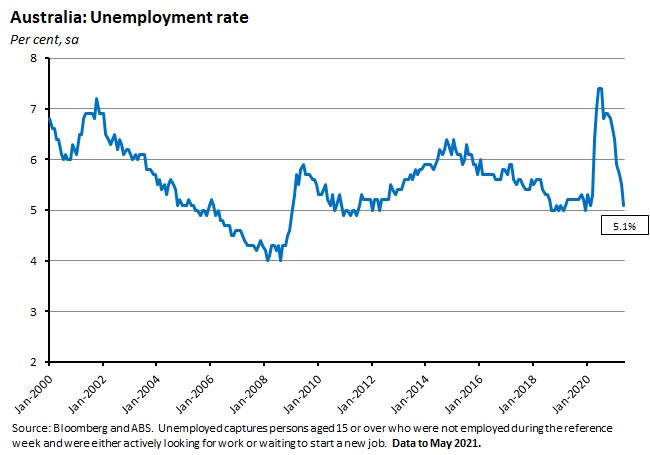

The ABS said that Australia’s unemployment rate fell to 5.1 per cent in May this year as employment rose by more than 115,000 people. Minutes from the 1 June Monetary Policy Meeting of the Reserve Bank Board provided some additional detail on the choices that the RBA will make next month, including a confirmation that it will persist with some version of its asset purchase program.

The ABS combined capital cities index of residential prices rose in the March quarter at the fastest rate since 2009 while the pace of house price increases was the strongest since the series began in 2002. In April, overseas visitor arrivals to Australia jumped by almost 172 per cent over the month as the New Zealand travel bubble took effect, although in overall terms arrivals remain extremely low. The ANZ-Roy Morgan Consumer Confidence Index edged higher, breaking a two-week run of declines. The US Fed left both the target range for the Fed Funds rate and the size of its QE program unchanged after the June FOMC meeting, but the latest economic projections from FOMC members show that the median forecast is for 50bp of rate increases by the end of 2023. One source of the relative increase in Fed hawkishness is recent US inflation readings: US consumer prices in May rose at their fastest rate since 2008, core prices increased at their fastest rate since 1992, and in the same month producer prices recorded their fastest growth in the history of the series.

This week’s readings include the RBA governor on why reports of worker shortages aren’t leading to higher wages, the Productivity Commission’s latest views on productivity developments plus an updated national dashboard, the ABS on Australia’s demographic profile, why the RBA shouldn’t target house prices, why JobSeekers mutual obligations requirements might hinder job search, the OECD on skills, is there an upside to population decline, the sad end of Jack Ma Inc, Green Revolution bottlenecks and the ‘Spectre of Havoc’.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

The ABS said that Australia’s unemployment rate fell to 5.1 per cent in May this year, down 0.4 percentage points from a 5.5 per cent rate in April. The number of unemployed people fell by 53,000 to 701,100.

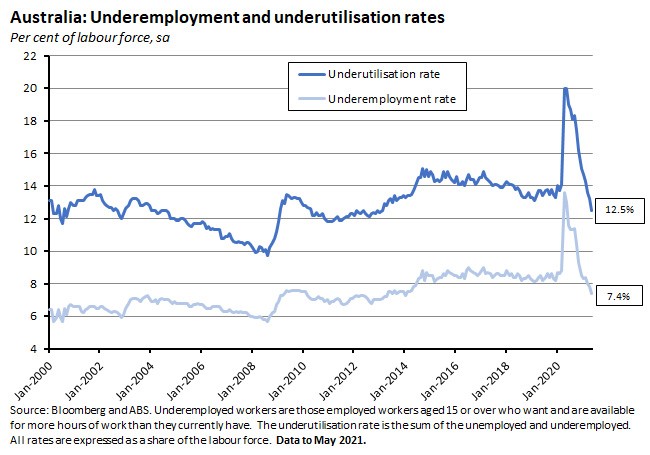

The underemployment rate also fell, dropping from 7.8 per cent in April to 7.4 per cent in May, helping take the underutilisation rate down from 13.2 per cent to 12.5 per cent.

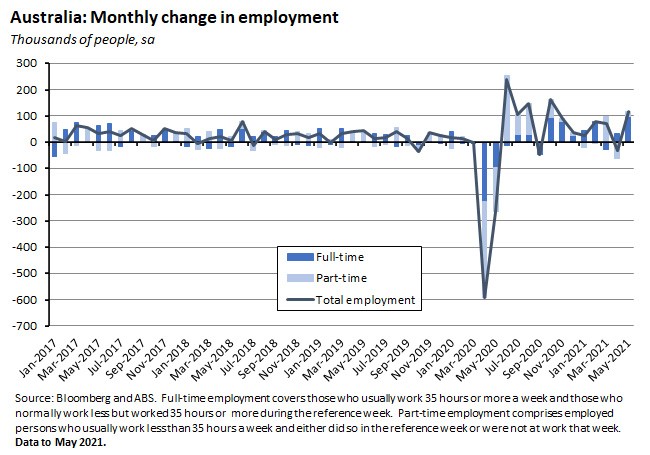

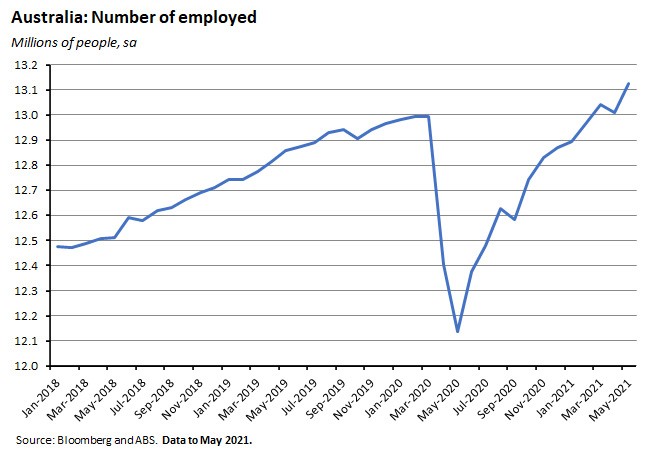

Employment rose by 115,200 people (0.9 per cent) in May to 13.1 million people. Full-time employment rose by 97,500 while part-time employment increased by 17,700. The share of part-time employment in total employment eased from 31.8 per cent in April to 31.7 per cent in May.

