This week’s RBA minutes show that earlier this month the central bank’s board remained confident that Australia was not headed for the kind of inflationary outbreak that would require an earlier-than-expected tightening of monetary policy. The report of the board discussions indicates that despite an anticipated rise in labour market demand, members saw little evidence of any sharp acceleration in wage growth ahead. Instead, they judged that ‘wage and price pressures remain subdued.’ All of which is consistent with the central bank’s forward guidance that the conditions for an increase in the cash rate ‘will not be met before 2024.’

Increasingly, however, financial market participants disagree. With rising signs of international inflationary pressures, market pricing this week implies a significant chance that the RBA will have to bring forward the timing of its first policy rate hike to as early as next year. Next week’s CPI release should provide some new evidence as to which view is correct.

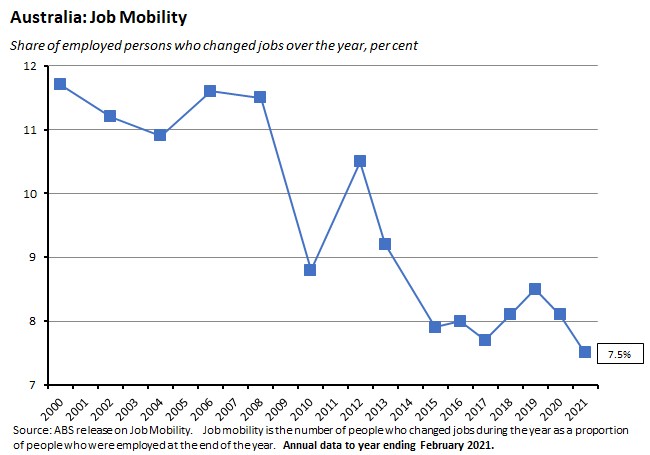

Labour market data released this week provided some useful insight on the extent to which the current fascination with the ‘Great Resignation’ applies to Australia. In fact, the latest ABS data on job duration provide little evidence of any big jump in the appetite to change jobs on the part of Australian employees, a finding that is consistent with earlier data showing that labour market mobility fell to record lows earlier this year. Of course, things could well change as the economy re-opens. But the numbers show that, for now at least, the Great Resignation here just hasn’t been that great.

Finally, this week brought the third quarter GDP reading for China. The growth rate of 4.9 per cent over the year was on the soft side and came in below market expectations. China’s economy is battling a range of headwinds including a faltering property sector and an ongoing energy crisis. That is likely to have implications for Australian exports and for our terms of trade.

We discuss the RBA, China and the labour market in more detail in this week’s Dismal Science podcast.

This week’s readings include Deloitte on remaking the Australian economy, getting to net zero emissions, living with COVID-19, how the pandemic left the world with a mountain of debt, labour scarcity in the United States, the OECD’s latest long-term scenarios, and McKinsey on the revolution in food delivery.

Listen and subscribe to Dismal Science podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

The Minutes of the 5 October 2021 Monetary Policy Meeting of the RBA Board were published. Key points included:

- Increased optimism regarding the outlook for the Australian economy, based on the rapid vaccine rollout: ‘members noted that the rapid increase in vaccinations, particularly in states with outbreaks of the Delta variant of COVID-19, would see restrictions on activity eased sooner than previously expected. The international border was also set to begin reopening earlier than had been assumed.’

- Reopening in New South Wales and Victoria ‘was expected to lead to a solid recovery in household consumption in the December 2021 and March 2022 quarters…supported by high accumulated savings, strong increases in household wealth and a rebound in employment…[although] households' consumption of discretionary services was not expected to return to pre-pandemic levels until 2022.’

- While the unemployment rate had been little changed, broader measures of labour market underutilisation had increased sharply since the middle of the year.This near-term deterioration had been offset by the fact that forward-looking indicators of labour demand such as the level of job ads had remained strong, however.And the RBA’s liaison program had also continued to report that firms had been reluctant to lay off staff.As a result, the RBA’s ‘central forecast scenario envisaged the level of employment, unemployment and participation to have broadly recovered to pre-Delta levels by around the end of the year, although there was considerable uncertainty around this projection.’

- Importantly, and despite this anticipated recovery in labour market demand, ‘there were few indications from disaggregated wages data or from the Bank's liaison program to suggest that aggregate wages growth was likely to accelerate sharply in the period ahead.’Likewise, board members noted that ‘underlying inflation pressures in Australia were more moderate than in other advanced economies. This reflected a range of factors, including the relatively slow rate of wages growth in Australia.’

