NAB’s monthly index of business conditions rose to another record high in May, propelled by record results for employment, profitability and trading conditions, although business confidence did retreat from April’s high. The Westpac-Melbourne Institute Index of Consumer sentiment fell for a second consecutive month in June, pulled down by the impact of Victoria’s lockdown.

NAB’s monthly index of business conditions rose to another record high in May, propelled by record results for employment, profitability and trading conditions, although business confidence did retreat from April’s high. The Westpac-Melbourne Institute Index of Consumer sentiment fell for a second consecutive month in June, pulled down by the impact of Victoria’s lockdown. ANZ Australian Job Ads rose 7.9 per cent over the month in May to be an impressive 38.8 per cent up on pre-pandemic levels. Labour account data from the ABS showed vacancy rates reached a series record high of two per cent in the March quarter of this year along with a strong recovery in the number of secondary jobs and the number of multiple job holders. Payroll job numbers were up 0.3 per cent between the weeks ending 8 May and 22 May this year and are up 0.2 per cent over the past month. New loan commitments for housing rose 3.7 per cent over the month in April to be 68.2 per cent higher over the year. The J P Morgan Global Composite PMI rose to a 15-year high in May and has now been in expansionary territory for 11 straight months. China’s rate of producer price inflation climbed to nine per cent in May, its fastest rate of increase since September 2008.

This week’s readings include the Productivity Commission on what it fears are misguided ideas around national self-sufficiency and overly sanguine views about debt and deficits, why Australia’s economic recovery is different, common ownership across Australian industry, monetary policy, central banking and inflation in the pandemic era, why the US recovery is different, some of the challenges facing multilateral tax cooperation and whether the theory of Bull**** jobs is just bull****?

Finally, stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

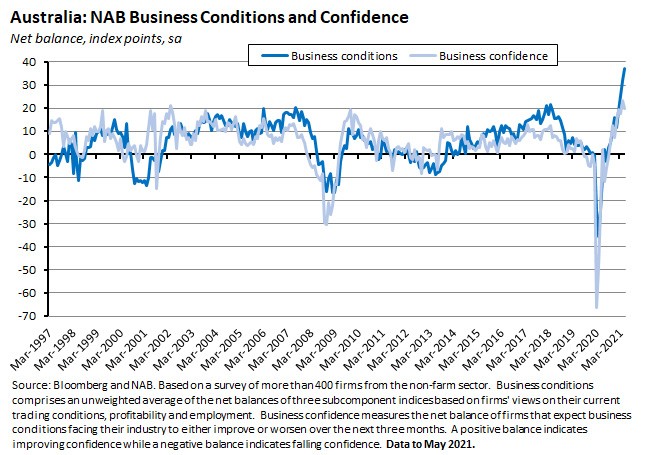

The NAB monthly business survey for May 2021 showed business conditions rising to an index value of +37, up from +32 in April. Business confidence slipped back a little, falling to an index reading of +20 in May from +23 in April.

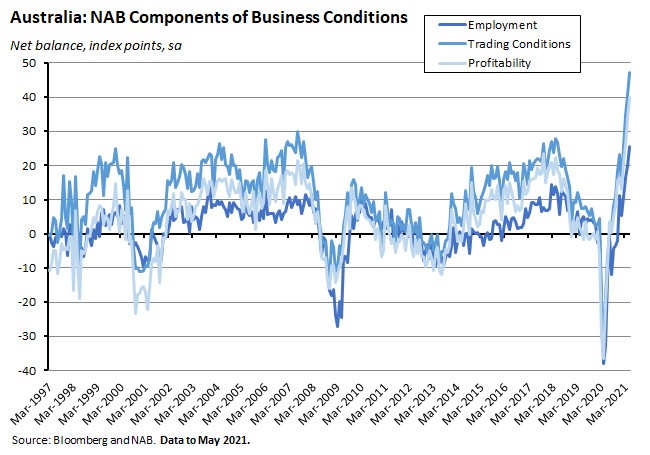

All three subcomponents for the business conditions index rose in May, with trading conditions up from +41 in April to +47 in May, profitability up from +34 to +40 and employment up from +20 to +25.

Gains in business conditions were also recorded by six out of the eight industry groupings tracked by the survey, with mining and recreational and personal services the two exceptions. Business conditions also improved in every state except for Queensland, with New South Wales and Victoria leading the monthly gains.

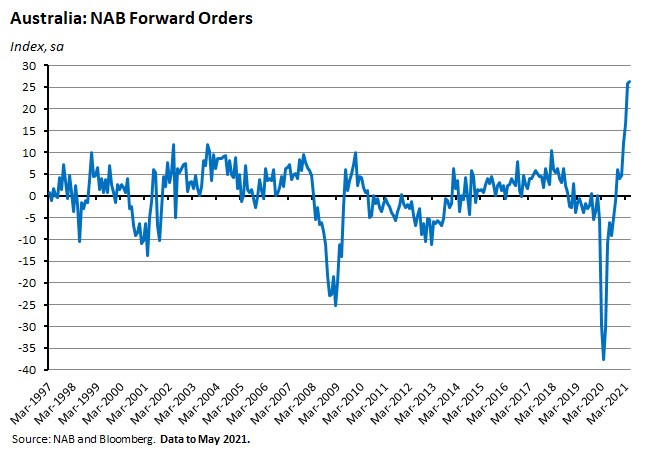

Forward orders were unchanged from April, with an index reading of +26.

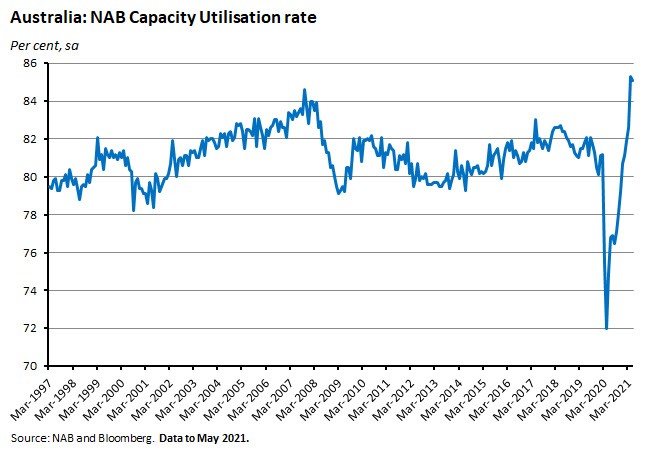

The rate of capacity utilisation slipped slightly over the month, down marginally from 85.3 per cent in April to 85.1 per cent last month.

