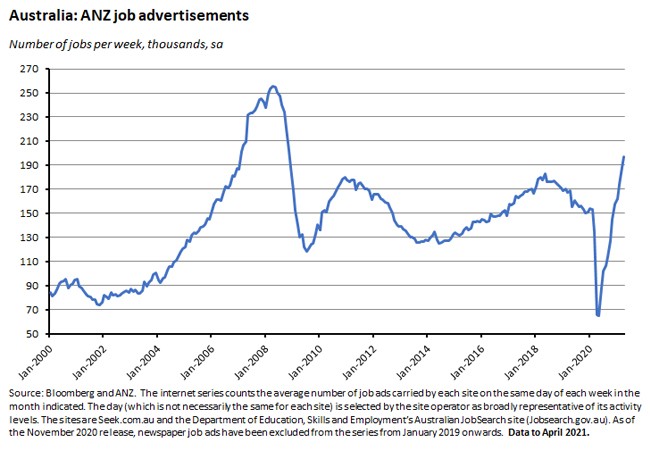

At its 4 May meeting the RBA again left all of its key policy settings unchanged despite flagging new and more optimistic forecasts for growth and unemployment. It also promised decisions on its yield curve control and asset purchase programs at the July Board meeting. As of April, ANZ job ads were almost 28 per cent higher than their pre-COVID level.

The CoreLogic national home values index climbed 1.8 per cent in April to be more than 10 per cent higher than last September’s COVID low. Lending to households reached a new record high in March, indicating more house price rises ahead. The total number of dwellings approved in March was the second highest on record while private sector house approvals set a new record high. Australia’s trade surplus slipped to $5.6 billion in March from $7.6 billion in February. Ahead of next week’s budget, data from last Friday showed that the underlying cash deficit in the financial year to March was $29.5 billion smaller than as projected in December’s Mid-Year Economic and Fiscal Outlook (MYEFO).

I have included a short budget preview below this week’s Australian data roundup. For those keen on (much) more detail, I’ve also added a selection of budget predictions and previews in part one of this week’s readings.

Part two of this week’s readings includes the RBA’s Guy Debelle on monetary policy during COVID, the ABS on how Australian businesses are adjusting operations in response to the pandemic, the FT’s take on Australia’s coal mining dilemma, the radicalisation of Paul Krugman, Greensill Capital and the Medici Bank, financial markets and UFOs, and a book seminar on one of last year’s most interesting SF novels.

Next week is budget week, and there’ll be no weekly note. Instead, there will be a quick take on the budget that should go out to members on budget night, and then another assessment in the form of a webinar next Thursday. And if you’d like even more budget, then the next Dismal Science podcast will provide a further fiscal fix. Normal weekly note service should then resume the following week.

Finally, here’s a link to our latest Director Sentiment Index (DSI), which recorded the largest jump in the history of the series and moved back into positive territory for the first time since 2018, and which also delivered some very interesting results on climate change policies. Many thanks to all of you who took the time to complete what is a pretty length survey. We really value your participation.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

At the 4 May meeting of the Reserve Bank Board, the RBA decided to maintain its current policy settings. The targets of 10bp for the cash rate and the yield on the three-year Australian government bond were left unchanged, as were the parameters of the Term Funding Facility (TFF) and the government bond purchase program.

The accompanying statement noted that the ‘economic recovery in Australia has been stronger than expected’ and that this is ‘forecast to continue.’ It added that:

‘The Bank's central scenario for GDP growth has been revised up further, with growth of 4¾ per cent expected over 2021 and 3½ per cent over 2022. A pick-up in business investment is expected and household spending will be supported by the strengthening in balance sheets over the past year. The unemployment rate is expected to continue to decline, to be around five per cent at the end of this year and around 4½ per cent at the end of 2022.’

Despite the strong recovery in activity, however, the statement also noted that ‘inflation pressures remain subdued in most parts of the Australian economy’, citing last week’s soft CPI reading. According to the RBA’s new forecasts:

‘A pick-up in inflation and wages growth is expected, but it is likely to be only gradual and modest. In the central scenario, inflation in underlying terms is expected to be 1½ per cent in 2021 and two per cent in mid-2023. In the short term, CPI inflation is expected to rise temporarily to be above three per cent in the June quarter because of the reversal of some COVID-19-related price reductions.’

