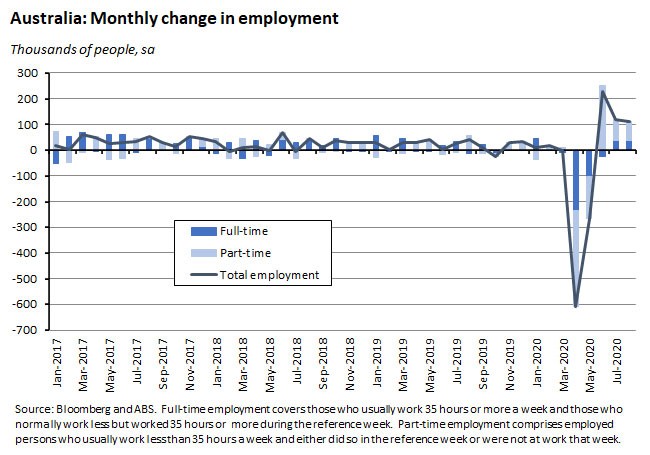

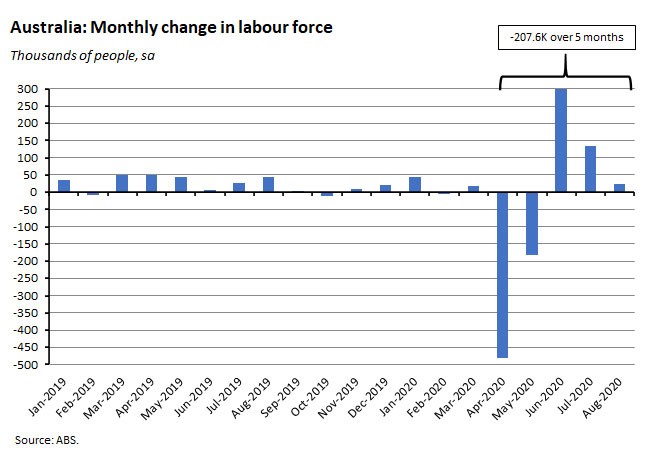

August’s labour market report was surprisingly strong, delivering a marked decline in the unemployment rate, a small rise in the participation rate and an increase of 111,000 in employment.

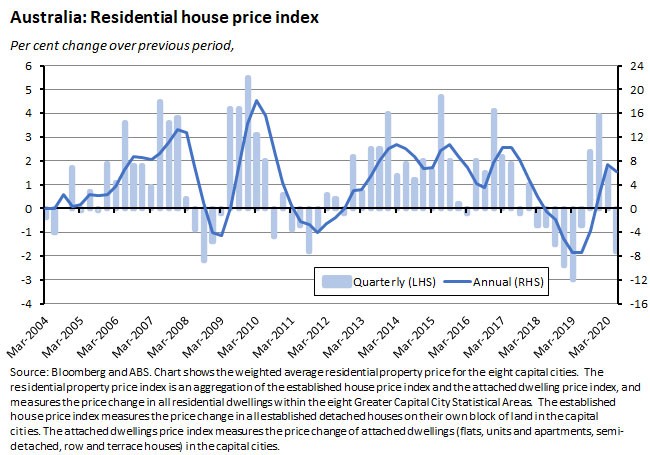

The minutes from the RBA’s 1 September meeting shed no new light on the central bank’s thinking about the possible mechanics of any future monetary easing. Average ABS residential property prices across the eight capital cities fell 1.8 per cent in the June quarter but were still up 6.2 per cent over the year. Weekly consumer confidence rose for a second consecutive week. The US Fed delivered its first FOMC meeting under its new monetary policy strategy but didn’t fill in any of the details. International data trends indicate that global activity has enjoyed a relatively strong bounce back from the initial bout of pandemic-driven economic dislocation, but there are also signs that recovery momentum may now have slowed.

This week’s readings include the ABS on an unprecedented series of events, a new RBA bulletin, CSIRO on science and technology growth opportunities, new economic updates from the OECD and the ADB, five book recommendations on the Classical Economists, a primer on Modern Monetary Theory (MMT) and a retrospective on Abenomics and six lessons from Japan for the rest of the world economy.

Also stay up to date on the economic front with our AICD Dismal Science podcast. This week we cover the surprise jobs report, house prices, the new Fed guidance and Kiwi GDP.

What I’ve been following in Australia

What happened:

According to the ABS, employment increased by 111,000 to 12,583,400 people in August. Full-time employment rose by more than 36,000 while part-time employment was up by almost 75,000.

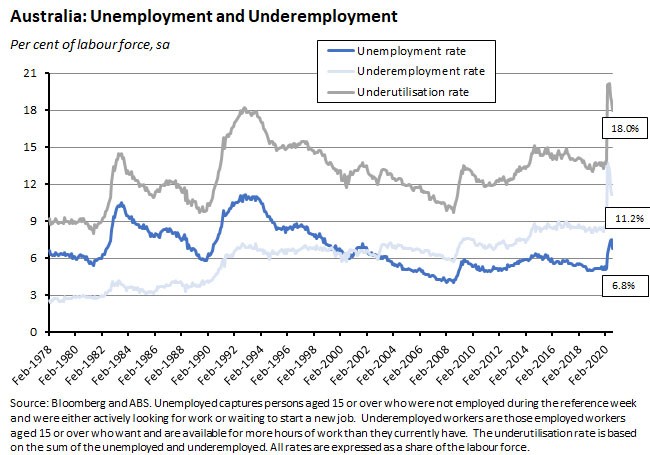

The number of unemployed fell by 86,500 to 921,800 people – back below one million after July’s unwelcome result – taking the unemployment rate down 0.7 percentage points to 6.8 per cent. With the underemployment rate unchanged at 11.2 per cent, the underutilisation rate likewise dropped 0.7 percentage points to 18 per cent.