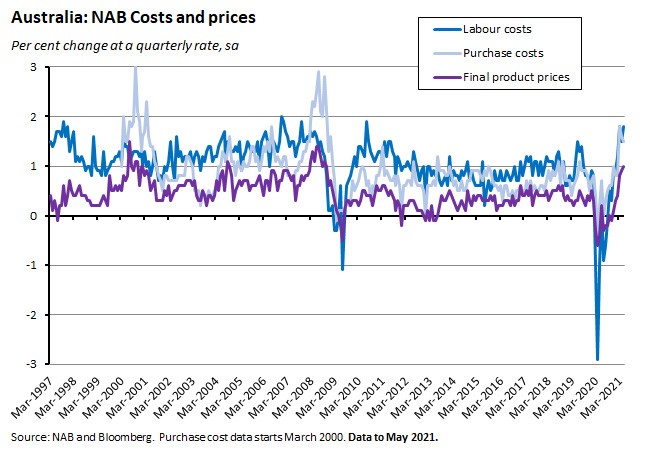

The survey’s inflation indicators were mixed over May. The rate of input cost growth slowed slightly but inflation in final product prices was a little higher and labour cost growth also increased (although NAB notes that this could also reflect firms hiring more employees as opposed to paying higher wages).

Why it matters:

After what had been an extremely strong result in April, May’s survey delivered another incredibly positive set of readings. Business conditions, employment, profitability and trading conditions all hit new record highs last month, while forward orders remained steady at the record level set in April and capacity utilisation continued to run hot. Granted, business confidence did fall back from April’s record high, but it too remains elevated. Note the fieldwork for the NAB survey took place between 18 and 28 May while the Victorian lockdown was announced on 27 May.

The strong employment reading is consistent with the May ANZ job ads report (see below) in suggesting ample scope for further gains in employment and falls in unemployment, and strong results for capacity utilisation and forward orders should likewise be positive for business investment intentions.

What happened:

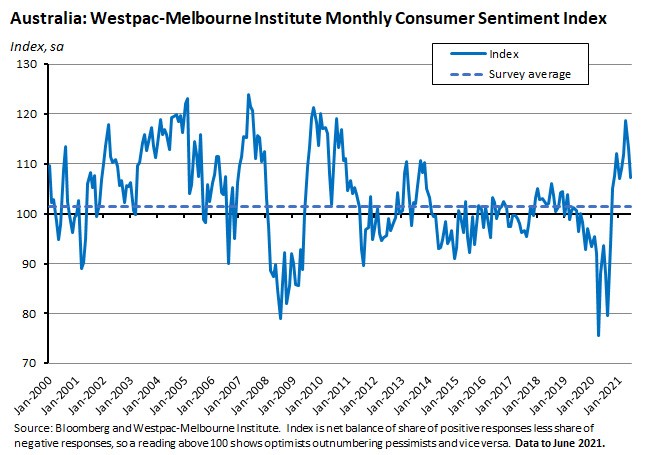

The Westpac-Melbourne Institute Index of Consumer Sentiment (pdf) fell to an index reading of 107.2 in June from 113.1 in May, a 5.2 per cent drop.

All of the individual index components also fell in June: ‘family finances vs a year’ ago (down 8.5 per cent over the month), ‘family finances next 12 months’ (down two per cent), ‘economic conditions next 12 months’ (down 10.3 per cent), ‘economic conditions next five years’ (down 1.4 per cent), and ‘time to buy a major household item’ (down 4.1 per cent).

By state, the Consumer Sentiment Index dropped 7.5 per cent over the month in Victoria, and also fell by nine per cent in Western Australia, by four per cent in Queensland and by 10.9 per cent in South Australia. The smallest decline was in New South Wales, where sentiment slipped just 1.1 per cent relative to May. Westpac noted the relative resilience of New South Wales, with sentiment in the state now 15.4 per cent above Victoria; 11 per cent above Queensland; 19.3 per cent above Western Australia; 14.4 per cent above South Australia and 29.6 per cent above Tasmania.

The Unemployment Expectations Index rose 8.2 per cent over the month, indicating a rise in the share of households expecting joblessness to increase in the year ahead.

‘Time to buy a dwelling’ dropped 7.1 per cent while the House Price Expectations Index fell 3.6 per cent relative to May’s readings.

Why it matters:

After hitting an eleven-year high back in April this year, the Consumer Sentiment Index has now fallen for two consecutive months, taking it back to the levels reported in January 2021. That still leaves sentiment this month above the corresponding levels in June 2020 and June 2019, and also well above the series average of 101.4.

Westpac note that the most likely driver of this month’s decline in sentiment is concerns around the lockdown in Melbourne, with the June survey conducted during the lockdown’s first week. That’s certainly consistent with the large drop in sentiment in Victoria this month. The sizeable falls in other states suggest some spillover effects on overall confidence are at work and Westpac also suggested the presence of some more direct spillovers for some states in terms of local tourism impacts.

The rise in the Unemployment Index cuts against the good news on job ads and on business employment expectations (although this index had delivered its best reading in a decade in May).

The ‘time to buy a dwelling’ index has now fallen for five consecutive months and has moved into pessimistic territory for the first time since April last year, indicating that rapid price increases are eroding affordability.

What happened:

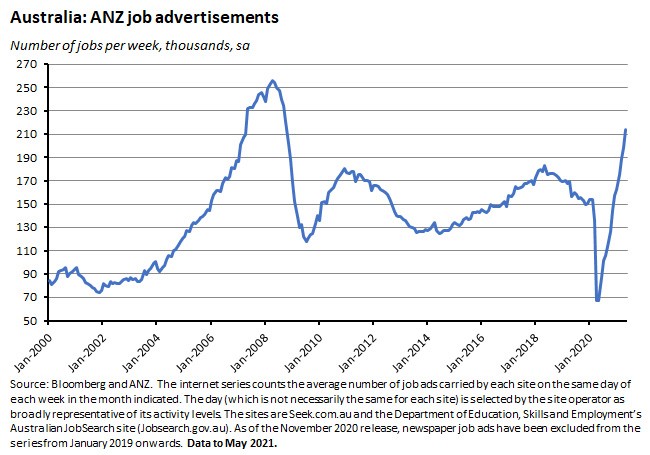

ANZ Australian Jobs Ads rose 7.9 per cent over the month in May to be a up substantial 38.8 per cent on pre-pandemic levels.

Why it matters:

The Job Ads series has now recorded 12 consecutive monthly gains and according to ANZ at its current level is consistent with an unemployment rate of around five per cent (as of April the official unemployment rate was 5.5 per cent).

What happened:

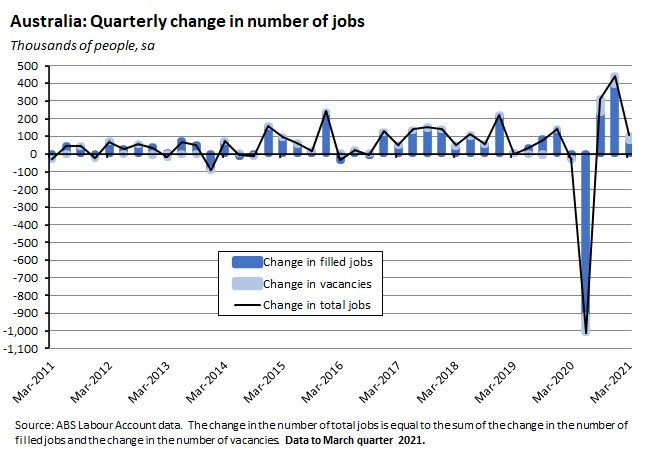

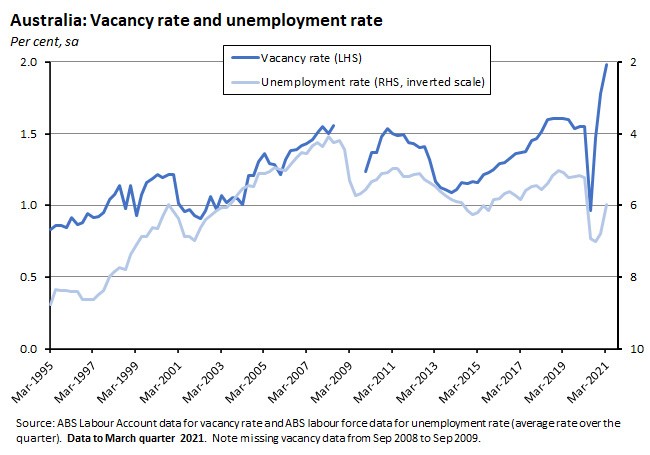

Labour account data released by the ABS showed that in the March quarter 2021 the total number of jobs increased by 0.7 per cent (seasonally adjusted) to 104,900 but were down one per cent over the year. The number of filled jobs rose 0.5 per cent over the quarter while the number of vacancies jumped by 12.1 per cent.

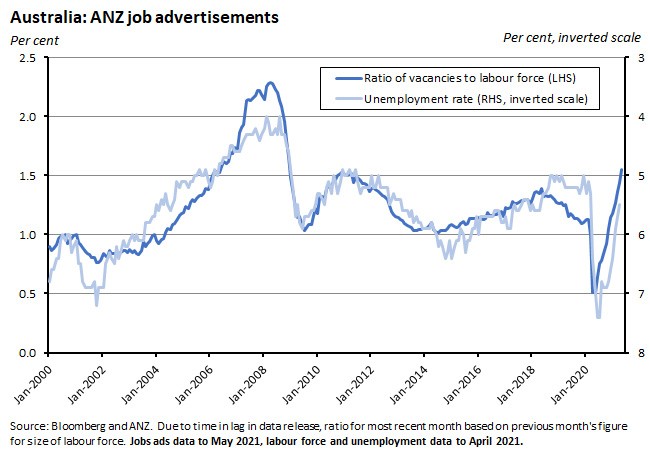

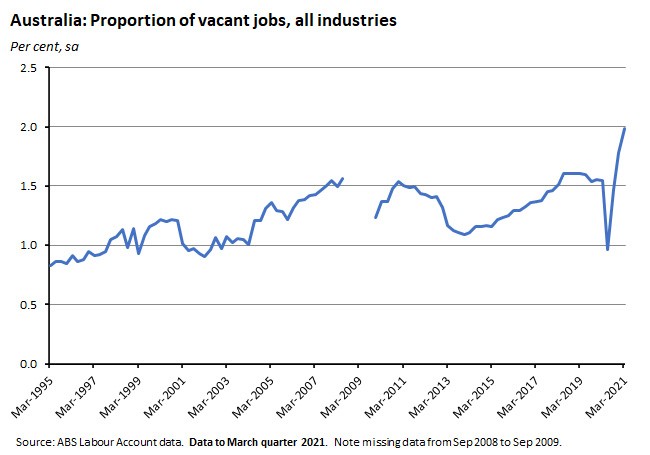

The proportion of vacant jobs across all industries rose to two per cent in the March quarter, a series high.

Main jobs were up 0.1 per cent over the quarter while secondary jobs rose 5.5 per cent (secondary jobs are where a person is working more than one job at the same time, and may consist of one or more additional jobs. Secondary jobs can be held by people who have their main job in the same or a different industry). On an annual basis, total job numbers were down one per cent relative to the March quarter 2020 with main jobs down 2.1 per cent. Secondary jobs, however, were up 7.5 per cent over the same period.

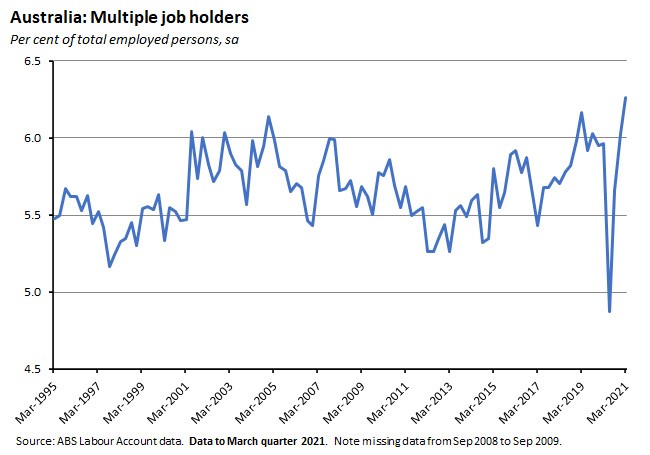

The number of people working multiple jobs increased by 4.6 per cent and the share of multiple job holders rose to a series high of 6.3 per cent in the March quarter of 2021 after having earlier fallen to a series low of 4.9 per cent in the June quarter of last year.

