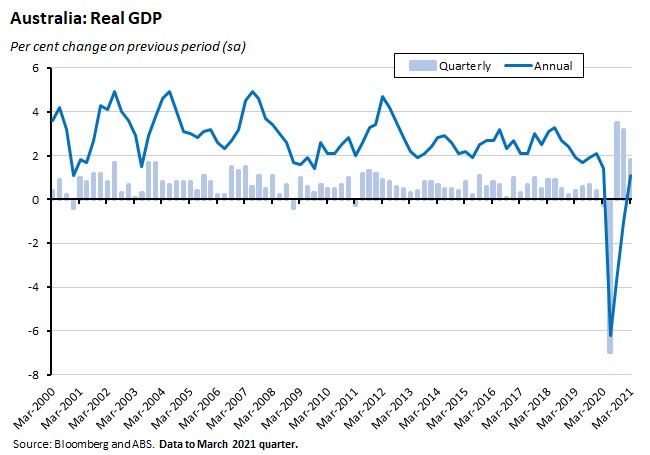

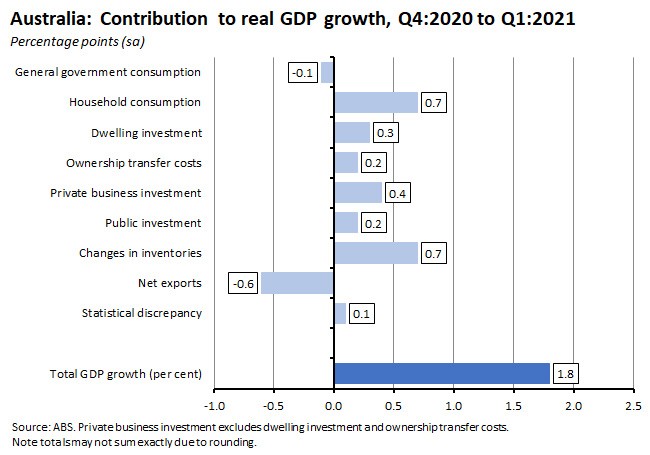

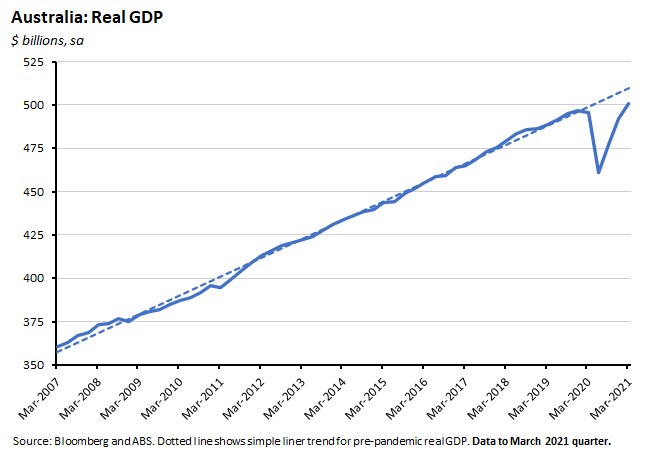

Australia’s real GDP rose 1.8 per cent over the March 2021 quarter to be 1.1 per cent higher over the year. Strong contributions from consumption, the housing sector and business investment on machinery and equipment meant that real output is now 0.8 per cent higher than it was in Q4:2019, before the onset of the pandemic. The RBA left monetary policy settings unchanged at its 1 June meeting but reminded us that next month it would make important decisions on both the future of yield curve control and on its program of government bond purchases.

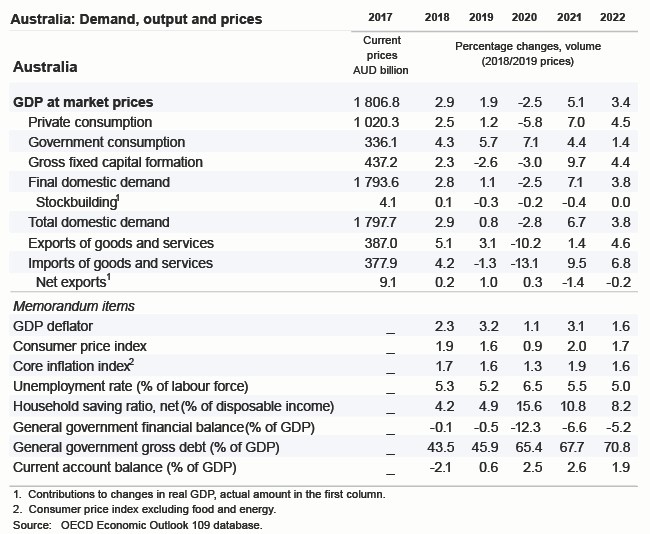

Australia reported a record $18.3 billion current account surplus in the March quarter, marking an eighth consecutive quarter in which current account credits exceeded debits. CoreLogic’s national home price index rose 2.2 per cent over the month in May to be 10.6 per cent higher over the year as Australia’s housing boom continued. The number of private sector dwellings approved fell in April, pulled down by a sharp fall in approvals for dwellings excluding houses, even as approvals for houses hit a new record high. Total private credit growth rose 0.2 per cent over the month in April and was up 1.3 per cent year-on-year. Australia recorded an $8 billion trade surplus in April this year. The final numbers for retail turnover in April were in line with the preliminary estimates. The OECD now forecasts global real GDP growth rising to 5.8 per cent this year before slowing to 4.4 per cent in 2022. For Australia, it projects growth rates of 5.1 per cent in 2021 and 3.4 per cent in 2022 but also warned that ‘without widespread vaccination, the economy is vulnerable to a sizeable outbreak and accompanying restrictions’.

This week’s readings include an economic update from the Treasury Secretary, the RBA on risk and uncertainty before and after the pandemic, the Productivity Commission on recovery and reform, Grattan on rethinking Australia’s skilled migration program, tracking the shift in Australia-China relations, 60 reform suggestions from the NSW Productivity Commission, the coming global investment boom, Operation Warp Speed as a triumph of industry policy, how COVID-19 has changed economics, and challenges to meritocracy.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

The ABS said that in the March quarter of this year, Australia’s real GDP rose by 1.8 per cent over the quarter (seasonally adjusted) to be up 1.1 per cent over the year.

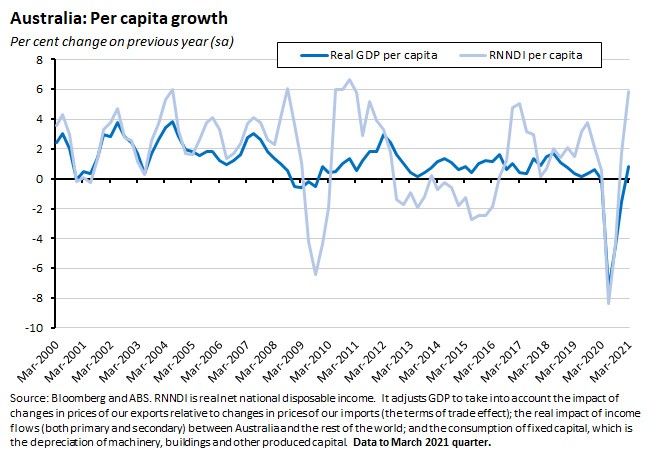

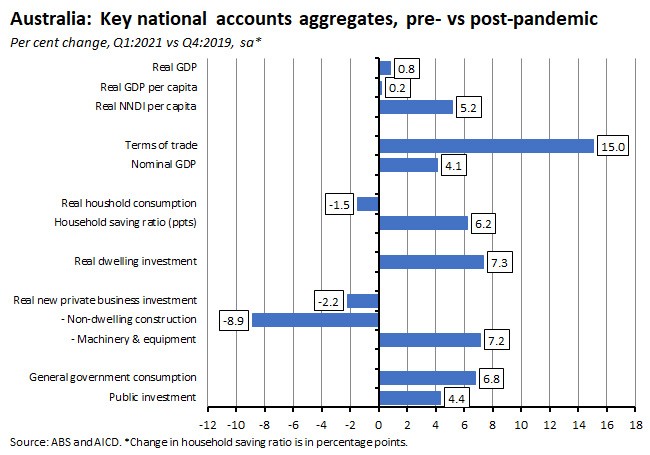

In per capita terms, real GDP grew by 1.7 per cent over the quarter and was up 0.8 per cent relative to Q1:2020. Growth in real net national disposable income per capita, which takes into account the impact of changes in the terms of trade effect, was much stronger, rising by 3.4 per cent over the quarter and jumping 5.8 per cent in annual terms.

