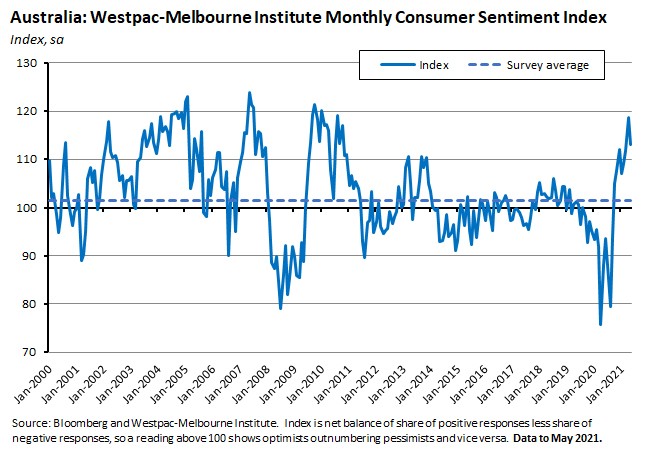

The unemployment rate fell for a sixth consecutive month in April dropping to 5.5 per cent in a result that suggests Australia’s labour market is taking the end of the JobKeeper program in its stride. Wage growth remains anaemic, however, with the Wage Price Index rising at an annual rate of just 1.5 per cent in the first quarter, and with public sector wage growth at record lows. The minutes from the 4 May RBA monetary policy meeting showed that while the central bank is more upbeat on growth and employment it still expects only modest increases in inflation. The Westpac-Melbourne Institute Index of Consumer Sentiment fell 4.8 per cent in May as households gave a lacklustre response to the 2021 Budget.

Catching up on some earlier releases: the NAB monthly business survey delivered a ‘stunning’ result for April with business conditions and business confidence both hitting record highs. The RBA’s May Statement on Monetary Policy set out the central bank’s new forecasts. Payroll data showed job numbers up 0.4 per cent in the fortnight to the week ending 24 April 2021 compared to a decrease of 1.6 per cent in the previous fortnight. Retail sales rose 1.3 per cent over the month in March in nominal terms while turnover was down 0.5 per cent over the first quarter in volume terms.

This week’s readings include the Treasury Secretary on recovery and reform in the Australian economy, a selection of post-budget analyses, the GFC as the ‘secret sauce’ behind Australia’s successful response to the pandemic, lots on inflation risk in the world economy, whether we are living in a science fiction novel, the IEA’s big new report on net zero by 2050, and the world’s supply chain nightmare.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia . . .

What happened:

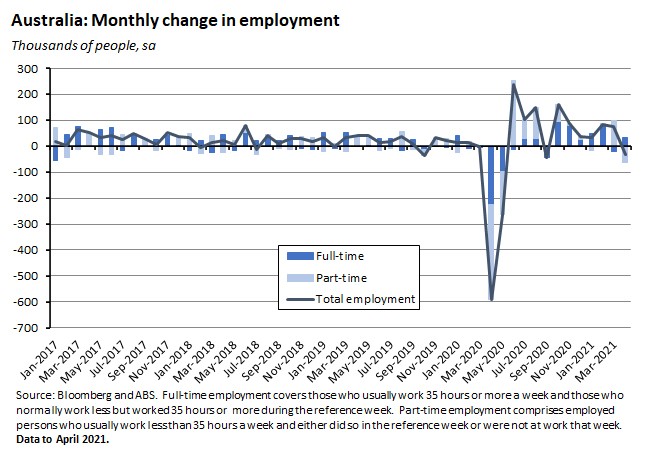

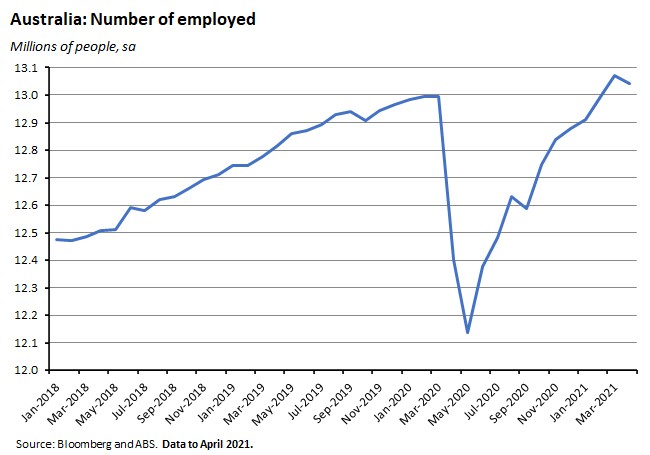

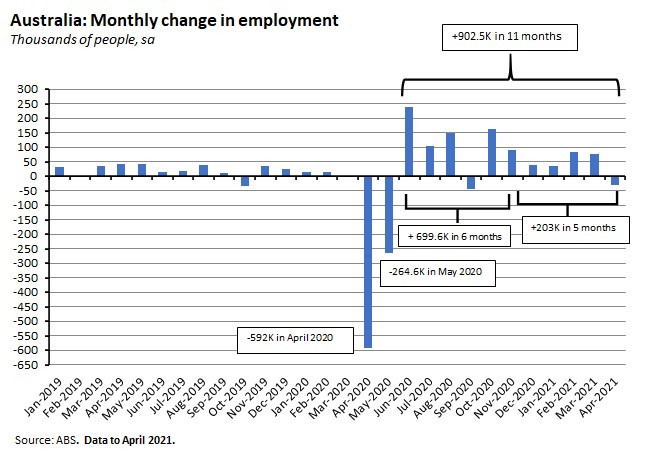

The April 2021 Labour Force results showed employment falling by 30,600 people (down 0.2 per cent) over the month with a gain in full-time employment of 33,800 more than offset by a fall in part-time employment of 64,400.

At 13.04 million, employment was still more than five per cent higher than in April 2020.

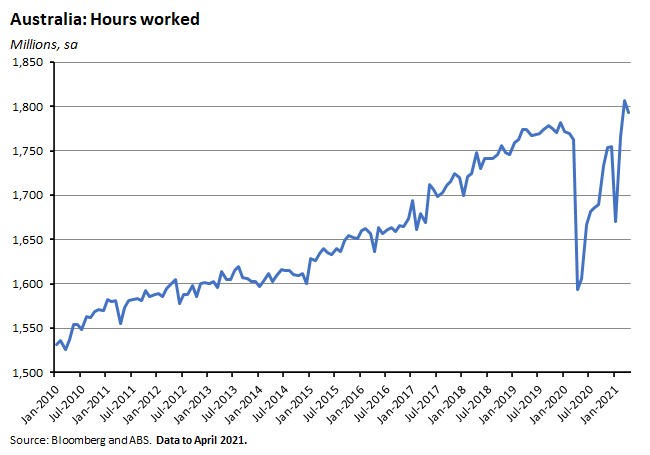

Hours worked in April 2021 fell 0.7 per cent (13 million hours) from March 2021 – a bigger percentage decline than the fall in employment, which the ABS said reflected a larger number of people than usual taking leave over the Easter holiday period.

