The AICD’s H2 Director Sentiment Index shows a marked improvement in sentiment relative to the first half of this year. Even so, the index is still deep in negative territory.

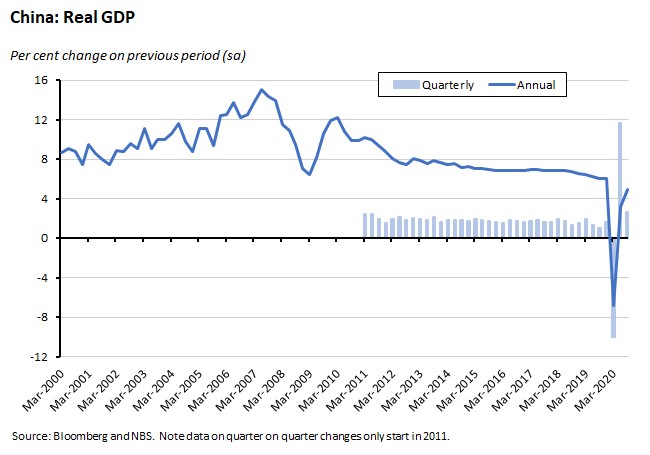

The minutes from the RBA’s 6 October meeting add to the conviction that November will bring further monetary easing. Payroll job numbers declined in the two weeks to 3 October. The weekly index of consumer confidence rose for a seventh consecutive time. Preliminary retail turnover fell over the month in September but rose in annual terms. China enjoyed real GDP growth of 4.9 per cent in the third quarter of this year.

This week’s readings include more from the RBA on assessing the stance of monetary policy in an age of unconventional policies, the ACCC on infrastructure after the pandemic, assessing the case for an Australian manufacturing strategy, the IMF’s regional outlook for Asia and the Pacific, lessons from history on pandemics and inequality, assessing President Trump’s economic legacy and the ‘funeral of austerity’.

What I’ve been following in Australia . . .

What happened:

The AICD’s latest Director Sentiment Index (DSI) has been published. The survey was in the field between 15 and 29 September (and therefore predates the October budget) and captures the responses of 1,777 AICD members. The headline result was that the overall DSI has climbed 22.4 points since the last survey in March, although that still leaves sentiment deep in negative territory at an index level of minus 37.2.

Why it matters:

As always, there’s lots to dive into here, but some of the results that caught my eye include:

- While the impact of COVID-19 – predictably – continues to be the top issue ‘keeping directors awake at night,’ the share of respondents listing this has dropped from 68 per cent to 41 per cent.

- Sixty-nine per cent of respondents expected the Australian economy to be weak over the next 12 months (including 16 per cent thinking it would be very weak) while only four per cent thought it would be strong. Note that October’s budget may have since changed at least some of those perceptions.

- Western Australia was the only state or territory to register a net positive assessment of the state economy over the next 12 months. Indeed, only 19 per cent of WA directors expect either weak or very economic conditions in the state over the next year. That compares with a 50 per cent share predicting weakness in New South Wales, a 70 per cent share in Queensland and an 80 per cent share in Victoria.

- China is the only region or economy where more respondents see economic strength than economic weakness over the next 12 months.

- Climate change and energy policy remain the top issues respondents think government should address in both the short term and the long term. Further down the listings, members have substantially upgraded the relative importance of engagement with Asia.

- More spending on infrastructure and a lower level of personal taxation remain popular (again, note this is a pre-budget assessment).

- A substantial majority (65 per cent) of respondents would be strongly in favour of large-scale public investment in innovation, R&D and skills and training and a smaller majority (51 per cent) would be strongly in favour of large-scale public investment in renewable energy and greening the economy. But on balance, respondents are sceptical about the case for using large-scale public investment to drive a ‘gas-led recovery’ (48 per cent opposed vs 41 per cent in favour).

- More respondents favour the idea of a citizens wealth fund or sovereign wealth fund than oppose it (58 per cent in favour vs 18 per cent opposed) and free universal child care (59 per cent in favour vs 34 per cent opposed) but the reverse is true for the idea of a government employment guarantee (33 per cent in favour vs 37 per cent opposed). There was also a net balance in favour of the idea of a universal basic income or negative income tax (43 per cent in favour vs 31 per cent opposed).