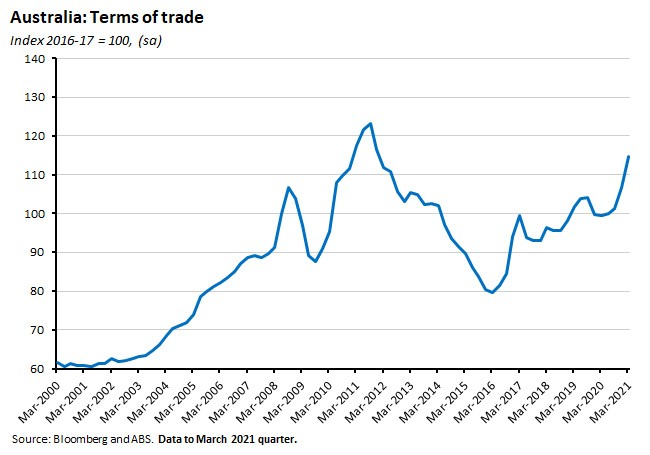

That difference reflects a 7.4 per cent increase in Australia’s terms of trade over the quarter and a 15.4 per cent annual increase, which took the ratio of export prices to import prices back up to their highest level since the December quarter 2011. Stronger export prices, particularly for iron ore and LNG, drove the quarterly rise.

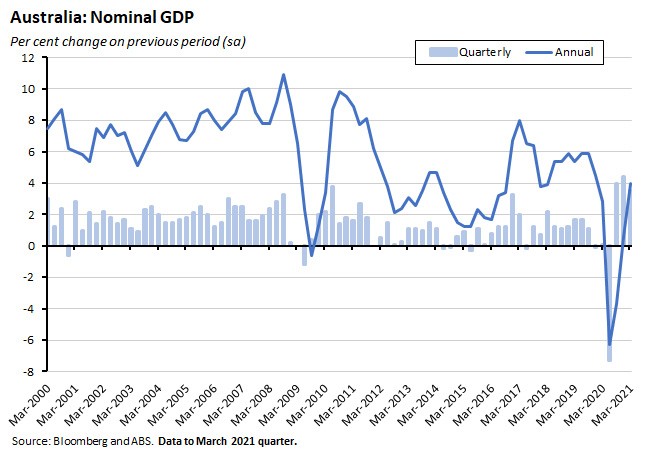

That strength in the terms of trade also contributed to a solid 3.5 per cent increase in nominal GDP over the quarter, which saw the dollar value of output up four per cent relative to Q1:2020.

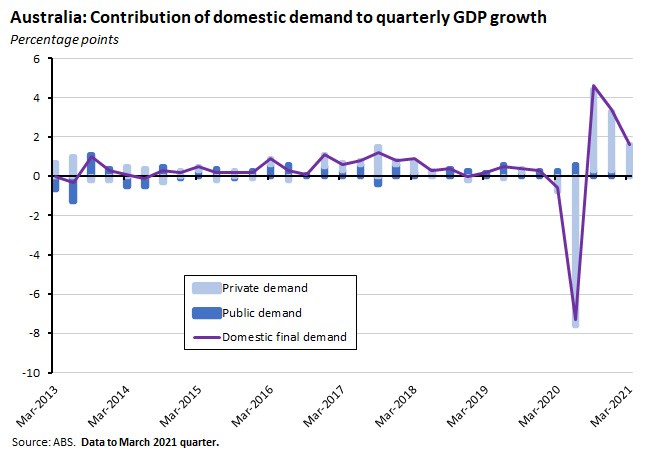

Turning to the drivers of real GDP growth on the expenditure side of the national accounts, growth over the March quarter reflected a combination of strong household consumption (which accounted for 0.7 percentage points of total quarterly growth), the housing sector (with dwelling investment contributing 0.3 percentage points to growth and ownership transfer costs a further 0.2 percentage points), private business investment (0.4 percentage points) and inventories (0.7 percentage points).

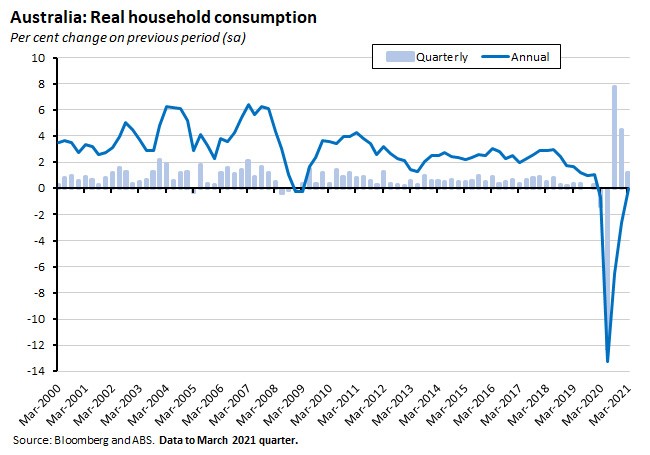

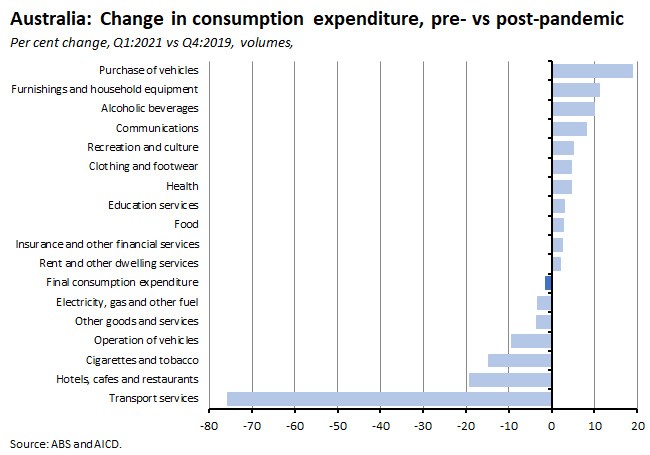

Household consumption rose 1.2 per cent over the quarter but was broadly unchanged in annual terms and is still 1.5 per cent below its pre-pandemic (Q4:2019) levels.

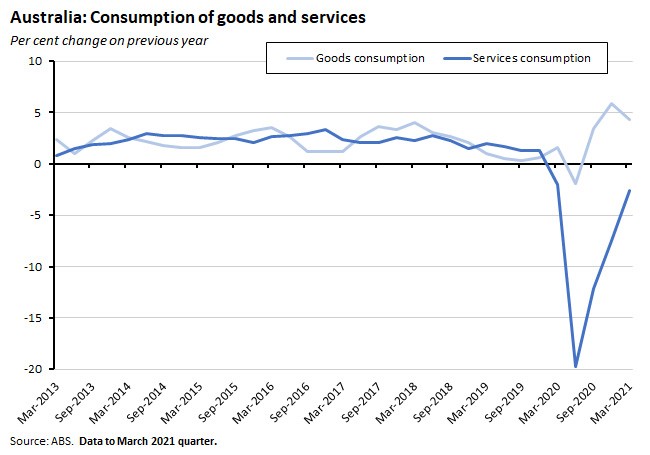

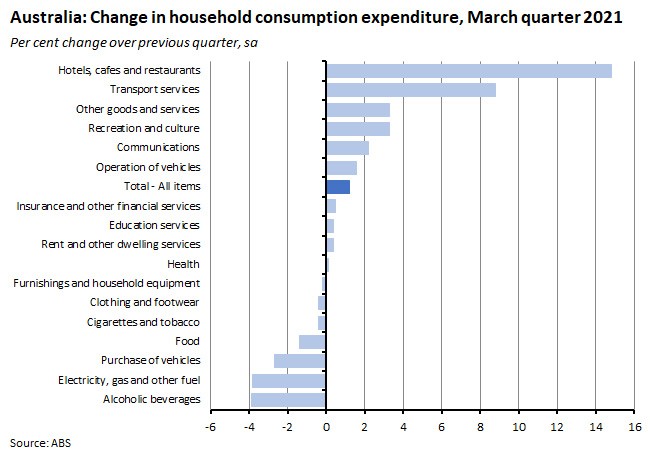

Spending on services (up 2.4 per cent) drove the quarterly rise in consumption, with a rebound in spending on Hotels, cafes and restaurants, Recreation and culture and Transport services as households rebalanced their consumption baskets following the easing of pandemic-driven restrictions. Even so, spending on services remains below pre-pandemic levels, particularly on those services impacted by the closure of international borders. In contrast, while spending on goods fell 0.5 per cent over the quarter, it remains high relative to pre-COVID spending patterns.

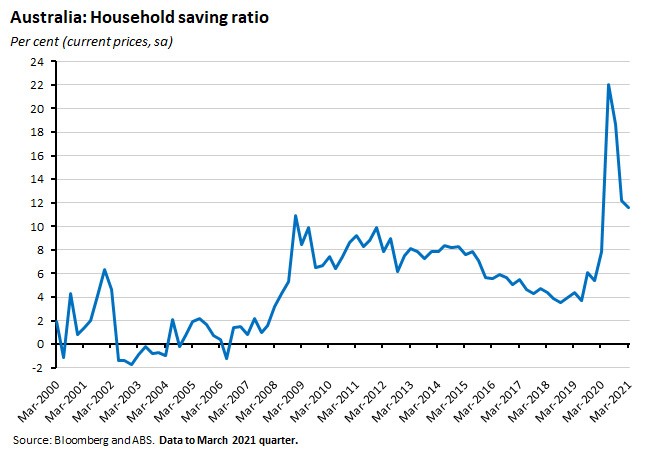

Growth in household consumption exceeded growth in household disposable income, leading to a modest fall in the household saving ratio. The latter edged down from 12.2 per cent in the December 2020 quarter to 11.6 per cent in the March 2021 quarter but still remains high relative to its pre-pandemic average.

