Overview

- Despite the largest supply disruption in the history of the global oil market, oil prices have risen by less than history might have suggested. That leaves markets exposed if current assumptions about the likely duration of the conflict prove incorrect. Cracks in market confidence that go beyond geopolitical risk are also adding to market nerves.

- Meanwhile, energy prices continue to grind higher, as the Strait of Hormuz remains effectively closed and as the damage to regional energy infrastructure mounts. Forecasts for growth and inflation are being adjusted accordingly, as are assumptions about the likely trajectory of global monetary policy.

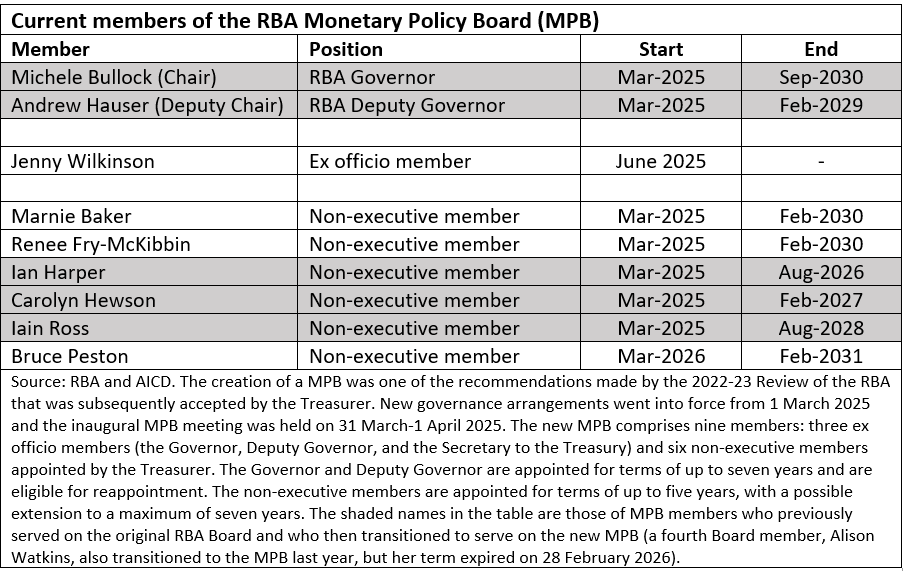

- The RBA, which had already tightened policy once to tackle stubborn domestic inflationary pressures, is ahead of many of its peers here. This week it delivered a second 25bp rate hike since last year’s easing cycle, in line with market expectations. Yet the vote was a close-run thing, splitting the Board 5-4 in favour of tightening. That suggests MPB members remain mindful of the big unknowns around the economic fallout from the war.

- The February 2026 Labour Force report delivered mixed messages in the form of stronger-than-expected employment growth alongside a higher-than-expected unemployment rate.

In this week’s issue, we review the ongoing impact of the war in the Middle East on the global economy, consider the fallout in terms of this week’s (split) vote by the RBA’s Monetary Policy Board (MPB) to lift the cash rate target by 25bp, and review February’s labour market numbers. We also cast our eye over the latest data on consumer confidence and inflation expectations and provide our regular roundup of further reading

and listening.

Why has an historic oil shock had such a muted price effect (so far)?

The war in the Middle East is now deep into its third week, with the oil price back above US$100/barrel (Brent) and at the time of writing pushing past US$110/b. Price pressures are likewise mounting across a

range of other markets, from gas to fertiliser.

Yet despite the effective closure of the Strait of Hormuz and the growing impairment of regional energy infrastructure, including new and extensive damage to Qatar’s Ras Laffan, the world’s largest LNG facility, in relative terms the surge in oil prices seen to date remains modest. According to the IEA, after all, this is the largest supply disruption in the history of the global oil market. Yet in that context, the price reaction has been limited relative to both the 2022 jump in prices triggered by the Russian invasion of Ukraine and in the context of the longer-term trajectory of real (inflation-adjusted) prices. After all, past estimates have suggested that the ‘nightmare scenario’ of a sustained closure of the Strait would be associated with considerably higher prices.

As suggested in previous notes, some of this moderation likely reflects the declining dependence of the world economy on oil, plus the situation of excess supply prevailing in the oil market before the launch of Operation Epic Fury. And some of it is the product of an ongoing market judgment that the conflict is unlikely to be prolonged in the face of mounting global economic pain. But it follows that, should markets decide their assumption relating to likely conflict longevity is wrong, the subsequent price adjustment could prove brutal.