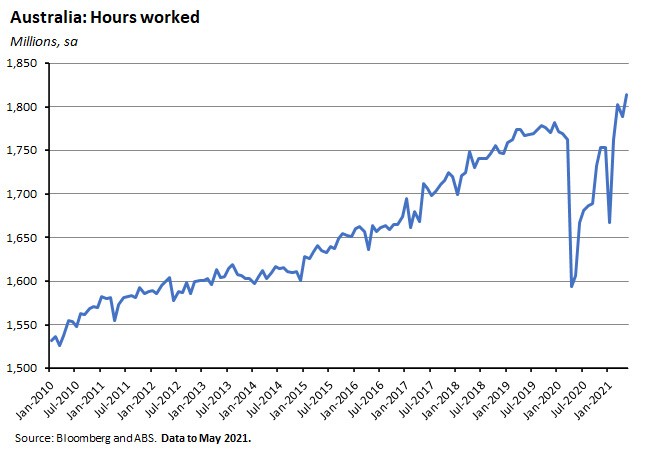

Hours worked increased by 25.2 million hours (1.4 per cent) over the month.

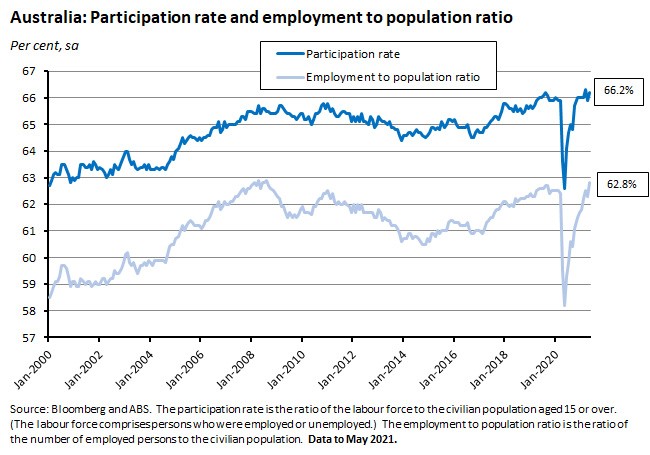

The employment to population ratio increased by 0.5 percentage points to 62.8 per cent in May, while the participation rate rose by 0.3 percentage points to 66.2 per cent.

Why it matters:

Australia’s labour market recovery continues to go from strength to strength. This month’s decline in the unemployment rate not only comfortably beat market expectations of a 5.5 per cent print, but also took the rate back to down to a level not seen since February 2020. That is, the unemployment rate is now back to its pre-pandemic level. In yet more good news, at 7.4 per cent, the underemployment rate is now at its lowest level since January 2014 and the underutilisation rate (now at 12.5 per cent) has not been this low since February 2013.

What’s more, these results came despite a potentially offsetting rise in the participation rate. That was because the economy generated more than 115,000 jobs over the month – again comfortably exceeding the median forecast for a 30,000 jobs lift – and that was more than enough to offset the increased number of workers entering the labour force. The number of people in employment now stands above 13.1 million.

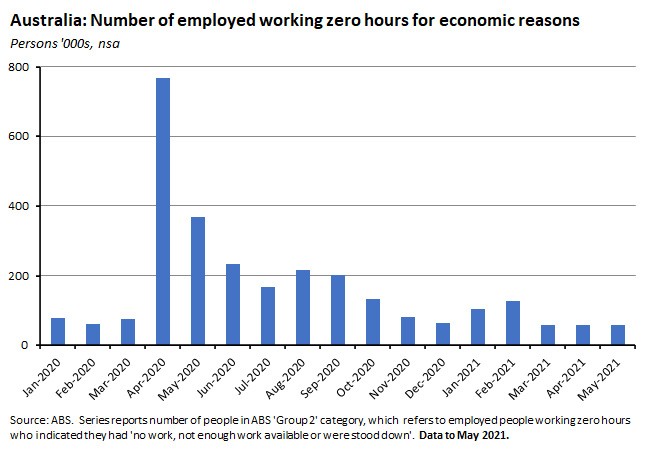

The number of employed people working zero hours for economic reasons (which captures the impact of lockdowns on the labour market) fell in May and is now only a little above 58,000, but note that the May survey reference period was from 2 May to 15 May and therefore before the introduction of the Victorian lockdown from 28 May.

With employment continuing to surprise on the upside, and with the labour market recovery apparently powering through the end of JobKeeper largely unscathed, the focus is increasingly shifting to the implications for wage growth and inflation. To date, the recovery in wages has been much more muted than the recovery in jobs, and both the Treasury and the RBA have estimated that the unemployment rate is likely to need to have a four in front of it to deliver the higher wages that will be needed to allow the RBA to hit its inflation target.

We’re not there yet, but we are getting closer, and we’re doing so much faster than expected. As a result, an increasing number of observers now expect that when the RBA has to make a choice over its Yield Curve Control (YCC) policy next month, it will decide to stick with the April 2024 government bond as its target and not shift to the November 2024 bond, implying that the likely timing for a rate increase has started to narrow from the three-year window previously set by the central bank. For more on this see the latest set of minutes (next story) and this week’s Governor’s speech (covered in the weekly readings).

What happened:

The RBA published the Minutes from the 1 June Monetary Policy Meeting of the Reserve Bank Board. On international inflation dynamics, the minutes reported that:

‘…global supply chain bottlenecks and higher commodity prices had contributed to an increase in producer price inflation in a number of countries. However, increases in wages and other production costs, which are key components of the overall cost base for many firms, had generally been more subdued. Wages growth in the United States had been noticeably stronger than elsewhere. Year-ended consumer price inflation had increased in advanced economies because of the upstream price pressures and an increase in consumer demand as containment measures were relaxed. However, measures of underlying inflation that exclude volatile items had been lower… in most advanced economies, including Australia, spare capacity in labour markets was likely to contain underlying inflationary pressures for some time. Measures of inflation expectations in advanced economies were around or below central banks' targets.’

