The unemployment rate fell for a sixth consecutive month in April dropping to 5.5 per cent in a result that suggests Australia’s labour market is taking the end of the JobKeeper program in its stride. Wage growth remains anaemic, however, with the Wage Price Index rising at an annual rate of just 1.5 per cent in the first quarter, and with public sector wage growth at record lows. The minutes from the 4 May RBA monetary policy meeting showed that while the central bank is more upbeat on growth and employment it still expects only modest increases in inflation. The Westpac-Melbourne Institute Index of Consumer Sentiment fell 4.8 per cent in May as households gave a lacklustre response to the 2021 Budget.

Private new capital expenditure jumped 6.3 per cent in the March quarter, powered by higher spending on equipment, plant and machinery. Payroll job numbers fell 0.5 per cent over the fortnight ending 8 May and are down 0.4 per cent over the past month but remain 1.5 per cent above their pre-pandemic level. Construction work done rose 2.4 per cent over the March quarter this year, lifted by residential construction and engineering work. Bloomberg’s May 2021 survey of economists brought new consensus forecasts for inflation and unemployment. The ANZ-Roy Morgan Index of Consumer Confidence is now at its highest level since September 2019. Preliminary data show Australia’s exports of metalliferous ores hitting a record high in April and contributing to the third largest monthly merchandise trade surplus on record. Flash estimates of May’s PMIs show overall business activity at close to record highs and rapidly improving employment conditions but also indicate ongoing supply chain disruptions and rising inflationary pressures. Preliminary estimates of retail turnover for April reported healthy monthly growth while the annual rate of increase was supercharged by base effects reflecting last year’s lockdown measures. According to the Bloomberg COVID-19 vaccine tracker, there have now been more than 1.7 billion vaccines administered across the world economy and the latest average daily vaccination rate has risen to 29.8 million doses. At this rate, it would take another 11 months to vaccinate 75 per cent of the world’s population. World trade volumes rose 2.2 per cent over the month in March as trade momentum remained strong, although supply chain pressures and capacity constraints also continue to manifest across the international trading system.

This week’s readings include new research on central bank communication, grading the federal budget, the ABS on the differing profiles of discretionary and non-discretionary inflation, leaders and laggards in the post-pandemic recovery, more on the digitalisation of money, how the IMF is adapting its advice as the global economic landscape shifts, the rise and rise of superstar firms, the great worker shortage, risky cities, plus Michael Lewis on the pandemic and Niall Ferguson on the politics of catastrophe.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

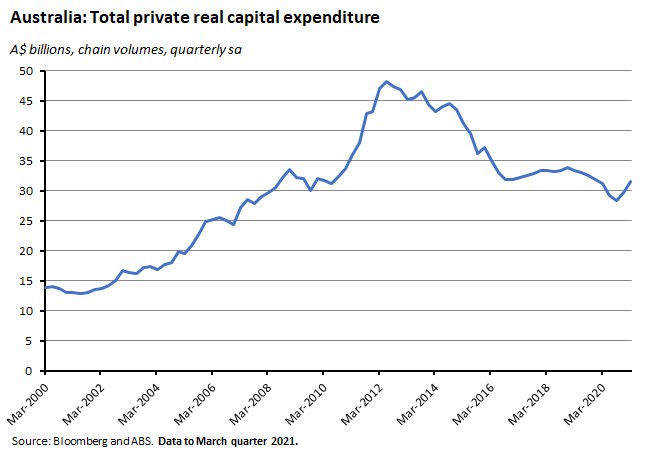

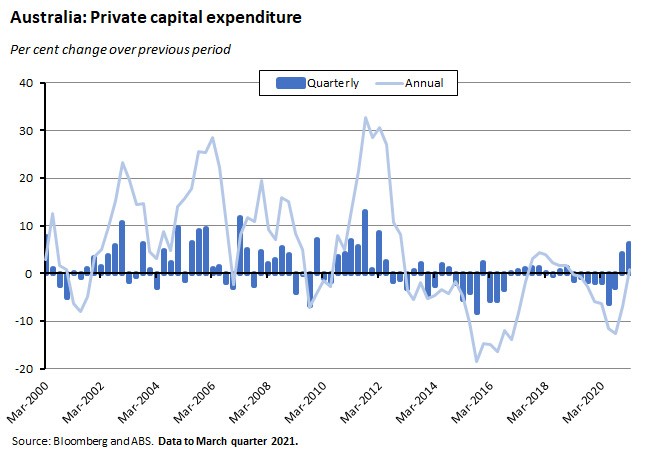

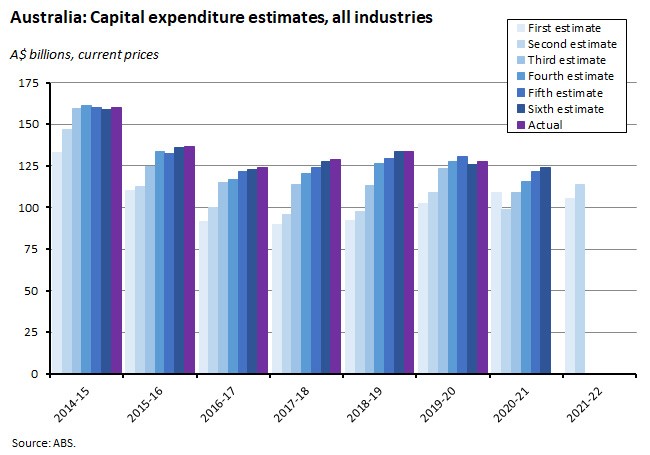

Private new capital expenditure rose by 6.3 per cent in the March quarter of this year to be 0.8 per cent higher than in the same quarter in 2020.

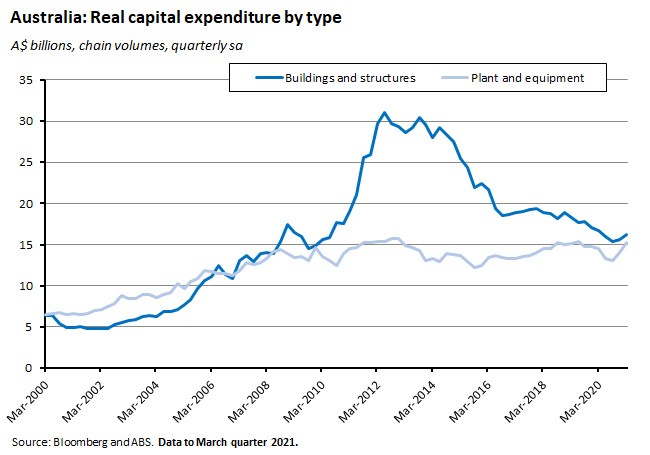

According to the ABS, capex on buildings and structures rose 3.8 per cent over the quarter but was down 3.4 per cent over the year, while investment spending on equipment, plant and machinery was up a strong 9.1 per cent in quarterly terms and rose 5.6 per cent in annual terms.

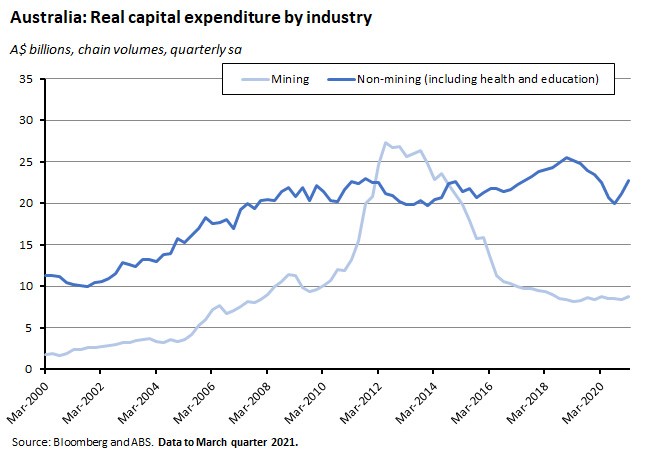

ABy industry, mining investment rose 4.1 per cent over the quarter and was up 0.7 per cent in annual terms, while non-mining investment jumped by 7.1 per cent in quarterly terms and rose by 0.8 per cent in annual terms.