Other points to note:

- The RBA said that, given ‘the environment of rising housing prices and low interest rates, the Bank will be monitoring trends in housing borrowing carefully and it is important that lending standards are maintained.’

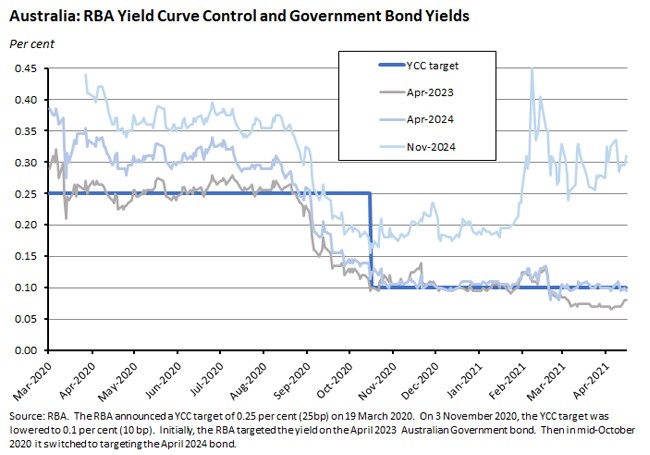

- At the July meeting, ‘the Board will consider whether to retain the April 2024 bond as the target bond for the 3-year yield target or to shift to the next maturity, the November 2024 bond. The Board is not considering a change to the target of 10 basis points.’

- And at that same meeting, ‘the Board will also consider future bond purchases following the completion of the second $100 billion of purchases under the government bond purchase program in September.’

- July will also mark the end of the TFF, with the statement noting that the Board is not considering a further extension of the program.Final drawings under the TFF will be on 30 June this year.

Finally, in terms of guidance, the RBA continues to say that it ‘will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range. For this to occur, the labour market will need to be tight enough to generate wage growth that is materially higher than it is currently. This is unlikely to be until 2024 at the earliest.’

Why it matters:

Once again, the latest monetary policy meeting was pretty much a non-event in terms of policy decisions, with the RBA leaving all of its policy levers unchanged. And once again, that was just as expected.

Instead, the main focus this month was on how the recent strong flow of economic data, particularly from the labour market, would influence the RBA’s latest set of forecasts. Those are due be released in detail on Friday in the May Statement on Monetary Policy. And the key related question was whether those new forecasts would have significant implications for the future trajectory of policy.

On the former, the statement gave us a preview of the critical changes:

- Forecast GDP growth for this year has been upgraded to 4.75 per cent, which compares to a previous year-average forecast of four per cent and a year-end projection of 3.5 per cent.

- The RBA’s forecast for unemployment at the end of this year has been cut from six per cent to five per cent, while the forecast for end-2022 has been cut from 5.5 per cent to 4.5 per cent.

- Underlying inflation is now expected to be 1.5 per cent in 2021, slightly stronger than the previous forecast of 1.25 per cent.It is then expected to rise to two per cent by mid-2023 compared to the previous forecast of 1.75 per cent.

The big changes here are for the labour market, where the rate of improvement is now expected to be much quicker than the RBA had previously anticipated: for example, the unemployment rate is now forecast to be just five per cent by the end of this year – a low last seen in early 2019, well before the pandemic. Importantly, however, these expectations for a stronger labour market have generated only a modest change in the RBA’s inflation outlook: by mid-2023, underlying inflation is still only expected to be at two per cent.