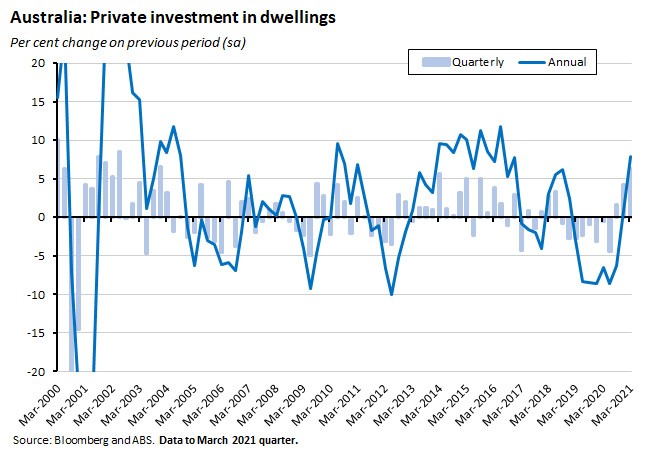

Private investment rose 5.3 per cent in the March quarter to be up 3.6 per cent up in annual terms. This marked the strongest quarterly increase since Q3:2017 and the first annual increase since Q2:2018. Total private investment was driven by a combination of stronger housing investment (including a sizable contribution from ownership transfer costs) and a pick-up in business investment.

Dwelling investment rose 6.4 per cent over the quarter and 7.9 per cent over the year while ownership transfer costs jumped 10.6 per over the quarter and soared 26.8 per cent year-on-year.

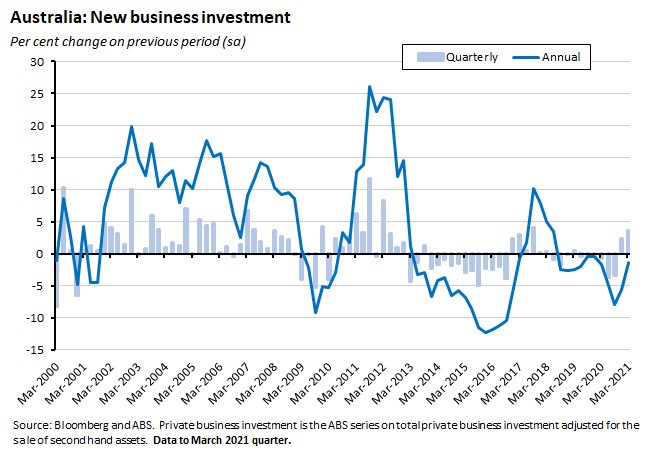

Private new business investment rose for a second consecutive quarter but still remains down on a year ago and below pre-pandemic levels.

By sector, mining investment was up 2.5 per cent over the quarter and 3.4 per cent over the year while non-mining investment rose 4.5 per cent over the quarter but was still three per cent below investment levels in the same quarter last year.

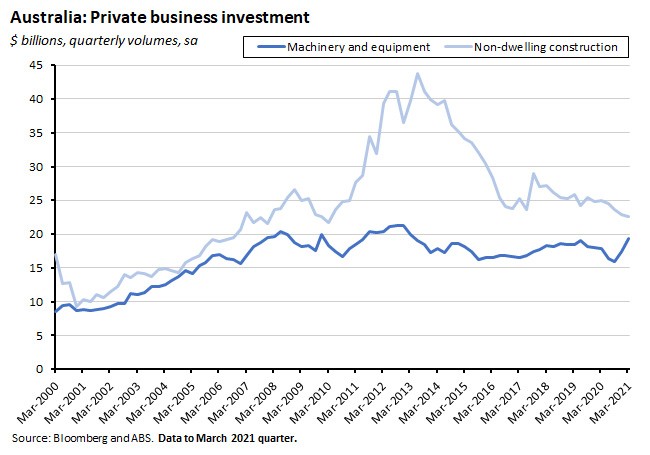

By type of investment, spending on machinery and equipment was up a strong 11.6 per cent over the quarter and 8.6 per cent higher in annual terms. In contrast, non-dwelling construction fell 1.1 per cent over the quarter and was also down 9.3 per cent over the year.

There was also a substantial contribution to growth this quarter from an increase in inventories, which rose $3.3 billion following a slight decline in the December quarter. The largest contributors to the rise were a $2.4 billion rise in wholesale trade and a $2.3 billion increase in retail trade as businesses restocked following the surge in goods demand during the pandemic.

Government spending made only a modest direct contribution to GDP growth this quarter, with an increase in public investment offsetting a decline in general government consumption. And with imports up more than exports, net exports served as a drag on growth despite Australia delivering another record current account surplus (see story below).

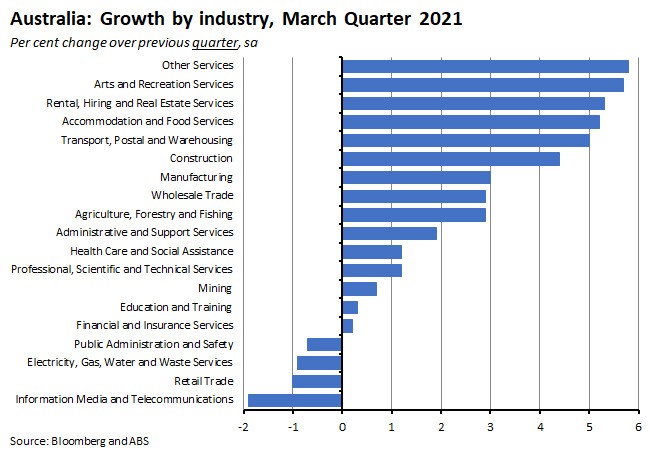

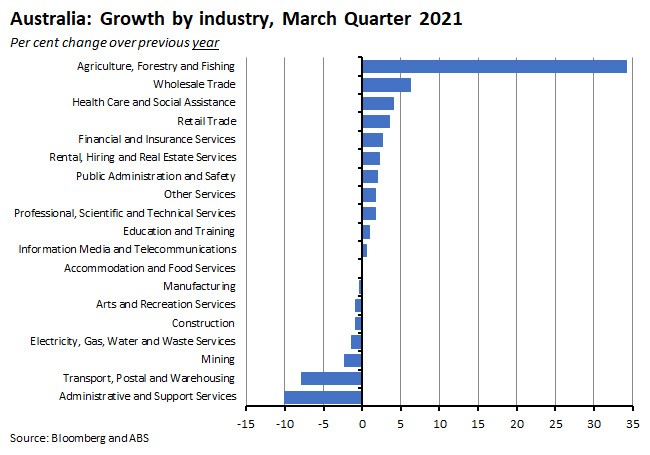

On the production side of the national accounts, activity rose over the quarter across a range of services including Arts and recreation, Rental, hiring and real estate, and Accommodation and food services – in line with the recovery in services consumption already noted above. The biggest contributions to quarterly growth came from construction (which added 0.3 percentage points) followed by Transport, postal and warehousing services and Manufacturing (both contributed 0.2 percentage points).

In annual terms, growth was strongest in Agriculture, forestry and fishing as improved weather conditions lifted crop production and there were also solid results for wholesale and retail trade and for health care. In contrast, activity in many services industries, including Transport services, Administrative and support services and Arts and recreation services was still down relative to the March quarter of last year.

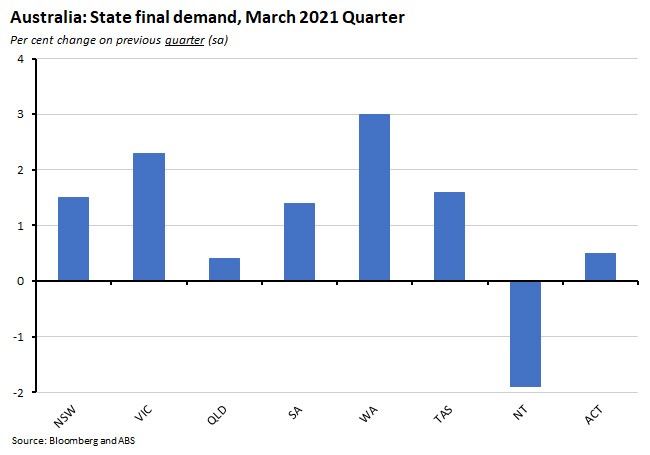

Turning to the states, state final demand rose over the quarter in every geography except the Northern Territory (which saw a fall of 1.9 per cent). The strongest growth was in Western Australia (up three per cent) followed by Victoria (up 2.3 per cent) and Tasmania (up 1.6 per cent).