- There was an interesting mix of opinion on the state of the bilateral relationship with China: 28 per cent judged that Canberra had been too confrontational in its approach to Beijing, 27 per cent thought it had got things about right, and 26 per cent felt that the approach had been too accommodative.

What happened:

The RBA published the minutes from the 6 October meeting of the Reserve Bank Board. The minutes report a detailed discussion over the case for the RBA doing more:

‘The Board discussed the case for additional monetary easing to support jobs and the overall economy. As in previous meetings, members discussed the options of reducing the targets for the cash rate and the three-year yield towards zero, without going negative, and buying government bonds further along the yield curve. These options would have the effect of further easing financial conditions in Australia.’

They also recorded the role that monetary policy decisions in other central banks were having on the RBA’s calculations:

‘Members noted that the larger balance sheet expansions by other central banks relative to the Reserve Bank was contributing to lower sovereign yields in most other advanced economies than in Australia. Members discussed the implications of this for the Australian dollar exchange rate.’

And set out the Board’s belief in the changing efficacy of additional policy action:

‘Members also discussed how much traction further monetary easing might obtain in terms of better economic outcomes. They recognised that some parts of the transmission of easier monetary policy had been impaired as a result of the restrictions on activity in parts of the economy. However, as the economy opens up, members considered it reasonable to expect that further monetary easing would gain more traction than had been the case earlier.’

The Board also discussed changes to the RBA’s approach to forward guidance:

‘Over recent months, the Board had communicated that it would ‘not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band’. Given the higher level of uncertainty about inflation dynamics in the current economic environment, the Board agreed to place more weight on actual, not forecast, inflation in its decision-making. Members indicated that they would also like to see more than just progress towards full employment before considering an increase in the cash rate, as the Board views addressing the high rate of unemployment as an important national priority.’

In this light, the Board decided that Governor Lowe would announce the proposed change to forward guidance in his speech on 15 October.

Why it matters:

Last week, we covered Governor Lowe’s latest speech in some depth, noting that along with the change to the central bank’s approach to forward guidance, it had also been widely interpreted as indicating that the RBA would move to ease monetary policy at its 3 November meeting. The publication these minutes has reinforced that interpretation, covering as they do much of the same ground as Lowe’s 15 October presentation:

- They suggest that if the RBA were to act, its options would be ‘reducing the targets for the cash rate and the three-year yield towards zero, without going negative’ along with ‘buying government bonds further along the yield curve’.

- They raise the concern that large balance sheet expansions by other central banks relative to the actions taken by the RBA to date have had (unwelcome) implications for the value of the Australian dollar.

- And they propose that a decision to ease monetary policy now would have traction, given that the economy was opening up again in a way that it might not have, if the RBA acted earlier. All three points are, of course, consistent with the views set out in last week’s speech. They are also consistent with the proposition that next month’s meeting will see the central bank cut the cash rate, the yield curve target and the rate on the Term Funding Facility (likely to 0.1 per cent) and that the RBA will also commence a new program of asset purchases. A 15bp cut in the cash rate is now the consensus forecast (see below).

What happened:

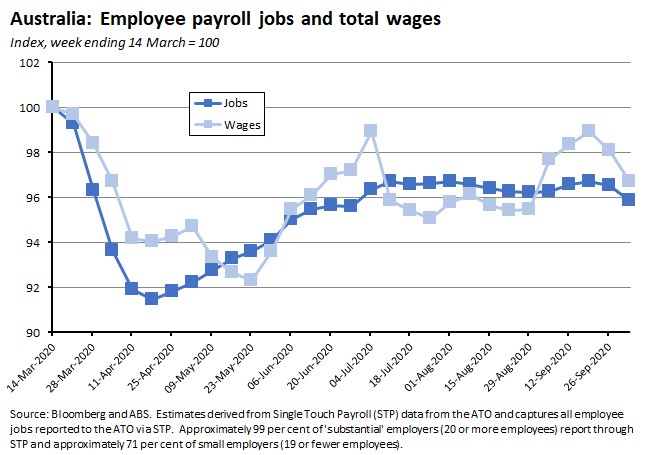

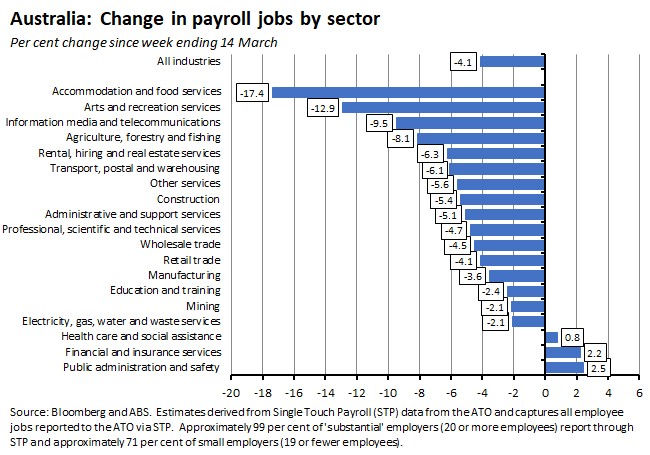

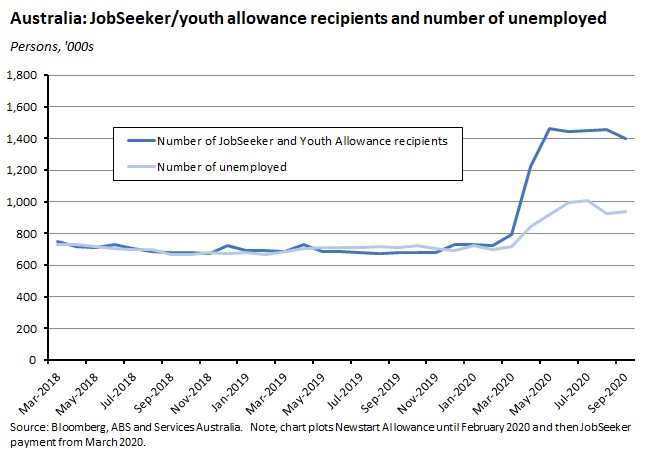

The ABS released the latest set of fortnightly payroll data. The numbers show that between the week ending 14 March and the week ending 3 October 2020, payroll jobs decreased by 4.1 per cent while total wages decreased by 3.3 per cent. As a result, by 3 October, there were approximately 440,000 fewer payroll jobs than there had been on 14 March.

According to the most recent data, for the period between the week ending 19 September and the week ending 3 October 2020, the number of payroll jobs fell 0.9 per cent (compared to an increase of 0.5 per cent over the previous fortnight). Total wages paid decreased by 2.2 per cent over the same period, compared to an increase of 1.3 per cent in the previous fortnight.

