Two weeks ago we flagged ‘the rising chances of a macroprudential policy intervention’ in Australia’s housing market and this week the Australian Prudential Regulation Authority (APRA) acted, instructing banks to increase the minimum interest rate buffer they use when assessing the serviceability of home loan applications. The regulator said that it was worried that increases in the share of heavily indebted borrowers, and rising leverage in the household sector more broadly, were pushing up risks to financial stability.

APRA reckons that its 50bp increase in the serviceability buffer will reduce maximum borrowing capacity for the typical borrower by around five per cent and judges that the likely impact on housing credit growth will be ‘fairly modest.’ But if the housing market doesn’t cool, more policy interventions are likely to follow.

You can find a new chart pack looking at recent developments in the housing market here. The pack includes last week’s CoreLogic dwelling value numbers plus recent data on building approvals and home lending – here.

APRA’s move came less than 24 hours after the RBA’s October monetary policy meeting, which had just highlighted the central bank’s view that it was ‘important that lending standards are maintained and that loan serviceability buffers are appropriate.’ Otherwise, this week’s RBA meeting was a fairly understated affair. Aside from housing market concerns, the main takeaway was that Martin Place remains optimistic that Australia will bounce back from the current Delta-induced economic setback, citing information suggesting that many firms are seeking to hire workers ahead of the expected reopening of the economy later this year. That’s consistent with last week’s ABS vacancies data and this week’s ANZ job ads numbers, which although down over recent months are both still elevated relative to pre-pandemic levels. Meanwhile, lockdowns continue to take a toll on the labour market, with payroll jobs dropping another 0.7 per cent over the most recent fortnight of data, taking job numbers down to below pre-COVID levels.

A big story in the international economy this week has been the intensifying global energy crisis and fears about the possibility of stagflation. We dig into some of the details – and also talk about the latest US debt ceiling drama – in this week’s Dismal Science podcast. Global energy developments also made themselves felt in August’s trade numbers, where Australia reported yet another record monthly trade surplus as a jump in the value of coal and gas exports helped offset the impact of lower iron ore prices.

This week’s readings include the Department of Industry’s latest analysis of Australia’s resource and energy exports, the role of housing in the CPI, an explainer on bracket creep and its fiscal impact in Australia, international commodity market mayhem, the global energy crisis, Britain’s Winter Blues, the US debt limit crisis, and are we on track for a ‘looming financial reckoning’?

Listen and subscribe to Dismal Science podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

At its monetary policy meeting on 5 October 2021, the RBA Board decided to:

- Maintain the cash rate target at 10bp.

- Maintain the target of 10bp for the April 2024 Australian Government bond.

- Continue to purchase government securities at a rate of $4 billion/week until at least mid-February 2022.

The accompanying statement noted that:

- The RBA continues to expect the Delta-driven setback to the economy to be temporary in nature.

- While the RBA forecasts an economic bounce back, it also accepts that there is ‘uncertainty about the timing and pace’ and that the recovery ‘is likely to be slower than that earlier in the year.’

- Wage and price pressures remain subdued in Australia with only a limited impact from disrupted global supply chains.

Consistent with previous RBA communications, the statement noted that the RBA will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range, and that under the RBA’s central scenario for the economy, ‘this condition will not be met before 2024.’

The statement also referred to September’s meeting of the Council of Financial Regulators (see also this week’s readings below), noting that the Council ‘has been discussing the medium-term risks to macroeconomic stability of rapid credit growth at a time of historically low interest rates’ and adding that it was ‘important that lending standards are maintained and that loan serviceability buffers are appropriate.’

Why it matters:

After September’s announcement of the tapering of the RBA’s bond purchase program and Governor Lowe’s 14 September speech in which he noted that he found it ‘difficult to understand why rate rises are being priced in next year or early 2023’ contrary to the RBA’s forward guidance that any move was unlikely before 2024, there was no expectation of any significant monetary policy announcement this month. And, just as expected, the RBA left the levers of monetary policy as they were.

Instead, post-meeting attention focused on two things.

First, the fact that the RBA continues to be relatively optimistic about Australia’s economic outlook, predicting a bounce back that will see the economy growing again in the December quarter and back around its pre-Delta growth path by the second half of next year. In this context, the statement noted that ‘the Bank's business liaison and data on job vacancies suggest that many firms are seeking to hire workers ahead of the expected reopening in October and November.’

