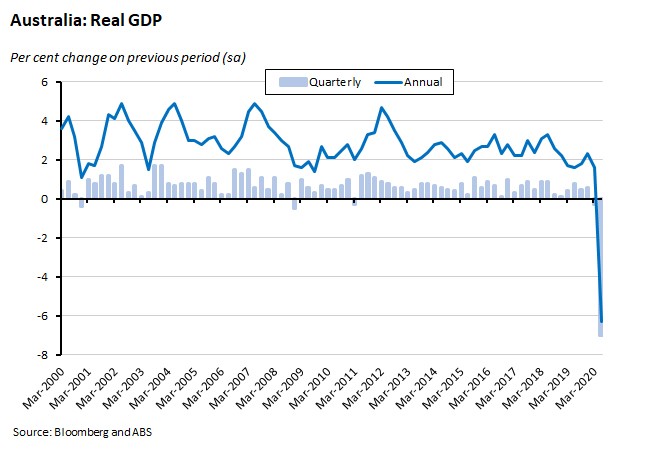

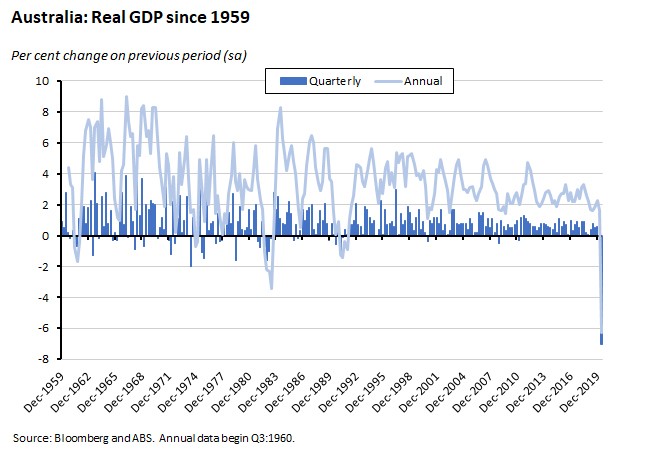

Real GDP dropped by seven per cent in the June quarter in the steepest fall since quarterly records began, bringing Australia’s golden run of 28 years of uninterrupted growth to a brutal end.

The RBA left its targets for the cash rate and the yield on three-year government debt unchanged at its September meeting, but boosted its Term Funding Facility and indicated that more monetary easing could be on the way. Australia reported a record current account surplus in Q2:2020. Dwelling approvals rose in July, but home values suffered a fourth consecutive monthly decline in August. The weekly index of consumer confidence fell. And July saw Australia record a 31st consecutive monthly trade surplus.

This week’s readings include a new ABS survey on the impact of COVID-19 on Australian households, new research on inequality in Australia, a range of views on the US Fed’s new monetary policy strategy, WFH, COVID-19 and commuting, and a piece on the tyranny of chairs.

Stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

Real GDP fell by seven per cent in the June quarter to be down 6.3 per cent over the year, according to the ABS.

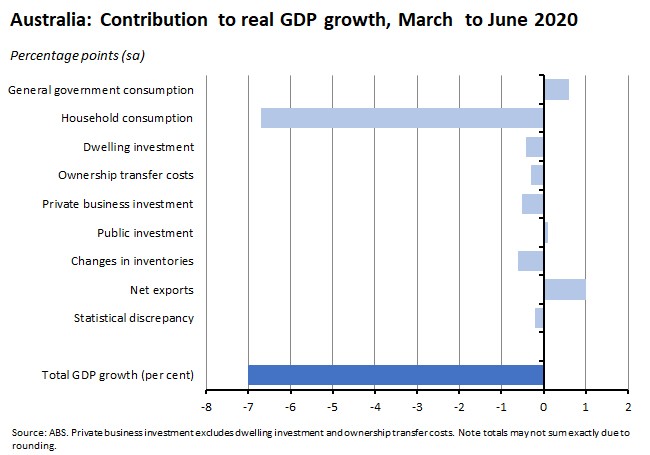

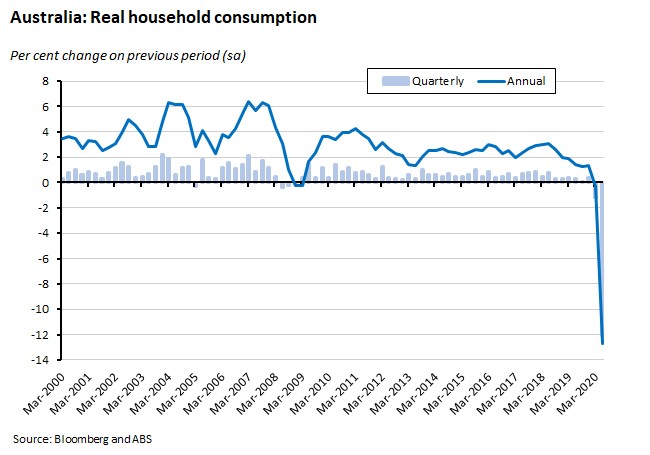

Strip out population growth, and in per capita terms real GDP shrank 7.2 per cent over the quarter and 7.4 per cent over year. The overwhelming driver of the fall in economic growth was a precipitous decline in household consumption, which fell by a record 12.1 per cent over the quarter, subtracting 6.7 percentage points from the growth rate. Other headwinds included the housing sector and private investment, with private demand overall staging a sharp fall. Only the public sector and net exports made a positive contribution to overall activity in Q2.

That 12.1 per cent plunge in household consumption over the quarter saw annual consumer spending fall 12.7 per cent, while consumption was down 2.6 per cent over 2019-20 as a whole – marking the first yearly fall recorded in the national accounts.

That 12.1 per cent plunge in household consumption over the quarter saw annual consumer spending fall 12.7 per cent, while consumption was down 2.6 per cent over 2019-20 as a whole – marking the first yearly fall recorded in the national accounts.