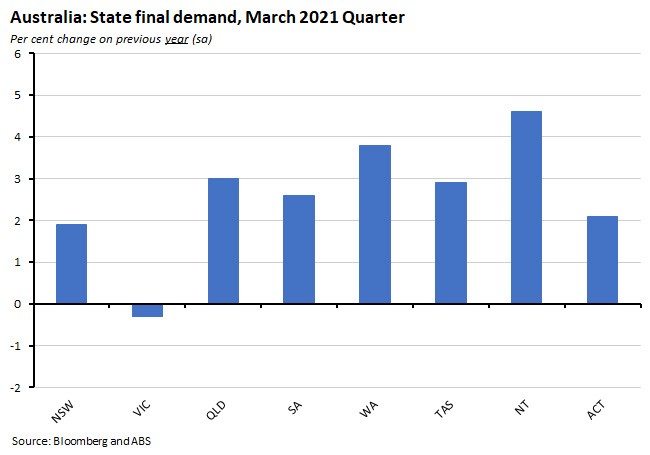

In annual terms, only Victoria saw a decline in state final demand with a 0.3 per cent drop. The strongest year-on-year gains were in the Northern Territory (up 4.6 per cent), Western Australia (up 3.8 per cent) and Queensland (up three per cent).

Why it matters:

The Q1:2021 GDP result exceeded the median forecast for a 1.5 per cent quarterly growth rate and a 0.6 per cent year-on-year increase and in doing so took the level of real GDP to 0.8 per cent above the pre-pandemic Q4:2019 result. Note, however, that this still leaves real output below where we would have expected it to be in the absence of the COVID-19 shock.

The March quarter’s GDP result was powered by strong private domestic demand, with significant direct contributions from household consumption, the housing sector and private business investment. The household sector in particular continues to be a key driver of overall activity: combine household consumption, dwelling investment and ownership transfer costs, and the sector contributed 1.2 percentage points to quarterly growth. Also notable was the increased contribution from business investment in the form of a sharp increase in expenditure on machinery and equipment.

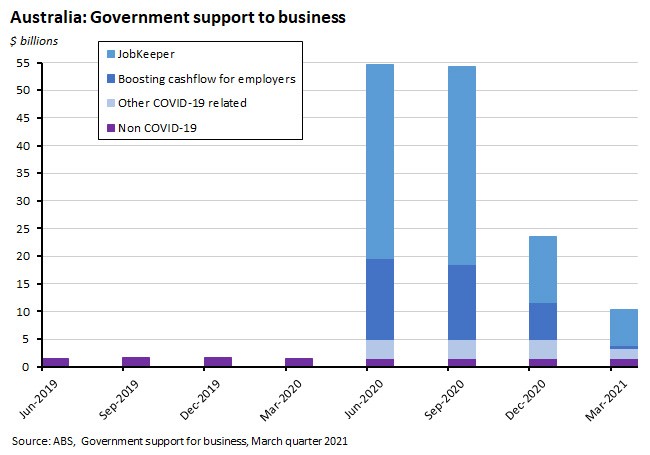

The ongoing decline in the importance of direct policy support to growth was visible in the drop in the value of government support to business, which has now fallen from more than $53 billion in the June quarter of last year to less than $9 billion in the March quarter of this year, with JobKeeper accounting for the bulk of that change.

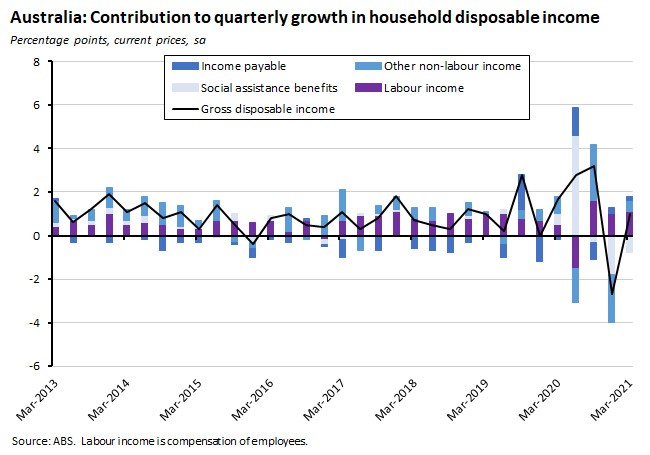

Similarly, a look at the drivers of household disposable income shows that while in the June 2020 quarter social assistance benefits contributed 4.6 percentage points to total income growth, that contribution has now been negative for the past three quarters.

While the direct contribution from the public sector is now much more modest than at the start of the pandemic, however, the overall impact of government policy remains substantial and goes beyond the generally supportive macro policy stance. The government’s HomeBuilder grant has (along with the RBA’s easy monetary policy) helped drive a surge in demand in the housing sector that has shown up in strong dwelling investment and in a big increase in ownership transfer costs (stamp duty, real estate agents fees and so on). Likewise, tax incentives for business investment – extended for another year in Budget 2021-22 – have contributed to that big rise in capital expenditure on machinery and equipment, which the Bureau said recorded its strongest quarterly increase since December 2009. And stored-up fiscal largesse from earlier in the pandemic continues to bolster private sector balance sheets.

A comparison with the state of the national accounts pre-pandemic (Q4:2019) reveals some interesting patterns. While real GDP and real GDP per capita are up only modestly, real net national disposable income is more than five per cent higher. As noted earlier, that reflects a large contribution from the terms of trade, which were 15 per cent higher in Q1:2021 than in Q4:2019. Likewise, the nominal side of the economy has outperformed the real side, with nominal GDP 4.1 per cent than its pre-COVID level.

By expenditure component of GDP, real household consumption is still down on its pre-pandemic levels, as is real business investment (although the machinery and equipment component is now well up). The household saving ratio also remains more than six percentage points higher than its pre-pandemic ratio – suggesting both ongoing household caution and some significant scope for further consumption growth provided that household confidence holds up.

The pattern of consumption also remains heavily influenced by the pandemic, with spending on transport services and on hotels, cafes and restaurants still very depressed relative to the final quarter of 2019. In contrast, spending on vehicles, furnishings and household equipment, alcoholic beverages and communications remains elevated.

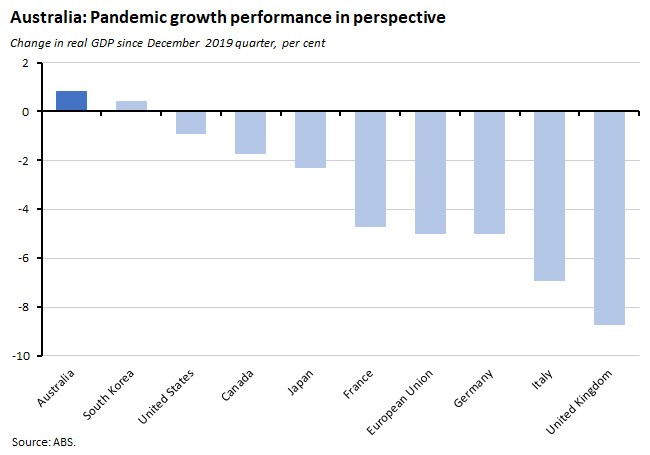

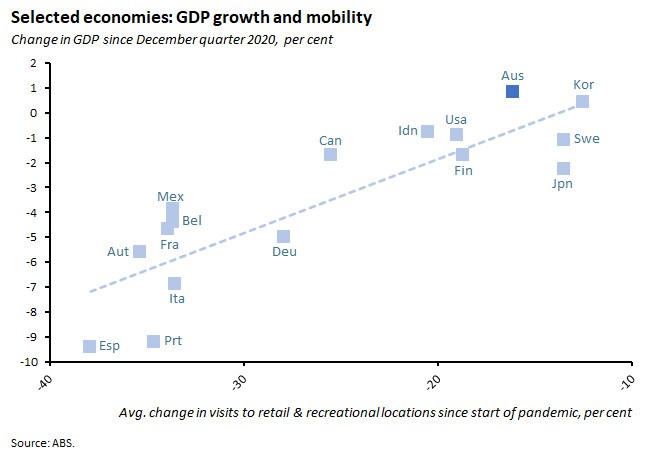

Finally, the ABS included a section this quarter looking at Australia’s GDP results in an international context. As the Bureau points out, Australia’s relative growth performance over the period since the pandemic looks pretty good relative to most other OECD economies. With real GDP 0.8 per cent higher than in December 2019, Australia is one of a handful of economies to have managed to get output back above pre-pandemic levels.

That growth outperformance reflects Australia’s success in controlling the pandemic which not only allowed a reduction in official restrictions on mobility, but which also boosted confidence in a way that underpinned changes in private, voluntary behaviour. The correlation between Australia’s relatively high levels of mobility and relatively strong GDP performance highlighted by the ABS serves both as evidence of past success in this regard but also argues against complacency regarding the pace of our vaccine rollout.

What happened:

At the 1 June meeting of the Reserve Bank Board, the RBA decided to leave all of its current monetary policy settings unchanged. The targets of 10 basis points for the cash rate and the yield on the three-year Australian Government bond, the parameters of the government bond purchase program, and the rate of zero per cent on Exchange Settlement balances were all left untouched.

