The unemployment rate edged up to 6.9 per cent in August. A new speech from the RBA governor appeared to herald further monetary loosening next month, introduced changes to the RBA’s approach to forward guidance and teased a broader evolution in Australia’s monetary policy framework.

Consumer sentiment bounced in October, propelled higher by a positive response to last week’s budget. The IMF has adjusted its forecasts for world growth this year to be slightly less bleak, although it still foresees a record post-war recession. The Fund also predicts a gloomy medium-term future characterised by less growth, more debt, more inequality, more poverty, less human capital and potentially higher taxes relative to its pre-pandemic projections.

This week the regular list of readings has been replaced by a review of the data we missed while the Weekly was off on its budget and school holiday break. The back data cover the ‘no change’ RBA meeting on 6 October and the release of the latest Financial Stability Review, recent labour market data in the form of the latest fortnight of payroll jobs numbers plus ABS quarterly vacancies and ANZ job ads, September’s NAB business survey, August’s retail sales, and several readings on the bousing market comprising price developments, building approvals and new lending commitments. The normal roundup of readings will return next time.

What I’ve been following in Australia . . .

What happened:

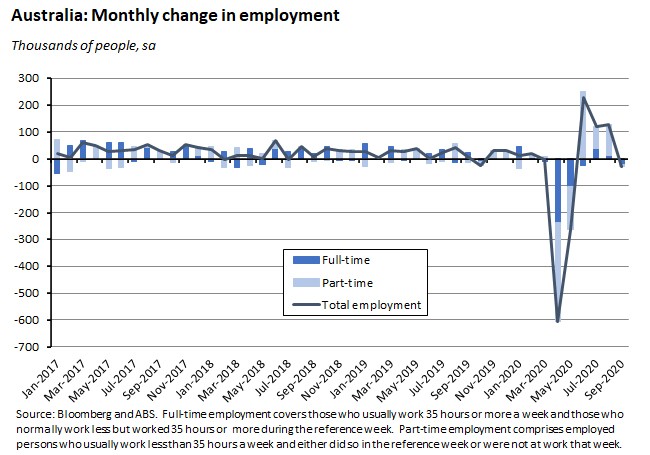

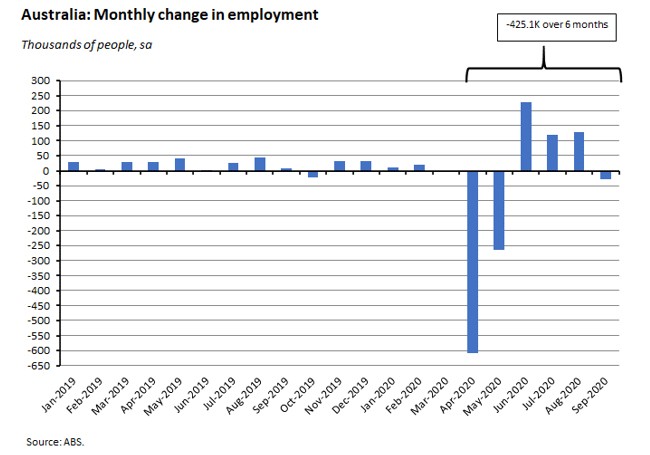

The ABS reported that employment decreased by 29,500 people (0.2 per cent) in September (seasonally adjusted), with full-time employment falling by 20,100 and part-time employment dropping by 9,400.

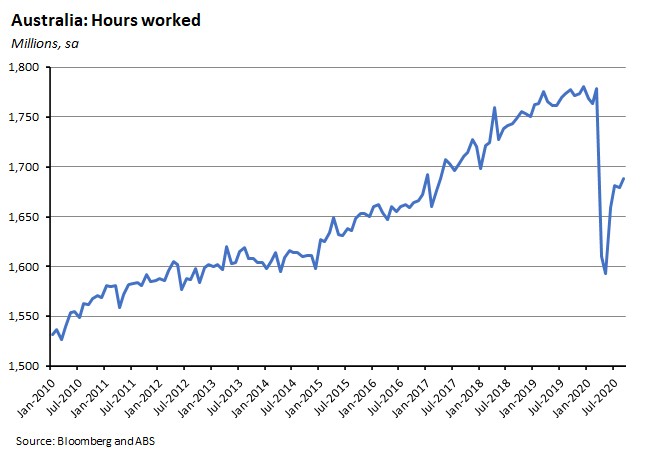

Although employment fell over the month, the number of monthly hours worked in all jobs increased in September by 8.7 million hours (0.5 per cent).

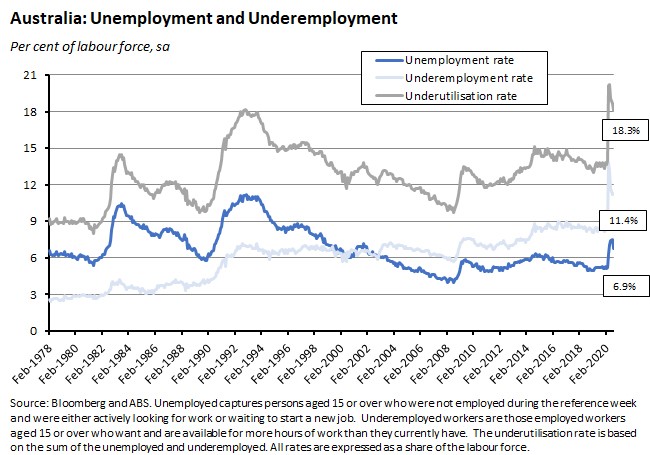

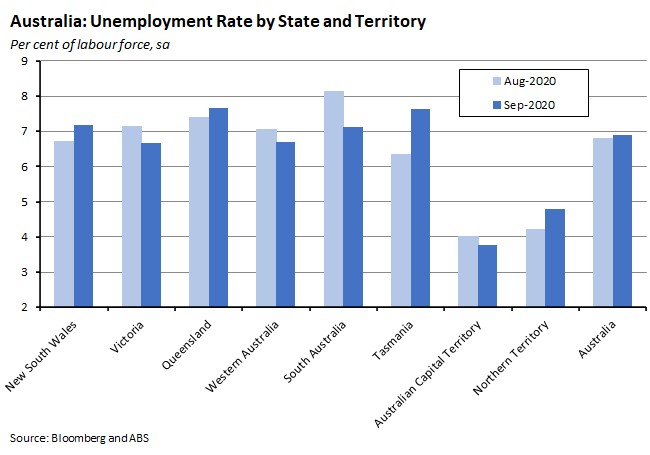

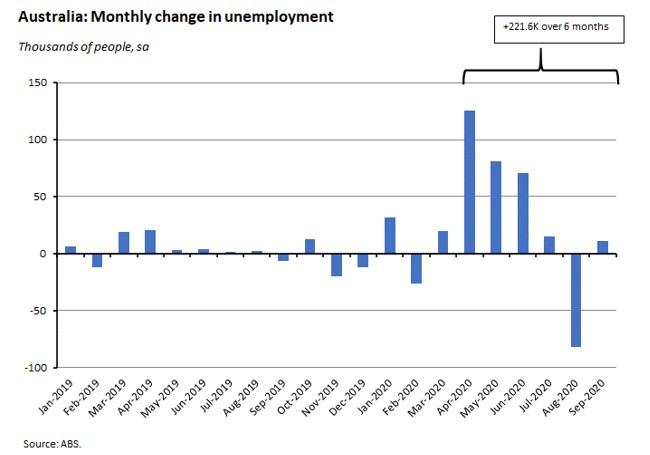

September’s unemployment rate increased by 0.1 percentage points to 6.9 per cent while the underemployment rate increased by the same amount to 11.4 per cent. As a result, the underutilisation rate increased by 0.2 percentage points to 18.3 per cent.

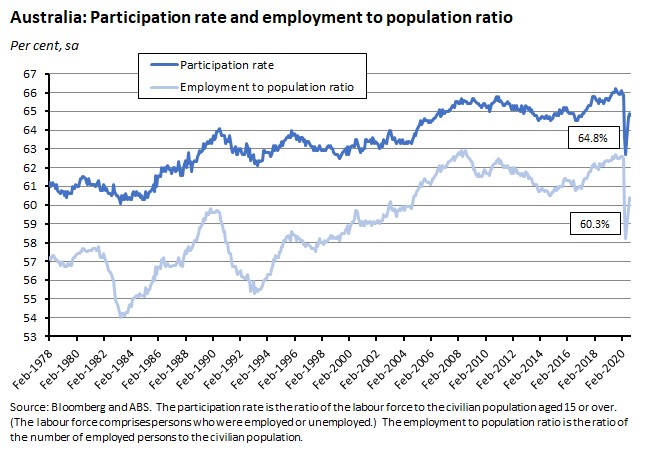

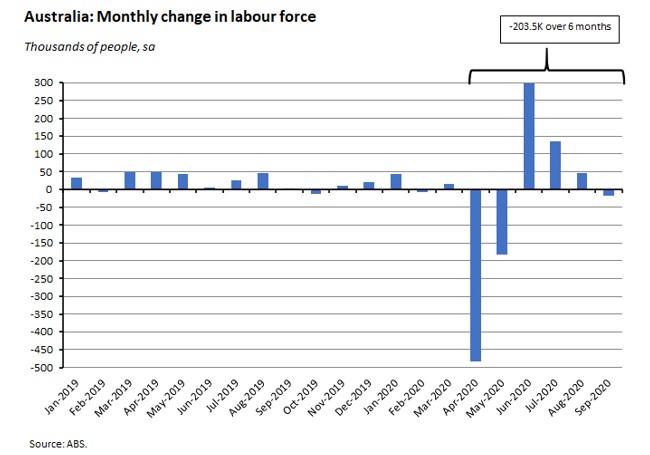

The participation rate decreased by 0.1 percentage points to 64.8 per cent while the employment to population ratio fell 0.2 percentage points to 60.3 per cent.