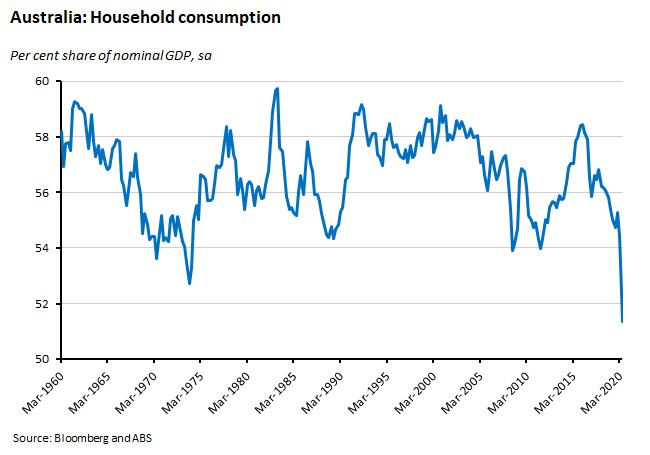

As a result, as a share of nominal GDP, consumption dropped to below 52 per cent.

Spending on services collapsed by 17.6 per cent in the June quarter as spending on transport services slumped 88.2 per cent in quarterly terms, on accommodation services 77.5 per cent and on catering services 55.7 per cent, while spending on recreational and cultural services declined 54.5 per cent. In contrast, spending on goods was down a relatively more modest 2.8 per cent with some categories (household tools and appliances, audio-visual and exercise equipment and alcoholic beverages) up quite sharply.

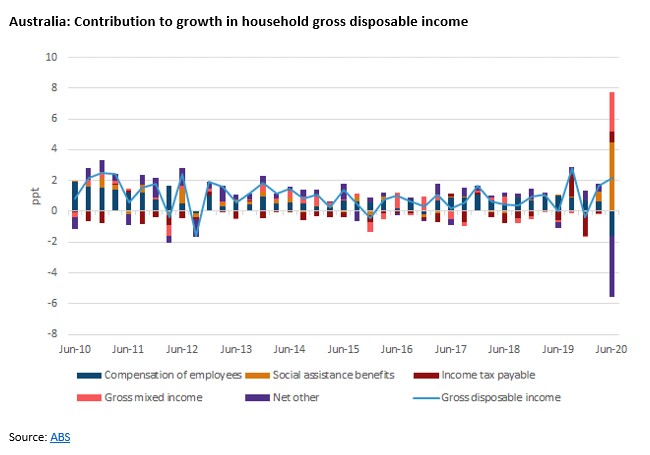

The big drop in consumption spending came despite a 2.2 per cent rise in household gross disposable income. The growth in income was driven by a rise in non-labour income, consisting of investment income, earnings from unincorporated businesses and social assistance benefits. Earnings from unincorporated businesses (measured as mixed income in the chart below) rose 21.9 per cent as businesses received government support from the JobKeeper and the Boosting Cash Flow for Employers programs, while social assistance benefits increased by a record 41.6 per cent thanks to an increase in the number of benefit recipients and additional COVID-19 related support payments including the coronavirus supplement (an additional $550 payment) and the initial Economic support payment (a one off $750 payment).

All up, the ABS estimates that government support boosted household gross disposable income by about $48 billion this quarter or around 17 per cent. On the other hand, labour income, measured as household compensation of employees, fell by a record 2.2 per cent over the quarter, reflecting big falls in employment and (another record) 9.8 per cent decline in hours worked.

Source: ABS

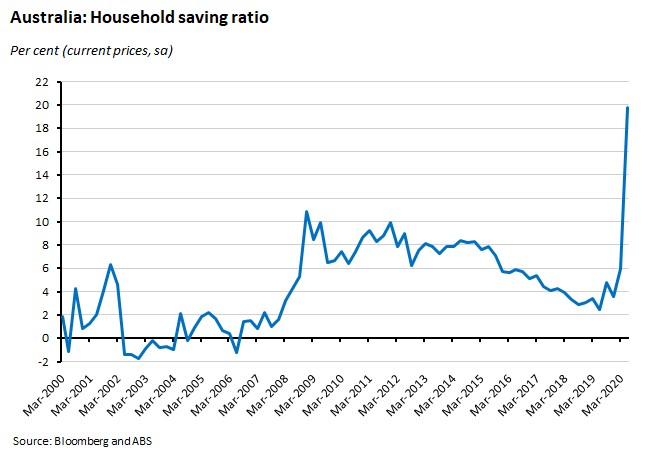

The combination of an increase in household income and a collapse in consumption spending meant that the household saving ratio jumped from six per cent in the March quarter to 19.8 per cent in the June quarter, its highest rate since June 1974. With net savings up $42 billion, that implies that a significant share of the increase in assistance to households was saved. Excluding COVID-19 related government support payments, the household saving ratio would have been 4.6 per cent, assuming unchanged household consumption behaviour. On the other hand, including other support initiatives that don’t show up in the national accounts calculation of household income, such as early access to superannuation and loan and rent deferrals (which the ABS puts at $19.6 billion), would have increased the household saving ratio to 24.8 per cent.

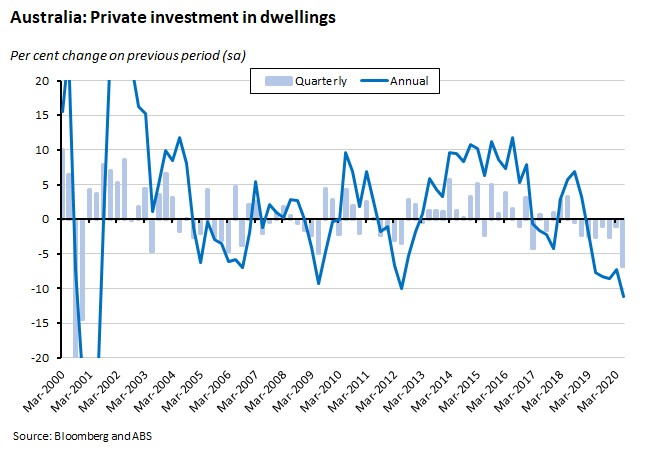

In terms of the other components of private demand, private investment declined 6.5 per cent over the quarter. Part of the story here was the downturn in the housing sector, with dwelling investment falling 6.8 per cent (down 11.2 per cent in annual terms) while ownership transfer costs dropped 18.5 per cent (4.2 per cent in annual terms).

