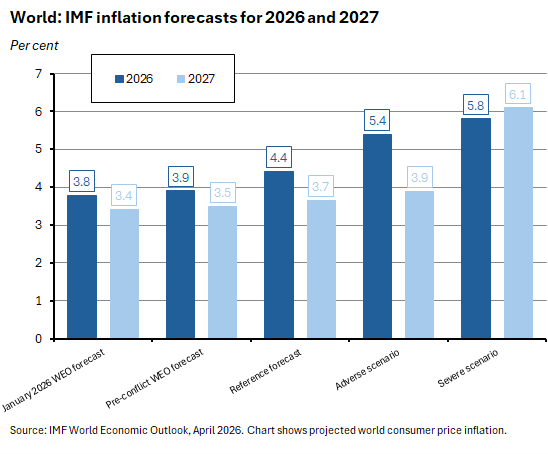

1. In the IMF’s reference forecast, the war is assumed to be short-lived from this point. That implies oil prices averaging around US$82/b this year and US$76/b in 2027, up from around US$68/b last year. On that basis, global economic growth is forecast to be 3.1 per cent this year and 3.2 per cent in 2027. Expected growth this year is therefore down from 2025’s estimated 3.4 per cent outcome, although this represents ‘only’ a modest 0.2 percentage point cut to the growth projection for this year in the January 2026 WEO Update. Then, the IMF had predicted real GDP growth of 3.3 per cent this year and 3.2 per cent next year. Note, however, that the Fund says that an updated pre-war forecast would have instead increased the growth outlook for this year to 3.4 per cent. That implies a 0.3 percentage point hit to global growth due to the war. The reference scenario projects world consumer price inflation to run at 4.4 per cent this year and at 3.7 per cent next year. That represents increases of 0.6 and 0.3 percentage points respectively, relative to the January 2026 WEO, which had anticipated inflation running at 3.8 per cent in 2026 before easing to 3.4 per cent in 2027.

2. In the adverse scenario, a longer conflict sees the oil price average around US$100/b across this year before falling to US$75/b next year. Gas and food prices are also higher in this scenario, inflation expectations increase further, and a risk-off move in financial markets sees financial conditions tighten through 2026 before easing in 2027. As a result, the downgrade to global growth is greater than in the reference forecast, at 0.8 percentage points in 2026, with the economy expected to grow at just 2.5 per cent. The growth projection for 2027 is also lower by 0.2 percentage points, at three per cent. Inflation is projected to be higher, running at 5.4 per cent this year and 3.9 per cent in 2027.

3. Finally, in the Fund’s severe scenario, the shock to oil prices is larger and more persistent, extending into next year. Under this scenario, the oil price averages US$110/b through this year and US$125/b in 2027, only falling in 2028. The assumed increases in gas and food prices – and therefore in inflation expectations – are also larger, and the resulting risk-off episode and consequent tightening in financial conditions is more brutal than in the adverse scenario. In this version of the world, global growth in 2026 is projected to be just two per cent and growth next year would be a subdued 2.2 per cent. In this severe scenario, inflation would also run much hotter, at 5.8 per cent this year and 6.1 per cent in 2027.

Should the third, severe scenario eventuate, the world economy would be flirting with falling into a global recession (defined as sub-two per cent growth). To date, there have only been four global recessions since 1980, with the most recent two triggered by the global financial crisis and the COVID-19 recession.

No surprise, then, that the IMF warns that risks to the global economic outlook are now ‘firmly on the downside’, with those threats dominated by threats arising from the conflict in the Middle East but also including the danger of markets turning pessimistic on the AI story, the possibility of a further international shift towards protectionist policies, the scope for high sovereign borrowing needs to trigger a repricing of financing costs, and an erosion of confidence in economic institutions, for example via the decline of central bank independence (in which context, there were overnight headlines citing President Trump’s latest threats to fire US Federal Reserve Chair Jerome Powell). Set against those worries, the Fund does list three upside risks: an earlier-than-expected materialisation of productivity gains from AI; accelerated structural reforms should policymakers ‘seize the moment’ offered by crisis; and the possibility of progress in new trade deals and greater policy predictability.

Financial markets continue to bet that another TACO episode will mean that it is the Fund’s reference scenario that will come to pass. And that may prove to be the case. But the list of downside risks is concerning, and the prospect of the world economy having to deal with one or more disruptions in addition to the war in the Middle East is a daunting one.