Monthly hours worked in all jobs increased by 1.6 million hours (0.1 per cent) to 1,683.4 million hours.

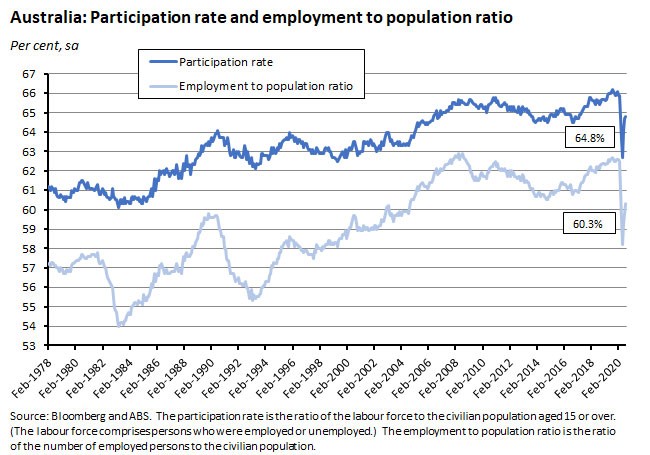

The participation rate edged up to 64.8 per cent while the employment to population ratio rose to 60.3 per cent.

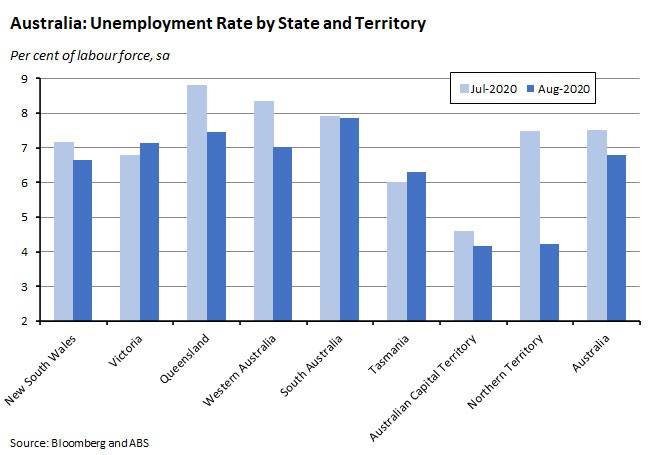

All states and territories recorded increases in employment last month apart from Victoria, where the number of employed people fell by 42,400. The NT enjoyed the fastest rate of employment growth (up 4.6 per cent) but in absolute terms the largest gains were in New South Wales (with an increase of 51,500 employed people) and Western Australian (up 32,200).

The unemployment rate rose in Victoria (up 0.4 percentage points to 7.1 per cent) and Tasmania (up 0.3 percentage points to 6.3 per cent) but fell in most other states, with the largest decline in the NT (down 3.3 percentage points to 4.2 per cent).

Why it matters:

This was an extremely strong labour market result and much better than expected. The median forecast had been for employment to fall by 35,000, the unemployment rate to rise to 7.7 per cent, and the participation rate to dip to 64.6 per cent. In all three cases, the consensus was wrong not just about the magnitude of the outcome but also about the direction of change. That’s because there had been two reasons to think that August’s labour market report would not deliver good news.

First, the intensification of restrictions in Victoria had been expected to push up unemployment in August after Melbourne had moved to stage four restrictions and regional Victoria stage three restrictions on 4 August. The August labour force survey ran over the two weeks from 2 August to 15 August, so although it picked up the early impact of these restrictions it did not capture the full month. And while the data did show employment falling and unemployment rising in Victoria in August, large employment gains in the other states more than offset this in terms of the national outcome.

Second, and as we’d noted just last week, the weekly payroll data had been painting a picture of a relatively soft labour market performance over the same period. So, while this week’s August labour force report has employment rising by 0.9 per cent, the earlier payroll numbers had shown jobs falling by 1.2 per cent over a similar period. The ABS explains this discrepancy in terms of a strong increase in the number of ‘Owner managers of an unincorporated enterprise’ in employment (this category captures, for example, a self-employed person operating a business as a sole trader).

The original ABS data show a 44,500 net increase in employment between July and August before seasonal adjustment, which was driven by an increase of 50,200 in the number of owner managers or self-employed people without employees, most of whom were working in an unincorporated enterprise. In contrast, there was only minimal growth in the number of employees (up just 2,600) and a 9,300 fall in the number of Contributing family workers. Importantly, payroll jobs include the jobs held by employees and owner managers of incorporated enterprises but do not include owner managers of unincorporated enterprises, the largest component of the employment growth in August. The payroll series also has relatively lower coverage of small businesses and therefore the increase in owner managers of incorporated enterprises without employees is also less likely to be reflected in the payroll jobs series. And to cap it all off, while changes in the number of employees and owner managers without employees were relatively similar between April and July, August saw a big divergence in the two series.

Coming after a fairly decent July report (which also delivered stronger employment growth, a lower unemployment rate and a higher participation rate than had been expected) this month’s numbers suggest that the labour market may be in better shape than the recent run of payroll data had been indicating. Granted, adjusting the headline numbers for the decline in the size of the labour force since March would push the unemployment rate up to around 8.2 per cent. But this would still be well down on the nine per cent equivalent unemployment rate in July, let along the 11.6 per cent rate that applied in May.

