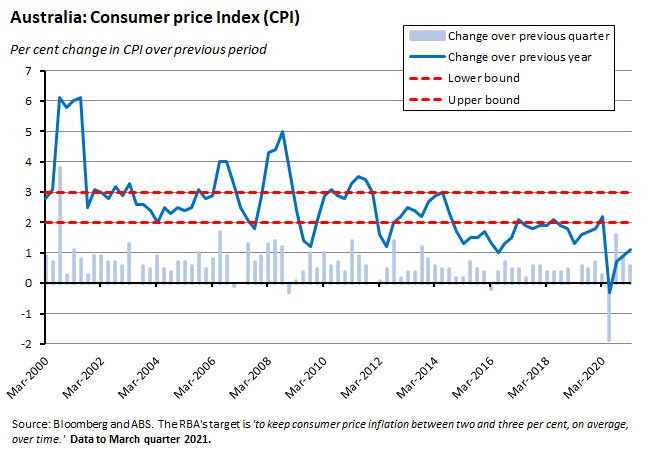

Australia’s consumer price index (CPI) rose 0.6 per cent over the March quarter to be up just 1.1 per cent in annual terms. The annual rate of underlying inflation fell to a record low of 1.1 per cent. Ahead of the May budget, the Treasurer said that the government would avoid any ‘sharp pivots’ toward austerity and instead would continue to focus its fiscal strategy on prioritising job creation and driving down unemployment to below five per cent.

The latest set of payroll data showed job numbers falling over the past fortnight although it was difficult to disentangle seasonal effects from the impact of the end of the JobKeeper program. Exports of iron ore hit a new record last month as did imports of road vehicles, electrical machinery and vaccines. Australia’s general government net operating balance swung from a surplus of $16.6 billion in 2018-19 to a deficit of $107 billion in 2019-20, helping take net public sector debt up to a series high of 31.2 per cent of GDP. The ANZ-Roy Morgan weekly index of consumer confidence fell 1.4 per cent, likely reflecting the impact of the three-day Perth and Peel lockdown. Australia’s flash Composite PMI rose to a record high in April, indicating the fastest rate of expansion in private sector activity in the history of the series. Net Overseas Migration to Australia fell by almost 47,000 to 194,400 in 2019-20 as the impact of the pandemic started to influence population dynamics. According to the Bloomberg vaccine tracker, more than one billion doses have now been administered worldwide. But the divergence in country coverage remains substantial. Global trade volumes edged up 0.3 per cent over the month in February to be 5.3 per cent higher in annual terms.

This week’s readings include new Treasury estimates of Australia’s Non-Accelerating Inflation Rate of Unemployment (NAIRU), an analysis of the Commonwealth’s fiscal sustainability by the PBO, upside risks to Australia’s unemployment rate, reshaping our cities and regions to drive a COVID recovery, scenarios for a leadership transition in China, the implications of India’s second COVID wave, the OECD on prospects for a green recovery, and economic history lessons from previous pandemics.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

The ABS reported that in the March 2021 quarter, Australia’s consumer price index (CPI) rose by 0.6 per cent over the quarter to be up just 1.1 per cent in annual terms.

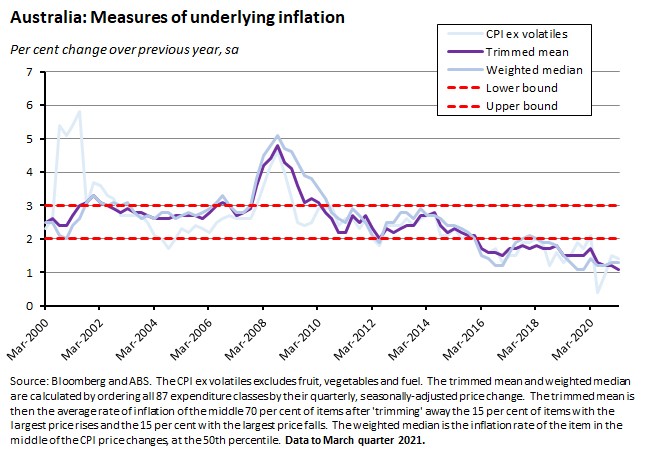

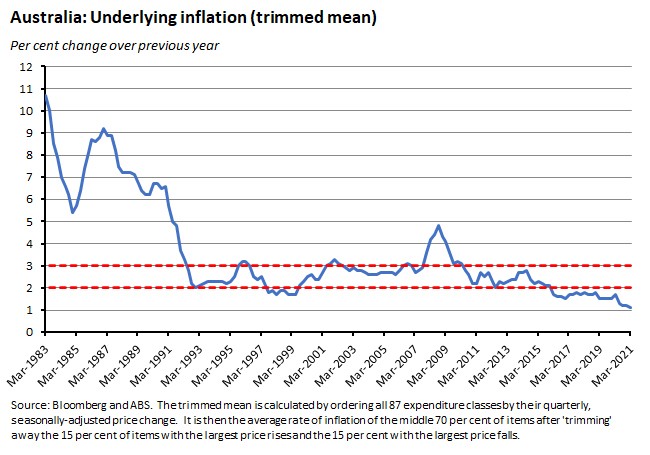

Measures of underlying inflation remained subdued. The trimmed mean – typically understood to be the RBA’s preferred measure of underlying inflationary pressures – rose 0.3 per cent over the quarter and 1.1 per cent over the year, while the weighted median was up 0.4 per cent in quarterly terms and 1.3 per cent in annual terms.

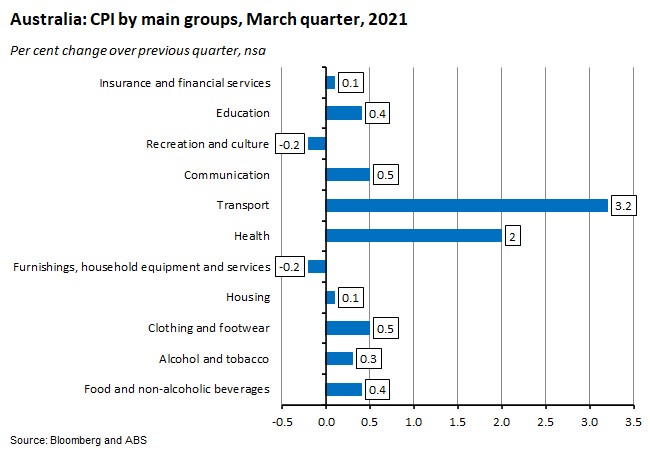

Nine of the eleven main groups that constitute the CPI showed price increases over the March quarter. According to the Bureau, the transport group (up 3.2 per cent over the quarter) was the most important contributor to this quarter’s headline CPI change, with the main driver an 8.7 per cent increase in automotive fuel, reflecting a further recovery in world oil prices from large price falls in early 2020 due to COVID-19 related global lockdowns. There was also a significant increase in annual terms for motor vehicles (up 5.7 per cent) as growing demand ran into supply disruptions.

Another group to show strong price growth was the health group (up two per cent over the quarter) reflecting increases in medical and hospital services (up 1.5 per cent) and pharmaceutical products (up 5.3 per cent) following the resetting of the Medicare and Pharmaceutical Benefits Scheme safety nets.

The ABS also pointed to a notable rise in prices for accessories (up 7.3 per cent) which it said reflected high consumer confidence and demand for discretionary items such as jewellery, allowing jewellers to pass through elevated input costs.

There were also some mild disinflationary forces visible in this quarter’s results, with falls in two of the main groups. The recreation and culture group and the furnishings, household equipment and services group were both down 0.2 per cent over the quarter. In the case of the former, the ABS said that the easing of COVID-19 related restrictions and changes in the airline market were key drivers, as domestic holiday travel and accommodation fell 1.8 per cent on the back of lower airfares due to significant discounting between domestic carriers. The latter reflected a three per cent fall in furniture as prices fell due to post-Christmas discounting.

