Are the federal government's budgetary support measures enough to counter the economic destruction caused by COVID-19?

The year 2020 was devastating for the Australian economy and much worse for many of our advanced-economy peers. Looking back to its opening months, the early sense was that, for Australia, much of the year’s business would involve grappling with the lessons from last summer’s terrible bushfires.

The fires sparked in our hottest and driest year on record burnt more than 17 million hectares of land and resulted in the deaths of at least 33 people, the loss of huge numbers of animals, the destruction of thousands of homes, choking air pollution, a direct financial cost of more than $10b and a total economic cost likely to be far larger.

Significant subplots for 2020 were expected to include ongoing US-China trade wars abroad and any collateral damage for us, the search for faster growth and greater economic dynamism here at home, and a policy tug-of-war between a Reserve Bank focused on easy monetary policy to combat below-target inflation and employment and a government targeting fiscal policy at a much-promised budget surplus.

Instead, we got a worldwide pandemic, the deepest global recession since the 1930s and a major shift in priorities.

The International Monetary Fund’s (IMF) latest estimate is that world output will shrink 4.4 per cent in 2020 — a calamitous outcome that dwarfs the 0.1 per cent contraction associated with the global financial crisis (the worst outcome for global growth in the postwar period to date) and one the IMF believes could tip around 90 million people into extreme poverty and supercharge inequality.

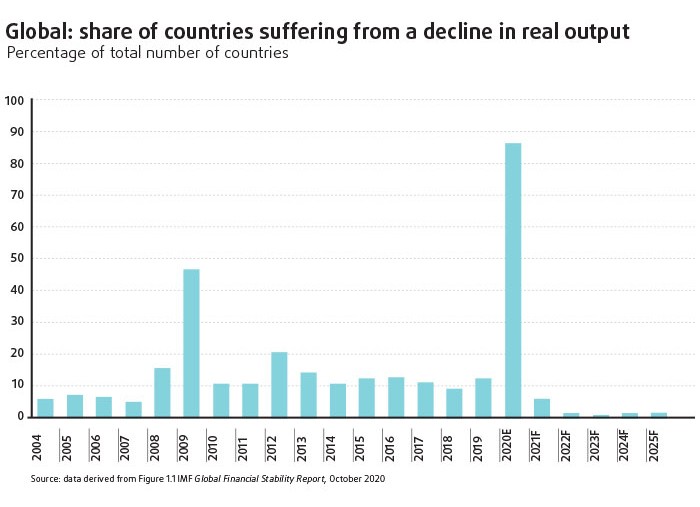

The economic destruction has been widespread: more than 85 per cent of the world’s economies will see real output decline in 2020, with China the only major economy expected to achieve positive growth.

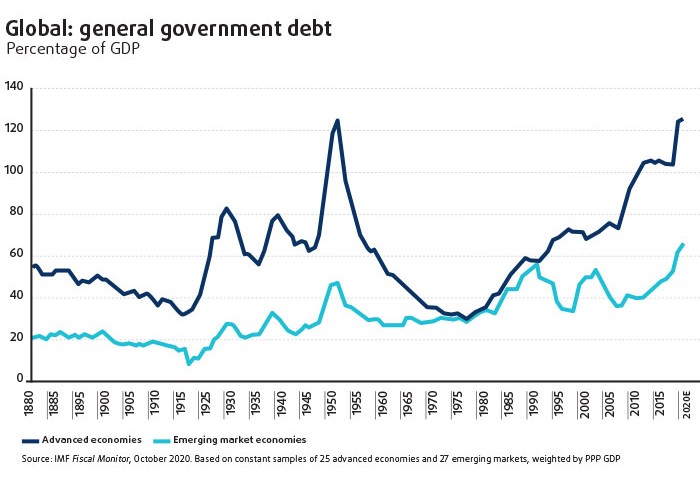

The policy response has been almost as dramatic as the economic shock. Collective global fiscal measures announced as of early September are around US$11.7 trillion, or nearly 12 per cent of world GDP. That, in turn, will push global public debt close to a record-breaking 100 per cent of GDP in 2020. Monetary policy has been put to work, too, as the world’s leading central banks first reprised their GFC playbooks and then went even further.

The key economic question for the global economy in 2021 is whether all this policy support, plus a huge public health effort, will be enough to restore confidence and growth. The IMF’s view is that the world economy will expand by 5.2 per cent in 2021, but this forecast is conditional on continued progress with controlling the pandemic and developing a vaccine, the maintenance of sustained policy support and the successful avoidance of significant non-COVID-related risks, including financial market flux, geopolitical turmoil and domestic political unrest.

Australia’s economic and public health performance in 2020 has been superior to that of many advanced economies. Even so, the pandemic and government lockdowns have resulted in a heavy economic cost. In July, for example, Treasury estimated that, relative to a pre-pandemic economy, the restrictions that were in place from late March to mid-May had cost the economy around $4b a week. More recently, it put the daily economic cost of Victoria’s lockdown at around $100m, including the loss of an average of 1200 jobs per day during August and September. Real output is forecast to contract 3.75 per cent, marking Australia’s deepest recession in the postwar period.

Like their global counterparts, both Canberra and Martin Place have been aggressive in their policy response. Pre-crisis dreams of a balanced budget have been banished for at least a decade, with the government rolling out an incredible $257b in direct budgetary support — an effort that will see gross government debt climb above $1 trillion by next financial year and stabilise at around 55 per cent of GDP in the medium term. Meanwhile, the cash rate has been slashed to a record low of 0.1 per cent and the RBA’s deployment of unconventional monetary policy measures, including yield curve control and aggressively expansionary forward guidance, has now been augmented by quantitative easing in the form of a promise to purchase $100b of government bonds over the next six months.

Treasury’s best guess is that this will help deliver economic growth of 4.25 per cent in 2021. But again, this assumes that any future localised outbreaks of COVID-19 are largely contained and that a population-wide Australian COVID-19 vaccination is fully in place by late 2021. That in turn would allow the lifting of most state border restrictions, followed first by a gradual return of international students and permanent migrants and later a gradual recovery in international tourism.

Two of the most critical economic questions for 2021 will be whether Treasury’s assumptions regarding the trajectory of the pandemic are on the money and whether the front-loaded budgetary support that’s been delivered to date will prove sufficient to buttress private sector spending.

The answer to the first will play a large part in determining the answer to the second. While the pandemic and its consequences look set to determine the economic course of the year ahead, the lessons of the 2019-20 bushfires should not be forgotten. Both disasters can be linked to our anthropogenically challenged global environment and both are potent examples of a cost-benefit trade-off that strongly favours prevention and insurance. The Royal Commission into National Natural Disaster Arrangements, completed in October, warned that extreme weather events have already become more frequent and more intense due to climate change and that with further global warming “inevitable” over the next two to three decades, Australia will face even greater challenges ahead.

The commission judged that “natural disasters are expected to become more complex, more unpredictable and more difficult to manage” and that we’re more likely to see “compounding natural disasters on a national scale with far-reaching consequences”, including the challenge of “cascading effects” that would threaten “not only lives and homes, but also the nation’s economy, critical infrastructure and essential services”. COVID-19 and the bushfires both suggest that working towards recovery and building national resilience should be priorities for 2021.

Latest news

Already a member?

Login to view this content