The July labour force report saw the unemployment rate tumble to 4.6 per cent, its lowest rate since 2008, defying consensus forecasts of a lockdown-driven increase in joblessness. The median forecast also got the direction of change in employment wrong, with the economy adding a modest 2,000 jobs instead of shedding a predicted 43,000.

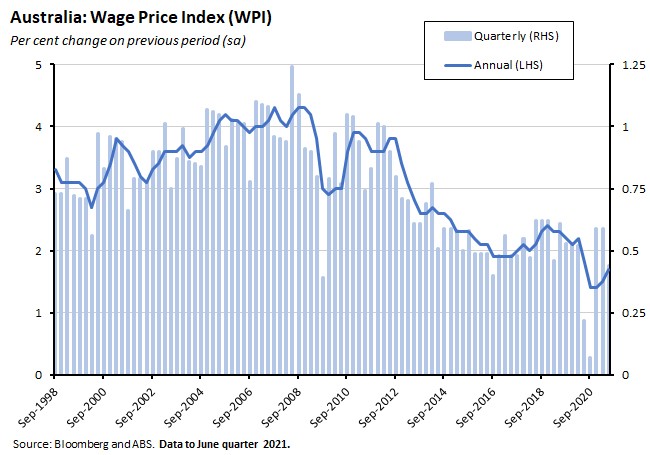

Rather than signalling a tightening of labour market conditions, however, the ABS said that last month’s drop in the unemployment rate should be seen as ‘another indication of the extent of reduced capacity for people to be active in the labour market’ as July also brought a fall in the number of hours worked in the economy, an increase in the rate of underemployment, and a slide in the participation rate as workers left the labour force. In another key piece of labour market news, the Wage Price Index (WPI) for the June quarter showed that even before the Delta variant tightened its grip on Australia there was little sign of a lower unemployment rate prompting stronger wage growth. The annual rate of increase in the WPI did climb to 1.7 per cent in Q2:2021, but some of this simply reflected base effects from Q2:2020’s very weak outcome. Meanwhile, the quarterly growth rate slipped to just 0.4 per cent, one of the softest readings in the history of the series. The annual rate of increase in public sector wages is now at its lowest on record and the ABS said there was little sign of significant wage pressures across the private sector.

Also this week, the minutes from the RBA’s 3 August monetary policy meeting reported that while the central bank did consider the case for reversing course on its plan to start tapering asset purchases later this year, ultimately the Board judged that any positive impact would likely be too late and that anyway fiscal policy was better suited to the task. The minutes confirm that the discussion did allow for the possibility of a future rethink ‘in response to further bad news on the health front should that lead to a more significant setback for the economic recovery.’ And as noted last week, risks to the RBA’s baseline forecast do now look skewed to the downside.

This week’s collection of links includes the case for a review of the RBA, George Megalogenis on Australian politics after the pandemic, the Productivity Commission on supply chain vulnerability (again) and on the register of foreign-owned water entitlements, the ABS on overseas visitor arrivals and average weekly earnings, Australia-China relations (again), an assessment of the drivers of China’s growth prospects, some reading recommendations from the IMF, Greg Ip on the IPCC report, junk bonds and corporate credit risk, Matt Klein on US inflation and an Australian foreign policy perspective on recent developments in Afghanistan.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast .

Listen and subscribe: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

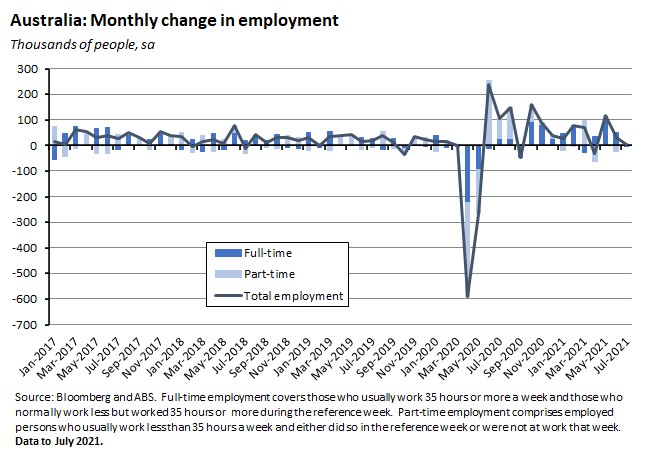

According to the ABS Labour Force report for July 2021, employment rose by 2,200 people (seasonally adjusted) last month. Full-time employment fell by 4,200 people but part-time employment increased by 6,400 people. The part-time share of employment was 31.5 per cent.

