Overview

- Elevated levels of energy price volatility over the past week reflect ongoing uncertainty as to the duration of the Middle East conflict, although current pricing continues to suggest that market participants are still thinking interms of weeks, not months.

- Meanwhile, the global oil market is undergoing an historic shock with Gulf oil production lower by at least 10 million barrels per day, shipping through the Strait of Hormuz down to a trickle, widespread force majeure declarations, and mounting damage to regional energy infrastructure. The disruption is also spilling over into other markets and supply chains.

- As Australian petrol prices and inflation expectations head up, markets and RBA-watchers alike now expect the central bank’s Monetary Policy Board to deliver a 25bp rate hike at next week’s meeting. That policy tightening would come despite recent signs of softening business and consumer confidence and the presence of persistent war-related uncertainty.

In this edition, we update our previous assessment of the global energy shock triggered by the war in the Gulf as oil markets undergo the largest supply disruption in their history. We also look ahead to next week’s meeting of the RBA’s Monetary Policy Board. And we provide a quick round up of recent data on Australian consumer and business sentiment and check in on labour market vacancies and marketversus non-market sector employment growth.

The Fog of War keeps markets guessing and on edge

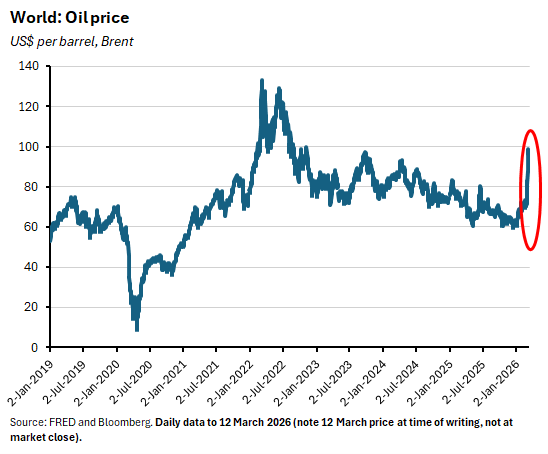

Oil prices have been on a wild ride this week as markets repeatedly reassessed the likely duration of the war in the Middle East.

As the week opened, oil prices surged during Asian trading in response to growing market fears about intensifying supply disruption. Later in the day, news that G7 finance ministers were contemplating a possible joint drawdown of petroleum reserves to stabilise energy markets sent prices into retreat. Then came an afternoon telephone interview with President Trump, during which he told a CBS news reporter that ‘I think the war is very complete, pretty much’ which sent prices lower again. Over the course of 23 hours of turbulent market trading, the Brent oil price surged past US$119 per barrel (/b) before later falling to US$84/b. It was the biggest intraday swing in US dollar terms on record.

And then the next day brought another bout of volatility, after a social media post from the US energy secretary erroneously declared that the US Navy had successfully escorted a tanker through the Strait of Hormuz.

As we discussed in last week’s assessment, markets remain laser-focused on the shifting probabilities regarding the likely duration and intensity of conflict and hence the likely scale of disruption to global energy markets. We suggested then that markets’ belief (hope?) that the conflict was more likely to last weeks than months was at least in part based on the assumption that Washington retained the ability to declare victory and move on at a time that suited the White House. That CBS media interview with President Trump suggested that this scenario was indeed in play (for markets it was ‘Taco time again’). That still seems a plausible interpretation as to the conflict’s likely duration. But as we cautioned last week, there is no guarantee that events will play out this way, perhaps because Tehran might not cooperate (in war, ‘it takes two to Taco’), or just more generally because as Clausewitz put it, ‘In war more than anywhere else things do not turn out as we expect.’

All that said, the oil price remains well up on the start of the year. Recall, many pre-war economic forecasts for the world economy (including the IMF’s January 2026 projections) assumed an oil price that was little changed from where it finished last year – that is, at around US$60/b. For now, the world is diverging significantly from that assumption.

Supply disruption in the Gulf grows

That divergence reflects the fact that both the ‘chokepoint risk’ and energy infrastructure risk we analysed last week have clearly eventuated.