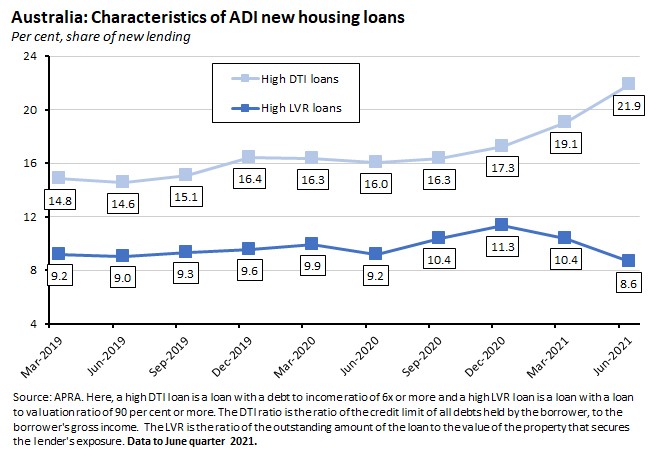

Second, the central bank’s latest take on the housing market and in particular its signalling an upcoming change in macroprudential policy.* A couple of weeks back we had flagged the rising chances of a future macroprudential policy intervention in response to property market developments, and this week’s mention of lending standards and loan serviceability buffers, following on from the Council of Financial Regulators announcing last week that it was discussing possible interventions, delivered a strong signal that a policy response was on the way. Recent RBA commentary focused on the risks associated with highly indebted borrowers suggested that such a policy might focus on limiting loans with high debt to income (DTI) ratios, which have been rising as a share of new lending over recent months, exceeding more than 20 per cent in the June quarter of this year.

In fact, and as set out in the next story, the day after the RBA board meeting the Australian Prudential Regulation Authority (APRA) announced that it would seek to moderate the growth in household leverage, albeit not by direct limits on high DTI loans, but instead by tightening (that is, increasing) the interest rate buffer that it requires lenders to use in their debt serviceability assessments.

*What is macroprudential policy? There is no universally accepted definition, but the general idea is that it involves the use of prudential actions to contain risks that could have systemic implications for the financial system as well as for the real economy. The ‘macro’ in macroprudential refers to this systemic element. The policy actions themselves typically involve employing a range of tools, often grouped into four categories: (1) broad-based capital tools such as dynamic provisioning requirements and time-varying leverage ratio caps; (2) specific sectoral capital and borrower-based tools including restrictions on borrowers such as caps on loan to value ratios (LVRs), DTIs and debt-service-to-income ratios, and restrictions on lenders such as risk-weight floors; (3) liquidity-related tools such as reserve requirements, funding ratios, and caps on loan-to-deposit ratios; and (4) structural tools aimed at mitigating contagion risks such as interbank exposure limits.

In the (relatively) recent past, APRA has twice before introduced macroprudential limits focused on Australian mortgage lending. In 2014, it required banks to limit their lending to housing investors and in 2017 it imposed limits on interest-only mortgages. Recent research from the RBA has found that both policies ‘quickly reduced growth in the targeted type of credit while total mortgage growth remained steady’ and that the policies ‘achieved their stated aims and contributed to a reduction in risk in the financial system.’

What happened:

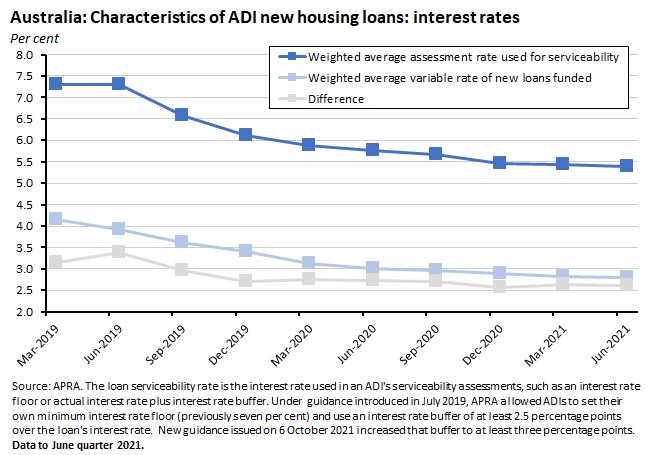

The Australian Prudential Regulation Authority (APRA) has instructed banks to increase the minimum interest rate buffer it expects them to use when assessing the serviceability of home loan applications. In a letter to authorised deposit taking institutions (ADIs), APRA said that it would now expect lenders to assess new borrowers’ ability to meet their loan repayments at an interest rate that is at least three percentage points above the loan product rate. Prior to this week’s announcement the ‘interest rate buffer’ APRA required ADIs to apply to new loans was at least 2.5 percentage points.

According to APRA, the move ‘reflects growing financial stability risks from ADIs’ residential mortgage lending.’ The regulator said that although ‘the banking system is well capitalised and lending standards overall have held up, increases in the share of heavily indebted borrowers, and leverage in the household sector more broadly, mean that medium-term risks to financial stability are building. More than one in five new loans approved in the June quarter were at more than six times the borrowers’ income, and at an aggregate level the expectation is that housing credit growth will run ahead of household income growth in the period ahead.’