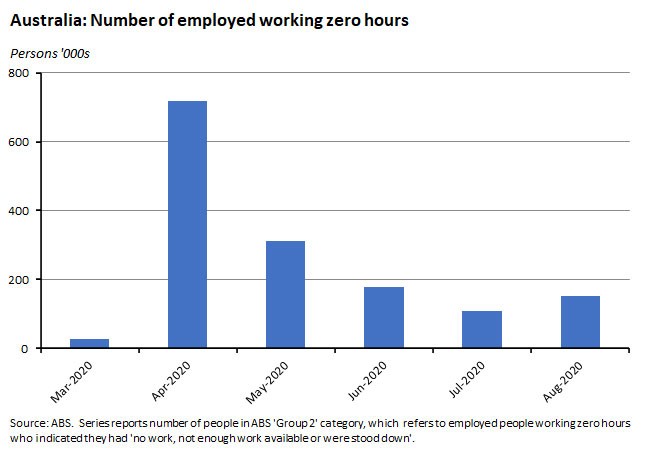

While it wasn’t enough to derail the August results, the impact of Victoria’s lockdown was still quite visible in the national data. For example, although national employment rose 0.9 per cent, hours worked only rose by 0.1 per cent, reflecting a 4.8 per cent decline in hours worked in Victoria that offset most of the 1.8 per cent increase across the rest of Australia. There was also an increase in the number of employed working zero hours in August, bringing to an end three consecutive months of falls. Again, while there were modest increases in several states, the big story here was in Victoria, where the both the number and share of people working zero hours for economic reasons almost doubled.

What happened:

The RBA published the minutes of the 1 September Board meeting, at which the central bank had announced that it would both increase the size of the Term Funding Facility (TFF) and make it available for longer than originally announced.

The RBA’s meeting was held before the release of the June quarter national accounts, but the Board’s assessment of economic conditions was consistent with the subsequent numbers. The minutes note that members agreed:

‘The Australian economy had been going through a very difficult period and was experiencing the biggest shock to economic activity since the 1930s. Nevertheless, members noted that the downturn had not been as severe as earlier expected and a recovery was under way in most of Australia. However, the recovery was likely to be uneven, with the COVID-19 outbreak in Victoria having a major effect on the economy. Uncertainty about the health situation and the future path of the economy was continuing to affect the spending plans of many households and businesses. Wage and price pressures remained subdued and this was likely to continue for some time.’

The minutes also record some discussion over the level of the Australian dollar:

‘The appreciation of the Australian dollar had been consistent with the increase in commodity prices, particularly iron ore prices, over recent months. While members noted that the Australian dollar was broadly aligned with its fundamental determinants, a lower exchange rate would provide more assistance to the Australian economy in its recovery.’

In terms of the change to the TFF, the minutes note:

‘Members reviewed the operation of the TFF, given the uncertain economic outlook and that the initial allowance of three per cent of credit had to be drawn down by the end of September 2020. They agreed that the TFF had worked as intended and that, given the economic outlook, an expansion of the TFF was appropriate. In particular, the Board agreed to increase the size of the TFF and allow drawing of funds up until June 2021. Under an expanded TFF, authorised deposit-taking institutions (ADIs) would have access to additional funding, equivalent to two per cent of their outstanding credit, at a fixed rate of 25 basis points for three years. ADIs would be able to draw on this extra funding until the end of June 2021. This extension would ensure that all ADIs continued to have access to the TFF after the end of September 2020. The availability of additional allowances associated with an ADI's growth of business credit would also be extended beyond the end of March 2021 to the end of June 2021. This further easing of monetary policy would bring the total amount available under this facility to around $200 billion. This would help keep interest rates low for borrowers and support the provision of credit by providing ADIs greater confidence about their continued access to low-cost funding.’

The Board also agreed ‘to maintain highly accommodative settings as long as required and to continue to consider how further monetary measures could support the recovery.’

Why it matters:

Back at the time of the September Board meeting, we noted that ‘after several monthly RBA meetings which have largely been non-events, this week’s meeting offered quite a bit more action, with the ramping up of the TFF and a message that more monetary easing may be in store.’ That was because not only did the 1 September meeting deliver that expansion and extension of the TFF, but the accompanying statement also noted that:

‘The Board will maintain highly accommodative settings as long as is required and continues to consider how further monetary measures could support the recovery.’

RBA watchers seized on the message that the central bank was considering further measures as an indication that more monetary easing lay ahead. But this week’s minutes shed no further light on the central bank’s thinking in terms of the mechanics of any possible future policy adjustment.

There was also little more on the changes to the TFF, other than a confirmation that the RBA considered this shift equivalent to a ‘further easing of monetary policy.’ (Readers will recall that the TFF was designed to offer a source of low-cost funding to the banking system by providing three-year funding at a fixed interest rate of 0.25 per cent. This was intended to meet two objectives: (1) to reinforce the impact of a lower cash rate by reducing bank funding costs and thereby helping to reduce interest rates for borrowers and (2) by linking part of the facilities’ funding allowance to growth in business lending, to encourage banks to expand their lending to businesses.)

What happened:

The ABS said that weighted average residential property prices across the eight capital cities fell 1.8 per cent in the June quarter, but were still up 6.2 per cent over the year.

In quarterly terms, the only capital city to see a rise in the residential price index in the June quarter was Canberra, where the index was up 0.8 per cent. The index fell in Sydney (-2.2 per cent), Melbourne (-2.3 per cent), Brisbane (-0.9 per cent), Perth (-0.7 per cent), Adelaide (-0.8 per cent), Darwin (-1.4 per cent), and Hobart (-0.4 per cent). In annual terms, the index rose in Melbourne (+8.8 per cent), Sydney (+8.1 per cent), Hobart (+6.1% per cent, Canberra (+3.6 per cent), Brisbane (+2.3 per cent) and Adelaide (+0.7 per cent), but fell in Darwin (-2.7 per cent) and Perth (-0.2 per cent).

Why it matters:

As we’ve noted in the past when reporting on the falls seen in the monthly CoreLogic series, the decline in house prices to date looks quite modest when set against the scale of the employment and output shocks triggered by COVID-19. That relative resilience reflects the support to the housing market provided by low interest rates, government fiscal spending, targeted support packages from federal and state governments and loan repayment holidays.