The Strait of Hormuz has effectively been closed after at least 13 vessels have been attacked to date. Gulf producers including Saudi Arabia, Iraq, Kuwait and the UAE have all announced production cuts, due to a mix of safety concerns and mounting storage constraints. According to the International Energy Agency (IEA)’s latest assessment of market conditions, the world is now experiencing ‘the largest supply disruption in the history of the global oil market’ as oil flows through the Strait have fallen ‘to a trickle.’ The IEA reckons Gulf countries have cut total oil production by at least 10 million barrels per day (mbpd), and it expects global oil supply to slump by eight mbpd this month.

QatarEnergy, the world’s largest LNG company, had already declared force majeure (which allows producers to halt shipments without being penalised for failing to deliver contracted oil or gas) and suspended gas production as of last week. Then the Kuwait Petroleum Company (KPC) declared force majeure on its sales of crude oil and petroleum products and the Bahrain Petroleum Company (Bapco) declared force majeure on its refinery operations. Subsequently, major Western energy companies including Shell and TotalEnergies have reportedly begun declaring force majeure on shipments to their own customers.

At the same time, damage to regional energy infrastructure continues to accumulate. Iranian drone attacks have now reportedly triggered fires or other forms of damage at Qatar’s Ras Laffan LNG complex, Saudi Arabia’s Ras Tanura refinery, the UAE’s Ruwais refinery and the Fujairah oil tanker terminal, Bapco’s oil refinery in Bahrain and fuel storage facilities in Oman’s Duqm commercial port. There have also been repeated attempted attacks on Saudi Arabia’s Shaybah and Berri oil fields. In addition, Israeli attacks have damaged a range of Iranian energy infrastructure, including the Tehran Oil Refinery, as well as storage facilities at Aghdasieh and Shahran and other depots in the city.

To mitigate some of the economic fallout from this disruption, IEA members have agreed to release 400 million barrels of oil from their emergency reserves, in what the IEA says is the largest ever oil stock release. According to the Agency, members hold emergency stockpiles of more than 1.2 billion barrels, with a further 600 million barrels of industry stocks held under government obligation. While this will ease the supply crunch, it will not provide a long-term offset to the underlying damage to infrastructure caused by the conflict.

Scope for broadening disruption

As highlighted last time, one significant difference between this Middle East energy price shock and its regional predecessors has been the greater role played by the disruption to LNG flows. As disruption to the Strait extends, the consequences of the interruption to trade flows beyond oil and gas are also becoming apparent. We flagged the importance of fertiliser last week, and warnings of the impact on the global food supply have started to appear. A sharp increase in the price of sulphur is also having ripple effects across a range of industries, including a semiconductor industry which also relies on helium, where Qatar is a key supplier.

Next RBA meeting could now deliver rate hike

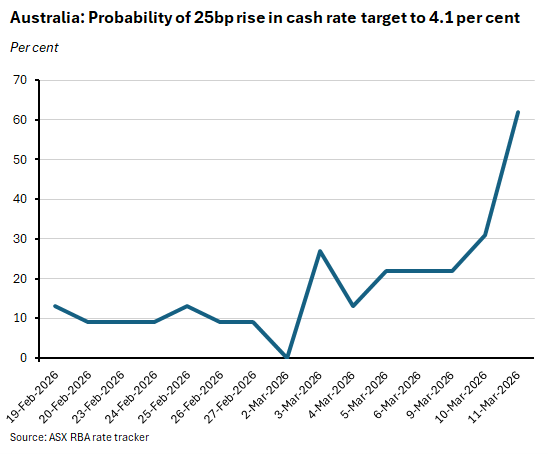

This unfolding global shock has compelled domestic financial markets and many RBA watchers to revise expectations as to the likely trajectory of Australian monetary policy. As a result, next week’s Monetary Policy Board (MPB) meeting is now widely expected to deliver another 25bp increase in the cash rate target. After hovering at around 10 per cent through late February, markets’ assessment of the probability of a rate increase has jumped up over the past few days.

Although abrupt, the shift in market expectations is not unexpected.

Last week, we wrote that the unfolding energy price shock was about to complicate life at Martin Place. Even setting aside the prospect of a new global energy shock, the context for the 16-17 March MPB meeting had already looked challenging. Headline and underlying inflation were running uncomfortably above target and had done so for some time and in response, the MPB had already voted to tighten monetary policy in February. Moreover, further tightening had been priced in by markets and was likewise baked into the assumptions of the latest forecasts in last month’s Statement on Monetary Policy; the latest inflation reading had come in relatively hot; and last week’s December quarter 2025 GDP numbers had depicted an economy growing at well above what the RBA thinks is its speed limit. While all that hadn’t quite convinced markets that a March rate increase was on the cards, they had fully priced in a hike at the following MPB meeting in May.