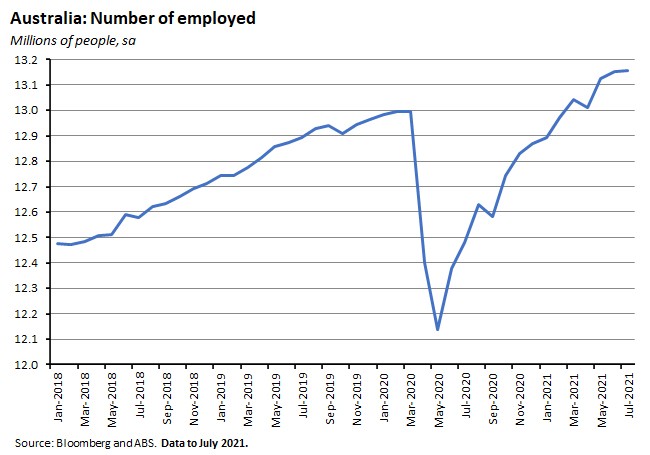

Total employment is now approaching 13.2 million people and is 161,600 (1.2 per cent) higher than it was in March 2020.

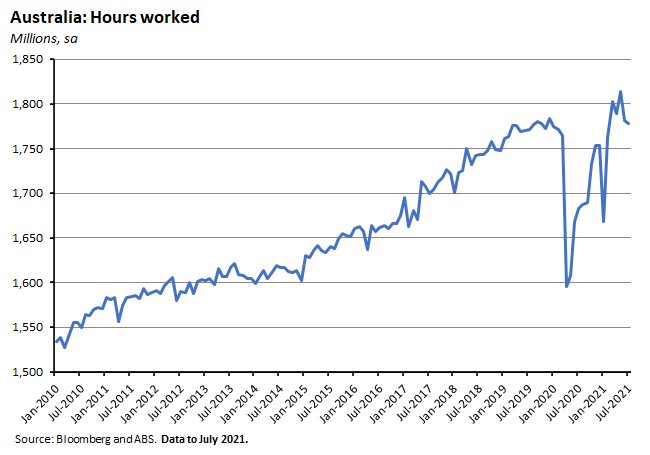

Monthly hours worked in all jobs fell by 3.1 million hours in July or by 0.2 per cent (seasonally adjusted). Hours worked are now 13.1 million higher (0.7 per cent) than in March 2020.

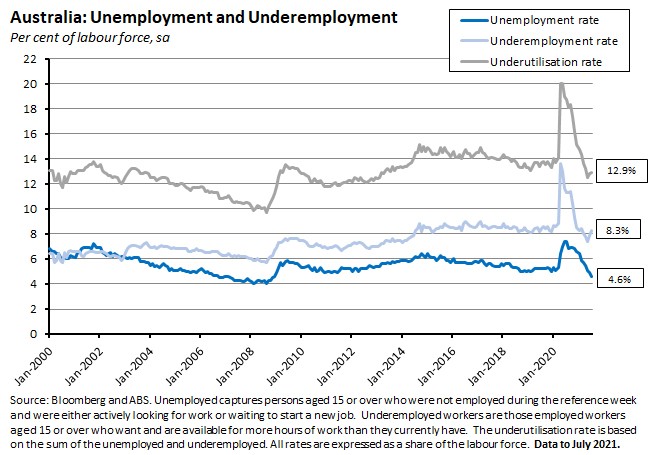

The unemployment rate fell 0.3 percentage points to 4.6 per cent in July while the underemployment rate moved in the opposite direction, rising by 0.4 percentage points to 8.3 per cent. The net result was that the underutilisation rate rose by 0.1 percentage point to 12.9 per cent.

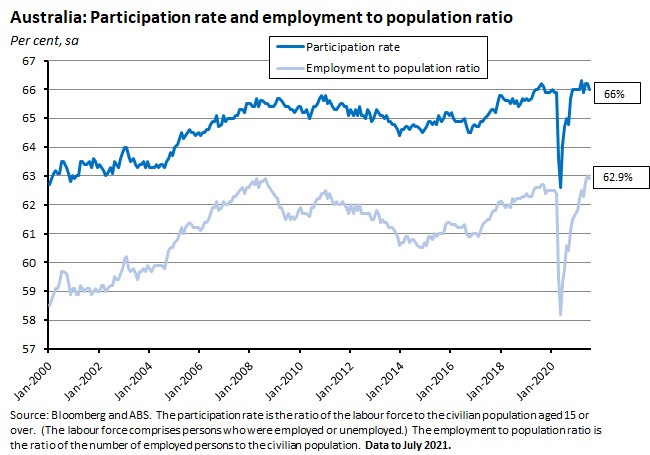

The participation rate fell 0.2 percentage points to 66 per cent in July, while the employment to population ratio fell by a little less than 0.1 percentage points to 62.9 per cent.

