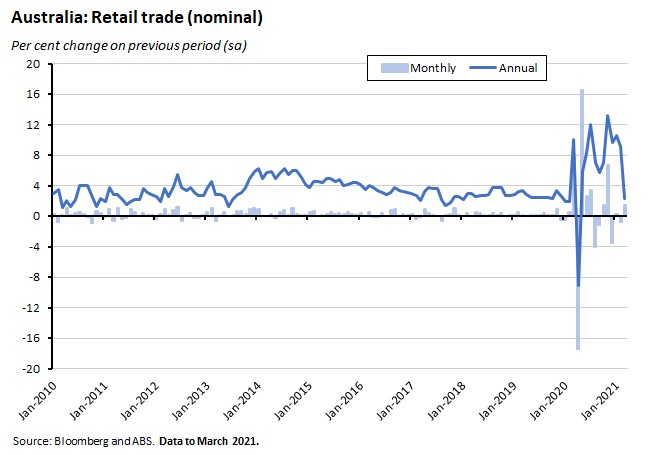

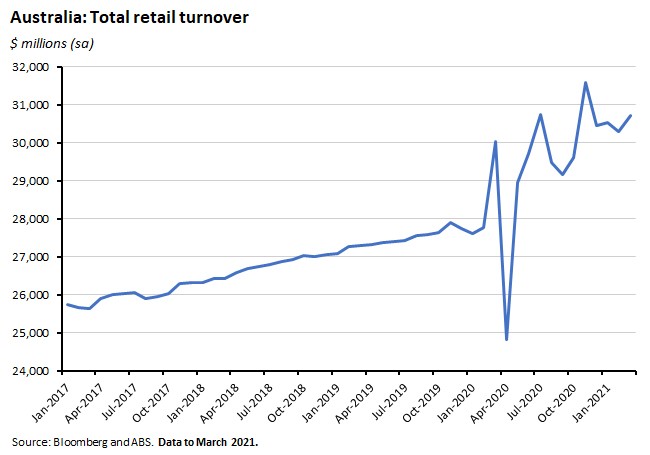

Retail turnover rose 1.4 per cent over the month in March, boosted by growth in Victoria and Western Australia after both states had exited from February lockdowns. Minutes from the RBA’s 6 April meeting showed the central bank pleased with the pace of recovery, sticking to its guns on the inflation outlook, and casting a wary eye over housing market developments and commercial bank refinancing needs.

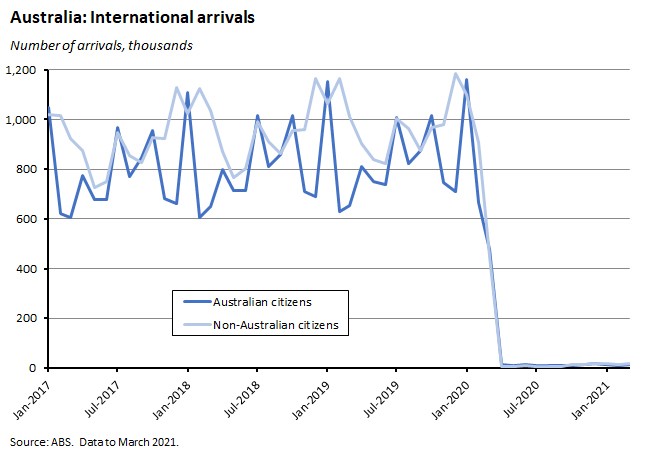

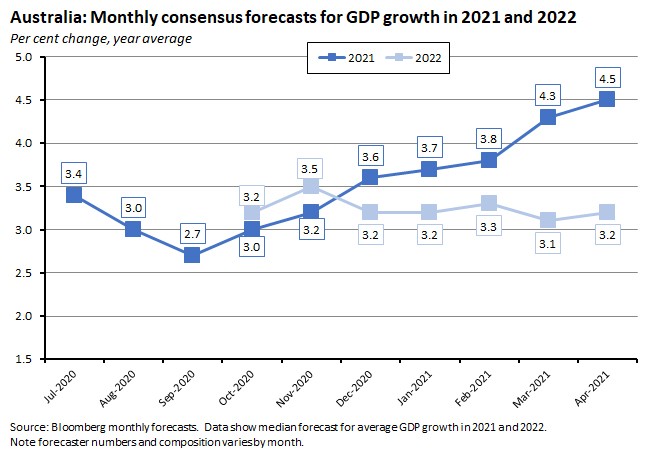

With restrictions still in place, overseas travel remained moribund last month despite an uptick over February. Bloomberg’s latest survey of economists registered an upgrade to the median growth forecast for this year for a seventh consecutive month. NAB’s quarterly business survey reported improving conditions and confidence in the first quarter of this year as well as a sharp rise in investment intentions. Consumer confidence was little changed over the week. Last week’s labour market report delivered another excellent result with marked falls in both unemployment and underemployment. The number of Jobseeker claimants also fell again. Bloomberg’s daily activity indicators suggest that the global economic recovery continued through March and into the first weeks of this month. China’s GDP growth hit a record high in annual terms in Q1:2021 although the quarterly figures suggest a moderation in the pace of activity.

This week’s readings include new ABS data on household finances in the early months of the pandemic, a look at productivity in Australia’s services industries, the OECD’s recommendations on how we should ‘go for growth’, a vanishing billionaire, global trends 2040, how to survive a killer asteroid and the Weimar hyperinflation.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

The ABS said that the preliminary estimate for retail trade rose 1.4 per cent (seasonally adjusted) over the month in March 2021. In annual terms, turnover was up 2.3 per cent. Also, according to the Bureau, in current price seasonally adjusted terms turnover across the March quarter overall was down just 0.1 per cent from last year’s December quarter.

By state, the increases in retail turnover were led by Victoria (up four per cent) and Western Australia (up 5.5 per cent), with both states rebounding from the removal of COVID-19 lockdown restrictions that had been imposed in February. In contrast Queensland – where the authorities introduced a three-day lockdown in Brisbane at the end of March – saw a small decline in turnover.