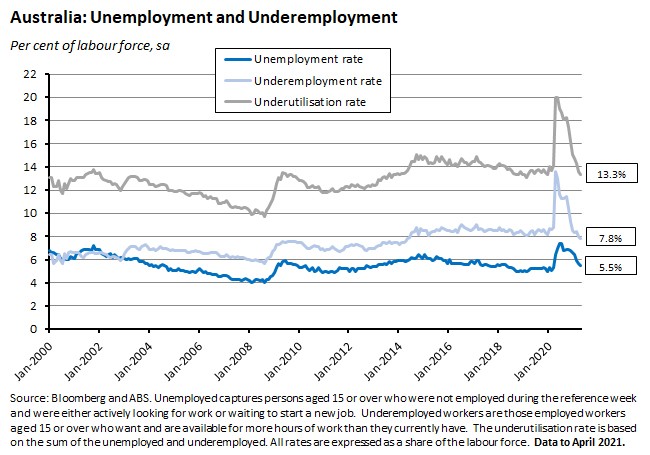

The unemployment rate fell 0.2 percentage points to 5.5 per cent (after the March rate was revised up from 5.6 per cent to 5.7 per cent) while the underemployment rate also fell 0.2 percentage points to 7.8 per cent, taking the underutilisation rate down to 13.3 per cent, a 0.4 percentage point decline from the March 2021 outcome.

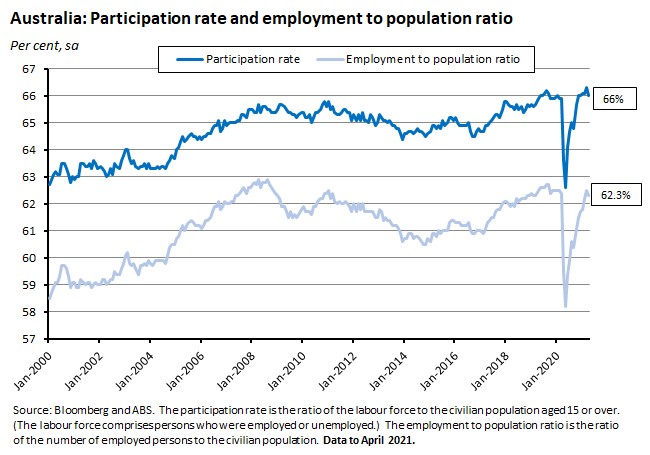

The combination of a fall in employment and a fall in the unemployment rate reflected a decline in the participation rate, which fell from 66.3 per cent in March to 66 per cent last month as more than 64,000 people left the labour force. The employment to population ratio also declined, falling by 0.2 percentage points to 62.3 per cent.

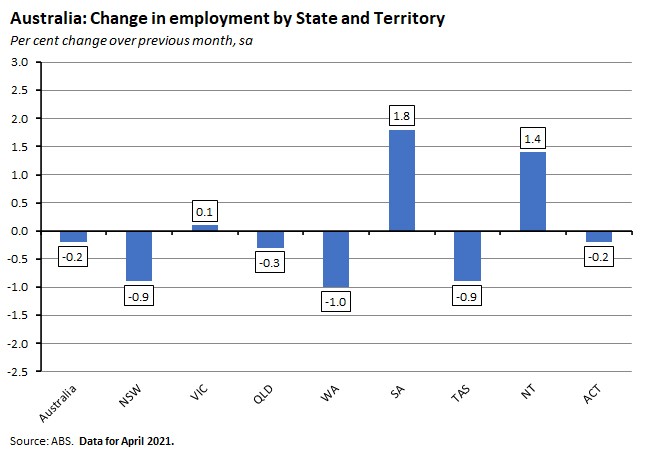

By state, the monthly change in employment ranged from a one per cent decline in Western Australia to a 1.8 per cent gain in South Australia.

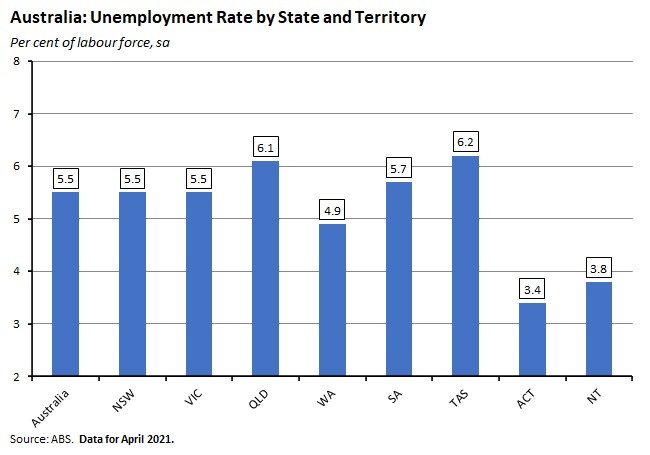

The unemployment rate in May ranged from a low of 3.4 per cent in the ACT to a high of 6.2 per cent in Tasmania, while monthly changes in the rate spanned a 1.8 percentage point drop in the Northern Territory and a 0.2 percentage point increase in Tasmania.

Why it matters:

As the first month following the end of the JobKeeper program, April’s labour force results were the focus of some interest, with the median forecast calling for employment to increase by 20,000 and the unemployment rate to be flat at 5.6 per cent. The actual result therefore managed to combine a weaker than forecast employment outcome with a lower than expected unemployment rate, with a drop in the participation rate reconciling those diverging outcomes.

Did that 30,600 drop in employment in April reflect JobKeeper’s demise? The ABS said that in its judgment, ‘the end of the JobKeeper wage subsidy did not have a discernible impact on employment between March and April.’ According to the Bureau, the data failed to display the ‘large changes in the indicators that would suggest a clear JobKeeper impact, such as an increase in people working reduced or zero hours for economic reasons or because they were leaving their job.’ And while it conceded that some of the fall in employment could be JobKeeper related, the Bureau also pointed to the ‘usual month-to-month variation in the labour market and some larger than usual seasonal changes.’

The fall in employment last month brought to an end a run of six successive months of job gains, and that, together with a slowdown in the pace of employment growth over recent months, suggests that the immediate post-crisis phase of a rapid snapback in employment may now be coming to an end. At the same time, however, that fall in the participation rate extended the run of consecutive monthly declines in the unemployment rate to six months, while the underemployment rate fell below eight per cent for the first time since June 2014. And in more good news, the youth unemployment rate fell to its lowest level since the Global Financial Crisis.