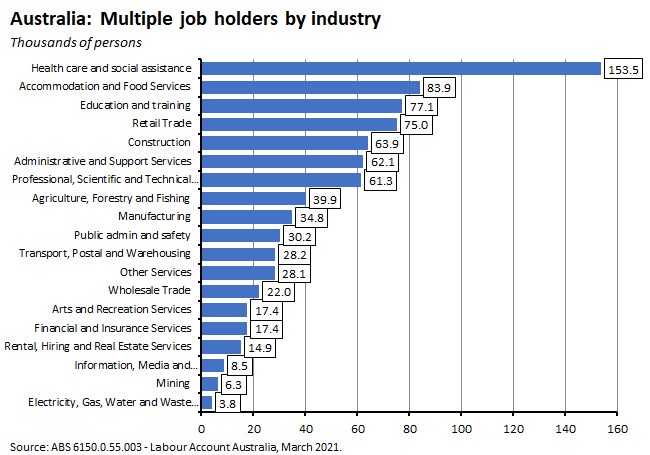

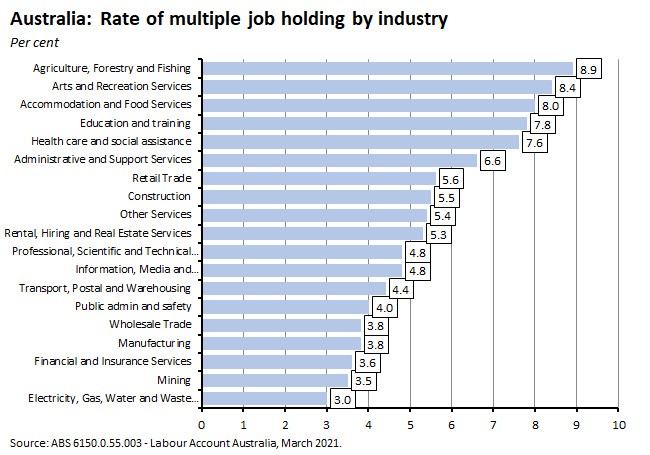

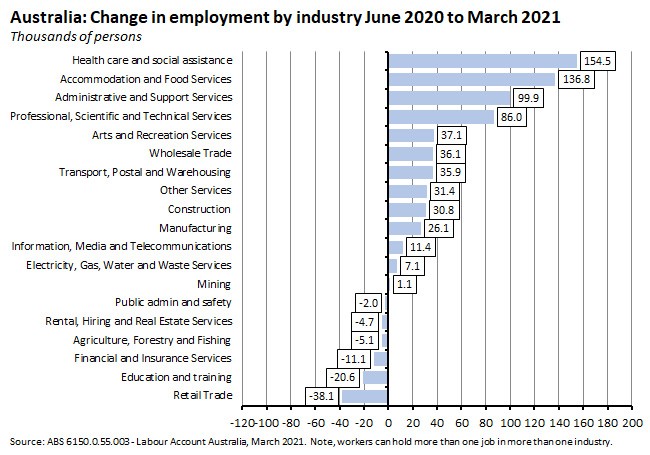

By industry, the largest number of multiple job holders are employed in health care and social assistance services.

Although the industry with the largest share of multiple job holders is Agriculture, forestry and fishing.

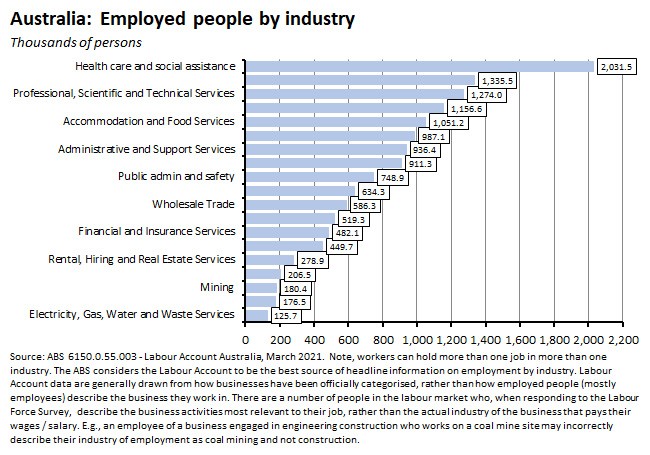

The largest number of employed people in the March quarter of this year was found in health care and social assistance, followed by retail trade, and then professional, scientific and technical services.

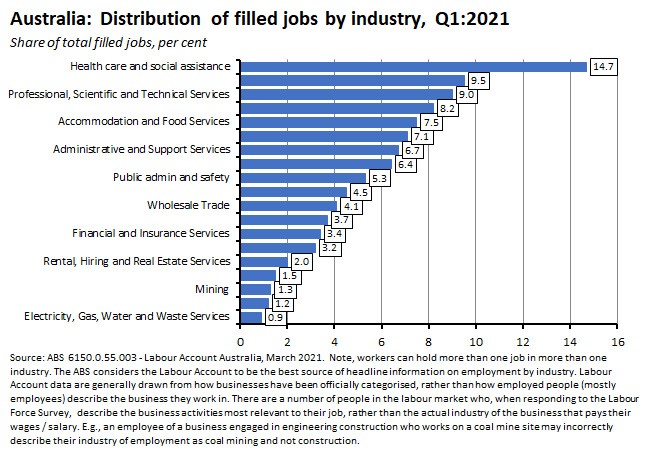

In terms of the share of filled jobs (total jobs is equal to the sum of filled jobs plus vacancies), health care and social assistance accounted for 14.7 per cent, followed by retail trade (9.5 per cent) and professional, scientific and technical services (nine per cent).

Why it matters:

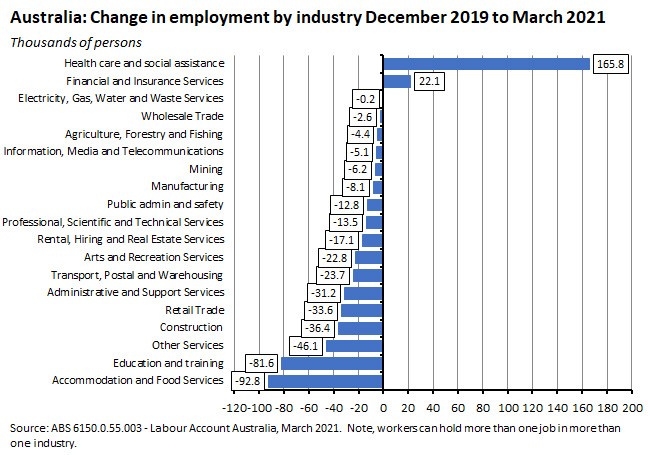

According to the ABS, the Labour Account provides the best source of headline information on employment by industry, and recent shifts in the employment data here paint a picture of the impact of COVID-19 on the structure of employment. For example, over the period between the December quarter of 2019 and the March quarter of this year, the Labour Account numbers show that the pandemic has led to substantial declines in the number of people employed in Accommodation and food services (down almost 93,000), education and training, and other services. Over the same period only two industries have seen a rise in total employment, although there has been a particularly large increase in the number of those employed in health care and social assistance.

At the same time, the Labour Account data also show that, since the June quarter of last year, some of the industries that were initially hit very hard by the pandemic have enjoyed sizeable gains in the number of people employed. Even so, and as the previous chart shows, that growth has been insufficient to restore all of preceding decline in employment.

The Labour Account numbers also depict substantial swings in the number of multiple job holders – starting with a sharp decline early in the pandemic and followed by strong growth over the last three quarters.

Finally, by providing information on vacancy rates, the Labour Account release also offers another source of evidence on the tightness of the labour market and, in conjunction with the labour force survey data on the unemployment rate, a measure of the efficiency of labour market matching.

As noted above – and consistent with the previous story on the high level of job ads – the national vacancy rate rose to a series high of two per cent in the March quarter. As the chart below shows, typically rising vacancy rates are associated with falling rates of unemployment. It also shows that the current recovery has been characterised by a particularly sharp increase in the vacancy rate.

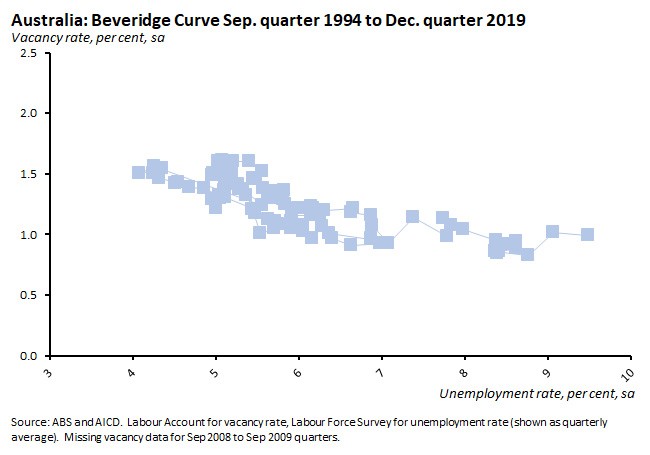

The standard way to depict the relationship between the unemployment rate and the vacancy rate is the Beveridge Curve (named after the British economist William Henry Beveridge, author of the Beveridge Report that underpinned the UK’s post-WW2 welfare state). A stylised version of the curve would slope down from left to right, depicting an inverse relationship between the vacancy rate and the unemployment rate:

- Movements along the curve are assumed to capture different stages of the business cycle.So, for example, during a recession when an economy is shedding jobs, we would expect to see a movement down and to the right along the curve, as the number of vacancies falls and the unemployment rate rises.Once recovery sets in, however, vacancies will start to rise and the unemployment rate decline, implying a movement up and to the left.