The housing group (up 0.1 per cent over the quarter) was of particular interest this quarter given the ongoing boom in the housing market. Here, the ABS emphasised the important role played by state and Commonwealth government assistance schemes, highlighting several developments:

- Maintenance and repair of dwellings rose 1.1 per cent as prices returned to previous levels following the completion of the Northern Territory Government's Home Improvement Scheme.

- Electricity fell 0.9 per cent as an annual review of Victorian electricity prices drove a fall in Melbourne. At the same time, prices in Perth rose 41.6 per cent, as electricity costs returned to more normal levels following the introduction of a $600 household electricity credit by the Western Australian Government in the December 2020 quarter.

- New dwelling purchase by owner occupiers fell 0.1 per cent. The ABS said that the HomeBuilder scheme plus state-based housing construction grants in Western Australia and Tasmania had a significant impact on this series. There was a substantial increase in the number of payments of these grants, absent which price would have instead have risen by 1.9 per cent, reflecting increases in materials and labour prices in response to strong demand.

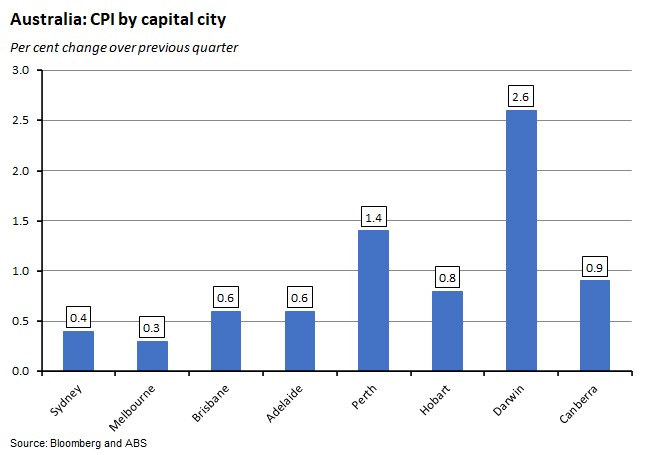

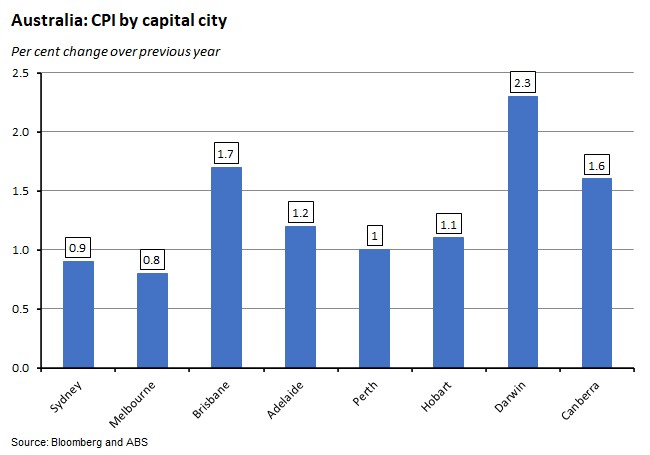

By capital city, the largest increases in the CPI over the quarter were seen in Darwin (up 2.6 per cent) and Perth (up 1.4 per cent) while the smallest rises were in Sydney (up 0.4 per cent) and Melbourne (up 0.3 per cent). In the case of Darwin, the strong increase reflected the end of the Northern Territory Government's Home Improvement Scheme as noted above, along with large increases for automotive fuel and secondary education. Similarly, in Perth, one important driver of the quarterly increase was the 41.6 per cent increase in electricity discussed above. And in Melbourne the state government’s review of electricity prices was an important factor in the quarterly outcome.

In annual terms, there was some significant diversity in headline rates of CPI inflation, varying from 2.3 per cent in Darwin to 0.8 per cent in Melbourne.

Why it matters:

There is an ongoing debate as to whether the RBA’s forecasts for inflation (and therefore prospects for the cash rate) are too cautious, with some market participants judging that inflationary pressures are likely to increase earlier than projected by the central bank. That in turn has implications for the expected future trajectory of interest rates, where the RBA has been working hard to convince the economy that rate hikes are still some way off - not ‘until 2024 at the earliest’, according to April’s RBA meeting.

Next month’s release of the May Statement on Monetary Policy will bring new RBA forecasts and a new chance to assess Martin Place’s take on the state of price pressures in the economy. In the meantime, however, it seems fair score this latest data release in favour of the RBA. The consensus forecast had expected a stronger result (0.9 per cent quarter-on-quarter and 1.4 per cent year-on-year) vs the actual outcomes of 0.6 per cent and 1.1 per cent. Strip out automotive fuel prices – which contributed about 0.3 percentage points to the quarterly rise – and price pressures were even more subdued.

The same was true for underlying inflation, with the median forecast for the increase in the trimmed mean calling for a 0.5 per cent quarterly rise and a 1.2 per cent annual rate vs actuals of 0.3 per cent and 1.1 per cent, respectively. Moreover, that 1.1 per cent annual rate of increase was the lowest in the history of the series (which runs back to 1983). It also marks the 21st consecutive quarter that the trimmed mean has been below the bottom of the two-to-three per cent target band for headline inflation.

All that said, inflation numbers continue to be knocked around quite a lot by changes in government programs: this quarter, the Commonwealth’s HomeBuilder scheme and similar state schemes in Western Australia and Tasmania helped keep down the price of new dwellings, the Federal Government's Job-ready Graduates Package resulted in a fall in tertiary education fees (on average, the costs for commencing students increased but those for continuing students fell, mainly due to grandfathering arrangements included in the package), and state government policies affected electricity prices in various directions.

Looking ahead, base effects in particular are expected to help drive the annual rate of headline inflation up to around three per cent in the June quarter, but the RBA has repeatedly said that it expects the increase, thinks it will be temporary, and as such plans to look through it when considering the future path of monetary policy.

What happened:

Treasurer Josh Frydenberg gave an address to the Australian Chamber of Commerce and Industry setting out the government’s fiscal strategy in advance of the May budget. The Treasurer began by referring to the existing post-COVID fiscal strategy, introduced last year, which was based around two phases. The first phase would focus on securing a ‘strong and sustained economic recovery and drive the unemployment rate down’ while the second phase would shift the focus to longer-term fiscal sustainability.

Back then, the guidance was that the first phase would remain in place until the unemployment rate was ‘comfortably below six per cent.’ Now, he noted, the unemployment rate has fallen to 5.6 per cent, employment is at a record high, consumer confidence is at an 11-year high, and busines conditions are at their highest on record. What does this all this mean for the future of his fiscal strategy? According to the Treasurer, ‘we remain firmly in the first phase’ and therefore the focus on driving down unemployment will continue. He said:

‘We will not move to the second phase of our fiscal strategy until we are confident that we have secured the economic recovery. We first want to drive the unemployment rate down to where it was prior to the pandemic [5.1 per cent] and then even lower. And we want to see that sustained.’

He then listed several reasons why fiscal policy would continue to be focussed on the unemployment rate:

- ‘Against the backdrop of a highly uncertain global economic environment, it is prudent to continue to support the economy and ensure that our recovery is locked in.’

- With the RBA’s policy rate already close to zero, ‘monetary policy is heavily constrained…This has placed more of the burden on fiscal policy.’

- The economy can operate with a lower unemployment rate than had been previously assumed, as ‘estimates of the ‘NAIRU’ or the rate of unemployment below which inflation is expected to accelerate over time, have come down’, with new work from Treasury (see this week’s readings, below) suggesting that the NAIRU is now between 4.5 and five per cent, lower than its previous estimate of five per cent.That ‘means a lower unemployment rate will now be required to see inflation and wages accelerate… the unemployment rate will now need to have a four in front of it to deliver this outcome.’