By industry, the ABS said that cafes, restaurants and takeaway food services (up six per cent) led the rises in March, with turnover in both cases driven by Victoria and Western Australia. The same two states also saw rises for clothing, footwear and personal accessory retailing, and for department stores. March also saw a one per cent decline in turnover in food retailing.

Why it matters:

The consensus forecast was for a one per cent month-on-month increase, so the actual March outcome was quite a bit stronger than expected as the boost to retail activity from the end of lockdowns in Victoria and Western Australia more than offset a modest drag from the short Brisbane lockdown.

Note that the big decline reported in the pace of annual growth (from 9.1 per cent in February to 2.3 per cent in March) reflects base effects: the introduction of COVID-19 restrictions in March 2020 led to a surge in sales, particularly in food retailing, as households built up supplies in expectation of lockdowns. The same effect will work in the opposite direction next month, as April 2020 saw a sharp decline in the value of retail trade (see chart above).

What happened:

The minutes of the 6 April Monetary Policy Meeting of the Reserve Bank Board were published on Tuesday. Points of note included an interesting overview of the differences in Australia’s recent economic performance relative to that of our peers:

- A ‘recurring theme’ of the discussion at the meeting ‘was that Australia had fared relatively well in terms of output levels and labour market outcomes…GDP in Australia had recovered to close to pre-pandemic levels, whereas GDP was still considerably below pre-pandemic levels in many other countries. The loss of output over 2020 as a whole had also been smaller in Australia than in many other countries. This reflected both the relatively smaller initial decline in output in Australia and the swift recovery since then.’

- ‘Despite the rapid recovery in employment in Australia, members noted that wages growth domestically had slowed to a greater extent and had been more subdued than in other countries. The labour market adjustment in Australia in response to the pandemic had principally taken the form of adjustment to hours worked and widespread wage restraint. In contrast, in some other countries, including the United States, the adjustment had mainly been through a decline in employment.’

- ‘Members discussed cross-country differences in population growth stemming from international border closures…The decline in population growth in Australia had been particularly steep relative to other countries; in the 3 months to September, the Australian population had declined for the first time in several decades as a result of a reversal in net overseas migration.’

- ‘Members observed that corporate profitability during the pandemic had varied considerably across countries…In Australia, business profits had increased in 2020 as output had fallen by less than elsewhere and fiscal support had been targeted more towards wage subsidies than loan guarantees. The JobKeeper program had been particularly supportive of industries where labour costs comprise a high share of the total cost base.’

On the Australian economy itself, the minutes reflected the RBA’s recent messaging on the economy - upbeat on the recovery but cautious on the implications for hitting its inflation target:

- Members noted that ‘preliminary data suggested that [Australia’s] GDP in the March quarter was likely to have recovered further to around its pre-pandemic level, earlier than previously expected.’

- On the labour market, ‘members noted that both the initial increase and the subsequent decline in the unemployment rate had been much sharper than observed during the economic downturns of the 1980s and 1990s. This was likely to limit the longer-term scarring effects that had hampered the recovery in labour market conditions following those downturns…Employment had returned to pre-pandemic levels considerably faster than expected. There had also been a shift in growth from part-time to full-time employment. Forward-looking indicators of labour demand had remained strong, with job vacancies and advertisements above pre-pandemic levels, and employment intentions trending higher.’

- ‘These indicators suggested that at least some of the job losses that were likely to follow the end of the JobKeeper program would be offset by new hiring. As a result, while the overall recovery in the labour market was expected to pause in the period ahead, this was expected to be only temporary. Members also noted it was likely that the full effect of the end of the JobKeeper program would become apparent over several months.’

- Members noted that housing prices had increased significantly in recent months…although the increase in overall housing prices in Australia during the pandemic had been more modest than in a number of other countries. Members noted that low interest rates had been one of the factors contributing to the increase in demand for housing, alongside other policies such as government grants.’

- ‘Demand for new housing finance had been strong, and the high level of loan commitments indicated that housing credit growth was likely to increase in the months ahead. However, there was no notable evidence of a deterioration in housing lending standards.’

- ‘Despite these generally positive developments, wage and price pressures had remained subdued and were expected to remain so for several years. The economy had been operating with considerable spare capacity and the unemployment rate was still too high. It would take some time to reduce this spare capacity and for the labour market to be tight enough to generate wage increases consistent with achieving the inflation target. It was likely that wages growth would need to be sustainably above 3 per cent, which was well above its current level.’

- ‘While annual CPI inflation was expected to rise temporarily to around 3 per cent around the middle of the year as a result of the reversal of some pandemic-related price reductions, in underlying terms inflation was expected to remain below 2 per cent over both 2021 and 2022.’

Why it matters:

As noted at the time of the 6 April meeting itself, the RBA’s message has been one of sticking with the monetary policy status quo. Unsurprisingly, this week’s minutes did nothing to change that assessment although their release did add some detail.

On the economic outlook, while the central bank is happy to concede that the economic recovery in general and the labour market recovery in particular has been faster and stronger than it expected – and judges that the impact from the end of JobKeeper will only be a temporary pause in that recovery – it still does not see this feeding quickly into faster wage growth and (therefore) higher inflation. The RBA wants to see wage growth ‘sustainably’ above three per cent as an indicator that its inflation target is within grasp.

Likewise, Martin Place will look through a temporary boost in headline inflation around mid-year, which will see the rate of annual increase in the CPI at around three per cent. The RBA thinks that underlying inflation will remain below two per cent both this year and next.

The RBA was also sanguine on housing market risks, noting that while low interest rates (as well as other policies including government grants) had been responsible for spurring demand, household balance sheets were in decent shape and there was ‘no noticeable sign of a deterioration in housing lending standards.’

Finally, two new points are worth mentioning.

First, the discussion highlighted the fact that ‘Members noted that banks have a sizeable refinancing task in 2023–24, with the maturing of their three-year loans under the Term Funding Facility’ but then continued on to comment that ‘the banks were planning for this and there had been strong demand for the smaller volume of wholesale debt that banks had issued recently.’