By state, employment rose over the month in New South Wales (up 0.1 per cent), Queensland (up 1.3 per cent), South Australia (up one per cent) and Western Australia (up 0.2 per cent) but fell in Victoria (down 1.1 per cent), Tasmania (down one per cent), the NT (down 5.1 per cent) and the ACT (down 0.3 per cent).

The unemployment rate rose in New South Wales, Queensland, Tasmania and the NT with participation rates also rising in the first three cases. Elsewhere, unemployment rates fell as participation rates dropped.

Why it matters:

After last month’s surprisingly positive result, the September outcome was broadly in line with (if still slightly better than) market expectations: the median forecast had been for a 40,000 fall in employment instead of the actual drop of 29,500 while the consensus forecast for a rise in the unemployment rate to seven per cent wasn’t too far removed from the 6.9 per cent outcome. The fact that the economy lost jobs rather than adding them over the month is obviously very disappointing, although there was some offsetting positive news in the form of a modest rise in hours worked over the month.

The ABS pointed out that developments in Victoria continue to weigh on the national results as employment in the state decreased by 36,000, following a fall of 37,000 in August. Hours worked in Victoria also fell by 2.1 per cent, after a 4.6 per cent fall in August.

An 18.3 per cent underutilisation rate plus a headline unemployment rate that is still well above pre-crisis estimates of a sub-five per cent equilibrium unemployment rate shows that Australia’s labour market continues to require a lot of repair. And that message is further reinforced if we step back and look at the change in the labour market since the onset of the pandemic. Over the six months from April, the economy is currently down more than 425,000 jobs.

Over the same period, unemployment has risen by a bit less than 222,000.

The gap between these two series consists of the more than 200,000 Australians that have left the labour force over this period. This number is reflected in a participation rate that at 64.8 per cent remains significantly below its pre-COVID level of around 66 per cent.

What happened:

RBA Governor Philip Lowe gave a speech on ‘The recovery from a very uneven recession.’

There were two main components to the governor’s talk. Most of the presentation involved describing ‘the shadow cast by the very uneven nature of the recession that we have been living through’ as captured by diverging labour market trends across age, industry, firm size and region, along with a discussion of the sharp increase in household saving and other factors likely to shape the pace of the economic recovery.

The section that has attracted the most attention, however, came at the end of the speech, when Lowe turned to the RBA’s thoughts on what more monetary policy could be doing ‘to support jobs, incomes and businesses in Australia to help build that important road to the recovery.’ Here, the governor talked first about the RBA’s evolving approach toward forward guidance before moving on to highlight some of the issues that the RBA board is currently its working through.

Starting with forward guidance, the governor noted that the RBA’s thinking had changed. In particular, the focus would now shift from its forecast for future inflation to the actual inflation rate. Thus:

‘In terms of inflation, our forward guidance has been forward looking – we have focused on the outlook for inflation, not just current inflation. This was a sensible approach when the inflation dynamics were relatively stable and well understood. In today's world, things are much less certain. So, we will now be putting a greater weight on actual, not forecast, inflation in our decision-making.’

And again:

‘The Board will not be increasing the cash rate until actual inflation is sustainably within the target range. It is not enough for inflation to be forecast to be in the target range.’ Lowe also tied this back to the labour market, noting that:

‘In terms of unemployment, we want to see more than just ‘progress towards full employment’. The Board views addressing the high rate of unemployment as an important national priority. Consistent with our mandate, we want to do what we can do, with the tools we have, to ensure that people have jobs. We want to see a return to labour market conditions that are consistent with inflation being sustainably within the 2 to 3 per cent target range.’

And again:

‘… achieving inflation consistent with the target is likely to require a return to a tight labour market. On our current outlook for the economy – which we will update in early November – this is still some years away. So, we do not expect to be increasing the cash rate for at least three years.’

After introducing this change to the policy framework in the form of a new approach to forward guidance, the speech then closed by setting out three key issues that the RBA is currently considering.

- First, to what extent would any further easing of monetary policy deliver better economic outcomes (in particular, lower unemployment)? Lowe explained the RBA’s view that when ‘the pandemic was at its worst and there were severe restrictions on activity we judged that there was little to be gained from further monetary easing. The solutions to the problems the country faced lay elsewhere.’ But now, he went on, as ‘the economy opens up…it is reasonable to expect that further monetary easing would get more traction than was the case earlier.’ [emphasis added]

- Second, what would be the impact of any additional easing of monetary policy on financial stability and longer-term macroeconomic stability? Here, Lowe suggested that while these kinds of risks were something that the RBA has ‘paid close attention to in the past when we were considering reducing interest rates in a relatively robust economic environment,’ under current circumstances ‘the considerations have changed somewhat.’ That’s because to ‘the extent that an easing of monetary policy helps people get jobs it will help private sector balance sheets and lessen the number of problem loans. In so doing, it can reduce financial stability risks.’

- Finally, how have the international forces operating on monetary policy changed during the crisis? In the past, looking at interest differentials (for example, the difference between the RBA cash rate and the US Fed Funds rate) ‘provided a reasonable gauge to the relative stance of monetary policy across countries.’ But today, Lowe argued, ‘things are not so straightforward, with monetary policy also working through balance sheet expansion.’ While the RBA has grown its balance sheet quite considerably this year, those increases have been much smaller than seen elsewhere in the world economy.

During the subsequent Q&A session, the governor offered some additional, important insights into the RBA’s thinking.

First, he highlighted the higher levels of yields on ten-year Australian government debt compared to ten-year yields elsewhere. Here he noted that – with the exception of its early efforts to stabilise markets back in March – the RBA hadn’t been buying government debt in the five- to ten-year segment of the yield curve, while in contrast other central banks had been active here. Lowe said that the RBA was now considering first, whether this difference in policy explained the observed difference in yields and second, if so, whether RBA actions to drive down yields at this longer end of the yield curve (and any associated effect on the dollar) would have a material impact on employment and growth.

Second, he talked about the future of the RBA’s inflation targeting regime. Here, he conceded that in recent years the central bank has ‘had some difficulty’ with hitting its inflation target and that the pandemic was only ‘going to make that much more difficult.’ In this context, the governor argued, more important than the inflation target were the RBA’s three overriding objectives as set out in the 1959 Reserve Bank Act: the stability of the currency, the maintenance of full employment and the economic prosperity and welfare of the Australian people. While these three core objectives would not change, Lowe continued, the new environment and the difficulties around getting inflation to its target rate meant that ‘we will have to evolve how we operate monetary policy.’ The changes he had just announced to forward guidance should be seen as an example of this evolution and we should expect to see more evolution in the policy framework over time.

Why it matters:

Aside from an interesting and data-rich discussion on how COVID-19 has been reshaping the Australian economy, there were three big takeaways from this week’s speech.

- First, markets have taken the governor’s words as indicating that the chances of more monetary policy easing on 6 November are now materially higher. At the time of writing, futures markets were pricing in a 72 per cent chance of a rate cut next month.

- Second, the change to the RBA’s forward guidance means that the prospect of any future hike in interest rates has now receded still further into the future. That’s because the new approach sets a higher bar for central bank action. It’s no longer sufficient for the RBA to think that inflation will be headed higher for it to tighten policy. Now it will wait until actual inflation is back – and sustainably back – within the target range before reacting.

- Third, the RBA is in the process of thinking about how to change the monetary policy framework in response to the post-pandemic world. The governor has talked about evolution, not revolution. But more change, it appears, is on its way.

If markets are correct and we do see a change in monetary policy settings in November, what’s likely to be involved? Drawing on what the RBA has already said on the subject, this week’s speech, and the emerging consensus among central bank watchers, a best guess as to the content of a likely package of measures would suggest: (1) 15bp of cuts in the cash rate, the rate on the RBA’s term funding facility (TFF) and the yield curve control target on the three-year government bond yield to take all three to 0.1 per cent from 0.25 per cent; and (2) the introduction of outright quantitative easing (QE or asset purchases) in the five- to ten-year segment of the yield curve. Analysts are currently divided on the relative probabilities surrounding the two elements of this package with different calls on whether QE, rate cuts or both will feature, and will be watching future RBA communications for more clues.