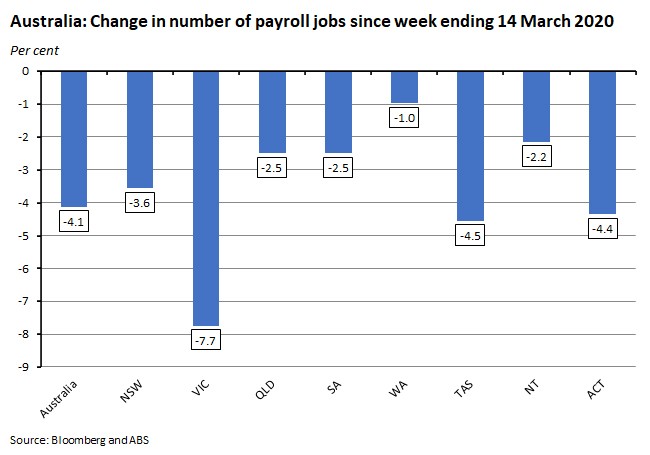

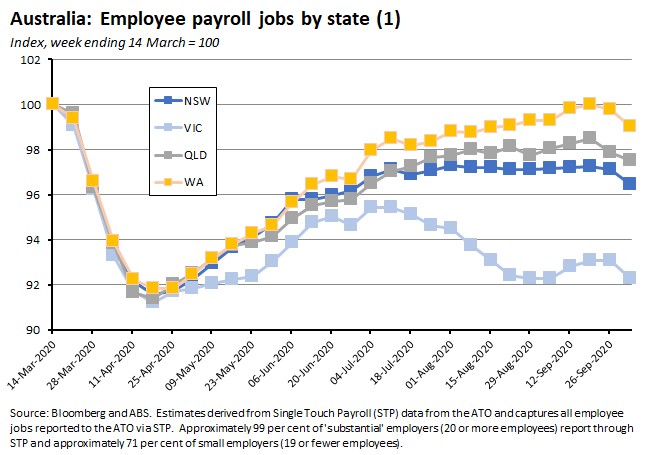

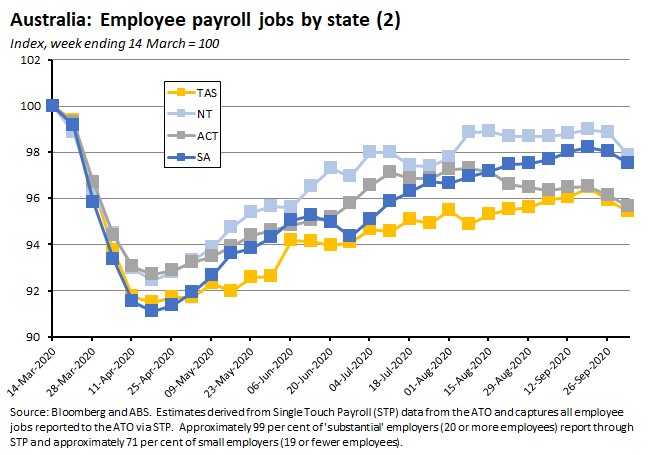

By state, the largest changes since 14 March included a 7.7 per cent fall in payroll jobs in Victoria and a 4.5 per cent decline in Tasmania.

Between the week ending 19 September and the week ending 3 October, the number of payroll jobs fell in every state and territory, with the largest declines in the NT (down 1.2 per cent) and Tasmania and Queensland (both down one per cent).

By industry, the biggest declines in payroll job numbers since 14 March have been in accommodation and food services (down 17.4 per cent), arts and recreation services (down 12.9 per cent) and information, media and telecommunications (down 9.5 per cent).

For the most recent fortnight, the largest job losses were in electricity, gas, water and waste services (down 3.7 per cent), and in agriculture, forestry and fishing and professional, technical and scientific services (both down 2.3 per cent). There were also sizeable falls in other services (down 1.9 per cent) and in construction and information media and telecommunications services (both down 1.7 per cent).

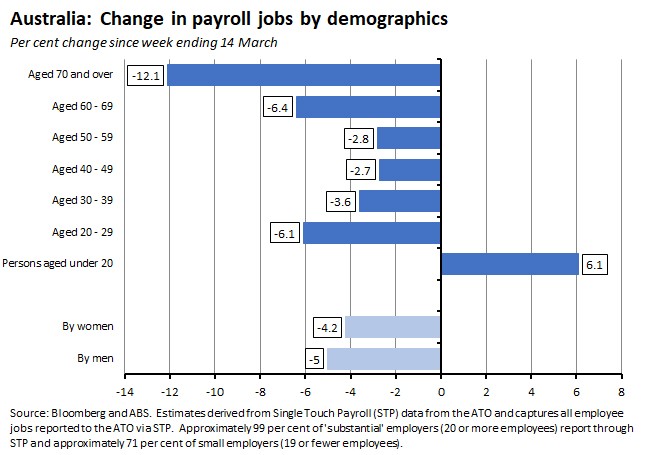

By workforce demographics, male jobs are down five per cent since 14 March while female jobs are down 4.2 per cent, and job numbers are down across all age segments with the exception of workers aged under 20.

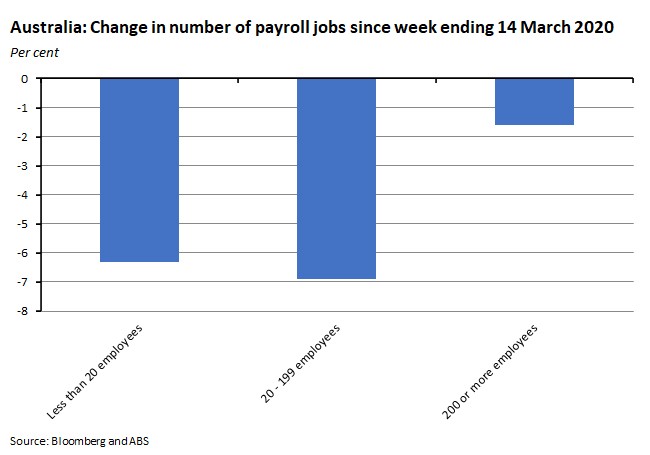

Finally, by firm size the rate of job loss has been largest for small- and medium-sized employers.

