According to the monthly NAB survey, business conditions hit a record high in March, underpinned by record highs for trading conditions, profitability and employment. In March Labour Force figures announced by the ABS yesterday, the unemployment rate fell from 5.8 per cent in February to 5.6 per cent in March, while an extra 70,700 people found work since February, taking the number of people with a job to 13.08 million, a new record high.

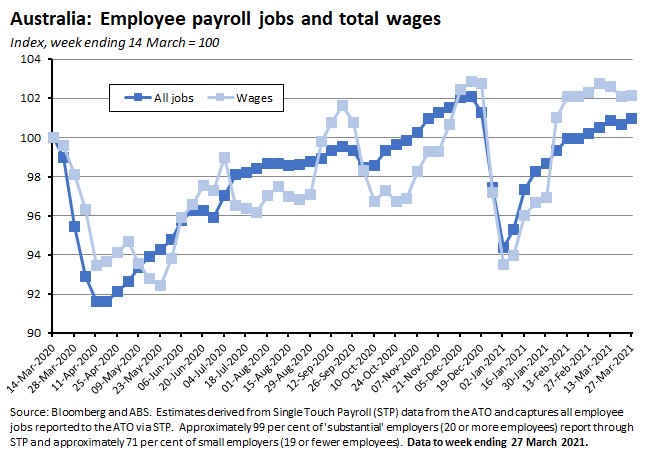

The number of payroll jobs in the week ending 27 March 2021 was one per cent higher than in the week ending 14 March 2020, when Australia recorded its 100th COVID-19 case. The latest RBA Financial Stability Report judged that both the Australian and global financial systems have proved resilient in the face of the COVID-19 shock and is sanguine about rising house prices. According to the Bloomberg Vaccine tracker, more than 814 million doses of vaccine have now been administered across 152 countries putting the world on track to have vaccinated 75 per cent of the global population in another 19 months. The J P Morgan Global Composite PMI rose to a 79-month high in March, posting one of its strongest readings over the past decade.

This week’s readings include the COVID recovery in Australia, change at the RBA, housing market policies, how to achieve net zero emissions for the national electricity market, the shrinking global middle class, the future of work, an economic biography of Janet Yellen and Mario Draghi, rising input prices and inflationary pressures, Bidenomics, how China lends, and the legacy of Milton Friedman.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

In March Labour Force figures announced by the ABS yesterday, the unemployment rate fell from 5.8 per cent in February to 5.6 per cent in March, while the participation rate rose to 66.3 per cent from 66.1 per cent in February. Unemployment is now 0.4 of a percentage point higher than it was before the COVID-19 pandemic was declared last year. The numbers relate to employment over the first two weeks of March, before JobKeeper ended. An extra 70,700 people have found work since February, taking the number of people with a job to a record 13.08 million, a new record high. The figures will be analysed in detail next week.

What happened:

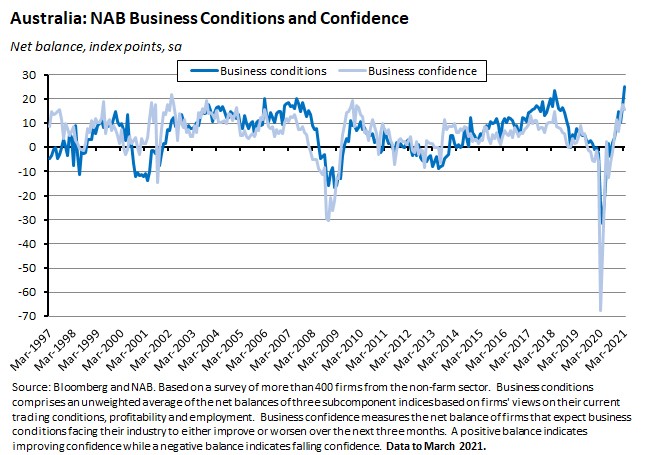

The monthly NAB Business Conditions Index rose eight points to a record +25 index points in March while Business Confidence fell three points to +15 index points.

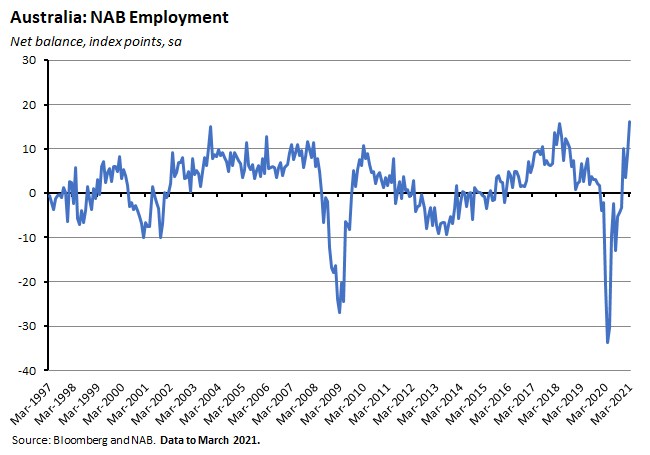

The rise in conditions was broad-based across all states and industries, and across all three index subcomponents: trading conditions (up 12 points), profitability (up eight points) and employment (up seven points) all rose to record highs in March.