Similarly, in terms of domestic inflationary pressure, the minutes recorded that:

‘Inflation and wage pressures remained subdued, despite the strong recovery in the economy and employment. A pick-up in inflation and wages growth was expected, but this was likely to be only gradual and modest…The reversal of some COVID-19-related price reductions would see inflation temporarily rise above three per cent in the June quarter before falling back below the target…the strong focus on cost containment by businesses meant that it would take some time for spare capacity to be reduced and the labour market to be tight enough to generate wage increases consistent with achieving the inflation target. Moreover, it was likely that overall wages growth would need to be sustainably above 3 per cent to achieve the target.’

The minutes also provided some additional detail around the decisions to be made at July’s RBA meeting, when the central bank will decide on the futures of both its yield curve control (YCC) and its asset purchase or quantitative easing (QE) programs. On YCC, the minutes stated that:

‘Regarding the 3-year yield target, the Board will consider whether to retain the April 2024 bond as the target bond or extend the target to the next maturity, the November 2024 bond…the Board had previously stated that it would not increase the cash rate until actual inflation is sustainably within the two to three per cent target range. A key consideration for the decision regarding the yield target would be an assessment of the prospect of this condition being met some time in 2024. Members also discussed the likely effect…on overall financial conditions.’

And on QE:

‘In relation to the government bond purchase program, the Board would decide upon future government bond purchases at the July meeting ahead of the completion of the second $100 billion of purchases in early September 2021. The options discussed included ceasing purchasing bonds in September (other than to support the yield target if necessary); repeating $100 billion of purchases for another 6 months; scaling back the amount purchased or spreading the purchases over a longer period; and moving to an approach where the pace of the bond purchases is reviewed more frequently, based on the flow of data and the economic outlook. Key considerations…would be the progress made towards the Board's goals for employment and inflation, and the likely effect of different options on overall financial conditions. Observing that the bond purchase program had been one of the factors underpinning the accommodative conditions necessary for the economic recovery, members thought it would be premature to consider ceasing the program.’

The RBA is forecast to own around 30 per cent of Australian Government Securities outstanding and around 15 per cent of bonds issued by Australian states and territories outstanding by the end of its second asset purchase program in September 2021, a share which the RBA puts ‘at the lower end of other central banks' ownership share of outstanding government bonds.’

Why it matters:

This week’s release of the minutes for the June meeting provided a little more context for the decisions on YCC and QE that will be taken next month. On the former, the key determining factor will be whether the central bank thinks that inflation is likely to be sustainably on target by the first half of 2024, or whether more time will be needed. Here, this week’s labour market report is already being interpreted as supporting the case for H1:2024. On the latter, the minutes told us that the RBA has ruled out the case for ceasing QE altogether, a move which members viewed as ‘premature’, but will instead choose from three other options: (1) replicating the parameters of the two previous programs (QE1 and QE2); (2) either scaling back the size of the program or stretching the purchases out over a longer period – either or both of which would represent a tapering of the existing QE program; or (3) increasing the frequency of program reviews and thereby implicitly adopting a more variable or flexible version of QE.

The RBA continues to make the case that any increase in actual inflation is likely to be transitory, emphasising that there is little sign of any sustained increase in wage pressures. It judges that there is still scope for further increases in the participation rate, and that this means there remains a pool of workers available to meet rising demand for labour. And while the RBA’s liaison program is telling the central bank that labour shortages are emerging in some pockets of the economy – with reduced access to foreign labour and barriers to interstate people movements being contributory factors – the same program is also reporting that firms remain resistant to paying increased wages, noting that: ‘firms facing labour shortages were citing a preference for non-wage measures to attract and retain staff, such as one-off bonuses and more flexible working arrangements. Some firms were also opting to ration output because of labour shortages, rather than pay higher wages to attract new workers.’ See also the discussion in this week’s reading section on Governor Lowe’s 17 June speech, below.

There was another nod towards developments in Australia’s booming housing market, with the discussion noting that ‘members continued to emphasise the importance of maintaining lending standards and carefully monitoring trends in borrowing.’

Lastly, the minutes also included some further discussion on the implications of climate change for monetary policy and financial stability, highlighting that the private sector both in Australia and internationally was increasing the disclosure of climate-related risks and developing ‘green finance’ products, that central banks and financial regulators were now more actively accounting for climate-related risks in carrying out their policy and regulatory responsibilities, and that developments globally relating to the management and regulation of climate-related risk were now ‘increasingly prominent in the asset allocation decisions of international investors…[which]…could affect the cost and availability of finance for corporations and governments.’

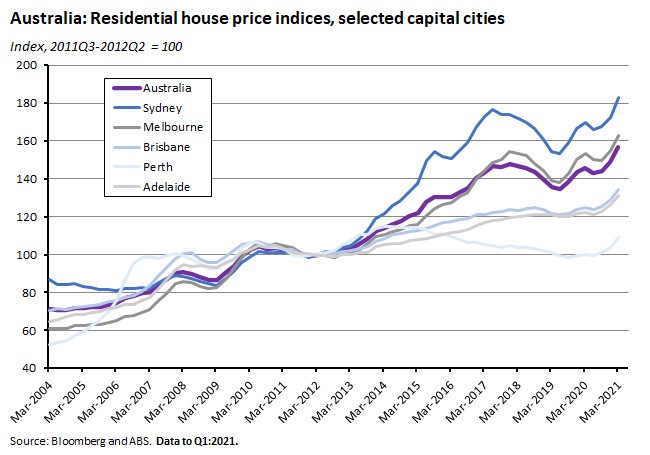

What happened:

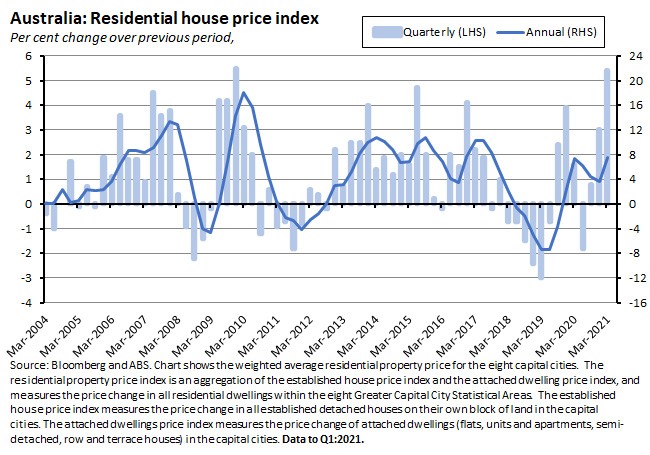

According to the ABS, the weighted average of the eight capital cities Residential Property Price Index rose 5.4 per cent over the March quarter of this year to be 7.5 per cent higher than the corresponding quarter of 2020.