Why it matters:

Subject to the usual caveats about the experimental nature of this series and the associated shortcomings of the data, this latest set of payroll jobs numbers indicates that the pace of labour market recovery has been disappointing over the past month. Over the period from 5 September to 3 October, the number of jobs has fallen by around 0.4 per cent, with all states with the exception of Victoria (where job numbers were flat) having shed jobs.

The JobSeeker claimant count for September, along with last week’s labour market report for the same month, also tell a story of a labour market that is still far from returning to health.

What happened:

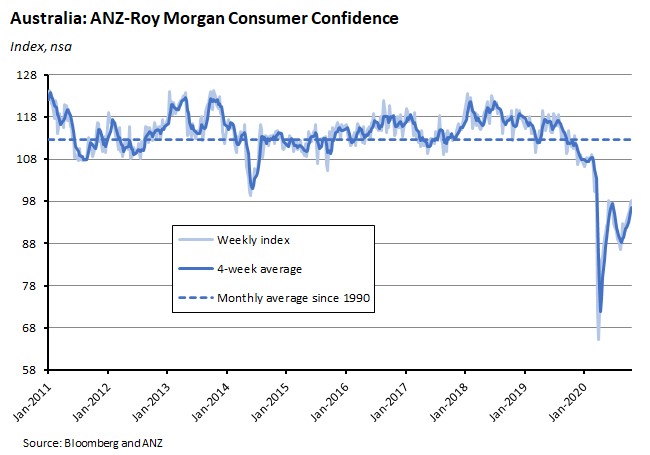

The ANZ-Roy Morgan weekly index of consumer confidence rose 0.4 per cent to 98.1 on October 17/18.

In terms of the five subindices, the main driver of the latest weekly rise in the overall index was a 5.8 per cent gain in the ‘time to buy a household item’ component. There were also modest increases in the survey measures of current economic and current financial conditions, but these were offset by falls in future economic and future financial conditions.

Why it matters:

Following on from the previous reading’s post-budget bounce, this latest rise in consumer confidence represents a seventh consecutive weekly increase. The index is now at its highest level in more than four months.

According to ANZ, the index is now in positive territory in all but three states (New South Wales, Victoria and Tasmania).

What happened:

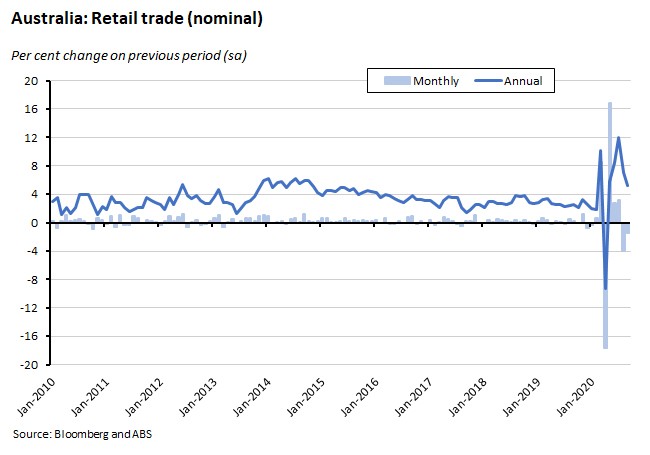

The ABS said that preliminary retail turnover fell 1.5 per cent over the month (seasonally adjusted) in September, but was still up 5.2 per cent relative to September 2019. (The preliminary estimate is based on preliminary data provided by businesses that make-up approximately 80% of total retail turnover and is therefore subject to revision.)

(The preliminary estimate is based on preliminary data provided by businesses that make-up approximately 80% of total retail turnover and is therefore subject to revision.)