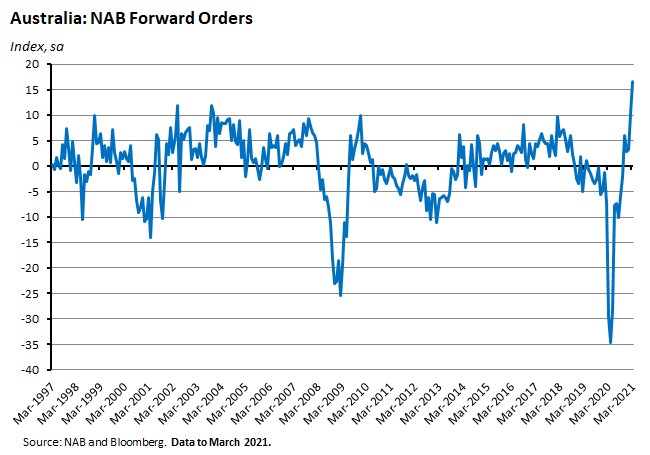

While business confidence did edge lower over the month, other forward-looking indicators sent strong positive signals. Forward orders rose seven points to a record high +17 index points.

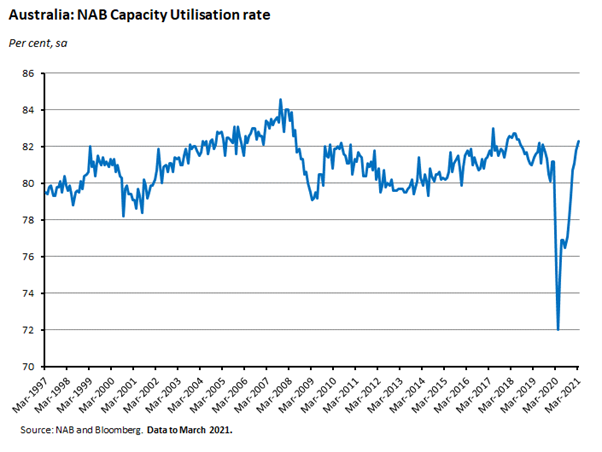

And capacity utilisation rose from 81.8 per cent in February to 82.3 per cent in March.

Why it matters:

Despite the drop in business confidence – which nevertheless remained well-above its long-run average – this was an extremely strong survey result, with record highs not only for business conditions, but also for all three subcomponents of that index as well as for forward orders.

Together with another healthy result for capacity utilisation, the March report tells the story of a strong recovery in business activity as the economy completed the first quarter of this year. The positive survey reading on employment – consistent with the stories told by vacancies and job ad numbers described last week as well as the latest payroll numbers (below) – is also welcome news before the impact of the end of labour market support from the JobKeeper program, which concluded on 28 March, starts to appear in the data.

What happened:

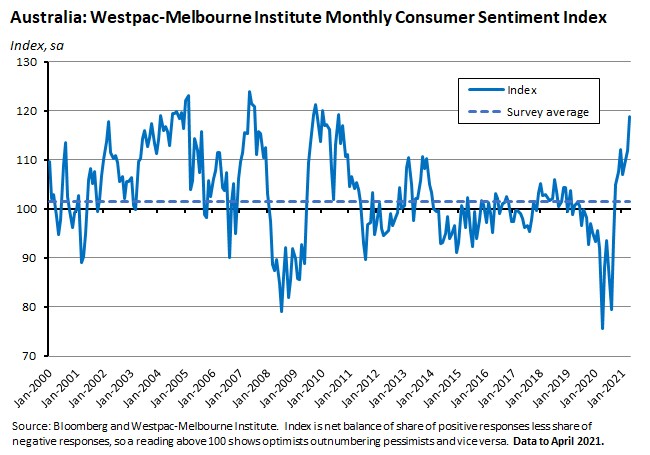

The monthly Westpac-Melbourne Institute Index of Consumer Sentiment (pdf) jumped 6.2 per cent to an index level of 118.8 in April from 111.8 in March.

Confidence increased in four of the five index subcomponents: ‘family finances vs a year ago’ soared 13.4 per cent, ‘family finances next 12 months’ rose by a healthy 5.4 per cent, ‘economic conditions next 12 months’ jumped by 10.3 per cent, and ‘economic conditions next five years’ was up 4.1 per cent. The only subcomponent to register a modest fall in April was ‘time to buy a major household item’ which edged lower by 0.2 per cent over the month.

Separately, the Westpac-Melbourne Institute Index of Unemployment Expectations increased by 5.6 per cent in April (an increase indicates that more respondents expected the unemployment rate to rise). Westpac noted that the unemployment index appears to have bottomed out and is now 11.4 per cent above its low in December last year.