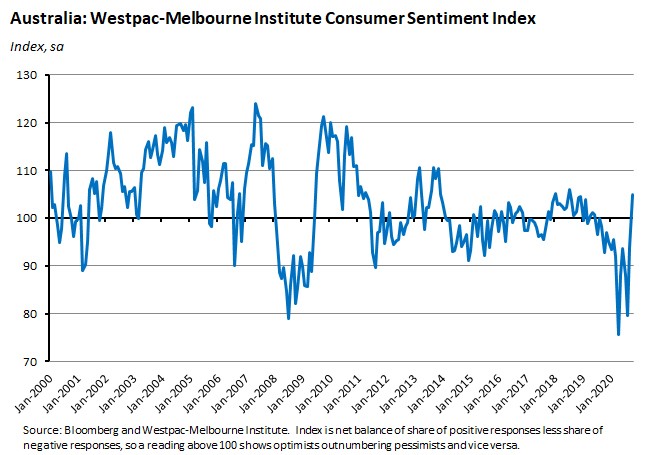

What happened:

The monthly Westpac-Melbourne Institute Index of Consumer Sentiment jumped 11.9 per cent in October, taking the index up from 93.8 to 105.

All five components of the Index rose in October, several of them climbing to recent highs:

- The ‘economy, next 12 months’ sub-index surged by 24 per cent, taking it back to near-August 2019 levels.

- The ‘economy, next 5 years’ sub-index was up by 14 per cent lifting it to its highest level since August 2010 and signalling a very positive view of the medium-term economic outlook.

- The ‘finances vs a year ago’ sub-index climbed 6.2 per cent to the highest level since February 2016.

- The ‘finances, next 12 months’ sub-index rose 9.4 per cent, reaching its highest level since September 2013.

- The ‘time to buy a major item’ subindex rose 8.2 per cent, although this still left it below its December 2019 reading, indicating ongoing caution when it comes to consumer spending.

There were two other very positive survey results, as well. The ‘unemployment expectations index’ plummeted by 14.2 per cent (remember, for this particular index, a fall is a good thing, indicating improved expectations about job security) and is now back around early 2019 levels. And the ‘time to buy a dwelling’ index rose 10.6 per cent to its highest level since September 2019.

Westpac also reported that confidence lifted across all states. New South Wales enjoyed a particularly strong result, with confidence surging by 17.5 per cent, while Victoria saw a 13.7 per cent rise, taking confidence back to levels similar to most other states except New South Wales. Queensland (up 7.1 per cent), Western Australia (up 2.4 per cent) and South Australia (up 9.3 per cent) all reported increases.

Finally, this month’s survey also included a question asking respondents to report their assessment of the budget. The net balance of respondents who assessed that Budget 2020-21 would ‘improve their finances’ was a positive 9.5 per cent. According to Westpac, this post-budget question has been asked since 2010, and over that period, the net balance of respondents who assessed that the Budget would ‘improve their finances’ was minus 29 per cent, suggesting that in the past a clear majority of respondents have expected budget measures to worsen their finances. Strikingly, this is the first budget to deliver a net positive outcome. Several groups of respondents were particularly upbeat about the impact of the budget: there was a positive balance of 21.9 per cent for males (compared to a slight negative balance of 3.7 per cent for females), a net positive balance of 19 per cent for those in the 35 – 49 age group; and a positive balance of 25.7 per cent for those with annual incomes over $100,000.

Why it matters:

The monthly sentiment reading has returned to above pre-pandemic levels (to about 10 per cent above the average level in the six months prior to the pandemic) and is now at its highest level since July 2018. A significant contributor to this recovery has been a very positive response to last week’s budget, along with improving news on the public health front (note that the weekly consumer confidence series discussed below had already been rising for several weeks before the budget). Westpac also suggests that another contributory factor may have been the expectation of further monetary policy easing by the RBA.

What happened:

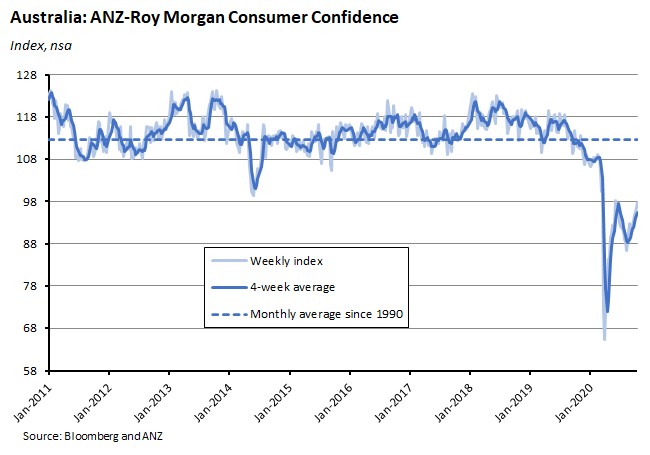

The weekly ANZ-Roy Morgan Consumer Confidence index increased 2.1 per cent to 97.7 on the weekend of 10-11 October.

What happened:

The ABS said that overseas visitor arrivals to Australia in August decreased 14 per cent from July, dropping to just 3,030 trips. This was a decrease of 99.6 per cent when compared to August 2019. At the same time, Australian resident returns from overseas fell 21.5 per cent over the month to just 8,070 trips, a decrease of 99.1 per cent compared to the same month last year.

For 2019-20 overall, there were 6.7 million visitor arrivals, down 27.9 per cent on the previous year and the marking the lowest number of arrivals since 2013-14. Similarly, there were just 8.6 million resident returns from overseas in 2019-20, down 23.8 per cent on 2018-90 and the lowest number of arrivals since 2012-13

Why it matters:

It’s no surprise given the persistence of travel restrictions and public health concerns, but the number of visitor arrivals and returning residents (both classed as those taking short-term trips of less than one year) remains extremely low, with ongoing adverse implications for those parts of the Australian tourism sector focussed on servicing the international market.

In its baseline assumptions underpinning Budget 2020-21, Treasury assumes that inbound and outbound international travel remains low though to the ‘latter part’ of 2021, after which a gradual recovery in international tourism is expected to occur.

What happened:

The ABS published the results of its latest survey on the household impacts of COVID-19. Findings from this survey (which was conducted in mid-September) include:

- 31 per cent of Australians with a job reported that they worked from home most days in September compared with 12 per cent before COVID-19 restrictions started in March.

- People in Victoria (43 per cent) and New South Wales (32 per cent) were more likely to work from home than those in the rest of Australia (22 per cent).

- 35 per cent of Australians in households with children attending school or care said that they had kept their children home due to COVID-19 in the month leading up to the survey, of which 48 per cent was due to illness and 48 per cent due to school closures.

- 15 per cent of respondents in Victoria reported having a job and not working paid hours compared with four per cent in New South Wales and five per cent in the rest of Australia.

- 18 per cent of people with a job did not have enough paid sick leave to take two weeks leave, while 33 per cent had no access to paid sick leave.

- In the four weeks leading up to the survey, 72 per cent of respondents reported their household finances remained unchanged, 16 per cent said they had worsened and 12 per cent felt they had improved. 21 per cent of households with children said their household finances had worsened over this period compared to 14 per cent of lone person households and those without children.

- 15 per cent of Australians have both increased savings and reduced debt since the COVID-19 restrictions began in March.

- 14 per cent of respondents said they were currently receiving the JobKeeper Payment from their employer, with 60 per cent receiving less income than their usual pay, 18 per cent receiving about the same income, and 22 per cent receiving more. Paying household bills (77 per cent) was the most commonly reported use of the JobKeeper Payment followed by paying mortgage/rent (47 per cent).

- Ten per cent of respondents said they were currently receiving the Coronavirus Supplement. Paying household bills (71 per cent) was the most commonly reported use of the Coronavirus Supplement, followed by purchasing household supplies, including groceries (67 per cent).

Why it matters:

These regular ABS surveys of households provide useful snapshots of how COVID-19 has been changing Australia and the lives and livelihoods of Australians.

While the Weekly was away . . .

What happened:

At its meeting on 6 October (Budget day), the RBA Board decided to leave current policy settings, including targets for the cash rate, the yield on three-year Australian Government bonds and parameters for the expanded Term Funding Facility (TFF) unchanged.

The accompanying statement judged that a ‘… recovery is now under way in most of Australia, although the second-wave outbreak in Victoria has resulted in a further contraction in output there. The national recovery is likely to be bumpy and uneven and it will be some time before the level of output returns to its end 2019 level’.