Meanwhile, prices continue to grind upwards and in response, growth and inflation forecasts are also starting to shift. This week, Australia’s Treasurer reported the results of a Treasury modelling exercise covering several scenarios for the Australian economy. Under a scenario of short-term disruption (which assumes an oil price of around US$100/b through H1:2026 falling to a pre-conflict US$70/b by year-end) inflation could peak at around 4.5 per cent, while GDP this year would suffer a temporary, short-term hit of 0.2 per cent. Under a more prolonged conflict (oil price at US$120/b by mid-year and three years to return to US$70/b), inflation would reach at least five per cent this year, while the hit to GDP would be larger, with output 0.6 per cent lower next year.

Those adjustments to projections for activity and prices both for Australia and the world economy more broadly are in turn prompting shifting expectations about the trajectory of monetary policy. Rising inflation risk has seen markets trim their expectations of future interest rate cuts from key players, including the US Federal Reserve, the European Central Bank, and the Bank of England. Here at home, the conflict looks to have encouraged the RBA’s Monetary Policy Board (MPB) to bring forward a cash rate increase that pre-war had only been expected to arrive in May this year, as discussed below.

Finally, events in the Gulf are not the only factor weighing on market nerves. In recent updates we’ve highlighted market jitters about AI, ranging from concerns about the disruption of other business models (see, for example, the so-called Saaspocalypse) to elevated valuations of AI-related stocks. But recent months have also brought a steady drip feed of stories about cracks and problems in private credit markets. The two stories are also linked, given that private credit funds have significant exposures to software companies, for example. True, a recent OFR report argues that the potential scale of the private credit problem is modest, albeit still worth monitoring. Even so, it is yet another factor currently keeping investors awake at night.

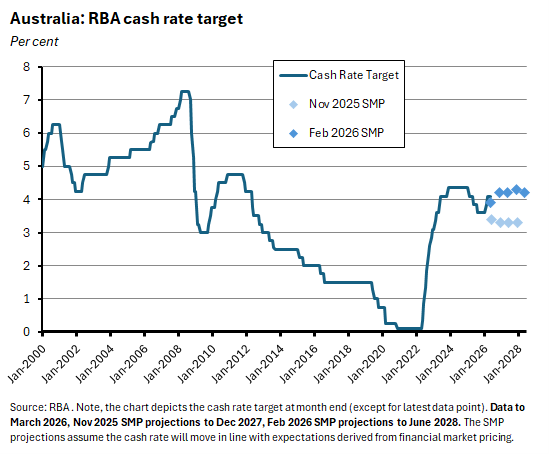

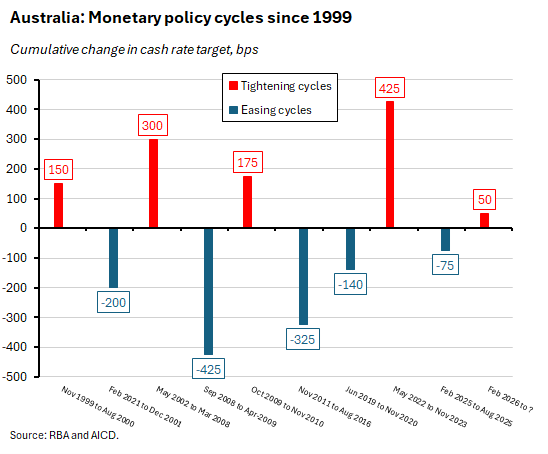

RBA increases cash rate target to 4.1 per cent

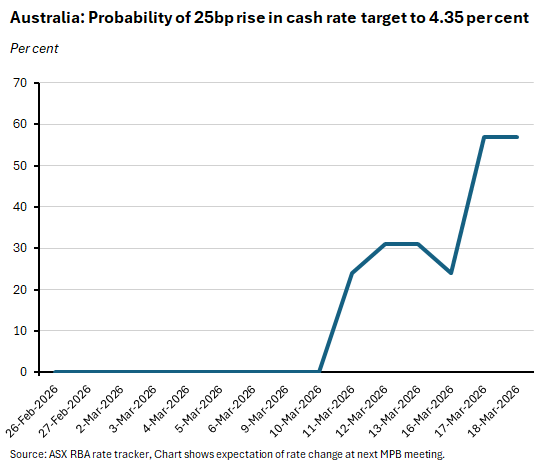

At its meeting this week, the MPB voted to increase the cash rate target by 25bp to 4.1 per cent.