What about fiscal sustainability? Here the Treasurer made several important points:

- He emphasised that ‘the best way to repair the Budget is to repair the economy’, citing the example of the positive impact of the turnaround in the labour market on government finances: ‘200,000 more Australians in work and off Jobseeker equates to almost $3 billion less being paid out in direct income support payments each year. It also generates, on average, over $2 billion in additional income tax receipts each year. That is around a $5 billion turnaround to the Budget. And these are just the direct effects. The indirect effects of a stronger economy and more people in work go well beyond this.’

- He also acknowledged the benefits of the current low interest rate environment, pointing out that despite ‘a substantial increase in gross debt, the MYEFO showed that the cost of servicing that debt is actually lower today than in 2018-19, as a result of historically low interest rates’ and noting that the government had extended the maturity of its borrowing to lock in these lower interest rate costs.

- Sticking with this theme, the Treasurer also added that ‘Treasury’s projections are that nominal economic growth will exceed the nominal interest rate for at least the next decade…economic growth will more than cover the cost of servicing our debt interest payments. As a result, by growing our economy we can maintain a steady and declining ratio of debt to GDP over the medium term as we continue to move towards balancing the Budget.’

Why it matters:

This week’s speech provided some useful guidance on the government’s thinking as we look forward to the May budget. In particular, there was a clear message that Australia ‘won’t be undertaking any sharp pivots towards “austerity.”’ Instead, the Treasurer stressed that for ‘fiscal consolidation to be sustainable, it should rely on gradual changes that are made over time and that provide the foundation for a growing, thriving economy.’

The speech also reflected some recent shifts that have taken place in the conventional wisdom regarding fiscal policy. Several of the key themes that we’ve discussed in previous issues of the Weekly made an appearance here:

- A shift in the relative importance of fiscal and monetary policy in terms of macro stabilisation in favour of the former.

- A recognition that the NAIRU has fallen, that it is therefore possible to run the economy ‘hotter’ than previously thought, and that macro policy should actively seek to drive down the unemployment rate.

- And finally, the increase in available fiscal space provided by very low interest rates and the framing of debt sustainability issues around the gap between the nominal growth rate and the nominal interest rate.

What happened:

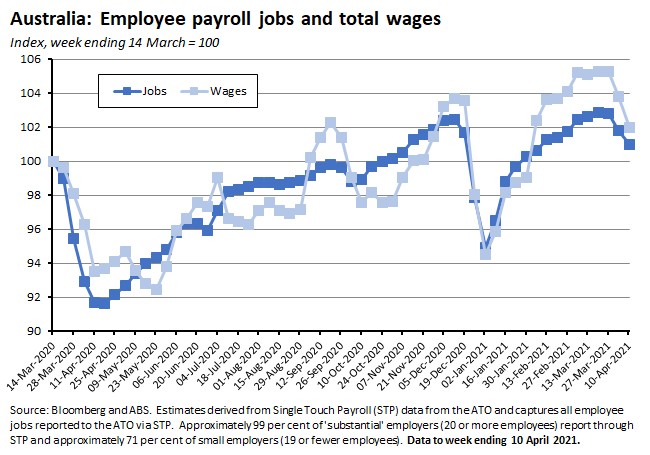

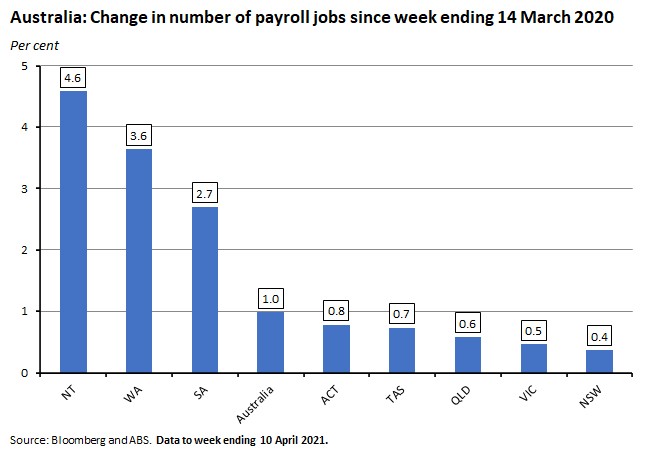

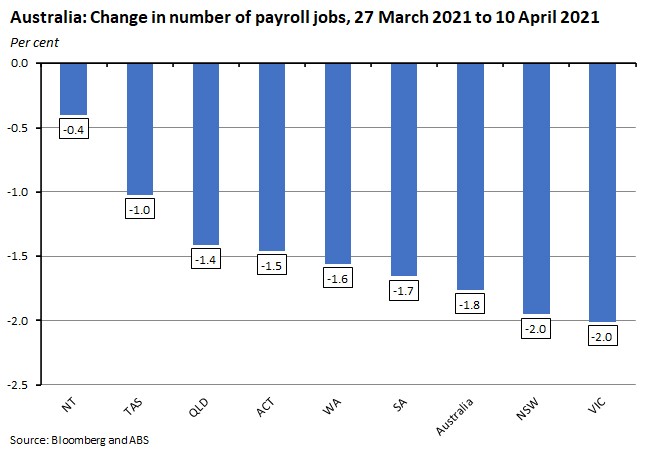

The latest set of weekly payroll jobs data from the ABS showed that in the period between the week ending 14 March 2020 (the week of Australia’s 100th COVID-19 case) and the week ending 10 April 2021, the number of total payroll jobs has increased by one per cent while total wages paid are up two per cent. For the most recent fortnight of data, between the weeks ending 27 March and 10 April 2021, payroll jobs fell by 1.8 per cent compared to an increase of 0.2 per cent in the previous fortnight while total wages paid dropped by 3.1 per cent after rising 0.2 per cent in the previous two weeks.

Over the year to the week ending 11 April 2021, payroll jobs are now up by 10.2 per cent.

By state, the biggest gains in the number of payroll jobs since the onset of the pandemic are in the Northern Territory (up 4.6 per cent), Western Australia (up 3.6 per cent) and South Australia (up 2.7 per cent). The smallest gains are in Victoria (up 0.5 per cent) and New South Wales (up 0.4 per cent).

Over the most recent fortnight of data, the number of payroll jobs fell in every state and territory, with the biggest declines coming in New South Wales and Victoria (both down two per cent) followed by South Australia (down 1.7 per cent) and Western Australia (down 1.6 per cent).

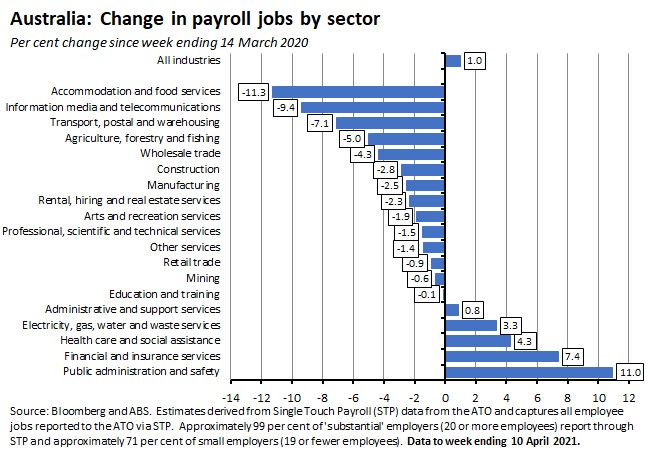

By industry, the number of payroll jobs since the onset of COVID-19 is now markedly higher in public administration and safety (up 11 per cent) and in financial and insurance services (up 7.4 per cent) and has also increased in health care and social assistance, in utilities, and in administrative and support services. In all other industries job numbers are still below where they were in the week ending 14 March 2020, with the largest shortfalls in accommodation and food services (down 11.3 per cent), information, media and telecommunications (down 9.4 per cent) and transport, postal and warehousing (down 7.1 per cent).