In the accompanying statement, the RBA noted that while Australia’s economic recovery ‘is stronger than earlier expected and is forecast to continue’ and although ‘progress in reducing unemployment has been faster than expected,’ nevertheless ‘inflation and wage pressures are subdued. [And] While a pick-up in inflation and wages growth is expected, it is likely to be only gradual and modest.’

Reflecting this assessment, the RBA continued to pledge that:

‘It will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range. For this to occur, the labour market will need to be tight enough to generate wages growth that is materially higher than it is currently. This is unlikely to be until 2024 at the earliest.’

The statement also acknowledged the ongoing surge in the housing market, including rising investor interest, stating that:

‘Housing markets have strengthened further, with prices rising in all major markets. Housing credit growth has picked up, with strong demand from owner-occupiers, especially first-home buyers. There has also been increased borrowing by investors. Given the environment of rising housing prices and low interest rates, the Bank will be monitoring trends in housing borrowing carefully and it is important that lending standards are maintained’.

It also confirmed that Martin Place will use next month’s meeting to decide whether to retain the April 2024 bond as the target bond for the three-year yield target or to shift to the next maturity, the November 2024 bond, and will also consider the option of additional government bond purchases following the completion of the second $100 billion of purchases when the current bond-buying program concludes in September.

Why it matters:

Once again, and just as expected, this month’s meeting was yet another non-event in terms of monetary policy. The RBA is sticking with its view that while Australia’s recovery has been stronger and faster than expected, it still expects any pick-up in wage growth and inflation to be ‘gradual and modest’ and therefore does not anticipate an adjustment in the cash rate ‘until 2024 at the earliest.’

Still, there were a couple of notes of caution. Rising house prices means the RBA will be ‘monitoring trends in housing borrowing carefully’ and keeping an eye on lending standards. And in a recognition of recent developments in Victoria, this week’s statement also warned that an ‘important ongoing source of uncertainty is the possibility of significant outbreaks of the virus’ although it also added that ‘this should diminish as more of the population is vaccinated.’

Otherwise, we will have to wait until next month for any significant action on the monetary policy front. Decisions on the future of yield curve control (YCC) and of the RBA’s quantitative easing (QE) programs should then provide us with some important signals on the likely trajectory of monetary policy, as discussed in some detail after May’s meeting. In this context, several RBA watchers noted that a sentence relating to QE that appeared in the statement following the 4 May meeting (‘The Board is prepared to undertake further bond purchases to assist with progress towards the goals of full employment and inflation’) was dropped from the June statement in what some think may be an indicator of an RBA rethink in this area. We’ll find out in July.

What happened:

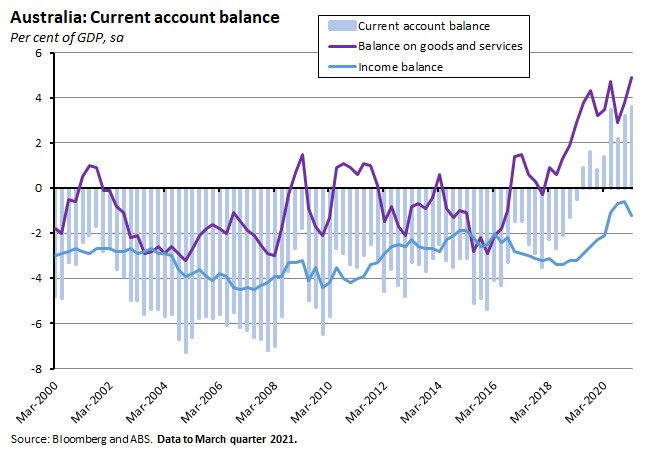

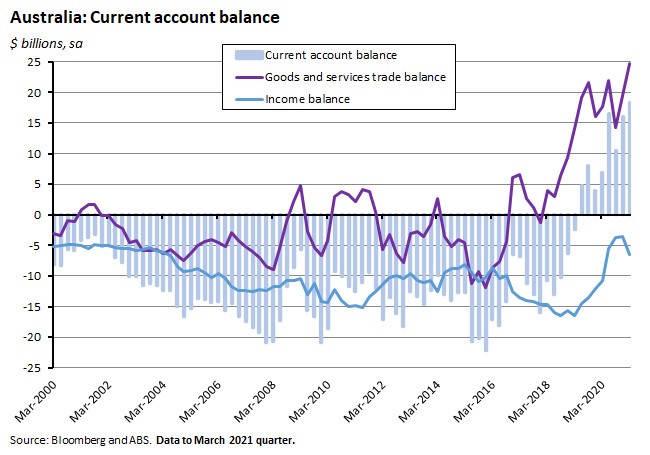

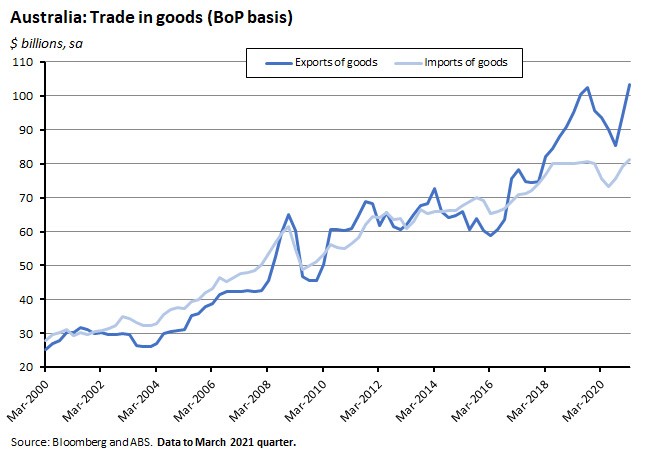

The ABS reported that Australia recorded a record current account surplus of $18.3 billion in the March quarter of this year, or about 3.6 per cent of GDP.

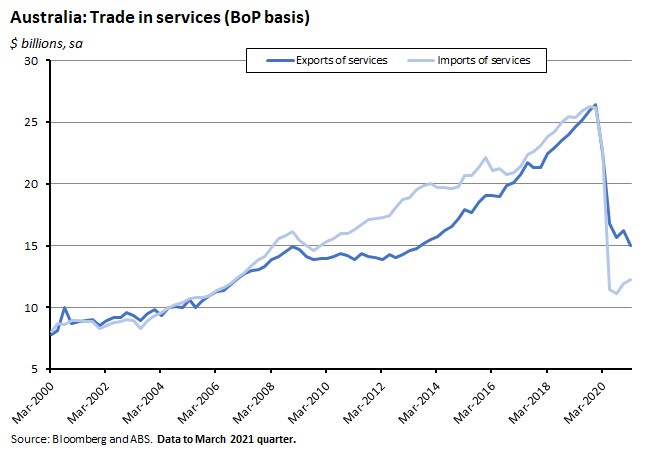

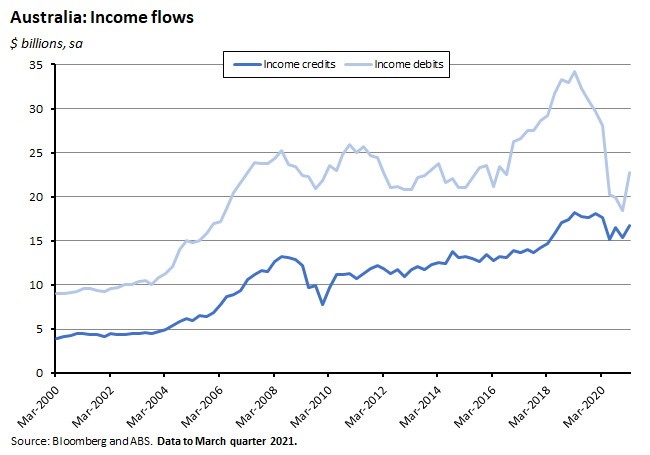

The overall surplus reflected a $22 billion merchandise trade surplus, a $2.7 billion surplus on services trade, a $6 billion net primary income deficit and a $0.3 billion secondary income deficit.

The capital and financial account recorded a deficit of $15.4 billion in the March 2021 quarter, reflecting a $15.2 billion deficit on the financial account driven by a net outflow of equity of $21.4 billion and a net inflow of debt of $6.2 billion.

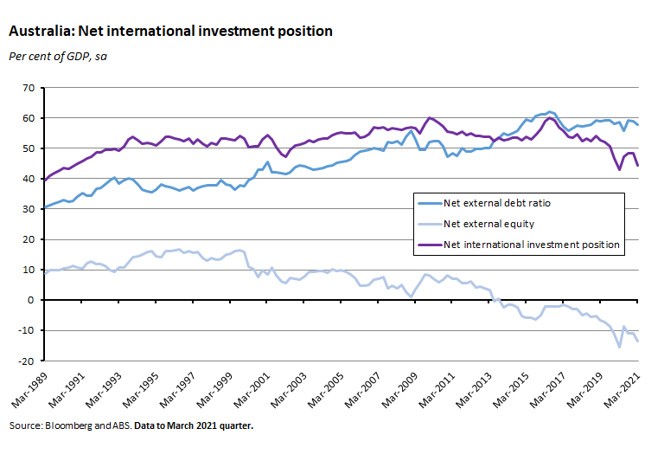

Australia's net international investment position (IIP) was a liability of $874.6 billion at the end of the March quarter, or about 44.4 per cent of GDP. That marked a fall of $75.4 billion on the (revised) 31 December 2020 position of $950 billion. Relative to end December last year, the net foreign debt liability position had fallen by $23.2 billion to $1,138.9 billion while the net foreign equity asset position had increased by $52.1 billion to $264.2 billion.