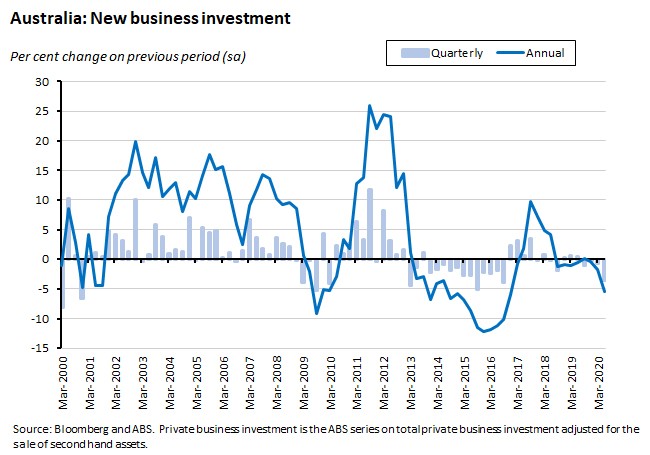

Private business investment fell 4.8 per cent over the quarter and was down 7.6 per cent over the year, while new business investment was down 5.5 per cent in quarterly terms and 3.5 per cent in annual terms. Non-mining investment dropped 6.9 per cent in quarterly terms but this was partially offset by a 1.3 per cent quarterly rise in non-mining investment.

All up, private demand fell 10.8 per cent over the quarter, subtracting 7.9 percentage points from GDP growth in the June quarter.

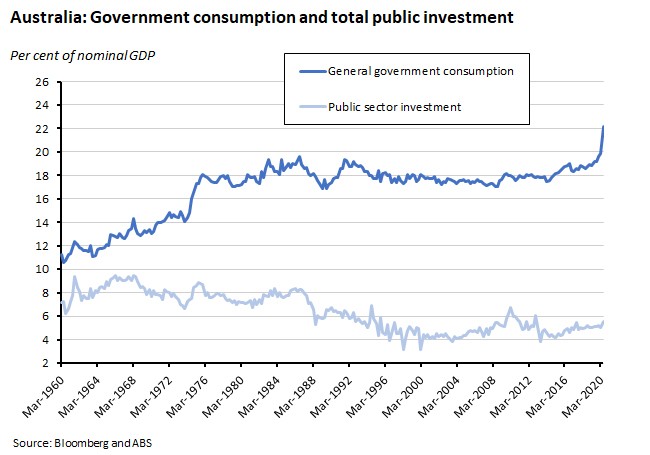

Public demand partially offset the collapse in the private sector, growing 2.5 per cent over the quarter and contributing 0.6 percentage points, as government increased spending in response to COVID-19.

Government consumption expenditure rose 2.9 per cent relative to the March quarter, driven by a 4.2 per cent rise in state and local expenditure, a six per cent rise in national defence expenditure and a 0.1 per cent rise in national non-defence expenditure. Public investment increased by one per cent, driven by a 7.5 per cent rise in state and local government capital spending.

Net exports also made a positive contribution to the overall growth outcome this quarter, as the decline in imports exceeded the decline in exports. Exports of goods and services fell 6.7 per cent over the quarter, while imports of goods and services were down 12.9 per cent (see the story below on the Q2:2020 current account for more detail).

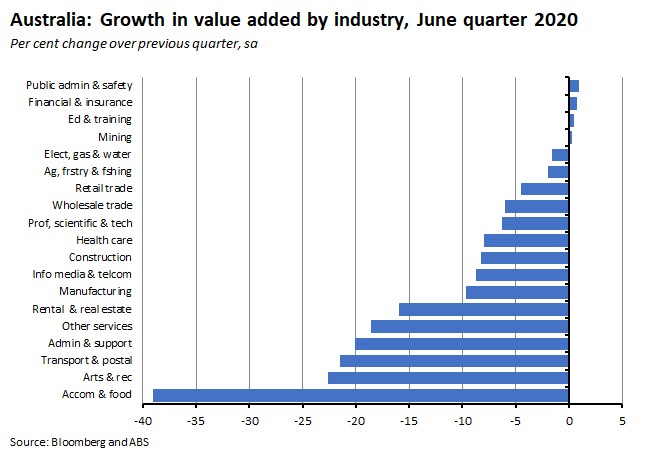

Turning from the expenditure to the production view of the national accounts, gross value added fell 6.5 per cent over Q2 with falls in 15 of the 19 industry categories, including record declines in accommodation and food and arts and recreation services. Gross value added fell 39 per cent in Accommodation and Food Services, 22.6 per cent in Arts and Recreation Services, 21.5 per cent in Transport, Postal and Warehousing, 18.5 per cent in 0ther Services, 15.9 per cent in Rental, Hiring and Real Estate Services, 9.6 per cent in manufacturing and 8.2 per cent in construction.

The extraordinary nature of the results was also apparent in terms of developments in national income. Compensation of employees or COE which is equal to the sum of wages and salaries and employers social contributions fell by a record 2.5 per cent over the quarter (although average compensation per employee actually rose 3.1 per cent, reflecting the concentration of job losses in part-time and lower paid work). On the other hand, profits (the gross operating surplus of private non-financial corporations) jumped 14.9 per cent and gross mixed income increased by 21.9 per cent.

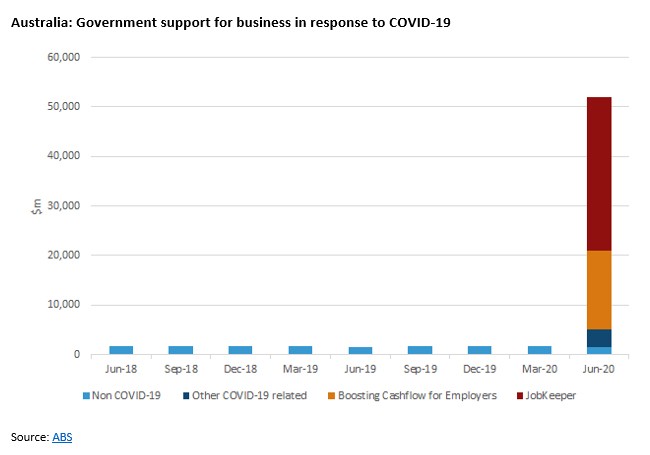

The big increase in company profits was another artefact of government policy, with the increases concentrated in the construction, retail, and professional, scientific and technical services industries and reflecting a large rise in government subsidies. The ABS notes that subsidies on production rose to record levels in the June quarter, reaching $52 billion, of which JobKeeper payments accounted for $31 billion and Boosting Cash Flow for Employers a further $16 billion – the largest and second largest subsidies ever recorded in the national accounts.