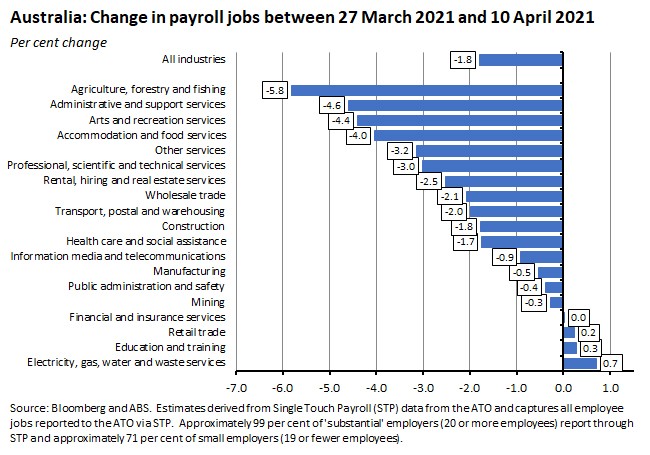

Over the most recent fortnight of data, payroll jobs numbers fell in all but four industries with some of the steepest declines suffered by administrative and support services (down 4.6 per cent), arts and recreation services (down 4.4 per cent) and accommodation and food services (down four per cent).

Why it matters:

With the JobKeeper program ending on 28 March 2021, the latest set of payroll numbers offer the first opportunity to assess the implications for the labour market. And at first glance, they suggest that there has been quite a significant one: job numbers are down 1.8 per cent over the fortnight between the week ending 27 March and the week ending 10 April this year, and the number of jobs fell in every state and across most industries.

There is, however, an important caveat. As we’ve noted before, as a new series the payroll jobs numbers come with several important shortcomings. One of these is that they are not seasonally adjusted (which the ABS says generally requires at least three years of data). And in this case, this is particularly significant because the Bureau notes that:

“The latest fortnight included the Easter holiday period which regularly sees a seasonal fall in a range of labour market indicators, especially hours worked. These seasonal factors make it difficult to gauge any effect of the end of the JobKeeper wage subsidy on 28 March. The next fortnight of data (available on 11 May) should provide a better sense of the state of the labour market after JobKeeper.”

In other words, the lack of seasonal adjustment means that it is difficult to distinguish between a fall in job numbers in response to the end of JobKeeper and a fall due to regular, seasonal declines in labour market activity. That means that we now have to wait for the next payroll jobs data release – and the April labour market report – to get a clearer signal on the JobKeeper story.

What happened:

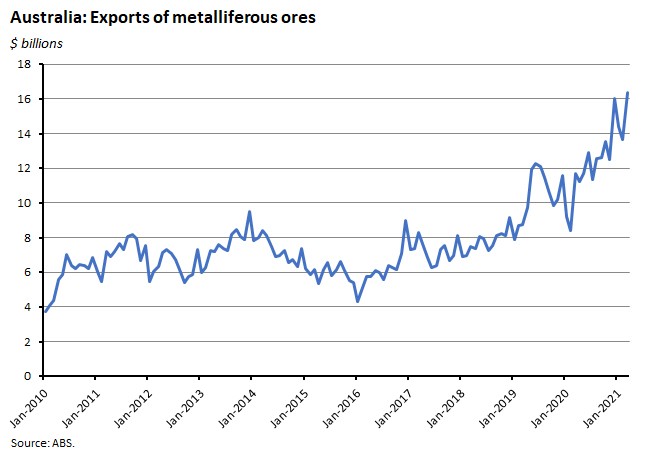

The ABS said that preliminary estimates of merchandise trade showed goods exports in March increasing by 15 per cent to $36.3 billion and goods imports likewise up 15 per cent to $27.7 billion, implying a goods trade surplus of around $8.5 billion (original basis).

Exports of metalliferous ores reached a record high of $16.4 billion last month, driven by strong growth in exports of iron ore and copper ore.

Why it matters:

The details of the March trade numbers tell several interesting stories.

- First, iron ore continues to underpin Australia’s overall export performance, with sales hitting a record $14 billion in March (up 21 per cent) and accounting for 39 per cent of all goods exports in the month.

- Likewise, and as our leading iron ore market closely related, China still dominates our export profile.Exports were up 17 per cent over the month, accounting for almost 42 per cent of the increase in export values in March month and 37 per cent of total exports.

- Exports of copper rose even faster in percentage terms than exports of iron ore, up by 62 per cent to $745 billion, marking their third highest monthly total on record.The ABS also noted that March was the second month on record that Australian copper ore fetched a unit value above $4.50kg, adding that the recent price strength is demand driven, reflecting the copper-intensity of green technologies.

- On the import side of the trade account, road vehicle imports hit another record high in March, their second since December 2020. The increase was led by major diesel vehicle categories along with a rise in imports of hybrid vehicles.

- Imports of electrical machinery also reached a record high last month, led by an increase in assembled solar arrays and solar cells.

- Vaccines increased 101 per cent to their highest value on record, the majority made up of seasonal flu vaccines and some COVID-19 vaccines.

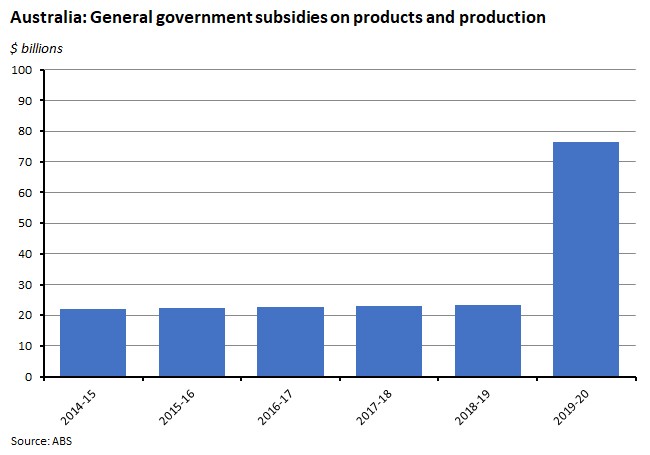

What happened:

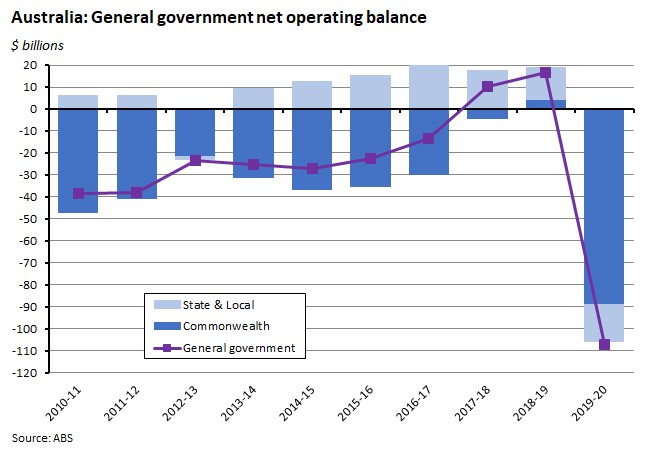

The ABS published Government Finance Statistics (GFS) for the 2019-20 financial year. The general government net operating balance fell from a surplus of $16.6 billion in 2018-19 to a deficit of $107 billion in 2019-20. That overall shift comprised a fall in the Commonwealth general government net operating balance from a surplus of $4.3 billion in 2018-19 to a deficit of $89.1 billion in 2019-20 and a decline in the net operating balance for all of Australia state and local general government from a surplus of $14.8 billion to a deficit of $16.9 billion over the same period.