APRA explained that it decided to use an increase in the interest rate buffer as it was the ‘most appropriate tool to use’, would act as a cap on leverage, be relatively easy to implement, and would not have any impact on mortgage interest rates. It also noted that it chose not to follow the alternative route of imposing an interest rate floor because the impact of a buffer was likely to be relatively greater for investors than owner-occupiers, as investors typically tend to borrow at higher levels of leverage and may also have other existing debts (to which the buffer would also be applied). In contrast, a floor would be relatively more onerous for owner-occupiers.

The regulator also acknowledged that introducing direct limits on the extent of high debt to income (DTI) borrowing would have been a more precise way of targeting more highly indebted borrowers. But it said that compared to raising the interest rate buffer ‘limits would be more operationally complex to deploy consistently, and [could] lead to higher interest rates for some borrowers as lenders effectively seek to ration credit to this cohort.’

APRA also said that ‘it does not rule out that the other measures might be used in the future.’

Why it matters:

APRA acted within a day of the RBA board meeting flagging the likelihood of a macroprudential policy intervention in the housing market. The regulator was keen to stress that the motive for its action this week was to moderate the current growth in household indebtedness and reduce risks to future financial stability by ensuring ‘that mortgage lending is conducted on a prudent basis, and that borrowers are well-equipped to service their debts under a range of scenarios.’ It emphasised that it was not seeking to target the level of housing prices.

APRA also acknowledged that the impact of this week’s move is likely to be limited: it estimates that a 50bp increase in the serviceability buffer will reduce maximum borrowing capacity for the typical borrower by around five per cent. Moreover, since some borrowers are already constrained by the floor rates used by individual lenders, and since many borrowers do not borrow at their maximum capacity anyway, APRA’s judgment is that ‘the overall impact on aggregate housing credit growth…is expected to be fairly modest.’ In that context, the regulator’s comment that it does not rule out using other measures such as an interest rate floor or a direct limit on high DTI lending in the future might be taken as indicating that more such policy interventions are on the cards if the housing market does not start to cool off in coming months.

What happened:

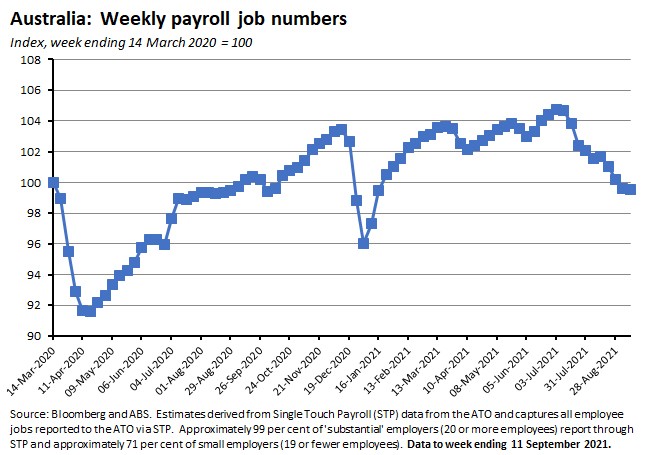

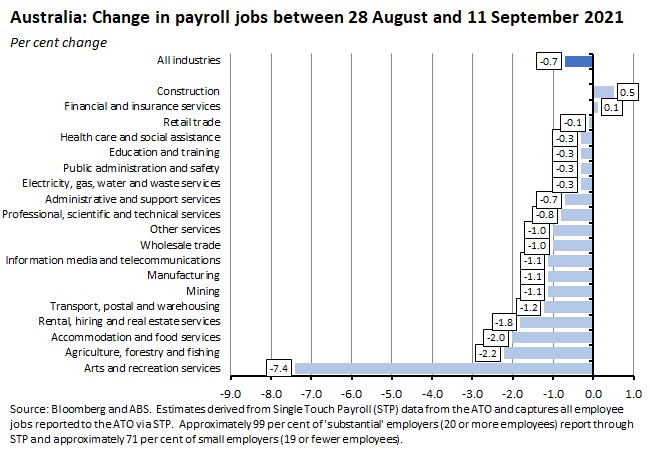

The ABS said that payroll job numbers fell 0.7 per cent between the weeks ending 28 August and 11 September 2021, after having fallen 1.5 per cent over the previous fortnight. Total wages paid were up 1.8 per cent over the most recent two weeks of data compared to a fall of 0.8 per cent over the previous two-week period.

