The main domestic economic developments this week included the release of the Minutes for the 11-12 August 2025 meeting of the RBA’s Monetary Policy Board (MPB) and the publication of a surprisingly strong Monthly Consumer Price Index (CPI) Indicator for July 2025.

The RBA Minutes depicted a MPB feeling broadly comfortable that the economy is tracking in line with the central bank’s forecasts. On that basis, they report that the MPB judges that further modest policy easing will still be required to return the cash rate to a more neutral setting consistent with the central bank’s twin objectives of returning inflation sustainably to target and maintaining full employment. At the same time, the Board remains unsure as to the appropriate pace of that easing, in part due to the volatile external environment but also because of uncertainties around the prevailing degree of labour market slack and the implications for ongoing inflationary pressures in the economy. That in turn implies continuing caution, data-dependency, and a careful meeting-by-meeting approach to policy setting from here, in line with our previous post-meeting assessment.

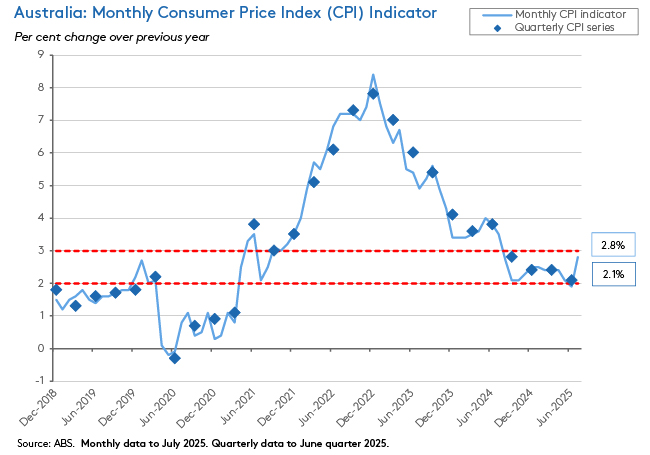

In that context, the latest monthly read on inflation will have reinforced the MPB’s cautious approach, with the Monthly CPI Indicator rising by an unexpectedly strong 2.8 per cent over the year to July. The market had expected that the headline rate would nudge up from June’s subdued 1.9 per cent reading, due to the impact of expiring electricity rebates, but had pencilled in a more moderate 2.3 per cent rate. While we know that the RBA is inclined to place limited weight on the CPI Indicator (a complete monthly measure of the CPI will be published from November this year), given that the July readings on underlying inflation also came in hot, at this stage Martin Place seems unlikely to be in a rush to resume rate cuts when the next MPB meeting rolls around on 29-30 September.

Sticking with central banks but moving further afield, the focus of much of the international financial press this week has been on developments at the US Federal Reserve. Ordinarily at this time of year, Fed-related coverage would involve dissecting the implications of the Fed Chair’s speech at the Jackson Hole conference, which this year involved an update on the US central bank’s evolving monetary policy framework. And there were noteworthy changes to be found here. For example, the Fed has decided to remove language indicating that the effective lower bound (ELB) is a defining feature of the economic landscape. Similarly, it has decided to eliminate the ‘makeup’ strategy of allowing an intentional moderate inflation overshoot to offset a previous period of inflation undershoot. In Powell’s words, this commitment has ‘proved irrelevant’ in the aftermath of the post-pandemic inflationary breakout. All of which tells us something interesting about how the Fed now sees the contemporary inflation environment. But attention has instead been captured by the escalating conflict between the Trump administration and the central bank, where the administration is now seeking to fire one of the Fed’s board of governors. At the time of writing, it was still too soon to tell how this latest showdown will play out, although thereare already concerns about the potential implications for interest rates and borrowing costs. Here, it is worth reminding readers once again of our piece a few weeks back on the rising risk of fiscal dominance.

Below we dig into the MPB minutes and the monthly inflation numbers in more detail and provide our regular linkage roundup which includes the aftermath of last week’s Economic Reform Roundtable. As usual, the accompanying charts are available in the web version.

Finally, a note to say that the Weekly economic update is about to go on an extended break due to a mix of travel, family commitments, and holiday. It won’t be back in your inboxes until 3rd October, I’m afraid, and I apologise for the extended absence of your regular economics fix.