In terms of the labour market, the RBA thinks ‘conditions have improved somewhat over the past few months and the unemployment rate is likely to peak at a lower rate than earlier expected. Even so, unemployment and underemployment are likely to remain high for an extended period. Wage and inflation pressures remain very subdued’.

The Board also judges that the central bank’s ‘policy package is working as expected and is underpinning very low borrowing costs and the supply of credit to households and businesses’.

The key paragraph in the statement was the final one, which noted:

‘The Board is committed to do what it can to support jobs, incomes and businesses in Australia…The Board views addressing the high rate of unemployment as an important national priority. It will maintain highly accommodative policy settings, as long as is required, and will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the 2–3 per cent target band. The Board continues to consider how additional monetary easing could support jobs as the economy opens up further.’ [emphasis added]

New RBA forecasts will be released on 6 November, with the publication of the bank’s latest Statement on Monetary Policy, following next month’s Board meeting on 3 November.

Why it matters:

In the aftermath of Deputy Governor Debelle’s 22 September speech, there had been some speculation that the RBA would act to ease monetary policy, either at this meeting or next month. Markets were pricing in about a 40 per cent chance of a cut in the cash rate to 0.1 per cent but in the end, the RBA decided to leave the field clear for the government’s budget announcement.

Attention now turns to the 3 November meeting, with expectations mounting for some further policy action. The final paragraph in the governor’s statement accompanying this month’s meeting has been interpreted as increasing the chances of such a move. The introduction of the argument that tackling the high rate of unemployment is now ‘an important national priority’ and the tweak in language from ‘The Board will maintain highly accommodative settings as long as is required and continues to consider how further monetary measures could support the recovery’ in September’s Statement to ‘The Board continues to consider how additional monetary easing could support jobs as the economy opens up further’ have both been cited as evidence of a further dovish shift in the RBA’s thinking.

Central bank watchers were also carefully parsing this week’s speech from Governor Lowe for additional clues (see previous section).

What happened:

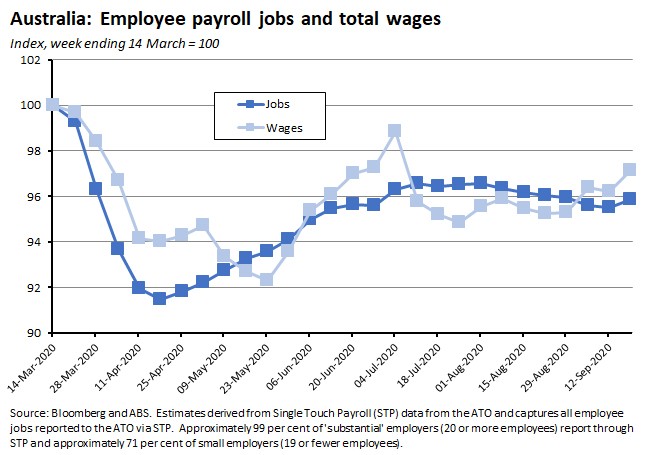

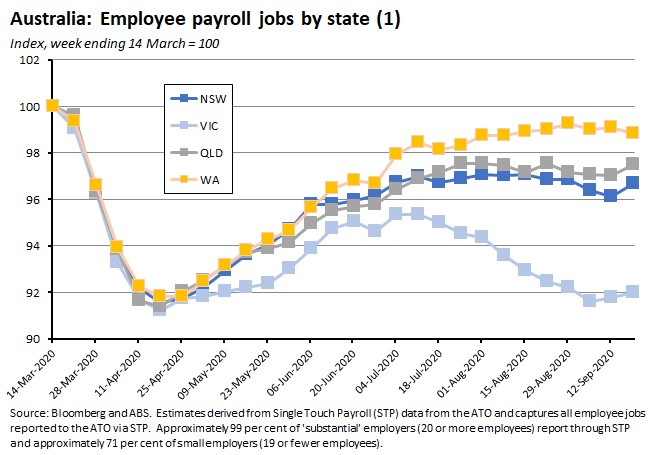

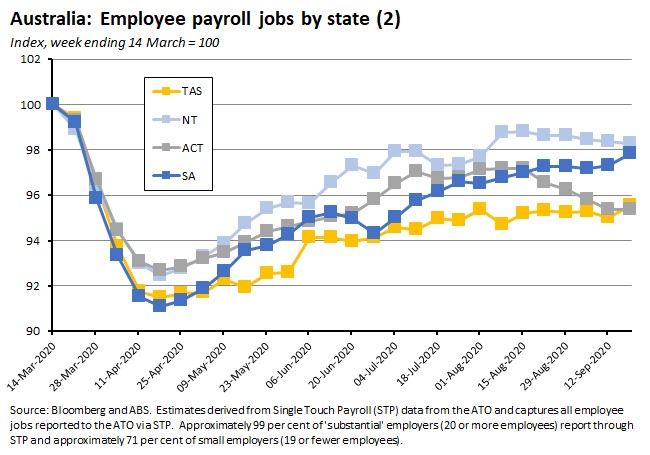

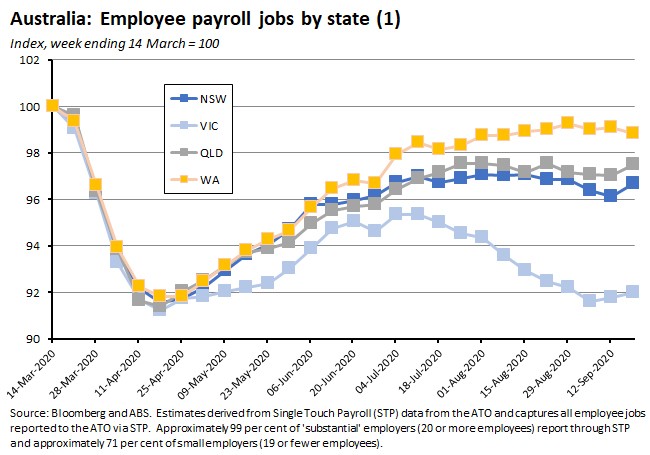

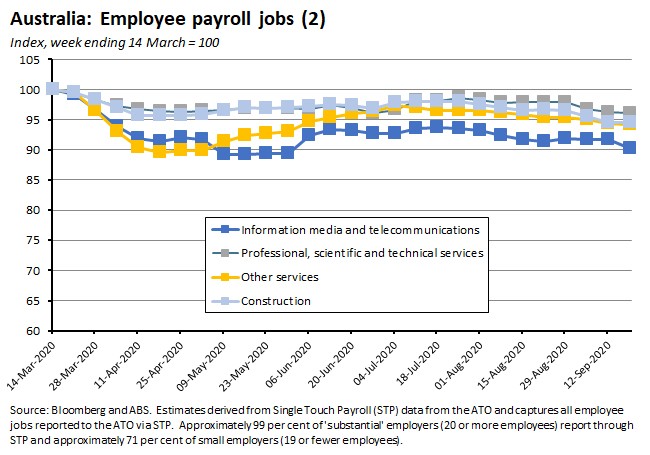

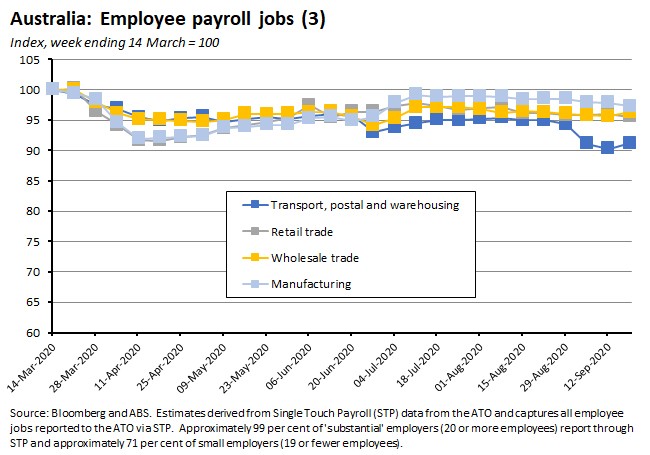

According to the ABS, between the week ending 14 March 2020 (the week Australia recorded its 100th confirmed case of COVID-19) and the week ending 19 September 2020, the number of payroll jobs decreased by 4.1 per cent while total wages paid fell 2.9 per cent. The ABS said there were approximately 440,000 fewer payroll jobs on 19 September 2020 than on 14 March 2020. For the most recent two weeks of data, the ABS reported that between the week ending 5 September and the week ending 19 September 2020, payroll jobs increased by 0.3 per cent, compared to a decrease of 0.5 per cent in the previous fortnight.