As discussed last time, the increase was widely expected both by RBA-watchers and by financial markets. Yet the actual vote turned out to be a close-run thing, with five members voting in favour of a rate hike versus four voting for the status quo. Last week, we wrote that despite the strong consensus that the RBA would lift the policy rate, it did not negate the fact that there was still ‘a decent case for rates remaining on hold until there is greater clarity on the implications of the war’. It appears that four MPB members shared some version of that assessment.

This week’s increase in the cash rate target takes the RBA’s policy rate back up to the level prevailing before the 25bp rate cut delivered on 21 May 2025. It also means that policy is now tightening more aggressively than in the projections set out in the February 2026 Statement on Monetary Policy (SMP), which were based on market pricing at the time. Those SMP projections had assumed the cash rate would still have a ‘three’ in front of it by June this year, with the policy rate rising to around 4.2 per cent by year-end and peaking at 4.3 per cent in the December quarter of next year.

Financial markets currently expect another rate increase to follow at the 4-5 May MPB meeting.

The RBA has already removed 50bp of the 75bp of easing it delivered across the course of last year. If, as market pricing currently anticipates, the MPB delivers another 25bp hike in May, then the preceding easing cycle will have been fully unwound over the space of just four months.

The MPB statement accompanying this week’s decision covers much of the same ground we rehearsed last week. So, it reports that the recent flow of data served to reinforce the RBA’s view that the economy has been running hot with demand pushing up against supply constraints, and that inflation risks are tilting to the upside. Hence:

‘Information since the February meeting suggests that some of the increase in inflation reflects greater capacity pressures.’

And later:

‘A wide range of data over recent months have confirmed that inflationary pressures picked up materially in the second half of 2025. While part of the pick-up in inflation is assessed to reflect temporary factors, the Board judged that the labour market has tightened a little recently and capacity pressures are slightly greater than previously assessed.’

Likewise, the RBA remains uncertain as to the current degree of monetary policy restrictiveness, with the statement citing the ‘ready availability’ of credit to households and businesses despite some modest tightening in financial conditions.

Of course, Australia’s central bank has now added the impact of the war in the Middle East to its worry list, warning that the consequent spike in energy prices will lift headline inflation, threaten to push up inflationary expectations, and keep inflation further away from target for longer:

‘…the conflict in the Middle East has resulted in sharply higher fuel prices, which, if sustained, will add to inflation. Short-term measures of inflation expectations have already risen. As a result, the Board judged that there is a material risk that inflation will remain above target for longer than previously anticipated.’

At the same time, the statement also acknowledges that the ultimate impact of the conflict in the Persian Gulf is uncertain, with downside risks to activity running alongside the upside risks to inflation:

‘Globally, the conflict in the Middle East poses substantial risks in both directions. A longer or more severe conflict could put further upward pressure on global energy prices; this will push up near-term inflation and could also increase inflation further out if it impairs supply capacity or price rises get built into longer term inflation expectations. Higher prices and prolonged uncertainty may cause growth to be lower in Australia’s major trading partners and also in Australia.’ [emphasis added]

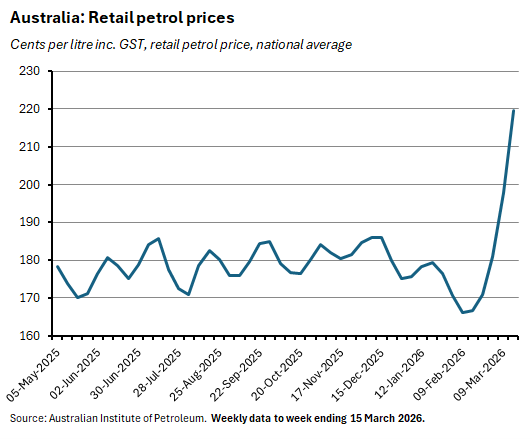

Meanwhile, higher energy prices are continuing to flow through into higher prices at the pump:

And the latest data also show those petrol price rises feeding into higher short-term inflation expectations as well as into weaker consumer sentiment (see the Australian data roundup below for more detail on the latest weekly consumer confidence numbers). The mixed messages from this week’s labour force report as set out below – with higher unemployment accompanied by higher employment – are unlikely to change the picture by much.