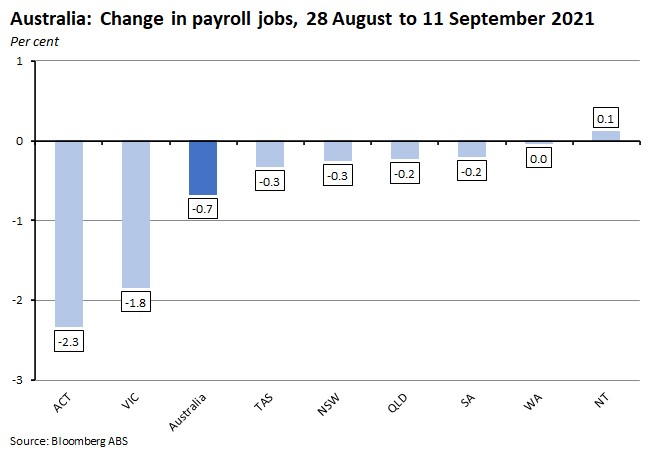

By state and territory, the largest percentage declines in jobs numbers over the past fortnight were in the ACT (down 2.3 per cent) and Victoria (down 1.8 per cent). Jobs were flat in Western Australia and up marginally in the Northern Territory.

By industry, the biggest percentage declines in payroll jobs in the two weeks between 28 August and 11 September were in arts and recreation services (down 7.4 per cent) and accommodation and food services (down two per cent) as well as in agriculture, forestry and fishing.

By demographic characteristics, jobs worked by men were down 0.7 per cent over the last two weeks of data, jobs worked by women were down 0.8 per cent, while the largest decline by age group was for those aged between 15 and 19, with a 1.6 per cent fall over the same fortnight.

Finally, by firm size jobs fell in small (less than 20 employees) and medium (between 20 and 199 employees) size businesses but edged higher in large (200 employees and over) businesses.

Why it matters:

Payroll jobs have now fallen 2.1 per cent over the past month and are down about five per cent since the start of July. Job numbers have now dropped back below their pre-pandemic levels (they are down 0.5 per cent from the week ending 14 March 2020) and – excluding the seasonal drop that took place after Christmas – are currently at their lowest level since August 2020 and Victoria’s second wave lockdown.

The payroll data once again highlight the impact of public health restrictions on the labour market. For example, job numbers are now below their pre-pandemic levels in New South Wales, Victoria and the ACT, all of which had lockdowns in effect over this period. The largest job losses were in Victoria (which accounted for almost 72 per cent of all jobs lost over the fortnight) and in the ACT while the pace of job loss moderated in New South Wales.

Similarly, job losses were largest in the accommodation and food services and arts and recreation services industries, with jobs in both industries about 24 per cent below their pre-pandemic levels. In Victoria, payroll jobs in arts and recreation slumped 21.7 per cent over the two weeks to the week ending 11 September.

For more charts on the payroll jobs release as well as updated charts on ABS job vacancies and ANZ job ads, you can take a look at our updated labour market chart pack.

What happened:

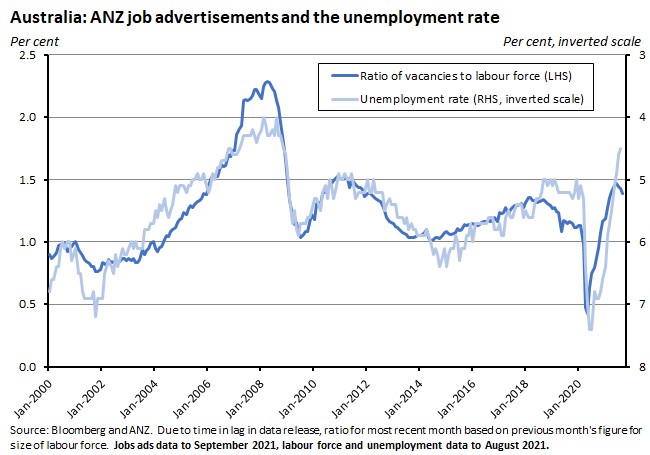

ANZ job ads fell 2.8 per cent over the month in September but were still 21.9 per cent higher than their pre-pandemic level.

Why it matters:

Job ads have now fallen a cumulative 6.8 per cent over the past three months, providing another indicator of the toll that state lockdowns have taken on labour market conditions. But in this case, that toll has been relatively modest: as ANZ note, between February 2020 and May 2020 job ads had plunged by more than 64 per cent during Australia’s first national lockdown.

That relative resilience should be good news for the labour market looking forward and is consistent with the RBA’s observation that firms are planning to boost hiring once state economies re-open. At current levels, job ads are consistent with a modest rise in the unemployment rate from its current (artificially low) level to a bit above five per cent.