Source: ABS

The growth in profits combined with the fall in COE saw the share of COE in total factor income fall below 50 per cent for the first time since the September quarter of 1959 while the share of profits rose to a record high.

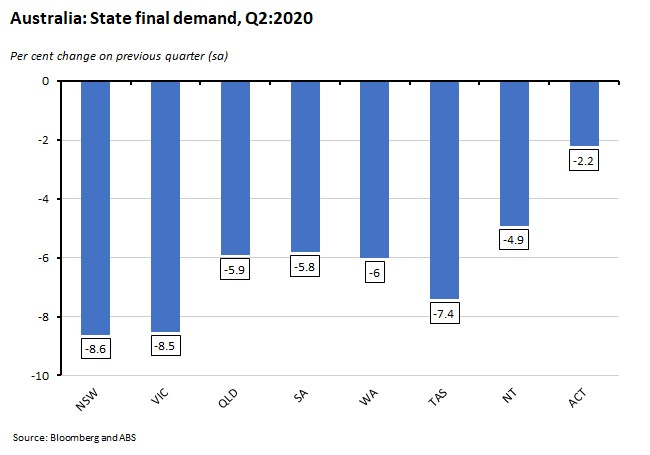

Finally, every state and territory suffered a sharp quarterly decline in final demand over the June quarter. The biggest declines were in New South Wales (down 8.6 per cent) and Victoria (down 8.5 per cent) while the smallest was in the ACT (down 2.2 per cent).

Why it matters:

June 2020 was a quarter for breaking national accounts records.

The quarter on quarter decline in real GDP in June was – by far – the deepest since quarterly records began back in 1959 (until now, the biggest fall had a been a two per cent decline in Q2:1974). It was also the steepest annual decline over the same period.

Other notable feature of the June quarter results included:

- A record quarterly decline in household consumption.

- The first annual decline in household consumption on record in 2019/20.

- A record fall in household spending on services.

- Record falls in gross value added in hospitality- and tourism-related industries and in health care services.

- The highest household savings rate since 1974.

- An historic 41.6 per cent rise in social assistance benefits.

- A record 2.5 per cent decline in compensation of employees.

- A record 9.8 per cent fall in hours worked.

- A record level of government support payments to business ($55.5 billion), with JobKeeper payments this quarter exceeding the cumulative amount of all previous employment subsidies.

- A record high for the profit share in total factor income.

- The wage share of total factor income fell to its lowest level since 1959.

The slump in activity was worse than market expectations (the median forecasts were for a six per cent drop quarter-on-quarter and a 5.1 per cent fall year-on-year). And after delivering a second consecutive quarter of negative growth, this result brought Australia’s record 28-year long economic expansion to a particularly brutal end.

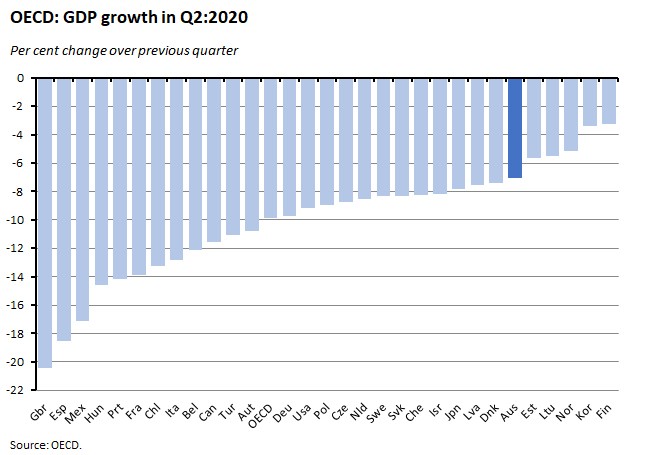

All that said, by the standards of our peers, Australia’s performance was fairly decent: only a handful of OECD member economies managed a smaller fall in output in the June quarter while several suffered a contraction that was more than twice as deep as our downturn.

Finally, the detail in this quarter’s national accounts confirms that what was already a record contraction in Q2 would have been much worse without the substantial level of government support that was deployed across the economy. While important elements of that support have since been extended, albeit in a modified form, it seems clear that the government will have to use the upcoming 6 October budget to introduce further measures to sustain economic activity.

What happened:

The RBA left its targets for the cash rate and the yield on three-year Australian Government bonds unchanged at 0.25 per cent at its meeting on 1 September. But the central bank did announce that it would increase the size of its Term Funding Facility (TFF) to around $200 billion while also extending the life of the facility until the end of June 2021. (In its original 19 March policy package, the RBA said that the TFF would provide access to ‘at least’ $90 billion and would run until end March 2021.)

The RBA’s assessment of economic conditions as reported in the governor’s statement was little changed:

‘In Australia, the economy is going through a very difficult period and is experiencing the biggest contraction since the 1930s. As difficult as this is, the downturn is not as severe as earlier expected and a recovery is now under way in most of Australia. This recovery is, however, likely to be both uneven and bumpy, with the coronavirus outbreak in Victoria having a major effect on the Victorian economy.’

And the statement concluded by noting that the RBA would not only continue to support the economy by maintaining its current policy settings but would also consider the scope for possible other measures in the future:

‘The Board is committed to do what it can to support jobs, incomes and businesses in Australia…The Board will maintain highly accommodative settings as long as is required and continues to consider how further monetary measures could support the recovery. It will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band.

Why it matters:

After several monthly RBA meetings which have largely been non-events, this week’s meeting offered quite a bit more action, with the ramping up of the TFF and a message that more monetary easing may be in store.