Which, alas, brings us back to Finagle’s Law.

Australia’s labour market remains resilient

On a more positive note, and despite a backdrop of global economic turmoil, Australia’s labour market continues to demonstrate its ongoing resilience.

According to the ABS’s Labour Force report for March 2026, the impact of the war in the Middle East has not yet had a major influence on business hiring decisions. Granted, at 17,900 the monthly (seasonally adjusted) increase in employment was a bit softer than the market consensus forecast which had called for a 20,000 print. A 52,500 increase in full-time employment was partly offset by a 34,600 drop in part-time employment. But in a sign of ongoing strength, monthly hours worked in all jobs increased by nine million hours over the month (0.5 per cent) to be up 2.5 per cent over the year.

At the same time, the unemployment rate was unchanged at 4.3 per cent, this time in line with the consensus forecast. With the underemployment rate also unchanged at 5.9 per cent, the underutilisation rate likewise held steady, at 10.2 per cent.

Continuing the theme of stability in last month’s data, March also brought no change in the employment to population ratio, which remained at 64 per cent. There was a change in the participation rate, however, which nudged down to 66.8 per cent from 66.9 per cent in February.

While the March labour force numbers are broadly consistent with the RBA’s judgement (reported in the Minutes of the March 2026 MPB Meeting and discussed here) that the balance of risks in the first quarter of this year had shifted away from a weakening labour market to one where conditions looked to be on the tight side, that judgement is now very much hostage to developments in the Persian Gulf. A prolonged disruption will manifest in fewer hours worked and more job losses. Indeed, given the energy shock to date plus the two rate increases already delivered by the RBA, some future labour market weakening is probably already locked in.

The DSI on productivity, AI, and the pre-war economy

The results from the AICD’s latest Director Sentiment Index (DSI) are now in. Thank you to all those readers who were able to participate this time.

The underpinning poll for the H1:2026 DSI was in the field between 20 February and 10 March this year, with the majority of the responses collected before the 28 February start of war in the Middle East. That means the DSI mostly offers a snapshot of the Australian economy on the eve of the war, before directors had to fully consider the implications of escalating geopolitical risk, rising energy prices, and the threat of outright fuel shortages. As a result, the slight improvement recorded in the overall DSI score (from -29.1 in H2:2025 to -24 in H1:2026, so still deep in negative territory) is almost certainly an overestimate of the current level of sentiment.

What the DSI does tell us is that, even before the onset of Gulf War 3.0, respondents were concerned about the economic situation. Domestic economic conditions were the number one issue keeping directors awake at night (cited by 34 per cent of respondents, up from 28 per cent in the previous survey), and ahead of legal and regulatory compliance (31 per cent) and cyber-crime/data security (29 per cent). Directors identified the top economic challenges facing Australian business as productivity growth (cited by 41 per cent of respondents), global economic uncertainty (34 per cent) and regulation requirements/red tape (29 per cent). They were also mindful of the headwinds coming from global economic conditions, with 25 per cent saying that the recent state of the global economy had seen their company scale back investment plans. And they felt that Australian trade flows (57 per cent of respondents), supply chains (47 per cent), exchange rates (46 per cent) and commodity prices (44 per cent) could all be significantly influenced by the Trump administration’s exercise of economic diplomacy over the coming 12 months.

Pre-war, productivity was very much front of mind according to the H1:2026 DSI. As well as being the top economic challenge facing business, respondents said that productivity growth should be the top issue that the Federal government addresses both in the next three years and over the next 10 to 20 years. A clear majority of respondents (68 per cent) agreed with the proposition that regulatory and compliance requirements were limiting productivity growth in their business and 73 per cent thought that a major business deregulation agenda would have a positive impact on Australia’s productivity and economic growth, with planning regulations (cited by 50 per cent of respondents), industrial relations (also 50 per cent) and construction and building regulations (33 per cent) the top three choices for policy focus.

Housing supply was viewed as the most important investment priority for enhancing national productivity (cited by 56 per cent of respondents), followed by regional infrastructure (43 per cent) and renewable energy (36 per cent).

More than 60 per cent of directors said that AI tools had made either a significant (12 per cent) or somewhat positive (51 per cent) impact on performance and productivity in their business, although in the overall rankings, technology solutions still fell behind workplace culture and leadership and management quality as the factors with the largest impact on boosting productivity.