- The curve itself can also shift inwards or outwards, depicting a change in the relationship between unemployment and vacancies.The position of the curve can be interpreted as reflecting the overall efficiency of the labour market.For example, an outward shift of the curve (such that a given unemployment rate is associated with a higher vacancy rate) could reflect one or a combination of: a decline in the efficiency with which the labour market matches workers with jobs, a rise in the prevalence of skill mismatches, an increase in the labour market participation rate, an increase in the share of long-term unemploymentor an increase in the rate of job churn.Alternatively, an inward shift of the curve would imply that the labour market was now doing a more efficient job of matching labour demand and supply.

(For more background on what is the Beveridge Curve and what does it tell us – in this case using US data – see this blog post by the Conversable Economist.)

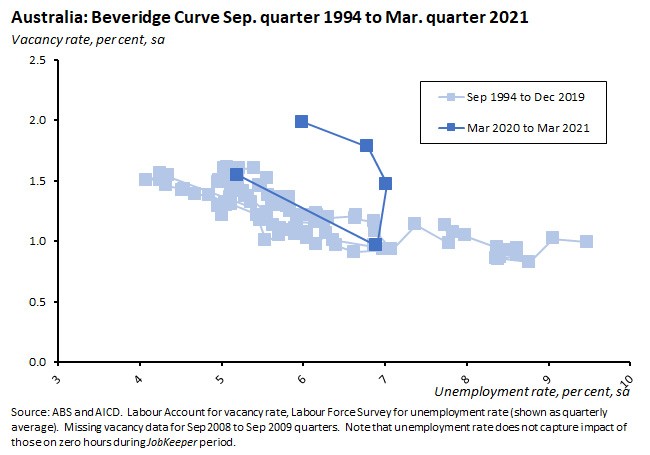

Recent work by Melbourne University’s Jeff Borland (see his April 2021 labour market snapshot – unfortunately the AICD firewall won’t allow a direct link) notes that while the Beveridge Curve for Australia tends to show the expected relationship over time, the most recent set of numbers show higher vacancy rates for a given unemployment rate – suggesting the possibility that the curve might have shifted outwards.

One interpretation of this result is that the Australian labour market has become less efficient at matching jobseekers with jobs, which if correct would be a concerning development. But the more likely scenario is that this pattern in the data reflects the rapid pace of recent moves, and as such is consistent with the broad predictions that would be made by economists’ matching models of the labour market. The intuition here is that the process of matching job to worker (that is, for search and recruitment) typically takes time and therefore in the early stages of recovery, rises in vacancies are likely to outpace actual hiring decisions, and hence the increase in the vacancy rate will tend to outstrip any decline in the unemployment rate. This will particularly be the case if there has been a very rapid bounce back in employment demand – a scenario which has been unfolding here in Australia in recent months. If this interpretation is right, then over time hiring rates will catch up. But it will be important to continue to monitor this relationship to track the ongoing efficiency of the Australian labour market.

What happened:

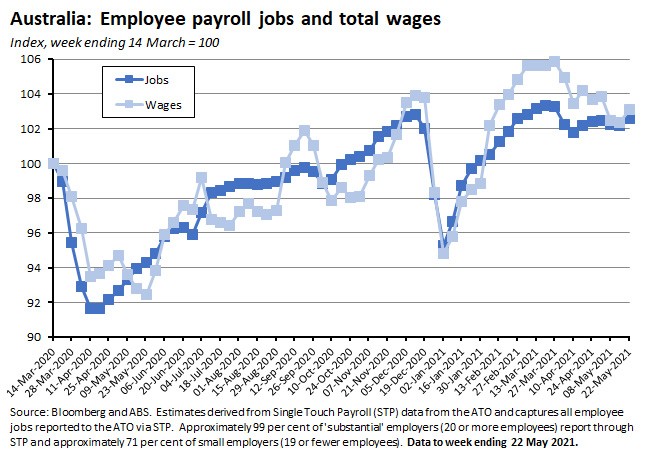

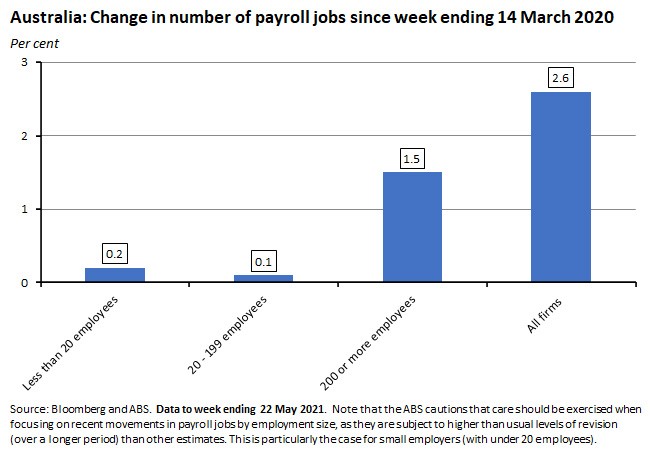

The ABS said that the weekly payroll jobs data showed the number of payroll jobs increased by 0.3 per cent between the weeks ending 8 May and 22 May 2021, compared to a decrease of 0.1 per cent over the previous two weeks. Total wages paid over the same period increased by 0.8 per cent compared to a fall of 1.2 per cent over the previous fortnight.

Since the week ending 14 March 2020, the number of payroll jobs has now increased by 2.6 per cent and total wages paid are up by 3.1 per cent.

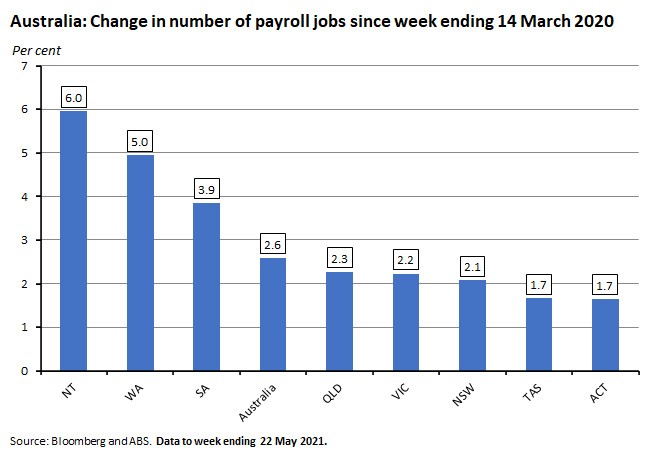

By state, the largest increases in the number of payroll jobs since the week ending 14 March 2020 have been in the Northern Territory (up six per cent), Western Australia (up five per cent) and South Australia (up 3.9 per cent). Job growth has been slowest in Tasmania and the ACT (both up 1.7 per cent).