Turning from actual to expected capital expenditure, Estimate Six for total capex in 2020-1 was $124 billion, which is a 2.2 per cent increase compared to Estimate Five for the same year. It was 1.4 per cent lower than Estimate Six in 2019-20.

Estimate Two for 2021-22 was $113.6 billion, which is 7.9 per cent higher than Estimate One for the same year and 14.9 per cent up on the corresponding estimate made last year. Estimate Two for mining investment was up 1.5 per cent relative to Estimate One while Estimate Two for non-mining investment was a marked 11.3 per cent higher than the previous estimate.

Why it matters:

The Q1 data on investment show that capital expenditure in the economy has continued to increase, building on the recovery that started in Q4:2020. This was the strongest quarterly result since 2012 and at 6.3 per cent the print was also significantly better than market expectations for a more modest two per cent increase. The main drivers of the rise were non-mining investment and spending on machinery and equipment, with the strength of the latter again likely influenced by the government’s tax incentives, now reinstated by May’s budget for another year. With forward-looking indicators (such as the PMI and NAB business survey) also sending positive signals, and with healthy growth expectations for this year, the outlook for investment is brightening.

What happened:

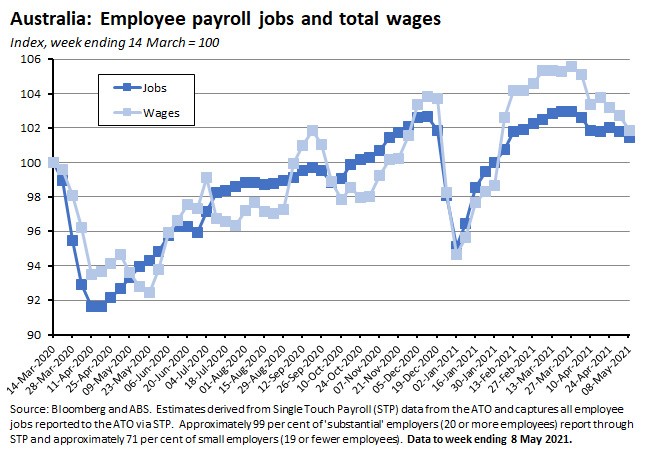

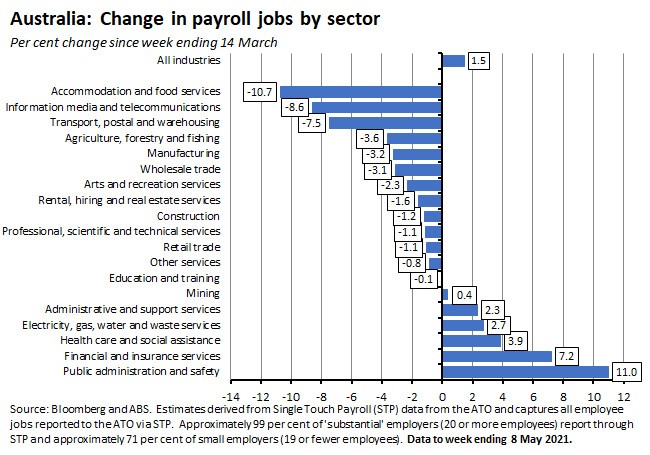

The ABS reported that between the weeks ending 24 April and 8 May 2021 the number of payroll jobs fell 0.5 per cent (after having risen by 0.2 per cent over the previous fortnight) while total wages paid fell 1.3 per cent. Since the start of the pandemic (the week ending 20 March 2020) the number of payroll jobs has now risen by 1.5 per cent.

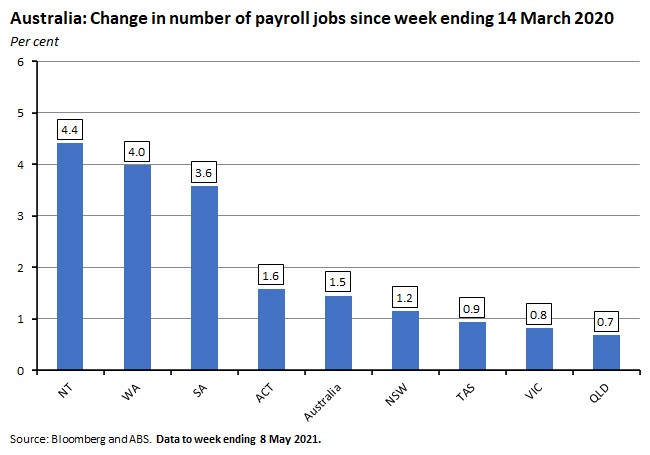

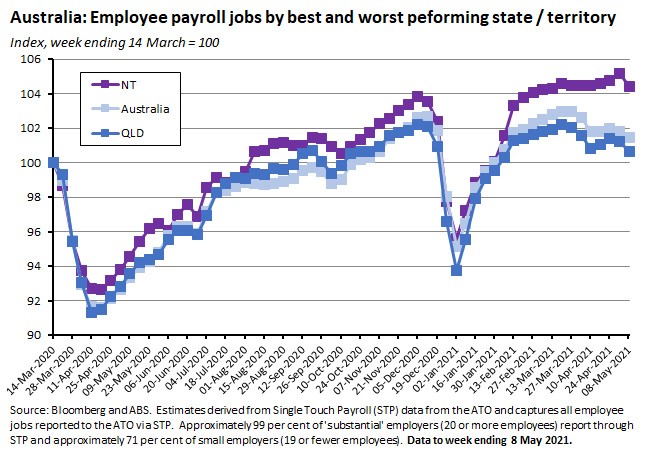

By state, the largest gains in job numbers since the start of the pandemic (treated as the week ending 20 March 2020, which was the week of Australia’s 100th case of COVID-19) have been in the Northern Territory (now up 4.4 per cent) and Western Australia (up four per cent) while the most modest increases have been in Queensland (up 0.7 per cent) and Victoria (up 0.8 per cent).

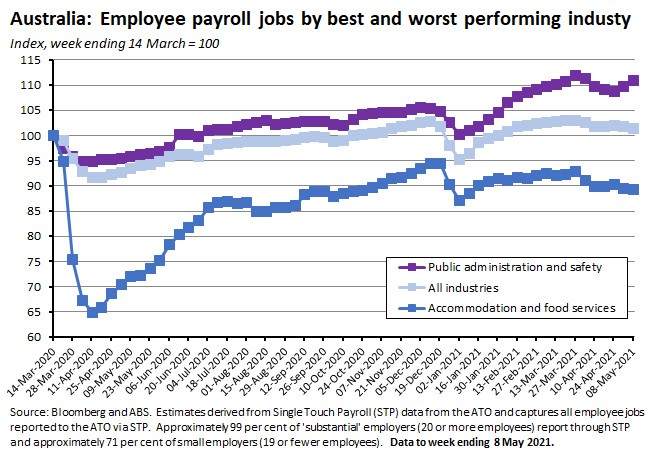

By industry, job gains over the past fortnight were strongest in education and training (up 3.5 per cent) and public administration and safety (up 2.1 per cent) while losses were largest in agriculture, forestry and fishing (down 4.3 per cent) and professional and scientific services (down 2.9 per cent). Over the whole period since the start of the pandemic, job losses have been greatest in accommodation and food services (down 10.7 per cent), information, media and telecommunications (down 8.6 per cent), and transport, postal and warehouse services (down 7.5 per cent). The biggest increases in job numbers have been in public administration and safety (up 11 per cent) and financial and insurance services (up 7.2 per cent).