Add the energy shock to this environment, however, and calculations started to shift.

In that context, we noted that in a post-speech Q&A session last week, Governor Michele Bullock had declared:

‘I’m not making a prediction about March, but it will be a live meeting. We have inflation at 3.8 per cent headline and we have unemployment at 4.1…The Board will be actively looking at whether or not it needs to move more quickly.’

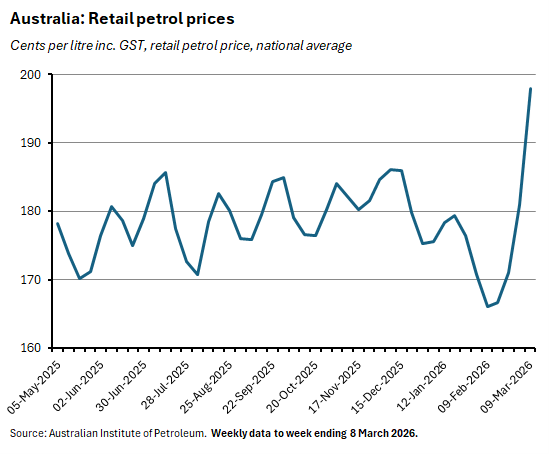

Since then, the conflict has pushed petrol prices higher.

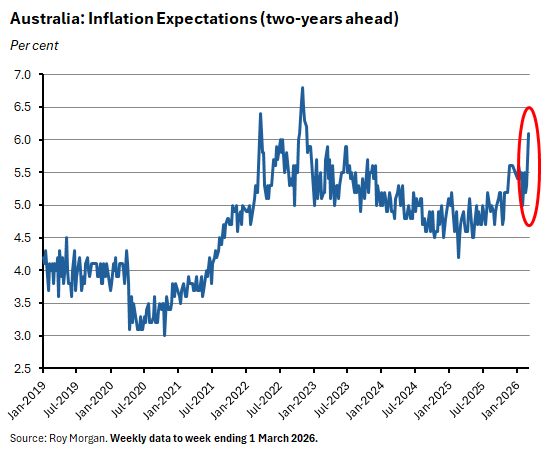

And consumer inflation expectations have also jumped, with the latest ANZ-Roy Morgan weekly inflation expectations leaping by 0.8 percentage points over the week ending 1 March. That increase was the largest weekly rise in the history of the series (which starts in 2010) and pushed inflation expectations up to 6.1 per cent – their highest level since November 2022.

The RBA also sent out further signals regarding its thinking. In an interview on 10 March, Deputy Governor Andrew Hauser said risks to what were already uncomfortably-high pre-war inflation forecasts have now tilted to the upside:

‘We don’t have updated numbers on our forecasts now…But it clearly is the case that it’s an upside risk to that projection in February...I don’t want to give a number that might give a false sense of accuracy, but certainly directionally it’s higher than the projection we published in February.’

When asked whether the Middle East conflict would make a rise in rates more or less likely next week, Hauser set out both sides of the argument. On the case for tightening, he noted that given pre-war data releases had already offered some cause for concern, the prospect of higher energy prices would be unhelpful:

‘We’ve had some data that seem to have confirmed even more decisively than we had before, that our economy currently has limited spare capacity…So against that backdrop…further increases of prices from Iran, if that is what we end up seeing, and that is a big if, is not a helpful development from the perspective of our policy discussion.’

But Hauser also acknowledged that the case was not a slam dunk one:

‘That said, there are arguments…on the other side as well…two in particular. The first…is the uncertainty over developments in Iran is extremely high. That will, if it persists, press down on global activity, and that’s a downside effect to throw into the mix. The other point is, if you look at the domestic data carefully, not everything came in as strongly as expected. Consumption growth in the last quarter of last year was a bit weaker, and unit labour costs, which is something that we look at closely, fell back a little bit further than we’ve been expecting. So there are arguments on both sides.’