- On housing market developments in general and the rise in household indebtedness in particular, the minutes report that members thought ‘these risks would be best addressed with a serviceability-based macroprudential measure, which would ensure that borrowers would have more income left over after home loan repayments and other expenses.’ More generally, their view was that the ‘Australian financial system remained resilient. The loan-to-valuation ratios on most outstanding home loans meant that banks would be well protected against even large housing downturns.’

- On the international economy, members discussed recent developments in labour markets, the impact of supply chain disruptions, rising energy prices and strong demand on inflationary pressures, and the slowdown in Chinese economic growth.

Why it matters:

There were two main themes from the minutes of this month’s RBA monetary policy meeting.

The first was that while the success of the vaccine rollout has given the RBA more confidence in its forecast that the economy will bounce back from the current bout of Delta-led dislocation, this has not changed the central bank’s view on inflation. Thus the minutes note that ‘the economy [is] anticipated to bounce back as vaccination rates continue to rise and restrictions are eased’ but then go on to state that ‘wage and price pressures in Australia remain subdued…while disruptions to global supply chains were affecting the prices of some goods, the effect of this on the overall rate of inflation in Australia was limited. Wages growth and underlying inflation were expected to pick up only gradually as the economy recovers.’

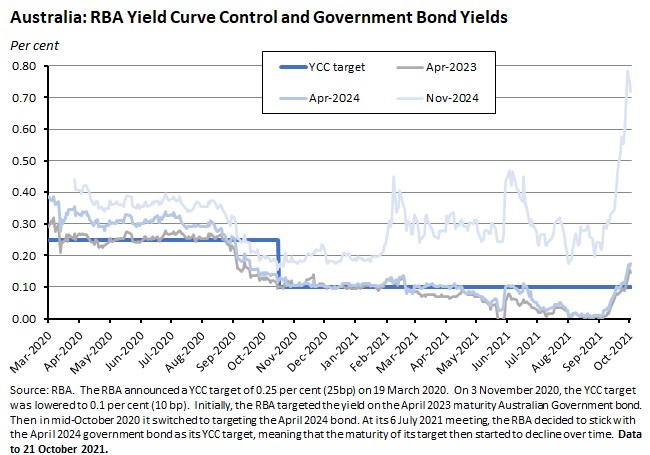

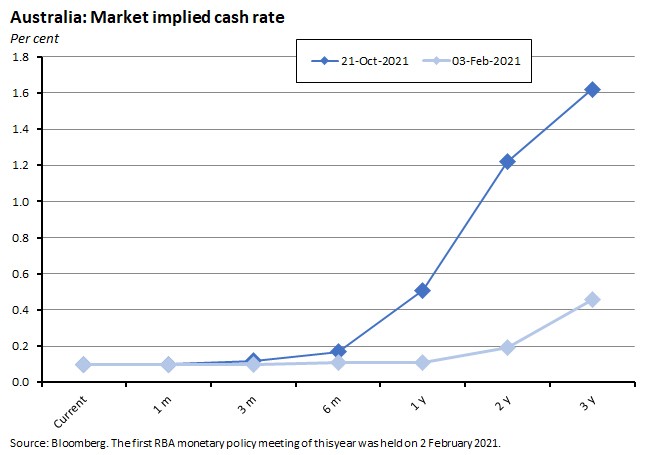

Financial markets, however, are currently much less convinced than the RBA that the inflation rate will remain subdued for a prolonged period, and that this will allow the central bank to stick with its plan to keep the cash unchanged until 2024. This week has seen the market testing the RBA’s commitment to its yield curve control (YCC) target of 0.1 per cent on the April 2024 Australian government bond (remember, the July 2021 meeting saw the RBA decide to stick with the April 2024 bond as its YCC target).

Moreover, current market pricing suggests that expectations for the cash rate have shifted quite significantly, as markets look outward to inflation developments in the rest of the world economy and fret that rising prices risk surprising on the upside. Contrary to the RBA’s view that no change in the cash rate is likely until 2024, markets are now pricing in rate hikes as early as next year.

Next Wednesday’s CPI release will provide a key data point for this debate: last quarter’s release showed headline CPI running at a high 3.8 per cent annual rate but underlying inflation (as measured by the trimmed mean) at a much more subdued 1.6 per cent.