And second, the minutes reported that members had ‘agreed to have a broader discussion of the implications of climate change for financial stability in coming months.’

What happened:

Provisional overseas travel statistics from the ABS showed 32,900 arrivals in March this year, an increase of 27.4 per cent over February. There were 32,400 departures in the same month, a 1.2 per cent decline from February.

Why it matters:

With international travel restrictions still in place, overseas travel remains limited despite that 24 per cent increase in arrivals in March. Both arrivals and departures in March this year remain more than 96 per cent down on their March 2020 numbers.

What happened:

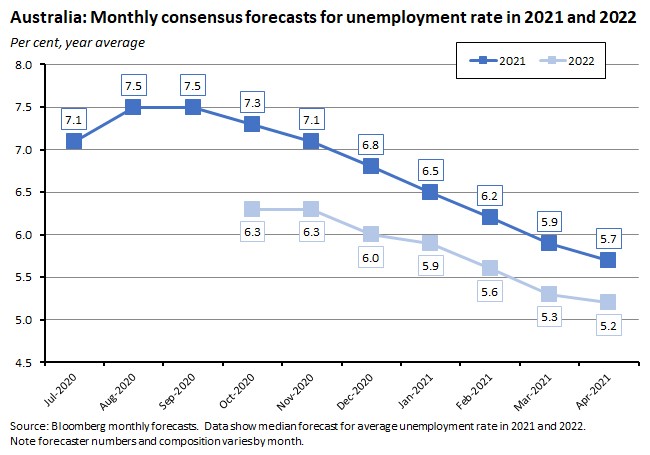

According to the latest (April 2021) set of monthly consensus forecasts collated by Bloomberg, the median forecast for Australia’s average real GDP growth this year is 4.5 per cent, with growth then expected to moderate to 3.2 per cent in 2022 and 2.7 per cent in 2023.

he unemployment rate is expected to average 5.7 per cent this year (but finish Q4:2021 at 5.5 per cent), before falling to 5.2 per cent next year and 4.7 per cent in 2023.

That trajectory sees the average rate of wage growth forecast to run at 1.6 per cent in 2021, two per cent in 2022 and 2.6 per cent in 2023. Over the same period, the median expectation for the rate of CPI inflation is 1.8 per cent this year and next year and two per cent in 2023.

Why it matters:

Economists continue to upgrade their forecasts for the Australian economy in 2021. After reaching a nadir of 2.7 per cent in September 2020, April 2021 marks the seventh consecutive monthly increase for the median growth projection for this year. Likewise, the predicted outlook for unemployment has also improved again. Both trends are consistent with a still-strengthening recovery. Even so, and in something of an echo of the views of Martin Place discussed earlier, the consensus take is that this will not be sufficient to generate the more than three per cent sustained annual pace of wage inflation that the RBA is looking for through 2023, and that headline CPI inflation will still only average two per cent across that year.

What happened:

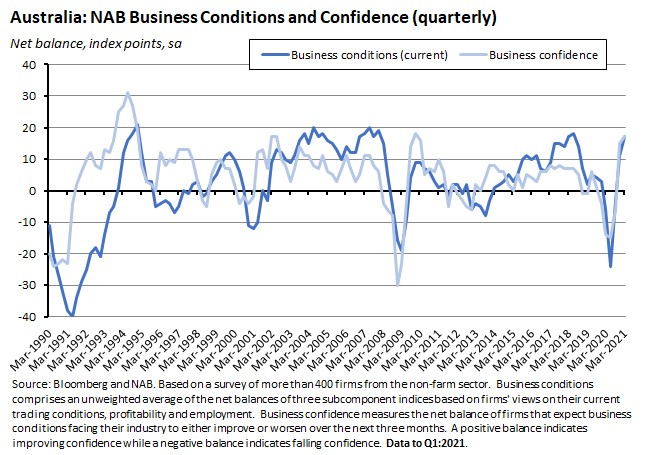

NAB’s quarterly business survey showed business conditions and business confidence each increased in the first quarter of this year, with both indices rising to +17 index points.

All three sub-indices for business conditions improved substantially over the quarter, with readings for profitability, trading and employment all comfortably into expansionary territory and profitability at a record high.

Also of particular note in the quarterly results, NAB said that capex expectations strengthened to +34 index points, marking the highest level since the mid-1990s.

Why it matters:

Last week’s note reported that the NAB monthly business survey for March had business conditions hitting a record high and business confidence well-above above its long-run average, making this quarterly result an additional confirmation of the recovery in business activity over the opening months of the year. The sharp jump in investment expectations also offers some hope that the strengthening recovery and business optimism may be translating into additional plans for capital expenditure.

What happened:

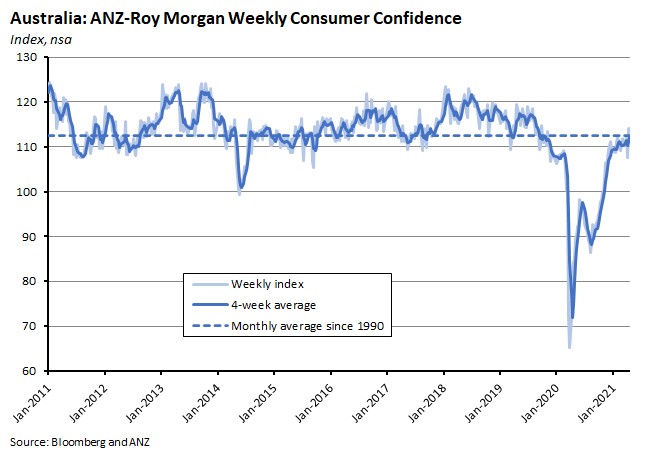

The weekly ANZ-Roy Morgan Index of Consumer Confidence was little changed over the week to 18/19 April, down by just 0.1 per cent.

Subindices painted a mixed picture with diverging views between financial and economic conditions: ‘Current financial conditions’ fell 3.4 per cent, ‘future financial conditions’ dropped 1.6 per cent, ‘current economic conditions’ rose two per cent, ‘future economic conditions’ increased 1.2 per cent, and ‘time to buy a major household item’ was up 1.4 per cent.