By state, the change in the number of employed people ranged from increases of 2.6 per cent in the Northern Territory and 1.2 per cent in South Australia to falls of 0.2 per cent in Queensland and 0.9 per cent in New South Wales. Changes in the unemployment rate ranged from falls of 0.7 percentage points in South Australia and 0.6 percentage points in New South Wales to an increase of 0.1 percentage points in Queensland, while the unemployment rate itself spans a low of 4.5 per cent in New South Wales, Victoria and Tasmania to a high of 5.2 per cent in Queensland.

Why it matters:

With the July labour market report expected to capture the impact of the Greater Sydney lockdown, the consensus forecast had been for a drop in employment of more than 43,000, a drop in the participation rate to 66 per cent, and a rise in the unemployment rate to five per cent. While the call on the participation rate turned out fine, the median forecast got the rest wrong: employment actually increased – if only marginally – over the month while the unemployment rate dropped to its lowest reading since the end of 2008. So, what did the forecasts miss, and why was the shift into lockdown associated with a fall and not a rise in the unemployment rate?

There are several things going on here.

First, start with the timing of the July labour force survey, which ran between 4 July and 17 July. That did capture the second and third weeks of the New South Wales lockdown (which had begun on 26 June) but it missed most of Victoria’s fifth lockdown which started on 16 July, the intensification of the New South Wales lockdown announced on 19 July, and all of the seven-day South Australian lockdown that started on 20 July. As well as only providing a partial picture of the overall impact of July’s lockdowns, another implication of this timing is that the national figures reflect the combined impact of offsetting developments in New South Wales and Victoria. For example, while the number of employed people fell 0.9 per cent over the month in the former, it rose by 0.5 per cent in the latter.

Second, under lockdowns the information content of the unemployment rate changes. In normal times, a fall in the unemployment rate would typically be a strong indicator of a tightening labour market. During lockdowns, it shifts toward (also) becoming an indicator of the difficulty of being able to actively look for work / be available for work while restrictions are in place. As a result, the reported number of unemployed people drops not only because people are finding jobs, but also because they are instead giving up looking for work and exiting the labour force altogether. As well as the 0.2 percentage point drop in the national participation rate noted above, for example, note that the participation rate slumped by a full percentage point in New South Wales in July.

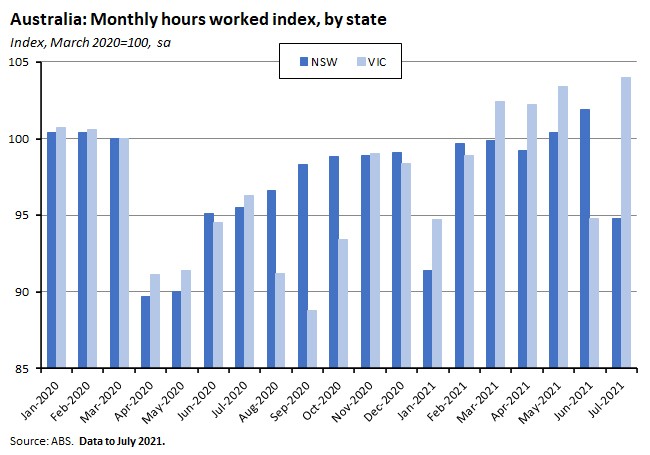

Third, this effect means that developments in hours worked become a more useful guide to labour market conditions during lockdowns. Here, the data show that while national hours worked fell 0.2 per cent between June and July, hours worked in New South Wales plummeted by seven per cent. At the same time, that was partially offset by a 9.7 per cent recovery in hours worked in Victoria.

The lockdown-driven decline in hours worked also shows up in the underemployment rate. Remember, that moved in the opposite direction to the unemployment rate in July, rising by 0.4 percentage points across Australia and jumping by 2.1 percentage points in New South Wales (but also falling by 1.9 percentage points in Victoria).