The second theme highlighted by the minutes relates to financial stability and the housing market. Readers will recall that it was the day after the 5 October meeting that APRA introduced macro-prudential measures targeting the housing market, instructing banks to increase the minimum interest rate buffer they use when assessing the serviceability of clients’ home loan applications. The minutes provide some additional background on the RBA’s thinking in this area, reporting that given ‘the environment of rising housing prices and low interest rates, members continued to emphasise the importance of maintaining lending standards and agreed that loan serviceability buffers were appropriate.’ They also repeat the RBA’s judgement that macro-prudential measures, not monetary policy tightening, were the appropriate response: ‘Members also agreed that, while less accommodative monetary policy would, all else equal, see lower housing prices and credit growth, it would result in fewer jobs and lower wages growth, which would in turn create further distance from the goals of monetary policy – namely, full employment and inflation sustainably within the target range.’

What happened:

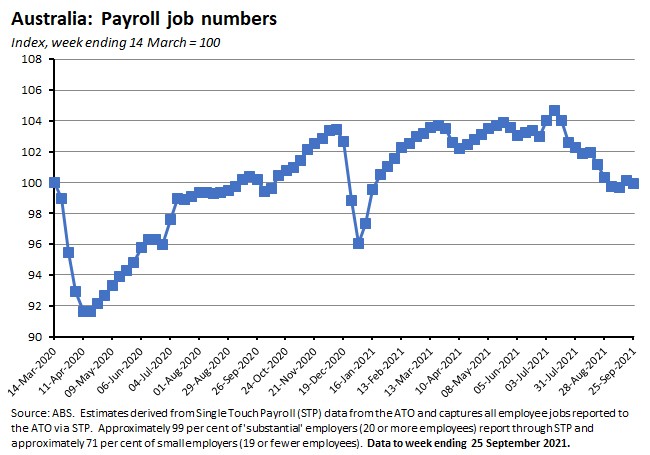

According to the latest interim release from the ABS, the number of payroll jobs rose 0.2 per cent over the fortnight to 25 September 2021 after having fallen 0.6 per cent over the previous fortnight.

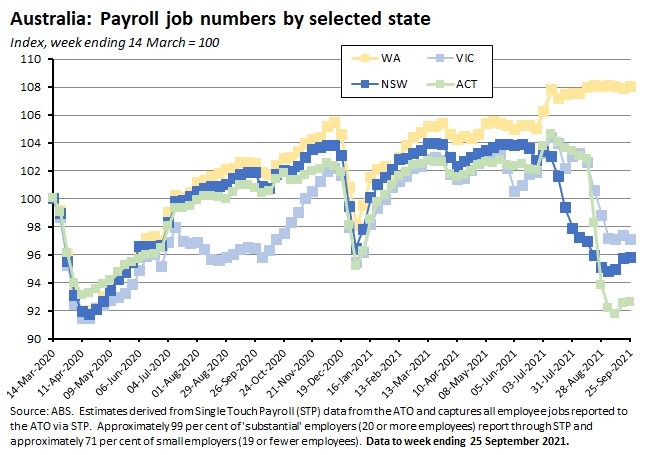

By state and territory, jobs over past fortnight rose everywhere except Queensland (down 0.3 per cent in the two weeks to 25 September) and Tasmania (down 0.9 per cent) with jobs up by 0.9 per cent in New South Wales and the ACT. Over the past month as a whole, job losses have been largest in Victoria (down 1.8 per cent), the ACT (down 1.3 per cent) and Tasmania (down 1.1 per cent). Jobs in New South Wales were up 0.7 per cent over the same period.

Why it matters:

This interim release of payroll data is light on data relative to the broader take on job developments that comes with its more detailed counterpart. Still, the new numbers do suggest that – after a series of declines – there has now been some stabilisation in the labour market. In particular, job numbers have stopped falling and started climbing in both New South Wales and in the ACT, while in Victoria numbers stabilised over the most recent fortnight of data. Granted, in all three states numbers are still well below pre-lockdown levels. But with state re-openings ahead, there is clearly scope for the upturn in numbers to be sustained.