What happened:

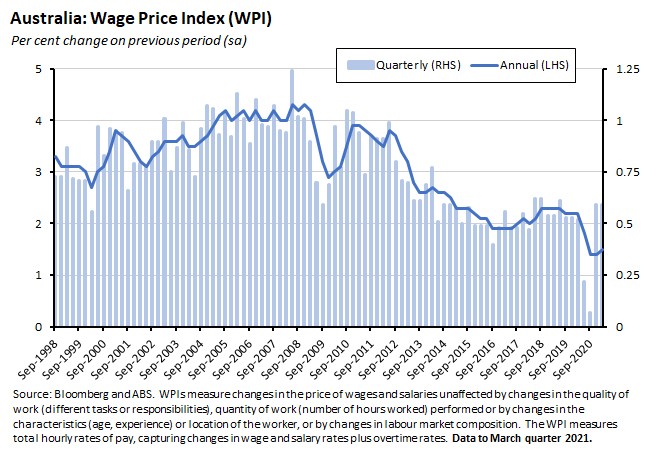

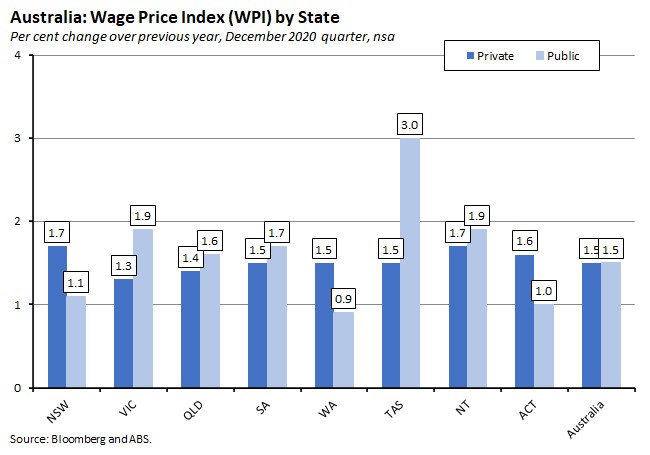

According to the ABS, the Wage Price Index (WPI) rose 0.6 per cent (seasonally adjusted) over the March quarter of this year to be up 1.5 per cent over the same quarter in 2020.

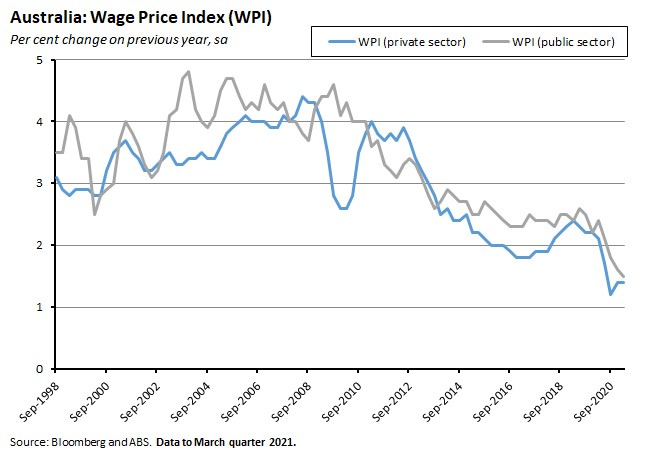

The WPI in the private sector rose 0.6 per cent quarter-on-quarter and 1.4 per cent year-on-year, while the corresponding rates of increase in the public sector were 0.4 per cent and 1.5 per cent, respectively.

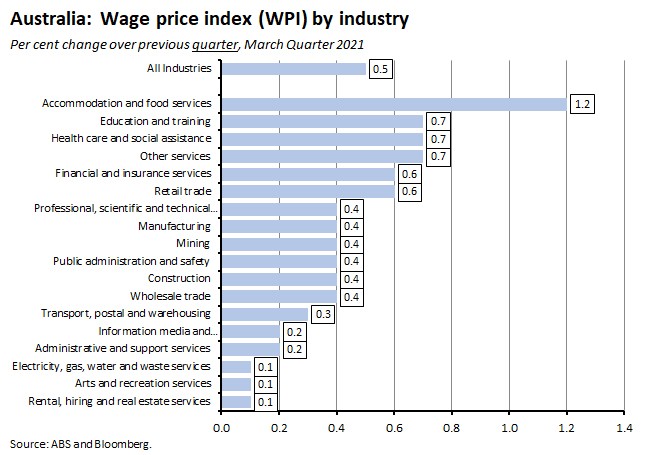

By industry, the largest quarterly gains in the WPI were in accommodation and food services (up 1.2 per cent), followed by education and training, health care and social assistance, and other services (all up 0.7 per cent).

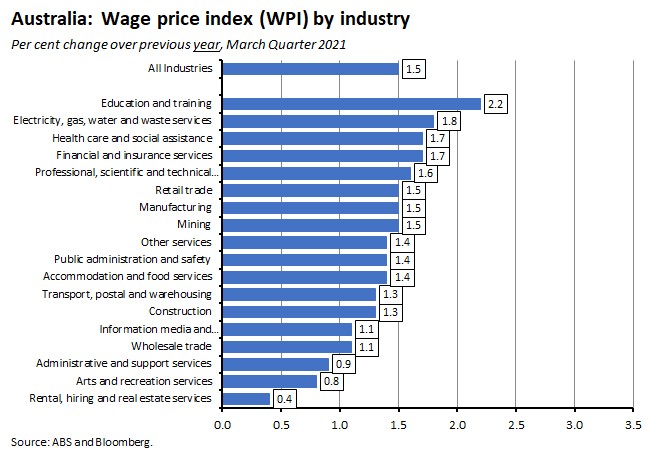

The annual rate of increase in the WPI in the first quarter was highest in education and training (up 2.2 per cent), followed by utilities (up 1.8 per cent), health care and social assistance and financial and insurance services (both up 1.7 per cent). The slowest pace of increase was in rental, hiring and real estate services, which saw a 0.4 per cent annual gain.

For all industries, the pace of annual wage growth in Q1:2021 was below the annual rate of increase recorded in Q1:2020.

By state, the annual rate of growth in the WPI ranged from a high of two per cent in Tasmania (driven by a three per cent year-on-year increase in the WPI in the public sector) to a low of 1.3 per cent in the Australian Capital Territory (driven by public sector wage growth of just one per cent due to wage deferrals and lower increases).

Again, all states and territories saw lower annual wage growth in the first quarter of this year compared to the same quarter in 2020.

The ABS said that wage growth in the March quarter ‘was mainly influenced by regular scheduled enterprise agreement increases, salary reviews for jobs paid by individual arrangements, and a proportion of modern awards receiving increases as a result of the Fair Work Commission (FWC) Annual Wage Review 2019-2020 decision…The FWC phased implementation schedule of award increases saw the final group of awards (accommodation and food services, retail trade, arts and recreation, aviation and tourism industries) receive scheduled increases in March quarter. The shift in timing of these award increases, from a regular September quarter, has dispersed the influence these jobs have had on quarterly growth across the September, December and March quarters.’