According to the ABS, monthly turnover fell in food retailing, household goods retailing, and other retailing, but turnover in all these industries was still up on the corresponding result in September 2019. Clothing, footwear and personal accessory retail turnover also fell over the month, while there were rises in turnover for department stores, and cafes, restaurants and takeaway food services, marking recovery from some substantial declines in last month’s release that were associated with Victoria’s tightening of public health restrictions back in August.

Every state and territory, except the NT, saw retail turnover decline in September, although Victoria suffered only a small fall after the 12.6 per cent drop reported in August.

Why it matters:

An estimate for the Q3 change in retail volumes will have to wait for the final release of turnover data next month. In the meantime, the preliminary estimate shows turnover in the September quarter rose 6.8 per cent in seasonally adjusted, current price terms, following a fall of 2.3 per cent in the June quarter.

What happened:

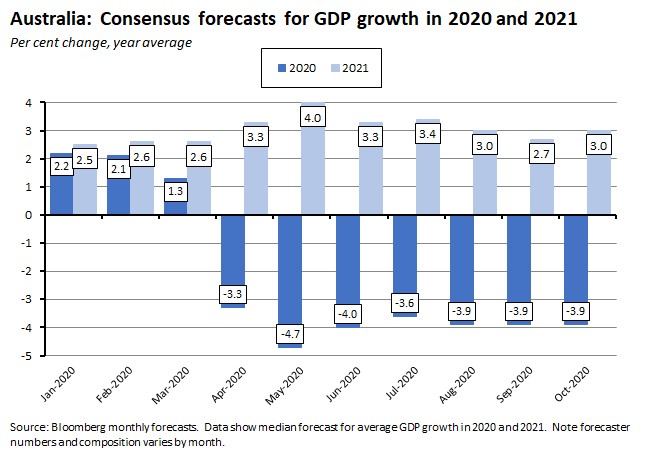

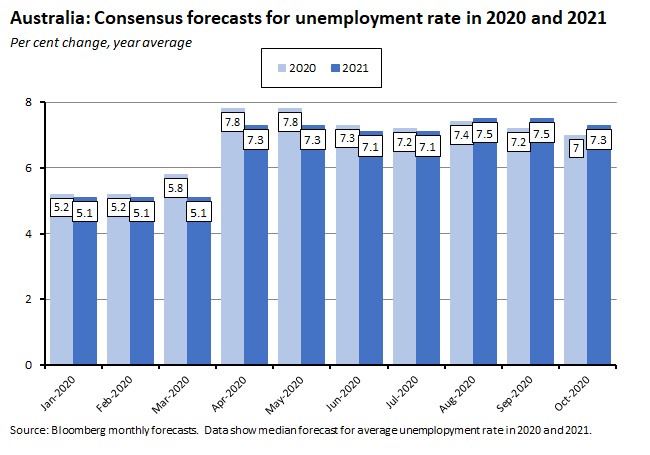

Bloomberg’s October poll of economists found that the median forecast for GDP growth this year was unchanged from September’s poll, with a predicted decline of 3.9 per cent. The consensus forecast for next year edged back up to growth of three per cent.

Forecasters have become slightly more upbeat on the outlook for the labour market, with falls in the median forecast for the average unemployment rate in 2020 and 2021.

Also notable in this month’s set of forecasts was that the cash rate is now expected to end the year at 0.1 per cent instead of 0.25 per cent, and to stay there through 2022 and into 2023 (see also the story on the RBA above). Consistent with this forecast of no change in monetary policy, headline inflation is expected to remain below the bottom of the RBA’s target range though 2022.

Why it matters:

Expectations for growth this year and next are little changed from last month’s forecasts. The main development is that a cut in the cash rate to 0.1 per cent before year-end is now the consensus view.

. . . and what I’ve been following in the global economy

What happened:

According to the country’s National Bureau of Statistics (NBS), China’s real GDP rose by 4.9 per cent over the year in the third quarter. Across the first three quarters of the year, output was up 0.7 per cent over the same period in 2019.