What happened:

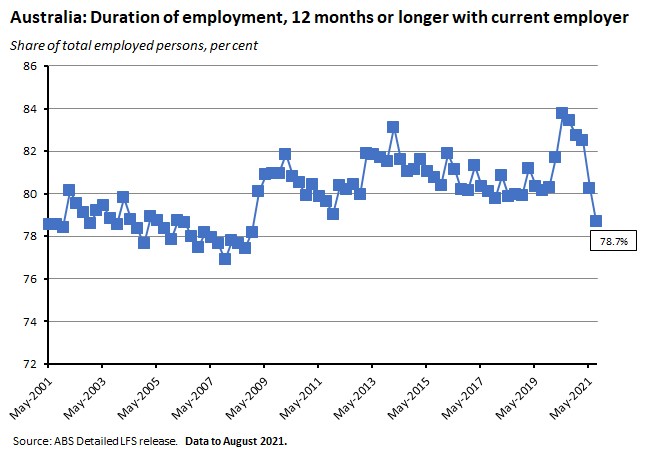

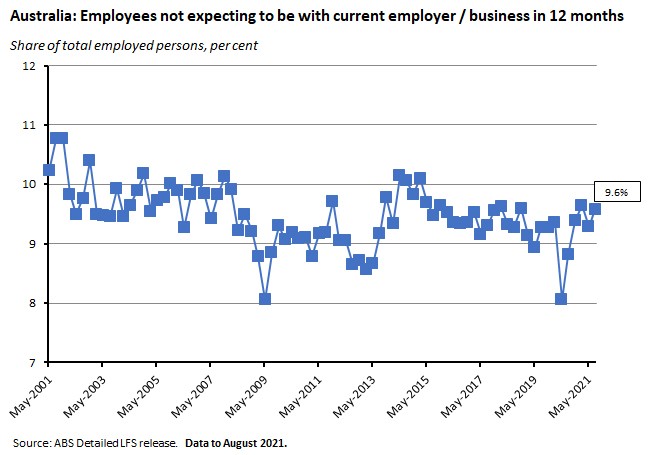

The ABS released detailed monthly and quarterly labour force data which includes findings on job search and job duration.

The new figures show that the majority of Australian workers have been with the their current employer 12 months or more, and that although this share has declined during the pandemic (as would be expected given the fall in employment created by lockdowns), it still applied to more than 78 per cent of employed persons as of August this year.

The share of employees not expecting to still be with their current employer or business in 12 months edged up to 9.6 per cent in August this year from 9.3 per cent in May.

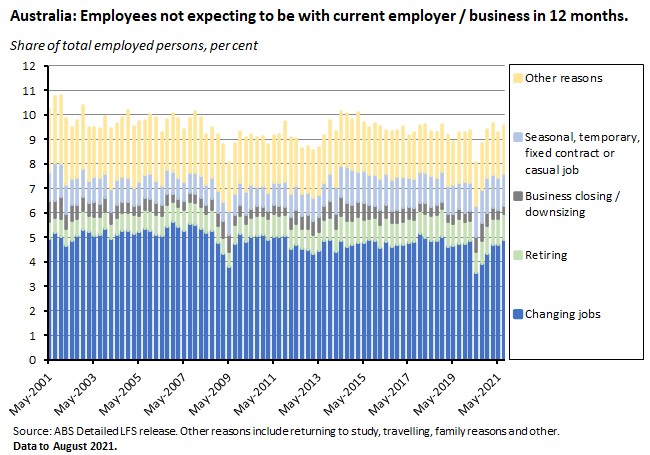

Of that 9.6 per cent of total employed persons, the single largest contribution was from those looking to change jobs or seek other forms of employment (4.9 percentage points), with retiring (1.1 percentage points), business closures and downsizing (0.3 percentage points), seasonal, temporary, fixed contract or casual jobs (1.3 percentage points) and other reasons (two percentage points) accounting for the remainder.

Why it matters:

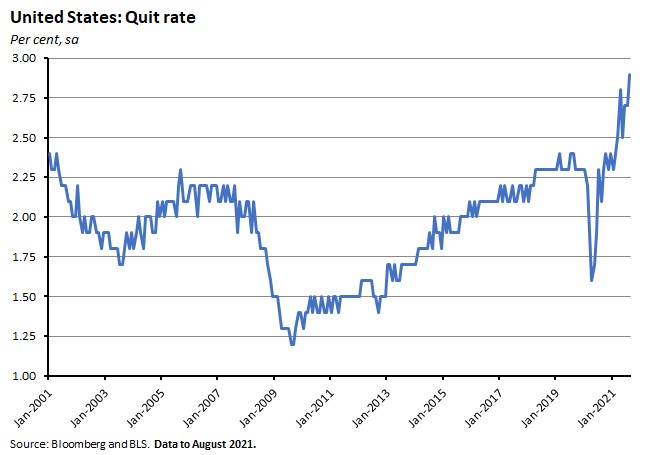

There has been a lot of talk about the ‘Great Resignation’ in recent weeks. The term originated in the United States, where there has been a sharp rise in the number of Americans leaving their jobs. (This also includes those retiring, with the ‘Great Retirement’ sometimes appearing as a co-star in the main story).