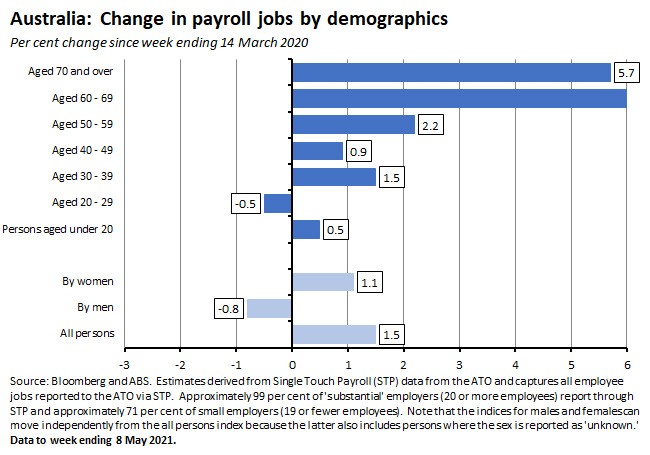

By demographics, payroll job numbers for men are still below pre-pandemic levels while job numbers for women are now higher.

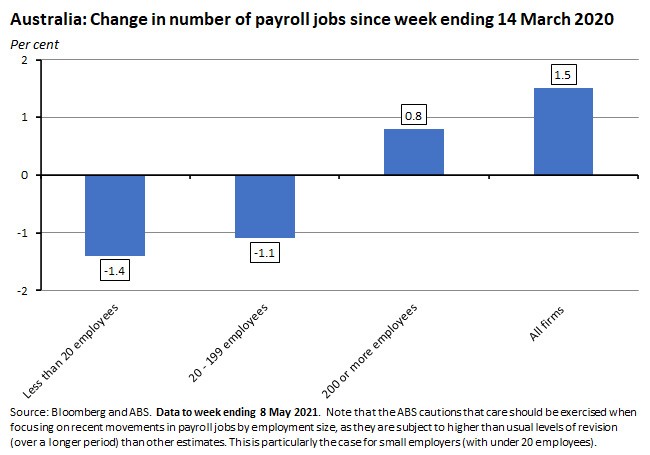

By firm size, employment is still below pre-pandemic levels in small- and medium-sized employers but has now exceeded those levels in firms with 200 or more employees.

Why it matters:

By early May, payroll jobs were 1.5 per cent above pre-pandemic levels although they were down 0.4 per cent over the month since 10 April and down 1.5 per from the end of March 2021. That fall in job numbers over the past month of data, along with the 30,600 drop in employment captured by the April labour force report, suggests that the pace of labour market recovery may now have slowed from its earlier rapid clip. An important complication in interpreting this data, however, is that the ABS continues to caution that over this period it is difficult to disentangle the effects of the end of JobKeeper, seasonality in the labour market around Easter and short-term restrictions in some states.

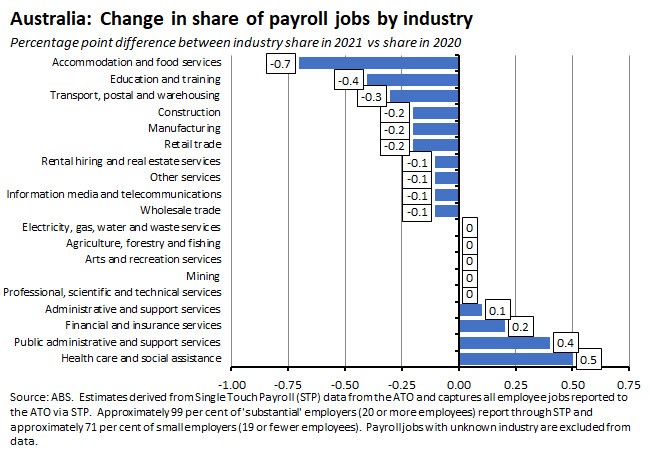

This week’s release also contained an article looking at the distribution of payroll jobholder and employer characteristics. The article notes that the distribution of state and territory payroll jobs remained very similar on both the week ending 14 March 2020 and a year later (the week ending 13 March 2021). In terms of industry, the distribution of payroll jobs sees most of those industries where jobs currently remain below pre-pandemic payroll job levels also seeing a decrease in their share of total payroll jobs by mid-March this year. For example, in the case of accommodation and food services where job numbers are still more than 10 per cent below pre-pandemic levels, the industry’s share of total payroll job numbers has fallen by 0.7 percentage points.

What happened:

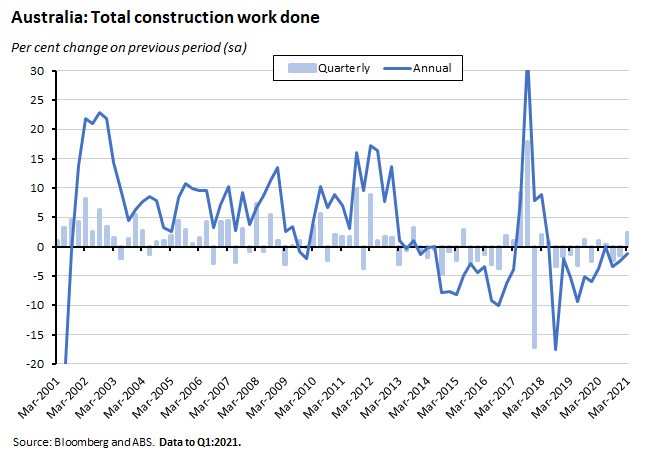

According to the ABS, total construction work done rose 2.4 per cent over the March quarter (seasonally adjusted) but was down 1.1 per cent over the year. Building work done was up 2.5 per cent quarter-on-quarter and down 1.8 per cent year-on-year while engineering work done rose 2.2 per cent over the quarter but edged 0.3 per cent lower in annual terms.

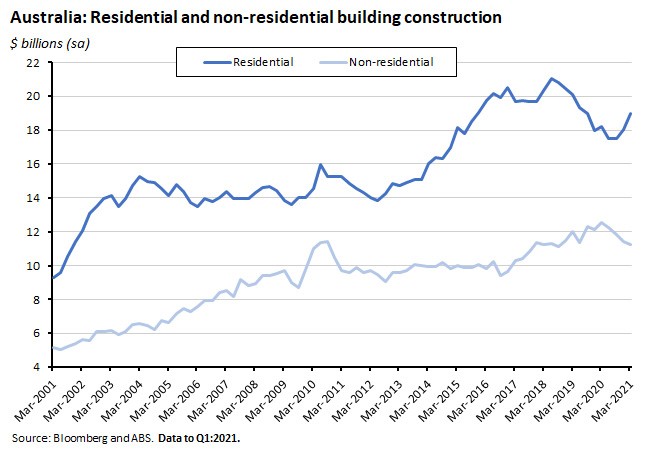

The increase in construction work done in the March quarter was largely driven by a rise in building work which in turn reflected a 5.1 per cent quarterly increase in residential construction (also up 4.2 per cent over the year). Growth in construction of new houses was particularly strong, up more than ten per cent over the quarter. That was all more than enough to offset a 1.6 per cent quarterly fall in non-residential construction.

Public engineering rose 3.1 per cent over the quarter, outpacing growth of 1.6 per cent in private engineering.

Why it matters:

The market consensus had been for a two per cent quarterly print, so the Q1:2021 result was a little stronger than expectations, supported by strong residential construction activity including for new homes. It also brought to an end a run of two previous consecutive quarters of falling activity.