The TFF was designed to offer a source of low-cost funding to the banking system by providing three-year funding at a fixed interest rate of 0.25 per cent. The RBA originally set the TFF two objectives: (1) to reinforce the impact of a lower cash rate by reducing bank funding costs and thereby helping to reduce interest rates for borrowers and (2) by linking part of the facilities’ funding allowance to growth in business lending, it was also intended to encourage banks expand their lending to businesses, with particular incentives to encourage lending to small and medium-sized enterprises (SMEs). According to the governor, banks have to date drawn $52 billion under the TFF and ‘further drawings are expected over coming weeks’.

This week’s changes extend the lifetime of the program and its scale, with the RBA noting that they ‘build on the existing facility by providing access to more low-cost funding for all ADIs [authorised deposit-taking institutions] and over a longer period than originally specified. In particular, the changes provide ongoing access to the TFF after the $84 billion initial allowance of the TFF expires on 30 September 2020. All other parameters of the TFF remain unchanged.’

Along with the changes to the TFF, the other feature of this week’s meeting to draw widespread attention was the line in the final paragraph of the statement cited above, the one saying that: ‘The Board will maintain highly accommodative settings as long as is required and continues to consider how further monetary measures could support the recovery’ [emphasis added].

RBA watchers have seized on the message that the central bank is considering further measures as an indication that more monetary easing lies ahead. As discussed in previous notes, the RBA has repeatedly signalled its dislike of a range of non-conventional policy options including negative interest rates, monetary financing and (for the moment at least) intervention in the FX market. That would appear to leave the possibility of a minor adjustment to the cash rate (from 25bp to 10bp, which seems unlikely to do much beyond acting as a signalling device) or more bond purchases as part of a quantitative easing (QE) program to supplement or extend the RBA’s existing yield curve control (YCC) policy.

What happened:

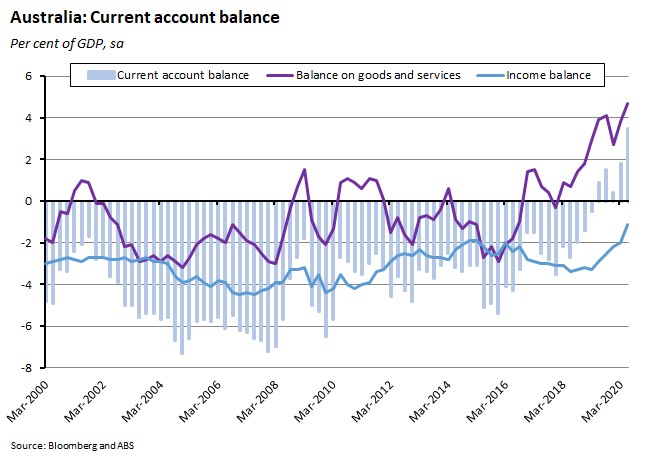

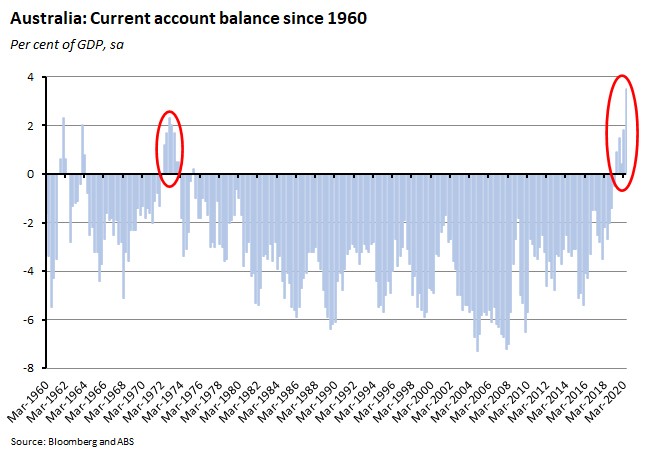

The ABS reported that Australia ran a record current account surplus of $17.7 billion (seasonally adjusted) in the June quarter of this year, equivalent to about 3.5 per cent of GDP. The surplus on the goods and services trade balance rose to $23.9 billion (around 4.7 per cent of GDP) while the deficit on the income balance fell to $5.6 billion (about 1.1 per cent of GDP).

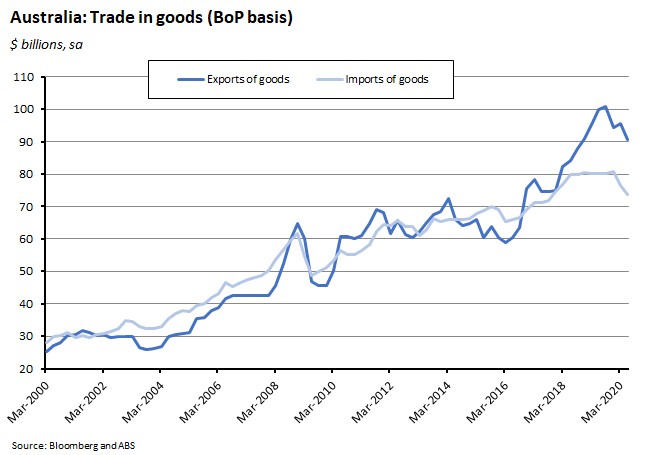

On the goods account, the seasonally adjusted balance was a surplus of almost $17 billion, which was down about $2.3 billion on the March quarter 2020 surplus. Export values fell five per cent over the quarter with volumes down three per cent and prices down two per cent, while imports of goods four per cent in dollar terms, with volumes down two per cent and prices down one per cent.