Why it matters:

Consumer confidence overall was left largely unchanged by developments over the previous week. It remains above its long-term average and is more than 35 per cent higher than in the corresponding weekend last year.

. . . and a review of last week’s labour market data

What happened:

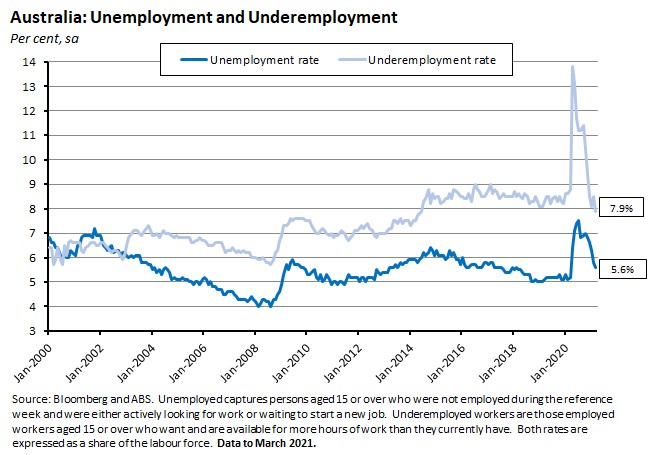

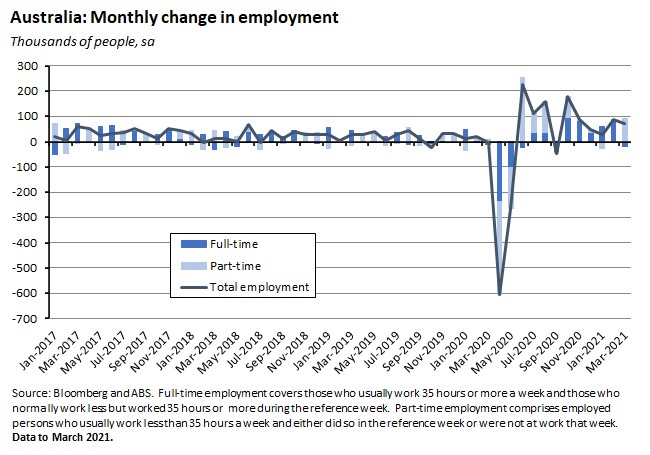

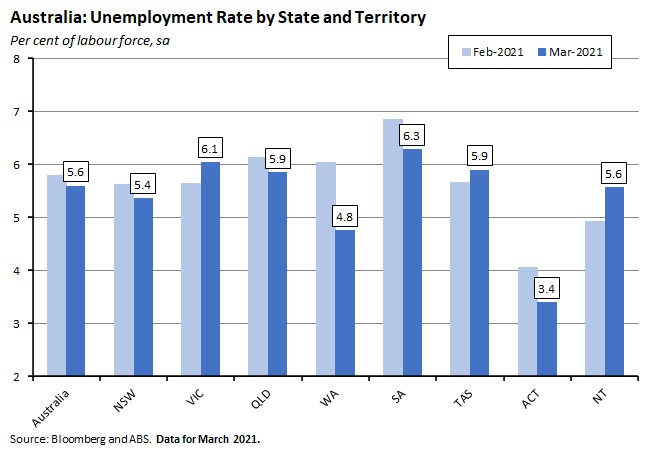

Last Thursday, the ABS said that Australia’s unemployment rate fell to 5.6 per cent (seasonally adjusted) in March, down from 5.8 per cent in February, as the number of unemployed persons fell by 27,100 persons. The underemployment rate fell even more, dropping by 0.6 percentage points over the month to 7.9 per cent in March.

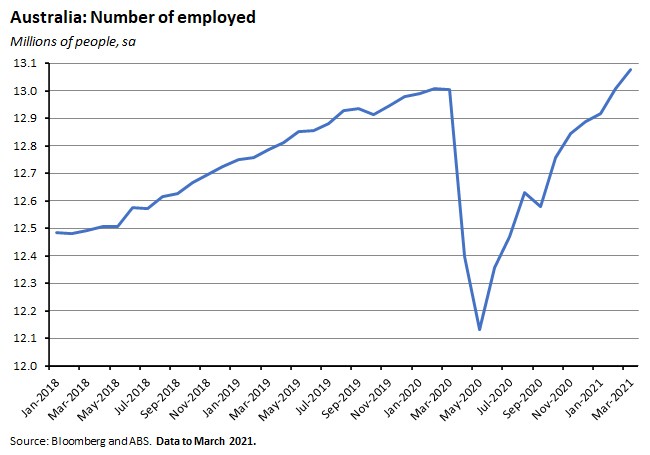

In seasonally adjusted terms, total employment increased by 70,700 people (0.5 per cent) in March to 13,077,600 people. That also left employment up 74,300 (0.6 per cent) relative to March last year.

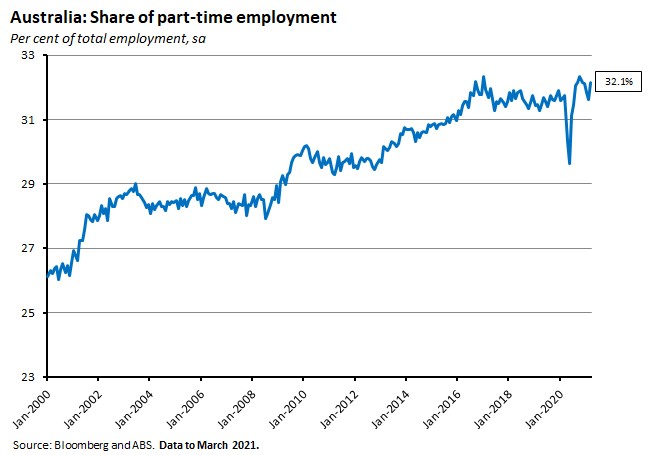

All of the increase in employment last month was part-time in nature: full-time employment fell by 20,800 to a little less than 8.9 million over the month (seasonally adjusted) while part-time employment increased by 91,500 to 4.2 million.