What happened:

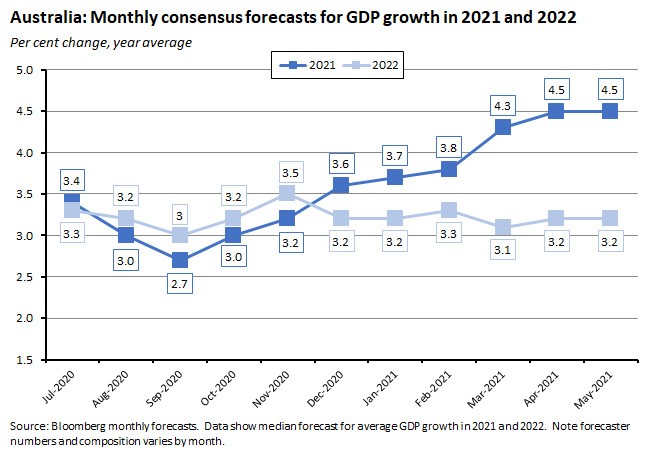

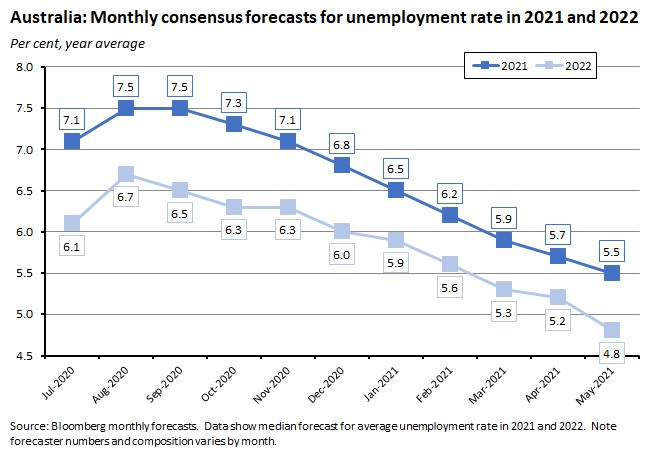

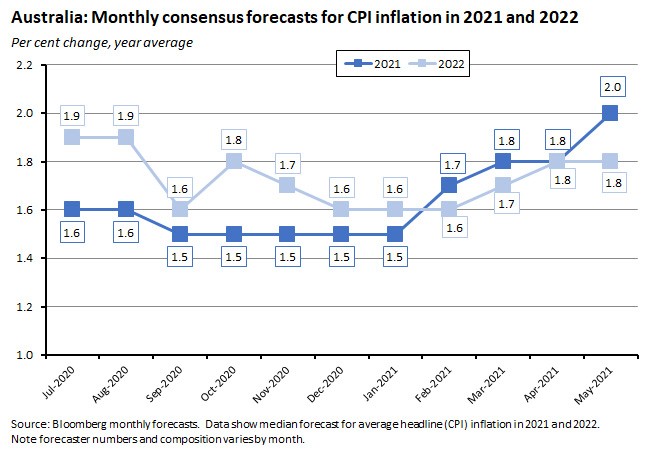

The Bloomberg May 2021 survey of economists reported that the median forecasts for GDP growth in 2021 and 2022 were unchanged (at 4.5 per cent and 3.2 per cent, respectively) from April’s survey.

But forecasters have continued to become more optimistic on the labour market. The unemployment rate is now expected to average 5.5 per cent this year and fall to 4.8 per cent across 2022.

Expectations for average inflation this year have also increased, rising from 1.8 per cent in the April survey to two per cent in the May survey. The median forecast for next year was unchanged.

Why it matters:

Forecasters continue to upgrade their expectations for the labour market. There has also been an increase in inflation expectations for this year, likely reflecting a combination of that better labour market performance plus evidence of rising input price pressures. For now, however, the consensus view is that this will not translate into a significantly higher inflation rate in 2022.

What happened:

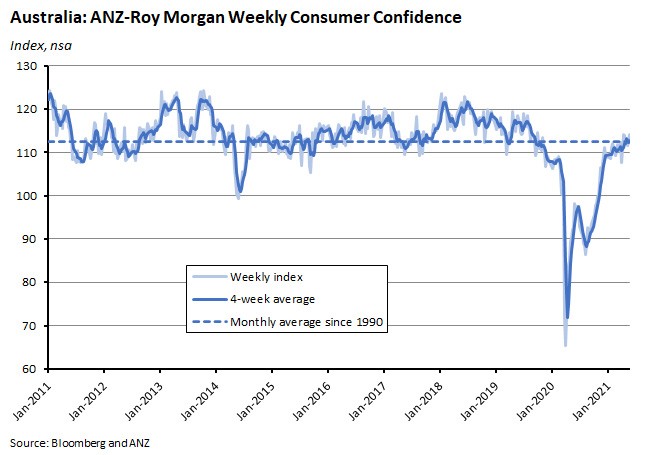

The ANZ-Roy Morgan Index of Consumer Confidence rose 1.5 per cent to 114.2 over the week to 22-23 May 2021.

In terms of the subindices, there were increases for ‘current financial conditions’ (up 4.6 per cent), ‘future financial conditions’ (up 3.3 per cent) and ‘future economic conditions’ (up 1.9 per cent). ‘Current economic conditions’ fell 0.8 per cent and ‘time to buy a major household item’ was down 0.7 per cent.

Why it matters:

Consumer confidence is now at its highest level since September 2019 – so well before the start of the pandemic – and on this measure is more than 23 per cent higher than index reading for the corresponding week last year. With the consumer expected to play a key role in driving growth, strong sentiment readings are good news in terms of indicating future prospects (see also story on retail turnover, below).

What happened:

The ABS said that preliminary estimates of Australian’s international merchandise trade in April 2021 showed exports of goods almost unchanged over the month (up just $13 million) while imports fell by seven per cent or $1.9 billion. That delivered a preliminary goods trade surplus of $10.1 billion (original basis).

Why it matters:

April’s merchandise trade surplus was the third largest on record. Exports of metalliferous ores (which includes iron ore) hit a new record high of $16.5 billion last month while the drop in import values was led by a fall in imports of non-monetary gold, reversing most of March’s earlier increase.

The Bureau also highlighted an eight per cent increase in the value of coal exports over the month. This was driven by a 16 per cent ($203 million) rise in exports of thermal coal, including an increase of $116 million in sales to India. Coal exports to India have been steadily rising since mid-2020, following a large reduction in Chinese demand for Australian coal.

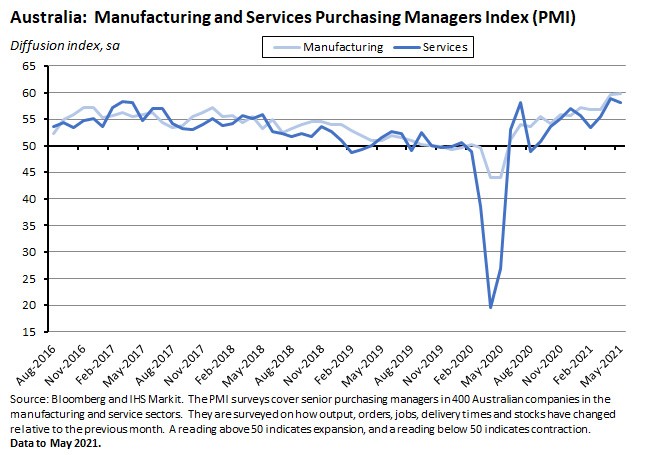

What happened:

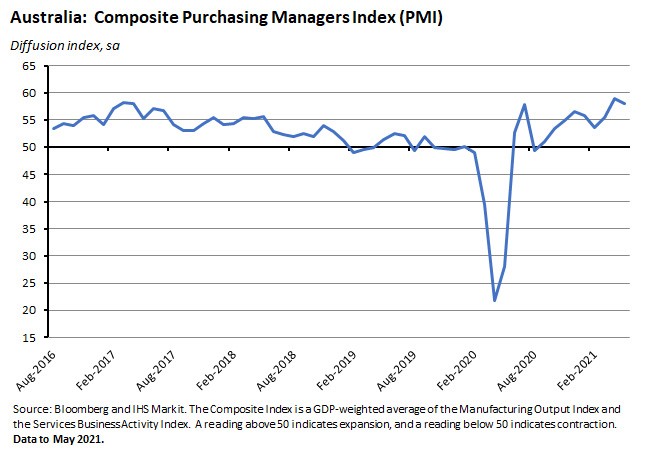

The IHS Markit Flash Australia PMI (pdf) eased from 58.9 in April to 58.1 in May. (Flash indices are based on about 85 per cent of total survey responses and are designed to provide an advance indicator of business activity.)