Why it matters:

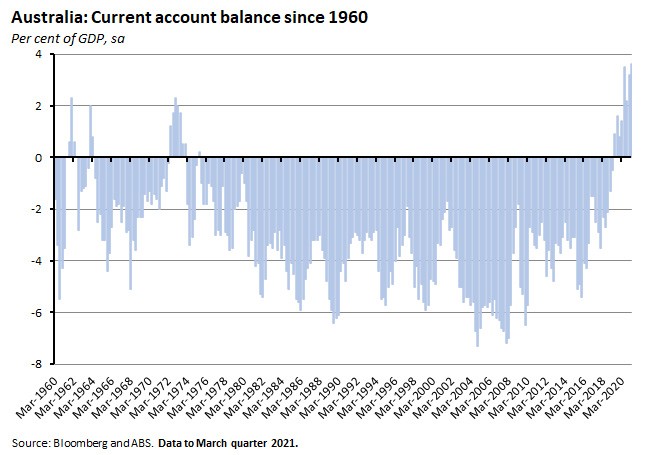

The March 2021 quarter’s record current account surplus means that Australia has now reported a surplus for eight consecutive quarters starting from Q2:2019. Not only does that mark a return to sustained surpluses not seen since the early 1970s but it now exceeds the run of seven consecutive surpluses achieved between Q2:1972 and Q4:1973, delivering the longest run of surpluses in considerably more than half a century.

In balance of payments terms, the main driver of this trend over the past two years has been the extremely strong performance of Australia’s goods exports, particularly iron ore, where dollar values have been pushed up by high prices. Exports of metal ores and minerals reached a record $48.2 billion in the March quarter of this year.

The current account surplus has also benefited from a smaller deficit on the income balance over recent years, as payments to overseas investors and creditors have fallen relative to receipts, although the deficit did widen this quarter as income debits increased.

What happened:

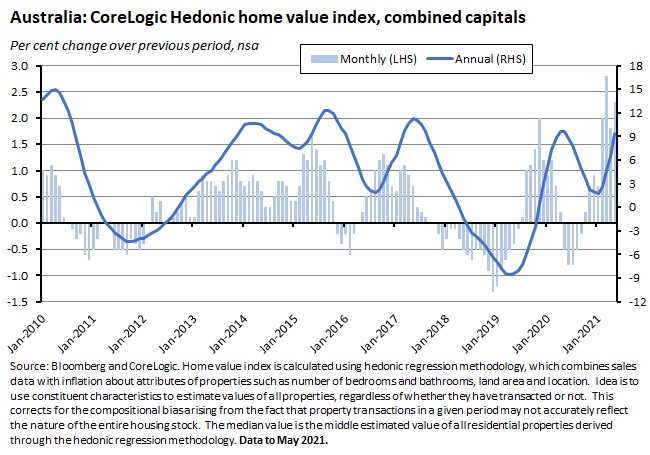

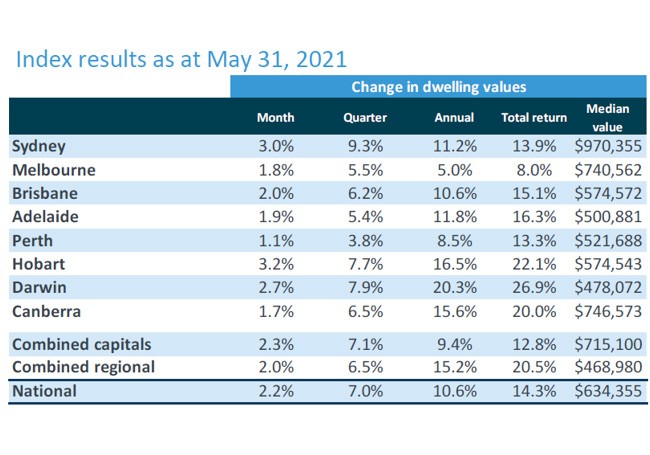

CoreLogic’s national home value index rose 2.2 per cent over the month in May 2021 to be up 10.6 per cent relative to May 2020. The combined capital city index was up 2.3 per cent over the month and 9.4 per cent over the year while the combined regional areas index was up two per cent in monthly terms and 15.2 per cent in annual terms.

Across the capital cities the rate of monthly increase varied from a 1.1 per cent increase in Perth up to a 3.2 per cent jump in Hobart, while in annual terms the gains ranged from a low of five per cent growth in Melbourne to a high of 20.3 per cent growth in Darwin – that city’s strongest annual gain on record.

CoreLogic also reported that a combination of strong demand and below-average supply was keeping auction clearance rates high – well above their decade average of around 64 per cent – although they have now slipped to below 80 per cent.

Why it matters:

Australia’s housing market boom continued in May with another strong monthly increase that beat April’s 1.8 per cent rise but was below the 32-year high of 2.8 per cent recorded in March this year. While the rate of house price appreciation has slowed since the end of the first quarter however, and auction clearance rates have come off a little, CoreLogic notes that housing values are still rising faster than the peak rate of growth in recent cycles.

The agency also highlighted the synchronised nature of the upswing, pointing out that values were up by more than one per cent across every capital city over the month, with both house and unit values climbing. And of the 334 sub-regions analysed by the agency, 97 per cent have recorded a lift in housing values over the past three months.

Finally, this month’s release also highlighted some changes in the underlying dynamics: after lagging regional price growth earlier in the year, capital city price growth has now outpaced its regional counterpart for the past two months; it’s now the most expensive end of the market that is seeing the highest rate of price appreciation across most capital cities, as opposed to earlier in the price cycle when the less expensive end of the market was outperforming; and Sydney has now recorded the largest capital gain over the past three months, surpassing the smaller capital cities that initially sparked the current boom.

What happened:

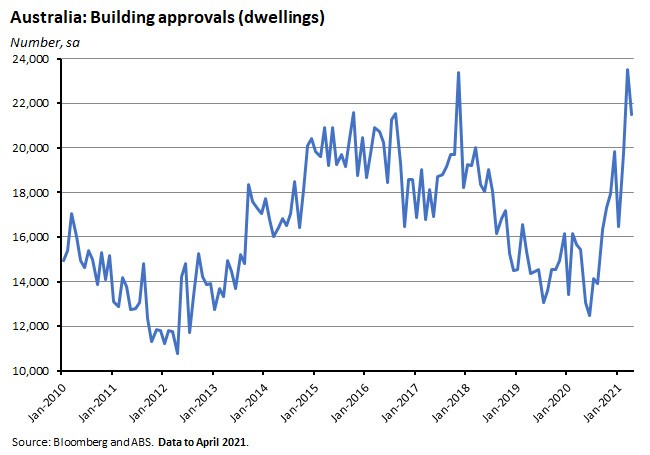

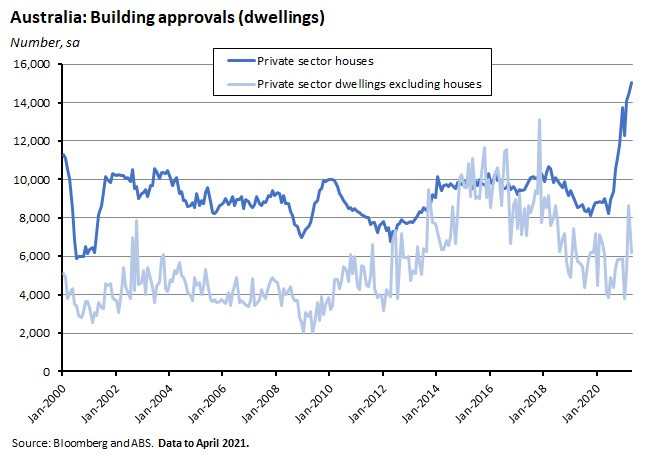

The ABS said that the seasonally adjusted estimate for total dwellings approved fell 8.6 per cent over the month in April but was still more than 39 per cent higher than the number of approvals in April 2020.

Approvals for private sector dwellings excluding houses fell 28.6 per cent over the month to be up 1.7 per cent over the year, while approvals for private sector houses rose 4.6 per cent month-on-month and jumped 67.4 per cent year-on-year.

The value of total building approved decreased 22.6 per cent over April with the value of total residential building down 7.1 per cent (comprising a 7.6 per cent fall in new residential building and a 3.8 per cent fall in residential alterations and additions) and the value of non-residential building slumping 43.2 per cent. The latter was mainly driven by a drop in the number of public sector approvals, falling back from the record high reached in March.