Sticking with AI, more than 80 per cent of respondents expected an increase in AI and digital implementation in their business over the next 12 months. In terms of the associated labour market implications, 24 per cent of directors said that AI would have a significant impact on skill requirements over the coming year and a further 52 per cent foresaw a slight impact. The expected impact on workforce size is more modest, with only six per cent predicting a significant effect while 36 per cent are anticipating a slight one.

Other Australian data points to note

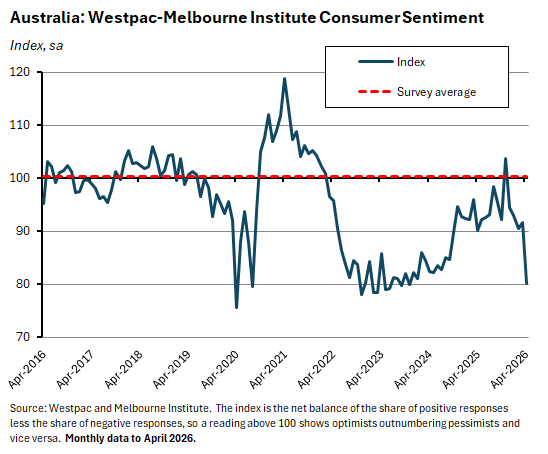

The monthly Westpac-Melbourne Institute Consumer Sentiment Index slumped by 12.5 per cent over the month in April 2026, falling to a reading of just 80.1. That monthly fall in sentiment is the largest since the onset of the COVID-19 pandemic and returns the index to close to (but still above) historic lows. Westpac noted that all five sub-components of the headline index fell sharply in April, with double-digit monthly declines for ‘Family finances vs a year ago’ (down 16.7 per cent), ‘Time to buy a major household item’ (down 15 per cent), ‘Family finances next 12 months’ (down 13.9 per cent) and ‘Economic conditions next 12 months’ (down 12.4 per cent). There was also a relatively more modest 5.1 per cent decline for ‘Economic conditions next five years.’

Consumer sentiment is being hit by higher fuel prices, higher interest rates, and increased concerns about job losses. The Westpac-Melbourne Institute Mortgage Rate Expectations Index (which tracks expectations for variable rate mortgages over the coming year) rose 3.9 per cent, as amongst those with a view, just over 80 per cent said they expected mortgage rates to rise further over the next 12 months, with 40 per cent expecting that rise to be greater than 100bp. At the same time, the Westpac-Melbourne Institute Unemployment Index jumped 9.7 per cent, indicating a sharp increase in the share of respondents expecting unemployment to rise over the year ahead. Westpac said that this was the worst read on job expectations since August 2020 and the COVID-19 pandemic.

Shifting from a monthly to a weekly frequency, the ANZ-Roy Morgan Consumer Confidence Index recorded a second consecutive weekly increase, rising by 2.2 points to 64.5 for the week ending 12 April 2026. ANZ noted that the modest improvement in confidence may have reflected news of the US-Iran ceasefire, although the result still marked the fourth-lowest reading in the history of the series. The ceasefire – and the consequent dip in oil prices – may also explain a 0.5 percentage point fall in weekly inflation expectations, which dropped to 6.7 per cent last week. Again, however, the improvement was limited: at seven per cent on a four-week moving average basis, inflation expectations remained at their highest level since the inflation series was introduced in 2010.

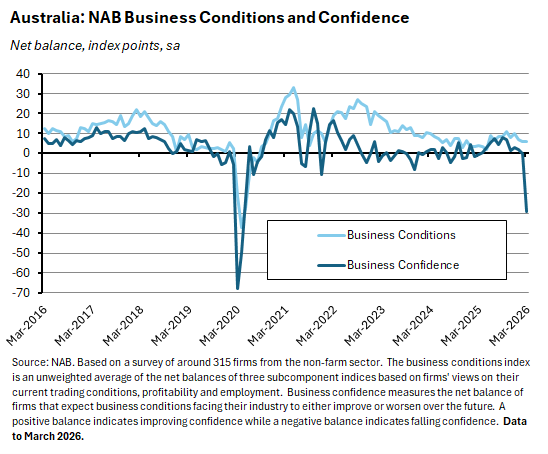

The NAB Monthly Business Survey reported a sharp fall in business confidence in March 2026. The measure of confidence slumped by 29 points to -29 index points, the second largest monthly fall in the history of the survey. In contrast, business conditions eased by just one point to a reading of +6 index points. The gap between the two measures shows that while the conflict in the Middle East has already triggered a sharp decline in sentiment, the initial impact on activity has so far been modest. Indeed, the capacity utilisation rate nudged higher last month, rising from 82.9 per cent to 83.1 per cent.