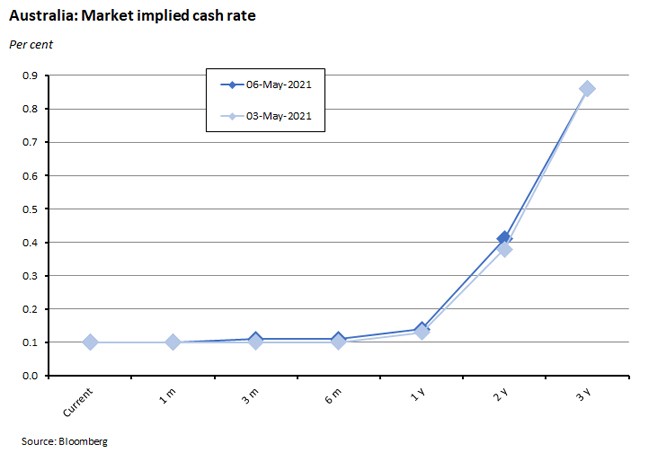

What does this mean for the trajectory of the cash rate? In the short-term, very little: the RBA’s guidance this month continued to be that no changes are likely until 2024, although some RBA watchers did point to a tweak in the bank’s wording on this point: after the last three statements have ended with ‘The Board does not expect these conditions to be met until 2024 at the earliest’ this month’s statement concluded with ‘This is unlikely to be until 2024 at the earliest.’ Hardly a radical change, but a change, nevertheless. All else equal, a more optimistic forecast must mean that the probability of an earlier move has increased – it’s just not clear whether that increase is material. Market implied pricing did edge slightly higher after the meeting, for example, but it was an extremely modest move.

Aside from the new forecasts, the other piece of ‘news’ was the end of the TFF. Back in February, in his speech on the year ahead, Governor Lowe noted that: ‘Banks are able to draw on the facility up until end June, which means they will have the benefit of low-cost funding out to mid-2024. The Board would consider extending this facility if there were a marked deterioration in funding and credit conditions in the Australian financial system.’ No such deterioration has occurred, and the bank’s view is that the state of funding and credit conditions mean that further support from the TFF is no longer required.

If the May meeting was something of (another) damp squib, however, it did signal that July’s meeting is shaping up to be more interesting. That’s because we will get a better read on any future policy shift as the RBA has committed to making decisions then on yield curve control (YCC) - will it stick with the April 2024 bond or shift to the November 2024 bond for its target? - and whether the current round of asset purchases (QE2) will be followed by a third (QE3). Both choices should allow us to gauge the bank’s thinking on how much monetary support is still required.

Why the focus on whether the RBA will shift to targeting the November 2024 Australian government bond? Remember, back on 19 March 2020, when the RBA first announced it was introducing YCC (then at 0.25 per cent), it said that it was choosing to target the three-year yield for two reasons. First, because that maturity was important for funding rates in the Australian economy. And second, because three years fit with the RBA’s sense of how long it planned to keep the cash rate unchanged. That same logic persisted when the cash rate and the YCC target were both lowered to 0.1 per cent on 3 November 2020.

That second reason means that YCC is also partly related to the RBA’s forward guidance on monetary policy, and specifically to the part of that forward guidance that is calendar-based (the one that says that an increase in the cash rate ‘is unlikely to be until 2024 at the earliest’).* The three-year yield target is for the Australian Government bond nearest to a three-year maturity. When YCC was first introduced, the target bond was the April 2023 maturity. In mid-October 2020, it then switched to the April 2024 maturity. And in comments on monetary policy he made in March this year, Governor Lowe noted that ‘The Board has…discussed the question of whether to keep the April 2024 bond as the target bond, or to move to the next bond – that is the November 2024 bond – later this year. If we were to keep the April 2024 bond as the target bond, the maturity of the yield target would gradually decline as time passes until the bond finally matures in April 2024.’ So, if the RBA were to shift the target to the November 2024 bond, it would be indicating that it thinks no cash rate change is likely until at least the second half of 2024. And if it chooses not to do so, it would be signalling that the maturity of the YCC target would be falling over time, and therefore that any potential change would likely no longer be a full three years out.

*Note that the RBA also uses outcomes-based forward guidance, relating the future stance of monetary policy to the rate of inflation (‘actual inflation is sustainably within the two to three per cent target range’) and of the rate of wage growth it thinks will be needed to deliver it (likely above three per cent).

What happened:

ANZ job ads rose 4.7 per cent over the month in April to 196,612. That’s almost double the number of ads in April 2020 during the pandemic lockdown.

Why it matters:

Job ad are now almost 28 per cent higher than their pre-COVID (January 2020) level and based on past relationships, are consistent with further falls in the unemployment rate.