Not surprisingly, there has also been a fair bit of speculation that the Great Resignation will also apply to Australia. That may well turn out to be the case in the future. But for now, there’s little evidence in the data. As the latest numbers show, over the next 12 months the share of employees planning to leave their current employer / business looks little different to the kind of numbers we’ve seen over most of the current century (the series average is 9.5 per cent but this includes the sharp fall during the worst of the pandemic). Likewise, the share of those specifically looking to change jobs is relatively low (at 4.9 per cent) and in line with the series average.

Other measures tell a similar story: the ABS annual measure of job mobility has been trending down for some time now, and as of the start of this year was at a series low.

What happened:

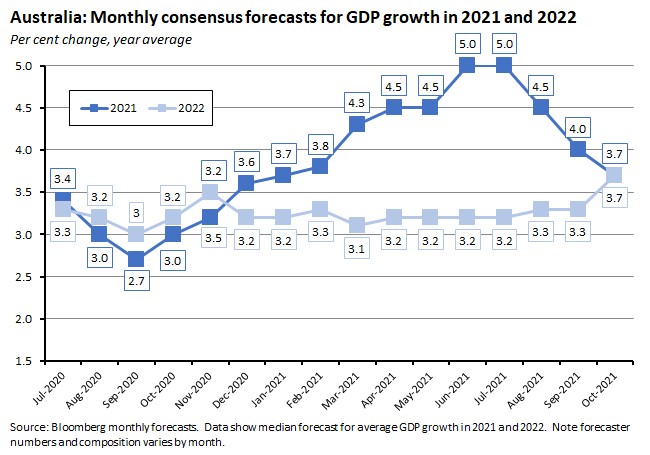

The Bloomberg October 2021 survey of economists shows that the median consensus for GDP growth this year has fallen to 3.7 per cent from four per cent in September’s survey. At the same time growth prospects for next year have been revised up to 3.7 per cent from 3.3 per cent as forecasters have reallocated their growth expectations by pushing predictions of stronger activity into next year. Average GDP growth is then expected to fall back to three per cent in 2023.

The consensus forecast for unemployment sees the unemployment rate falling from 5.2 per cent this year to 4.5 per cent in 2022 and 4.1 per cent in 2023. That’s a slightly flatter trajectory than the September forecasts, which had the rate moving from 5.3 per cent to 4.6 per cent to 4.1 per cent.

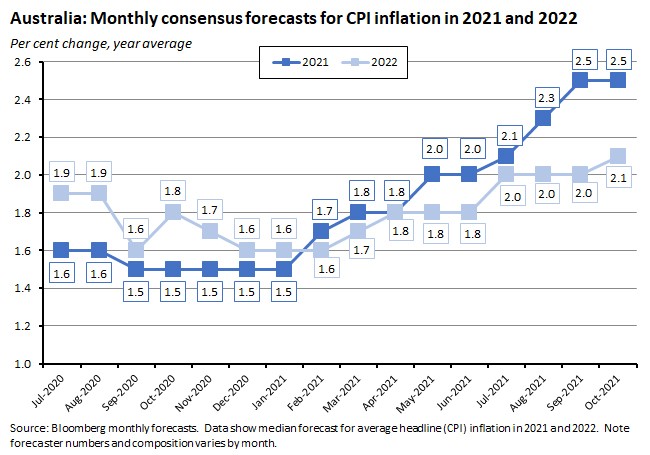

The annual rate of CPI inflation is predicted to slow from 2.5 per cent this year (unchanged from September’s survey) to 2.1 per cent next year (up from two per cent) and then edge up to 2.2 per cent in 2023.

The Bloomberg survey covered 41 economists and was conducted between 14 and 19 October this year.

Why it matters:

The consensus view is that the Australian economy will enjoy a moderate, balanced economic recovery from here. Granted, the median forecast for GDP growth this year has fallen but the ‘missing’ GDP growth has largely been pushed into 2022, where growth expectations have risen. The unemployment rate is expected to head down over the next two years. And headline inflation is predicted to be within the RBA’s target range – but in the bottom half: the median expectation does not foresee any dramatic inflationary breakout and envisions only modest policy tightening by the RBA through into late 2023 / early 2024. That’s a more conservative view than financial markets which (as noted above) currently expect a more aggressive interest rate profile.