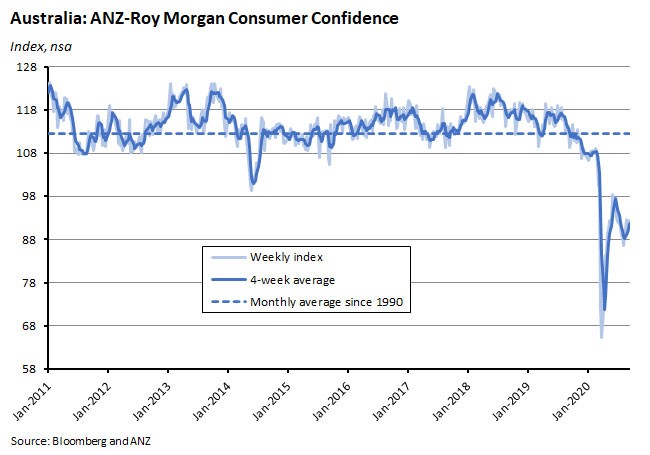

What happened:

The ANZ-Roy Morgan weekly index of consumer confidence rose 1.4 per cent to an index value of 92.4 on September 12/13.

Four out of five subindices rose over the week, with the exception being ‘future economic conditions’ (which had increased strongly last week). The largest rise was for ‘time to buy a major household item’ which was up 5.3 per cent, taking the subindex back above the neutral level of 100 for the first time since June this year. The ‘current finances’ subindex rose by 3.7 per cent while future finances were up a more modest 1.2 per cent and ‘current economic conditions’ was up just 0.5 per cent.

By capital city, confidence was down in Melbourne, dropping more than five per cent to a reading of just 85.8, following the announcement that stage 4 lockdown measures would be extended until the end of this month. Confidence was also down more than three per cent in Sydney, but was up strongly in Perth and Brisbane in a reminder of the diverging nature of economic conditions right now.

Why it matters:

This marked a second consecutive weekly rise and left two subindices (‘time to buy a major item’ and ‘future finances’) with readings above 100.

What I’ve been following in the global economy

What happened:

The Federal Open Market Committee (FOMC) of the United States Federal Reserve published the statement from its 15-16 September meeting. As expected, the Fed left the target range for the federal funds rate unchanged, with the statement recording that:

‘The Committee decided to keep the target range for the federal funds rate at 0 to 0.25 percent and expects it will be appropriate to maintain this target range until labour market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.’ [emphasis added].

The Statement also referred to the Fed’s new policy framework, noting that:

‘the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved.’

In addition, the Fed promised that ‘over coming months the Federal Reserve will increase its holdings of Treasury securities and agency mortgage-backed securities at least at the current pace to sustain smooth market functioning and help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses.’ (The ‘current pace’ consists of monthly purchases of US$120 billion of assets, comprising US$80 billion of Treasuries and US$40 billion of mortgage securities.

The FOMC also published updated economic projections. These showed that the central bank has become more optimistic about the near-term outlook for the US economy. Back in June, the median FOMC member projection was for fourth quarter GDP to decline at an annual rate of 6.5 per cent. The new forecast has a more modest decline of 3.7 per cent. Similarly, in June the unemployment rate in the fourth quarter was expected to average 9.3 per cent. The new forecast is for an average unemployment rate of 7.6 per cent. Forecasts for core personal consumption expenditure (PCE) inflation – the Fed’s preferred measure – have also edged up slightly. Even so, the median forecast still sees inflation below two per cent until 2023 and then at two per cent for that year.

Why it matters:

This was the first meeting since the Fed announced changes to its long-term policy framework (for more background, see the readings from a couple of weeks ago) and the last scheduled meeting before the 3 November presidential election. It therefore provided the first opportunity for the Fed to test drive its new monetary policy strategy with its increased focus on employment and accompanying greater tolerance for (a bit) more inflation and to provide financial markets with a greater sense of the how that would work in practice. The FOMC statement was consistent with that new framework, with the Committee saying it would target ‘inflation moderately above two percent for some time’ and pledging that there would be no increase in the Fed funds rate ‘until labour market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.’

In conjunction with updated forecasts showing that most FOMC members see no change in the Fed Funds rate through 2023, the message from this month’s meeting is consistent with the initial take on the Jackson Hole shift in strategy in indicating that markets should expect there to be no rate hikes from the Fed for at least the next couple of years. Beyond that, however, September’s statement did little more to flesh out the new strategy, with the Fed’s interpretation of ‘moderately above two per cent’ and ‘for some time’ still left to the discretion of the FOMC and to the market’s imagination.

What happened:

A range of economic indicators signal that global economic activity has rebounded from the deep slump experienced during the second quarter of this year. As a result, forecasters have become relatively more optimistic about the likely depth of the recession that will mark this year (see this week’s readings for the new OECD projections, for example). At the same time, however, the recovery to date has only been partial. And it may also be losing momentum.

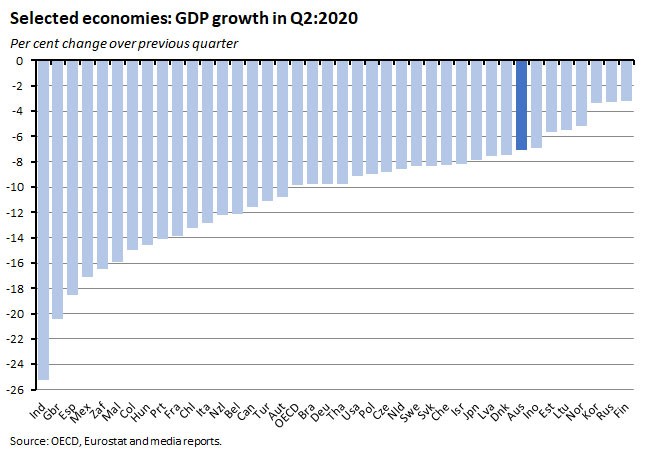

We’ve noted in several previous issues of the Weekly that Q2 GDP results across much of the world economy painted a picture of an extremely severe economic downturn triggered by the coronavirus crisis (CVC), with several major economies including India, the UK, Spain and Mexico suffering from brutal, double-digit quarterly falls in real GDP. This week, New Zealand joined the double-digit-decline club, reporting a record 12.2 per cent fall in quarterly GDP.