That should help to offset some of the likely negative impact of the end of JobKeeper, which is expected to start to show up in the unemployment rate from April onwards with Treasury previously estimating that between 100,000 and 150,000 workers could lose their jobs after the program finished at the end of March this year.

What happened:

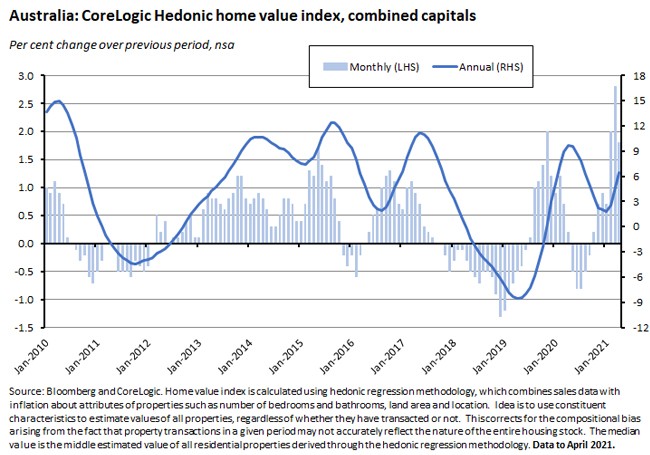

The CoreLogic national home value index rose by 1.8 per cent in April to be up 7.8 per cent over the year. The combined capital index was up 1.8 per cent month-on-month and 6.4 per cent year-on-year while the corresponding gains for the combined regional index were 1.9 per cent and 13 per cent, respectively.

Prices rose over the month in every capital city in April, with the largest monthly gains in Darwin (up 2.7 per cent), Sydney (2.4 per cent) and Adelaide (two per cent) and the smallest rise in Perth (up 0.8 per cent). In annual terms, Darwin, Canberra and Hobart lead the pack.

Houses continue to out-perform units, according to CoreLogic, with combined capitals house values rising at about twice the pace of unit values (8.6 per cent vs 4.3 per cent) over the first four months of this year.

In other signs of continued market strength, although auction clearance rates have come off recent highs, they remain above 80 per cent, the median selling time has fallen to a record low of just 26 days, and the median discount rate has likewise fallen to a record low of just 2.7 per cent across the combined capitals.

With housing values rising at a faster pace than rents, rental yields have been trending down. Nationally, Corelogic estimates that the gross rental yield has eased from 3.7 per cent last year to a record low of 3.5 per cent. In Sydney, yields now average just 2.69 per cent and in Melbourne they are down to 2.87 per cent.

Why it matters:

The rate of month-on-month growth in home values slowed in April, easing to 1.8 per cent after having hit a 32-year high of 2.8 per cent in March, and CoreLogic judge that further moderation lies ahead. Even so, that still leaves home prices high and rising, with values up 6.8 per cent over the past three months and 10.2 per cent higher than last September’s COVID low.

CoreLogic pointed to increasing pressure on affordability as one likely source of the modest easing in the pace of house price appreciation last month, noting that there was some sign of lower activity in the price-sensitive category of first home buyers. A second factor at work is that supply has been responding to higher prices: 40,630 new residential property listings were added to the national market over the four weeks to 25 April, a rate which is almost 14 per cent above the five-year average. Even so, total advertised stock levels were still 25 per cent below their five-year average in late April, so buyer demand is continuing to push on supply.

Finally, the presence of low yields across Australia’s capital cities is now indicating a significant imbalance between prices and rents.

What happened:

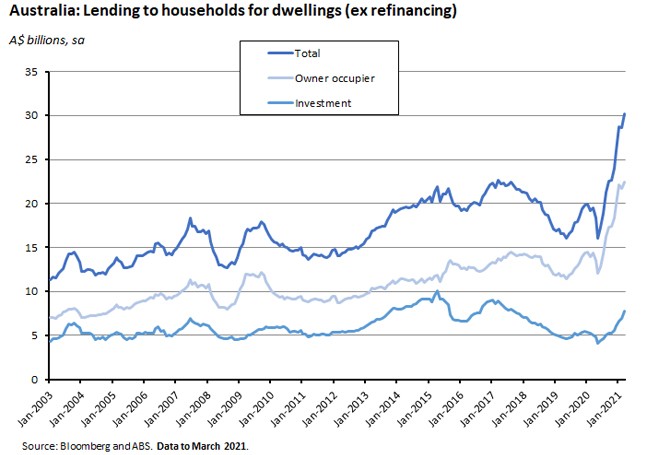

The ABS said that new lending for housing rose 5.5 per cent over the month in March to be up 55.3 per cent over the year. Lending to owner-occupiers was up 3.3 per cent over the month and 55.6 per cent over the year, while lending to investors jumped 12.7 per cent over the month to be up 54.3 per cent in annual terms.