MPB Minutes suggest further easing ahead, but at an uncertain pace

The RBA published the Minutes of the 11-12 August Monetary Policy Board (MPB) meeting, at which board members voted unanimously for a 25bp cut in the cash rate target. According to the Minutes:

‘Members agreed that the information received since the previous meeting had provided the further support that they had been seeking for the judgement that inflation was heading sustainably towards the midpoint of the target range. Members observed that the staff forecasts were consistent with the Board achieving its inflation and full employment objectives over the medium term, conditional on reducing the cash rate at this meeting and somewhat further thereafter. However, there were plausible risks to these forecasts in both directions. Members unanimously agreed that these considerations formed a strong case for lowering the cash rate target by 25 basis points at this meeting.'

The Minutes also cover the MPB’s ruminations on the future trajectory of the cash rate, where the MPB thinks that further policy easing will be required. There is no direct guidance at to how many more rate cuts that might involve, although the judgment that current policy is ‘slightly restrictive’ suggests that the current level of the cash rate target is now not too far away from neutral. The Minutes do note that this decision will be data-driven and take place on a meeting-by-meeting basis:

‘Members agreed that – based on what they knew at the time of the meeting – preserving full employment while bringing inflation sustainably back to the midpoint of the target range appeared likely to require some further reduction in the cash rate over the coming year. They also agreed that it was important for the pace of decline in the cash rate to be determined by the incoming data on a meeting-by-meeting basis.’

In terms of the likely pace of any further policy easing, the Minutes rehearse the case for a gradual approach, listing several considerations:

‘…various indicators suggested that labour market conditions remained a little tight, and the forecast for inflation was for it to be marginally above the midpoint of the target range in the medium term. In addition, private demand was showing signs of recovering, with risks on both sides of the forecast. And uncertainty about the degree of spare capacity and the neutral interest rate could warrant a measured approach to assess what incoming information reveals about these and other uncertainties.’

But they then go on to acknowledge the case for a ‘slightly faster reduction in the cash rate over the coming year’ than currently envisioned:

‘…such an approach would be appropriate if the labour market turned out already to be in balance. In such circumstances, maintaining a slightly restrictive stance of monetary policy could result in inflation undershooting the midpoint of the target range as excess capacity emerged in the labour market. A slightly faster reduction would also be appropriate if the overall balance of risks to the forecasts became more clearly skewed to the downside, perhaps because of adverse developments in the global economy or the anticipated handover from non-market sector to market sector employment growth not proceeding smoothly.’

So, the policy outlook continues to be conditioned on some familiar risks, including the ‘true’ state of spare capacity in the labour market (or equivalently, the ‘true’ level of ‘full employment’) and ongoing uncertainties around the global economic outlook. Regarding the former, for example, the Minutes report ‘members noted that, as the economy approaches balance, it was becoming more challenging to determine if there was spare capacity in the labour market.’ And in terms of the global picture, they comment that after taking lags into account, ‘any effects of increased trade policy uncertainty on spending were expected to become evident only from late 2025 and, even then, were expected to be modest.’

Finally, as to which of these two approaches to the pace of policy easing is more likely? The MPB does not feel able to make a call just yet:

‘Members agreed that it was not yet possible to judge between these alternative scenarios for the pace of future reduction in the cash rate, given the prevailing uncertainties.’

July’s Monthly CPI Indicator surprised to the upside

The ABS said that the Monthly Consumer Price Index (CPI) Indicator rose 2.8 per cent over the year to July 2025. That was up sharply from June’s 1.9 per cent annual increase as well as considerably stronger than the market consensus forecast, which had anticipated a 2.3 per cent print. It also marks the highest year-on-year result for the CPI Indicator since last July’s 3.5 per cent outcome.