Monthly price gains across the capital cities ranged from a low of four per cent in Brisbane and Adelaide to a high of 6.1 per cent in Sydney and Hobart. In annual terms, growth was highest in Canberra (up 10.9 per cent over the year) and Hobart (up 10.2 per cent) and lowest in Melbourne (up 5.9 per cent) and Darwin (up 6.4 per cent).

The total value of residential dwellings in Australia rose $449.9 billion to $8,293.2 billion in the first quarter of this year. The mean price of residential dwellings in Australia was $779,000, up from $739,900 in the December quarter 2020.

Why it matters:

The ABS quarterly data tell the same story as the CoreLogic monthly numbers that we also track - Australia’s house prices are booming. The March quarter’s 5.4 per cent growth in residential prices was the strongest quarterly result since the December quarter 2009, with all capital cities recording an increase in prices. The Bureau reported price rises across all segments of the housing market although growth in house prices (up 6.4 per cent) continued to outpace price growth in attached dwellings (flats, units and apartments plus semi-detached, row and terrace houses – up 2.7 per cent). The rise in house prices in the March quarter was the strongest since the series began in the March quarter of 2002.

The increase in the total value of Australia’s 10.6 million residential dwellings was also the largest rise on record for this series as the total value of residential dwellings in Australia exceeded $8 trillion for the first time. According to the ABS, New South Wales accounted for approximately 40 per cent or $3.3 trillion of Australia's total value of dwellings as the average price of residential dwellings in the state rose to $1.01 million, marking the first time that any state or territory had seen the average price of dwellings rise above $1 million.

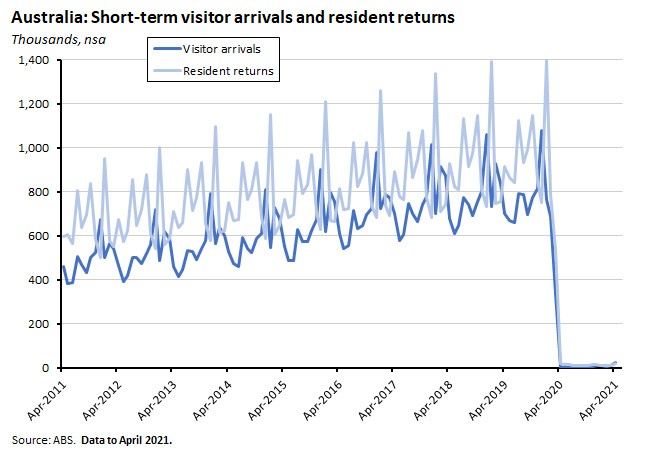

What happened:

Overseas visitor arrivals to Australia in April jumped by 171.9 per cent over the month while Australian resident returns from overseas increased 83.6 per cent from March this year. The ABS said that the number of short-term arrival trips was 22,610, an increase of 20,360 compared with the corresponding month of the previous year but down almost 97 per cent when compared with pre-COVID levels in April 2019.

For resident returns, a total of 16,990 short-term trips were recorded, a decrease of 60 per cent compared with the corresponding month of the previous year and a fall of more than 98 per cent when compared with pre-COVID levels in April 2019.

Why it matters:

The number of overseas visitor arrivals trips to Australia and the number of Australian residents returning from short-term trips (less than one year) both rose to their highest level since COVID-19 travel restrictions were imposed in March last year. The ABS noted that the increase mainly reflected the introduction of the trans-Tasman travel bubble on 18 April 2021, allowing quarantine-free travel between Australia and New Zealand, with New Zealand accounting for 72 per cent of all arrivals and 60 per cent of all resident returns in the month. Even so, overall travel numbers remain extremely low compared to pre-pandemic levels.

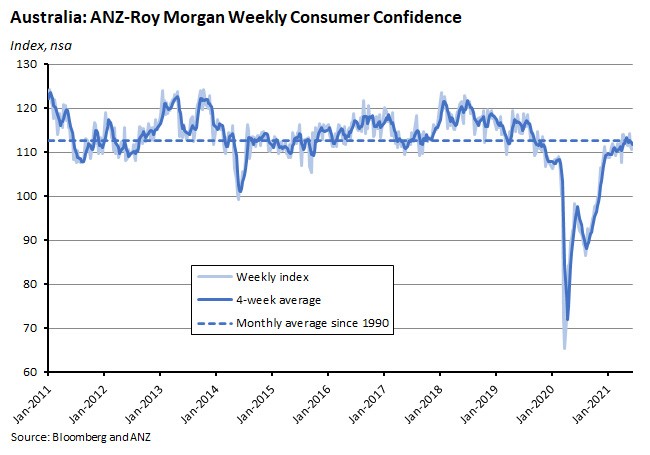

What happened:

The ANZ-Roy Morgan Consumer Confidence Index increased 0.3 per cent to an index reading of 111 for the week of 12-13 June.

Why it matters:

The small weekly rise followed two consecutive weekly declines in the index and marks the end of the two-week Melbourne lockdown.

. . . and what I’ve been following in the global economy.

What happened:

The US Federal Reserve Open Markets Committee (FOMC) left the target range for the fed funds rate unchanged after its 15-16 June meeting and said that it would continue with its program of asset purchases. But Fed officials also used the occasion to indicate that they now expect to start increasing interest rates in 2023 rather than 2024.

The FOMC statement said:

‘The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labour market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to two percent and is on track to moderately exceed two percent for some time. In addition, the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee's maximum employment and price stability goals.’