The Flash Services Business Activity Index slipped from 58.8 in April to 58.2 in May while the Flash Manufacturing PMI rose to a new record high, hitting 59.9 in May, up from 59.7 in April (the previous record).

Why it matters:

April saw the Composite PMI hit its highest level since the survey began in May 2016, so although this month did bring a decline, the overall level of the index is still more than consistent with a strong rate of expansion in business activity. Indeed, the manufacturing PMI hit a new record this month while services activity also remained strong. May also marked a ninth consecutive month of overall business expansion.

IHS Markit said the survey results showed the expansion of activity was underpinned by a combination of improved client confidence, buoyant market conditions, strengthening demand, the easing of COVID-19 restrictions and low interest rates. Export orders were strong and the survey’s employment measure improved at the fastest rate in the history of the series.

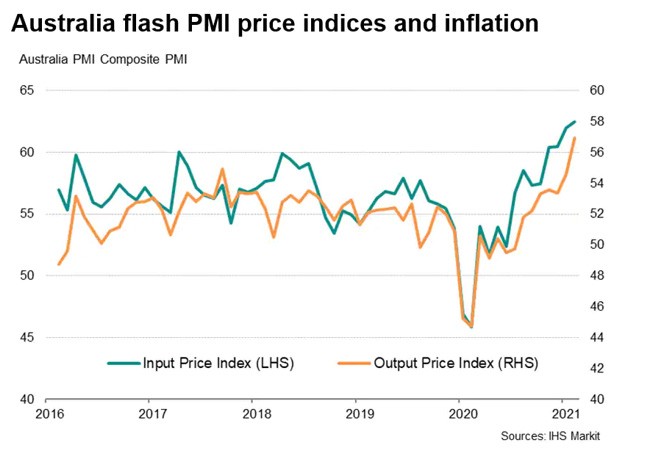

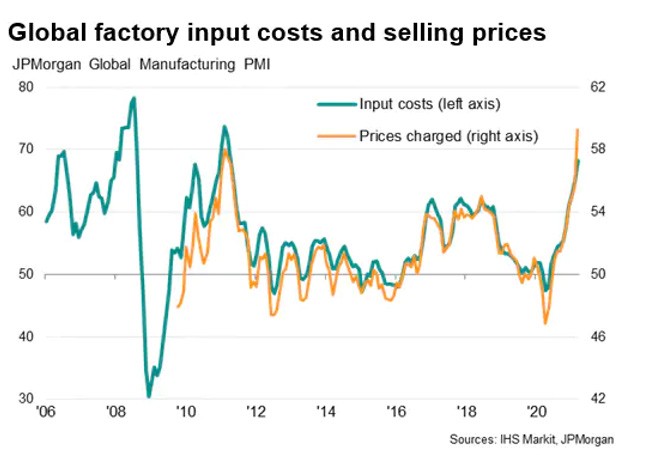

At the same time, however, both manufacturing and services firms continue to report supply chain disruptions, rising input costs and rising output prices.

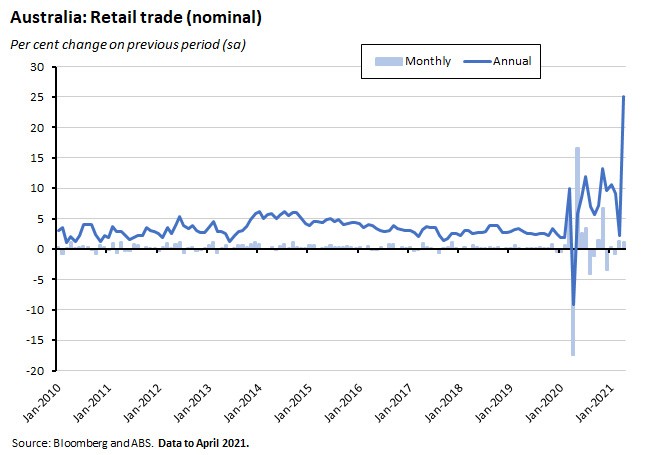

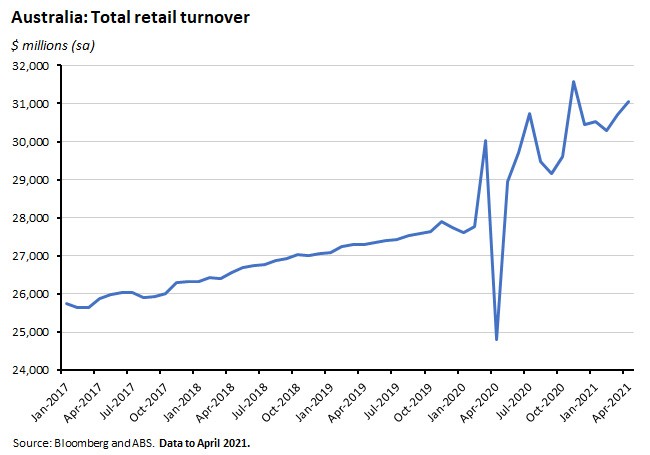

What happened:

The ABS said that preliminary retail turnover in April 2021 rose 1.1 per cent over the month (seasonally adjusted) to be a hefty 25.1 per cent up on the April 2020 outcome. (The preliminary data is based on businesses that make-up approximately 80 per cent of total retail turnover and is therefore subject to revision. The final monthly estimate will be published on 3 June.)

The Bureau said that the monthly increase in turnover was led by an increase in food retailing (up 1.5 per cent), following falls in the previous two months. There was also an increase in turnover for cafes, restaurants and takeaway food services (up 2.5 per cent).

By state, New South Wales and Victoria both enjoyed increases of two per cent with turnover rising in all industries except for department stores. In contrast, Western Australia saw a 1.5 per cent fall following the introduction of a lockdown in April.

Why it matters:

As noted last week when discussing the RBA’s May 2021 Statement on Monetary Policy, one of the key uncertainties around the domestic economic outlook is the future trajectory of household consumption – reflected in the RBA’s producing three scenarios based on different assumptions regarding consumer spending. Retail sales provide a partial guide to overall consumption trends, accounting for roughly 34 per cent of total final consumption expenditure in the economy, and the preliminary May results were comfortably better than market expectations for a 0.5 per cent monthly gain. Some of that increase may have reflected the impact of the New South Wales dine and discover vouchers, with the ABS noting that growth in the state in turnover in cafes, restaurants and takeaway food services across April was ‘especially strong’.

The outsized jump in annual growth last month reflects the large base effect driven by the introduction of COVID-19 restrictions in April last year, which had produced a sharp fall in turnover after physical stores were closed for all but ‘essential’ retail along with the introduction of general lockdown restrictions.

. . . and what I’ve been following in the global economy.