Why it matters:

The fall in the number of dwellings approved in April was driven by the sharp decline in approvals for private sector dwellings excluding houses. In contrast, approvals for private sector houses rose to a new record high. The ABS noted that since the introduction of the Government’s HomeBuilder grant in June last year, private house approvals have risen 84 per cent, and although the grant finished on 14 April this year, the Bureau said that this ‘did not have a material impact on the April building approvals data, as the building approval process typically occurs after the submission of the HomeBuilder application.’

What happened:

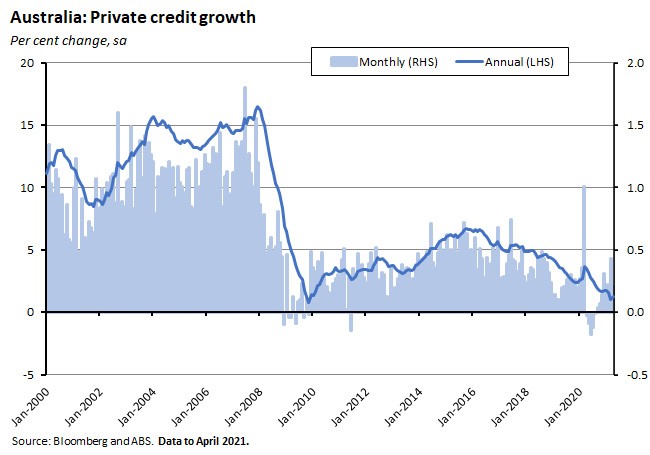

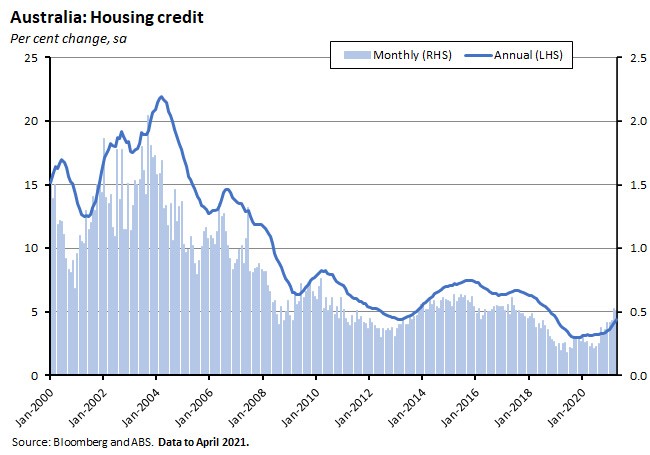

Data from the RBA show total private credit growth in the economy in April running at 0.2 per cent month-on-month (seasonally adjusted) and 1.3 per cent year-on-year.The value of total building approved decreased 22.6 per cent over April with the value of total residential building down 7.1 per cent (comprising a 7.6 per cent fall in new residential building and a 3.8 per cent fall in residential alterations and additions) and the value of non-residential building slumping 43.2 per cent. The latter was mainly driven by a drop in the number of public sector approvals, falling back from the record high reached in March.

Growth in housing credit was 0.5 per cent over the month and 4.4 per cent in annual terms.

Personal credit growth was flat over the month and down 7.8 per cent relative to April 2020 while business credit growth fell 0.3 per cent in April was down three per cent relative to the same month last year.

Why it matters:

Growth in both personal and business credit remained weak in April, but housing credit growth continue to demonstrate some momentum. Credit for owner-occupied housing is growing at 0.6 per cent in monthly terms and at 6.2 per cent in annual terms, while the corresponding rates of credit growth for investors are 0.4 per cent and 1.1 per cent, respectively.

What happened:

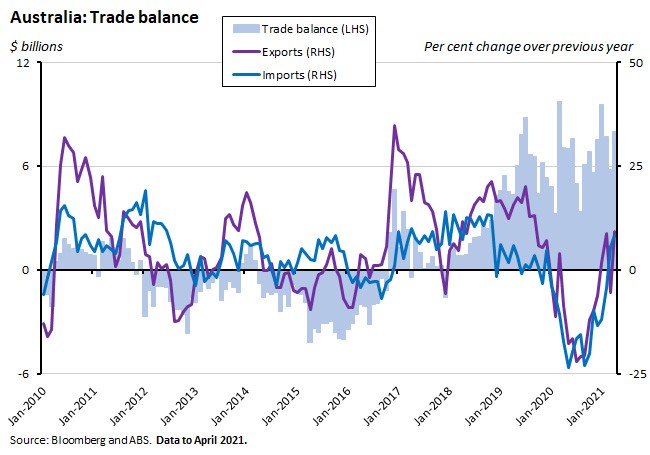

The ABS reported that the balance on international trade in goods and services rose $2.2 billion to $8 billion (seasonally adjusted) in April this year. Exports of goods and services were up three per cent over the month and 9.3 per cent over the year while imports of goods and services fell three per cent over the month but were up 8.2 per cent over the year.

Why it matters:

Following on from a record current account surplus in the first quarter of this year (see earlier story), April delivered another large trade surplus to kick off the second quarter.

What happened:

The final estimate for retail turnover in April 2021 was a 1.1 per cent monthly increase and a 25 per cent jump relative to April 2020 (when the sector was disrupted by widespread lockdowns).

Why it matters:

The final estimate for retail turnover was unchanged from the preliminary estimate we discussed in the previous edition of the Weekly.

. . . and what I’ve been following in the global economy.

What happened:

The May 2021 OECD Economic Outlook was published. The OECD’s new forecasts see global real GDP growth rising to 5.8 per cent this year before slowing to 4.4 per cent in 2022, while growth across the OECD is expected to be 5.3 per cent this year and 3.8 per cent next year. That growth projection for this year represents a significant upgrade on the OECD’s December 2020 forecasts, which had predicted growth of 4.2 per cent for 2021.

The Outlook’s projections imply that the world economy has returned to pre-pandemic levels of activity, but also that output will still be below what was expected pre-crisis even by the end of next year: the OECD reckons that global income will still be some US$3 trillion less by end-2022 than was expected before the crisis hit. That’s a shortfall roughly equivalent to the size of the French economy.

Global growth is assumed to be powered by strong fiscal stimulus in the United States (the OECD sticks with its earlier view that President Biden’s US$1.9 trillion American Rescue Plan package could raise US output by between three and four per cent in the first full year following implementation (the four quarters to 2021Q1), and lift global output by around one per cent) and a successful vaccine rollout. In the case of advanced economies, the Outlook assumes that the rollout of effective vaccines will be completed by the (Northern) autumn of this year, allowing the relaxation of restrictions on a range of activities. As a result, increased confidence, stronger labour market conditions and a gradual decline in household saving ratios are all also expected to help support activity into next year.

For emerging economies, however, the OECD judges that prospects for an early finalisation of vaccination programs are much more limited, and – with some important exceptions – growth prospects will suffer as a result.

The Outlook’s projections imply that the world economy has returned to pre-pandemic levels of activity, but also that output will still be below what was expected pre-crisis even by the end of next year: the OECD reckons that global income will still be some US$3 trillion less by end-2022 than was expected before the crisis hit. That’s a shortfall roughly equivalent to the size of the French economy.

Global growth is assumed to be powered by strong fiscal stimulus in the United States (the OECD sticks with its earlier view that President Biden’s US$1.9 trillion American Rescue Plan package could raise US output by between three and four per cent in the first full year following implementation (the four quarters to 2021Q1), and lift global output by around one per cent) and a successful vaccine rollout. In the case of advanced economies, the Outlook assumes that the rollout of effective vaccines will be completed by the (Northern) autumn of this year, allowing the relaxation of restrictions on a range of activities. As a result, increased confidence, stronger labour market conditions and a gradual decline in household saving ratios are all also expected to help support activity into next year.

For emerging economies, however, the OECD judges that prospects for an early finalisation of vaccination programs are much more limited, and – with some important exceptions – growth prospects will suffer as a result.

Turning to the ongoing inflation debate, the Outlook notes that there have been signs of higher input cost pressures. It explains the recent upturn in headline inflation in terms of the recovery of oil and other commodity prices, a surge in shipping costs, the normalisation of prices in hard-hit sectors as restraints are eased and one-off factors such as tax changes, and argues that many of these pressures are likely to ease in the near term. The OECD’s view is that with significant spare capacity across the world economy – it doesn’t think that unemployment rates will return to pre-pandemic lows in many countries until after the end of next year – there is unlikely to be a sustained increase in underlying inflation.

The OECD points to both upside and downside risks to its Outlook:

- It warns that there is ‘the possibility of new more contagious and lethal variants [of the virus] that are more resistant to existing vaccines unless effective vaccinations are quickly and fully deployed everywhere. That could require ‘the reimposition of strict containment measures, with associated economic costs related to lower confidence and spending.’

- On the other hand, if progress with vaccination roll outs are faster than assumed, the recovery would be faster and stronger.