On the housing market, the ‘time to buy a dwelling’ index fell by 7.9 per cent from 116.4 in March to 107.2 in April. It is now 18.8 per cent below its November high, suggesting that rise prices are now taking a toll on affordability. The Westpac Melbourne Institute Index of House Price Expectations rose by 2.7 per cent in April to be eight per cent above its pre-pandemic level. The national index is now at its highest level since December 2013 and only 1.6 per cent off that previous peak.

Why it matters:

In what the accompanying Westpac release described as ‘an extraordinary result’ the monthly consumer sentiment index is now at its highest level since August 2010, a time when the economy was enjoying a post-GFC rebound and another phase of the mining boom.

As the commentary notes, this increase comes despite a series of developments that might otherwise have been expected to dent household confidence: the survey was conducted in the week following the end of the JobKeeper program, there had been disappointing news on the pace of Australia’s vaccine rollout, and there had been a series of media reports around potential rare but serious health risks associated with the AstraZeneca vaccine, culminating in advice against giving the vaccine to the under-50s. Yet sentiment was robust in the face of all of this, suggesting that the ongoing strength of Australia’s economic recovery continues to boost household confidence in a way that more than offsets other concerns. That is an interpretation that is also consistent with the latest weekly confidence numbers discussed below.

While the resilience of household sentiment is the key message from April’s result, there were a couple of other points worth noting too. First, and despite the overall sense of optimism, respondents do appear to have become slightly more pessimistic about the outlook for the labour market post-JobKeeper. And second, expectations for house prices continue to rise.

What happened:

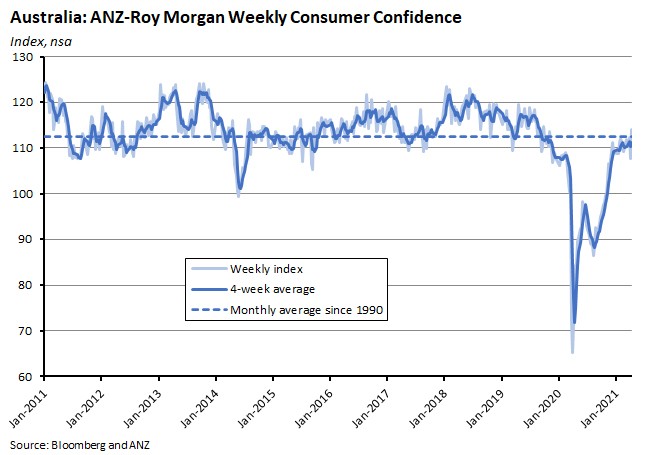

The weekly ANZ-Roy Morgan Index of Consumer Confidence rose 5.9 per cent taking the index to 114.1.

All five subindices rose strongly over the week. ‘Current financial conditions’ rose 8.3 per cent, ‘future financial conditions’ were up 4.8 per cent, ‘current economic conditions’ rose 7.1 per cent and ‘future economic conditions’ increased 4.8 per cent. ‘Time to buy a major household item’ was up 5.7 per cent.

Why it matters:

After the previous week’s 4.1 per cent dip following the short Brisbane lockdown, confidence has rebounded to its highest level since September 2019 with the gains led by increased confidence readings in Greater Brisbane and New South Wales. The weekly index is also now back above its long-run average.

ANZ noted that the rise in confidence came despite the problems with Australia’s vaccine rollout and as well as reflecting overall economic conditions may also in part reflect a positive response to the announcement of the trans-Tasman travel bubble.

What happened:

Last Friday, the RBA published the April 2021 Financial Stability Review. Key points:

- Thanks in part to the financial sector reforms prompted by the global financial crisis (GFC), which led to banks holding more high quality liquid assets and more capital, both the Australian and global financial systems have been resilient in the face of the COVID-19 shock.Substantial policy support has also played an important role.

- Overall, the RBA judges that Australia’s banks ‘are in a strong financial position coming out of the pandemic…non-performing loans have increased, but by less than expected, and their current provision balances are expected to be sufficient to absorb the impact of future defaults.’

- In Australia, ‘the vast majority of households and businesses who had deferred loan repayments have now resumed full repayments…some increase in household and business financial stress is likely as temporary support measures progressively end and borrowers deplete financial buffers. Households and businesses that derive their incomes from sectors most heavily affected by the pandemic face an elevated risk of repayment difficulties if their buffers prove to be insufficient. Overall though, the share of heavily indebted households and businesses in this position is small.’

- For example, ‘The share of housing loans (by value) on repayment deferrals at the end of February 2021 had declined to 0.7 per cent, from a peak of 11 per cent in May 2020. Almost all borrowers whose repayment deferral has come to an end – including many who chose to resume payments early – have resumed full repayments and are up to date with their loan schedule.’