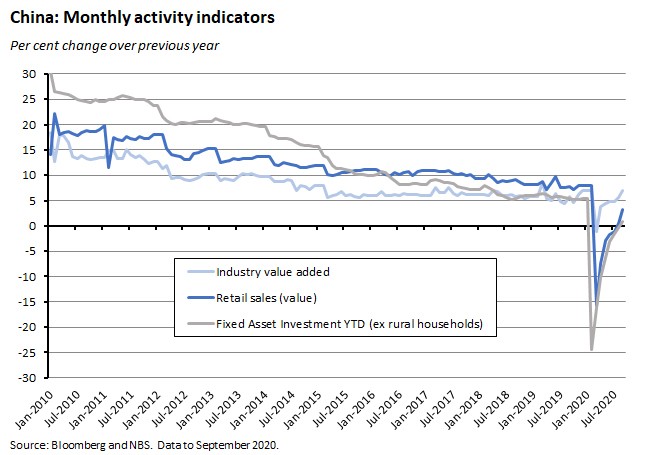

China’s industrial sector continues to be the main force driving the recovery, with industry value added up 6.9 per cent over the year in September, in what was its best result since the start of the pandemic. Still, there are other signs of economic recovery in the Chinese numbers that suggest some broadening of economic activity may be underway. For example, retail sales in September rose 3.3 per cent over the year, powered by a surge in vehicle sales. Until now, the consumer has been reluctant to spend: sales were up just 0.5 per cent over the year in August, and before that had contracted for seven consecutive months.

Fixed asset investment returned to positive annual growth in September, driven by government spending. Private fixed asset investment, however, continued to decline.

Why it matters:

Although the 4.9 per cent Q3 GDP print was a bit weaker than market expectations for a 5.5 per cent growth outcome, it sustains the recovery that started in the second quarter and moves cumulative real output back into positive territory for the first three-quarters of 2020. As noted in last week’s look at the IMF’s latest World Economic Outlook forecasts, China is one of the few economies – and the only major one – that the Fund thinks will see output rise this year, with growth predicted to be a modest (by Beijing’s past standards) 1.9 per cent. This result keeps that forecast broadly on track.

A recovering Chinese economy is also welcome news for regional trading partners, including Australia (despite recent trade tensions). The Q3 GDP numbers reported a sharp jump in imports, while monthly trade data for September showed a record dollar value for imports which were up 13.2 per cent, including an Australian-friendly 17.1 per cent increase in the value of imports of iron ore.

What I’ve been reading . . .

Christopher Kent, RBA Assistant Governor (Financial Markets) spoke on The Stance of Monetary Policy in a World of Numerous Tools. Kent’s message was that in a changed monetary policy landscape, it no longer makes sense to just look to the cash rate as guide to monetary policy. First, because in terms of interest rate tools, the cash rate has now been supplemented by the RBA’s yield curve target, along with an intensified use of forward guidance. And second, because interest rate tools have now been joined by balance sheet measures that provide liquidity or longer-term funding. For example, according to Kent, the RBA’s Term Funding Facility (TFF) has ‘lowered a broader range of interest rates in the economy and put more money into the hands of borrowers and investors.’ Combining both interest rate and balance sheet measures, Kent argues, gives a better picture of the overall stance of monetary policy. For example, although the RBA has only cut the cash rate by 50bp in response to COVID-19 vs 400bp of cuts in response to the GFC, the ‘the breadth and the durability of the easing in financial conditions associated with…balance sheet tools has been greater now than was the case during the GFC’. In the subsequent Q&A session, Kent also told listeners it would not be unexpected for Australian short-term rates (specifically the BBSW rate) to pop below zero.

Deloitte Access Economics summarises the latest business outlook for the Australian and global economies.

The Grattan Institute’s Brendan Coates and Matt Cowgill worry that the 2020-21 budget won’t be enough to deliver a rapid recovery for Australia, partly because they think that the quantum of government stimulus will be wound back too quickly, and partly because they think that the composition of that stimulus won’t generate enough jobs.