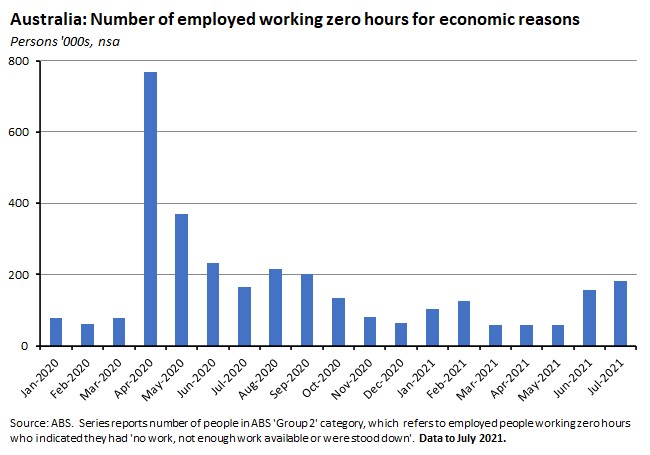

It’s also for this reason that in recent months we’ve been tracking developments in the number of people working zero hours for economic reasons (that is, due to no work, not enough work available, or being stood down). That number climbed to more than 181,000 in July, its highest level since September last year.

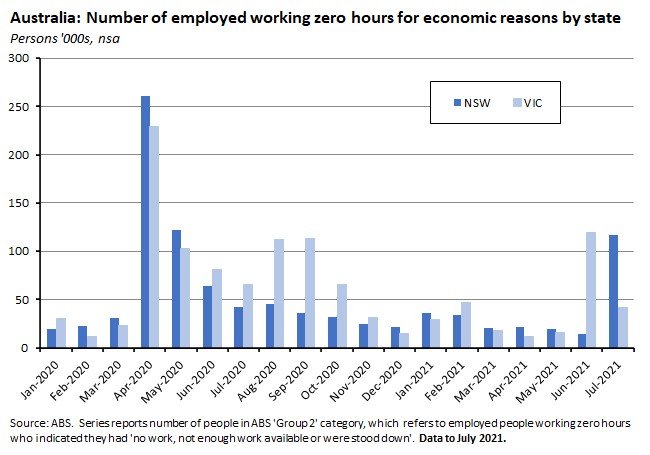

In New South Wales, the number of people in this category rocketed from less than 14,000 in June to more than 116,000 in July, the highest reading since April 2020. And once again, there was an offsetting move in Victoria over the same two months, where the number of people working zero hours for economic reasons fell from almost 120,000 to closer to 41,000.

Seen in this light, then, the headline unemployment results from July risk giving a misleading picture of the state of the labour market and a deeper dive into the numbers is required. Note that it’s also likely that the scale of the labour market impact from the Delta variant will become more apparent in the August and September labour force data.

What happened:

The ABS said that in the June quarter of this year the Wage Price Index (WPI) rose 0.4 per cent over the quarter and 1.7 per cent over the year (seasonally adjusted).

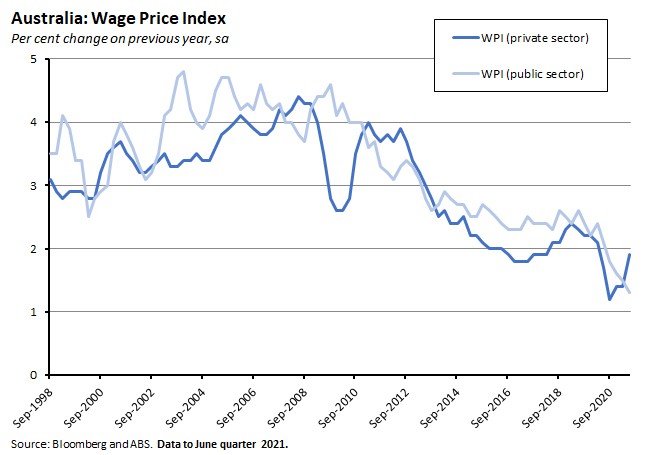

The WPI for the private sector rose 0.5 per cent over the quarter and 1.9 per cent over the year, while the public sector WPI rose 0.4 per cent quarter-on-quarter and 1.3 per cent year-on-year.

By state, the ACT recorded the largest quarterly rise in the June quarter, with an overall increase of 0.6 per cent driven by the private sector. The lowest quarterly increase (0.1 per cent) in the WPI came in the Northern Territory. In annual terms, Tasmania reported the fastest rise in the WPI (2.2 per cent) and South Australia and Western Australia the lowest (1.6 per cent).

By industry, quarterly growth was weakest in electricity, gas, water and waste services, in transport, postal and warehousing, in health care and social assistance, and in arts and recreational services (all up just 0.1 per cent). Quarterly growth was strongest in rental, hiring and real estate services (up 0.6 per cent). Year-on-year growth was weakest in arts and recreation services (0.9 per cent) and strongest in other services (up 2.6 per cent).