The GFS net acquisition of financial assets was $43.6 billion in 2019-20, and the overall GFS net borrowing requirement for the general government was $150.5 billion. Add in the rest of the non-financial public sector, and the operating deficit in 2019-20 increases to $115.8 billion for the whole public sector while the overall net borrowing requirement for the public sector rises to $174.7 billion.

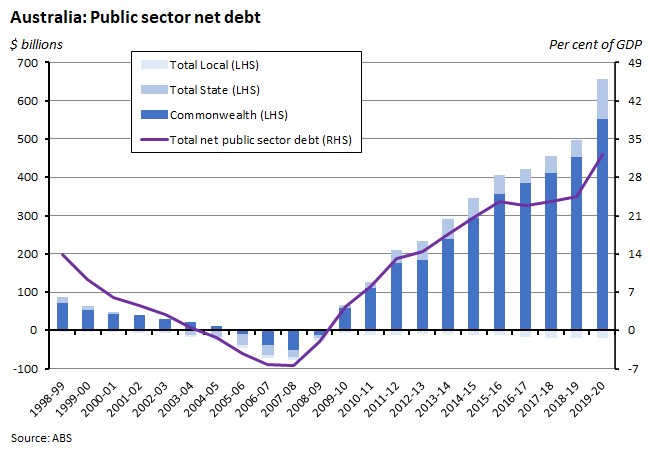

Australian net public sector debt rose to $637.9 billion in 2019-20 reaching a high of 32.1 per cent of GDP. Commonwealth net public sector debt increased by $99.5 billion to $553.4 billion, or 27.9 per cent of GDP and total state net public sector debt increased $59.6 billion to $101.3 billion or a bit more than five per cent of GDP.

Why it matters:

The impact of the pandemic and the combined fiscal response by the Australian federal and state government is apparent in the big swing in the general government operating balance described above.

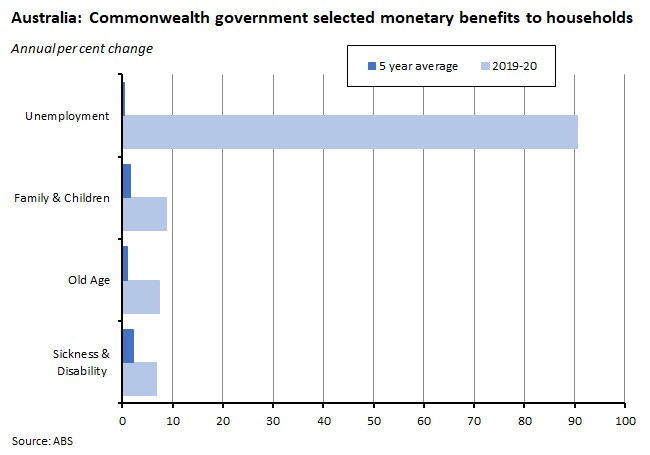

The Commonwealth government drove the lion’s share of the swing in the overall government financial accounts as it ramped up fiscal support. For example, the ABS reports that monetary transfers to households increased significantly in 2019-20, rising to record levels due to increased numbers of people on income support programs such as JobSeeker plus additional payments for eligible individuals to assist with the impacts of COVID-19. As a result, Commonwealth general government monetary transfers to households rose to $144.7 billion in 2019-20, up from $125.3 billion in 2018-19.

At the same time, the Commonwealth also ramped up its support for Australian businesses via the introduction of a number of subsidies on products and production programs of which the two largest were JobKeeper and Boosting Cash Flow for Employers. State and territory governments also introduced a number of subsidy programs, including Business Support Funds and electricity rebates for small and medium enterprises to help businesses impacted by COVID-19. As a result, the ABS estimates that all general government subsidies on products and production rose to record levels, reaching $76.5 billion in 2019-20, up from $23.3 billion in 2018-19. Commonwealth general government subsidies on products and production increased by $50.6 billion, from just below $13 billion in 2018-19 to $63.6 billion 2019-20. JobKeeper payments accounted for $35 billion of this total and Boosting Cash Flow for Employers a further $14.6 billion. At the same time, Australia state and local subsidies on products and production increased by $2.6 billion to $12.9 billion in 2019-20.

(By way of background on GFS methodology, the GFS provides details of revenues, expenses, cash flows and assets and liabilities of the Australian public sector and comprises units which are owned and/or controlled by the Commonwealth, state and local governments. The GFS net operating balance is the difference between GFS revenues and GFS expenses and is equivalent to the change in net worth arising from government transactions. GFS revenues are broadly defined as transactions that increase net worth and GFS expenses as transactions that decrease net worth. Net acquisition of non-financial assets equals gross fixed capital formation, less depreciation, plus changes in inventories plus other transactions in non-financial assets. GFS net lending/borrowing measures the financing requirement of the government and is calculated as the net operating balance less the net acquisition of non-financial assets. A positive value reflects a net lending position, and a negative result reflects a net borrowing position.)

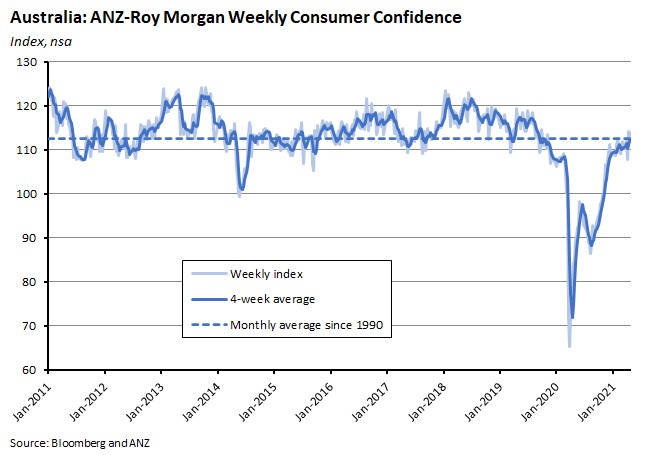

What happened:

The ANZ Roy Morgan weekly index of consumer confidence fell 1.4 per cent over the week to 24-25 April 2021.

Three out of the five subindices fell: ‘current economic conditions’ declined 2.1 per cent, ‘future economic conditions’ dropped 4.1 per cent, and ‘future financial conditions’ was down 2.1 per cent. ‘Current financial conditions’ rose 0.5 per cent and ‘time to buy a major item’ increased 0.9 per cent.

Why it matters:

ANZ pointed to the impact of the three-day lockdown of the Perth and Peel region as the most important driver of the decline in consumer confidence. Confidence in Perth fell 8.2 per cent over the week, although there were also smaller falls in Brisbane (down 4.9 per cent), Melbourne (down 4.4 per cent) and Sydney (down 3.6 per cent).