What happened:

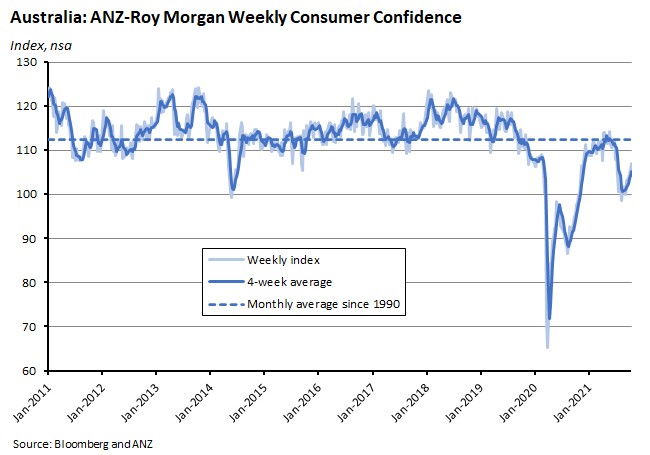

The ANZ-Roy Morgan Consumer Confidence index rose 1.3 per cent last week.

Three of the five subindices rose over the week to 17 October, with increases for ‘current economic conditions’, ‘future financial conditions’ and ‘time to buy a major household item.’ The ‘future economic conditions’ subindex was unchanged while ‘current financial conditions’ edged lower.

Weekly inflation expectations were unchanged at 4.7 per cent.

Why it matters:

This was the sixth consecutive weekly rise in consumer confidence, with increases in the indices for Sydney, Melbourne, Brisbane and Perth. The New South Wales reopening and the scheduled end to Victoria’s restrictions have propelled sentiment in Sydney to above its 2021 average while confidence in Melbourne is now back to its mid-July level.

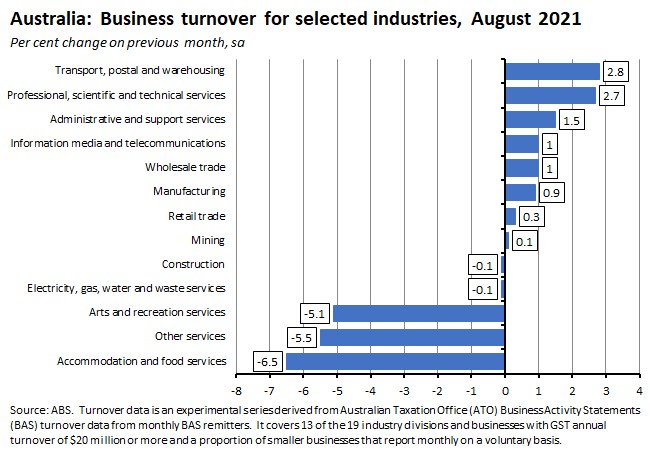

What happened:

Last Friday, the ABS published a new experimental indicator on monthly business turnover. The new data showed moderate rises in turnover for most industries in August 2021, with the largest monthly increases in transport, postal and warehousing (up 2.8 per cent, seasonally adjusted) and professional, scientific and technical services (up 2.7 per cent).

The biggest declines in monthly turnover in August were in accommodation and food services (down 6.5 per cent), other services (down 5.5 per cent) and arts and recreation services (down 5.1 per cent).

Why it matters:

This was the first release of a new ABS series that uses big data to provide insights on business turnover. The data is derived from turnover data in monthly Business Activity Statements submitted to the Australian Taxation Office and covers 13 of the standard 19 industry divisions and businesses with an annual GST turnover of $20 million or more (along with a proportion of smaller businesses that report monthly on a voluntary basis). The numbers for August – and the longer time series that are also available – show that lockdowns and other public health restrictions have produced a significant fall in turnover in service industries where in-person interactions are relatively important.