What happened:

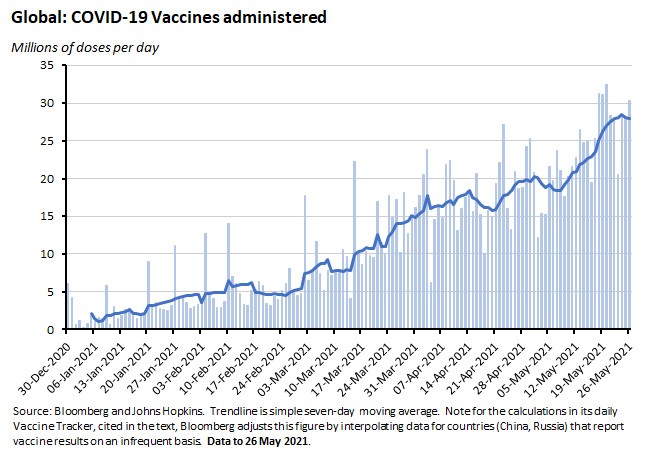

According to the Bloomberg Global Vaccine Tracker, there have now been more than 1.7 billion vaccines administered across the world economy. Globally, the latest average daily vaccination rate is 29.8 million doses. At this rate, it would take another 11 months to vaccinate 75 per cent of the world’s population.

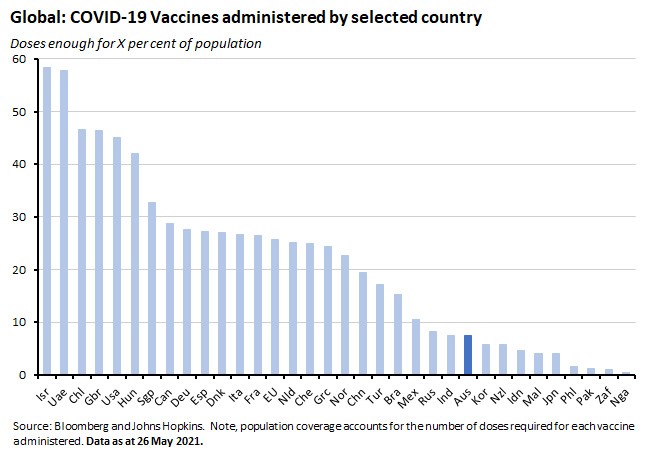

Country coverage continues to differ significantly, ranging from enough doses administered to cover 58 per cent of the population in Israel (and even higher in small island places such as Gibraltar (more than 100 per cent), the Seychelles (68.5 per cent) and the Maldives (63.1 per cent)) to just 0.4 per cent in Nigeria and less than 0.1 per cent in Yemen and South Sudan.

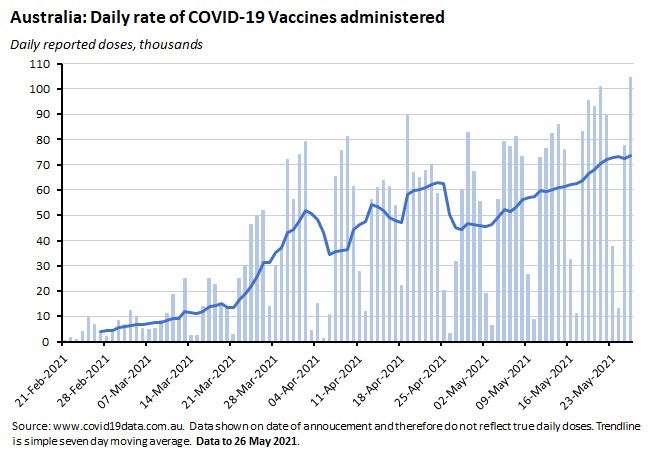

Here in Australia, vaccine trackers put total administered doses at around 3.8 million and the current seven-day rolling average of vaccines at about 73,800 doses. At this rate it would take roughly another 19 months to administer a total of 45 million doses or a bit more than 16 months to administer a total of 40 million doses.

Why it matters:

A successful global rollout of COVID-19 vaccinations underpins forecasts of a continued global economic recovery, and the pace of that vaccine rollout continues to accelerate. By way of comparison, at the end of April the vaccination rate was only running at 20 million per day with estimated time to 75 per cent coverage at 17 months while back in late March, those numbers had been even lower at 11.9 million and 2.5 years, respectively.

Bloomberg calculates that in theory enough doses have now been administered to fully vaccinate just over 11 per cent of the global population. In practice, of course, vaccine distribution has been very lopsided: countries and regions with the highest incomes are getting vaccinated more than 30 times faster than those with the lowest. The United States, for example, which accounts for 4.3 per cent of the global population, accounts for 17.3 per cent of world vaccinations, while the wealthiest 27 countries and regions now account for 31 per cent of vaccinations but only 10 per cent of the world’s population.

In this context, see this week’s reading list for the IMF’s new proposals on how to vaccinate the world.

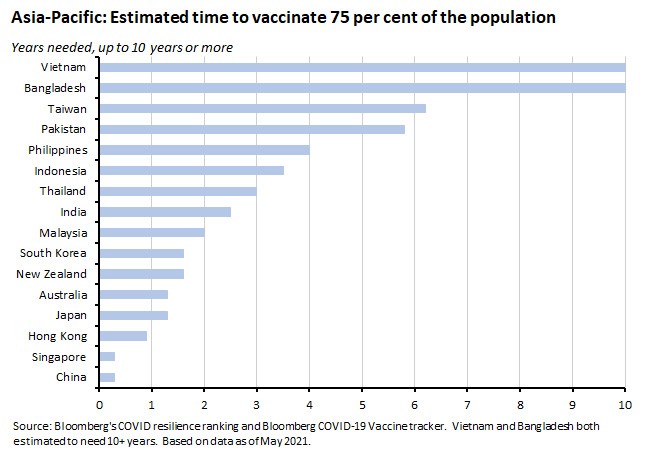

It’s also interesting to look at how the differential pace of vaccine rollout (and the impact of new waves of the pandemic) are influencing Bloomberg’s COVID resilience ranking, which attempts to rank 53 large economies by where the pandemic is being handled most effectively in terms of generating the least social and economic disruption. It is based on ten metrics including mortality and testing rates, vaccine access, freedom of movement and forecast economic growth.

In the past, this set of rankings had been dominated by the Asia-Pacific region (and to some extent still is – the top three spots are held by New Zealand, Singapore, and Australia with South Korea in fifth place behind Israel). But the region overall has now started to see its ratings slip as a combination of sluggish vaccine rollouts and resurgent case numbers in parts of South and Southeast Asia have tarnished some of the earlier success, as at current vaccination rates, it will take some regional economies multiple years to complete their vaccination programs. On the other hand, the US and some European countries have seen their rankings climb in line with their successful vaccination programs.

All that said, it’s also useful to keep in mind Ruchir Sharma’s recent admonition that picking winners in the middle of a fight is a mistake.