What happened:

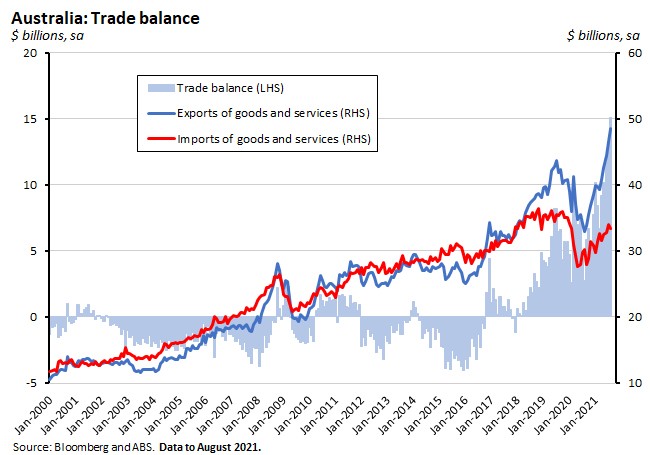

The ABS said that Australia’s monthly trade surplus rose to $15.1 billion in August (seasonally adjusted), a $2.4 billion increase over the previous month. Exports of goods and services rose $1.9 billion (four per cent) over the month to $48.5 billion while imports of goods and services fell $0.5 billion (one per cent) to $33.4 billion.

Why it matters:

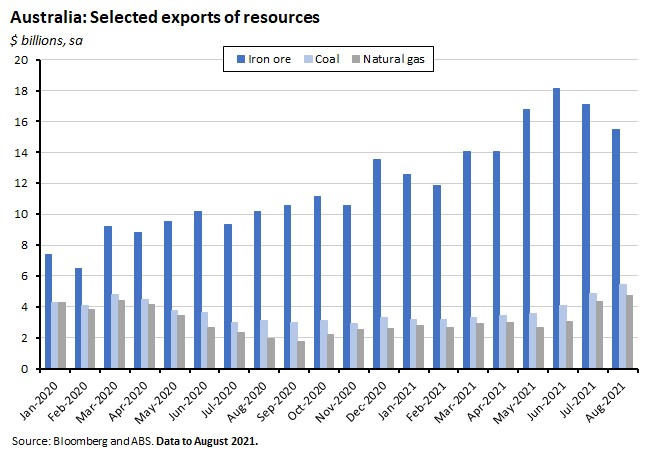

Hot on the heels of July’s record trade result, August saw Australia report yet another new record surplus, with the $15.1 billion outcome comfortably exceeding market expectations of a $10.1 billion print. August’s result was all the more impressive given that it took place against the backdrop of a sharp decline in the price of iron ore over the month, with the commodity falling from around US$180/t at the end of July to around US$140/t by the start of September. After peaking at more than $18 billion in June, the monthly value of Australia’s exports of iron ore and concentrates had already edged down to (more than) $17 billion in July, but then dropped by more than $1.7 billion to less than $15.5 billion in August.

At the same time, however, other exports had a strong month. Exports of coal and coke were up $0.6 billion over the month, and exports of natural gas rose by $0.4 billion, reflecting strong energy demand from Asia. Exports of rural goods were up almost $0.6 billion, led by an increase in the value of exports of cereal grains and preparations as supply and production disruptions affecting other key wheat exporters advantaged Australian producers. The trade surplus was also boosted by a decline in imports, with falls in imports of capital (down four per cent) and intermediate goods (down seven per cent) in August more than offsetting a four per cent rise in imports of consumption goods, where the latter was powered by a 12 per cent jump in the value of imports of non-industrial transport equipment as demand for passenger vehicles contributed to a record high.

See also this week’s readings for a look at the latest Resources and Energy Quarterly and its forecasts for Australian exports.

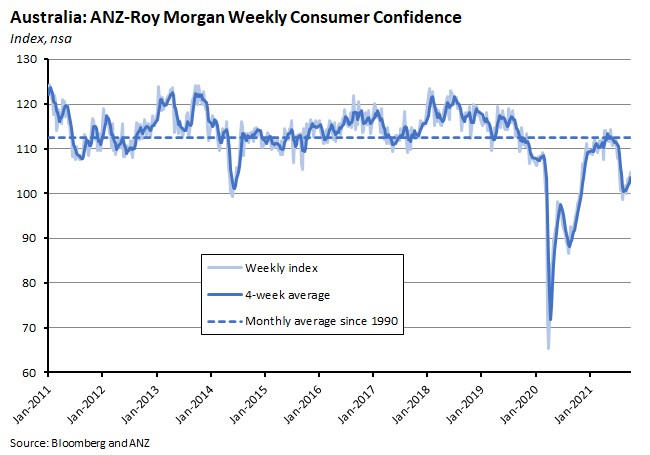

What happened:

The ANZ Roy Morgan Index of Consumer Confidence rose 0.9 per cent last week, taking the index up to a level of 104.6.

Three of the five subindices (‘current financial conditions’, ‘current economic conditions’ and ‘future economic conditions’) rose over the week while there was a slight decline for ‘future financial conditions’ and a larger one for ‘time to buy a major household item.’