Why it matters:

Lending to households hit a new record high ($30.2 billion) in March. Notably, lending to investors accounted for half of the monthly increase in what was the largest gain since July 2003. That strong activity suggests that although price momentum might have eased in April (see story above), prices are still set to rise further.

The ABS also noted that the value of owner occupier loan commitments for the construction of new dwellings fell 14.5 per cent in what was the first fall since the HomeBuilder grant was introduced in June 2020 (the grant was reduced from $25,000 to $15,000 with effect from 1 January this year).

What happened:

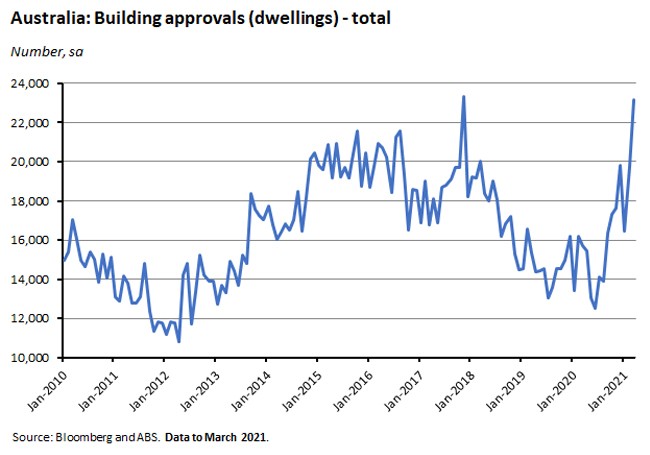

According to the ABS, the total number of dwellings approved rose 17.4 per cent (seasonally adjusted) over the month in March to be more than 47 per cent higher than in the same month last year.

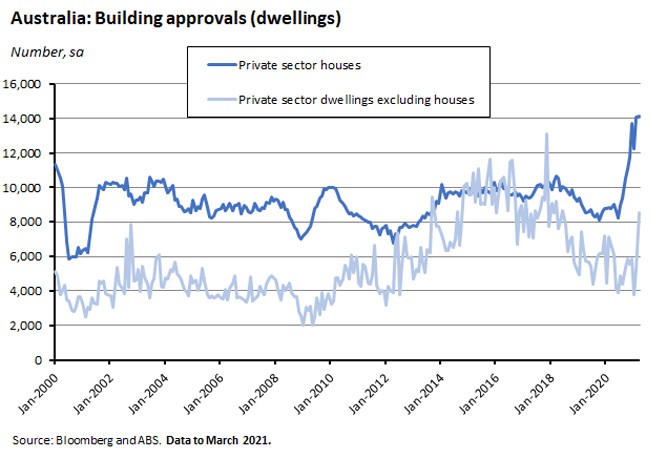

Approvals for private sector dwellings excluding houses soared by 63.6 per cent over the month and were up more than 27 per cent in annual terms, while approvals for private sector houses were almost flat in March, rising by just 0.1 per cent from February, but were still up 60.9 per cent over the year.

The ABS also reported that the value of non-residential building approved rose 59.4 per cent over the month, with that increase reflecting a strong rise in both private and public projects approved.

Why it matters:

The consensus forecast had been for a three per cent monthly increase in total approvals, so the actual rise of more than 17 per cent – driven by strong growth in approvals for units and town houses – far exceeded expectations. Indeed, the total number of dwellings approved in March was the second highest on record, behind only the November 2017 result.

The ABS continues to attribute the high level of private sector house approvals, which also hit a new record high, to the impact of the HomeBuilder scheme. That program concluded at the end of March, however, so going forward the impact should now drop out of the numbers.