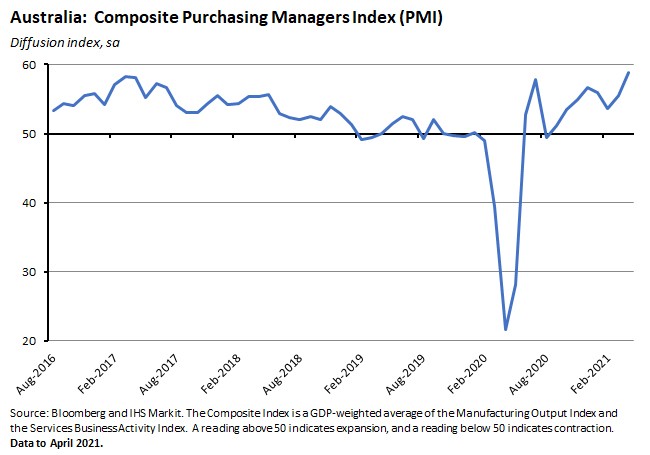

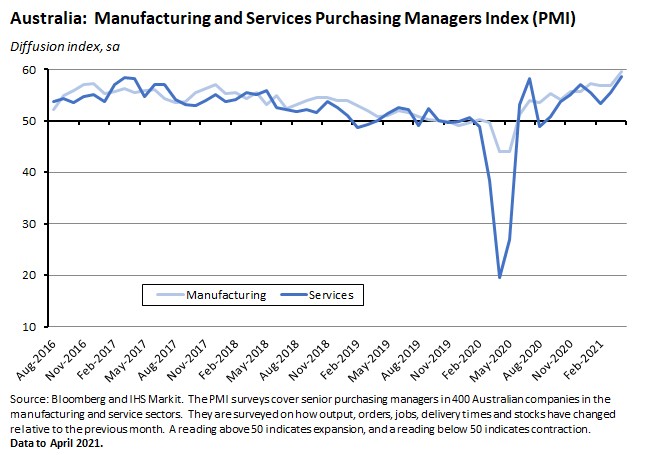

What happened:

Last Friday, the IHS Markit Flash Composite Output PMI (pdf) rose to 58.8 in April from 55.5 in March.

The Flash Services PMI rose to 58.6 in April from 55.5 in March while the Manufacturing PMI was up to 59.6 in April from 56.8 in March.

Why it matters:

The April 2021 increase in the PMI was the steepest rate of expansion in private sector activity in the history of the survey (which runs back to May 2016) and suggests that the second quarter got off to a strong start. According to IHS Markit, ‘the upturn was associated with improved client confidence, buoyant market conditions, strengthening demand, the easing of COVID-19 restrictions and low interest rates.’ At the same time, both the services and manufacturing PMIs also hit record highs in April. The survey results also reflect continued disruption to supply chains, which are creating some inflationary pressures: two more records set in the April results were for the steepest increases in input costs and in selling charges since the survey began.

What happened:

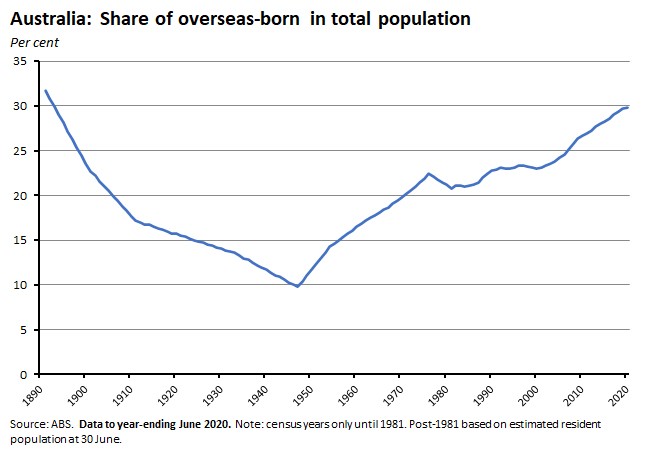

Last Friday, the ABS released new data on migration for the year ending 30 June 2020.

According to the Bureau, in 2020 there were more than 7.6 million migrants living in Australia, or 29.8 per cent of the population. This was up slightly from the 7.5 million people born overseas in 2019.

People born in England continued to be the largest group of overseas-born residents, accounting for 3.8 per cent of Australia's total population (980,400 people), followed by residents from India (2.8 per cent or 721,000), China (2.5 per cent, 650,600), New Zealand (2.2 per cent, 565,000) and the Philippines (1.2 per cent, 310,000).

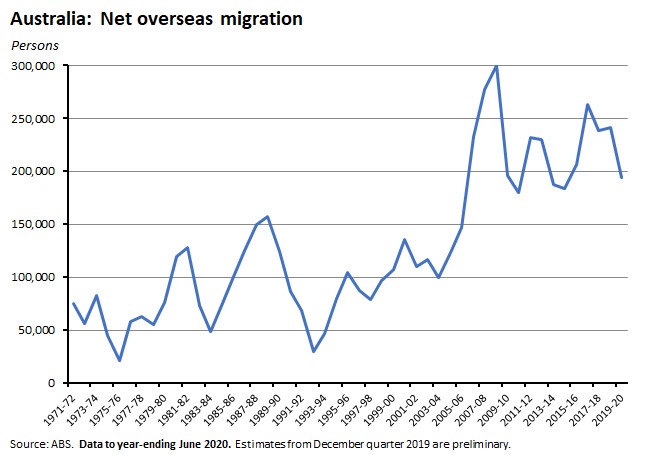

In terms of people flows, net overseas migration in the year ending 30 June 2020 was 194,400 people, comprising 509,600 arrivals and 315,200 departures. That was down almost 47,000 relative to 2018-19.

Why it matters:

As we’ve noted before, net overseas migration plays a critical role in driving overall population growth in Australia and in shaping population demographics. The impact of COVID-19 and the subsequent restrictions on international travel have had a dramatic impact on people flows and (therefore) future demographic projections. With this data release only covering the 2019-20 year, it only partially captures the effect of the pandemic. Still, the disruption to international migration flows is apparent: overseas migrant arrivals were down by 40,800 on 2018-19 while the more than 315,000 people who left Australia to live overseas represented the most departures ever recorded. At the same time, there were also a record number – 99,000 – of Australian citizens returning home.

. . . and what I’ve been following in the global economy

What happened:

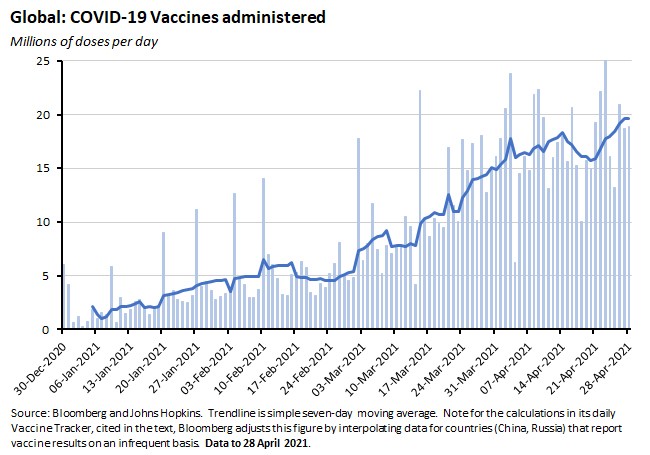

The Bloomberg vaccine tracker reported that more than one billion doses of COVID-19 vaccine have now been administered across 172 countries – enough to vaccinate approximately 7.1 per cent of the global population.

The average daily vaccination rate is now running at a bit below 20.3 million doses per day. At this rate it would take another 17 months to cover 75 per cent of the world’s population.

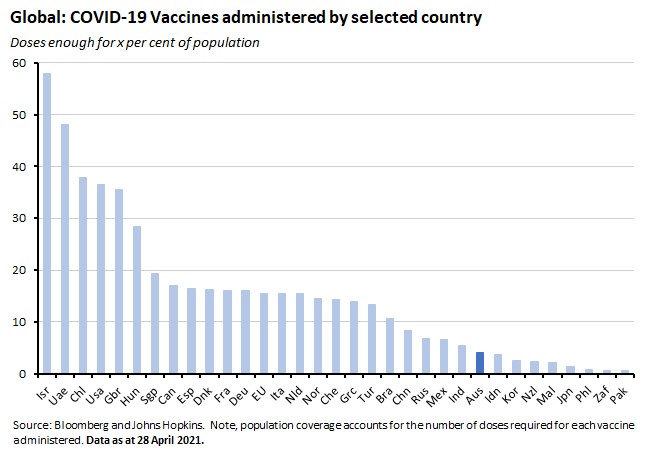

The distribution of vaccines across the world economy remains highly uneven, with high income economies being vaccinated at a rate that is roughly 25 times faster than low income ones. Small island polities such as the Seychelles (enough vaccines administered to cover 64 per cent of the population) and the Maldives (52 per cent) are doing well, as are some smaller economies including Israel (57.9 per cent) and the UAE (48.1 per cent). The United States is also performing strongly in terms of the vaccine rollout, having administered enough doses to cover 36.5 per cent of its people, closely followed by the UK (35.6 per cent). But coverage is much lower in many poorer economies across the globe.