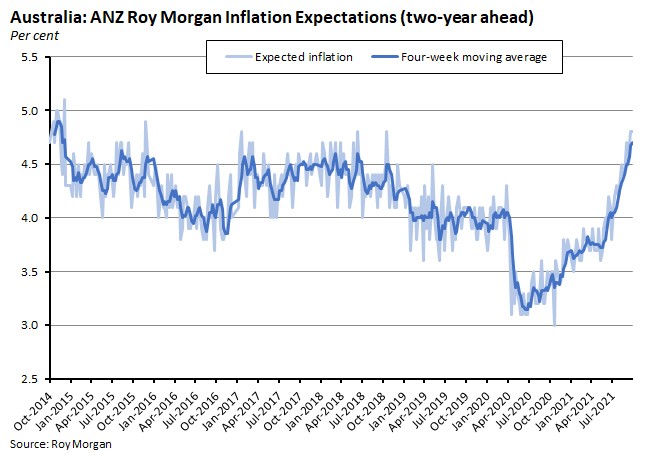

After hitting a pandemic high of 4.8 per cent the previous week, weekly inflation expectations were unchanged last week.

Why it matters:

Consumer confidence has now registered four consecutive weeks of modest gains, with the index rising by a cumulative 4.6 per cent over the past month. That still leaves confidence below its long-term average but does indicate a degree of resilience in terms of sentiment.

Inflation expectations remain elevated but did not increase over the past week.

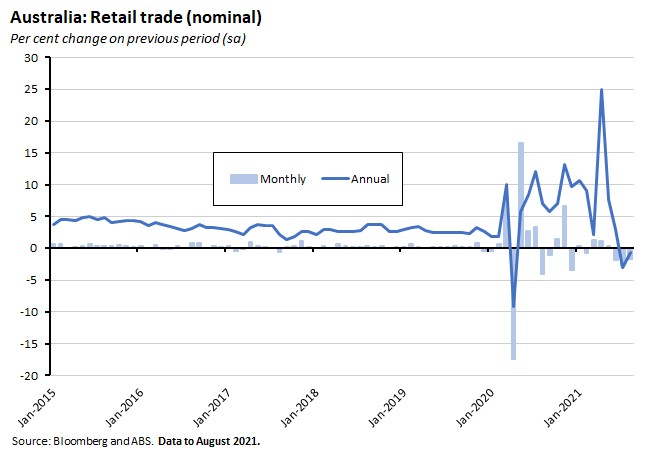

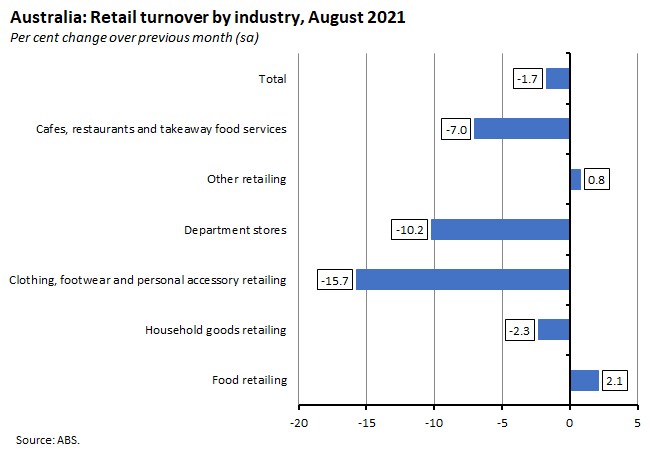

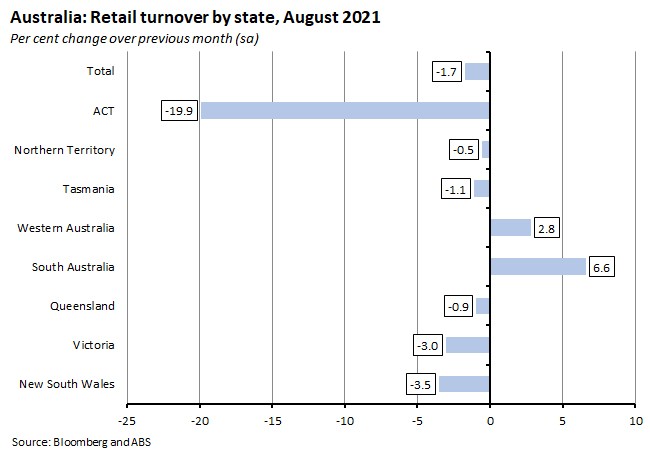

What happened:

Last week, the ABS reported that retail turnover fell 1.7 per cent over the month in August 2021 to be down 0.7 per cent over the year.

By industry, retail trade over the month was down sharply in clothing, footwear and personal accessory retailing (down 15.7 per cent), department stores (down 10.2 per cent) and cafes, restaurants and takeaway food services (down seven per cent). Only food retailing and other retailing enjoyed increases in August.

By state and territory, turnover slumped by 19.9 per cent month-on-month in the ACT alongside more modest declines in New South Wales (down 3.5 per cent), Victoria (down three per cent) and in Tasmania, Queensland and the Northern Territory. Only South Australia and Western Australia reported monthly gains.