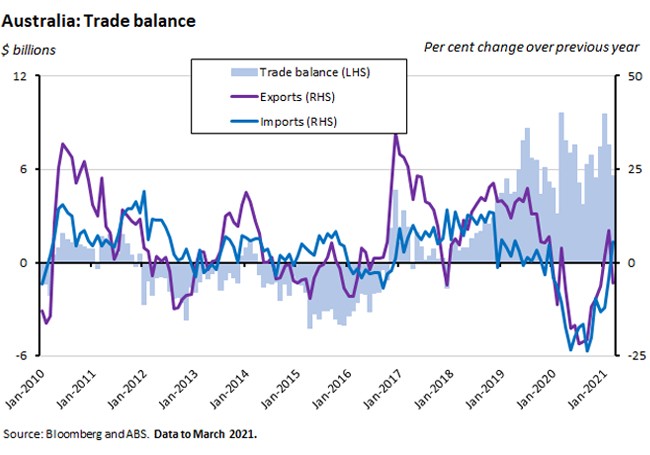

What happened:

Australia recorded a trade surplus of $5.6 billion (seasonally adjusted) in March, down from $7.6 billion in February and $9.5 billion in January. Exports of goods and services fell two per cent over the month and were down 5.6 per cent in annual terms while imports were up four per cent month-on-month and 5.7 per cent year-on-year.

Why it matters:

The consensus forecast had been for an $8.2 billion trade surplus in March, so while the actual surplus was quite substantial, it was well-down on expectations. It was also well down on the January and February outcomes. A key driver of the monthly decline in the surplus relative to February was trade in non-monetary gold, which is often quite volatile month to month: exports were down 25 per cent while imports surged 117 per cent.

What happened:

Last Friday, the Minister of Finance released the Australian Government General Government Sector Monthly Financial Statements for March 2021. The data allow for a comparison between the actual budgetary outcomes for the 2020-21 financial year through to March and the expected monthly profile based on December’s Mid-Year Economic and Fiscal Outlook (MYEFO) estimates. The key results were:

- The underlying cash balance for 2020-21 in the (financial) year to 31 March was a deficit of $133.3 billion.That compares to the MYEFO projection of a deficit of $162.7 billion – representing an improvement of about $29.5 billion.

- Total receipts were $16.9 billion higher than the 2020-21 MYEFO profile while total payments were $12.6 billion lower than the MYEFO profile.

Why it matters:

The March monthly statement tells us that the actual budget deficit for 2020-21 will be significantly smaller than expected either at the time of November’s budget or after the revisions made in December’s MYEFO. A much stronger and faster economic recovery than anticipated in the official forecasts is a large part of the story, resulting in less need for policy support and therefore lower payments related to JobKeeper and JobSeeker as well higher revenues from more consumer activity. Another important factor has been the global economic recovery which has contributed to higher commodity prices in general, and robust economic growth in China in particular, which has helped drive iron ore prices that are substantially higher than those that were baked into the budget assumptions. That in turn has also contributed to revenue outperformance.

Importantly, all this means that the starting position for Budget 2021-22 will be significantly stronger than the Treasurer would have expected when he was announcing Budget 2020-21.

. . . and what I’m looking forward to in next week’s budget.

What will happen:

Next Tuesday, the Treasurer will announce the 2021-22 Federal Budget. Last week, in his 29 April speech on budget strategy, the Treasurer explained the context:

‘This will be another pandemic budget being delivered in the midst of a once in a hundred-year pandemic and just seven months after the last budget. The Budget will lay out the next phase of Australia’s economic recovery plan, to grow our economy so we can deliver the jobs and guarantee the essential services Australians rely on and keep Australians safe.’

Josh Frydenberg also stressed that the objective of next week’s budget would be to ‘drive the unemployment rate down to where it was prior to the pandemic and then even lower’, and to secure the economic recovery more broadly.