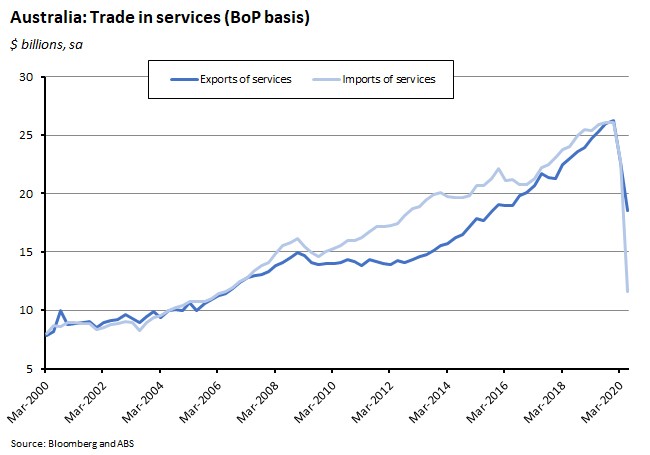

The fall in the size of surplus on the goods account was more than offset by a dramatic turnaround in the services account, which swung from a marginal deficit of less than $0.1 billion in the March quarter to a surplus of $6.9 billion in the June quarter. The value of services exports slumped 18 per cent, with exports of transport services dropping 44 per cent and exports of tourism-related services falling 28 per cent. But that decline was outpaced by a collapse in the value of services imports, which plunged 49 per cent, with transport services imports falling 25 per cent and imports of tourism-related services plunging 99 per cent.

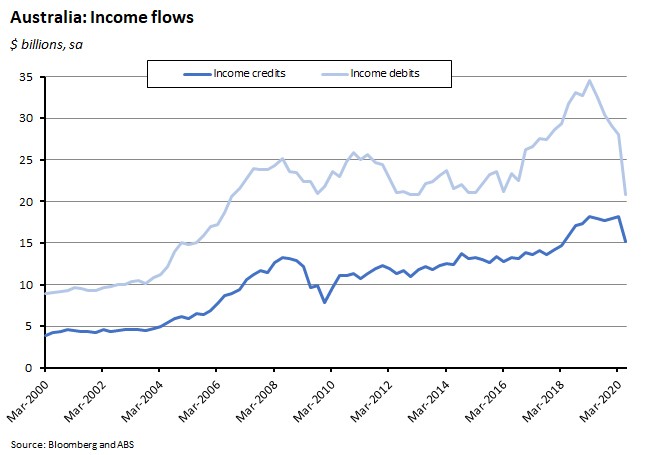

The deficit on the primary income account also shrank in the June quarter, falling by more than $4 billion as a decline in investment income credits was more than offset by a much steeper drop in investment income debits. (The net income balance mainly captures the difference between income paid by Australian entities to non-resident investors such as interest paid by Australian banks on foreign borrowings or dividends paid by Australian companies to overseas investors and the income received by Australian entities on their overseas investments such as the dividends earned by Australian superannuation funds on their holdings of foreign shares.)

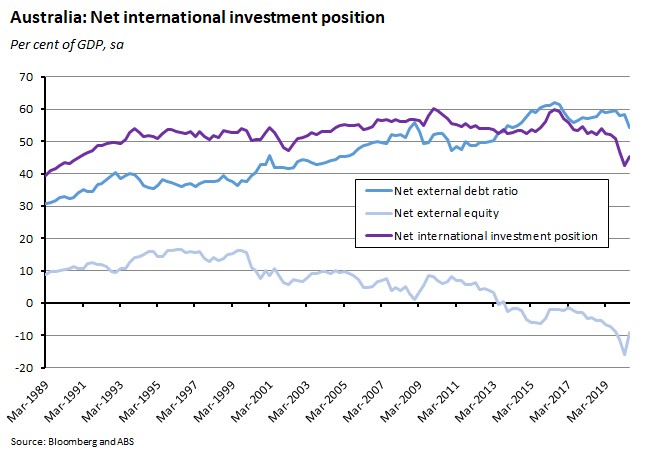

Australia's net international investment position (IIP) was a liability of $910.6 billion as of 30 June 2020, or about 45.3 per cent of GDP. Our net foreign debt liability was equivalent to about 54.4 per cent of GDP while our net foreign equity asset position was about 9.1 per cent of GDP.

For 2019-20, the current account recorded a surplus of $35.8 billion, a dramatic turnaround of $49.9 billion on the current account deficit of $14.1 billion recorded in 2018-19. The balance on goods and services was a surplus of $77.4 billion, up $28.3 billion on the 2018-19 surplus, with exports of goods and services one per cent higher while imports of goods and services fell five per cent. The 2019-20 primary income deficit fell $22.1b, with the 18 per cent fall in primary income debits comfortably outpacing a two per cent fall in primary income credits. There was modest increase in the second income deficit.

Why it matters:

The June quarter current account surplus was Australia’s fifth consecutive quarterly surplus and represented a new record. It was also significantly larger than market expectations, with the actual outcome of $17.7 billion comfortably beating the consensus forecast of a $13 billion surplus.

The key drivers of Q2’s record result were an increase in the goods and services trade balance and fall in the primary income deficit. As described above, the former was mostly a story of weaker imports, with the plunge in tourism service imports much larger than the (still sizable) fall in exports of tourism and education services. Imports of consumption goods were also down sharply, with a four per cent decline in value over the quarter led by a 45 per cent plunge in imports of non-industrial transport equipment. The latter reflects the fact that falls in payments made on Australian foreign liabilities have outpaced the decline in payments received from our foreign assets.

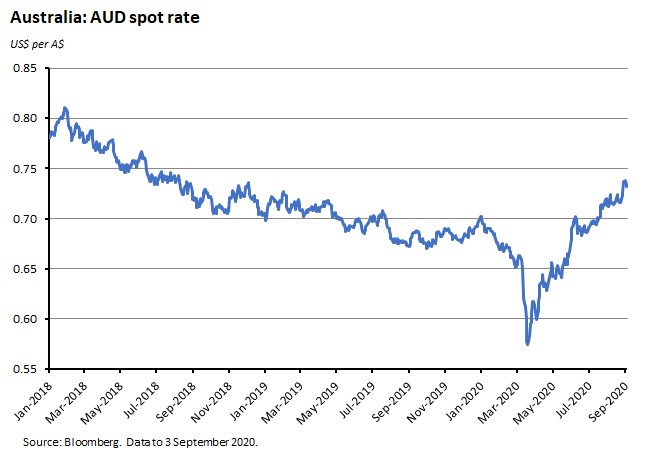

These large current account surpluses are one factor supporting the value of the Australian dollar (others include including relative monetary policy settings, trends in the US dollar, and the iron ore price).