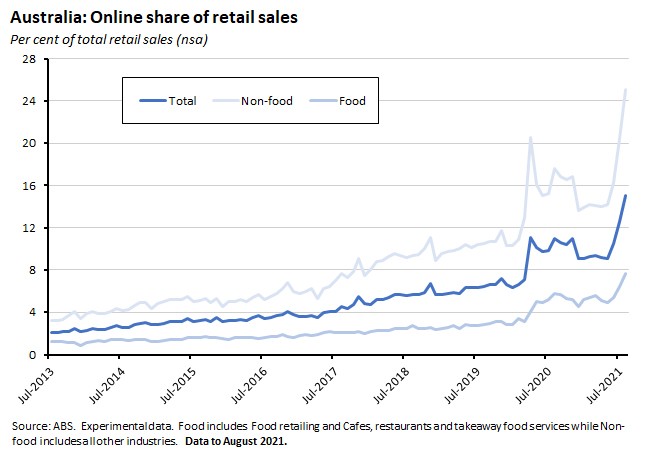

Total online sales rose to a record $4.2 billion in August after a $549 million (15.1 per cent) jump over the month. Online sales accounted for 15 per cent of total retailing in the month, breaking the previous record of 12.6 per cent set in July this year.

Why it matters:

August’s decline in retail trade was the third consecutive monthly drop in turnover (which also fell 1.8 per cent in June and 2.7 per cent in July) and continues to reflect the impact of the distribution of state lockdowns. In New South Wales, for example, turnover is now at its lowest level since April 2020 and the opening months of the pandemic, while the 12 August snap lockdown in the ACT was reflected in August’s sharp monthly drop. Moving in the opposite direction, the exit of South Australia from lockdown restrictions in late July was associated with a bump in August sales.

Lockdown effects were also apparent in the distribution of industry turnover (sharp falls for exposed businesses and an increase for food retailing) and in a new record share of online sales in total retail trade.

What I’ve been reading . . .

The September 2021 Resources and Energy Quarterly (REQ) estimates that after hitting a record $310 billion in 2020-21, Australia’s resource and energy exports will surge to a new record high of $349 billion in 2021-22 before falling back to $299 billion in 2022-23. Key projections include:

- After reaching a record $153 billion in 2020-21, the REQ sees iron ore export earnings sliding to $132 billion in 2021-22 and $99 billion in 2022-23.While export volumes are expected to grow steadily over the forecast period, prices have fallen from their highs of earlier this year in response to policy decisions in Beijing including efforts to cool the property market and introduce curbs on steel production. Further out, iron ore supply is expected to increase as Vale’s Brazilian operations gradually ramp up production although the REQ judges that global iron ore markets will remain relatively tight, with slow growth in both supply and demand over the next few years.The nominal iron ore price is forecast to fall from US$150/t in 2021 to US$93/t in 2022 and USA$81/t in 2023.

- The REQ forecasts exports of metallurgical (coking) coal to rise from $23 billion in 2020-21 to $32.8 billion in 2021-22 before easing back to $30 billion in 2022-23. In the near-term, prices have climbed to new peaks in recent months as supply shortages have combined with a recovery in global industrial production including catch-up growth in steel and auto making capacity. The REQ notes that China’s informal restrictions on Australian coal exports have seen other exporters, including Canada, step up sales to the country, along with the persistence of a price premium for non-Australian coal.However, the REQ also notes that Australian coal exports have now been successfully integrated into new supply chains including through increased sales to South Korea and Japan.

- Exports of thermal coal are expected to rise from $16 billion in 2020-21 to $24 billion in 2021-22 before falling back to $19 billion in 2022-23.The REQ notes that trade in thermal coal ‘remains subject to significant competing forces.’In the near-term, user restocking after an unusually cold Northern hemisphere winter, economic recovery and an increase in Asian demand following an unusually hot northern summer have all helped drive up prices for some grades of thermal coal to their highest levels in a decade.In the longer-term, however, the REQ comments that growing investor and policy pressure has seen the global coal-fired power plant construction pipeline shrink since 2015, while recent net zero emissions commitments from China (by 2060), the EU (by 2050), Japan (by 2050), and South Korea (also by 2050) will impact on prospects for potential new coal mines. At the same time, coal-fired power plants are still under construction in China and South Asia.The REQ also notes that the effect of Chinese informal import restrictions on Australian coal has now abated, with total monthly export earnings now exceeding pre-restriction levels.