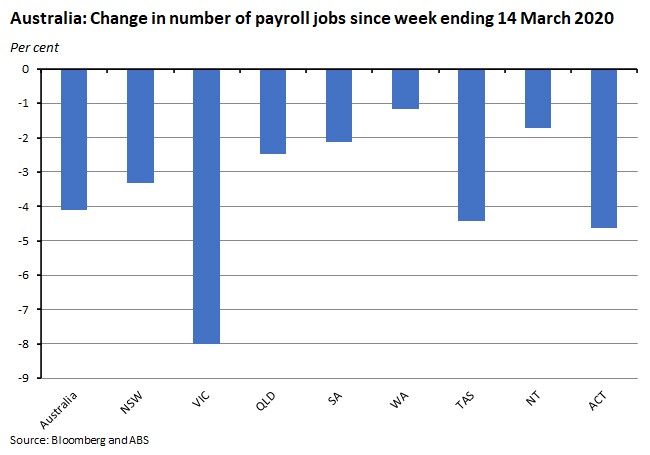

By state, the largest changes in payroll job numbers between 14 March and 19 September were declines of eight per cent in Victoria, 4.6 per cent in the ACT and 4.4 per cent in Tasmania.

Over the most recent fortnight, between 5 and 19 September, the biggest changes in payroll jobs numbers were increases of 0.7 per cent in South Australia, 0.5 per cent in Queensland and 0.4 per cent in Victoria. Job numbers also rose in New South Wales and Tasmania, but fell in Western Australia, the ACT and the NT, with the biggest decline suffered by the ACT (down 0.5 per cent over the fortnight).

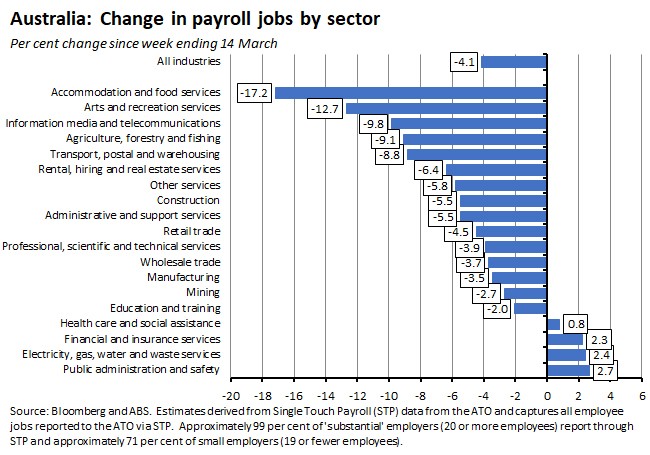

By industry, since the week ending 14 March 2020, the largest changes in payroll jobs numbers have been a 17.2 per cent decline in accommodation and food services jobs, a 12.7 per cent decline in arts and recreation services jobs and a 9.8 per cent decline in information, media and telecommunications job numbers.

Between the week ending 5 September and the week ending 19 September 2020, the largest job gains across industry were increases in payroll jobs in accommodation and food services (up 5.5 per cent) in education and training (up 2.3 per cent) and in finance (up 1.3 per cent). The largest declines were in information technology and agriculture (both down 1.7 per cent).

Why it matters:

The ABS reported that over the month to 19 September, payroll jobs fell by 0.5 per cent in Victoria and by 0.1 per cent in the rest of Australia, which is consistent with the story of a continued lacklustre national recovery in employment, with that overall story pulled down by developments in Victoria. But the most recent set of numbers tell a more positive story (subject to the usual caveats about volatility and the potential for substantial revisions): over the latest fortnight, payroll jobs were up by 0.4 per cent in Victoria, slightly outpacing national growth of 0.3 per cent.

What happened:

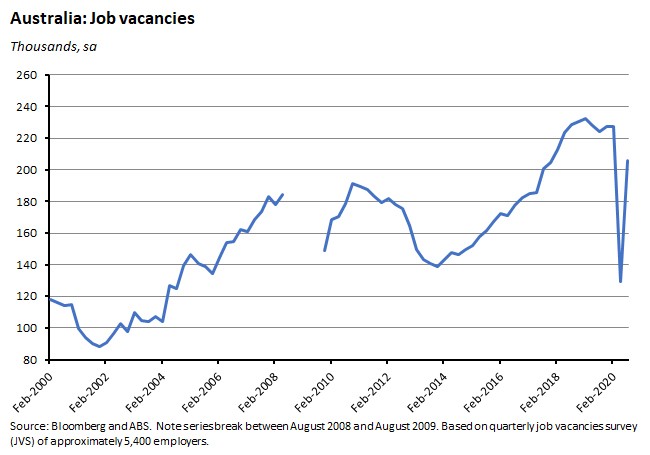

According to the latest ABS quarterly jobs survey, total job vacancies in August 2020 were 206,000, an increase of 59.4 per cent from May’s survey result. Private sector vacancies rose 65.4 per cent in May to number 184,100 in August, while public sector vacancies were up 22 per cent to 21,900.

All states and territories saw strong, positive growth in the number of vacancies over the quarter, with increases ranging from more than 50 per cent in New South Wales, Victoria and the ACT to more than 60 per cent in Queensland, more than 80 per cent in South Australia and Tasmania, more than 90 per cent in Western Australia and more than 140 per cent in the NT. In annual terms, however, only Queensland, South Australia and Western Australia saw vacancies up over August 2019.

The three industries with the largest per centage increases in job vacancies in the August 2020 quarter were the same three sectors that suffered the largest falls in May: Arts and recreation services; rental, hiring and real estate services; and accommodation and food services.

Why it matters:

May had seen the largest fall in job vacancies on record (a 43 per cent collapse) and August marks a substantial recovery from that low with the biggest increase in the history of the series. That still leaves the total number of vacancies about nine per cent below its February level, however.

What happened:

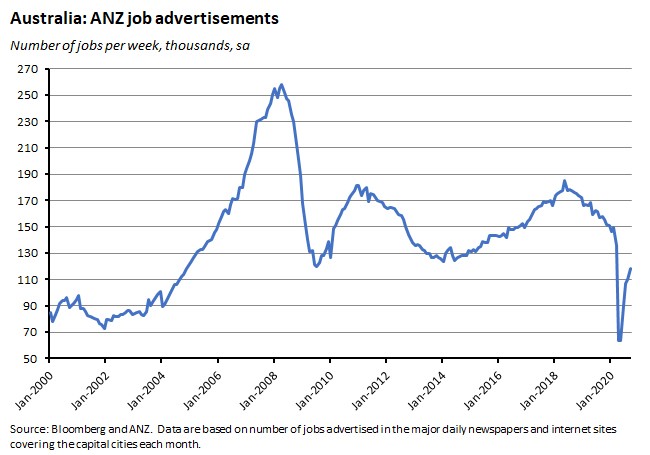

ANZ Job Ads rose 7.8 per cent over the month in September, but were still down 24.8 per cent relative to the same month last year.

Why it matters:

Consistent with the rise in ABS job vacancies, the number of job ads has also been increasing, with the growth in advertisements continuing into September, and at a somewhat faster clip than the (revised) 2.6 per cent monthly gain in August. But again like the ABS data, job ads are still well down on their pre-crisis February levels – in this case, 21 per cent below.

What happened:

The RBA published the October 2020 Financial Stability Review (FSR). Key points made were:

- The FSR judges that ‘Australian businesses and households are generally in a strong financial position’ but also warns that ‘some will struggle in the near term’.

- To date, many Australian households and businesses that have faced a loss of income have been able to defer loan repayments until later this year, or in some cases into next year. This has helped avoid a wave of defaults, but the FSR cautions that the banks will need to ‘deal carefully with the loans of borrowers who will not be able to resume repayments, in a way that balances avoiding further losses to the bank, the interests of the borrower and potential spillover effects from any sales of collateral’.

- In the case of the business sector, the FSR notes that many Australian businesses enjoyed relatively low levels of debt heading into the COVID-19 shock. Since then, a combination of income support measures, rent relief and loan repayment deferrals have helped maintain business cash flows, even in the face of sharp falls in revenues. This, plus temporary insolvency relief, means that business failures to date have trended lower this year. But the FSR warns that ‘business failures will rise substantially as loan repayment deferrals and income support come to an end’.

- A not dissimilar story applies to the household sector. Despite the pandemic, overall household incomes rose in the first half of the year as large fiscal stimulus payments more than offset falling employment income. Households found their cash flows were also buttressed by loan repayment deferrals and the early release of superannuation. This allowed the sector to increase its savings, including through payments into mortgage offset and redraw accounts. So, although some households are already struggling, the FSR reckons that the finances of most households are holding up. Again, however, the FSR warns that higher unemployment and reduced hours for many of those in work mean that not only has the number of households experiencing financial stress increased, but that this number is set to rise further.

- With respect to the housing market, the FSR notes that house prices in Sydney and Melbourne have fallen only a little, albeit with larger falls in inner city areas. There are offsetting forces at work here. On the one hand, credit is available at exceptionally low interest rates. On the other, reduced housing demand from very low immigration and the rise in unemployment both add to the risk of further falls in housing prices (see also the stories below on the latest trends in home values and new lending).