Current events, then, are serving as another example of why policymakers find negative supply shocks particularly unpleasant to deal with. The nasty (‘stagflationary’) combination of higher prices and lower activity sends contradictory signals about the appropriate policy response: tighten policy to head off inflation or loosen it to support growth. The optimal policy response will be heavily influenced by the expected scale and duration of the shock. That said, when inflation is already above target, as is currently the case here in Australia, the trade-offs become more heavily weighted towards the central bank’s inflation objective.

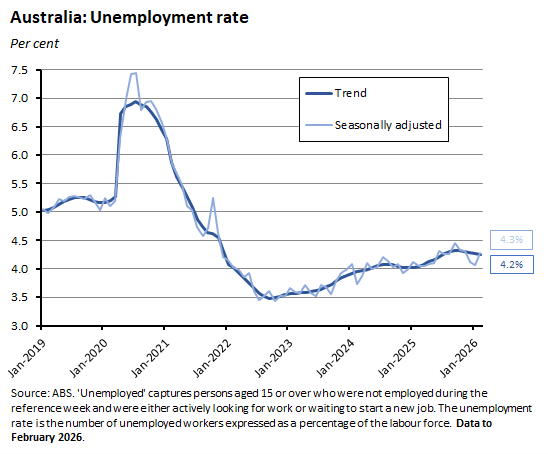

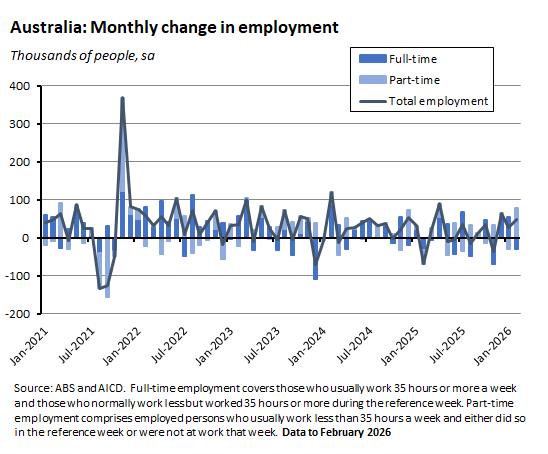

February 2026 labour market: Swings and roundabouts

The February 2026 Labour Force release from the ABS painted a mixed picture of the Australian labour market.

On the one hand, in a sign of some labour market loosening, the seasonally adjusted number of unemployed people grew by 35,000 last month, taking the unemployment rate up to 4.3 per cent from 4.1 per cent in January and returning the joblessness rate back to its November 2025 level. That represented a weaker outcome than the market had anticipated, with the consensus forecast having called for a 4.1 per cent print. Although note that on a trend basis the unemployment rate was down slightly from January, slipping from 4.3 per cent to 4.2 per cent.

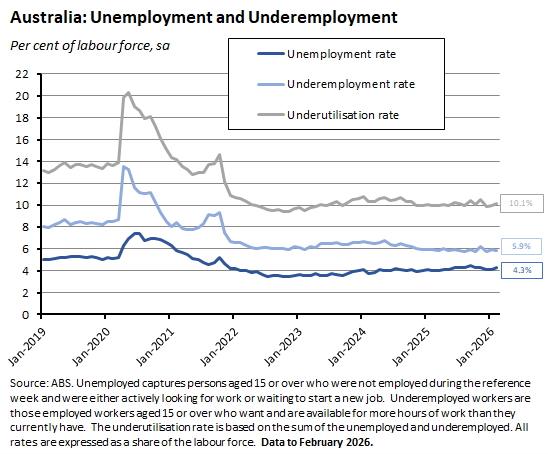

With the seasonally adjusted underemployment rate unchanged at 5.9 per cent, the overall underutilisation rate nudged up to 10.1 per cent last month.

On the other hand, and in a sign of ongoing labour market resilience, total employment rose by 48,900 people in February, comfortably outpacing the consensus forecast for a 20,000 gain. While full-time employment fell by 30,500, this was more than offset by a 79,400 increase in the number of people in part-time employment, with the Bureau highlighting both an increase in part-time work by those aged 65 and over and a shift to fewer people leaving jobs to retire compared to last year. This rise in participation could reflect a reaction to the cost-of-living squeeze and expectations of more of the same (higher rates, higher petrol prices) to come.