Why it matters:

Market expectations had been for a 0.5 per cent quarterly increase in the WPI and a 1.4 per cent annual gain, so the Q1 outcome was slightly (0.1 percentage points) stronger than the median forecast. This also marked the second consecutive quarter of 0.6 per cent quarterly wage gains, which the ABS said showed ‘a return to regular patterns of wage growth for the time of the year.’

Even so, overall growth in wages remains weak. At just 1.5 per cent, the annual rate of public sector wage increases is at a record low while the 1.4 per cent annual increase in private sector wages is only a little above the series record low of 1.2 per cent reached in the September quarter of last year. The RBA has said that it thinks wage growth of at least three per cent will be needed to meet its inflation target on a sustainable basis and thereby allow room for an increase in the cash rate. The March quarter saw wage growth at just half of that target rate.

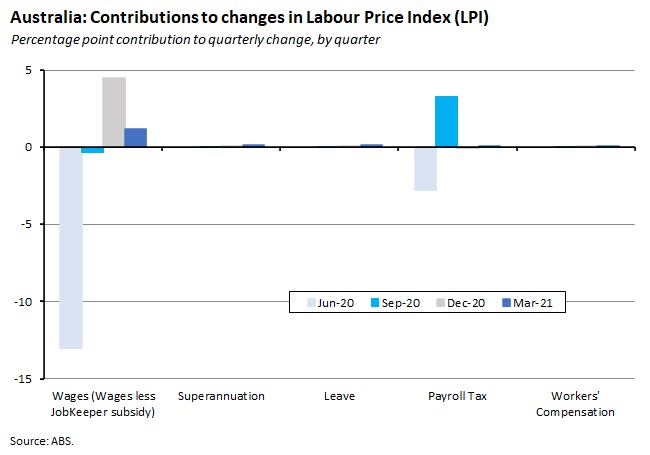

The Bureau also provided new estimates of the Labour Price Index (LPI) which measures the change in total labour costs including the impact of wage subsidies such as the JobKeeper program and state government measures such as payroll tax relief. The LPI rose by just 1.5 per cent in the March quarter, the slowest quarterly rise since the June quarter of 2020 (when the LPI fell by more than 12 per cent). The private sector saw a rise in labour costs of two per cent while the public sector increase was just 0.5 per cent, held down by a combination of continuing wage freezes and lower wage increases. While labour costs overall have now increased over the past three quarters, they are still 4.5 per cent below their pre-COVID levels.

What happened:

The RBA released the minutes of the 4 May 2021 Monetary Policy Meeting.

On the global economic backdrop, the discussion noted that the ‘global outlook had improved’ although the recovery ‘remained uneven.’ It also highlighted that a ‘key development’ in recent months had been ‘the rebound in commodity and producer prices’, driven by expansionary macro policies, strong global demand and a China-led recovery in industrial production. The latter was expected to ‘contribute to higher inflation globally in subsequent months.’

In terms of the domestic outlook, the minutes acknowledged that ‘the Australian economy was transitioning from recovery to expansion earlier and with more momentum than previously anticipated.’ An important source of uncertainty for the outlook was ‘the path for household consumption’ where the RBA’s baseline assumption was for a further decline in the saving ratio and a modest degree of consumption from accumulated savings. The outlook for dwelling investment was seen as strong, the outlook for business investment had improved, and the labour market recovery was expected to remain ‘firm.’

This environment meant that there was significant uncertainty around the prospects for inflation, with the minutes stating:

‘Despite the strong recovery in economic activity, the recent Consumer Price Index (CPI) confirmed that inflation pressures remain subdued in most parts of the Australian economy. The forecast for inflation had been revised upwards slightly, in line with the stronger outlook for activity, but inflation was still expected to increase only gradually…Members noted that the extent of spare capacity in the economy at the end of the forecast period was uncertain, which meant that the gradual increase in inflation could be slower or faster than envisaged in the baseline scenario. Wage and price inflation were at much lower levels than over the preceding decade, and, because of inertia in wage- and price-setting practices, it was possible that price pressures could be slow to build even if spare capacity were absorbed more quickly than expected. Alternatively, higher commodity prices, persistent supply chain bottlenecks and firms' reduced ability to address labour shortages through access to workers from abroad could mean that wages growth and inflation picked up earlier and more rapidly than expected as the economy continued to expand.’ [emphasis added]

The minutes repeated the commitment made following the May meeting, that the Board would use the upcoming July meeting to decide ‘whether to retain the April 2024 bond as the target bond for the 3-year yield target or to shift to the next maturity, the November 2024 bond’ and would also ‘consider future bond purchases following the completion in September of the second $100 billion of purchases under the government bond purchase program.’

They also confirmed the RBA’s mix of calendar-based and data-based forward guidance, stating that ‘The Board will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range. For this to occur, wages growth would need to be materially higher than it is currently…The Board viewed these conditions as unlikely until 2024 at the earliest.’

Why it matters:

The minutes didn’t add a great deal to the insight already provided by recent RBA communication including the 4 May decision itself, the 6 May speech on monetary policy during COVID by Deputy Governor Guy Debelle, and the 7 May publication of the Statement on Monetary Policy (see below). The main message continues to be that while the RBA is now much more upbeat on the pace of recovery in the real economy – transitioning from recovery to expansion – Martin Place does not think that this will trigger significant inflationary pressures in the near term:

‘A pick-up in inflation and wages growth was expected, but this was likely to be only gradual and modest despite the lift in the forecast for output growth…inflation would rise temporarily above three per cent in the June quarter before falling back below the target. Spare capacity in the economy and a strong focus on cost containment by businesses were both expected to contribute to continued subdued wage and price pressures…public sector wage policies were likely to restrain aggregate wage outcomes. It would take some time for spare capacity to be reduced and the labour market to be tight enough to generate wage increases consistent with achieving the inflation target. Moreover, it was likely that wages growth would need to be sustainably above three per cent, which was well above its current level.’

As noted above, the minutes do acknowledge that there is some significant uncertainty around the degree of price pressures in the economy. But for now, this uncertainty has not led the RBA to tweak its forward guidance for monetary policy.

The other message was that, as we discussed in an earlier note, July’s RBA meeting will be important in signalling any potential change in timing regarding a future adjustment to the RBA’s monetary policy settings.

What happened:

The Westpac-Melbourne Institute Index of Consumer Sentiment (pdf) fell 4.8 per cent in May to an index reading of 113.1.

All five components of the index fell over the month. ‘Family finances vs a year’ ago dropped 5.4 per cent, ‘family finances next 12 months’ fell 6.9 per cent, ‘economic condition next 12 months’ fell 3.5 per cent, ‘economic conditions next five years’ was down 6.7 per cent and ‘time to buy a major household item’ fell 1.5 per cent.

Other survey results had ‘time to buy a dwelling’ down 3.4 per cent and the house price expectations index edging lower by 0.1 per cent.

The Unemployment Expectations Index plummeted by 15.3 per cent in May, indicating that households expect unemployment to fall over the year ahead.