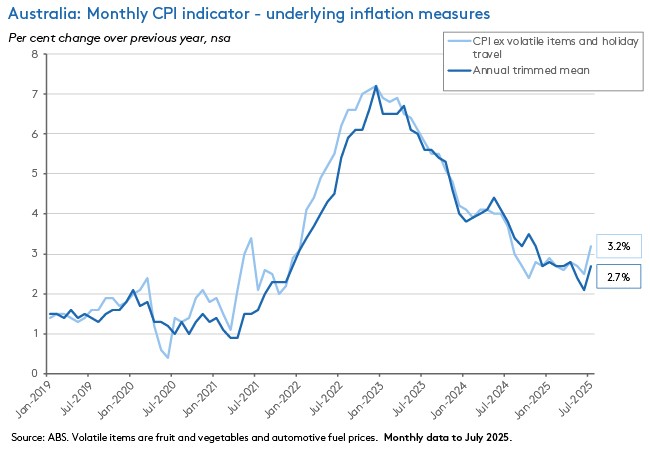

The strong inflation numbers were not just visible in the headline rate. Measures of underlying inflation also picked up last month. Annual trimmed mean inflation rose from 2.1 per cent in June to 2.7 per in July, while the rate of increase in the CPI excluding volatile items and holiday travel accelerated from 2.5 per cent to 3.2 per cent over the same period.

According to the Bureau, the main drivers of the rise in July’s inflation readings were the Housing (up 3.6 per cent from 1.6 per cent in June), Food and non-alcoholic beverages (up three per cent after a 3.2 per cent reading in the previous month and reflecting strong increase in coffee, tea and cocoa prices due in part to adverse weather conditions in overseas coffee bean growing areas) and Alcohol and tobacco (up 6.5 per cent from 5.7 per cent) groups. There was also a marked rise for the Recreation and Culture group, where after falling by 0.7 per cent over the year in June, prices rose by 2.6 per cent year-on-year in July as the school holidays saw higher demand for domestic airfares and accommodation.

That increase in Housing inflation reflected a sharp rebound in electricity costs, which rose 13.1 per cent over the year last month after having fallen by 6.3 per cent in the 12 months to June. Electricity costs jumped 13 per cent month-on-month in July due to the combination of several developments. First, households in New South Wales and the ACT did not receive electricity rebates under the extended Commonwealth Energy Bill Relief Fund (EBRF) last month, with payments due to commence in August.* Second, annual electricity price reviews came into effect. And third, state government electricity rebates have now been used up by households across some capital cities. In contrast, price pressures in other parts of the Housing Group remained moderate, with annual growth in new dwelling prices unchanged at 0.4 per cent and rental inflation easing to 3.9 per cent year-on-year, its lowest rate since November 2022.

As we have noted before, the monthly CPI Indicator can be volatile, is an imperfect proxy for the quarterly CPI, and tends to be treated with caution by the RBA. Even so, July’s jump in the both the headline and underlying rates of price increase is likely to reinforce the MPB’s cautious approach discussed above.

*The EBRF rebates were extended for six months from July to December 2025.

What else happened on the Australian data front this week?

The ABS said that private new capital expenditure rose 0.2 per cent quarter-on-quarter (seasonally adjusted, volume basis) and 1.7 per cent year-on-year in the June quarter 2025. Spending on buildings and structures was up 0.2 per cent in quarterly terms and 4.3 per cent higher on an annual basis, while expenditure on equipment, plant and machinery rose 0.3 per cent over the quarter but was down 1.1 per cent over the year. Business investment rose 0.9 per cent over the quarter in the non-mining industries but mining investment fell 1.4 per cent. The Bureau highlighted a 22.8 per cent rise in information media and telecommunications investment, due to a rebound in data centre investment, along with an 18.9 per cent rise in investment by the Retail trade sector, due to an increase in supply chain and fulfilment centre automation.

According to the ABS, total Construction Work Done rose three per cent (seasonally adjusted) over the June quarter 2025 to $76.1 billion. That was 4.8 per cent higher than in the same quarter last year. The rise was driven by growth in Engineering work done, which rose 6.1 per cent quarter-on-quarter and 8.5 per cent year-on-year to $37.1 billion. Building work done in the June quarter was up 0.2 per cent over the quarter and 1.6 per cent over the year, propelled by a 0.1 per cent monthly increase in residential construction to $24.2 billion and a 0.3 per cent rise in non-residential construction to $14.8 billion.