In the accompanying press conference (pdf), Fed Chairman Jerome Powell painted a positive picture of the status of the US economic recovery, noting that real GDP growth this year was on track to post its fastest rate of increase in decades, household spending was rising at a rapid clip, the housing sector was strong, and business investment was increasing at a solid pace. But he also cautioned that ‘the recovery is incomplete and risks to the economic outlook remain’ and observed that employment remained well down on pre-pandemic levels.

Powell also acknowledged that inflation ‘had increased notably in recent months’ (see next story) and that price increases would ‘likely remain elevated in coming months before moderating.’ He pointed to base effects arising from the very low readings from early in the pandemic, the pass-through of higher oil prices to consumer energy prices, and upward pressure on prices from the combination of rebounding spending and supply bottlenecks limiting the production response. According to Powell, these ‘bottleneck effects have been larger than anticipated, and FOMC participants have revised up their projections for inflation notably for this year.’ However, he continued,

‘As these transitory supply effects abate, inflation is expected to drop back toward our longer-run goal, and the median inflation projection falls from 3.4 per cent this year to 2.1 per cent next year and 2.2 per cent in 2023.’

He also reaffirmed the Fed’s new approach to policy, reminding us that ‘with inflation having run persistently below two per cent, we will aim to achieve inflation moderately above two per cent for some time so that inflation averages two per cent over time and longer-term inflation expectations remain well anchored at two per cent.’ Any change to the fed funds rate remains conditional on labour market conditions reaching ‘levels consistent with the Committee’s assessment of maximum employment’ and inflation rising ‘to two per cent and…on track to moderately exceed two per cent for some time,’ adding:

‘As is evident in the SEP [summary of economic projections], many participants forecast that these favourable economic conditions will be met somewhat sooner than previously projected; the median projection for the appropriate level of the federal funds rate now lies above the effective lower bound in 2023.’

The median projection for the fed funds rate now rises from 0.1 per cent in 2022 to 0.6 per cent in 2023. Back at the time of the March Fed meeting, the median projection still had the fed fends rate at 0.1 per cent in 2023. The range of projections for the fed funds rate in 2023 has also widened: in March the range was 0.1 per cent to 1.1 per cent and that has now expanded to 0.1 per cent to 1.6 per cent.

The Fed Chair also told the press confidence that Fed officials had discussed an eventual reduction (‘talking about talking about tapering’) of the Fed’s quantitative easing (QE) program but that the timing of any such move had yet to be determined, noting that ‘reaching the standard of “substantial further progress” [on meeting the Fed’s goals] is still a ways off.’

Why it matters:

A sequence of faster growth, strong inflation readings and rising inflation expectations (see next story) has prompted an ongoing debate as to when and how quickly the US Fed Reserve might start to raise interest rates – which will have important flow-on effects for global monetary and financial conditions. This week’s FOMC meeting saw the Fed leave the target range for its main policy rate unchanged and persist with the current rate of QE of US$120 billion a month. Actual policy has remained unmoved by the debate – a decision likely reinforced by the fact that the Fed remains some distance from achieving its target of ‘full employment’ with US employment still about 7.6 million jobs down from pre-pandemic levels.

Importantly, however, there was also evidence that recent data outcomes have made Fed officials somewhat more hawkish than they were at the time of the March FOMC. That shift in sentiment appeared in the FOMC’s updated economic projections, which included an upgrade to growth forecasts, an increase in inflation projections and a rebalancing on views on the likely timing of a future rate cut. In particular, the median expectation is now for a rate increase in 2023, not in 2024 as previously expected. The infamous ‘dot plots’ (pdf) which comprise a chart showing each individual FOMC member’s forecast for interest rates as a dot and which appear as part of the SEP package four times a year, now show that a clear majority - 13 out of 18 FOMC members - expect a first interest rate increase to come in 2023. That’s up from a minority (seven out of 18 members) in March (pdf) this year and an even smaller number (only five) in December (pdf) last year. The median projection for the US policy rate is now for it to be 50bp higher by the end of 2023. At the same time, the number of FOMC members projecting a rate increase as early as next year has also increased, rising from just one in December 2020 to four in March 2021 to seven at this week’s meeting. At the same time, the median forecast is still for no change next year and not a single FOMC member expects a change in rates this year.

(All that said, do note that Jerome Powell did warn that changes to the dot plot should be taken with a ‘big grain of salt.’)

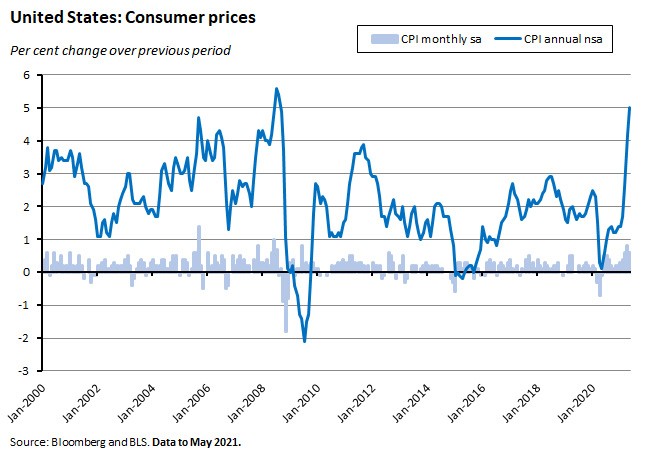

What happened:

Last week, the Labor Department said US consumer prices rose 0.6 per cent over the month in May (seasonally adjusted). In annual terms, consumer prices rose five per cent (original terms).

- The energy index was unchanged over the month but up 28.5 per cent over the year.

- The food index was up 0.4 per cent over the month and 2.2 per cent over the year.

- Used cars and trucks were up 7.3 per cent over the month and 29.7 per cent higher in annual terms.

The large rise in the price of used cars and trucks accounted for about one-third of the seasonally adjusted all items increase last month.