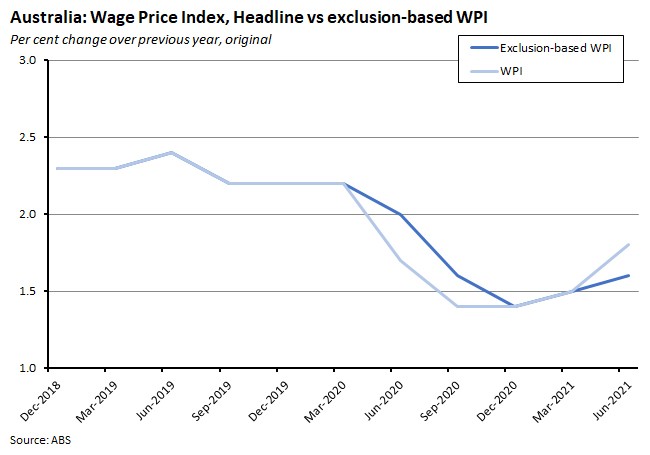

Starting with the December 2020 WPI release, the ABS has also provided an exclusion-based measure of the WPI. It is designed to respond to the impact of the significant number of short-term wage reductions that were recorded across senior executive and higher paid jobs in the June quarter of last year in response to the initial round of lockdowns. Most of those wage reductions were unwound in the following quarters, injecting a significant element of volatility into the WPI that the ABS thought ‘somewhat obscured the wage growth that was occurring in other parts of the labour market.’ To adjust for this, the exclusion-based measure stripped out the impact of these large swings in wages. The adjusted series puts the annual rate of increase in the WPI (on an original – not seasonally adjusted) basis at 1.6 per cent instead of the headline rate of 1.8 per cent.

Why it matters:

The consensus expectation for the June WPI had been for a 0.6 per cent quarterly rise and a 1.9 per cent annual gain, so the actual print (0.4 per cent and 1.7 per cent, respectively) was on the soft side. Indeed, excluding the pandemic-driven slumps of Q3 and Q4 last year, the Q2:2021 quarterly rise is one of the weakest in the history of the survey. Moreover, the annual rate was boosted by base effects, with the June quarter of last year capturing the first impacts of COVID-19 and lockdowns on the WPI. The Bureau’s exclusion-based measure of the WPI, which as noted above adjusts for some of the big swings in wages seen at the start of the pandemic, suggests a more modest profile for the pickup in year-on-year growth in the June quarter.

The ABS reported that ‘apart from a few isolated examples of skills shortages placing pressure on employers to meet expected market rates’ private sector wage growth in the June quarter ‘was generally subdued.’ Public sector wage growth was even softer, with the lowest rate of increase in the public sector WPI since the start of the series in 1997. The Bureau noted that in this case, wage growth had been ‘dampened by on-going negotiations around new enterprise agreements and the postponement of scheduled wage rises.’

The subdued wage result comes despite the unemployment rate having dropped to just 4.9 per cent in June. That suggests that the RBA’s caution – the central bank has repeatedly noted that it expects any recovery in wage growth to be slower than the recovery in employment – is on point. In a July 2021 speech on the labour market and monetary policy, for example, RBA Governor Lowe remarked that it was noteworthy that the positive surprises on jobs seen to date have not been matched with equivalent surprises on wages and prices in a pattern that was already familiar pre-pandemic. Granted, the continued improvement in the labour market pre-Delta had seen the RBA tweak its projections a little, although in its Economic Outlook and the forecasts presented in the August 2021 Statement on Monetary Policy, the RBA still said that it expected only a gradual lift in wage growth, with its liaison program telling it that wages growth in many firms is returning to around the pre-pandemic norm of two to 2.5 per cent this year, but not stronger than this. Those latest RBA projections have annual growth in the WPI picking up to 2.25 per cent by the December quarter of 2021 and then gradually increasing to around 2.75 per cent by 2023. But there’s a now significant headwind for that outlook since the onset of the Delta variant and subsequent lockdowns has clouded the labour market picture for at least the third quarter of this year and quite possibly longer.