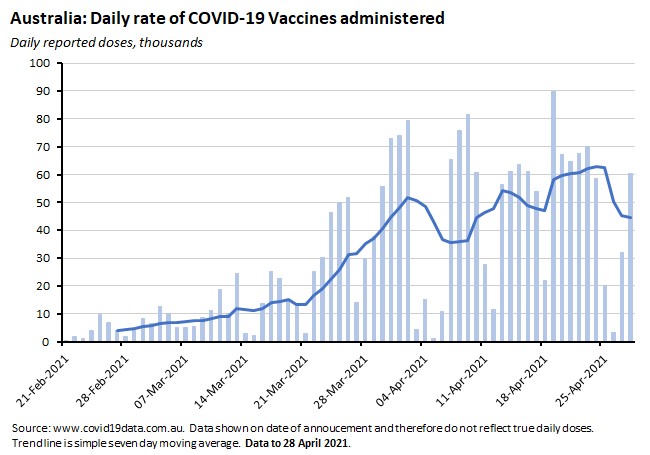

Here in Australia, vaccine trackers are reporting that the current seven day rolling average rate of vaccination is running at around 44.5 thousand doses. At this rate, it would take another 32 months to administer a target of 45 million doses.

Why it matters:

The assumption of a successful global vaccine rollout underpins the outlook for the world economy and the same ‘good news-bad news’ pattern on this front continues to unfold. The good news is that the worldwide pace of vaccine administration is still ramping up and as a result, the estimated ‘time to vaccinate’ keeps falling: a couple of weeks ago the estimate stood at 19 months and now it’s down to 17. The bad news is that there remains a considerable gap in country performance, and in particular (although certainly not exclusively) between richer and poorer economies.

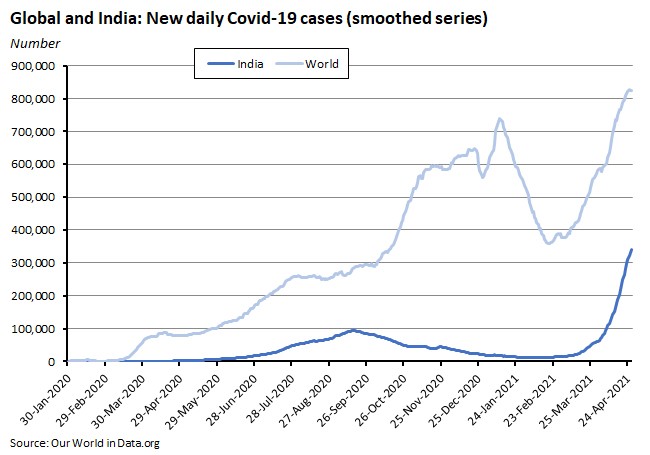

The importance of the latter effect has been reinforced by the dramatic surge in the number of COVID-19 cases in India, which has helped drive global daily infection rates to new highs.

What happened:

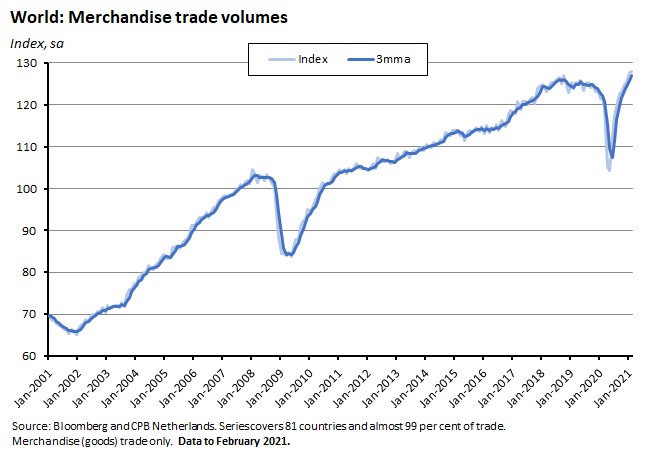

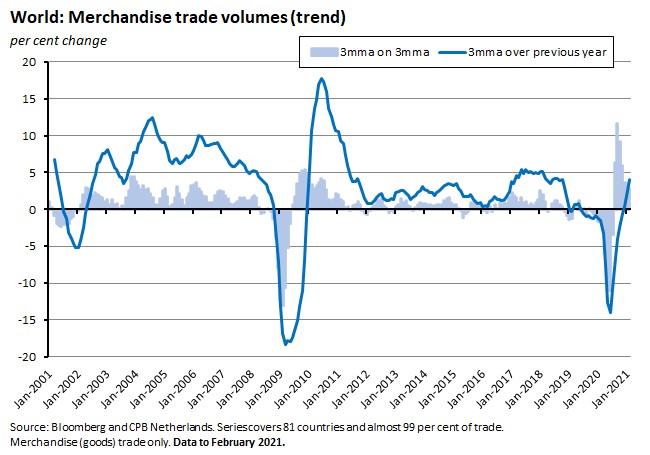

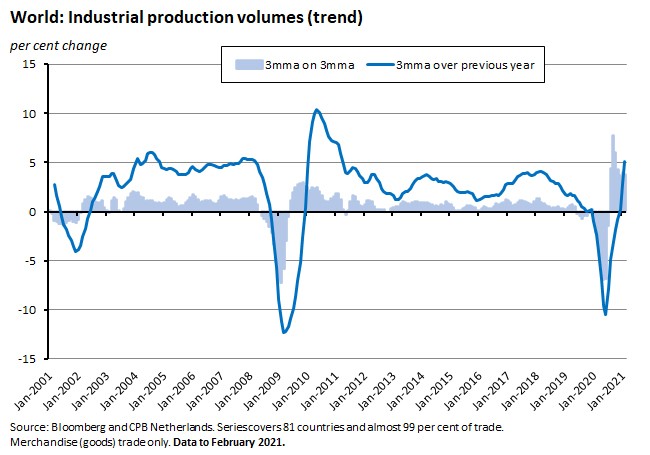

The CPB World Trade Monitor (pdf) said that world trade volumes rose 0.3 per cent month on month in February 2021 to be up 5.3 per cent over the year.

World trade momentum eased to 2.9 per cent in February from 3.5 per cent in January. (Momentum is measured by the CPB as the average of the three months up to the report month over the average of the preceding three months.)

According to the same release, world industrial production fell 0.3 per cent month on month in February although the CPB’s momentum measure rose 3.7 per cent.

Why it matters:

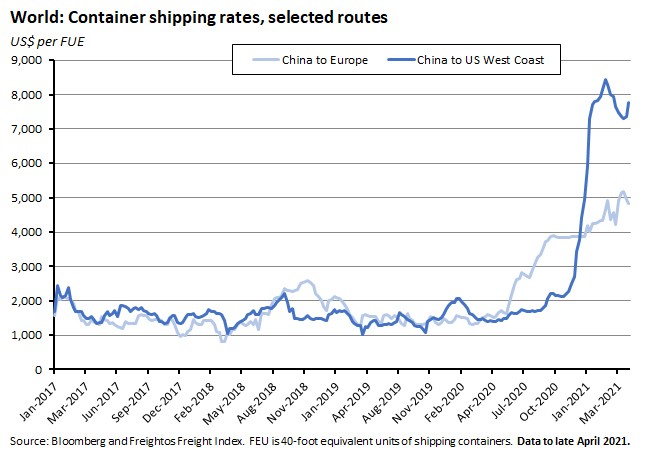

After taking a hard hit early in the pandemic, merchandise trade flows and industrial production have both staged a robust recovery. And while actual data on global trade flows come with a significant lag, the strong results from global PMI surveys (we covered the March global composite PMI results a couple of weeks ago) have been consistent with an ongoing recovery. Likewise, the latest official forecasts from the IMF see world trade volumes (goods and services) rebounding by 8.4 per cent this year after contracting 8.5 per cent in 2020 while the WTO expects world merchandise trade to increase eight per cent this year. Media reports also suggest that cargoes delayed by the grounding of the Ever Given in the Suez canal are now arriving in global ports, although the consequent surge in container traffic is placing additional pressure on already-stressed supply chains. As a result, shipping rates remain elevated.