What happened:

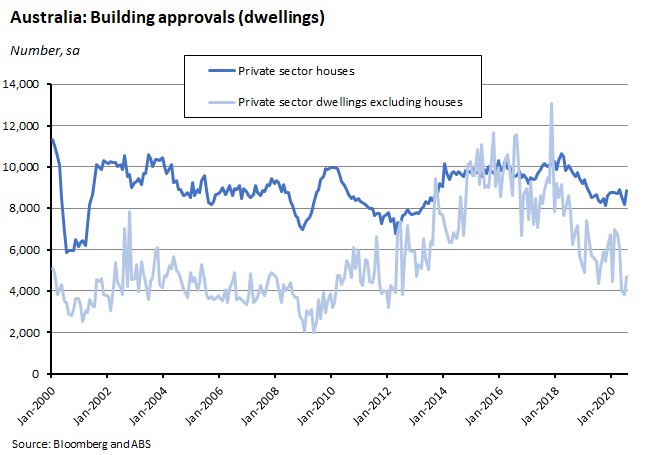

The ABS said that the number total dwellings approved rose 12 per cent in July (seasonally adjusted) to be up 6.3 per cent over the year. Approvals for private sector houses rose 8.5 per cent over the month and 5.6 per cent in annual terms while approvals for private sector dwellings excluding houses rose 22.7 per cent month-on-month and 7.5 per cent over the year.

Across the states, dwelling approvals rose over the month in Tasmania (50 per cent), New South Wales (32 per cent), Victoria (9.3 per cent) and Queensland (7.7 per cent). South Australia (10.5 per cent) and Western Australia (8.3 per cent) both recorded decreases in seasonally adjusted terms.

The value of total building approved fell 3.9 per cent in July, reflecting a 19.8 per cent drop in the value of non-residential building (which hit its lowest level since January 2018). The value of residential building rose 9.5 per cent in July.

Why it matters:

The sharp rise in approvals numbers for private sector dwellings excluding houses marked a significant bounce back after approvals had fallen to an eight-year low in June, while the rise in approvals for private sector housing was the strongest recorded monthly increase since January 2014. The ABS said that the increases in both sets of approvals in July ‘likely reflect improved consumer sentiment in May, on the back of falling COVID-19 cases and easing of restrictions.’ If that’s right, the subsequence weakening in consumer confidence from late June is likely to translate into softer numbers over the months ahead.

What happened:

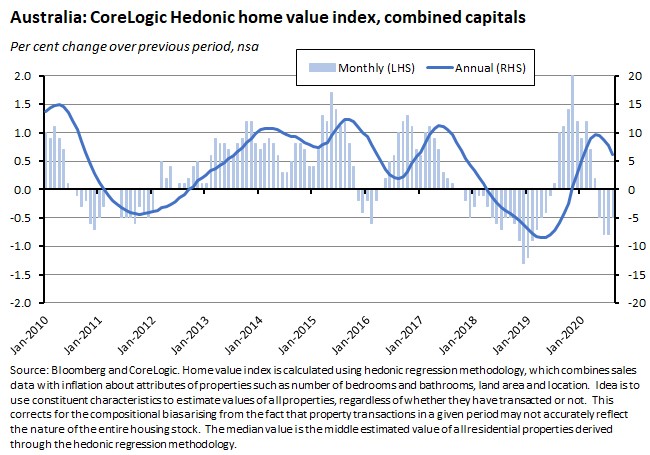

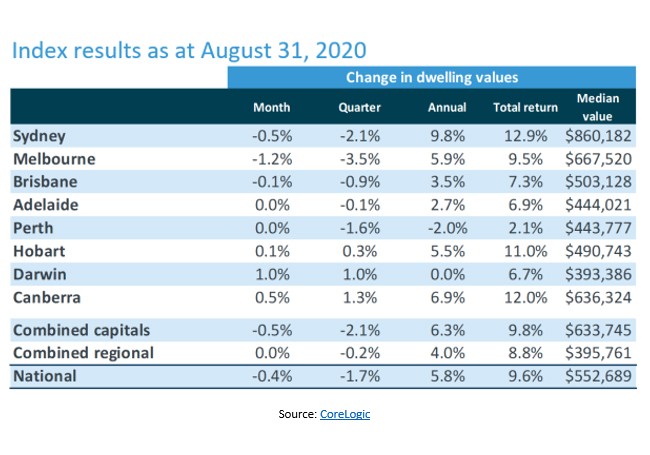

According to CoreLogic, Australian national home values fell 0.4 per cent in August relative to July but were still up 5.8 per cent in annual terms. Across the combined capitals, dwelling values were down 0.5 per cent over the month but were still 6.3 per cent above their August 2019 levels – although the pace of annual growth has continued to trend lower.

By capital city, values fell in Sydney, Melbourne, and Brisbane, were flat in Adelaide and Perth, and rose in Hobart, Darwin and Canberra.

Source: CoreLogic

{kind=link}

The combined regional index was flat over the month and up 8.8 per cent over the year.

Why it matters:

There have now been four consecutive monthly declines in the home value index, with the national decline led by Melbourne (down 1.2 per cent this month and by 4.6 per cent over the COVID-19 period to date).

But as we’ve noted before, with values still up relative to this time last year, the scale of the fall in home prices so far has actually been pretty modest relative to the magnitude of the economic shock that has hit the economy. With some analysts expecting the pandemic to trigger house price declines well into the double-digits, the relative resilience of the housing market has been a positive surprise. As noted last month, that’s likely the joint product of the unprecedented amount of government fiscal largesse which has supported household incomes, the widespread provision of distressed borrower repayment holidays by lenders, and the cushion provided by record low mortgage interest rates. Set against those supportive forces are the headwinds of higher unemployment and lower levels of net overseas migration (and therefore population growth).