What happened:

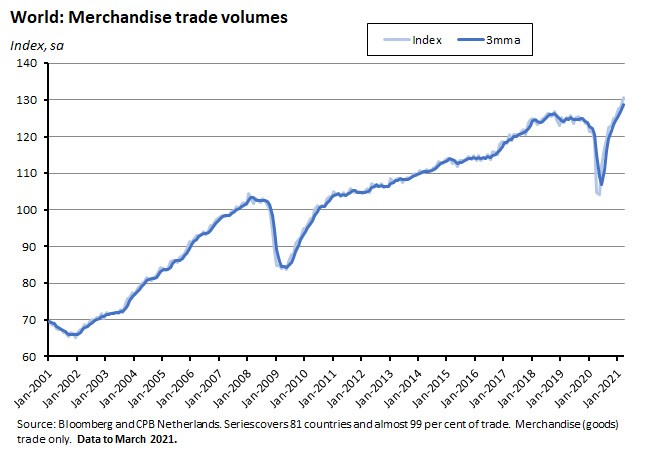

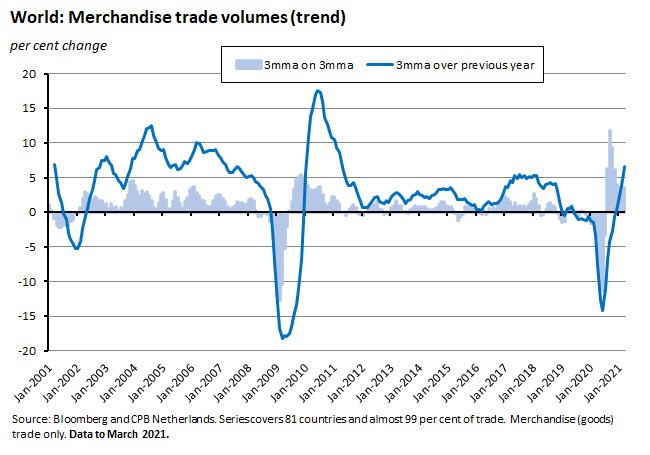

World merchandise trade volumes (pdf) rose 2.2 per cent over the month in March 2021, up from 0.1 per cent growth in February, according to the CPB Netherlands World Trade Monitor. The pace of quarterly growth eased to 3.5 per cent in Q1:2021, however, down from 3.9 per cent in the final quarter of last year.

Trade momentum (measured as the average of the three months up to the report month over average of the preceding three months) rose to 3.5 per cent in March from 2.8 per cent in February.

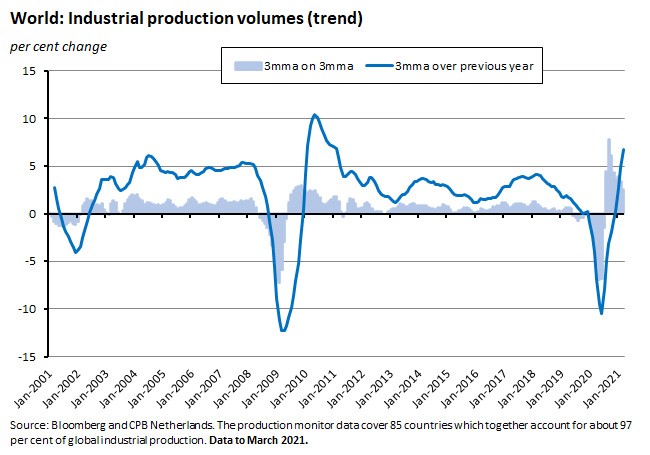

The same report also said that world industrial production rose 0.3 per cent over the month in March 2021 after having contracted by 0.6 per cent in February, while momentum eased from 3.5 per cent to 2.7 per cent. On a quarterly basis, growth slowed from 3.6 per cent in Q4:2020 to 2.7 per cent in Q1:2021.

Why it matters:

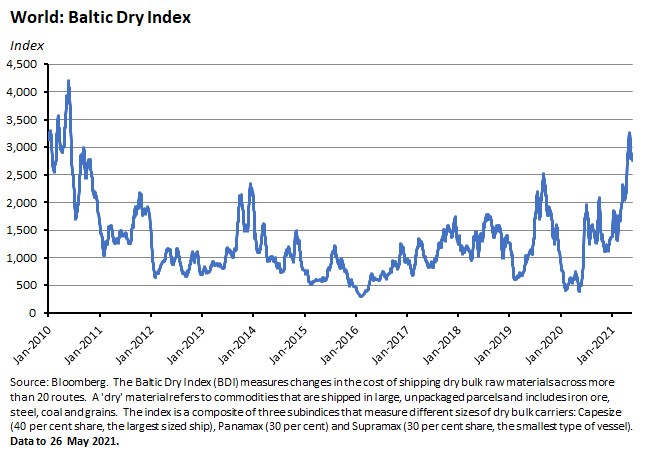

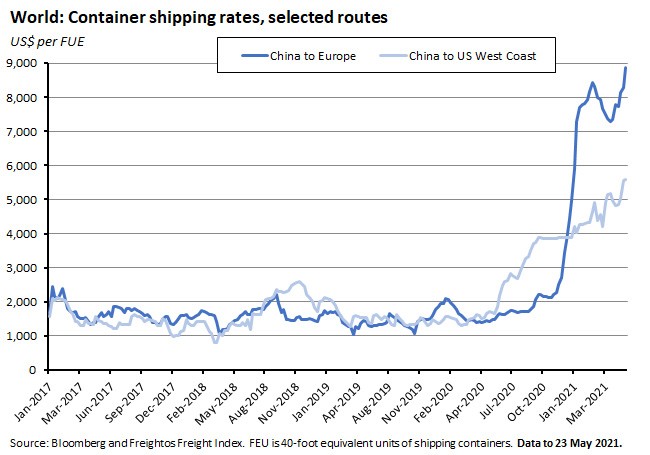

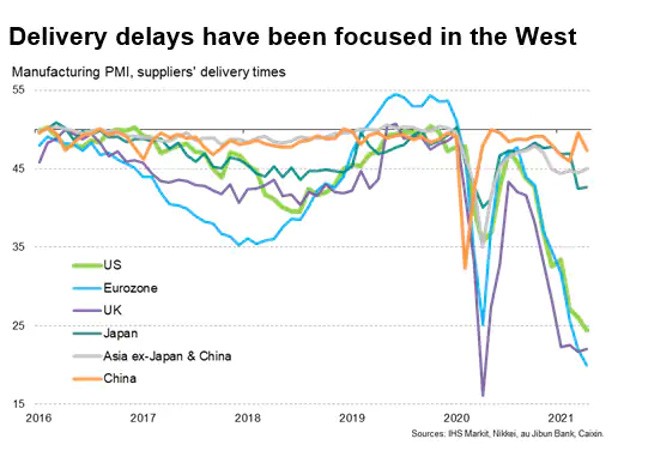

Global merchandise trade volumes have staged a dramatic recovery from the pandemic and are now comfortably above pre-COVID levels. At the same time, however, the global trading system is showing signs of strain, with global supply chains subject to stress as businesses struggle to restock. Strong consumer demand for goods (propelled by a mix of income effects from policy support and substitution effects as households redirect spending from pandemic-restricted services to goods) has run into supply constraints and one result has been a mix of surging transport costs and extended delivery times. And with supply chains already at full stretch, the impact of any adverse shock such as the grounding of the Ever Given in the Suez Canal or the Texas deep freeze / mass blackout are compounded.

Those pressures are showing up in rising transportation costs. Back at the start of this month, bulk shipping costs as measured by the Baltic Dry index, rose to their highest level in more than a decade.

Likewise, the cost of container shipping on major routes has also surged.

And as already noted in the Australian context (see above), these pressures are also contributing to reports of lengthening delivery delays and higher global factory input costs.

What I’ve been reading . . .

- A new Research Discussion Paper from the RBA looks at Central Bank Communication. The combination of central bank independence and an increased focus on the importance of expectations means that central banks now spend a lot of time and effort trying to communicate – both with the general public and with more specialist audiences. The paper measures central bank communications in terms of readability (how information is expressed), reasoning (conveying meaningful and useful information) and audience diversity. Interesting findings here include that simple readability metrics turn out to be barely correlated with survey evidence on readability and reasoning, that readability and reasoning are not strongly correlated, communicating with economists is very different to communication with non-economists (not surprising on the surface, but an interesting wrinkle is that non-economists might benefit relatively more from longer sentences and more detail) and that readability alone is insufficient to capture the essence of transparent communication.

- The AFR on why Australia is running low on timber, cars and pianos.

- Peter Martin on how a sample of Australian economists graded the budget: lots of Bs and Cs.