What happened:

The RBA published the minutes of the 3 August monetary policy meeting of the Reserve Bank Board. The minutes note that ‘the recovery had established strong momentum prior to recent outbreaks of the Delta variant of COVID-19’ but add that ‘outbreaks of the Delta variant and accompanying lockdowns had introduced a high degree of uncertainty to the outlook for the second half of 2021.’ The discussion also reviews the forecasts presented in the August 2021 Statement on Monetary Policy, with the minutes reporting that based on ‘the assumption that further lengthy lockdowns would be limited, the economy was forecast to rebound from the current setback later in the year as restrictions are eased, consistent with the previously observed pattern in Australia and overseas.’ This optimism about the outlook beyond the current outbreak rests on:

- The underlying momentum in the economy and strengthened balance sheets pre-Delta;

- The substantial fiscal support provided to households and businesses in lockdown;

- Progress with the vaccination rollout; and

- Confidence in the economy’s ability to adapt.

The minutes also report that members discussed the balance of risks to the RBA’s baseline forecast, with its assumptions that while the Greater Sydney lockdown would extend through the September quarter, there would only be ‘some further brief and/or less severe restrictions assumed to occur in parts of Australia in the December quarter’ and that ‘the domestic vaccine rollout would accelerate in the months ahead, reducing the frequency and severity of lockdowns and allowing the international border to be reopened gradually from mid-2022.’

In terms of the backdrop for this month’s decision on monetary policy, the minutes record:

‘Experience to date had been that, once virus outbreaks were contained, the economy bounced back quickly. The vaccination program would assist with containment of the virus and longer-term economic recovery. Although uncertainty had increased, the central scenario was still that the Australian economy would grow strongly again next year.’

Many RBA-watchers had expected that Martin Place would use August’s meeting to reverse the decision the central bank had made at the July meeting to start to taper its asset purchase program from September this year. Here the minutes note:

‘Members…considered the case for delaying the tapering of bond purchases to $4 billion a week currently scheduled for September 2021. They noted that the outlook for the economy is for a resumption of strong growth in 2022. Members judged that any additional bond purchases would have their maximum effect at that time, with only a marginal effect at present, which is when the extra support might be required… fiscal policy is a more appropriate instrument than monetary policy for providing support in response to a temporary, localised reduction in incomes, [and] members welcomed the substantial fiscal measures that had been announced. Given these considerations, the Board reaffirmed the previously announced change in the rate of bond purchases. That said, the bond purchase program will continue to be reviewed in light of economic conditions and the health situation…The Board would be prepared to act in response to further bad news on the health front should that lead to a more significant setback for the economic recovery.’

And the discussion again confirmed that the RBA does not expect to adjust the cash rate before 2024.

Why it matters:

As we noted in last week’s review of the August Statement on Monetary Policy, the RBA’s baseline view is quite upbeat in terms of its assessment of the economy’s ability to manage the challenge of the Delta variant, its expectation that the Greater Sydney lockdown will be mostly done by the end of the current quarter, and the prospects for a relatively rapid return to growth. We also noted that risks to this outlook were skewed to the downside: a view since reinforced by another week of high case numbers. In this context, these minutes do confirm that if the RBA decides that the Delta setback is leading to a ‘more significant setback for the economic recovery,’ it will act. Whether recent developments are enough to meet the RBA’s definition of ‘significant’ and therefore trigger a reassessment of the planned taper remains to be seen, particularly since the central bank has been clear in signalling both that it thinks that a change in the asset purchase program will have little impact on the economy in the near term, and that anyway in its view fiscal policy dominates monetary policy under current circumstances.

What happened:

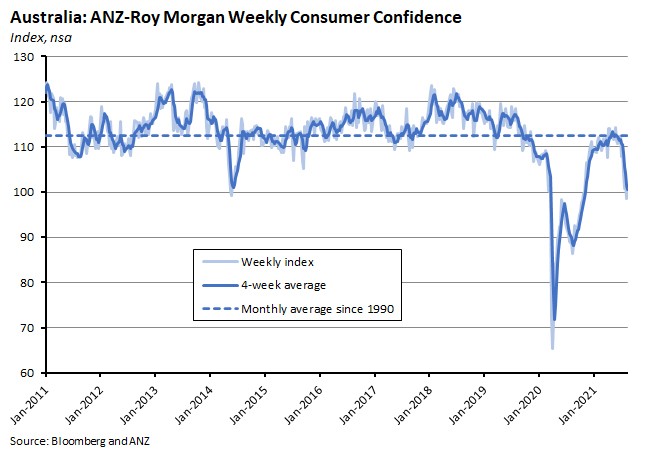

The ANZ Roy Morgan Consumer Confidence index rose 2.5 per cent over the week to 15 August, climbing to an index level of 101.1.