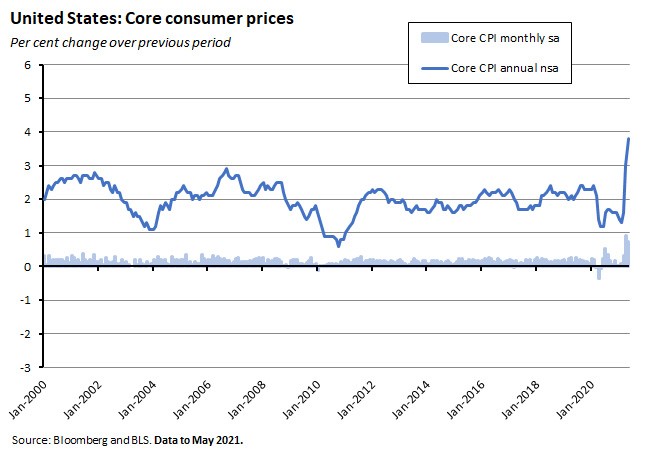

Core consumer prices (all items excluding food and energy) rose 0.7 per cent over the month (seasonally adjusted) and 3.8 per cent over the year (original terms).

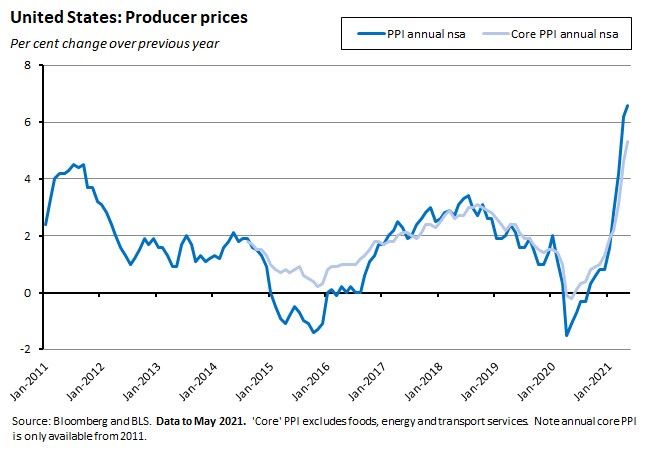

This week, the Labor Department said that US Producer Prices rose 0.8 per cent over the month in May (seasonally adjusted) and increased by 6.6 per cent in annual terms (original basis). A measure of core producer prices, which excludes food, energy and trade services rose 0.7 per cent over the month and 5.3 per cent in year-on-year terms.

Why it matters:

As noted in last week’s discussion on the latest China CPI and PPI readings, questions around the future trajectory of inflation sit at the heart of one of the most important international macroeconomic debates currently underway. In the case of the United States, of course, that debate is given added force by the potential consequences for future monetary policy decisions by the US Federal Reserve, the closest we currently come to having a ‘global’ central bank.

In that context, the five per cent annual increase in the US CPI in May marked the fastest increase in that index since August 2008 while the 3.8 per cent yearly increase in the core CPI was the largest such rise since June 1992. At the same time, the year-on-year growth producer prices was the largest recorded since the start of annual growth data for that series in 2010. All of which would seem to add to the inflationistas case that price pressures are a real and present danger.

As elsewhere in the global economy, the general story behind the spike in US inflation numbers is one of resurgent demand meeting constrained supply, triggering significant price responses in several sectors. Base effects too are playing an important role, with current price comparisons set against last year’s pandemic-depressed price levels. And it’s also the case that the biggest price gains tend to be concentrated in sectors where COVID-related effects are dominating. Producer prices, meanwhile, are being driven higher by supply chain disruptions, soaring transport costs, rising commodity prices, and other increases in input costs.

To date, the Fed’s mantra has been that the increase in inflation will prove to be transitory and as such will not call forward an aggressive monetary policy response. And the composition of the May consumer price surprise does provide support for that thesis. Bloomberg Economics, for example, has calculated that it was mainly a small number of reopening-sensitive categories driving price pressures in May, with an estimated 52 per cent of the month-on-month increase coming from just six components (used cars, rental cars, vehicle insurance, lodging, airfares, and food away from home) that also drove 64 per cent of the overall price increase in April.

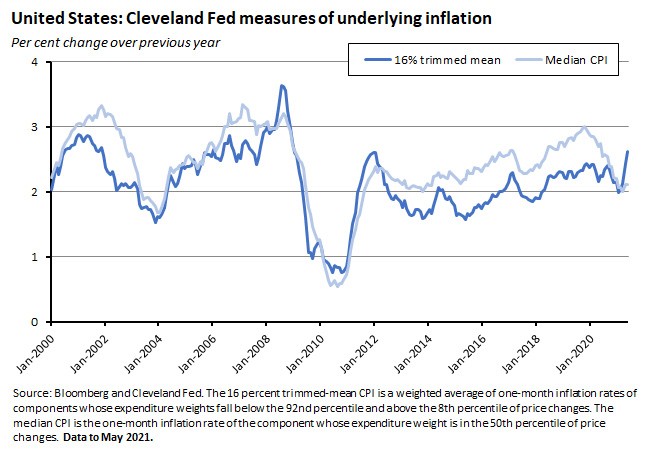

Several of the regional US Fed Reserve banks construct their own analytical inflation series that offer alternative perspectives on recent developments. One approach is to look at underlying inflation measures similar to those provided in the Australian context by the ABS. For example, the Cleveland Fed’s 16 percent trimmed-mean CPI is a weighted average of one-month inflation rates of components whose expenditure weights fall below the 92nd percentile and above the 8th percentile of price changes, while its median CPI is the one-month inflation rate of the component whose expenditure weight is in the 50th percentile of price changes. The idea in both cases is that by excluding outliers (that is, very small and very large price changes), the median and the trimmed mean provide a better signal of the underlying inflation trend. Both measures tell a more moderate inflation story than either the headline or core CPI, although it’s also the case that the trimmed mean measure of inflation has moved significantly higher.

A different approach is to look at the frequency of price changes. The Atlanta Fed constructs a sticky-price CPI that sorts CPI components into either flexible or sticky (that is, slow to change) components. The latest readings show flexible prices up 12.4 per cent year-on-year in May this year while sticky prices recorded a more modest 2.7 per cent year-on-year increase.

Overall, these various measures of inflation confirm that price pressures have increased in the United States while also offering some grounds for caution before asserting that a major inflationary outbreak is underway.