- Adam Triggs says that we shouldn’t worry about Australia’s COVID-19 debt. (On this topic, I’ve also gone into the debt sustainability issue in some detail both on the Dismal Science podcast and in this month’s budget webinar).

- Grattan offers some suggestions on stopping what it continues to see as a ‘death spiral’ for private health. Their report argues that this is the product of an ageing population using more expensive healthcare services, leading to insurers paying out more in benefits to their members, and therefore driving up premiums. Higher premiums make health insurance less affordable and less attractive particularly to younger and healthier people, who are therefore more likely to opt out of private insurance. By taking healthier people out of the insurance risk pool, the overall quality of those still insured declines, which means increased demand, another round of increases in premiums, additional exits from the young and healthy, and so on.

- The latest ANZ Stateometer. Western Australia is the standout performer overall.

- ABC Business digs into Australia’s unemployment statistics and the ‘one-hour’ rule.

- An ABS note on measuring discretionary and non-discretionary inflation. The intent is to measure differences in price trends for goods and services that are essential (or ‘non-discretionary’) vs discretionary purchases. Between 2005 and 2020, the rate of non-discretionary inflation exceeded overall CPI inflation, mainly driven by rising prices for housing, health and education. In contrast, from 2005 discretionary inflation rose more slowly than overall CPI inflation, mainly due to price falls for goods such as clothing, furniture, household appliances and motor vehicles. Tobacco was the biggest contributor to discretionary inflation, with prices increasing more than 400 per cent since 2005 following annual increases in the tobacco excise. Over the full period to December 2020, cumulative non-discretionary inflation was 44 per cent, cumulative discretionary inflation was 32 per cent and cumulative discretionary inflation excluding the impact of tobacco was just 18 per cent (which the ABS says is more representative of the majority of the population given that just 15 per cent of Australians are daily smokers).

- Also from the ABS, the Bureau published an updated version of the Water Account for Australia for 2018-19. The data show how lower rainfall led to structural change in water use, with higher water prices encouraging farmers to shift from rice and cotton to less water-intensive crops as well as encouraging a five per cent reduction in average water use per household in New South Wales (the state drought saw water restrictions instigated throughout 2018-19).

- And one last piece from the Bureau: The May 2021 Business Conditions and Sentiments Survey which reports responses collected between 12 and 19 May. One in five businesses report that they stopped accessing at least one support measure since March this year, with 17 per cent saying that measure was in the form of government wage subsidies such as JobKeeper. Of that one in five, 23 per cent said that the ending of support had impacted them to ‘a great extent’ with medium-sized businesses the most affected.

- McKinsey sets out how Australian companies can reinvent themselves in 2021.

- On the Lowy Interpreter, Greg Earl reviews Budget 2021-22 through the prism of economic diplomacy.

- Nouriel Roubini identifies some leaders and laggards in the post-pandemic recovery.

- A new BIS working paper on the digitalisation of money. The authors suggest that the growth of digital currencies could lead to the advent of digital currency areas that cover multiple countries, creating a risk of "digital dollarisation" in which the national currency is supplanted by the currency of a (systemically important) digital platform. Increasing competition between private and public monies could also influence the transmission of monetary policy and push central banks to introduce their own digital currencies (CBDCs). Note that we spent quite a bit of time talking about the rise of CBDCs in a recent episode of the Dismal Science podcast.

- Related, Grep Ip in the WSJ on cryptocurrencies.

- A blog post on how the IMF is adapting its advice to the new global economic landscape, with the Fund proposing to upgrade its approach to surveillance. For more detail, the Overview paper from the 2021 Comprehensive Surveillance Review is also available. There’s a huge amount of detail here, but key points include: (1) The way in which the pandemic has underscored the scale of global interconnectedness, such that events in one country can have sizable global effects. The Fund will increasingly consider new sources of such spillovers, including from health policies, climate change, and digitalization; (2) The Fund also needs to introduce a broader understanding of economic sustainability that goes beyond economic stability (which is necessary but not sufficient) and that accounts for trends in demographics, inequality, socio-political developments, and climate change; and (3) a deeper and better integration of macro-financial analysis.

- Also from the IMF, a proposal to end the COVID-19 pandemic. The Fund wants the world to: (1) vaccinate at least 40 percent of the population in all countries by the end of 2021 and at least 60 percent by the first half of 2022, (2) track and insure against downside risks, and (3) ensure widespread testing and tracing, maintain adequate stocks of therapeutics, and enforce public health measures in places where vaccine coverage is low. It puts the coast of such a package at around US$50 billion but the potential benefits at about US$9 trillion, implying an excellent rate of return on investment. Summary version here.

- An FT Big Read on Vaccines vs Variants.

- Bloomberg Businessweek reviews 30 years of data on Superstar firms and finds that they pay less tax (the median effective rate has fallen from 35 per cent in 1990 to 17 per cent last year), have fatter profit margins (up from seven per cent to 18 per cent over the same period), and devote a smaller share of revenues to investment (in 1990 IBM devoted nine per cent of revenues to capex: last year Apple spent three per cent). Their composition is changing too. The current list of top 50 exchange-traded companies has eight Chinese members: there were none in 1990. And technology firms now account for 21 of the top 50, up from three in 1990 and just eight as recently as 2010.

- Tyler Cowen explains why he thinks economics is failing us.

- A VoxEU column on why shareholder capitalism benefits wider society. If short-termism is a problem, it argues, the remedy is a greater focus on shareholder value rather than less.

- A new OECD report looks at inheritance, estate and gift taxes. While the OECD thinks they offer some attractive attributes – the linked report argues that well-designed inheritance taxes can raise revenue and enhance equity and do so at lower efficiency and administrative costs than other alternatives – in practice the experience to date has been disappointing. Only 24 (out of 37) OECD member economies currently levy inheritance or estate taxes, while nine members abolished them in the 1970s. And for those countries that do levy them, they raise only around 0.5 per cent of total tax revenues, with that low take largely reflecting narrow tax bases and extensive tax planning opportunities.

- The Economist on the great worker shortage – and some possible solutions.

- Ranking the world’s 576 largest cities based on their vulnerability to environmental and climate-related threats. On this metric, Jakarta is rated the world’s riskiest major urban centre but 414 cities with more than 1.4 billion inhabitants are judged to be ‘at high or extreme risk from a combination of pollution, dwindling water supplies, extreme heat stress, natural hazards and vulnerability to climate change.’ The report says 99 of the world’s riskiest cities are in Asia, including 37 in China and 43 in India, while India alone accounts for 13 of the world’s 20 highest risk locations.

- I’ve been listening to the audiobook version of the new Michael Lewis book on the pandemic – The Premonition. In many ways it reminds me of the last Lewis I read, The Big Short (I haven’t read his more recent one, The Fifth Risk) with its focus on a group of outsiders that can see what insiders keep missing or at least refuse to act on. Instead of Meredith Whitney, Steve Eisman, Michael Bury, Mark Baum and co. we have the likes of Charity Dean, Carter Mecher, Joe De Risi, Bob Glass, and Richard Hatchett. Since it’s a Lewis book, it’s pretty compelling, although I did find that a surprising amount of time was spent in the pre-pandemic setup and (less surprisingly) it’s often at least as much about the characters themselves as it is the pandemic or the role of non-pharmaceutical interventions. Still, there are also lots of thought-provoking points here including on the workings of bureaucracy, the challenges of acting on limited information, at what level is it best to allocate decision-making powers, the line between acting decisively and acting rashly, and so on. You can hear Lewis talk about the book and some of its key themes on various podcasts: there are good conversations with Talking Politics and the NYT’s Ezra Klein that are worth a listen. And this written take on Lewis’s approach to his books in the WSJ is also useful.

- Related, a more recent Talking Politics episode with Niall Ferguson on the politics of catastrophe.

Latest news

Already a member?

Login to view this content