- ‘Most households remain in a good position to service their debt given low interest rates and have the additional safety net of large mortgage prepayment buffers. Around half of all mortgages have prepayment buffers equivalent to more than three months' worth of repayments and, for more than one-quarter of loans, the buffer exceeds two years' worth of repayments.’

- Expansionary monetary policy has produced rising asset prices and ‘some appear high relative to their expected future stream of income. However, for most financial and real assets, this lower rate of expected earnings relative to the asset price is broadly consistent with the very low level of interest rates.’

- Housing prices have been one prominent example of this asset price inflation, with demand driven by ‘low interest rates, stimulus payments boosting household income, temporary additional support for first home buyers and the HomeBuilder program.’ But while prices have risen nationally, there have been significant compositional differences: prices in regional areas have increased by 11 per cent over the past year, compared to 5 per cent in the capital cities; price growth has been stronger for detached houses than for units; and rental conditions have also been weak, particularly in Melbourne and in the inner and middle suburbs of Sydney where vacancy rates have increased sharply and rents for units have fallen.Lower population growth and changing preferences are both suppressing the demand for inner city apartments, although this is being offset by a much smaller volume of higher-density inner city apartments due for completion in 2021 relative to previous years.

- In the RBA’s view, lending standards remain robust: the share of high LVR (loan to value ratio) lending has risen but remains low by historical standards, while the share of interest-only lending has been little changed at low levels. The share of lending at high debt-to-income (DTI) ratios has increased.Some of the increase in high LVR lending to owner-occupiers reflects the greater share of first home buyers in market activity.

- Business insolvencies have risen from their mid-2020 lows, with the increase at the very end of last year coinciding with the end of the moratorium on director liability for insolvent trading. The RBA think’s it likely that insolvencies will rise further for some months, despite a better economic backdrop.

- Commercial property exposures, in particular the office and retail property markets, has been affected by the pandemic.The Report notes that impairment rates on commercial property lending remain low, consistent with relatively low LVRs and strong debt covenants leading into pandemic, but the RBA expects them to increase.Vacancy rates continued to rise across most CBD office markets in the December quarter 2020, and in Sydney and Melbourne are currently around their highest levels in about 20 years.Tenant demand for offices is expected to remain weak in the early stages of the economic recovery, with some staff at many businesses continuing to work at least partly from home.

- The Report warned that cyber-attacks are a growing risk for financial stability.

- It also cautioned that ‘Climate change presents an ongoing challenge for the financial system, by exposing it to risks that will rise over time and, if not addressed, could become considerable.’

Why it matters:

Despite the scale of the economic shock created by the pandemic, the Financial Stability Report’s overall judgment is that both the Australian and global financial systems have proved resilient. Lessons learned at the time of the global financial crisis and the subsequent regulatory response meant that the system was better placed to weather COVID-19 than might otherwise have been the case. That said, as government support is wound back, there will be pockets of vulnerability – particular in those sectors most exposed to the adverse impact of the pandemic, and amongst those employed in those sectors. And any setbacks to the global or national economic recoveries will come with additional risks.

In terms of the recent debate on the state of Australia’s housing market, the Report sends the message thar the RBA is relatively relaxed, consistent with the official view as summarised in the previous Weekly. The commentary notes that the central bank remains content with the overall quality of lending and that household balance sheets and finances overall have actually improved over the course of the pandemic as higher household disposable income and a sharp decline in household consumption translated into a boost to the household savings rate. According to the RBA, these higher savings have been used to pay down debt and/or build liquidity buffers, with the aggregate household mortgage debt-to-income ratio declining over the course of 2020, and household deposit balances (including mortgage offset accounts) rising relative to household disposable income.

With no significant concerns raised around either the quality of lending or trends in household indebtedness, for now the RBA is not sending any major warning signals about the housing market in terms of potential adverse implications for either financial or macroeconomic stability.

What happened:

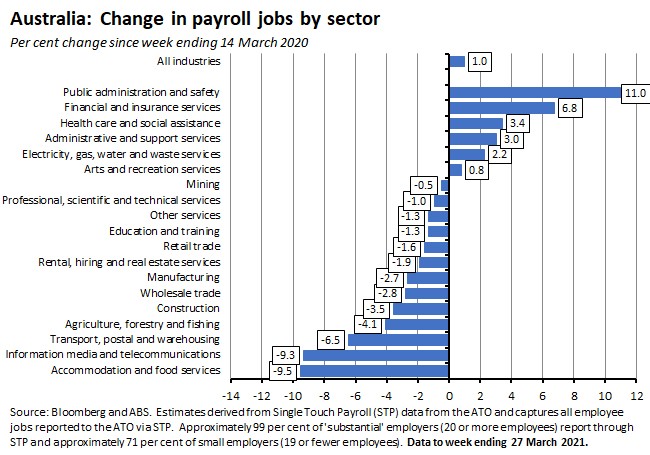

The ABS weekly payroll jobs and wages release showed that between the weeks ending 14 March 2020 (the week of Australia’s 100th case of COVID-19) and 27 March 2021, the number of payroll jobs rose by one per cent and total wages paid increased by 2.1 per cent. Over the most recent fortnight of data, between the weeks ending 13 and 27 March 2021, payroll job numbers increased by 0.1 per cent and total wages paid fell by 0.4 per cent.