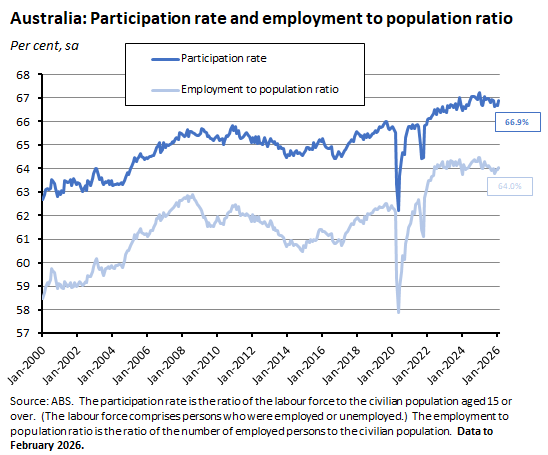

The employment to population ratio held steady at 64 per cent last month while the participation rate increased from 66.7 per cent to 66.9 per cent.

Monthly hours worked declined in February, dropping by 0.2 per cent (three million hours) over the month as more employees worked part-time rather than full-time hours.

Other Australian data points to note

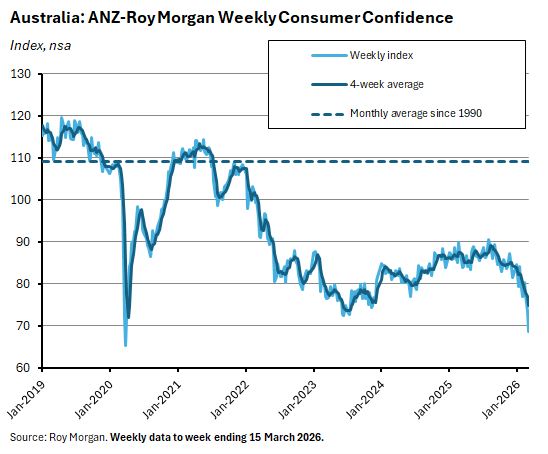

The ANZ-Roy Morgan Consumer Confidence measure fell 4.9 points to a reading of 68.5 in the week ending 15 March 2026. That marks the lowest weekly confidence reading since March 2020 and the early days of the COVID-19 lockdowns. Higher interest rates, increased price pressures, and the war in the Middle East are all likely contributors to softer sentiment.

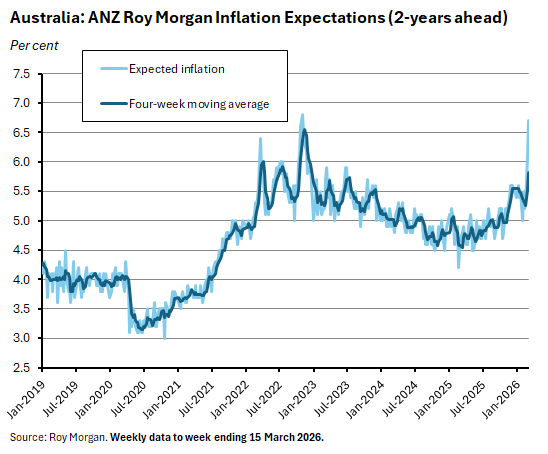

At the same time, the survey’s measure of weekly inflation expectations rose 0.6 percentage points to 6.7 per cent. That marks the highest result since November 2022.

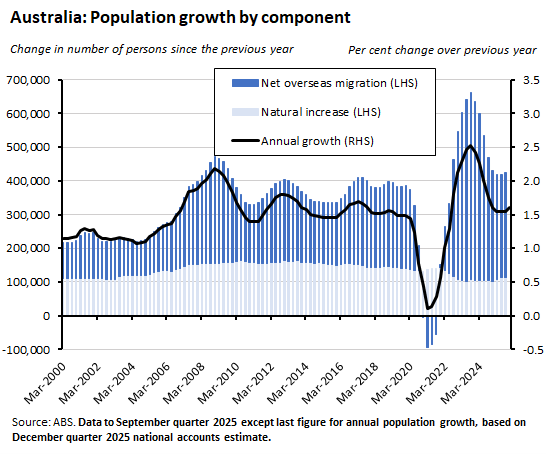

The ABS said Australia’s population grew by 1.6 per cent (423,600 people) over the year to the September quarter 2025, reaching 27.7 million. Of that increase, net overseas migration accounted for 311,000 while natural increase added a further 112,600.