(China is an important exception to this story, reflecting in large part its status as the country that entered and exited the CVC first, which saw the Chinese economy enjoy a strong 11.5 per cent quarterly rise in real output in Q2 after a ten per cent drop in Q1.)

Of course, quarterly GDP results are very much a lagging indicator in terms of economic activity. They are useful in telling us about the scale of economic destruction wrought by COVID-19, but less helpful in describing current economic conditions. With lockdowns having been eased across much of the world economy from the middle of the year onwards, the expectation has been that the pattern of activity in the current third quarter will look quite different to that seen in its predecessor.

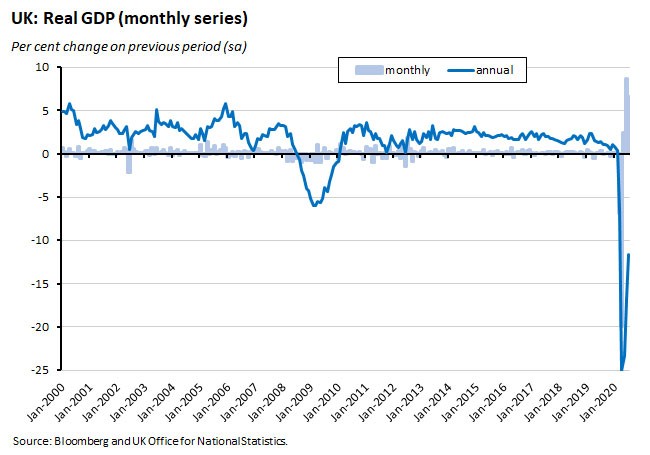

One alternative to waiting for the next quarterly GDP report to see if this expectation is fulfilled is offered by the fact that some countries now also produce monthly GDP estimates, providing a more current take on the economy. This group includes the United Kingdom, which suffered one of the world’s largest quarterly falls in output in Q2. Here, the latest ONS monthly data show that GDP grew by 6.6 per cent in July, following growth of 8.7 per cent in June and 2.4 per cent in May, coming back from a record fall of 20 per cent in April 2020. That’s consistent with the broad global narrative of an easing in lockdown conditions allowing for a recovery in economic activity. But although July 2020 GDP is now 18.6 per cent higher than its April 2020 low, it remains 11.7 per cent below the levels seen in February 2020 and the ONS estimates that the UK economy has still only recovered just over half of the lost output caused by COVID-19.

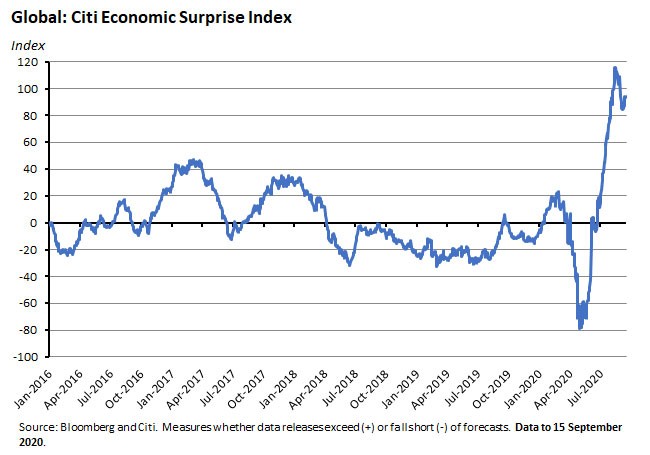

Another interesting piece of evidence on the shift in current global economic conditions is the Citi economic surprise index, which measures the extent to which actual economic outcomes exceed or fall short of forecasts. Not surprisingly, that index dropped sharply into negative territory during the early months of the pandemic, as economists were caught out by the size of the economic and market dislocation triggered by COVID-19. But the initial big decline in the index has since been followed by an even sharper move back into positive territory, with the global index hitting a record high last month, suggesting that just as the early part of the CVC surprised to the downside, so the recovery has surprised to the upside.

Of course, a more general point to note here is that these big swings in the index are also a powerful illustration of the fact that forecasting has been unusually challenging in recent months as the pandemic has scrambled economic relationships.