The implications for costs look to have been considerably larger, as the rate of growth in purchase costs (quarterly equivalent terms) jumped from 1.3 per cent in February to three per cent in March. Labour cost growth was unchanged at 1.5 per cent while growth in product prices accelerated from 0.7 per cent to 1.1 per cent. Retail price growth eased last month, slowing from 0.9 per cent in February to 0.5 per cent in March.

Further reading and listening

- A fireside chat with RBA Deputy Governor Andrew Hauser. According to Hauser, ‘…it’s obvious that inflation is going up in the short term, and people are very conscious of that. We can see that in consumer surveys. There’s not much monetary policy can do about that, other than prevent it from getting into long term inflation expectations. The big question for us is what it’s going to do to activity, and therefore what that’s going to do to inflation over the medium term…So it is a central banker’s nightmare. You know, the stagflationary shock: inflation up, activity down. Judging the balance between those two is, I guess, how we earn our money.’

- On Australian recession risk.

- A new Grattan Institute report offers some advice on how to future-proof Australian democracy. Proposals include: acting to reduce the influence of money in parliament; commissioning an independent review of parliament that could consider potential reforms to size, committees, standards and codes of conduct; creating more ways for Australians to have a say and be heard; disclosing ministerial diaries; considering the role of deliberative processes such as citizen assemblies; providing clearer pathways from permanent residency to citizenship; reinvigorating local government elections; and more.

- A sceptical take on Australia’s current approach to EV subsidies.

- Do Australian boards lack members with sufficient technological expertise?

- How the ABS quality assures Australian labour force data during times of change.

- From the WSJ, the Unravelling of the era of free seas. And Greg Ip writes that Chokepoints beat tariffs in economic war.

- A new IEA report, the State of Energy Policy 2026, says that in recent years ‘energy has been elevated to a core issue of national and economic security’ with governments spurred to act by the pandemic’s global supply chain disruptions, the Russian invasion of Ukraine, the proliferation of trade restrictions on key products, and now conflicts involving major energy suppliers. Direct government spending on energy has doubled since 2019 and the IEA projects it to remain elevated through 2030. The Agency also speculates that the current crisis could encourage longer-term structural shifts in energy policy, noting that as of April this year, ‘150 countries have active policies to advance renewable and nuclear deployment, 130 have energy efficiency and electrification policies, and 32 have policies to incentivise supply chain resilience and diversification across critical minerals and clean energy technologies.’

- Carnegie on China’s approach to energy security – electrification plus coal.

- Why corporate tax responsiveness varies widely across countries.

- This research from the US Fed says that US labour force growth could be near-zero starting from this year, reflecting a combination of low net immigration and declining labour force participation due to population ageing. If sustained, two implications are that breakeven employment growth will also be near-zero (such that in any given month, negative job growth will be almost as likely as a positive outcome) and that any growth in potential GDP will need to come from productivity growth.

- This policy brief from the United Nations Development Program (UNDP) provides an assessment of the impact on poverty of the war in the Middle East. The UNDP reckons that up to 32.5 million people across the Middle East, Africa and Asia could fall into poverty because of the ‘triple shock’ comprising lower energy affordability and availability, food price increases, and GDP downturns. The UNDP also estimates that Iran has lost the equivalent of one and a half years in human development (loss of physical infrastructure, energy infrastructure, and disrupted lives and livelihoods) in the first month of the conflict.

- According to the OECD, last year official development assistance (ODA) by Development Assistance Committee (DAC) members and associates suffered its largest annual contraction on record, dropping by 23.1 per cent. The five largest DAC providers (Germany, the US, the UK, Japan, and France) accounted for more than 95 per cent of the fall.

- Also from the OECD, a major new report on Foundations for Growth and Competitiveness. Here are the accompanying data dashboards.

- The Odd Lots podcast on the big macro force that’s been driving up US stock valuations.

- Adam Tooze on historical parallels with today’s energy crisis.

Latest news

Already a member?

Login to view this content