- LNG export earnings are forecast to jump from $30.5 billion in 2020-21 to $55.7 billion in 2021-22 in line with increases in oil-linked contract prices before slipping back to $50.2 billion in 2022-23 (the REQ notes that around three-quarters of Australian LNG is sold via long-term contracts that link the price of LNG to the price of oil). Again, the near-term story here has been driven in part by extreme weather events (a bitter Northern hemisphere winter followed by a hot Asian summer, as well as droughts in South America that affected hydro generation). On the demand side of the equation, China is expected to move from being the world’s second largest LNG importer last year to being its largest importer this year, driven by industrial and residential demand and gas-to-coal switching as part of Beijing’s net zero by 2060 target.

- The latest RBA chart pack.

- Last week, the September 2021 Quarterly Statement from Council of Financial Regulators reported that at its most recent meeting the Council ‘continued its dialogue on housing credit conditions and associated risks,’ noting that ‘a period of credit growth materially outpacing growth in household income would add to the medium-term risks facing the economy, notwithstanding that lending standards remain sound’ and reporting that the Council ‘discussed possible macroprudential policy responses.’ The Statement also noted that in the next couple of months APRA planned to publish an information paper on its framework for implementing macroprudential policy.

- I’ve had a couple of questions this week on the relationship between rising house prices and the consumer price index (CPI). This March 2017 ABS article explains the role of housing in the CPI. And this 2019 explainer from the RBA provides additional detail. After the 2020 annual re-weight of the CPI, the Housing group now has a 24.1 per cent weight in the index, making that group the largest component of household spending in the CPI. The Housing group includes new dwelling purchases by owner-occupiers (8.5 per cent of the total index), rents (6.8 per cent), other housing which includes maintenance and repair costs plus property rates and charges (almost four per cent) and utilities (4.8 per cent). The new dwelling purchases component measures the price of a new dwelling excluding the value of the land and is intended to capture the cost of adding to the housing stock in the form of newly built dwellings and major renovations. The rents component captures payments made by households to landlords as rent. It’s important to note that several key items are excluded from the CPI. (1) Purchases of established dwellings are excluded because they are treated as transfers of existing assets. (2) Land is excluded as it is treated as investment not consumption. (3) The cost of servicing a mortgage has also been excluded from the CPI since 1998. That means that changes in the price of established dwellings, changes in the price of land, and changes in the cost of servicing mortgage debt do not have a direct influence on CPI inflation.

- A Parliamentary Budget Office (PBO) explainer on bracket creep and its fiscal impact. Bracket creep describes the situation where income growth causes individuals to pay higher average income tax rates over time as rising incomes push taxpayers into higher tax brackets. In Australia, the PBO calculates that bracket creep is largest for individuals earning at the $45,000 threshold, followed by those earning at the $180,000 threshold. Bracket creep is also estimated to drive most of the anticipated reduction in Australia’s net debt to GDP ratio over the next decade: if instead the average tax rate were to remain at 2021-22 levels, the PBO reckons any decline in net debt from 2024-25 onwards would be negligible. Note that this is the first in a new series of budget ‘explainers’ from the PBO.

- Three ways China’s Evergrande collapse could hurt the Australian economy: lower iron ore prices, weaker Chinese growth and the potential for global contagion.

- Rajah and Grenville review the scope for Australia to negotiate with China on Beijing’s request to join the Comprehensive and Progressive Trans-Pacific Partnership (CPTPP).

- Peter Mares on Australia’s latest housing affordability inquiry.

- Grattan’s Marion Terrill defends Victoria’s (to be joined in the future by NSW and SA) plan to levy a new per kilometre charge on Electric Vehicles.

- Some short comments from Productivity Commission Chair Michael Brennan on Australia’s future productivity.

- The Economist’s Buttonwood column says that while commodity markets in the 2000s were all about the supercycle, commodity markets in the 2020s are about ‘supermayhem’. Three shocks (a stop-start, uneven economic rebound; governments trying to accelerate the green transition; and geopolitical tensions) and the interaction between them are generating chaos, it argues.

- Bloomberg Businessweek on why Europe’s energy crisis is part of a global problem.

- An FT Big Read on Britain’s winter blues as the country grapples with petrol, gas and food shortages.

- The WSJ examines how China’s power shortfalls are adding to global supply chain disruption.

- Analysis from the Bipartisan Policy Center on the unfolding US Debt Limit crisis and the costs of crossing the debt limit ‘X date’.

- Willem Buiter warns that we’re living in a world where financial fragility is rife, funding and market-liquidity crises are part of the new normal, risk assets appear to be overvalued and central banks need to prepare for a looming financial reckoning.

- Making the case for mandatory corporate carbon disclosures.

- What drives cryptocurrency investments? Two popular candidates – concerns about the security of cash and of commercial banking – don’t appear to be as important as is often assumed.

- The latest issue of the Journal of Economic Perspectives includes symposia on the Washington Consensus and Statistical Significance.

- Inside Apple’s battle over remote work.

- (Sort of) related: Existential optimism. Is power shifting from institutions to individuals, giving people more control over their lives?

Latest news

Already a member?

Login to view this content