The ANZ Roy Morgan Consumer Confidence Index dropped by 3.4 points to an index reading of 86 for the week ending 24 August 2025. That marked a two-month low. All five subindices fell over the week, led by a large 4.4 point fall in ‘short-term economic confidence’ and a 3.7-point decline in ‘medium-term economic confidence.’ Household confidence in the economy is now at its lowest level since June. Weekly inflation expectations rose 0.1 percentage points to five per cent.

New ABS data on Australia’s regional population by age and sex shows the median age for capital cities (36.9 years) was below that of the rest of Australia (42 years) in 2024. Australia’s youngest capital was Darwin (median age 34.8 years) and the oldest was Hobart (39.3 years). In the combined capital cities, therewere 98.4 males per 100 females, compared with 99 for the rest of Australia. Darwin was the only capital with more males than females.

The ABS said there were 2,729,648 actively trading businesses in the Australian economy as of 30 June 2025, up 2.5 per cent on the previous year. Of that total, 999,161 were employing businesses. The firm entry rate was 16.4 per cent while the exit rate was 13.9 per cent.

Last Friday, the ABS released data on Research and Experimental Development (R&D) conducted by businesses in Australia. According to the Bureau, during 2023-24, business expenditure on R&D (BERD) was $24.4 billion. That was up 18 per cent from the previous release, which reported on 2021-22 outcomes. As a share of GDP, BERD in 2023-24 was steady at 0.9 per cent, unchanged since 2017-18. The ABS noted that the strongest growth in R&D was seen in the Information and computing sciences research field, which includes spending on Artificial Intelligence (AI). Businesses have more than doubled (142 per cent) their investment in AI since 2021-2022, spending $0.7 billion.

Other things to note . . .

- Transcript of the Treasurer’s remarks at the conclusion of the 19-21 August Economic Reform Roundtable. He provided three lists covering quick wins, ten reform directions, and further work.

- Secretary to the Treasury Jenny Wilkinson’s remarks on fiscal sustainability at last week’s Roundtable.

- The CIS’s Simon Cowan sounds a sceptical note.

- The AFR’s Michael Read considers potential tax changes advocated by some participants at last week’s Roundtable, which would call for future taxes on trusts and superannuation earnings along with new limits on negative gearing and the 50 per cent capital gains tax discount.

- Related, Saul Eslake offers his take on the prospects for tax reform.

- The ABS presents seven facts about Australian businesses.

- A new RBA Research Discussion Paper introduces a new AI-powered tool for central bank business liaisons.

- Making a case for investing in Northern Australia’s connective corridors.

- Explaining the pause in changes to the National Construction Code.

- The Insurance Council of Australia’s commissioned report from Lateral Economics on the government’s plan to expand its Home Guarantee Scheme warns it will largely benefit borrowers who would have bought homes in any event, and that by driving up prices it will potentially price out some lower-income first home buyers.

- The Lowy Institute has a special feature on understanding democratic erosion.

- The agenda and links to some of the papers, presentations and handouts from last week’s Federal Reserve Jackson Hole Economic Policy Symposium. The theme this year was Labour Markets in Transition – Demographics, Productivity and Macroeconomic Policy.

- The WSJ on the shift in the Fed’s approach to monetary policy as officials rethink the central bank’s policy framework.

- And the FT on the twilight of the central banking elite.

- Also from the FT, the Netherlands’ quiet shift to a four-day work week.

- IMF research analysing medium-term growth prospects for Asia.

- The Economist magazine says, beware the deficit-populism doom loop. In Europe, several countries are now caught between big deficits on one side and voter revolts on the other, with little ability to keep both bond markets and voters happy.

- Also from the Economist, China’s mid-year economic wobble.

- Do tax havens undermine the rule of law by providing the rule of law?

- Goldman Sachs on Stablecoin Summer.

- How Generative AI’s impact on learning curves could reshape the workplace.

- Adam Smith at 250.

- Is the West at risk of becoming bored to death?

- The Australia in the World podcast in conversation with Richard McGregor on China in 2025.

- The FT Economics Show with Mari Pangestu on how Asia is coping with Trump’s tariffs.

- The FT’s Unhedged podcast on the Fed under attack.

- Related, the Odd Lots podcast discusses why Central Banking is now on hard mode.

Latest news

Already a member?

Login to view this content