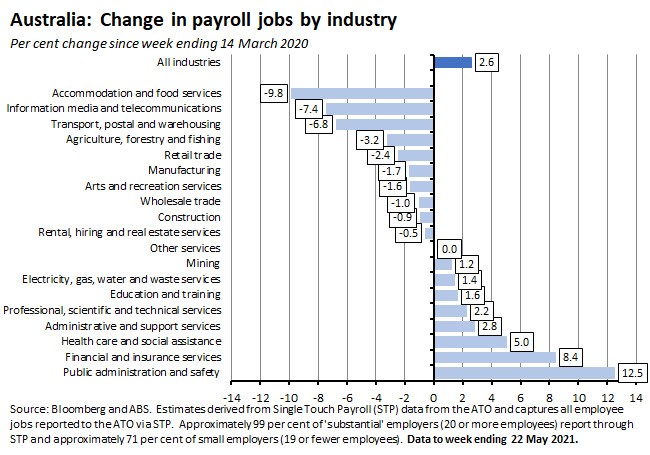

By industry, the biggest percentage declines in payroll jobs numbers since the start of the pandemic are in accommodation and food services (down 9.8 per cent), information, media and telecommunications services (down 7.4 per cent), and transport, postal and warehousing (down 6.8 per cent). The industries that seen the fastest growth in job numbers over the same period are public administration and safety (up 12.5 per cent), financial and insurance services (up 8.4 per cent) and health care and social assistance (up five per cent).

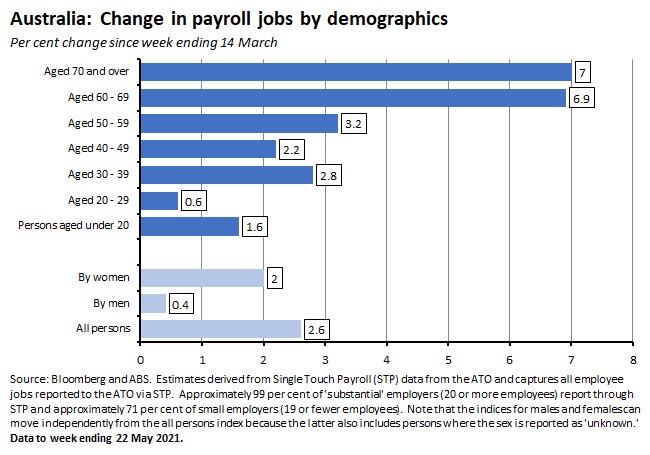

By demographics, all age groups now show job numbers above their pre-pandemic levels.

Likewise, job numbers are now up across all firm sizes.

Why it matters:

As of the week ending 22 May 2021, payroll job numbers were up 2.6 per cent relative to the start of the pandemic and up eight per cent over the same period last year. Job numbers are now up across both men and women, across all age groups, across all states and across all firm sizes. But there continues to be significant divergence by industry, with job numbers still down by almost double digits in accommodation and food services in particular.

Over the most recent fortnight, job numbers rose in every state except Tasmania but note that the latest estimates cover the period before the recent lockdown in Victoria.

With April’s payroll numbers having been influenced by a combination of strong seasonal effects and the end of the JobKeeper program, the May numbers should provide a cleaner take on labour market developments. In that context, payroll job numbers have only edged up by 0.2 per cent over the past month, suggesting that – as noted following the previous payroll job release – the pace of job creation appears to have eased from its earlier (very) rapid pace.

What happened:

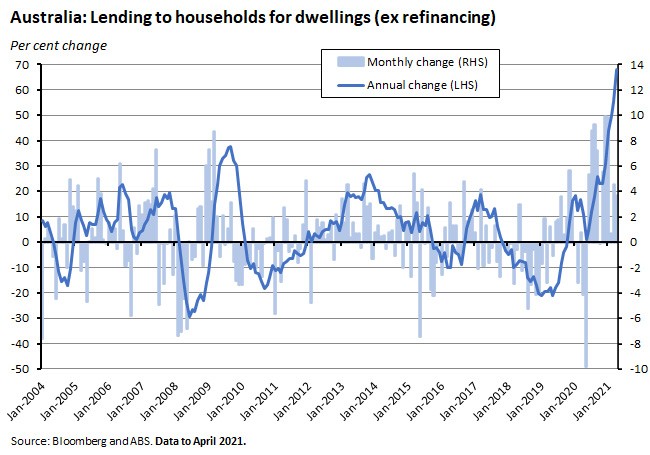

Last Friday, the ABS said that new loan commitments for housing in April rose 3.7 per cent over the month (seasonally adjusted) to be 68.2 per cent higher over the year.

New loan commitments for owner occupiers were up 4.4 per cent month-on-month and 70.1 per cent year-on-year while the corresponding growth rates for lending commitments to investors were 2.1 per cent and 63 per cent, respectively.

New loan commitments for personal fixed term loans rose 4.8 per cent over the month and 57.7 per cent over the year in April. Commitments for businesses for construction fell 10.5 per cent over the month while commitments for business purchase of property rose 27.8 per cent in monthly terms.

Why it matters:

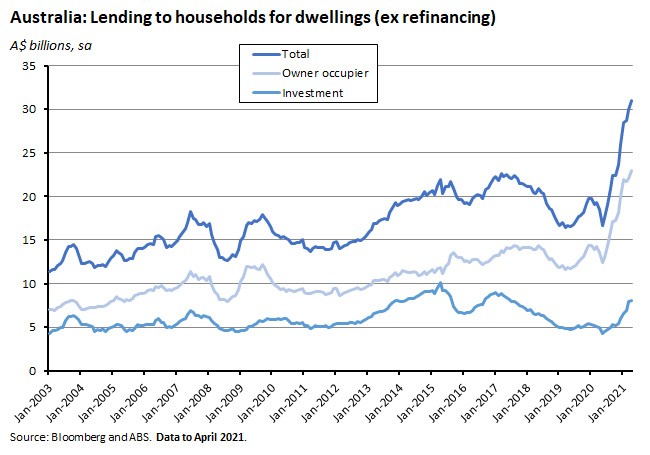

At $31 billion, new loan commitments for housing hit a new record high in April as new commitments for owner-occupiers set another record at $23 billion. New loan commitments to investors also demonstrated more strength, returning to their highest level since mid-2017.

The ABS also noted that the rise in owner occupier lending in April was driven by increased loan commitments for existing dwellings. In contrast, commitments for the construction of new dwellings fell 11.4 per cent, following a 14.8 per cent decline in March. These two falls marked the first monthly declines since the Homebuilder grant was announced in June last year, with the grant closing to new applications from 14 April 2021, although the Bureau also noted that the value of commitments remained at a high level. At the same time, the number of owner occupier first home buyer loan commitments fell 1.9 per cent to 15,171 in April 2021. This was a third consecutive month of decline, but even so commitments remain at their highest level since July 2009.