Why it matters:

The fall in consumer sentiment in May was quite steep at close to five per cent. But it’s important to keep in mind that this was a fall from the previous month’s very high reading which still left the index in absolute terms at its second highest level since April 2010. Note also, that despite the fall in the two economic subcomponents of the index, these remain well above their long-term averages.

The sharp drop in the Unemployment Expectations Index, which hit a ten-year low this month, indicates that sentiment around the health of the labour market has been able to take the end of the JobKeeper program in its stride – a result consistent with April’s labour market report.

Westpac suggested that the fall in May could reflect some disappointment with the budget, which took place in the middle of the survey: Pre-budget expectations had been very high, and the actual outcome may have failed to live up to them.

. . . and what happened over the previous week (and a bit).

What happened:

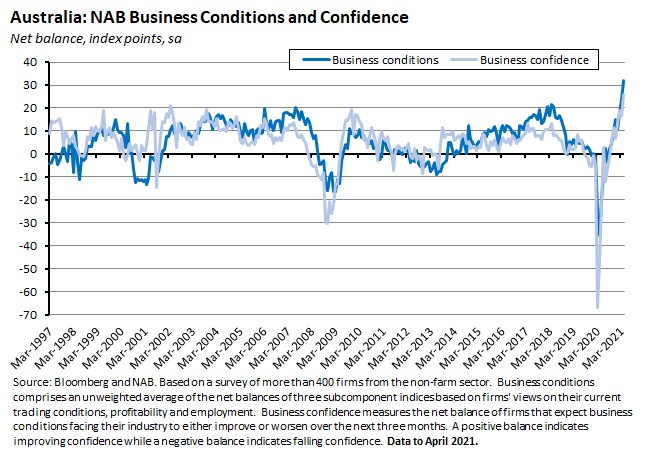

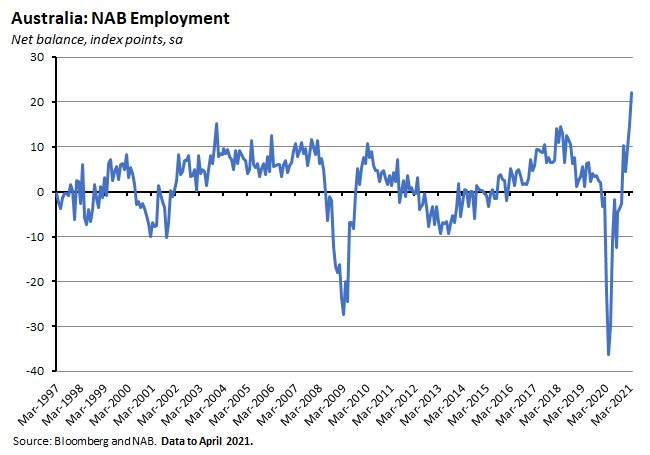

The April 2021 NAB Monthly Business Survey reported new record highs for business conditions and business confidence. Business conditions rose from +24 points in March to +32 points in April, while business confidence rose from +17 points to +26 points over the same period.

The rise in business conditions was driven by increases in all three subcomponents: Trading rose from +35 to +40 index points over the month, profitability rose from +25 to +33 and employment was up from +15 to +22.

Business confidence rose across all industries, led by an increase in retail.

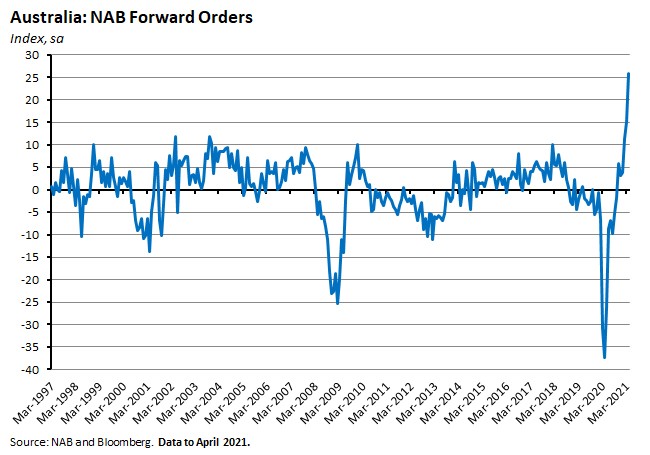

Leading indicators all showed strength in April. Forward orders rose to a new record high, up from +15 index points in March to +26 points last month.

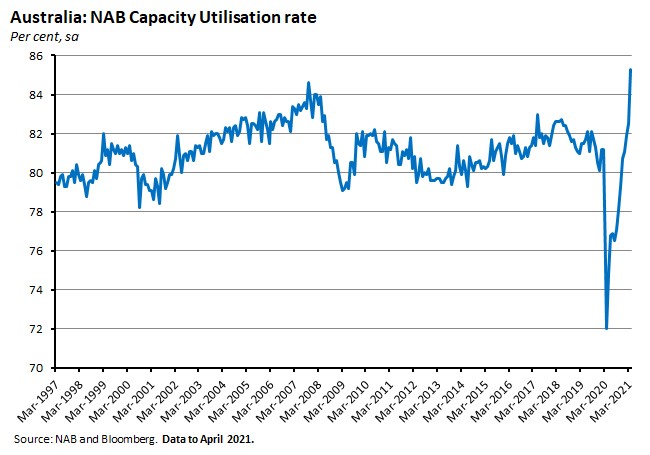

The rate of capacity utilisation climbed from 82.5 per cent in March to 85.3 per cent in April.

Finally, the survey showed a very slight slowdown in the rate of increase in labour and input costs, although final product prices edged up a little relative to March.

Why it matters:

The April survey results delivered another extremely strong reading – NAB described them as ‘simply stunning’. There were record highs across the board – for business conditions and all three subcomponents, for business confidence, for forward orders and for capacity utilisation. All of which should be good news for investment and hiring intentions. Also, worth keeping an eye on is that, once again, there were indicators of some significant cost pressures in the system.

What happened:

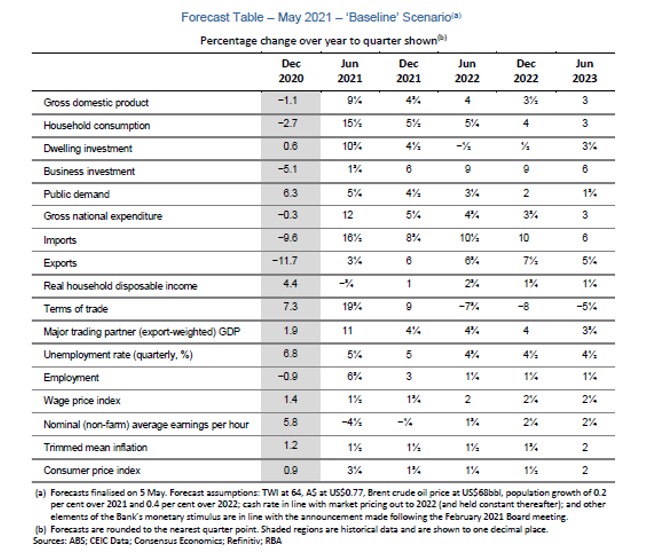

Back on Friday 7 May – just too late for the pre-Budget week Weekly Note – the RBA published its May 2021 Statement on Monetary Policy (SOMP), which provided additional detail on the RBA’s revised and updated outlook for the Australian economy.