. . . and what I’ve been following in the global economy

What happened:

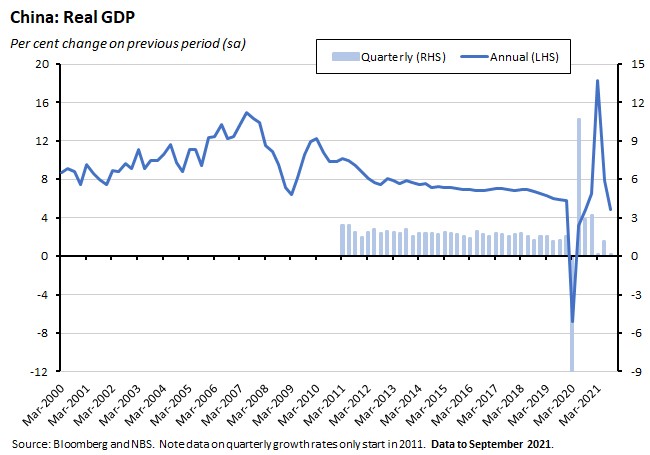

The National Bureau of Statistics (NBS) said that China’s real GDP in the September quarter of this year rose by just 0.2 per cent over the quarter to be up 4.9 per cent over the year. For the first nine months of the year, China’s GDP was up 9.8 per cent over the same period in 2020.

Other data released this week showed industrial production grew at an annual rate of 3.1 per cent in September, down from 5.3 per cent in August, while year-to-date growth in fixed asset investment slowed to 7.3 per cent for January- September from an 8.9 per cent rate over the January-August period. Moving in the opposite direction, the rate of annual growth in retail sales rose to 4.4 per cent last month from 2.5 per cent in August.

Why it matters:

China’s real GDP growth slowed markedly in the third quarter of 2021, dropping to the weakest reading in a year. Although the year-on-year growth rate of 4.9 per cent was only a little below the median forecast for a five per cent print, it does confirm that the economy is struggling in the face of a series of headwinds:

- Until recently, the authorities have been focused more on macroeconomic and financial stability risks than the economic growth rate.Beijing was quick to withdraw the stimulus it had deployed in its initial response to the pandemic,which was itself quite modest compared to the scale of developed country interventions such as those of Australian and the United States.Beijing has also signalled it is reluctant to embrace new stimulus policies with year to date growth at 9.8 per cent still running comfortably ahead of the official target of six per cent growth this year.

- As part of the enhanced focus on financial stability risks, the authorities have been trying to cool an overheated real estate sector by placing restrictions on home sales, putting limits on mortgage lending, introducing caps on rents, and tightening controls on lending to property developers (August 2020’s so-called ‘three red lines’ policy which placed restrictions on companies’ debt according to three balance sheet metrics relating to the ratio of liabilities to assets, net debt to equity, and cash to short-term borrowing).One consequence of this new environment has been a debt crisis at the heavily-indebted Evergrande group along with problems at a range of other developers, which according to Bloomberg estimates may now account for about half of the world’s distressed debt.This financial distress has in turn further weakened sentiment towards the property market and September’s data paints a picture of widespread weakness: China’s new home prices fell for the first time in six years; values in the secondary market dropped for a second consecutive month; the value of residential sales slumped by 16.9 per cent in annual terms after having already dropped by 19.7 per cent in August; real estate investment was down 3.5 per cent over the year, contracting for the first time since the start of the pandemic; and land sales have wilted as the rate of failed land auctions has risen. With some estimates suggesting that the property sector could count for as much as 23 – 29 per cent of GDP once related sectors are included in any calculation, declining activity in the industry imposes a significant drag on overall GDP growth.

- The official squeeze on the property sector is part of a broader policy shift in China as Beijing pursues Xi Jinping’s ‘common prosperity’ agenda which has been focused on controlling rising inequality and which has previously seen the authorities target the technology sector and private tutoring services. That has led to higher levels of uncertainty for businesses and investors.

- Further complicating the picture, the economy is also facing a significant energy squeeze, as a shortage of coal – which still counts for about 70 per cent of China’s electricity generation – has led to a drop in electricity output. The majority of the power sector’s coal comes from domestic sources and local production has faced a range of challenges.Along with a long-term decline in investment and government closure of mines on pollution and safety grounds, domestic coal production has been further disrupted this year by anti-corruption campaigns in Mongolia, flooding in Shanxi, and additional mine closures targeted at cleaning up air pollution ahead of key national events.Domestic shortages have then been compounded by trade developments as coal imports have been affected by restrictions on Australian coal exports and interruptions to Indonesian production.The consequences have included a spike in coal prices that has in turn squeezed electricity producers that have their output prices regulated by the government.As noted, this has seen them cut output, with the resultant energy rationing leading to factories in more than 20 Chinese provinces reported to be limiting or closing down their own production.The authorities have responded by telling China’s coal mines to boost production and allowing electricity producers additional scope to increase prices.