- Finally, in the case of commercial real estate, the FSR states that ‘some commercial real estate also poses significant risks for lenders and leveraged investors.’ The retail sector was already vulnerable prior to the pandemic with rising vacancy rates and falling valuations, and the FSR notes that the combination of mobility restrictions and voluntary physical distancing during the pandemic has worsened these trends. And while conditions in office markets had been tight prior to the crisis, both the current downturn and changing expectations of future office use have driven rising vacancy rates and expectations of declining capital values.

Why it matters:

The FSR’s key judgment is that the ‘Australian financial system has the strength to withstand the economic downturn and support the economic recovery’. But the assessment also concedes that although ‘the Australian financial system is in a strong position, risks are elevated’ and that these risks could be exacerbated by a weaker-than-expected economic recovery. Even then, the report reckons that stress tests of the Australian banking system show that banks would remain above their minimum capital requirements even if suffering from a downside scenario.

What happened:

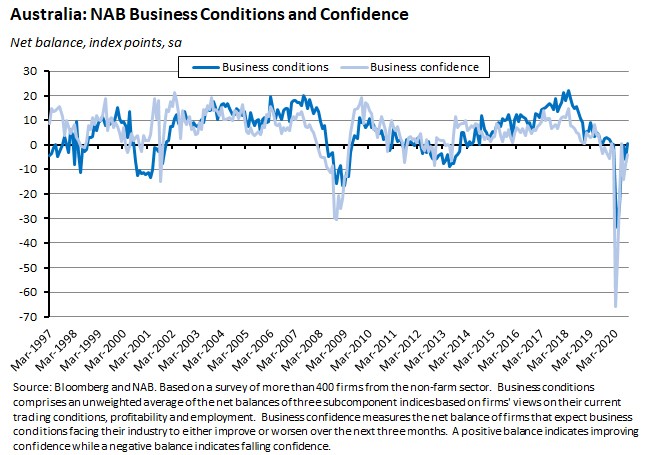

NAB’s monthly business survey for September showed business conditions rose six points over the month to take the index to zero, while business confidence rose by 4 points to minus 4.

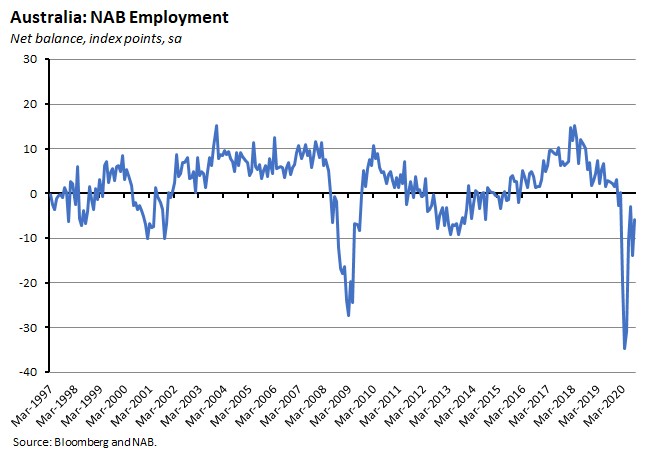

The improvement in business conditions was driven by a rise in all three subcomponents. Trading (up six index points) and profitability (up two index points) are now in positive territory, but the employment index remains negative, even after rising by eight points last month.

According to NAB, business confidence rose in most industries in September (although the increases in retail and recreational & personal services were marginal and finance, business & property services was unchanged) and confidence is now neutral or positive in all industries except retail and the services industries – personal & recreation and finance, business & property services.

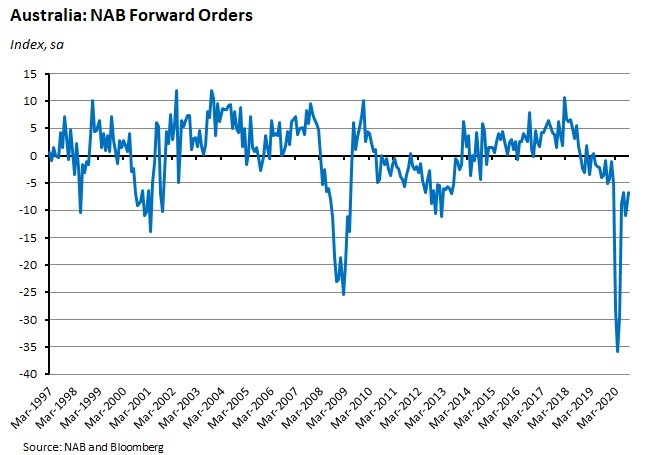

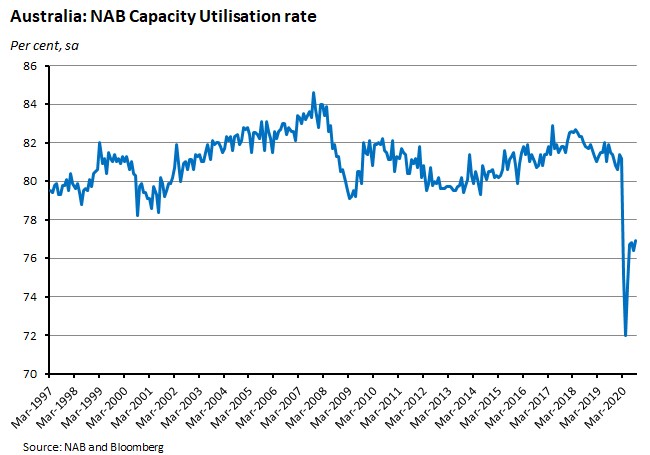

Despite rises in forward orders (up four points to minus seven index points) and capacity utilisation (up 0.5 per centage points to 76.9 per cent), both of these leading indicators remain weak.

NAB also pointed to the ongoing divergence in business conditions across the states, noting that conditions in Victoria are notably weaker than in the other states, while conditions are now above average in Western Australia, South Australia and Queensland indicating to an ongoing recovery in those states. Business conditions in New South Wales remain negative, but also improved in September.

Why it matters:

September delivered a modest improvement in both business conditions and business confidence, although in absolute terms both indicators remain weak. The NAB survey results also reflect Australia’s multi-speed recovery, with the impact of the ongoing lockdown in Victoria showing up in weaker readings for both conditions and confidence.

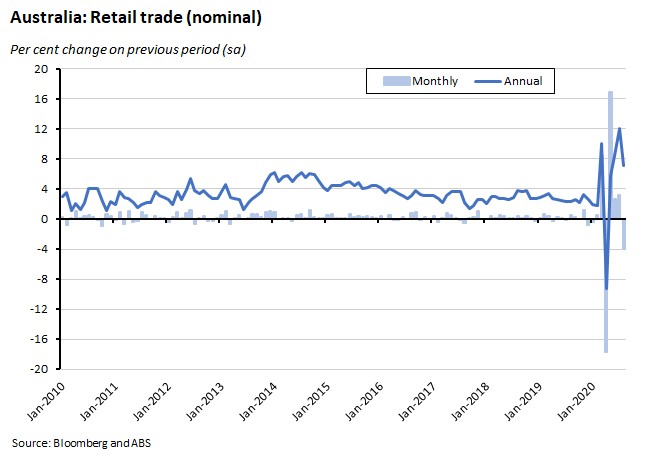

What happened:

According to the ABS, retail trade fell 4 per cent (seasonally adjusted) over the month in August but was still up 7.1 per cent over the year to August 2019. Those figures were broadly in line with the preliminary estimates of a 4.2 per cent monthly decline and 6.9 per cent annual growth.

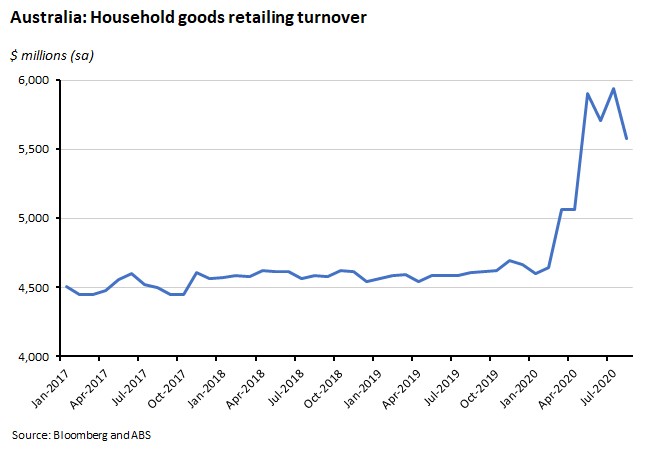

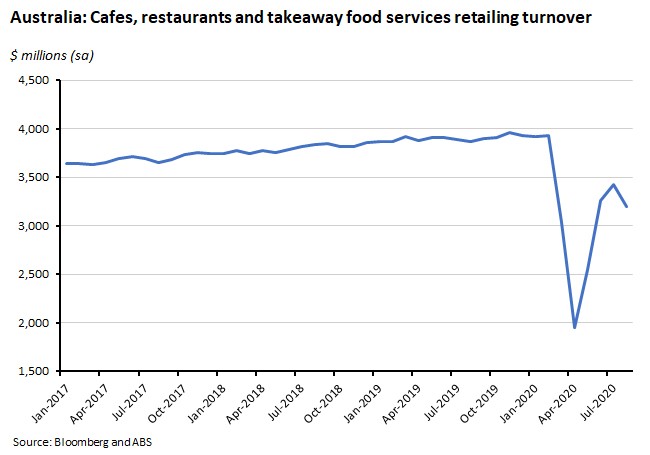

All industries experienced a fall in retail turnover August, with large falls suffered by household goods retailing (down six per cent), other retailing (down 5.1 per cent), clothing, footwear and personal accessory retailing (down 10.5 per cent), cafes, restaurants and takeaway food services (down 6.6 per cent), and department stores (down 8.9 per cent).