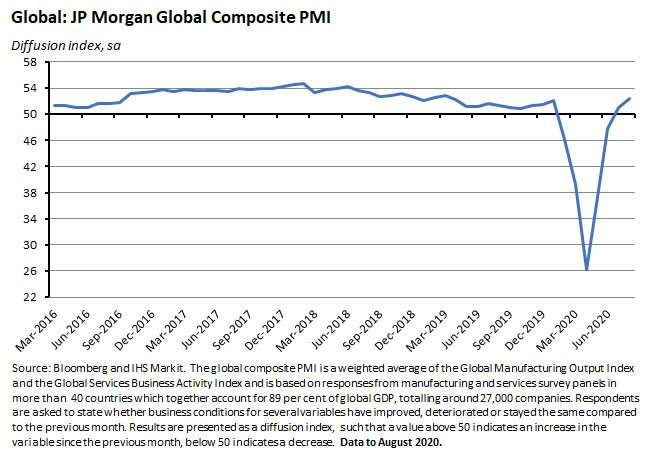

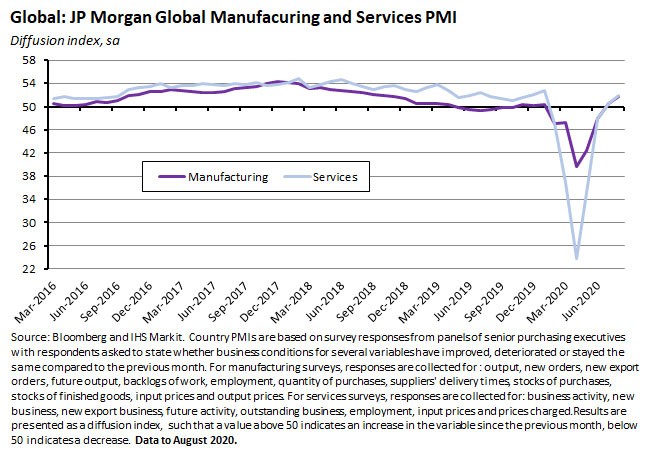

Another useful source of data on global economic conditions is provided by the pattern traced out by purchasing managers surveys, which offer a more contemporary read on business conditions than that delivered by typically lagging official numbers. The JPM global composite PMI hit a 17-month high in August after having also registered a positive outcome in July. Those two results follow a previous run of five consecutive months when the index was signalling falling output. Last month, five of the six sub-sectors covered by the series (financial services, business services, consumer goods producers, intermediate goods producers and investment goods producers) reported rising output, and all five also saw faster rates of expansion last month than in July. The exception to the story – consumer services – nevertheless saw the rate of decline ease to the lowest pace experienced during the seven-month downturn that began in February.

Both the manufacturing and services sector PMIs reported growth in August, with the former index hitting a 28-month high and the latter recording a seven-month high.

The strong message from August’s PMI readings was also echoed in Bloomberg’s global GDP tracker, which gave a reading of 5.3 per cent, down only slightly from July’s 5.4 per cent result. That reflects both the pickup in business survey readings and booming stock market outcomes.

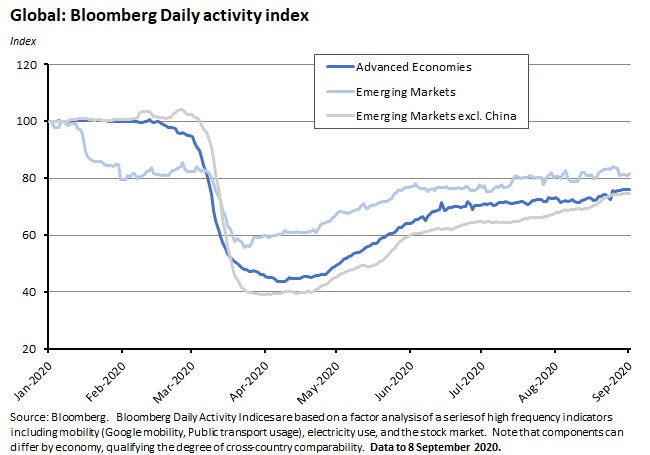

The demand for a quick read on rapidly changing economic conditions has also prompted an increased focus on so-called alternative data which often draw on relatively new series, including online and other digital sources. For example, Bloomberg Economics constructs Daily Economic Activity indices for a range of economies that incorporate Google and Moovit mobility data, electricity consumption, stock market indices and measures of retail footfall. These experimental series are subject to some limitations (they may overweight mobility indicators, the relative dearth of back data limits the ability to gauge statistical relationships with other data sets, and differences in data availability means that cross-country comparisons have to be qualified) but they still tell an interesting story.

In aggregate, these indicators suggest that activity in advanced economies overall is now running at around 24 per cent below pre-pandemic levels, with a similar result for emerging markets excluding China, where activity is about 25 per cent down. They also suggest that the pace of recovery in activity has slowed somewhat over the past couple of months relative to the previous surge.

Unsurprisingly, the aggregate numbers disguise some quite substantial variations across economies (subject to the caveat about cross-country comparisons noted above). For example, while they suggest that activity in China was running at about 90 per cent of pre-COVID levels as of early September and activity in Japan and Germany had recovered to more than 85 per cent, in the UK, United States and India, activity was still down around 30 per cent compared to before the pandemic.

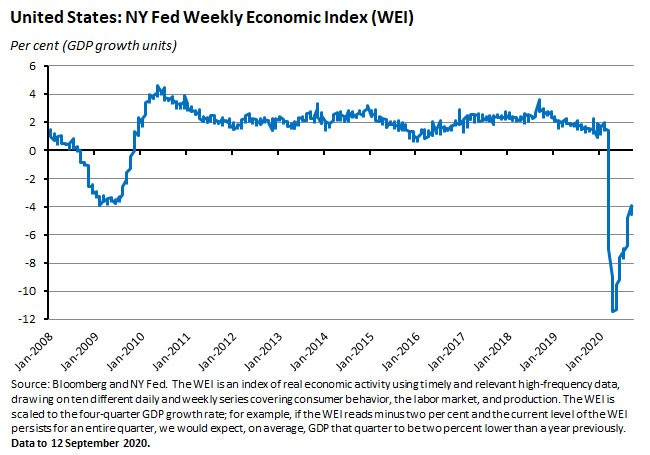

The official sector is also drawing on alternative economic indicators to produce its own estimates of economic activity. For example, in previous editions of the Weekly we’ve looked the New York Fed weekly economic index (WEI), which is an index of 10 indicators of real economic activity that are scaled to align with the four-quarter GDP growth rate: the WEI currently reads -4.6 per cent, so if that level of the WEI were to persist for an entire quarter, on average, GDP that quarter would be expected to be 4.6 per cent per cent lower than a year ago.

Why it matters:

In the months following the onset of the CVC, the initial pace of the global economic recovery from has been both relatively swift and relatively strong, with some of the data flow suggesting a ‘V’-shaped recovery took place from around late April until late June (with the exact timing differing across countries). But this initial phase of the recovery has still left output and activity well below pre-crisis levels and unemployment well above them, and activity indicators also suggest some slowdown in the pace of recovery from July onwards.