Why it will matter:

Last year, when previewing November’s 2020-21 budget, I argued that it needed to accomplish three key tasks, with the first by far the most important. Those tasks were (1) to continue the government’s already-impressive work in supporting the economy and offsetting the large, negative demand shock that had crushed economic activity and drove up unemployment early in 2020; (2) to demonstrate that Canberra was also thinking beyond the immediate need to support activity by offering measures designed to address the fact that economic performance pre-COVID was fairly lacklustre; and (3) to build on the government’s new fiscal strategy to provide a guide to the medium-term state of the government accounts. In my post-budget assessment, I judged that it had successfully delivered on (1), made a more modest contribution on (2) and on (3) stuck sensibly with the first phase of the government’s new two-phase fiscal strategy, with a core focus on achieving a strong economic recovery.

While the Treasurer has – quite rightly – pointed out that this year’s budget will again be delivered under the shadow of COVID-19, it’s also clearly the case that economic conditions now are very different from those prevailing through much of last year. So, given this combination of continuity and change in economic circumstances, what should we look out for on the 11th of May?

Below I suggest five things to expect. For (much) more on what next Tuesday might deliver, see the lengthy list of pre-budget readings that follows.

- Vaccine rollouts and COVID-19 willing, this should be a transition budget: one that bridges the crisis response of the 2020-21 budget and the post-crisis environment towards which we are now heading.It follows that, as with the economic circumstances, we should expect a mix of continuity and change.Continuity in that the priority will remain locking in the economic recovery.Change in that the economy has already travelled some distance from the crisis days of last year.The Treasurer’s 21 April speech, which was analysed in some detail last week, suggests that we should expect continuity to dominate change in terms of budget strategy, with the government still concentrating on phase one of its fiscal strategy and in particular on driving down the unemployment rate still further. Phase two and a focus on fiscal repair will have to wait.

- The turnaround already underway in the economy should be reflected in some significant upgrades to Treasury’s economic forecasts (likely in line with the new RBA forecasts discussed above and due to be rolled out in more detail in May’s Statement on Monetary Policy).Those new forecasts will also offer a guide as to when the government thinks any future shift in fiscal strategy to phase two and budget repair might become likely.

- While budget repair per se will not be a major policy theme, nevertheless, the economic turnaround is already delivering significantly better budget outcomes than were expected as recently as the December MYEFO (see story above).So, we should expect a smaller deficit and debt outcome for 2020-21 and, as a result, a much stronger starting position for 2021-22.That in turn will feed through into an improved profile for both variables over the budget forecasts in the years beyond.That is, a better economic performance will deliver some automatic fiscal restoration.

- While boosting employment and driving down unemployment will be one major theme of the budget, another will relate to measures to bolster the ‘Caring Economy’.In particular, the government has already flagged increased spending on Child Care and Aged Care, although the likely scale is smaller than many advocates would like.There has also been much talk of a budget ‘pitched at women’, with possible measures including policies aimed at improved access to superannuation and tackling domestic violence.

- In terms of further stimulus measures, there is an expectation that the government is likely to extend the Low and Middle Income Tax Offset (LMITO) for another year.More announcements on infrastructure – a staple of recent budgets – are also probable, as are additional measures designed to support COVID-hit sectors of the economy.

What I’ve been reading . . . (1) Pre-budget reading

An overview of the latest Deloitte Access Economics Budget Monitor. Deloitte reckons that budget revenues in 2020-21 could beat MYEFO expectations by $21 billion (about four per cent) and in 2021-22 by $28 billion (more than five per cent). Spending in 2020-21 could be $8 billion less than MYEFO projections, although in 2021-22 spending could overshoot by around $6.6 billion. All up, Deloitte reckons that underlying cash deficits in 2020-21 and 2021-22 will be $31 billion and $22 billion, respectively, better than forecast. And, it suggests, future deficits are likewise set to be considerably smaller than now outdated official projections.

ANZ Bluenotes on what to expect from the Federal Budget.

NAB’s Chief Economist on Budget 2021: Where to for business?

EY asks, will the budget do a good job of balancing the handbrake and the accelerator?

Saul Eslake on the coalition’s rethink on budget orthodoxy.

Peter Martin reckons budgets are more about values than money.

Grattan doesn’t expect to see a cash splash on the caring economy.

Related, Grattan on the government’s childcare reforms.

If this is a budget that will be designed in part to be a pitch to women, what might that involve?

Finally, a useful AFR roundup on what we know so far about the Budget.

What I’ve been reading . . . (2) Not (directly) about the budget

RBA Deputy Governor Guy Debelle on monetary policy during COVID.