Despite the six per cent decline in August, turnover in household goods retailing remains above pre-COVID values.

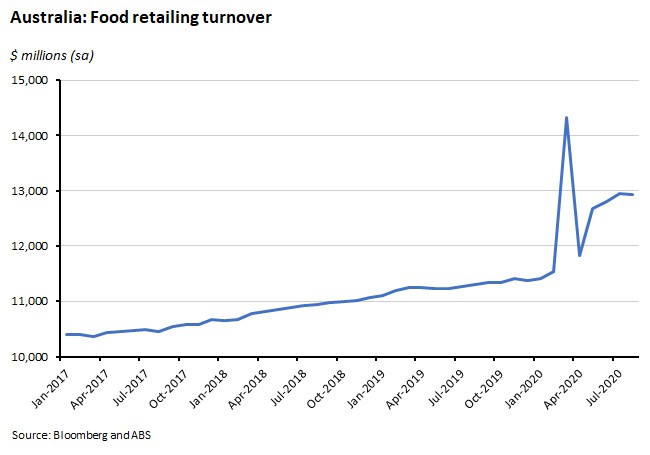

Food retailing only suffered a minor (0.2 per cent) fall over the month and is another industry that in absolute terms remains above pre-COVID levels.

Turnover for cafes, restaurants and takeaway food remains below pre-pandemic levels.

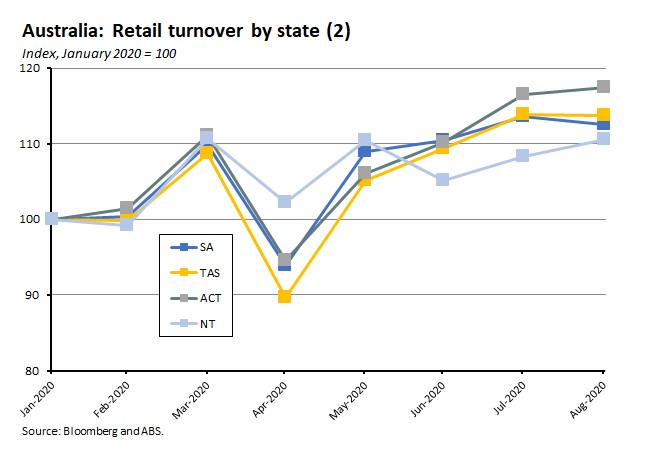

By state, turnover in Victoria slumped 12.6 per cent in August, with the state under stage 3 and 4 restrictions during the month. Turnover also dropped in New South Wales (down 2 per cent), Queensland (down 1.1 per cent), South Australia (down 0.9 per cent), Western Australia (down 0.4 per cent), and Tasmania (down 0.2 per cent). Only the NT and the ACT enjoyed gains in August.

Why it matters:

The national picture for retail sales in August was dominated by the sharp decline in Victoria due to the impact of stage 3 and stage 4 health restrictions.

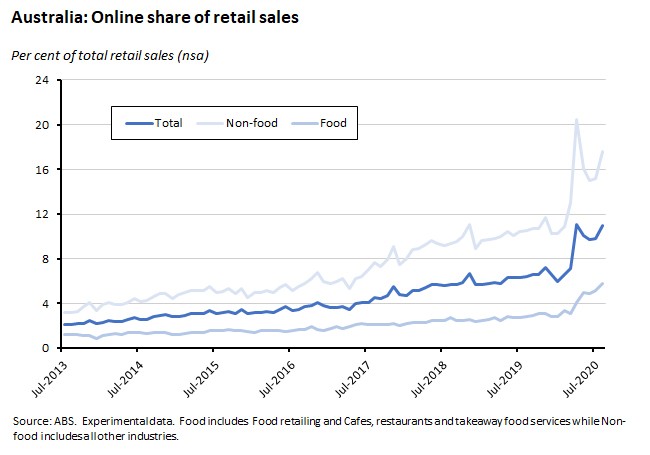

The data also continue to show a structural shift in spending patterns post-pandemic, with elevated turnover for food, household and other retailing. Online sales made up 11 per cent of total retail turnover in August 2020, compared to 6.4 per cent in the same month last year, but down slightly from the 11.1 per cent peak reached in April this year. The share of online sales in food was 5.8 per cent in August, compared to a 17.6 per cent share for non-food. Note that August’s online sales numbers would have been influenced by developments in Victoria.

Why it matters:

The national picture for retail sales in August was dominated by the sharp decline in Victoria due to the impact of stage 3 and stage 4 health restrictions.

The data also continue to show a structural shift in spending patterns post-pandemic, with elevated turnover for food, household and other retailing.

Online sales made up 11 per cent of total retail turnover in August 2020, compared to 6.4 per cent in the same month last year, but down slightly from the 11.1 per cent peak reached in April this year. The share of online sales in food was 5.8 per cent in August, compared to a 17.6 per cent share for non-food. Note that August’s online sales numbers would have been influenced by developments in Victoria.

What happened:

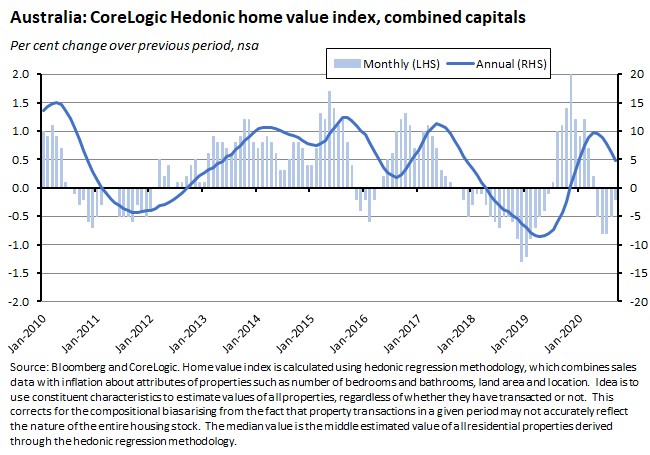

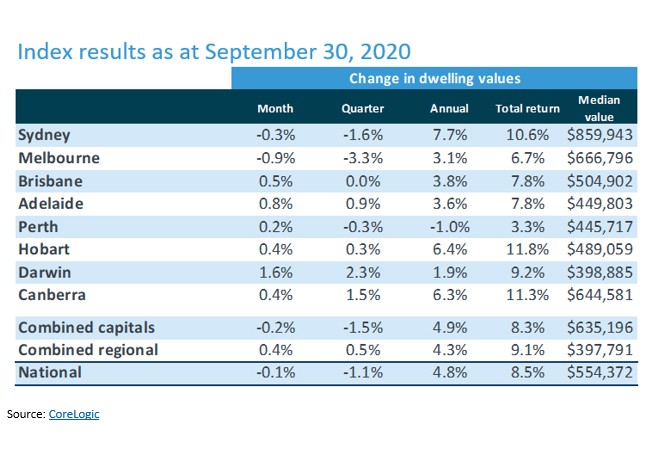

CoreLogic’s monthly national home value index fell 0.1 per cent in September, although it was still up 4.8 per cent over the year. The combined capital cities index fell 0.2 per cent over the month, while the pace of annual growth eased to 4.9 per cent.

Both Melbourne (down 0.9 per cent) and Sydney (down 0.3 per cent) suffered monthly falls again in September, and with those two capital cities together accounting for about 40 per cent of Australia’s housing stock by volume and 55 per cent by value, that was enough to pull the overall index down, despite all other capital cities recording rising prices last month.

Regional markets have continued to outperform relative to the capital cities. At a broad level, the combined regionals index has slipped only 0.8% since March, while capital city values have fallen by 2.6% over the same period.

Why it matters:

This was the fifth consecutive monthly decline in the national and combined capitals indices, as the impact of the pandemic continues to bite. Even so, the pace of decline in prices was the slowest since dwelling values started to fall back in May. Moreover, all but Sydney and Melbourne rebounded this month, and in the case of Sydney the rate of decline has been easing since July. Overall, therefore, CoreLogic judges that,

‘The aggregate effect of low mortgage rates, and the prospect that rates could fall further, low inventory levels, government incentives and improving consumer sentiment seems to be outweighing the negative economic shock brought about by the pandemic.’