- Another upside risk is that households could choose to run down some of the ‘excess’ savings built up during the pandemic, mainly in advanced economies.The OECD’s baseline assumes that much of this higher saving will be retained or used to pay down debt, but instead households could choose to use this to fund higher consumption.Note the parallel here with the RBA’s May 2021 Statement on Monetary Policy which also includes three scenarios based around different developments in household consumption.

- And if the recovery did turn out to be stronger than expected, that would also add to existing inflation risks.

In the case of Australia, the OECD thinks that real GDP will grow by 5.1 per cent this year and 3.4 per cent in 2022. It is cautious on the unemployment rate, which it only sees falling to five per cent next year. On inflation, after managing to reach two per cent this year, the headline rate of price increase is expected to fall back to below the bottom of the RBA’s target band in 2022, at 1.7 per cent.

On the macro policy front, the OECD is in broad agreement with the RBA, recommending that the stance of monetary policy should remain accommodative given the Outlook’s forecasts for inflation to remain below the target band. It also notes that ‘further fiscal support and bond purchases may be needed if the recovery falters or inflation undershoots. Additional targeted support may also be needed where international border closures and remaining physical distancing restrictions have the largest impact.’

Why it matters:

The OECD forecast upgrade for world growth this year is a substantial one, but not particularly surprising. Confidence in the global recovery has risen since the end of last year and the OECD’s new numbers are broadly in line with IMF’s March 2021 projections for six per cent growth this year and 4.4 per cent growth in 2022, for example. Likewise, while the OECD projections for Australia are somewhat lower than those set out in the RBA’s May Statement on Monetary Policy (which put average real GDP growth at 5.25 per cent this year and four per cent next year) they are certainly not indicating a dramatically different baseline scenario.

The Outlook also comes with the upfront caveat that ‘this is no ordinary recovery’ but rather one that the OECD reckons is ‘likely to remain uneven and dependent on the effectiveness of vaccination programmes and public health policies.’ It is also expected to be a multi-speed recovery. The OECD’s projections see Korea and the United States reaching pre-pandemic per capita income levels after about 18 months, for example, while much of Europe is expected to take nearly three years to recover and in some emerging markets, such as Mexico and South Africa, the recovery period could take between three and five years.

The accompanying warnings on vaccine rollout for both the global and Australian economies are also well worth keeping in mind. In our case, for example, the Outlook cautioned that the ‘vaccine rollout represents a risk in both directions. On the downside, without widespread vaccination, the economy is vulnerable to a sizeable outbreak and accompanying restrictions, and delays to skilled immigration could crimp growth.’

What I’ve been reading . . .

The Treasury Secretary’s opening statement to the Economics Legislation Committee. Dr Kennedy included an appropriate note of caution here, stating that ‘The mixed global position clearly shows that the pandemic is not over and that risks to Australia and the global recovery remain heightened. The recent outbreak in Melbourne again reinforces this point.’ Even so, his view was that ‘Momentum in the economy, the rollout of vaccines and continued fiscal and monetary policy support are expected to continue to drive broad-based growth over the next few years. The prospects for this are sound given strong household and business balance sheets, record job vacancies and high levels of consumer and business confidence’ as well as improved investment expectations. He also provided an update on how the labour market has coped with the end of JobKeeper, reporting that across the four weeks since the end of the program about 56,000 former JobKeeper workers lost employment. That compares with a normal monthly rate of labour market ‘churn’ (the number of people moving into and out of employment) of around 400,000.

Richard Holden on the good news in last week’s private capex numbers.

Brad Jones, Head of Economic Analysis at the RBA, delivered an interesting take on uncertainty and risk aversion – before and after the pandemic. Pre-pandemic, Jones suggests that uncertainty and risk aversion were high in the global economy reflecting some combination of lingering insecurity following the global financial crisis (GFC) and the Eurozone crisis, fears of a household debt overhang in some large advanced economies, international trade and political uncertainty (think US-China trade wars and Brexit, for example), and the growing global influence of risk averse investors, led by central banks in emerging market economies and retirees in advanced economies. environment then boosted desired saving relative to investment and so helps explain three ‘puzzles’ of the pre-pandemic world economy: (1) Very low neutral interest rates, beyond what could be explained by factors like population, potential GDP growth or the returns to capital; (2) subdued business investment and corporate risk-taking despite high profits and easy financing conditions; and (3) the investor premium for safe assets. What about post-pandemic? On the surface, the pandemic might be expected to have similar effects on risk aversion and uncertainty as previous crises such as the GFC. But Jones thinks there are two good reasons for thinking that this won’t be the case. First, the nature of the pandemic shock (and of the subsequent recovery) is very different from its predecessors. And second, many Australian household and business balance sheets are now in better shape than they were before the pandemic.

The RBA’s June 2021 chart pack is now available.

ANZ Bluenotes charts what happened to Australian wage deposits after the end of JobKeeper.

Productivity Commission Chair Michael Brennan gave a speech on Recession, Recovery and Reform. A key theme here is that ‘forced innovations’ from the pandemic provide the opportunity to ‘transform existing business models and production processes’ and boost productivity. His examples of such forced innovations are telehealth, online education, the increase in working from home and the uptake of online shopping.

A new report from Grattan on rethinking Australia’s skilled migration program.

I’m a bit late linking to this, but for those who haven’t read it already, Max Suich’s recent series in the AFR on Australia-China relations makes for a provocative read. There are three parts: How Australia got badly out in front on China; China confrontation: What were we thinking; and US-Australia alliance on China shows it’s best to go early, go hard.

Related, the Australia in the World podcast talks to Linda Jacobson on China (part 1). Part 2 is http:here.

And for a different perspective on these issues, here is Malcolm Turnbull launching Peter Hartcher’s new book Red Zone: China’s challenge and Australia’s Future at the Lowy Institute. This is the audio version. Video version is here.

Marcus Hellyer with ASPI’s defence budget brief 2021-22. Consolidated defence expenditure is $44.6 billion or almost 2.1 per cent of GDP for 2021-22. Although Hellyer reckons the government is doing a good job meeting the commitments made in the 2016 White Paper and subsequent 2020 Defence Strategic Update, his view is that ‘there are significant questions about how efficiently Defence is spending [and] there are even bigger questions about whether its spending it on the right things in the first place…huge investment is planned in capabilities that appear to have minimal deterrent effect on a great-power adversary…the force structure and timelines for delivery are holdovers from previous strategic planning documents developed in circumstances that bear little resemblance to our current one.’

Alex Evans examines Budget 2021-22’s move to reactivate the Corporate Collective Investment Vehicle.

The NSW Productivity Commission sets out 60 proposals for rebooting the state economy.

ABC Business on the changing prospects for a gas-fired recovery.

John Quiggin canvasses the end of the population pyramid. Are economic concerns around ageing populations an outdated relic of twentieth century thinking? Quiggin argues that the old view rests on the assumption that most work required young, strong workers to do physically demanding tasks. That world no longer applies, with extended working lives at one end of the age distribution and much more time spent in training and education at the other.

Ian Goldin and colleagues revisit the causes of the pre-pandemic stagnation in productivity performance in major advanced economies. Their verdict? Blame a combination of mismeasurement, slowdowns in capital deepening (for cyclical and structural reasons), spillovers from intangibles, trade integration, and the contribution of allocative efficiency (the drag on productivity from a decline in business dynamism, captured by a decline in business entry and exit rates and an increase in pure profits and market concentration).

An FT Big Read on Wall Street’s new love affair with China. Decoupling - what decoupling?

Also from the FT, Martin Wolf sets out why the 2020s will be a decisive decade for the UK. It must ‘grapple with recovery from Covid-19, the aftermath of Brexit, an ongoing technological revolution and the transition to net-zero emissions of greenhouse gases.’ While details differ, many of these challenges obviously resonate beyond the UK. Replace Brexit with Australia-China relations, for example, and that list would work fairly well for us, too.

The IMF on the New Zealand economy.

And IMF economists argue that current debt projections (which imply a quick stabilisation in post-COVID public debt ratios followed by a decline) may be too optimistic.

The Economist foresees a coming boom in business investment. Pre-pandemic, business investment had been weak across much of the world economy, but now the pandemic and its aftermath has boosted demand for – and therefore investment plans in – businesses in the global tech sector, discretionary consumer spending industries, and the shipping sector.

Inside Operation Warp Speed. A ‘triumph and validation of industry policy’?

Bloomberg economics says that COVID-19 has changed economics: ‘In the US…a blitz of public spending pulled the economy out of the deepest slump on record—faster than almost anyone expected—and put it on the verge of a boom. The result could be a tectonic transformation of economic theory and practice.’ Fiscal policy has taken the lead from monetary policy across the world economy, governments have channelled cash payments directly to households and businesses, and the financial sector was protected from the bottom up (making sure that firms and individuals had the cash to maintain payments) rather than the top down. Will the revolution in economic policy stick? Much will depend on the intensifying debate about prospects for inflation.

Adrian Wooldridge on meritocracy: contrary to some recent critiques, he argues, the problem is not with the idea of meritocracy itself but rather ‘the corruption of meritocracy by money, family connections and favouritism.’

Latest news

Already a member?

Login to view this content