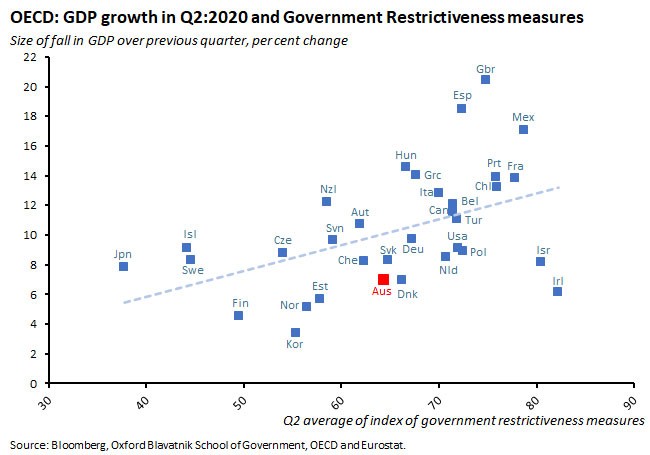

That broad economic trajectory maps on to what we know about the relationship between COVID-19 and its economic consequences, and in particular the combined impact of government-mandated restrictions and voluntary changes in behaviour on economic activity. So, for example, it’s no surprise that there’s a positive correlation between the stringency of government lockdown measures and the depth of the economic decline countries suffered in the second quarter of this year.

But clearly that’s not all that’s going on in the data. Some countries including the UK, Spain and Mexico appear to have suffered much larger falls in output than might have been expected given the degree of lockdown pursued by their policymakers, for example, while others – including Australia – appear to have suffered less.

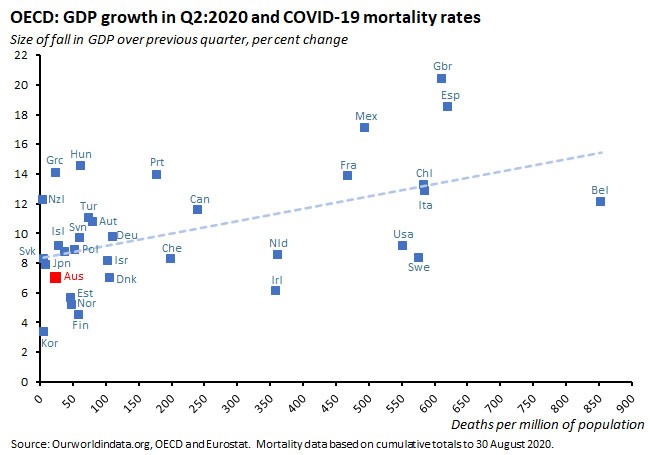

In part, that’s likely because consumer and business behaviour also reacted to the pandemic independently of government restrictions. A reasonable assumption to make here is that where the pandemic was more severe, so was the voluntary response (and - in many but not all cases - the official response, too). That relationship is reflected in a positive correlation between the size of the Q2 fall in GDP and deaths per million of the population.

Once again there are outliers, with the UK, Spain and Mexico looking like relatively poor performers. In terms of our OECD peers, Australia again looks pretty good, along with Norway, Finland, the Baltic States, Japan, Korea and Slovakia – all of which have managed to combine lower death rates with lower levels of economic damage.

These simple correlations are also found in more sophisticated studies. For example, this IMF working paper finds that containment measures are associated with large negative impacts on economic activity, with workplace closures and stay-at-home orders proving both more effective at curbing infections than other so-called non-pharmaceutical interventions but also associated with the largest economic costs. And this slightly earlier paper from the Fund finds that those European economies and US states that suffered larger COVID-19 outbreaks also suffered larger economic losses, with the deterioration in economic conditions preceding the introduction of government lockdowns.

The relative economic magnitudes of the economic consequences of voluntary and government-mandated policies is still the subject of conflicting evidence. For example, this study looking at US states uses cellular phone records data on customer visits to more than 2.25 million individual businesses across 110 different industries. It estimates that formal, legal shutdown orders accounted for only a modest share of the decline of economic activity: while overall consumer traffic fell by 60 percentage points, legal restrictions explain only seven points of that decline. Similarly, this paper finds that patterns of consumer spending and employment across different US states do not seem to be greatly affected by differences in the timing of lockdowns and re-openings. On the other hand, this paper, which is also based on US data, finds a much larger effect for policy interventions, estimating that the employment rate fell by about 1.7 percentage points for every extra ten days that a state experienced a stay-at-home mandate during the period 12 March to 12April, 2020.

Of course, a range of other factors are likely to help explain the different economic results across countries, including the relative economic importance of tourism and other services involving a high level of personal interaction and the nature, scale and duration of fiscal and monetary support.

Still, even the simplest story based on the interaction between voluntary and government mandated shifts in behaviour on the one hand and the level of economic dislocation on the other is consistent with the pattern of recovery seen to date. As COVID-19 case numbers fell and government restrictions were eased earlier this year, we would have expected to see a bounce back in economic activity, and that’s largely what happened. Then, as case numbers ticked back up again, and as governments considered – and in some cases implemented – new public health measures, then we’d expect to see that recovery start to run into some headwinds. And again, that’s pretty much what’s happened to date.

One again, that’s only going to be part of the story. As already noted, another important factor supporting economic activity has been the huge level of fiscal and monetary support that has been deployed. To the extent that some of that support is wound back, that will have consequences for the pace of activity and the shape of the recovery. Further, there are the longer-term consequences of the pandemic, including shifts in behaviour (we have evidence that crises are associated with sustained changes in savings rates and other precautionary behaviour, for example), labour market scarring effects, and structural change as economies adapt to new patterns of demand and ways of doing business. All of which suggest that, despite some significant positive surprises in the early pace of the recovery from the CVC, the risk remains that the adjustment process will still be longer and more painful than the initial V-shaped recovery might suggest.