What I’ve been reading . . .

- Treasury released two new working papers looking at aspects of the Australian labour market. One presents new estimates of the Non-Accelerating Inflation Rate of Unemployment (NAIRU) in Australia. Treasury’s previous estimate put the NAIRU at around five per cent, but now new estimates suggest it had fallen to between 4.5 per cent and five per cent in the years prior to the COVID recession. The other looks at historical trends and future prospects for Australian labour force participation. It tracks the rise in the aggregate participation rate from around 60 per cent in 1983 to almost 66 per cent in 2011 as well as the diverging patterns of male (falling) and female (rising) participation that sit behind it. It also highlights a significant shift from full-time to part-time participation over several decades for young males and females (although recent data suggests that this might now be stabilising), a shift to part-time participation for prime age males and rising full-time and part-time participation for prime age females.

- The Parliamentary Budget Office (PBO) has published a new report on fiscal sustainability (pdf). The PBO’s starting point is the observation that Commonwealth government gross debt has increased from 28 per cent of GDP before the pandemic to more than 40 per cent of GDP in 2020-21 and is expected to rise to more than 50 per cent of GDP in 2022-23 and then stay there for much of the next decade. Based on these projections (which are likely to be adjusted after next month’s budget) the report considers three drivers of the debt-to-GDP ratio: economic growth, interest rates and the budget balance. It then analyses a range of scenarios. In what is good news for sustainability, it concludes that ‘Only the highly unlikely scenario of a generation of low economic growth combined with high interest rates and large budget deficits results in debt increasing as a share of GDP, after 2050.’ But it also judges that ‘Reducing the government debt-to-GDP ratio to pre-pandemic levels will take decades, even under relatively optimistic scenarios.’ Still, debt servicing costs are nevertheless expected to remain modest ‘as the existing debt was borrowed at historically low interest rates.’

- Roger Wilkins of the Melbourne Institute of Applied Economic and Social Research warns that Australia’s unemployment rate could head back above seven per cent in coming months. As well as the ending of JobKeeper in March, Wilkins thinks that the tightening of requirements around JobSeeker could increase the labour supply. This effect would also manifest in a shrinking of the large gap between the number of unemployed and the number of JobSeeker claimants that opened up at the start of the pandemic (discussed in last week’s note).

- Philip Adams from the Victoria University Centre of Policy Studies reckons that the impact on the Australian economy of an EU carbon tariff would be fairly modest as the EU is not a large market for most Australian exports, with the partial exception of coal: he cites estimates of a long-run projected loss in GDP of 0.05 per cent or equivalent to about one weeks’ worth of normal growth. The same modelling suggests that the main loser would be the coal industry, which could see production down 3.8 per cent at the cost of about 3,000 jobs.

- DFAT Secretary Frances Adamson’s speech to the Asia Society: ‘Australian leaders and policy makers are navigating a new and immensely challenging period in the Indo-Pacific. Geostrategic competition between major powers … is focused increasingly on the stability and character of the regional order in the Indo-Pacific. Pressure on rules, norms and institutions is more acute, and tensions over territorial claims are escalating. The deployment of new threats like cyber-attacks and foreign interference is growing in frequency and sophistication.’

- APRA has released new guidance on managing the financial risks of climate change.

- From ABC Business, the number of home and small business loan deferrals has dropped to less than 5,000 from a peak of 854,606 by the end of last month. According to data from the Australian Banking Association, there were just 3,170 home loans with the big four banks and Suncorp still deferred by the end of March, down from a peak of 468,786 of total deferrals requested throughout the pandemic. That means only 0.7 per cent of the home loans originally deferred were still on mortgage holidays when those programs officially ended on March 31. The decline in business loan deferrals was even sharper, with only 508 on hold by March 31, compared to peak levels of 235,440, implying just 0.2 per cent remained deferred.

- Also from the ABC, Ian Verrender on the gap between government and corporate action on climate change.

- Deloitte on reshaping our cities and regions to drive a COVID recovery.

- A new Lowy Institute Analysis from Richard McGregor and Jude Blanchette looks at future scenarios for leadership succession in a post Xi Jinping China. The authors argue that ‘by removing de jure and de facto term limits on the most senior position of power, and thus far refusing to nominate his successor, Xi has solidified his own leadership position but potentially pushed the country towards a destabilising succession crisis.’ They discuss four possible scenarios: (1) An orderly transition in 2022; (2) a succession plan to retire at the 21st Party Congress in 2027 or the 22nd Party Congress in 2032; (3) A leadership challenge or coup; and (4) Unexpected death or incapacitation.

- The WSJ on how India’s COVID-19 agonies highlight a growing gap in vaccinations between rich and poor countries.

- Related, Martin Wolf in the FT on why rich countries need to focus on the policy challenges of a divided world.

- A long – and sceptical – essay on cryptocurrency.

- The OECD focuses on the prospects for a green recovery. It estimates that, to date, OECD member economies and some key partners have together announced US$366 billion of ‘environmentally positive’ measures as part of their COVID-19 recovery packages, or about 17 per cent of total spending. The OECD also estimates that this sum ‘is close to evenly matched by non-green measures (those with negative or “mixed” environmental impacts), for those measures that have a monetary value.’

- Two blog posts from the IMF. The first one looks at the debate over the implications of high public debt. And the second seeks to understand the recent rise in long-term interest rates.

- The Economist on the lessons from history about post-pandemic booms. This piece argues that the historical record ‘suggests that, following periods of massive non-financial disruption such as wars and pandemics, GDP does tend to bounce back. But it offers three further lessons. First, while people are keen to get out and spend, uncertainty lingers for some time. Second, the pandemic encourages people and businesses to try new ways of doing things, upending the structure of the economy. Third…political upheaval often follows, with unpredictable economic consequences.’ Or, put a bit differently: Post-pandemic, people save, then spend; firms look to technological change, especially labour-saving innovation; and the focus of politics tends to shift towards labour and away from capital.

- Related, a VoxEu column on inflation in the aftermath of wars and pandemics. The authors argue that while wars tend to result in higher inflation and higher bond yields, the same is not true of pandemics, where historical experience indicates that they are often followed by weaker inflation and falling bond yields.

- Also from VoxEU: new estimates suggest that at the height of the pandemic last year (in Q2:2020) about 557 million people (17 per cent of global employment) worked from home.

- This Zach Carter profile of the great Cambridge economist Joan Robinson in the NYT has attracted a fair bit of attention in the economic Twittersphere. It focuses on her path-breaking work on the economics of imperfect competition and that concept’s return to policy prominence in recent debates.

- Related, the Hexapodia podcast takes on the Cambridge Capital Controversy. In terms of appetite for the debate itself, I have to admit to a bit of nostalgia as it brought to mind first year undergrad economic history lectures from Geoff Harcourt – something I haven’t recalled for many years. But the conversation does move on to a discussion of approaches to modern macro and the role of models, which will be more interesting to those who don’t have those particular recollections.

Latest news

Already a member?

Login to view this content