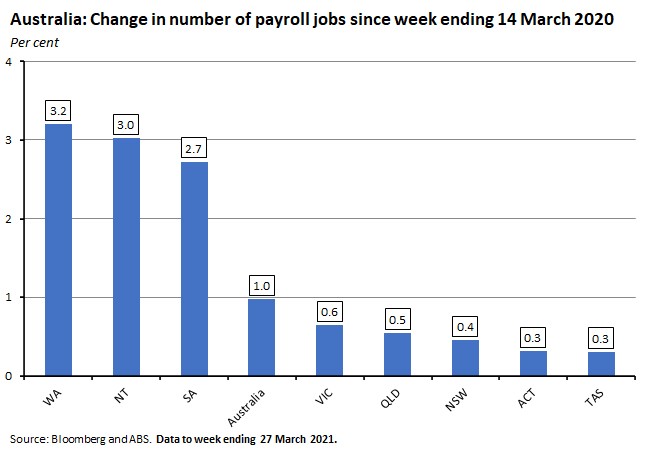

By state and territory, since the week ending 14 March 2020 the change in the number of payroll jobs ranges from increases of 3.2 per cent in Western Australia and three per cent in the Northern Territory to growth of 0.3 per cent in the ACT and Tasmania.

By industry, since the week ending 14 March 2020 the change in the number of payroll jobs ranges from increases of 11 per cent in public administration and safety and 6.8 per cent in financial and insurance services to declines of 9.5 per cent in accommodation and food services and 9.3 per cent in information, media and telecommunications services.

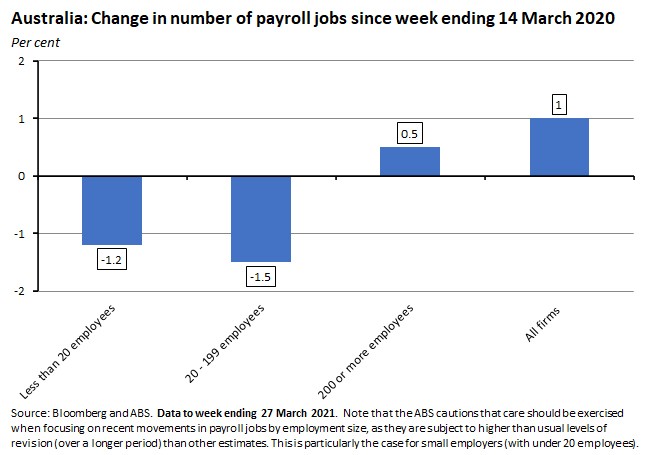

By firm size, the number of payroll jobs is still down in small (less than 20 employees) and medium (between 20 and 199 employees) sized businesses, but employment in large firms (200 or more employees) has increased by 0.5 per cent since the start of the pandemic.

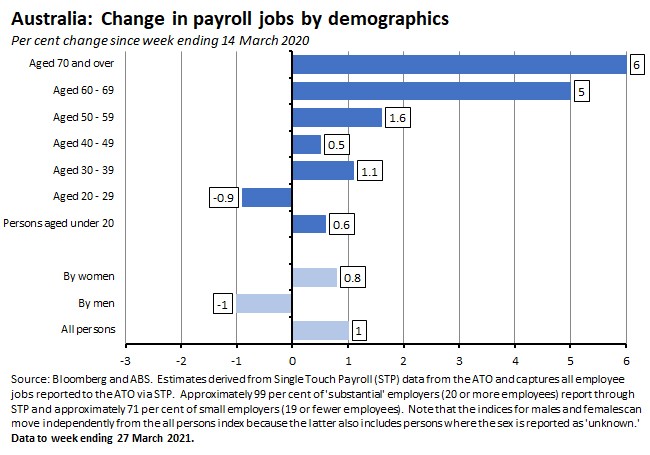

By demographics, since the week ending 14 March 2020 the number of payroll jobs worked by men has fallen by one per cent while the number worked by women has risen 0.8 per cent. By age group, the biggest gain in job numbers over the same period has been for the 70 and over category (up six per cent). In contrast, job numbers for the 20 – 29 age group are still down 0.9 per cent since the onset of the pandemic.

Why it matters:

Although payroll jobs only edged 0.1 per cent higher over the most recent fortnight of data, they were up 0.8 per cent over the month to 27 March 2021. According to the ABS, this rate of increase was similar to the rate of increase seen in the early weeks of March 2020, before the major COVID-19 health restrictions came into effect.

While payroll job numbers overall are now back above the levels prevailing at the start of the pandemic, there is still significant variation by industry with job numbers markedly lower in accommodation and food services and in information, media and telecommunications services. There are also some substantial variations across Australia’s states and territories, although in this case all geographies now have job numbers above those prevailing in the week that Australia reported its 100th case of COVID-19.