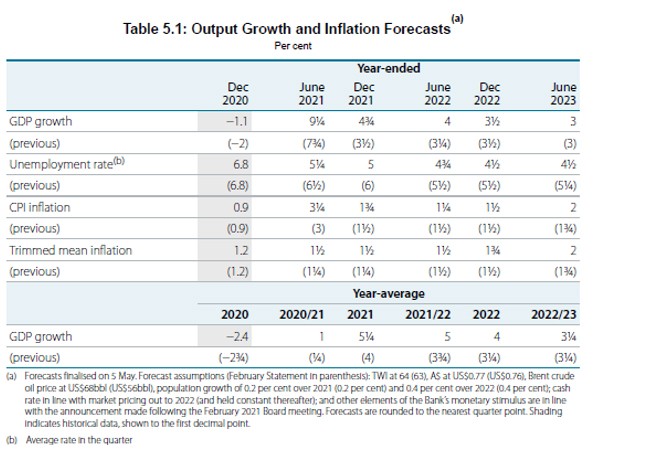

The key development underpinning these new forecasts is the RBA’s judgment that the ‘Australian economy is transitioning from recovery to expansion phase earlier and with more momentum than anticipated…In response to this stronger starting point for the forecasts and improved outlook further out, the baseline scenario for GDP and employment has been upgraded.’ Those upgrades see real GDP growth averaging around 5.25 per cent over this calendar year (up from February’s forecast of four per cent) and at four per cent over 2022 (up from 3.25 per cent). GDP is expected to have reached its pre-pandemic level by the March quarter of this year, and while the level of GDP is expected to remain ‘a little below that forecast pre-pandemic’ this is mostly due to lower population growth: in per capita terms, the RBA now thinks that GDP will be on a higher trajectory, ‘supported by higher per capita household income and a strong contribution from public demand.’

Stronger growth is accompanied by much better labour market results. The May SOMP forecasts now see the unemployment rate continuing to fall over this year, dropping to around five per cent by December 2021 (down from February’s forecast of six per cent), and then down again to 4.5 per cent by December 2022 (down from 5.5 per cent).

This stronger outlook for the real economy is accompanied by only a small upward adjustment to the RBA’s projections for wage growth and inflation. The annual rate of increase in the Wage Price Index (WPI) is now expected to have edged up to 1.75 per cent by the December quarter of this year, and then is projected to increase to two per cent by the June quarter of 2022 before reaching 2.25 per cent by the December quarter of next year. Headline CPI inflation is expected to finish this year at 1.75 per cent (up from the earlier forecast of 1.5 per cent) but to only hit two per cent by the June quarter of 2023 (up from 1.75 per cent). Underlying inflation is likewise only expected to hit two per cent by the June 2023 quarter.

The assumptions underpinning these projections are that the domestic vaccine rollout accelerates over the second half of this year, that the international border reopens gradually from early 2022, and that there are no further large outbreaks of COIVD-19, no accompanying extended hard lockdowns and any restrictions that are imposed in Australia are brief ones. These baseline projections also assume that household spending picks up, supported by positive income and wealth effects and a decline in the household savings ratio from around 12 per cent in Q4:2020 to eight per cent by the end of this year, before returning to its pre-pandemic average. The RBA sees upside and downside risks around this profile for consumption as critical determinants of the outlook and the SOMP also presents upside and downside scenarios based around stronger and weaker consumption stories.

Why it matters:

The new forecasts in May’s Statement have the economy in something close to a sweet spot. Real GDP growth is expected to be strong, employment growth to be healthy, and the unemployment rate is forecast to fall to below pre-pandemic levels by the end of this year, before dropping further. At the same time, this profile is not assumed to deliver any sustained increase in wage growth or inflationary pressures, which means that the RBA can stick with its existing calendar-based and data-based forward guidance, which says that no hike in the cash rate is likely until 2024 and until there has been a large enough increase in wage growth to deliver a rate of inflation that is sustainably within the two to three per cent target range.

In other words, as far as the future stance of monetary policy is concerned, the following is arguably the single most important judgment call in the May SOMP:

‘Despite the stronger outlook for output and the labour market, inflation and wages growth are expected to remain low, picking up only gradually…Some pick-up in wages growth is expected as the unemployment rate falls further. However, it is likely to be some years before wages growth is at a rate consistent with achieving the inflation target.’

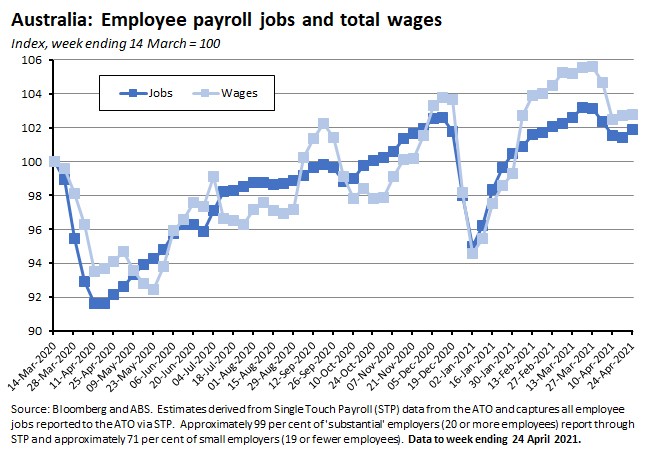

What happened:

The ABS said payroll job numbers in the fortnight up to the week ending 24 April 2021 increased by 0.4 per cent compared to a decrease of 1.6 per cent in the previous fortnight, while total wages paid increased by 0.3 per cent, compared to a decrease of three per cent in the previous fortnight.

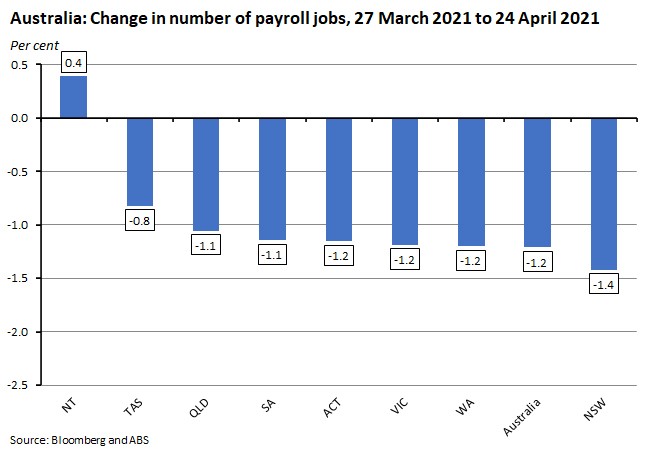

Over the month since 27 March, payroll job numbers across Australia are down 1.2 per cent, with the largest decline in New South Wales (down 1.4 per cent) and with the Northern Territory the only geography to report a rise (up 0.4 per cent).