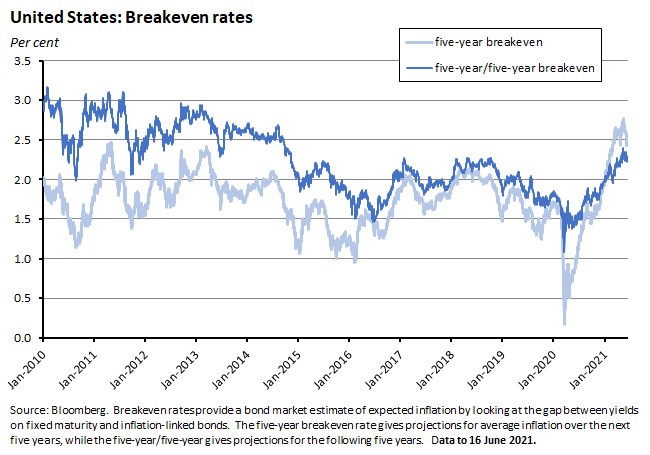

A separate but related concern is that the combination of higher headline inflation rates now plus all of the contemporaneous ‘inflation chatter’ will feed through into future expectations of inflation and then – by changing wage- and price-setting behaviours – risk turning forecasts of higher inflation into self-fulfilling prophecies. Here, the Fed can point to financial market expectations to argue that although price expectations have risen, markets are still not predicting any dramatic inflationary breakout. For example, while the five-year breakeven rate is currently higher than it has been for half a decade, it remains below 2.5 per cent. Similarly, the five-year/five-year rate (which captures inflation expectations for the following five years) is around 2.3 per cent and is still below recent highs. That said, inflationistas could fairly note the significant distortions to bond markets created by QE as a complicating factor in interpreting this kind of data.

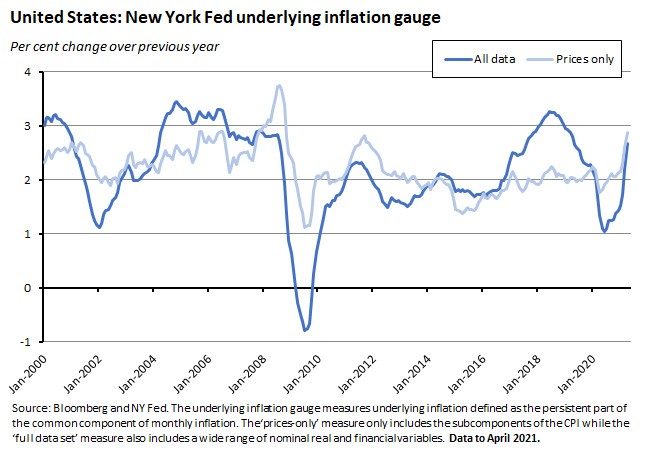

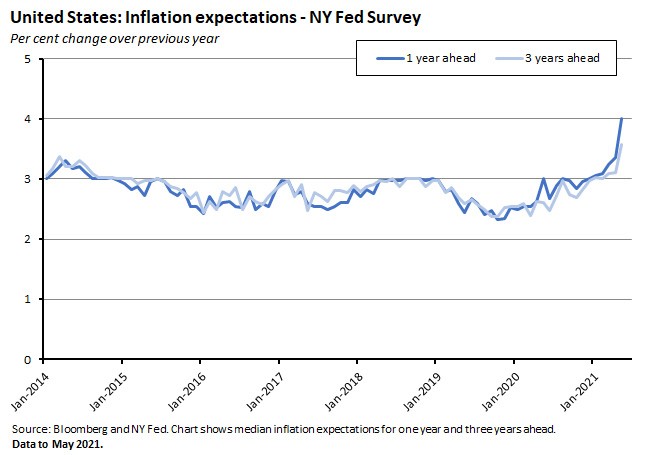

So, what about inflation expectations beyond financial markets? Recent survey results from the NY Federal Reserve again provide some ammunition both for inflationistas and for inflation sceptics. On the one hand, the latest results show the median expectation for inflation over one-year rising to a record high of four per cent in May, up from 3.4 per cent in April. And at the same time, inflation expectations at the three-year horizon rose to 3.6 per cent, up from 3.1 per cent in April, representing an eight-year high. On the other hand, however, the fact that short-term expectations rose more than medium-term ones (the Fed said the gap between the two series hit a record high last month), also provides some support for the argument that a significant share of the present increase in prices is not expected to persist.

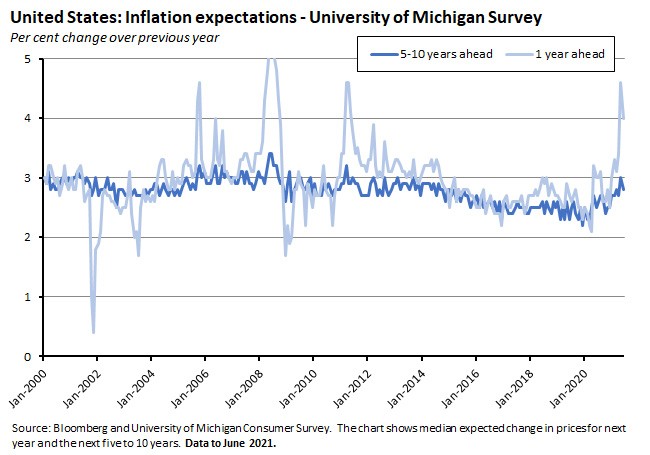

Preliminary results for June from the University of Michigan Consumer Survey suggest that inflation expectations may even have retreated a little this month: consumers expect prices over the next year to rise by about four per cent, down from 4.6 per cent in May. And medium-term expectations remain well-anchored, with prices over the next five to ten years expected to increase by 2.8 per cent, down slightly from a three per cent expectation in the previous month.

On this measure, medium-term inflation expectations have been stable across the current century and – again – are currently showing little sign of any significant breakout.

Overall, then, the data at this point are ambiguous on the inflation story and provide ammunition for both sides of the argument: there is no doubt that US inflation has risen and done so quite markedly, but the durability of that increase is still uncertain. All of which means that the great inflation debate is set to continue. Meanwhile, and as described above, the latest FOMC meeting did see Fed officials increase their inflation forecasts and bring forward their expectations of a future rate hike, albeit only 50bp in 2023.