Finally, note that the JobKeeper program expired on 28 March this year, and attention will now focus on any flow through to payroll job numbers in April and May.

. . . and what I’ve been following in the global economy

What happened:

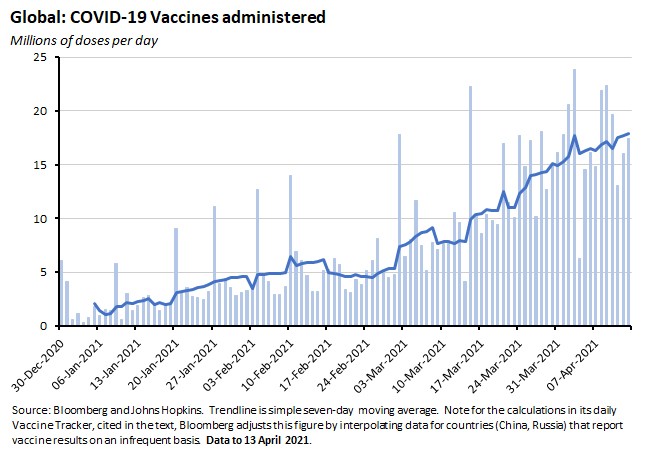

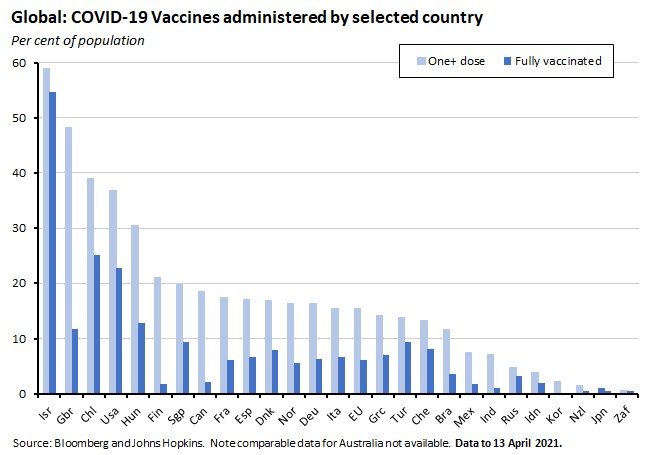

According to data compiled by the Bloomberg Vaccine tracker, as of 13 April 2021, more than 814 million doses of vaccine have now been administered across 152 countries. Globally, the latest vaccination rate is almost 18.3 million doses per day, on average. If this pace were sustained, it would take another 19 months to cover 75 per cent of the world’s population.

Vaccination rates and coverage continue to vary significantly by country ranging, for example, from 54.7 per cent of Israel’s population fully covered to 0.1 per cent for South Korea.

Comparable data for Australia is not available, but according to the ABC’s Australian Vaccine tracker, at the time of writing vaccinations were being carried out at a daily rate of roughly 0.2 doses per 100 people. That’s about 4.5 times slower than in the United States, three times slower than Canada and the UK and half the pace of France and Italy. The ABC notes that at our current pace of roughly 363,000 doses per week, the 40 million doses needed to vaccinate Australia’s adult population would be only achieved by early May 2023.

Why it matters:

As noted in last week’s discussion of the IMF’s new world economic outlook, a key assumption underlying its projections for global growth was that vaccines (and other therapies) would be accessible at affordable prices for all economies, and that this, combined with improved testing and tracing, would see local transmission of COVID-19 running at low levels everywhere by the end of next year. In this context, the positive news is that the global rate of vaccine rollout continues to ramp up: back when we first started reported these numbers in mid-February, the average vaccination daily rate was running at around 6.4 million and the estimated time to vaccinate 75 per cent of the world population was put at almost five years. That rate has now ramped up to a daily rate of 18.3 million and the time to vaccinate has fallen to 19 months. However, this notable global improvement continues to disguise wide variations in country performance.

What happened:

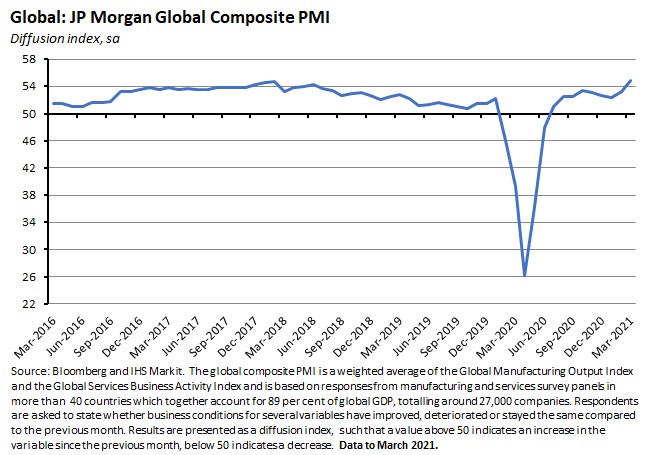

The JP Morgan Global Composite PMI (pdf) rose to 54.8 in March, up from 53.2 in February.