There were mixed readings across the subcomponents last week: ‘current financial conditions’ rose 2.9 per cent, ‘future financial conditions’ climbed 4.8 per cent and ‘time to buy a major household item’ gained five per cent while ‘current economic conditions’ eased by 0.5 per cent and ‘future economic conditions’ edged lower by 0.2 per cent.

Separately, the ‘weekly inflation expectations’ index rose to 4.5 per cent, hitting its highest level since May 2019.

Why it matters:

The weekly index of consumer confidence is now back above the neutral level of 100, partially unwinding the previous week’s 3.1 per cent decline. Last week’s recovery was in part driven by a 7.6 per cent gain in Queensland as the lockdown in the Southeast of the state ended. Strikingly, however, sentiment also climbed 7.1 per cent in Sydney despite the rising number of COVID-19 cases, suggesting that despite Delta, sentiment in New South Wales is still relatively robust.

What I’ve been reading . . .

The case for an external review of the RBA.

Saul Eslake in the AFR says this could be the recession we did not have to have.

Also from the AFR, perspectives from John Howard and Paul Keating.

I’m a little late to this one, but George Megalogenis’ Quarterly Essay on Australian politics after the pandemic is an interesting read. The argument is that while Australia has twice avoided the ‘supershocks’ of the 21st Century (the global financial crisis and the COVID-19 pandemic) thanks to a combination of policy ingenuity and social cohesion, in each case initial successes have later been undermined ‘by poor leadership once the immediate crisis passed’, and that Australia is ‘once again in danger of snatching mediocrity from the jaws of achievement.’ A selection of other observations that caught my eye include:

- The fiscal response to the pandemic was ‘radical and inspired policy-making on the run’.It saw Treasury build on what it had learned from the lessons of both the early 1990s recession and the response to the GFC: ‘the importance of getting cash into people’s hands and the danger of relying on infrastructure projects…You should deliver stimulus through existing payment channels. But forget about inventing new programs such as the pink batts scheme.’

- An important advantage that policymakers had this time vs the GCF was data: ‘The advances in technology since 2008 meant that the government no longer had to wait for the review of official statistics to see where the economy might be heading.Information could be pulled in real time, from the Australian Taxation Office, the banks and retailers…What those numbers showed proved to be invaluable in killing any intervention hesitancy within the government.’

- To a large extent, the policy response reflected the judgment that ‘in times of crisis, there are no ideological constraints.’ But Megalogenis argues that an important exception to this was the decision to exclude universities from JobKeeper.

- ‘The politics of lockdown weren’t local: they were colonial…We had slipped, instinctively, into our pre-federation identities, with Victoria and Queensland separating from Sydney’s rule, Western Australia happily closing itself off from the rest of the content, while South Australia and Tasmania reverted to insularity.’And later: the National Cabinet saw state premiers ‘claiming their greatest share of power in the federation since Whitlam commenced the long march of centralisation in the 1970s.’ Looking ahead, Megalogenis argues that the ‘Commonwealth needs to re-learn the art of running things, or…to fund the states to take even more matters off its hands.’

A new RBA Research Discussion Paper on Job loss, subjective expectations and household spending says that workers typically overpredict the probability of losing their job, particularly during downturns, while the unemployed typically underestimate how long they will be out of work. It also estimates that the typical household reduces total spending by nine per cent in the year of unemployment, and that consumption losses tend to extend to the period beyond unemployment.

The latest CBA survey of household spending intentions highlights the impact of recent lockdowns, with falls across most categories.

Two new items from the Productivity Commission (PC). First, the PC (still) isn’t particular worried about Australia’s vulnerable supply chains. Building on the analysis in its interim report, the PC finds that ‘few imports were used in the supply of essential goods and services, such as healthcare. Most vulnerable imports identified included non‑essentials such as Christmas decorations, luxury watches and sparkling wine. The main import vulnerabilities appear to be in certain chemicals, and in personal protective equipment.’ In addition, while the previous report had excluded food from the analysis of vulnerable imports, the final report finds that including food has only ‘minimal’ implications for the results. The final report also extends the analysis to exports. In the case of imports, the PC had defined ‘essential’ in terms of risks to ‘life and limb’ but for exports, the definition is widened to also include any goods and services that ‘provide a significant part of national income.’ Unsurprisingly, the report notes that on its own, iron ore accounted for nearly 95 per cent of the value of all vulnerable exports in 2019 but argues that with both Australia and China exposed to any disruption in the iron ore market, this ‘lessens the risk of geopolitically-inspired disruptions, as the two economies have a vested interest in the efficient functioning of the market.’