As a result, the part-time share of employment rose to 32.1 per cent, just a little below its recent high of 32.3 per cent, reached in October 2020.

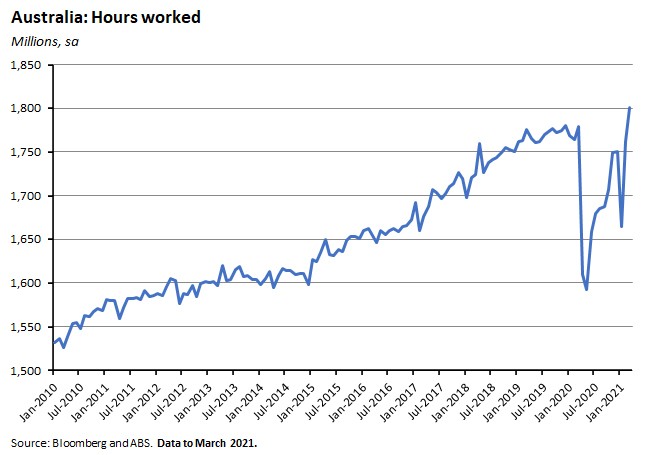

Monthly hours worked in all jobs rose by 38 million hours or 2.2 per cent over the month and were 1.2 per cent higher over the year.

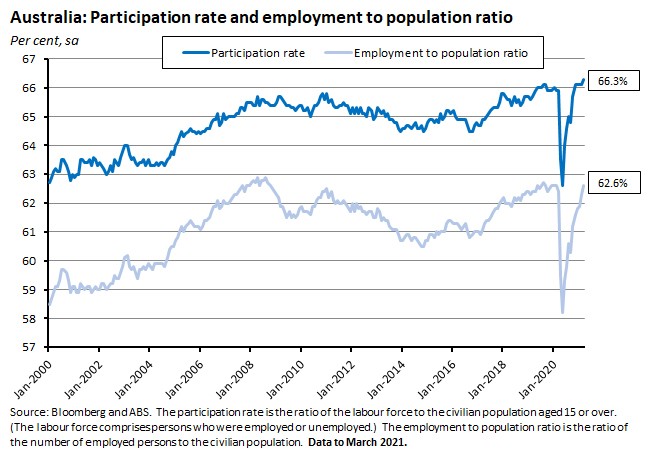

The participation rate increased 0.2 percentage points to a record high of 66.3 per cent. The participation rate for men dropped slightly to 70.9 per cent, but the rate for women increased 0.4 percentage points to a record 61.8 per cent. The employment-to-population ratio increased by 0.3 percentage points to 62.6 per cent.

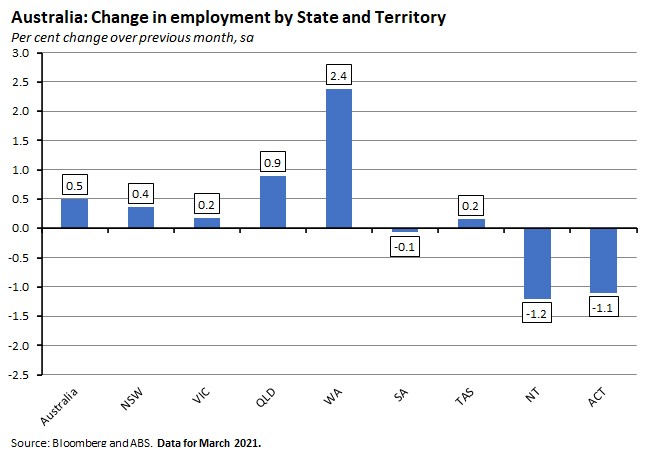

By state and territory, employment rose over the month in New South Wales, Victoria, Queensland, Western Australia and Tasmania, but fell elsewhere.

The unemployment rate in March this year ranged from a high of 6.3 per cent in South Australia to a low of 3.4 per cent in the ACT.

Why it matters:

Another month and another excellent labour market result, which once again beat the consensus forecast (which had expected a more modest fall in the unemployment rate to 5.7 per cent). At 5.6 per cent, the unemployment rate is now just 0.4 percentage points (or about 62,000 people) above its March 2020 reading of 5.2 per cent. And the good news didn’t stop there, as underemployment was also down. Indeed, the underemployment rate is now at its lowest level since June 2014. As a result, the overall underutilisation rate is at its lowest since December 2019 – that is, it is now below where it was at the start of the pandemic. To repeat, this is an excellent result overall.

The more than 70,000 increase in employment (the consensus forecast had been for a 35,000 increase) took the number of employed Australians up to almost 13.1 million in March. Employment was 0.6 per cent up on March 2020 while hours worked were 1.2 per cent higher than in the corresponding month of last year.

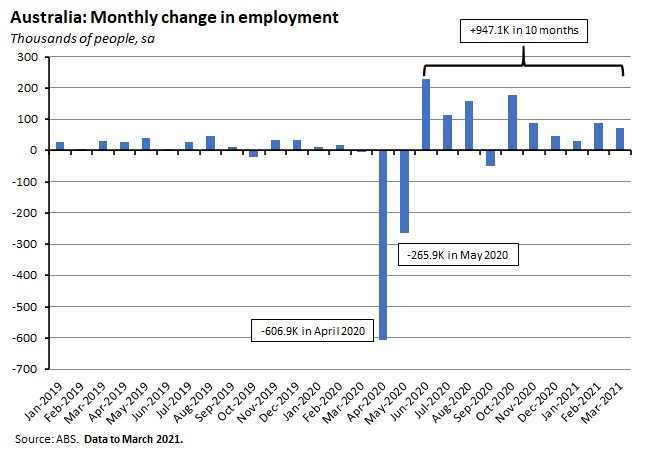

After the economy lost almost 607,000 jobs in April 2020 and about another 266,000 jobs in May 2020, over the next ten months it has now added more than 947,000 jobs.

The participation rate is now at a record high (as is the participation rate for women), while the employment to population ratio is slightly higher than it was in the same month last year.