Five out of the six sub-sectors covered by the survey registered expansions during March. The fastest growth was for financial service providers while rates of increase in activity strengthened in the consumer goods, intermediate goods and business services categories. The rate of expansion slowed in the financial services and investment goods industries. Consumer services providers registered another decline in activity, although here the rate of contraction fell to its weakest during the current 14-month downturn.

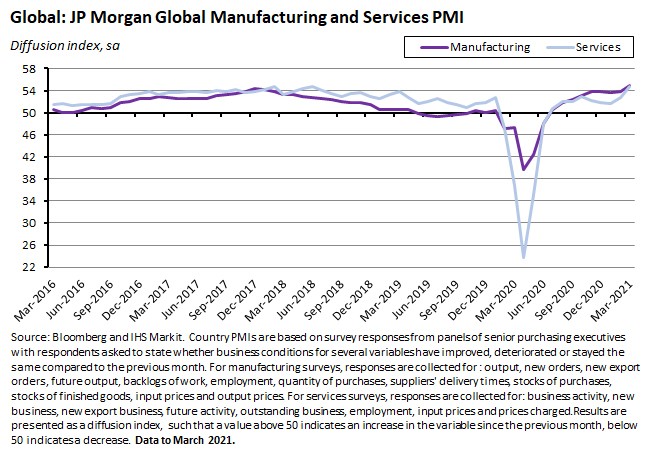

The J P Morgan Global Manufacturing PMI rose to 55 in March from 43.9 in February with operating conditions improving across operating conditions across the consumer, intermediate and investment goods industries, and with PMI readings above 50 (indicating expansion) in 23 of the 27 country surveys that comprised the aggregate March result. The J P Morgan Global Services Business Activity Index rose to 54.7 in March from 52.8 in February.

Why it matters:

The composite index rose to a 79-month high in March, posting one of its strongest readings over the past decade, and has now been in expansionary territory for nine consecutive months, consistent with the story of an ongoing global economic recovery, and one that now includes a large share of services too (albeit with the important exception of consumer services).

Likewise, the global manufacturing PMI rose to a 121-month high in March, its best reading since February 2011, indicating that the manufacturing sector has continued to enjoy a very strong start to this year. Once again, however, the monthly survey results also reported bottlenecks and other supply chain issues, placing significant upward pressure on both input and output prices. For more on this and the potential inflationary impact, see this week’s reading list, below.

What I’ve been reading . . .

- The latest ABS Household Impacts of COVID-19 survey (with a March 2021 reference period) is now available. Findings include that just 14 per cent of Australians reported using public transport in March 2021, down from the 23 per cent who reported regular use before COVID-19 restrictions began in March 2020. About 18 per cent of regular past users of public transport have not used it since the COVID-19 pandemic. There are also results on volunteering and unpaid work, emotional and mental wellbeing and the use of stimulus payments.

- John Edwards on COVID recovery, in Australia and the world.

- Ross Garnaut on historic change at the RBA in a response to Steve Grenville’s earlier piece defending the central bank (included here several weeks back).

- Richard Holden revisits the (politically problematic?) case for abolishing negative gearing while Coates and Mackey aren’t convinced by the idea of using superannuation to address housing affordability (shorter version: since low income Australians have little super, it would mainly help wealthy Australians buy more expensive homes and by increasing demand for housing it would also drive up prices, meaning the real beneficiaries from the policy would be existing home owners). Both columns also make the case for increasing housing supply.

- Deloitte Access Economics on Australia’s business outlook.

- Grattan have released a new report on how Australia can achieve a net-zero carbon emissions electricity system without threatening affordability or reliability of supply. The report argues three key points. First, that Australian can move to 70 per cent renewables across the National Electricity Market (NEM) with little risk to reliability or affordability, and that while going further and achieving 90 per cent renewables would be somewhat more expensive, it would still slash emissions at a relatively low cost. Second, that as the share of renewables increases, so too does the value of inter-regional transmission and an interconnected NEM to ensure supply when less wind and solar energy is generated. Battery storage and gas-fired generation will also be important in ‘balancing’ the system. Third, the best target today is net zero emissions, not zero emissions or 100 per cent renewables, as the physical and economic challenges of balancing a 100 per cent renewables system during periods of high demand, low wind and cloudy skies would be too large. The report’s authors judge that gas generation with offsets would be the lowest cost backstop solution until zero-emissions alternatives are economically competitive, but argue that gas ‘is likely to play a critical, but not expanded, role: the NEM faces a gas-supported transition, not a ‘gas-led recovery.’

- Bloomberg Businessweek on how the pandemic led to the shrinking of the global middle class last year in what was the first decline since the 1990s.