What I’ve been reading . . .

- RBA Governor Philip Lowe gave a speech on From Recovery to Expansion. Lowe touched on three issues relating to the transition from recovery to expansion: household spending, the labour market, and productivity growth. On the first of these, he repeated the key message of May’s Statement on Monetary Policy about the key role of future trends in the household savings rate. And on productivity growth, he pointed to the importance of boosting productivity growth and the need for a sustained pick up in the rate of business investment. But perhaps the most interesting comments related to the labour market, where the Governor mused on the apparent disconnect between reports of worker shortages and sluggish wage growth, with Lowe remarking that it was ‘noteworthy that even in those pockets where firms are finding it hardest to hire workers, wage increases are mostly modest.’ His explanation was that with most businesses feeling ‘they are operating in a very competitive market place [with] little ability to raise prices’ this had produced a ‘laser-like focus on costs: if profits can’t be increased by expanding or by raising prices, then it has to be achieved by lowering costs…[which]…has the effect of making wages and prices less responsive to economic conditions.’ As a result, when faced with labour shortages many firms are not inclined to raise wages but instead look for alternative non-wage strategies, while others are adopting what Lowe described as ‘a ‘wait and ration’ approach: wait until labour market conditions ease, perhaps when borders reopen, and until then, ration output…By waiting and rationing, firms can avoid entrenching a higher cost structure in response to a problem that might only be temporary.’

- The June 2021 RBA Bulletin is now available. I’ve not had time to dig into it yet, but as always there’s a range of interesting-looking articles including pieces on the role of the central bank’s balance sheet, the RBA’s bond purchase program, underemployment in the Australian labour market, and international experience with low interest rates and bank profitability.

- The June 2021 Quarterly Statement from the Council of Regulators tells us that members ‘discussed developments in household borrowing and the housing market’ and that ‘members are also paying close attention to the implications of trends in household debt. They discussed the risks that could build if growth in household borrowing substantially outpaced that in income, as well as potential policy options to address these risks.’

- The Productivity Commission’s Productivity Insights 2021 has been released. It notes that while overall labour productivity rose by a weak 0.56 per cent in 2019-20, multifactor productivity fell for the first time in nearly a decade, slipping by 0.68 per cent.

- And the Productivity Commission’s national performance reporting dashboard. It paints a fairly mixed picture on progress against targets.

- The Fair Work Commission issued the 2020-21 Annual Wage Review decision. The Commission decided to increase the National Minimum Wage (NMW) by 2.5 per cent to $772.60/week or $20.33/hour. That’s up from last year’s 1.75 per cent increase but below the RBA’s desire to see wage growth with a ‘three’ in front of it (although that figure does not include a 0.5 percentage point increase in the super contribution which in most NMW cases is likely to come on top of wage hikes).

- The latest ABS Household Impacts of COVID-19 Survey.

- ABS statistics on international services trade over the calendar year: exports of services fell $30 billion (down 29 per cent) in 2020 but imports of services dropped even more, falling by $47 billion (a 45 per cent slump).

- Also from the ABS, data on Australia’s national, state and territory population as at 31 December 2020 and on Migration in 2019-20. Australia’s population rose by 0.5 per cent during 2020, or 136,300 people. That was well down on the 1.5 per cent growth recorded in 2019. That in turn reflected a drop in net overseas migration, which was down almost 99 per cent over the year and which contributed only 3,250 people to population growth. As the Bureau notes, that’s a marked difference from recent years when the contribution has been closer to 250,000. As of June 2020, more than 7.6 million people living in Australia or about 30 per cent of the resident population were born overseas. That’s up from 27 per cent ten years ago. The ABS also reports that ‘there are no observed effects from COVID-19 in total births and deaths statistics to date.’

- Related, the AFR looks at some of the demographic trends that will shape the upcoming Intergenerational Report.

- Richard Holden says it’s not the RBA’s job to worry about house prices.

- Also from the Conversation, JobSeekers subject to mutual obligation rules take longer to find work than those who are not. The obligations also seem to lead to subjects taking less remunerative jobs.

- ACCC Deputy Chair Mick Keogh on competition in Australian agriculture.

- Trade Minister Dan Tehan announced the new free trade agreement (FTA) with the United Kingdom. Background on the deal from DFAT is here. Some caution on FTAs from ABC Business.

- The OECD has pulled together data and analysis on the housing sector across member economies, with contributions on housing and the pandemic and affordability, and links to working papers on Housing, wealth accumulation and wealth distribution and housing markets and macro risks.

- Also from the OECD, Skills Outlook 2021.

- Adair Turner considers the upside of population decline (echoes of the Quiggin piece linked to previously on the end of the population pyramid).

- Greg Ip in the WSJ examines the disconnect between US economic growth and jobs growth, with the gap explained by a dramatic productivity boom that has sent output per worker soaring. Firms are taking advantage of technology to introduce new business models that boost efficiency.

- Two from VoxEU. First, Nick Bloom and his co-authors think that returning to the office will be hard (based on UK survey data). Second, a look at how international capital flows have changed since the global financial crisis: a smaller role for banks and a greater role for market-based funding, increased reliance on domestic currency liabilities, and a less stable foreign direct investment environment.

- Forbes covers the sad end of Jack Ma Inc.

- Andy Haldane (the soon-to-be-former Chief Economist at the Bank of England) warns that the beast of inflation is stalking the land again. Haldane thinks that this could be the most dangerous moment for UK monetary policy since inflation targeting was introduced in 1992.

- Mark Blyth wonders how serious the G7 really is about pledges to reform tax settings.

- Noah Smith sets out how the US could win the global battle for microchip dominance.

- An Economist magazine Briefing on the bottlenecks now being triggered by the Green Revolution.

- Related, an FT Big Read on the copper boom.

- This essay from the Atlantic on How America Fractured into Four Parts has been receiving quite a bit of linkage.

- Two podcasts to finish. The Jolly Swagman podcast talks with Graham ‘Thucydides Trap’ Allison on the Spectre of Havoc. And Intelligence Squared asks Adrian Wooldridge, Is Meritocracy a Mayth? (very UK-centric).

Latest news

Already a member?

Login to view this content