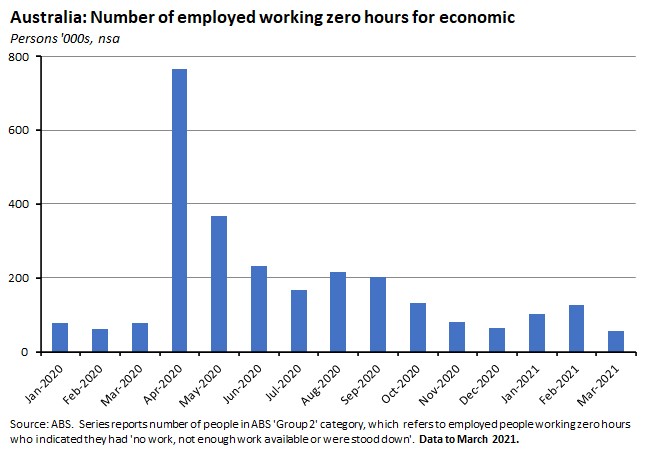

Note, however, that the March data was collected during the first half of the month, prior to the end of JobKeeper on 28 March. That means that the impact of the end of the scheme – which Treasury has estimated may see between 100,000 and 150,000 workers lose their jobs – will only start showing up from the April labour market report onwards. Still, there was some good new here, too. The number of persons working zero hours for economic reasons fell to below 57,000 in March, the lowest result since the onset of the pandemic and the start of lockdowns, and lower than the numbers reported pre-pandemic in January and February of last year.

Taken along with the recent strong results on vacancies and job ads, this result suggests that the hit to the labour market will prove manageable, delivering the kind of temporary pause in the jobs recovery anticipated by the RBA, not derailing it.

What happened:

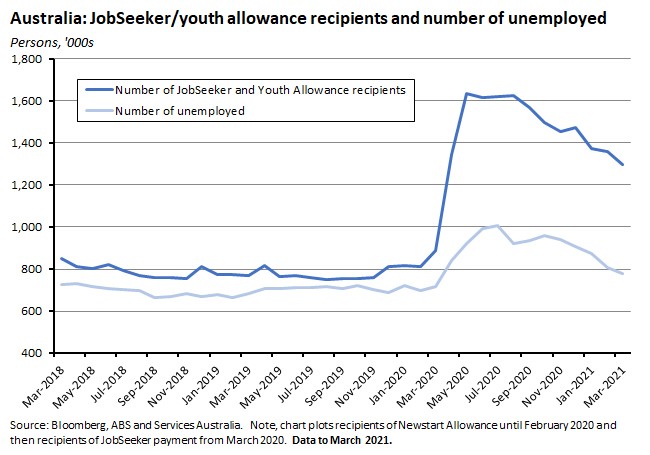

The number of JobSeeker claimants fell to 1,167.4 thousand persons in March, or to 1,296.4 thousand including Youth Allowance recipients.

The latter figure is down more than 60,000 from February and is almost 339,000 lower than the peak number of claimants reached in May 2020.

The large gap that opened up between the number of unemployed and the number of claimants in May last year is still apparent in the data but has now shrunk by more than 195,000.

Why it matters:

The decline in the number of JobSeeker and Youth Allowance recipients is consistent with the good news coming out of the labour market report (discussed above) and the payroll jobs numbers (discussed last week).

Note that the number of unemployed and the number of JobSeeker claimants differ in several ways. The ABS classifies individuals as either employed, unemployed or not in the labour force based on their activity in the survey reference week. This is done by collecting information from a representative sample of Australians every month which is then used by the ABS to estimate the number of people aged 15 years and over who satisfy the ABS definition of unemployed. These estimates are based on the number of people without work, who are actively seeking work and who are available for work in the survey reference week. The ABS does not use information on whether people receive a government job seeker income support payment to measure unemployment.

Differences between the two counts arise because:

- Some of the unemployed will not receive JobSeeker payments.For example, applicants are subject to personal income and assets tests for themselves and their spouse and as a result in some cases may not be eligible for support.Or they may be subject to an income maintenance period where a recent leave or redundancy payment from their previous employer is treated as income for the income test.Or they may only expect to be out of work for only a short period and may choose to support themselves financially through savings or the income of a spouse/partner over that period. Or they may be receiving another type of income support payment (such as a Disability Support Payment).

- Some JobSeeker recipients will not be classified as unemployed, For example, a recipient would not be classified by the ABS as unemployed if they undertook one hour or more of paid work in the reference week, or had not actively looked for work in the previous four weeks or were not available to start work immediately.JobSeeker recipients are able to undertake some paid work and to continue to receive their payment until the income from that paid work reaches a specified level.Under these circumstances, they would be classified as employed by the ABS, not unemployed.Other recipients could be engaged in training, study or full-time voluntary work as part of the activity test requirements, which may mean that they would not be available to start work and therefore would be classified by the ABS as not in the labour force.Similarly, some recipients may be temporarily exempt from the activity test requirements due to personal circumstances such as illness, homelessness or a major personal crisis. Again, these individuals would not be classified as unemployed according to the ABS definition if they did not actively look for work in the previous four weeks but instead would be classified as not in the labour force.

Changes to the JobSeeker allowance during the early months of the pandemic also softened the eligibility requirements for claims.

. . . and what I’ve been following in the global economy

What happened:

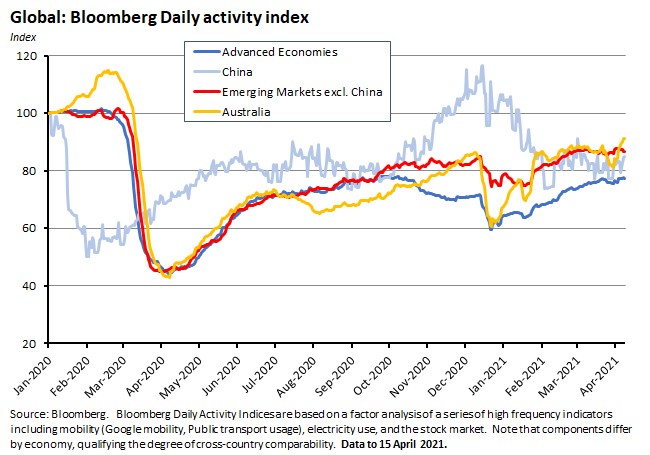

Bloomberg’s daily activity indicators – alternative, high-frequency measures based on mobility, travel and financial market data – show the global economic recovery continuing through March and into the first half of this month. Advanced and emerging economies have both seen activity trending higher, although China has seen some weakening in activity over the past two months. Australia, meanwhile, continues to out-perform.