- The Economist has a special report on the future of work. After reviews of recent labour market trends, the rise of hybrid work, the future of automation and changing government policy approaches, it reaches a relatively optimistic conclusion: although the pandemic has been ‘catastrophic’ for many, ‘it may presage improvements in the world of work. The shift to remote work may make many people happier and more productive. It is unlikely to encourage job-killing robots. And it is forcing policymakers to acknowledge some difficult truths about whose interests today’s economy serves best.’

- An Adam Tooze essay for Foreign Policy magazine looks at the challenges facing Janet Yellen and Mario Draghi in a thought-provoking economic biography of two long-standing – and emblematic – technocrats.

- IHS Markit on rising input prices and possible inflationary implications. Firms input costs are now rising at a faster rate than anything seen since comparable data were first available in late-2009, while manufacturing selling prices and average rates levied for services are likewise rising at survey-record rates.

- From VoxEU, work on the impact of disclosure and reporting requirements on corporate innovation. Empirical results based on Europe’s Community Innovation Survey (CIS) and on an enforcement reform that occurred in Germany which required limited-liability firms to disclose financial statements to the public, both suggest that reporting regulation is significantly negatively associated with corporate innovation at the country-industry level. Reporting regulation is also negatively associated with a broad set of measures on returns to innovation, including a reduction in firms’ profit margins, sales from new-to-market innovations, and cost reductions due to process improvements, supporting the idea that reporting regulation affects firms’ innovation activities through proprietary costs.

- Also from VoxEU, Paul Krugman on the late Robert Mundell’s contribution to economics. Great final line: ‘International macroeconomics is largely a house that Mundell built, even if he himself eventually chose to move out and seek lodging elsewhere.’

- Also from Krugman, and recommended by a regular reader: why the 2017 US tax cut for corporations was a flop. Krugman argues that: (1) the tax-deductibility of interest implies that the rate of return on debt-funded investment shouldn’t be influenced by a tax on profits; (2) most business investment isn’t particularly sensitive to the cost of capital anyway – because most business assets are relatively short-lived; (3) the growing importance of monopoly profits means that a significant share of any tax cuts swells monopoly profits with limited effects for the return on investment; and (4) previous US fears about capital flight (and the associated loss of jobs) were largely misplaced – there was little actual capital flight involved, just tax avoidance.

- Related, Richard Murphy on Biden’s tax plan. Murphy’s take: tax havens are ‘an assault on the right of states to tax’ and Biden’s Made in America tax plan is a belated US response.

- The WSJ’s Grep Ip on Bidenomics traces an intellectual history back to Keynes, Heller, Tobin and Okun. Key elements according to Ip comprise: (1) slack, not scarcity, is the default position for most economies; (2) macro policy should focus on driving down unemployment, with inflation much less of a constraint than usually supposed; (3) low interest rates reduce the importance of debt as a constraint on government spending and deficits; (4) aid should be universal rather than targeted; and (5) a world of monopoly power and barriers to market entry make higher tax rates and higher minimum wages more attractive options. Ip thinks that some of this is the product of observation – what the US economy actually looked like in recent decades – but also worries that ‘Bidenomics is more a political movement than a school of economic thought…[and] The problem with economic policies subject to political imperatives is that they have no limiting principle: if US$3 trillion in stimulus is OK, why not US$6 trillion? If a US$15 minimum wage is harmless, why not US$30?’

- The FT’s Martin Sandbu on the birth of a new Washington Consensus.

- An Issues Brief from the Atlantic Council on decoupling/reshoring vs dual circulation.

- How China lends. A look at what information from 100 debt contracts can tell us about Beijing’s profile as an official creditor highlights three key messages: (1) Contracts contain unusual confidentiality clauses that bar borrowers from revealing the terms or even the existence of the debt. (2) Chinese lenders seek advantage over other creditors, using collateral arrangements such as lender-controlled revenue accounts and promises to keep the debt out of collective restructuring (“no Paris Club” clauses). (3) Cancellation, acceleration, and stabilization clauses in Chinese contracts potentially allow the lenders to influence debtors’ domestic and foreign policies.

- Barry Eichengreen on the challenge of big tech finance.

- Noted but not yet read: a new WEF report on technology futures.

- The IMF has launched a new climate change indicators dashboard.

- Three podcast listens to finish with. First up, my fellow Dismal Science podcaster, Ivan Ah Sam, sent me to this good Macro Musings podcast interview with Ed Nelson on Milton Friedman’s legacy. Next, Bloomberg’s Odd Lots had an interesting episode with Slavoj Žižek on the Future of Capitalism, which starts with the implications of the GameStop saga and then ranges widely. And finally, a few weeks back I linked to the Adam Curtis TV series Can’t get you out of my head. Talking Politics podcast has a good discussion with Curtis that covers the main themes of the series but in a much shorter – and punchier – way than watching every episode on YouTube (although of course the podcast doesn’t deliver either the great visuals or sound track of the TV series).

Latest news

Already a member?

Login to view this content