Next week MPB members will have to weigh up the two arguments. There is still a decent case for rates remaining on hold until there is greater clarity on the implications of the war (will the deflationary impulse from weaker consumer and business sentiment, higher uncertainty, and reduced spending power dominate the direct impact of higher energy costs for underlying inflationary pressures?). Set against that is the argument for bringing forward what was anyway a widely expected cash rate increase to head off any destabilising shift in inflationary expectations and reinforce the central bank’s inflation-fighting credibility.

Markets and RBA-watchers alike are now confident that the second argument will win out.

It also seems possible that the RBA’s experience with its response to the Ukraine war energy price shock – which has been criticised as being too slow and/or complacent – will prompt a more aggressive approach this time around.

Meanwhile, there are several more days for developments in the Persian Gulf to deliver additional surprises and influence the MPB’s thinking before the meeting.

Australian data points to note

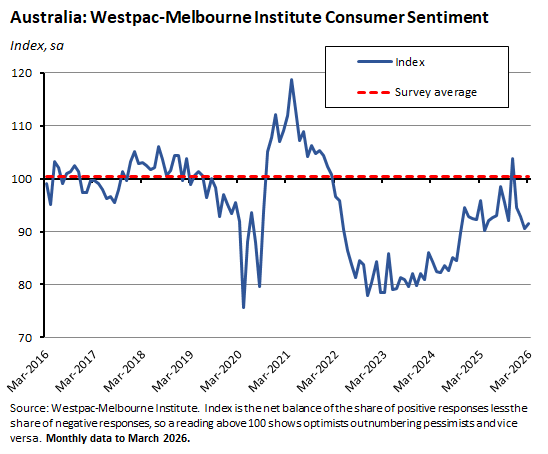

The Westpac-Melbourne Institute Consumer Sentiment Index rose 1.2 per cent to an index reading of 91.6 in March 2026, nudging higher after February’s rate-hike-induced dip. Although sentiment rose this month, Westpac reports the pattern of daily responses point to ‘a material weakening over the course of the survey week, likely reflecting growing concerns about the escalating conflict in the Middle East.’ For example, responses from those surveyed in the final three days were consistent with a much lower index read of 84.

The latest weekly ANZ-Roy Morgan Consumer Confidence reading showed confidence falling 3.7 points to an index reading of 73.4 points in the week ending 1 March 2026, as consumers digest the implications of higher interest rates and a war in the Middle East. The index is now at its lowest level since July 2023. And as already noted above, weekly inflation expectations jumped by 0.8 percentage points over the week to 6.1 per cent. That was the largest weekly increase since the series began in 2010 and returned inflation expectations to their highest level since November 2022.

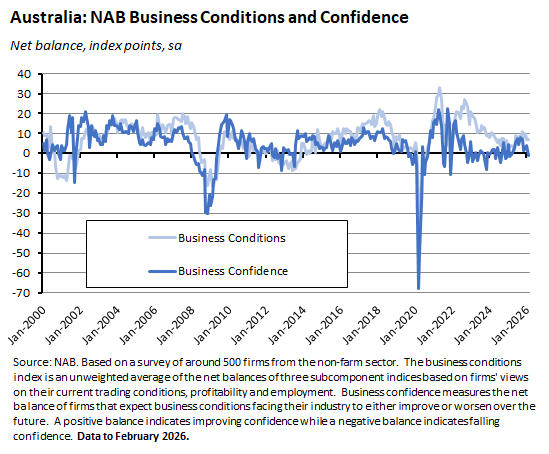

According to the NAB Business Survey, its measure of Business confidence fell four points to a reading of -1 index points. That marked the first time that confidence has fallen into negative territory in 11 months, which NAB linked to some caution in the wake of last month’s RBA rate hike. In contrast, the Business Conditions index remained in positive territory at +7 index points, which is around the survey’s long-term average. The capacity utilisation rate was unchanged in February at 82.8 per cent. Growth in both purchase costs and labour costs rose to 1.5 per cent (quarterly equivalent terms) while growth in final product prices was unchanged at 0.5 per cent. Retail price growth rose to one per cent.