What I’ve been reading

The ABS published a new essay – a series of unprecedented events – providing an overview of an historic June quarter which saw a range of statistical records topple as COVID-19 took a dramatic toll on the Australian economy.

I haven’t had a chance to dig into the content yet, but as always, the latest RBA Bulletin offers plenty of interesting-looking reading. I’ll probably start with the pieces on the economic effects of low interest rates and quantitative easing, the functioning of the government bond market during COVID-19 and the impact of recessions on the labour market, but there are several other articles that also caught my eye.

Also from the RBA, its latest (2019) Consumer Payments Survey finds that Australians increasingly prefer to use electronic payment methods rather than cash for their day-to-day payments, with debit cards now the most frequently used consumer payment method. Despite the growing use of innovative new payment services, however, a ‘material share’ of the population continues to make many of its payments in cash.

A new report from CSIRO examines science and technology growth opportunities that can help restore economic growth after the pandemic.

The ANU’s China database tracker estimates that Chinese investment in Australia fell from $4.8 billion in 2018 to $2.5 billion in 2019.

Related, the Guardian has an essay on Australia-China tensions while this Bloomberg piece suggests that Australia’s iron ore exports to China offer Canberra a nuclear option in terms of the bilateral relationship.

The Australian Council of Social Service (ACOSS) released a new report on JobSeeker it commissioned from Deloitte Access Economics. The report estimates that if Canberra cuts the Coronavirus Supplement on September 25 and then fully removes the Supplement at the end of December, this will reduce government spending on average by over $23 billion across 2020-21 and 2021-22. That in turn would reduce the size of the economy by $31.3 billion and generate an average loss of 145,000 Full-Time Equivalent jobs across 2020-21 and 2021-22. (Note, however, that the Prime Minister has already said that he ‘would be very surprised’ if there was no extension to the Supplement beyond Christmas.)

ABARES’ latest Agricultural Outlook has been published. The report reckons that the agricultural sector is on track for a recovery in output following years of drought-affected seasons, with grain production forecast to rebound in 2020–21 to the highest level since the record harvest of 2016–17. But while volumes are forecast to rise strongly, the gross value of production is projected to remain unchanged at $61 billion in 2020–21 due to falling prices. And a combination of falling commodity prices, reduced livestock exports and grain stock rebuilding is expected to result in a 10 per cent fall in the value of agricultural exports to $43.5 billion in 2020–21. In terms of the impact of COVID-19, ABARES notes that ‘demand for most agricultural products has fallen as a result of the continuing pandemic, although not to the same degree as discretionary goods and services.’

This is an older piece (it’s from July this year) but worth a read. Steve Grenville provides a primer on MMT and its relationship with mainstream economics from the perspective of a former RBA deputy governor. (See also the link to the Economist piece on government borrowing below.)

Related, a nice piece (with a neat chart) from Bloomberg on ‘the year unconventional monetary policy turned conventional.’

And Howard Davies on how monetary policy history appeared to end in the 1990s but has now resumed with a vengeance.

The OECD published its interim Economic Outlook. It now thinks that world output will fall 4.5 per cent this year, before growing by five per cent in 2021. That reflects a 1.5 percentage point upgrade to the projections in its June Economic Outlook, with large positive revisions for China (up 4.4 percentage points to growth of 1.8 per cent), the United States (up 3.5 percentage points to a contraction of 3.8 per cent), France (up 1.9 percentage points to a contraction of 9.5 per cent), the UK (up 1.4 percentage points to a contraction of 10.1 per cent) and Germany (up 1.2 percentage points to a contraction of 5.4 per cent). On the other hand, there were sizeable forecast downgrades for Argentina, India, Mexico and South Africa. In the case of Australia, the OECD now expects the economy to shrink 4.1 per cent this year (an upgrade of 0.9 percentage points relative to its June forecast) before growing by 2.5 per cent in 2021. That last change represents a substantial downgrade of 1.6 percentage points relative to its previous forecast.

According to the Asian Development Bank (ADB)’s latest economic update, developing Asia is expected to contract by 0.7 per cent this year, marking the region’s first annual decline in real GDP since the early 1960s. The downturn is projected to be broad-based with three-quarters of the region's economies forecast to shrink this year, including a nine per cent slump in India, an eight per cent fall in Thailand, a 7.3 per cent fall in the Philippines, and declines of more than six per cent in Singapore and Hong Kong (although China remains an important exception with the economy seen growing 1.8 per cent this year). Next year, developing Asia is forecast to grow by 6.8 per cent, but the ADB points out that this will still leave 2021 GDP substantially below pre-COVID-19 expectations and the development bank judges that the regional recovery ‘will be L-shaped or “swoosh-shaped” rather than V-shaped.’

Brad DeLong recommends five books on the Classical Economists. Also from DeLong, a short (just a bit more than ten minutes) lecture on growth, globalisation and political economy in the North Atlantic Economy between 1870 and 1914.

A VoxEU column on China’s mask diplomacy highlights the important role played by economic and/or political relationships with China’s provinces. Two from the Economist Magazine: The latest in the series on rethinking economic ideas covers the shifting consensus on government spending and borrowing. And an Economist Briefing on the future of the office.

The most recent BIS quarterly review is now available.

The macro musings podcast interviewed the FT’s Robin Harding on Abenomics and the ‘Japanification’ of monetary policy. Related, see this Harding article on six lessons for the rest of the world from Abenomics: (1) monetary policy works; (2) weak economies can’t handle tax hikes; (3) policy credibility is critical; (4) shifting inflation expectations alone is not enough; (5) stimulus doesn’t create public debt problems, it solves them; and (6) growth ‘strategies’ and modest reforms have only a limited impact on growth outcomes.

Latest news

Already a member?

Login to view this content