The second offering from the PC is a draft report on the register of foreign-owned water entitlements that proposes that the Register ‘plays a small, yet useful, role and apart from a few tweaks should continue for now, provided its costs remain low.’ The Register requires foreign persons to notify the ATO if they acquire a specified water asset, or if there are changes to their foreign status or water entitlement holdings. The collected data show that as of 30 June 2020, the foreign ownership rate of Australian water assets was around 11 per cent, with the largest source of investment in foreign-held water entitlements coming from (in descending order) Canada, China and the United States.

The ABS reported that average weekly ordinary time earnings for full-time adults (seasonally adjusted) rose 1.4 per cent over the year to May 2021, to $1,737. The Bureau comments that the rate of increase seen between November 2020 and May 2021 (a 1.5 per cent rise) was similar to pre-pandemic increases of 1.8 per cent in May 2019 and 1.4 per cent in November 2019. See here for a quick overview of the difference between the data on average weekly earnings and the WPI series discussed above.

Also from the ABS, overseas visitor arrivals were down by 98 per cent in 2020-21, with 6.6 million fewer arrivals than in the year before. Resident returns were down more than 97 per cent over the same period. The ABS also released details on visitor arrivals and resident returns for calendar year 2020. Arrivals in 2020 fell 80.7 per cent on 2019 numbers, dropping to 1.8 million or their lowest level since 1987, with 97 per cent of all arrivals occurring prior to the introduction of restrictions on international travel on 20 March 2020. Likewise, resident returns in 2020 were down 75 per cent on 2019, at 2.8 million – the lowest number since 1996 – with 92 per cent of returns occurring before 20 March 2020.

Lowy’s Sam Roggeveen reviews two recent Australian books on our relationship with China.

An Economist magazine briefing on China’s economic growth prospects. The proposition here is that with the working-age population having peaked and spending on infrastructure / capital arguably close to saturation point, productivity growth is ‘paramount’. But to the extent that past productivity growth came from loosening state control, recent measures to reassert the role of the Party could prove counterproductive. The briefing also points to Beijing’s current areas of focus: industrial modernisation (including modernising factories, upgrading technology, retaining a large manufacturing base and boosting self-reliance), new approaches to further urbanisation (based around securing the benefits of more agglomeration while managing the problems of congestion by ‘developing giant city clusters in which big hubs are linked to smaller satellites’) and catch-up reforms (efforts to raise a range of standards closer to those of advanced economies).

Greg Ip in the WSJ writes that last week’s IPCC report shows less cause for panic but more urgency to act. The IPCC has both ‘dialled back the probability of (without ruling out) more extreme changes in temperature’ while at the same time emphasising that ‘benign outcomes are also less likely, and uncertainty a less viable excuse for inaction.’

The IMF blog recommends some (Northern) Summer reads. FWIW, I’ve read and would happily recommend both the Harford and the Lonergan and Blyth books.

Also from the IMF, this working paper finds that mask mandates save lives, drawing on US data to estimate that mandates saved 87,000 lives through December 2020 and could have saved an additional 58,000. Related, Taleb and co-authors on why the effectiveness of masks in preventing respiratory infections may have been underestimated (pdf).

The Conversable Economist on rethinking the Great US housing bust of 2007-08. The conventional story is that excessively easy lending for home mortgages, including sub-prime loans, plus some tricky financial engineering, helped propel house prices to unrealistic levels and an eventual reckoning with reality. Yet from the perspective of continued trends in US house prices, it no longer looks like those high house prices in c.2006 were so unreasonable.

Matt Klein reckons that US inflation is normalizing.

Could junk bonds trigger the next financial crisis?

Related, could corporate credit losses turn out higher than expected?

An interesting roundup of some results in political finance from VoxEU. For example, one paper finds evidence of political polarization in corporate financial news by comparing coverage of the largest companies in the Wall Street Journal with coverage in the New York Times while another paper finds that executive teams in US firms are becoming increasingly politically homogenous.

Also from VoxEU, some findings on labour market reallocation in the wake of COVID-19 in the United States and the United Kingdom and the possibility of significant labour market mismatch.

Martin Sandbu in the FT argues that class conflict is back at the heart of economics as labour shortages prompt upward pressure on wages and channels a famous 1943 paper on the political aspects of full employment (pdf) by Michael Kalecki.

Peter Frankopan’s I’ve Been Thinking podcast looks at the Spanish Flu and pandemic impacts on elections. And an Australian foreign policy take on recent developments in Afghanistan from the Australia in the World podcast.

Latest news

Already a member?

Login to view this content