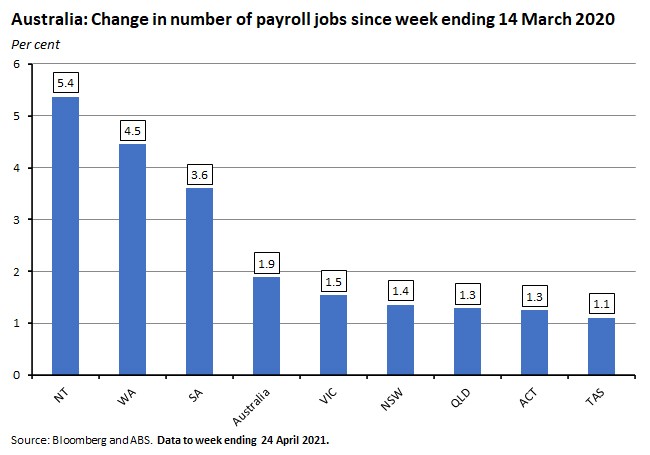

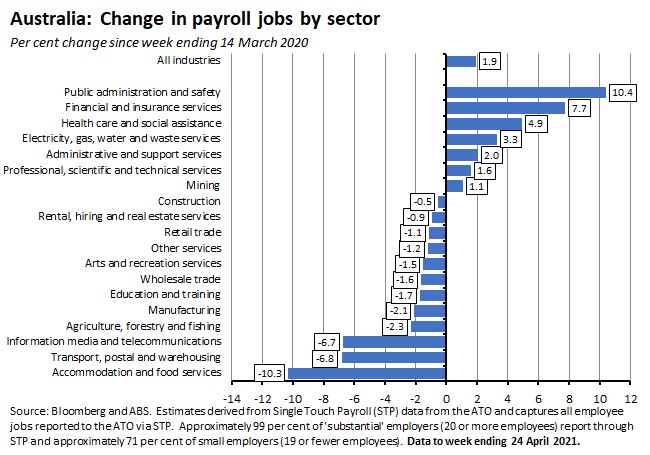

In the year since the week ending 11 April 2020, payroll job numbers Australia-wide are up 10.6 per cent. And in the period since Australia suffered its 100th case of COVID-19 in the week ending 14 March 2020, jobs numbers have increased by 1.9 per cent. By state, the largest gains over that period have been in the Northern Territory (up 5.4 per cent) and Western Australia (up 4.5 per cent) while the smallest have been in the ACT (up 1.3 per cent) and Tasmania (up 1.1 per cent).

By industry, over the period since the start of the pandemic, the largest job falls have been suffered by accommodation and food services (where payroll job numbers are still down 10.3 per cent), transport, postal and warehousing services (down 6.8 per cent) and information, media and telecommunications (down 6.7 per cent). The industries that have added the most jobs include public administration and safety (up 10.4 per cent), financial and insurance services (up 7.7 per cent) and health care and social assistance (up 4.9 per cent).

The ABS also noted that as of 24 April this year, the number of payroll jobs worked by women were 1.4 per cent above pre-pandemic levels, compared with 0.1 percent below for men.

Why it matters:

Payroll jobs are now 1.9 per cent higher than their pre-pandemic levels and exceed pre-COVID levels across all states and territories. By industry, the pattern is more mixed, with job numbers in accommodation and food services in particular still well down.

Unfortunately, the ABS note that the April payroll numbers continue to be significantly influenced by seasonal effects – including the April school holidays – which complicates any interpretation of the most recent set of numbers in the context of the end of JobKeeper. April’s labour force report provides a better guide.

What happened:

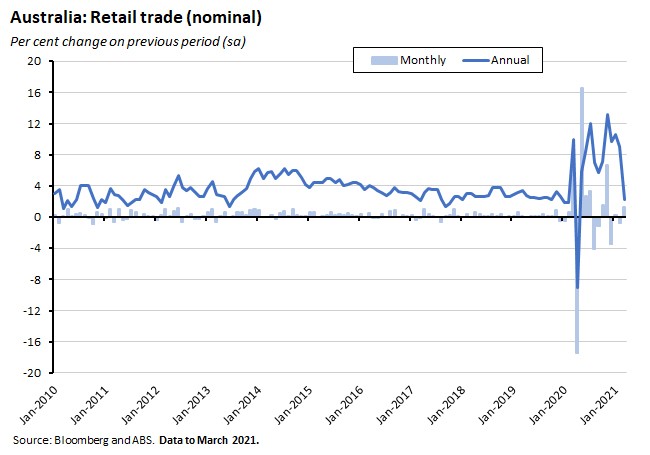

The final estimate for March retail turnover showed turnover up 1.3 per cent over the month (seasonally adjusted) and 2.2 per cent over the year.

Online sales made up 9.4 per cent of total retail sales in March 2021, up from a 7.1 per cent share in March 2020.

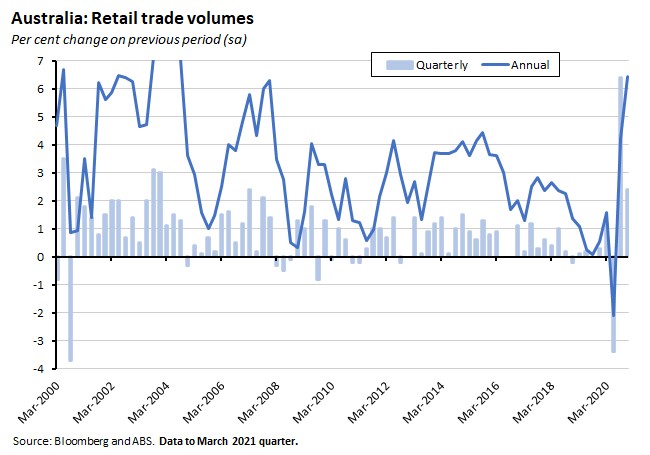

Over the March quarter as a whole, retail turnover in volume terms was down 0.5 per cent quarter-on-quarter but up 4.7 per cent relative to the same quarter last year.

Why it matters:

The final figure for the monthly rise in retail turnover over March (at 1.3 per cent) was only a little down on the 1.4 per cent preliminary estimate.

In terms of the quarterly result, the ABS noted that the decline in volumes was driven by households spending patterns gradually returning to those seen before the onset of the pandemic, with declines in spending on food retailing (down 2.7 per cent) and household goods (down 1.6 per cent) that were partially offset by a rise in spending on cafes, restaurants and takeaways (up 5.8 per cent).

What I’ve been reading . . .