. . . and what I’ve been following in the global economy.

What happened:

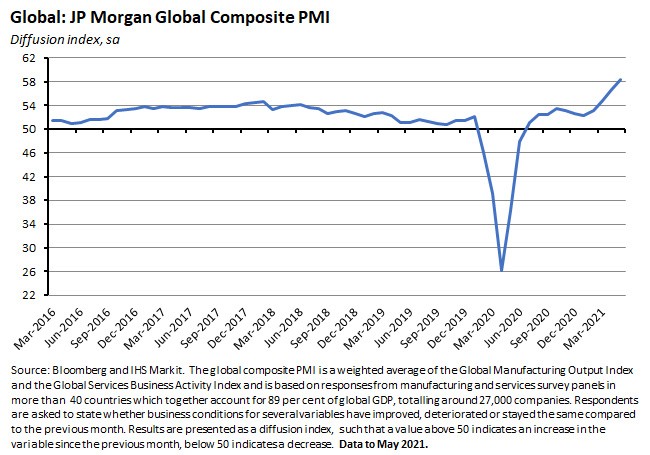

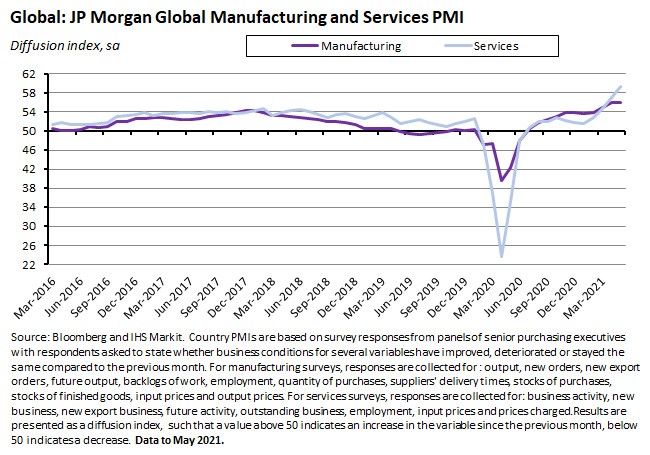

The J P Morgan Global Composite PMI (pdf) rose to 58.4 in May.

The Global Services Business Activity Index rose to 59.4 in May from 57 in April, propelled by strong increases in business activity and new orders. Export business and employment measures slowed relative to April but remained in expansionary territory while input prices and prices charged both accelerated over the month. All six subsectors covered by the survey reported output growth in May for the first time since November 2018.

The Global Manufacturing PMI (pdf) edged up to an index reading of 56 in May from 55.9 in April, reaching its highest level since April 2010, with gains across consumer, intermediate and investment goods sectors, and with 24 out of the 30 nations for which May data was available registering better business conditions. At the same time, the sector continued to report capacity pressures, with average vendor lead times lengthening by the most in the history of the survey, backlogs of work rising at a near-record pace, the steepest rise in input costs for more than a decade and a record inflation reading for selling prices.

Why it matters:

The Composite PMI shows the global economic recovery retains momentum as the index rose to a 15-year high in May, led by survey-record increases in the United States and the United Kingdom as well as a three-year high for the rate of expansion in the Eurozone. Asian economies did relatively less well, however, with growth slowing in China and activity contracting in Japan and India. The overall Index has now been in expansionary territory for 11 straight months while output and new orders rose at their fastest rates since April 2006.

The PMI results also continue to indicate substantial price pressures: input costs as captured by the Composite PMI rose at their fastest rate since August 2008 while output charges increased at the fastest rate on record (since at least October 2009).

What happened:

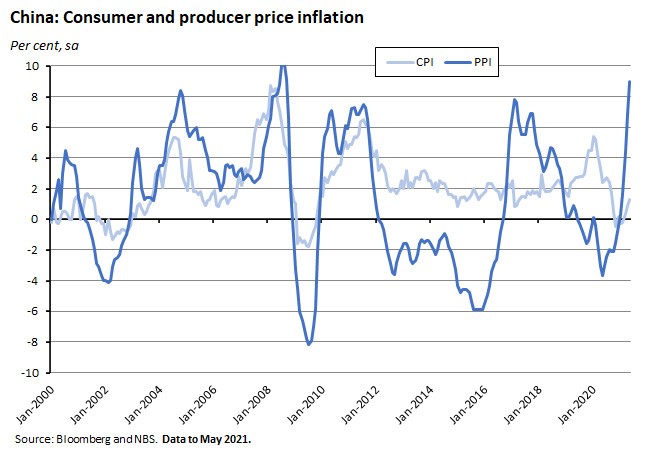

China’s National Bureau of Statistics (NBS) said that China’s Producer Price Index (PPI) rose at a nine per cent annual rate in May this year. The Consumer Price Index (CPI) rose 1.3 per cent over May 2020.

Why it matters:

May’s increase in the PPI beat consensus forecasts of an 8.6 per cent gain and marked the fastest annual pace of growth since September 2008. According to the NBS, large rises in prices for oil, metals (including iron ore) and chemicals helped drive the PPI result, as high commodity prices made their impact felt. Note also that base effects were at work here: the PPI was falling through much of 2020. At the same time, China’s CPI inflation remains subdued with May’s print coming in below market expectations for a 1.5 per cent annual rate (reflecting falling pork prices). All else equal, the divergence between rapidly increasing costs and much more constrained consumer prices implies that Chinese producers are largely absorbing these cost pressures, indicating a significant squeeze on profit margins.

With questions around the future trajectory of inflation one of the most important international macroeconomic debates currently underway, global economy watchers are keeping a close eye on developments in China. In large part, that’s because one of the biggest inflation stories in recent years has been the disinflationary impact of China on the world economy: hyper-competitive Chinese producers have limited the scope for price increases across a range of manufactured goods while the injection of a large supply of (relatively) high skill, low wage workers has applied similar competitive pressures to the world’s workers. But one favourite theory of the inflationistas is that this China effect could be coming to an end. They point to demographic shifts within China, adjustments to the Chinese economic model, and changes to the international trading framework as all likely to contribute to a major change in the role China plays in the world economy, leading to a different balance of inflationary and deflationary forces. And at the same time, of course, any sustained increase in inflationary pressures coming from the world’s factory would not only serve as a signal that such forecasts have some traction but would also warn of a direct risk of imported inflationary pressures.

What I’ve been reading . . .

- The Productivity Commission’s Michael Brennan on Productivity Priorities Post-Pandemic. Brennan’s good news: this is the second time in the last 12 years that ‘Australia has dealt with a global economic crisis better than almost any other economy in the developed world.’ That’s down to getting ‘some big things right’: ‘strong fiscal buffers, a reasonably flexible labour market, openness to trade, well capitalised banks, independent monetary policy, credible public sector institutions and a targeted but redistributive tax-transfer system’ are ‘among the key planks’ of an economic policy framework that COVID has demonstrated continues to work well. But, Brennan argues, he sees two reasons to worry about the nature of Australia’s current policy debate and its potential implications for future productivity performance. First, he is concerned by ‘the renewed promotion of ideas of national self-sufficiency and sovereign capability coming out of the pandemic’ noting that Australia’s past experience with the protection of domestic manufacturing ‘was not an overly happy one.’ And second, he also worries about ‘an overly sanguine view about ever-expanding debt and deficit as an ongoing approach to fiscal policy.’ While stressing that he has ‘no argument with the current fiscal stance’, the Commission’s Chair worries that the public debate could mistakenly assume that ‘debt and deficit no longer matter at all’ with potentially adverse macro- and microeconomic consequences.