- Iin addition to all of these headwinds, economic activity has also been hit by new COVID outbreaks that have led to the introduction of travel restrictions and other public health measures.

China’s current growth slowdown therefore reflects a mix of factors, some of which look temporary but others which are likely to be longer-lasting. That in turn has implications for global growth, for global commodity demand and (therefore) for commodity prices.

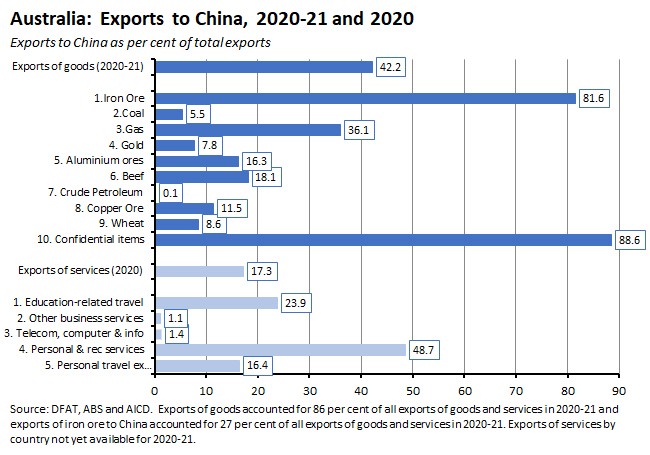

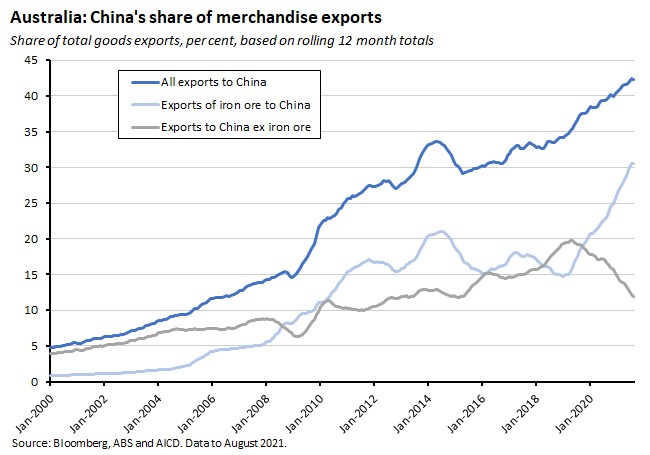

In the case of Australia, and despite the deterioration in the bilateral political relationship, China continues to be a major trading partner and – through its impact on commodity prices – a key driver of the terms of trade and of national income.

The nature of that relationship has been changing, however. While merchandise exports have been dominated by resources in general and iron ore in particular, until recently the importance of iron ore exports has been rising on the back of higher prices while at the same time there has been a marked fall in the relative importance of other exports.

What I’ve been reading . . .

- Deloitte’s new report, Australia remade: A country fit for the age of disruption.

- Tim Colebatch on getting from here to net zero and Mike Steketee on taking the pain out of the carbon transition.

- Despite its troubled political history, this poll suggests that most Australian economists still like carbon pricing (either in the form of cap and trade or as an emissions tax).

- In the AFR, Master, Laroca and Barnaba argue that while Australia is currently suffering from a big immigration shortfall, migration is not a substitute for structural shortcomings in the Australian labour market.

- Also from the AFR, Grenville vs Holden on interest rates and RBA monetary policy.

- An ACCC update on the franchise sector.

- Noted, but not read: the RBA annual report for this year and the Treasury annual report.

- An Economist magazine briefing on living with COVID-19.

- The FT’s Martin Wolf looks ahead to COP26.

- Michael Bordo offers an historical perspective on the prospects for central bank digital currency.

- Ryan Avent says – contrary to some current fears about stagflation – we’re not about to relive the 1970s.

- A new World Bank Working Paper: A mountain of debt: navigating the legacy of the pandemic.

- Two long reads from the WSJ. One on labour scarcity in the US economy and one on Brexit and its impact on UK trade.

- A new NBER paper says falling interest rates disproportionately benefit industry leaders, especially when rates are already low. Record low interest rates and the rise of superstar firms are connected. (h/t FT Alphaville).

- The OECD has updated its long-term scenarios to 2060 and looked at the implications for fiscal sustainability and risks.

- Tyler Cowen makes the case for Mexico.

- McKinsey on the revolution in food delivery.

- An alternative take on human history.

Latest news

Already a member?

Login to view this content