Treasury Secretary Steven Kennedy’s Address to the Australian Business Economists on 18 May. Dr Kennedy’s speech covered the strength of Australia’s economic recovery and in particular our success ‘in achieving suppression of the virus at relatively low economic cost’; the greater-than-anticipated efficacy of fiscal policy (JobKeeper in particular) in supporting the labour market and driving down unemployment; and fiscal sustainability, where he painted a positive picture, drawing on budget projections that show ‘the Government is on track to stabilise and reduce debt even though it remains firmly in the first phase of the fiscal strategy.’ Relatively positive debt dynamics for Australia ‘reflect the fact that nominal economic growth is expected to exceed the Government’s cost of borrowing for at least the next decade.’ Interestingly, the speech also dug into some of the implications of the significant boost in funding to what my budget analysis called the ‘Care Economy’ and what Dr Kennedy calls ‘non-market services’ (education and training, public administration and safety, and health care and social assistance), which collectively account for about 21 per cent of economic activity, 29 per cent of employment and a significant share of government spending. Non-market services refers to the fact that they lack a ‘meaningful’ market price, in the sense that they are often provided free of charge to the user or are heavily subsidised, meaning that even if a price exists it is not closely related to the cost of providing the service. One implication of their growing importance is that a key challenge for the economy is lifting (and measuring!) productivity growth in these sectors, and here the speech proposed four principles: (1) Provide users with more choice and with the information necessary to inform that choice; (2) Deliver appropriate competition and contestability for services – for example, by delivering subsidies to consumers instead of providers; (3) Set government prices efficiently in a way that ‘reflects all costs and clears the market’; and (4) Reform accountability and governance.

A selection of additional post-budget analysis:

- Deloitte’s Budget analysis.

- Tim Colebatch argues that this budget was a case of kicking the can down the road.

- The AFR wonders what will follow the immediate post-budget boom.

- Academics from the University of Canberra are unconvinced by the decision to extend the Low and Middle Income Tax Offset (LMITO).

- An assessment from the Grattan Institute plus a post-budget score card on aged care.

Peter Martin says the Global Financial Crisis (GFC) was the ‘secret sauce’ Australia used to ward off the COVID recession.

The Productivity Commission’s Stephen King gave a speech providing an overview of the Commission’s recent Mental Health Inquiry Report, which estimated that the cost to Australia of poor mental health and suicide is around $200 billion to $220 billion each year, including direct annual economic costs of around $40 billion to $70 billion.

The latest (April 2021) ABS Household Impacts of COVID-19 Survey. This edition includes insights on social connections, use of digital services, attitudes to COVID-19 vaccines (68 per cent of respondents agreed or strongly agreed that they would get a vaccine when it becomes available and is recommended for them, a decrease from 73 per cent in February 2021), income and savings (25 per cent of respondents expect their household income to increase over the next 12 months, 64 per cent expect no change and 10 per cent expect a decline), and activities (for the April survey, over the past four weeks fewer people with jobs worked from home compared with February 2021 (36 per cent compared with 41 per cent) and more people used public transport (15 per cent vs 11 per cent)).

Jim O’Neil asks, will the global economic recovery last? The key near-term risks: (1) winning the vaccine war on COVID-19 including the new variants; and (2) an early tightening in global financial conditions if inflation fears turn out to be justified.

De Bolle and Obstfeld’s take on the impact of waiving intellectual property (IP) protection on global vaccine distribution: their view is this is helpful, but no panacea. For example, one important complication is that even if poorer countries can overcome IP restrictions on vaccine production, they may ‘lack the know-how, facilities and trained personnel to produce them.’ A further challenge is that – in the context of complex global supply chains – patent and IP waivers can’t resolve export restrictions or deliver easy integration into global production networks.

Two of the big-name economic journalists on inflation risks. First, Martin Wolf in the FT argues that there are reasons to worry about US inflation (also in the AFR), not so much because of the appearance of short-term price pressures but rather because (1) monetary and fiscal policy settings are now ‘wildly expansionary’ by historical standards; (2) there’s a large overhang of private savings waiting to be spent; (3) the Fed’s new monetary framework creates some uncertainty about how it will respond; and (4) a political shift in favour of cheap money and big fiscal deficits.

And second, Greg Ip in the WSJ reckons that a shortage of workers is set to boost wages and inflation in both the United States and China. The world’s largest two economies have both recently reported that their population growth over the past decade was the slowest in generations, creating significant demographic headwinds.

Related, Paul Krugman on the return of the monetary cockroaches. Krugman accepts there are some reasons to worry about price pressures but argues that a simple relationship between the money supply and price rises isn’t one of them.

Also related, some remarks by the IMF’s Financial Counsellor and Director of the Monetary and Capital Markets Department on the recent review of monetary policy frameworks (pdf) conducted by the US Fed, the ECB and other advanced country central banks. The reviews focus on how central banks should manage the challenges posed by persistently low equilibrium interest rates. One key conclusion: policymakers face trade-offs between supporting the economy today through ‘lower for longer’ type policies and creating greater financial stability risks in the future. Macroprudential policies offer one important way to help manage these trade-offs.

After rising to a record high in 2020, global uncertainty has fallen back to its long-run average. Declines in uncertainty around US-China trade tensions and Brexit have been key contributors to the fall, while pandemic-related uncertainty is also starting to drop.

Chinese robots on Mars, digital currencies, and ransomware cyberattacks: Tyler Cowen wonders if we’re living in a Science Fiction novel.

The International Energy Agency (IEA)’s big new report on Net Zero by 2050: A roadmap for the global energy sector. To reach net zero emissions by 2050, the report reckons that annual investment in clean energy worldwide would need to more than triple by 2030, to around US$4 trillion. It would also require ‘huge declines in the use of coal, oil and gas’, including steps such as halting the approval of new oil and gas field for development, no new coal mines or mine extensions, stopping sales of new internal combustion engine passenger cars by 2035 and phasing out all unabated coal and oil power plants by 2040. The IEA also recommends that government R&D spending is increased and reprioritised towards key areas such as electrification, hydrogen, bioenergy and carbon capture, utilisation and storage.

A CSIS report on China’s critical role in global maritime connectivity.

A Brookings working paper on what account data leaked from an Isle of Man bank can tell us about the characteristics of firms and individuals that use offshore financial centres (tax havens). Clients tend to be rich people from rich countries (surprise!), a significant share of offshore deposits are controlled by clients connected to politically influential people such as current and former politicians, their family and friends – many of them from countries that score poorly on measures of corruption risks (surprise again!), and the legal structures used in these arrangements undermine standard measures of offshore wealth.

Why Civilisation is older than we thought (via Marginal Revolution).

From the latest issue of the Milken Review: The Money Plot. An excerpt from Frederick Kaufman’s book that provides a quirky, sideways look at the rise, fall and rise of the US dollar.

Bloomberg’s Odd Lots podcast on the world’s deepening supply chain nightmare. See also this Bloomberg piece on how the world economy is suddenly running low on everything.

Latest news

Already a member?

Login to view this content