The ABS said the total value of Australian dwellings rose by almost $385 billion over the December quarter 2025 to reach $12.3 trillion. With the number of residential dwellings rising by 54,100 to 11,452,200 over the same period, the mean price of residential dwellings now stands at $1,074,700. Housing values have risen for 13 consecutive quarters from the September quarter 2022. Three states (New South Wales, Queensland, and Western Australia) now have a mean dwelling price of more than $1 million.

Over the year ending in the December quarter 2025 there were 203 new industrial disputes and 213 total disputes. According to the ABS, a total of 112,500 employees were involved across all disputes, while working days lost were 166,700. Corresponding figures for the year ending 2024 were 194, total disputes involving 89,100 employees with 139,100 days lost.

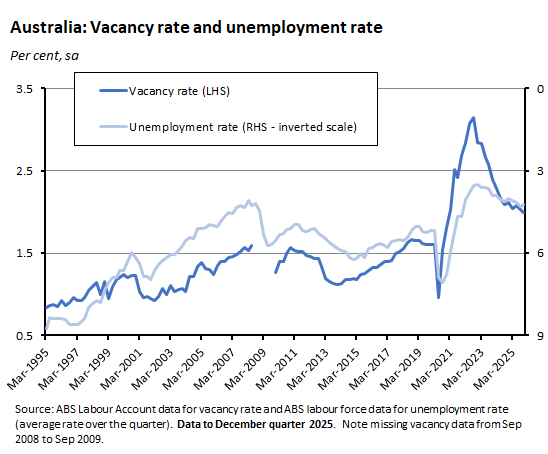

Last Friday, the ABS published the Labour Account for the December quarter 2025. On a seasonally adjusted basis, the total number of jobs rose to 16.4 million (up 1.2 per cent over the year) and the number of filled jobs rose to 16.1 million (up 1.3 per cent over the year). The proportion of vacant jobs was unchanged over the quarter at two per cent. That is well down on the peak of 3.1 per cent reached in the second half of 2022 but still higher than the pre-pandemic rate of 1.6 per cent.

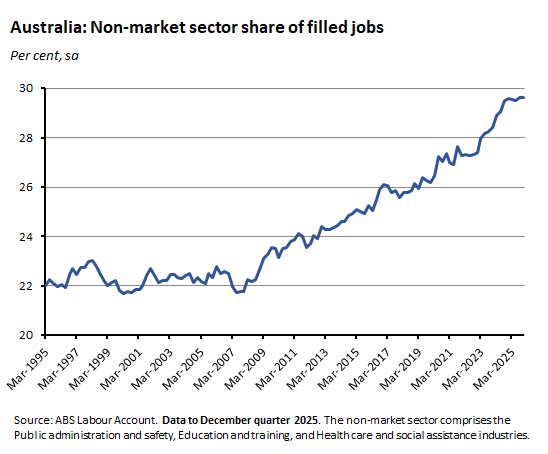

The Bureau also said that over the year to the December quarter 2025, market sector filled jobs rose 1.2 per cent and accounted for around 66 per cent of the growth in total filled jobs while non-market sector filled jobs rose 1.5 per cent and accounted for around 34 per cent of the growth.

Further reading and listening

- Allegra Spender on rewarding effort in taxing times.

- Grattan Institute submissions on a productivity agenda for Australia and the government’s proposed 2027 gas reservation policy.

- The e61 Institute says that inflation’s real driver is supply constraints and also digs into the decline in self-employment.

- New ABS statistics on personal fraud.

- RBA Deputy Governor Andrew Hauser on the safe-haven status of the US dollar.

- In the FT, Martin Wolf on the economic consequences of war with Iran.

- His counterpart at the WSJ, Greg Ip, reckons that a successful end to the US war with Iran could be transformational for world oil security.

- Bloomberg Economics on Iran’s cheap, plentiful weaponry.

- Work on the changing drivers of interest rates and business cycles reckons that the cycle in advanced economies is increasingly driven by global rather than domestic shocks, particularly global supply shocks.

- An FT Big Read on five ways demographics are transforming the world economy.

- After the AI Revolution – China and the United States through the prism of their pursuit of AI dominance.

- Lessons from the failures of Communist reforms.

- On reversing extinction.

- The Odd Lots podcast on how the war in the Gulf is creating a fertiliser crisis.

- The Trumponomics podcast says what you know about recessions could be all wrong.

- The FT Economics Show asks, is AI making us more productive?

Latest news

Already a member?

Login to view this content