Why it matters:

The daily activity indicators – despite their limitations – offer an interesting, alternative perspective on global activity to official data, and one that is available with less of a lag. The softer numbers for China here, for example, are also consistent with some signs in the official data that the pace of China’s economic recovery slowed over the first quarter of this year (see next story).

However, it’s also worth noting that there is now some evidence that the relationship between mobility and economic activity has been changing over the course of the pandemic. The latest IMF World Economic Outlook, for example, notes that the adverse impact of lockdown restrictions on public health appears to have declined over the course of 2020, as economic activity became less sensitive to curbs on public mobility. This is important because the Bloomberg indicators give a relatively high weight to travel and mobility data for most of the countries tracked.

That change in the relationship probably reflects some combination of more targeted lockdowns (which, for example, are now more likely to exempt sectors like construction and manufacturing) alongside the growing ability of businesses and workers to adapt to remote work and public health restrictions.

What happened:

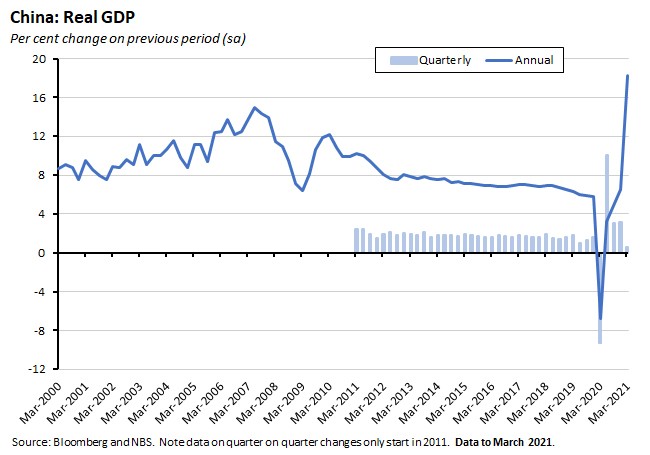

According to the National Bureau of Statistics, China’s real GDP rose by 0.6 per cent over the quarter in Q1:2021. In annual terms, output soared by 18.3 per cent.

Why it matters:

China was the only major global economy to register real GDP growth last year, with output up 2.3 per cent in 2020, and on the surface, the record-breaking 18.3 per cent year-on-year jump in growth in Q1:2021 is yet more evidence of the economy’s strong bounce back from the pandemic. Note, however, that much of this is the base effect in action: Q1:2020 saw China’s economy thrown into lockdown which in turn saw real GDP contract for the first time in decades. It’s the comparison with that unusually weak quarter that is pumping up in the annual numbers. In contrast, at 0.6 per cent the rate of quarter-on-quarter growth looks much more modest, and relative to previous quarters suggests a moderation in the pace of an economic recovery that began back in the second quarter of 2020.

What I’ve been reading . . .

The new ABS report on household financial resources for the September quarter of 2020 provides an overview of household finances in the months following the introduction of COVID-19 measures. According to the Bureau, average private household income which includes earnings from jobs (including JobKeeper payments), investments and superannuation remained stable in real terms, at $2,117 per week in September 2020, unchanged relative to Q3:2019. An $89 per week increase in income from government payments (pensions and other allowances including the Coronavirus Supplement), took such payments up to $300 per week. Even after this increase, however, total average household income remained stable in the September 2020 quarter at $2,417 per week. Around 19 per cent of households included someone receiving the JobKeeper payment through their employer or in their own business while more than 1.3 million households contained someone receiving the Coronavirus Supplement. The ABS said that most people who accessed their superannuation early due to financial hardship caused by COVID-19, used it to pay their mortgage or rent (29 per cent) or other household bills (27 per cent). Another 15 per cent used it to pay credit card or personal debts, while 13 per cent added it to their savings.

A new Productivity Insights report from the Productivity Commission (PC) looks at Australia’s services sector productivity. Services constitute about 79 per cent of value added and 88 per cent of employment in the Australian economy, although the PC is careful to note that there is no monolithic ‘service sector’ as such given that there are huge variations across and within sub-industries. Still, taken in aggregate, the service sector has actually had faster multifactor productivity (MFP) growth than the goods sector since 1993-94, although this is mainly due to the goods sector exhibiting close to zero MFP growth over the period, much of which the PC notes reflects the idiosyncratic dynamics of the mining industry’s investment and production cycle. Notably, while Australian service sector MFP growth has been strong, labour productivity has lagged, placing Australia as among both the best and worst performing developed nations in MFP and labour productivity respectively since 2000. The Commission also notes that the pandemic has forced many businesses, consumers and workers to experiment with remote delivery technology. It judges that this has demonstrated the potential for technology to alter the characteristics of many services and also raised the possibility of changes to potential productivity growth. (As a quick reminder, labour productivity — output divided by hours worked — measures the efficiency with which labour produces output while MFP measures the efficiency with which the combination of capital and labour produce output.)

John Kehoe in the AFR on Australia’s red-hot economic recovery.

Also from the AFR, a guide(s) to the new world disorder.

The ABC’s Ian Verrender offers a sceptical take on the great skilled worker shortage. If Australia suffers from a longstanding and widespread skills shortage, he asks, where is the accompanying surge in wages?