According to the ABS, short-term resident returns rose to 1,665,100 in January this year, an increase of 7.8 per cent over the year, and the highest gain on record. The Bureau said the number of return trips was 19.5 per cent higher than the pre-COVID-19 January 2019 result. Short-term visitor arrivals were 716,680 in January, up 0.9 per cent over the year. Total arrivals were up 5.7 per cent year-on-year to 2,519,500 while total departures rose 3.3 per cent year-on-year to 2,098,140.

The latest ABS Quarterly Tourism Labour Statistics estimates that in the December quarter 2025 there were 736,800 tourism jobs. That figure accounted for 4.5 per cent of all filled jobs in the Australian economy and was up a strong 4.7 per cent (33,100 jobs) from the December quarter 2024. By way of comparison, over the same period the number of jobs across the whole economy rose by a more modest 1.3 per cent.

Further reading and listening·

- This week’s Budget Preview speech from Treasurer Jim Chalmers has already been referenced above in the context of the global energy shock. Chalmers also noted that Treasury has now pushed back its estimate as the likely time it will take for Australian productivity growth to return to its long run trend of 1.2 per cent annual growth, from two years to closer to five years. And he told his audience that budget preparations are now focused on ‘three ambitious reform packages’ comprising a savings package, a productivity and investment package and a tax package.

- The March 2026 edition of the RBA Chart Pack is now available.

- The latest edition of the RBA’s Financial Stability Review says Australia’s ‘financial system is well placed to handle a challenging and uncertain global environment, but it remains important to be prepared for potential shocks’. While the Review assesses that risks to the global financial system have increased, it also judges that most Australian households with mortgages are in a solid position, that most businesses remain resilient, that Australian banks are in decent shape, and that risks posed by non-bank financial institutions remain contained.

- Grattan’s Brendan Woods on the tax treatment of superannuation.

- The e61 Institute on policy learnings for Australia from the 2022 energy price shock.

- Two recent reports from the Department of Industry, one on mobilising the ‘missing middle’ of Australian firms, and one on the Strategic examination of Research and Development. For a short take on the latter, see this column.

- An ASPI report on Australia and critical minerals in a changing global order.

- Two Economist magazine briefings related to the Middle East crisis, one on the damage to the world economy from the war in Iran and one on the impact on US military power.

- In the FT, Nicholas Mulder says the era of US dominance in economic warfare is over.

- A look at three hundred years of wars and the safety of government debt.

- The March 2026 edition of the BIS Quarterly Review.

- Could China stop growing by the 2030s?

- The World Bank has launched a major new report on Industrial Policy for Development. According to Indermit Gil, the Bank’s Chief Economist, the World Bank’s previous, sceptical take on industrial policy has ‘not aged well – it has the practical value of a floppy disk today.’ Back in 1993, the (infamous in some circles) East Asian Miracle report argued that, outside of East Asia, industrial policy was usually a costly failure. Now, the new approach says that in a 21st century global economic landscape ‘that would be unrecognizable to 1990s-era policymakers’ (world average income per capita has almost doubled, educational attainment levels are substantially higher, average inflation is lower and the quality of national economic management higher), the new conditions mean ‘industrial policy is far more replicable than previously thought—and it should be considered in the national policy toolkit of all countries’.

- Measuring national technological trajectories.

- The latest OECD Wage Bulletin reckons that while real wages continue to rise ‘in virtually all OECD countries’ the pace of recovery is slowing, while about half of member countries’ real wages are still below their early 2021 levels.

- Also from the OECD, 25 years of lessons on regulation and growth, drawing on lessons from retail trade and professional services across 15 member countries (not including Australia) between 1998 and 2023.

- The summary of the UBS Global Investment Returns Yearbook 2026 lists ‘ten timeless lessons’ for investors.

- This Aeon essay considers what it says is a looming insurance catastrophe.

- This IMF paper examines firm-level explanations for Europe’s productivity gap with the United States, highlighting smaller markets and limited market-base financing. Summary version on the need for Europe to scale up.

- A look at the economics of hosting the Olympic games.

- A WSJ obituary for Christopher Sims who won the economics version of the Nobel Prize for his work on causality in macroeconomics.

- The FT’s Unhedged podcast analyses markets’ sanguine response to the US war with Iran.

- The Odd Lots podcast on how the war is chewing through US missile stockpiles and a second episode on how the conflict is redrawing the map for natural gas.

- The Macro Musings podcast in conversation with Jesús Fernández-Villaverde on the Quandary of Global Demographic Decline.

Latest news

Already a member?

Login to view this content