- RBA Assistant Governor Christopher Kent spoke about The Term Funding Facility, Other Policy Measures, and Financial Conditions. Kent noted that ‘the improvement in the economic outlook globally and in Australia has contributed to a rise in sovereign bond yields to around pre-pandemic levels’ that has also had implications for other market interest rates. But his message was that these ‘adjustments in financial markets to date are not a cause for concern…Measures of inflation expectations have returned to levels of a few years ago, when inflation was consistent with, or even below, inflation targets…In other words, they don't point to inflation over the coming years sitting above central bank targets in a sustainable way. The increase in nominal yields has been smaller than the increase in expected inflation, which implies that real yields have declined…This is beneficial because it means that monetary policy is more stimulatory than otherwise.’

- The AFR’s John Kehoe analyses why Australia’s economic recovery is different. The key divergence from most past recessions and recoveries is the strength of household and business balance sheets – thanks to huge government stimulus payments that meant that the COVID recession was accompanied by increases in household income and business profits. (Note some parallels here with the United States as captured by the WSJ piece linked below.)

- S&P upgraded the outlook on Australia’s AAA sovereign rating from negative to stable in vote of confidence on the economic response to the pandemic. Fitch ratings is sticking with its negative outlook, however.

- A snapshot of ATO Taxation Statistics 2018-19 (tax stats are only available with a significant lag). Just over half of all tax revenue (51.2 per cent) in 2018-19 came from individual income tax, followed by a 21.1 per cent contribution from company income tax and a 15.5 per cent contribution from the GST.

- Adam Triggs on new research on common ownership across Australian industry. The results suggest that among firms where the research can identify at least one owner, 31 per cent share a substantial owner with a rival company. Across 443 industries, the research identifies 49 that exhibit common ownership, including commercial banking, fuel retailing, insurance and iron ore mining. Who are the common owners in the Australian case? Mostly institutional investors, mainly BlackRock and Vanguard. And why might this matter? Triggs’ concern is that increases in common ownership are another form of market concentration and could lead to decreases in competition and consequent welfare losses.

- A new ABS release of the Characteristics of Australian Business reports survey results on a range of issues including business use of selected information and communication technologies (ICT) and business innovation. Findings included: (only) 69 per cent of businesses recorded using one or more of a selection of ICT, although 95 per cent of large businesses did so; Cloud technology and Cybersecurity software were the most common ICTs used by businesses, followed by Customer relationship management software (CRM) and Electronic data interchange (EDI); leading impediments to ICT use included lack of skilled persons within the business and unsuitable internet speed; e-commerce use has increased, with 50 per cent of all businesses reporting have received online orders in 2019-20 vs 41 per cent in 2018-19; over the same period, the share of businesses placing online orders rose to 68 per cent from 63 per cent; 55 per cent of businesses used paid cloud computing services in 2019-20 up from 42 per cent in 2017-18; the share of businesses reporting internet security incidents or breaches fell to eight per cent in 2019-20, down from 11 per cent in 2017-18 and 16 per cent in 2015-16; and 20 per cent of all businesses said they upgraded their cyber security software, standards or protocols in 2019-20.

- Estimating the cost of Australia’s international border closures.

- Greg Earl on the retreat of Australian investors from China. Earl cites ABS data showing that Australia’s stock of foreign direct investment (FDI) in China almost halved last year, falling from $15.5 billion to $6.8 billion, its lowest level since 2011. And there wasn’t much offsetting diversification into other regional markets: Australian FDI into India also halved while FDI into Southeast Asia fell 40 per cent.

- A new e-book from the CEPR looks at Monetary policy and Central Banking in the COVID Era. It brings together the views of senior central bankers from eight advanced economies and eight emerging markets, including a chapter on Monetary policy in Australia during COVID by the RBA’s Guy Debelle.

- Related, the FT has been running a five-part series on inflation in the COVID Era, seeking to answer the question how much of the current increases in prices is temporary, or transitory to use central bankers’ preferred terminology, and how much is a sign that inflation is back? Current concerns reflect a mix of pandemic-generated effects (big increases in government spending and borrowing plus supply-side bottlenecks and rising commodity prices), longer-term structural shifts (ageing populations and the maturing of China’s economic transition) and a shift in central bank policy frameworks. There’s also a look at how the used-car market has been driving headline inflation in the United States, the way in which the pandemic has changed consumption patterns and thereby distorted official inflation statistics, and the vulnerability of developing countries to higher US inflation because of the potential spillovers from any increase in US interest rates.

- A WSJ long read on how the US economic recovery is unlike anything you’ve seen. It’s a recovery powered by consumers with trillions of dollars in excess savings, businesses keen to hire new workers, a record rate of new business births, record exit rates for workers from existing jobs, and household debt service burdens at near-record lows. At the same time, the economy seems to be suffering from some of the shortages of goods, raw materials and labour that are more commonly experienced toward the end of an economic expansion, not its beginning.

- Via FT Alphaville, how the one percent’s savings buried the middle class in debt.

- And also from the University of Chicago Booth School of Business, Is the Friedman doctrine (on the social responsibility of business) still relevant in the 21st Century?

- The Economist reports that the theory of ‘Bullshit Jobs’ is…maybe…bullshit.

- From the same source, Europe as a corporate also-ran. At the start of the current century, 41 of the world’s 100 most valuable companies were based in Europe, but now only 15 are. Over the same period, Europe’s share of the combined value of the world’s 1000 biggest listed firms and their profits has fallen by almost a half. In part, this is a mechanical result of the rise of China and the growing presence of Chinese businesses. But it’s also influenced by the continued success of corporate America. What explains Europe’s failure relative to the United States? The Economist suggests that (1) US firms have outmanaged their European counterparts, (2) Europe’s biggest firms have been in the ‘wrong’ industries (insurance and telecoms vs software and e-commerce); and (3) the lack of newly created European blue-chip firms (no Amazon, Netflix or Tesla). Other potential contributory factors? Slower European economic growth, a European ‘single market’ that remains much less unified than its US counterpart and which therefore offers fewer economies of scale, and less business-friendly policy regimes.

- A long essay in Vanity Fair on the lab-leak theory of COVID-19’s origins.

- The June 2021 BIS quarterly review focuses on corporate debt since the global financial crisis.

- The IMF lists four factors behind the boom in metals prices: a manufacturing-led recovery; supply side constraints and bottlenecks; expectations regarding a green energy transition and increased infrastructure spending; and relative storability vs other commodities.

- The Trade Talks podcast takes a detailed look at multilateral tax cooperation following the recent agreement reached at the G7.

Latest news

Already a member?

Login to view this content