Rose, Sinning and Breunig from the ANU’s Tax and Transfer Policy Institute discuss some of their findings on how corporate tax rates affect firm location decisions and national industry structures. Their starting point is the apparent paradox that ‘Australia has continued to attract large amounts of foreign investment, despite its high corporate tax rate in comparison to other countries.’ Yet the cross-country economics literature suggests a median value of the tax rate elasticity of around −3.3, suggesting that a one percentage-point reduction (increase) in a country’s tax rate raises (lowers) foreign direct investment (FDI) in that country by 3.3 per cent. They suggest that an important part of the story here is that much of Australia’s recent investment activity has tended to be concentrated in the mining and financial sectors: both tend to be highly profitable and enjoy location-specific rents, which might make them less sensitive to changes in the company tax rate, while in the case of the financial sector, many bank shareholders are domestic and benefit from dividend imputation, making company tax somewhat irrelevant. But non-mining, non-finance sector investment has done less well. The authors argue that a lower corporate tax rate would boost overall investment into Australia but that the government should go further and consider more comprehensive reform such as the Allowance for Corporate Equity (ACE) – which would provide a deductible allowance for corporate equity in computing a firm’s taxable profits. Their full report (pdf) is here.

Grattan has released a new report on the next steps for Aged Care after the Royal Commission.

The Australia Institute’s Jim Stanford on the changing economics of the minimum wage and the case for a higher rate.

The OECD’s going for growth reports and recommendations. The report sets out country-specific strategic priorities for the recovery for OECD member (and some selected non-member) countries. It’s policy advice here is arranged around three pillars: building resilience and sustainability with a focus on avoiding shocks and reducing risks; facilitating reallocation to better allocate resources and boost economic dynamism and productivity; and supporting people through transitions via health and education policies. In the case of Australia (pdf), the OECD makes the case for:

- improving business frameworks and increasing competition, including via legislating automatic mutual recognition of occupational licenses across jurisdictions, reducing the scope of occupational licencing more broadly, and adopting international product standards to reduce regulatory red tape.

- Measures to boost Research and Development (R&D) spending

- Efforts to improve the outcomes of disadvantaged students in schools and early childhood education.

- The adoption and implementation of an ‘integrated national energy and climate policy framework for 2030 based on a low emission development strategy for 2050.’

- ‘Shifting the tax mix away from heavy taxation of incomes to consumption and land taxes’ aligning the high corporate tax rates for large businesses with those on SMEs.

- Once the recovery is ‘firmly in place’, there is ‘scope to increase the Goods and Services Tax, while offsetting the regressive impacts for low-income households.’

- The OECD also argues for ‘giving Indigenous communities a greater role in policy design and implementation and introducing a whole-of-government evaluation strategy for policies affecting these communities’ in order to make growth more inclusive.

The Fed’s Richard Clarida explains the US Federal Reserve’s new monetary policy framework and outcome based forward guidance.

Noah Smith asks, why has climate economics failed us? Arguably this is overly harsh, but certainly worth a read. His latest hexapodia podcast with Brad DeLong and guest Zeke Hausfather also touches on his column but covers climate change policy more broadly.

From the Economist, the contrasting signals regarding the prospects for natural gas.

Related, Bloomberg Green warns that the natural gas sector could run into the same kinds of problems with stranded assets that are already hitting coal.

Jeffrey Funk in American Affairs on what’s gone wrong with US venture capital. According to this essay, more than 90 percent of ‘unicorns’—start-ups valued at US$1 billion or more while privately held (before IPOs) —lost money in 2019 or 2020, even though more than half of them were founded over a decade ago. Funk says part of the story here is just diminishing returns - as the amount of investment in the start-up market has increased, a larger share has necessarily gone to weaker opportunities, and thus the average profitability of investment has fallen. But he also thinks that a ‘lack of revolutionary technology’ has made it difficult to ‘create value at a scale sufficient to become profitable’. As a result, he reckons, many of today’s start-ups ‘are comparatively low-tech, even with the advent of the smartphone—perhaps the biggest technological breakthrough of the twenty-first century—fourteen years ago. Ridesharing and food delivery use the same vehicles, drivers, and roads as previous taxi and delivery services; the only major change is the replacement of dispatchers with smartphones. Online sales of juicers, furniture, mattresses, and exercise bikes may have been revolutionary twenty years ago, but they are sold in the same way that Amazon currently sells almost everything.’

Tributes (and some linked readings) for the late John Williamson. The Economist has more on the man who coined the term ‘Washington Consensus.’

Related, Jeffrey Frankel on what Williamson, Robert Mundell and Richard Cooper have taught us about currency regimes. All three were sceptical of floating exchange rates – a regime that has served Australia well.

The FT magazine on Jack Ma, the vanishing billionaire.

Also from the FT, the vaccines are working: Across five countries ‘rates of infection, hospitalisation and death have traced a lower path among the older, most vaccinated age groups than among the younger, who are least likely to have received the jab.’

Greg IP on the J&J vaccine and balancing pandemic risks.

The US National Intelligence Council’s Global Trends 2040. The NIC focuses on five key themes and also sets out five potential scenarios for the world in 2040. The themes are: (1) more frequent and more intense global challenges including climate change, disease, financial crises and technological disruptions; (2) increasing fragmentation within communities, states and the international system; (3) disequilibrium in the form of a growing mismatch between challenges and needs on the one hand and the systems and organisations to deal with them on the other; (4) greater contestation within communities, states and the international system; and (5) adaptation as both an imperative and a source of comparative advantage given the previous four themes. The five potential scenarios for 2040 it considers are: (1) Renaissance of Democracies, in which rapid technological advances in the US and its allies lead to higher incomes and a better quality of life across the globe; (2) Competitive Coexistence, which envisions a world of continued economic interdependence between the US and China alongside competition over political, strategic, technological and governance models; (3) Tragedy and Mobilisation, under which a global coalition led by the EU and China is responding to a global food catastrophe caused by climate events and environmental degradation; (4) A World Adrift, with a directionless, chaotic and volatile international system and slow growth, widening social divisions and political paralysis across the OECD; and (5) Separate Silos, in which the world has fragmented into several economic and security blocs.

Wired on how to survive a killer asteroid.

The Odd Lots podcast has an interview with Zach Carter on the Weimar hyperinflation.

Latest news

Already a member?

Login to view this content