The ABS April 2021 Business conditions and sentiments results, drawing on data collected between 14 and 21 April this year. This latest survey in the series contains some interesting insights on supply chain disruption and teleworking.

- 30 per cent of businesses report that they are currently suffering supply chain disruptions with 37 per cent of this group saying that they were affected to a great extent (suffering from major delays, or an inability to obtain certain items or experiencing a significant impact on revenue).

- Small businesses were more likely than medium or large businesses to report suffering supply chain problems to a great extent (37 per cent compared with 30 per cent and 25 per cent, respectively).

- By sector, industries experiencing significant supply chain disruptions included manufacturing (55 per cent of businesses reported experiencing disruption), other services (54 per cent), retail trade (52 per cent) and wholesale trade (50 per cent).

- Before COVID-19, 20 per cent of businesses had staff teleworking. Currently, 30 per cent of businesses have staff teleworking, down from 43 per cent in September 2020.

- Of the 30 per cent of businesses with staff currently teleworking, about 80 per cent expect to have them do so long term, of which 60 per cent think existing arrangements will stay the same.

- About 58 per cent of teleworking businesses reported at least one benefit from the arrangement, with those benefits including improved staff well-being (45 per cent), reduced overheads (27 per cent), increased productivity (26 per cent) and improved staff retention (18 per cent).

Also from the ABS, provisional internal migration estimates for the December 2020 quarter. A net 43,000 Australians moved to regional areas from capital cities last year overall in what was the largest net inflow to the regions on record (the current series dates back to 2001).

And one last one from the Bureau: updated cost of living indexes. Rises in the price of automotive fuels and health care costs are behind the latest increases.

The AFR on Australian business’ record $18.4 billion spend on software: the pandemic is accelerating the rate of the digitalization of the economy.

Related, ANZ Bluenotes on post-crisis investment.

Lowy’s COVIDPoll 2021: almost all Australian adults (95 per cent) say that Australia has handled COVID-19 well.

An FT Big Read on Australia’s coal mining dilemma.

Modern infectious diseases: macro impacts and policy responses.

The IMF says that the US dollar share of global foreign exchange reserves has fallen to a quarter-century low. Dig a little deeper, however, and the greenback is still comfortably number one in the international currency pecking order.

Adam Tooze on the radicalisation of Paul Krugman.

The OECD’s 2021 report on taxing wages. The pandemic has seen the largest decrease in taxes on wages since the global financial crisis. There were record falls across the OECD overall in the tax wedge (the total taxes on labour paid by both employees and employers, minus family benefits, as a percentage of the labour cost to the employer) as the tax wedge for a single worker fell in 29 OECD countries and increased in just seven. The falls were mainly due to changes in tax policy settings (and in particular falls in income taxes) although in some cases falling wages also played a role. In Australia (pdf) the tax wedge for the average single worker increased between 2019 and 2020. That left us with the 29th lowest tax wedge out of 37 OECD countries in 2020, compared to the 30th lowest in 2019.

The WSJ returns to the debate over who faces the largest burden from company tax increases, workers or shareholders?

An Economist Briefing on the alarming possibility of war in the Taiwan Strait.

Harold James compares the collapse of Greensill Capital to the decline and fall of the Medici Bank.

Related, the Odd Lots podcast talks to Bronte Capital’s John Hempton about Greensill, Archegos and market conditions more broadly.

Tyler Cowen reckons that markets should take UFOs seriously. Good for defence stocks and the US dollar?

Deutsche Bank economists on WFH and the productivity paradox. Found via this FT Alphaville post on Is WFH bad for productivity?

Related, Bloomberg Businessweek on the possibility of a pandemic-assisted productivity acceleration.

I’m pretty late to this one (the essay is from January), but I was only pointed to it recently: David Wallace-Wells on After Alarmism.

Finally, and also related, one of the books on my reading list last summer was Kim Stanley Robinson’s The Ministry for the Future. The Crooked Timber blog is hosting a seminar on the novel, pulling together views from economists, political scientists and others. And from the comments to that post, an interesting review from another genre writer I like, Adam Roberts.

Latest news

Already a member?

Login to view this content