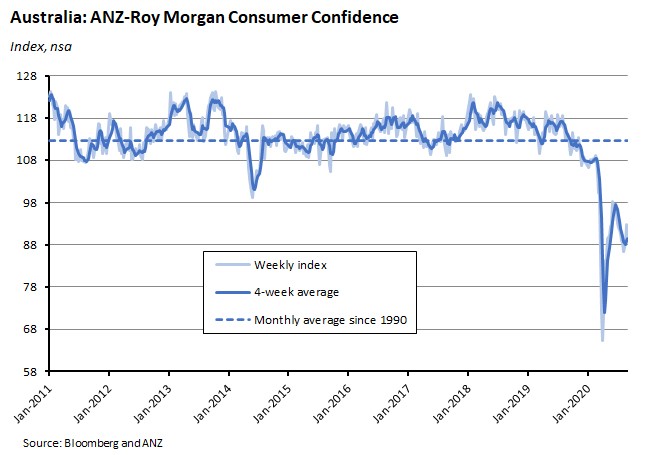

What happened:

The weekly ANZ-Roy Morgan consumer confidence index fell 2.7 per cent to 90.2 on 29/30 August.

All five subindices declined, with current economic conditions down 3.6 per cent, future economic conditions down 2.7 per cent, current finances down 2.5 per cent, future finances down 2.7 per cent and time to buy a household item down 2.4 per cent.

By state, the decline in confidence was mainly driven by falls in states other than Victoria and New South Wales, with confidence rising in the former, although the index is below 100 in all major cities.

Why it matters:

After two weeks of positive results, including a very large jump in the previous weekly reading, there was some payback this time as sentiment softened outside Victoria and New South Wales.

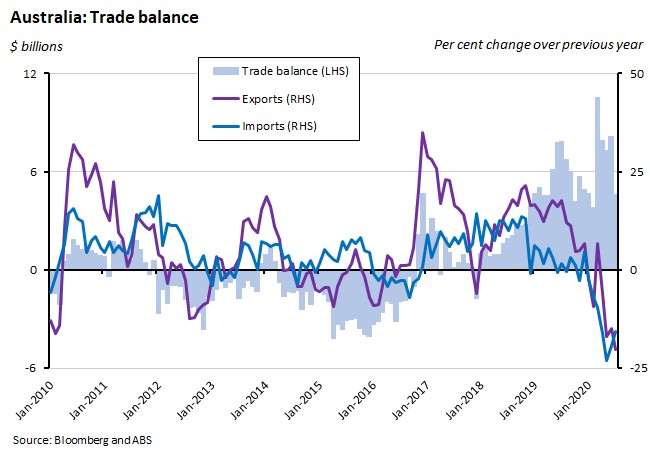

What happened:

The ABS said that Australia’s trade surplus fell to $4.6 billion in July from $8.1 billion in June (seasonally adjusted).

Exports of goods and services fell four per cent over the month and were down 20.3 per cent over the year. Imports of goods and services rose seven per cent relative to June 2020 but were still 15.6 per cent lower than in July 2019.

Why it matters:

Australia’s run of trade surpluses continues, albeit down from the very high levels recorded between March and June this year. The last time Australia recorded a monthly trade deficit was in December 2017, 31 months ago.

What I’ve been reading:

The ABS released its August survey on the Household Impacts of COVID-19. Findings included:

- Almost three in five Australians (58 per cent) including 99 per cent of Victorians reported wearing a facemask due to COVID-19 in mid-August compared with one in eight (13 per cent) in late June.

- 72 per cent of Australians went shopping in physical retail stores in the previous week but that was the case for just 45 per cent of Victorians versus 81 per cent for the rest of Australia.

- Similarly, while 66 per cent of Australians with jobs attended their workplace in person in the previous week, only 30 per cent of Victorians did so.

- 77 per cent of Australians reported their household could raise $2,000 for something important within a week, while 87 per cent said their household expects to be able pay bills received in the next three months.

- The proportion of Australian households unable to raise $500 within a week increased to six per cent in mid-August, compared with three per cent in mid-June.

- In mid-August, 13 per cent of Australians said they were currently receiving the Coronavirus Supplement. They most commonly reported using it to pay household bills (82 per cent).

- 14 per cent of Australians said they are currently receiving the JobKeeper Payment from their employer. Of those receiving the Payment, 64 per cent said they were receiving less income than their usual pay, 22 per cent said they received about the same, and 14 per cent said they received more income as of mid-August.

The Treasurer’s take on the June GDP results – a ‘devastating blow’ to the Australian economy.

The RBA’s September Chart Pack is now available.

In the AFR, Drysdale and Armstrong argue that Australia needs to create its own strategic policy space in Asia. ACOSS have released new research on inequality in Australia.

Fed Chair Jerome Powell’s speech on New Economic Challenges and the Fed's Monetary Policy Review at the Jackson Hole conference last week. Many central bank watchers see this as marking a watershed for Fed policy. He announced two key changes to the Fed’s policy framework, both of which imply that interest rate are likely to be lower for (even) longer: (1) ‘our revised statement says that our policy decision will be informed by our "assessments of the shortfalls of employment from its maximum level" rather than by "deviations from its maximum level" as in our previous statement. This change may appear subtle, but it reflects our view that a robust job market can be sustained without causing an outbreak of inflation.’ And (2) ‘our new statement indicates that we will seek to achieve inflation that averages 2 percent over time. Therefore, following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.’

Here is an explainer on the Fed’s new approach from The Hutchins Center at Brookings.

Willem Buiter is not a fan of the Fed’s new strategy, which he sees as a ‘collection of Type I and Type II errors’. But Adam Posen thinks that what the new approach does is ‘to catch the Fed's strategy up with today's economic realities, and the lessons learned from the last 20 years.’

The latest issue of the IMF’s Finance & Development magazine is now online, including articles on rethinking global resilience and the debt pandemic, an explainer on debt sustainability, and a profile of economist Mariana Mazzucato.

This VoxEU column argues that there is a U-shaped relationship between the employment and GDP effects of lockdowns on the one hand and the level of GDP per capita on other, implying that middle income economies will suffer the largest economic pain from lockdowns.

Related, another VoxEU column looks at US and UK evidence on the polarising effect of systematic differences in the ability to work from home.

Bloomberg’s Justin Fox on the rise of ‘work-from-home’ towns in the United States. And a follow up piece arguing that the ‘big-city exodus’ isn’t very big (yet).

Unherd on the UK’s revolting commuters.

The Economist magazine continues with its series on rethinking key concepts in economics. This one examines the relationship between the US dollar and international trade.

A Guardian long read on the tyranny of chairs.

Latest news

Already a member?

Login to view this content