This picture of a resilient housing market is reinforced by the August ABS lending data (see next story) which showed very strong growth in new loan commitments, particularly to owner occupiers.

CoreLogic also reports that to date it has not seen any sign of a rise in distressed listings or housing stock starting to pile up in the market (see also the discussion in the RBA’s latest FSR, summarised above).

Instead, new listings are being absorbed by the market faster than the rate at which they are being added. As mortgage repayment holidays wind down and the government tapers its fiscal support to household incomes, CoreLogic judges that pressures on the housing market seem likely to increase, exacerbated by slowing population growth due to the pandemic-inflicted decline in net overseas migration. Set against those headwinds are the budget tax cuts, low interest rates and the government’s plans to ease lending laws.

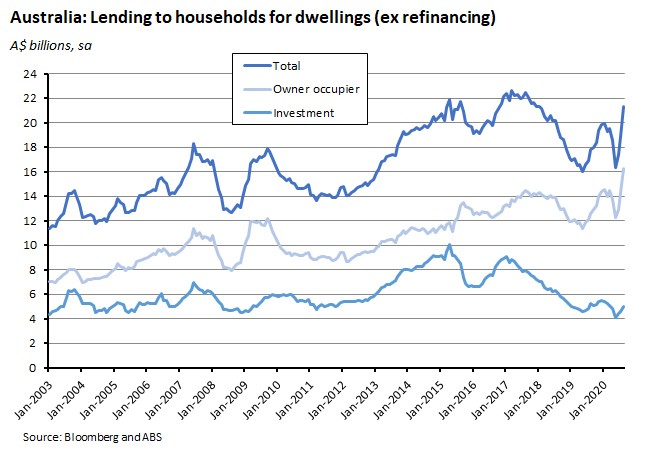

What happened:

The ABS reported that new loan commitments for housing in August rose 12.6 per cent over the month (seasonally adjusted) and were up 19.3 per cent over the year. Loan commitments to owner occupiers (excluding refinancing) were up 13.6 per cent over the month and 29.2 per cent over the year, while commitments to investors (excluding refinancing) were up 9.3 per cent over the month but down 4.6 per cent in annual terms.

Also in August, new loan commitments fell 12.5 per cent over the month for personal fixed term loans and dropped 42.9 per cent for business construction (the ABS notes that typically this is a volatile series, subject to large swings).

Why it matters:

August’s credit numbers are telling a story of future housing market strength, at least in terms of owner occupier sentiment, where the ABS said the value of owner occupier home loan commitments in August ($16.3 billion) was the highest value in the history of the series. Similarly, August’s 13.6 per cent increase in the value of owner occupier home loan commitments was the largest month-on-month rise on record, beating the previous record of 10.7 per cent set in July. First home buyer activity is also strong, with the number of owner occupier first home buyer loan commitments rising 17.7 per cent to reach the highest level since October 2009.

Note that the ABS said August commitments reported here reflect customer demand in June and early July, prior to Victoria imposing stage 3 and stage 4 restrictions.

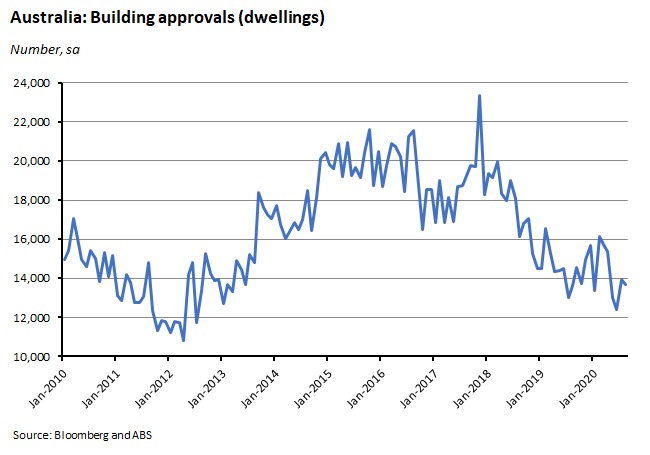

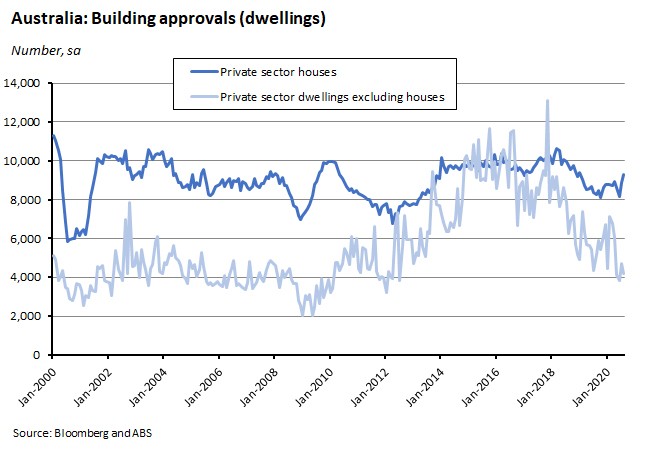

What happened:

The ABS said dwelling approvals fell in August. The number of total dwellings approved fell 1.6 per cent (seasonally adjusted) over the month to be up just 0.6 per cent over the year.

Approvals for private sector dwellings excluding houses – apartments – were down 11 per cent over the month and 18.4 per cent over the year. In contrast, approvals for private sector houses were up 4.8 per cent over the month and 12.4 per cent in annual terms.

By states, the number of dwelling approvals fell in Tasmania (down 26.2 per cent), New South Wales (down 14.2 per cent) and South Australia (down 4.8 per cent). Rises were recorded in Western Australia (up 33.8 per cent), Queensland (up 8.1 per cent) and Victoria (up 1.8 per cent). Both Western Australia (up 34.9 per cent) and Queensland (up 13.9 per cent) saw a particularly strong increase in approvals for private sector houses.

The seasonally adjusted estimate for the value of non-residential building approved rose 40.7 per cent, driven by large public projects in Queensland and the Northern Territory.

Why it matters:

August saw a diverging pattern in approvals, with the overall decline driven by a sharp fall in private sector dwellings excluding houses that unwound much of July’s rise, even as approvals for private sector houses rose for a second consecutive month.

The ABS said the August numbers reflected a combination of increasing demand for detached housing, following the relaxation of restrictions in most states and territories alongside continued weakness in approvals for apartments, which remain at near eight-year lows.

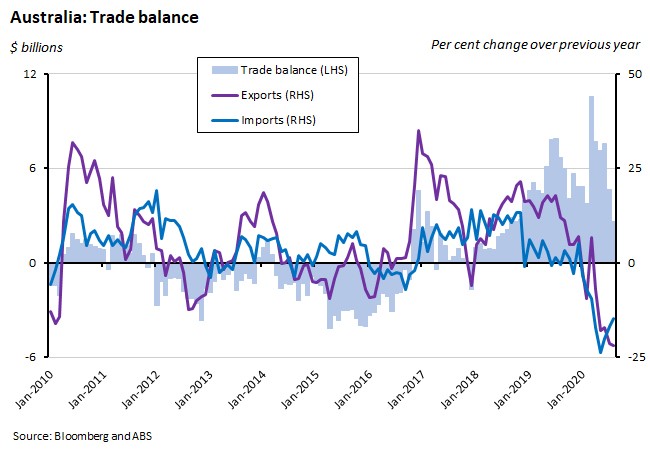

What happened:

The ABS reported that Australia’s seasonally adjusted trade surplus in August fell to $2.6 billion, down a little more than $2.0 billion from July. Exports of goods and services fell 4 per cent over the month, while imports were up two per cent.

The monthly fall (of $1.4 billion) in exports of goods and services was largely driven by a $2.2 billion drop in the value of – often volatile – exports of non-monetary gold. Also notable is the continued fall in the value of exports of services, which stood at just $5.2 billion in August, down from a peak of $8.8 billion in November 2019.

The $0.6 billion rise in imports of goods and services included a $0.6 billion rise in imports of consumer goods (including a jump in imports of cars) and a $0.3 billion rise in imports of intermediate goods, which more than offset a $0.5 billion fall in imports of capital goods. Services imports, like their export counterparts, remain depressed: In August they were worth just $3.7 billion, compared to a peak of $8.8 billion in December 2019.

Why it matters:

The last time Australia ran a monthly trade deficit was at the end of 2017: we’ve now seen a run of 32 months of consecutive surpluses. One part of the story behind these surpluses has been high iron ore prices and strong resource exports, while a more recent driver has been the impact of COVID-19, which until now has compressed imports more than it has squeezed exports.

Latest news

Already a member?

Login to view this content