Rod Sims, Chair of the Australian Competition and Consumer Commission (ACCC), gave a speech on infrastructure after the pandemic. Sims reckons that infrastructure has ‘become a drag on our economy. We seem often so focussed on assisting the owners of the infrastructure, that we lose sight of the damaging effect on the users.’ That bias towards owners rather than users, he continues, has produced a series of problems, including: privatisation policies skewed towards maximising the proceeds of any sale, rather than the efficient use of the asset or the benefits to consumers; a failure to regulate adequately monopoly infrastructure, such as ports; and extremely slow progress on road reform and a focus on toll roads. The rest of the speech reviews four major industries: the NBN, the electricity market, gas and the airlines. Issues raised here include the high level of concentration in the electricity market and the ACCC’s concern that ‘affordability is being given inadequate weight in our electricity market policy discussions,’ the observation that ‘east coast gas users are being offered prices significantly above export parity prices for contracts,’ and what Sims sees as the long and challenging road to recovery facing the domestic airline sector.

The Parliamentary Budget Office (PBO) has created a Public Debt Interest Calculator which it says can be used to estimate the likely borrowing costs associated with a specific policy.

Richard Holden examines the case for promoting Australian manufacturing.

Greg Earl, writing for ANZ Bluenotes, points out that despite a series of regional and bilateral trade agreements, along with Canberra’s push on economic diplomacy, growth in the number of Australian-owned businesses operating in Asia has been decidedly modest.

The ABS reports on the characteristics of Australian exporters.

Bloomberg Green looks at ambitious plans for major Australian hydrogen exports.

The Lowy Institute has released its annual Asia Power Index. Alyssa Leng summarises the results in five charts.

The IMF’s latest regional economic outlook for Asia and the Pacific is out. The region is forecast to see economic activity contract by 2.2 per cent in 2020, before growing by 6.9 per cent in 2021. This year’s predicted contraction in real GDP comes despite a positive growth outcome expected for China, with overall regional performance pulled down by large falls across a range of other economies including India, the Philippines, Malaysia and Thailand.

De Grauwe and Ji provide an interesting comparison of the global downturn triggered by the coronavirus crisis with the GFC and the 1930s Great Depression. They emphasise two points of difference: (1) the intensity of the fall in activity triggered by COVID-19 has been much greater and faster than that of the Great Depression and of the 2008 crisis, largely because the pandemic produced both a supply and a demand shock which then amplified each other; (2) the pace of the initial recovery from the coronavirus crisis has been much quicker than in the case of the other two shocks, probably because there has been no need to repair the financial system as a precursor to enjoying a recovery.

Via FT Alphaville, this Mainly Macro post draws an analogy between the economics/health trade-off created by the pandemic and the distinctions relating to conventional short-run and long-run Phillips Curve relationships between inflation and unemployment.

Also from FT Alphaville, a short post asking how much we can rely on really long run macroeconomic time series data. I liked this one because I’m a longstanding fan of the late, great Angus Maddison and his work constructing estimates of world GDP over time.

And while we’re on the general topic of economic history, here is an historical overview of the relationship between pandemics and inequality. This piece argues that the impact of the 14th Century ‘Black Death’ was a substantial and long-lasting decline in wealth inequality as the high death toll meant that labour became scarce leading to a rise in real wages and a boost in the relative bargaining power of the poor, who were therefore able to negotiate better conditions. At the same time, the fragmentation of large patrimonies caused by extremely high mortality saw many people inheriting more properties than they needed or wanted, leading to an unusual abundance of property being offered on the market which helped a larger share of the population gain access to property. But, it claims, in subsequent cases the impact of pandemics on inequality was either much more muted or operated in the opposite direction.

As the US Presidential Election draws ever closer, here’s the WSJ on President Trump’s economic legacy in a piece that contrasts the very different performance of the pre- and post-COVID US economy.

An FT Big Read on ‘the week we witnessed the funeral of austerity’ as fiscal austerity is replaced by fiscal activism. The focus is on the big macro policy rethink at the IMF and World Bank, with last week’s meetings pushing a new fiscal consensus that this piece argues was driven by the growth disappointments of the 2010s, the painful political consequences of austerity and as a pragmatic reaction changed economic circumstances. But note that the piece also concludes by cautioning that ‘Austerity might have been buried for now, but if governments’ luck does not hold on borrowing costs and when ageing hits, there is no guarantee it will not be resurrected.’

From a couple of weeks ago now, the Economist magazine had a special report on how COVID-19 will change world economy.

A sceptical examination of modern monetary theory from HSBC’s Stephen King.

Latest news

Already a member?

Login to view this content