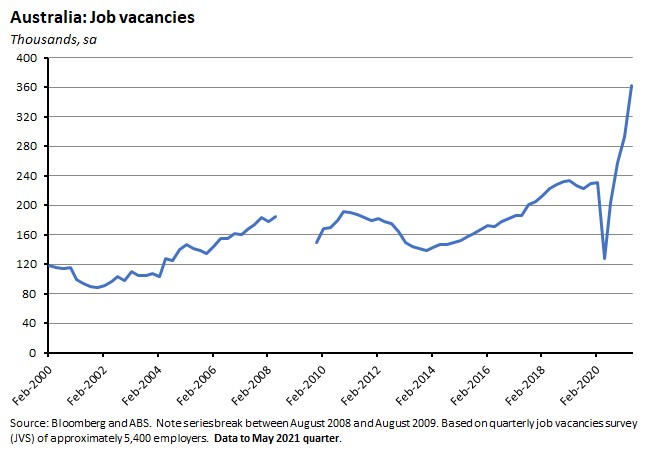

The ABS said that the number of job vacancies jumped to a record high of 362,500 in May 2021, up 57 per cent (132,000) from pre-pandemic levels. CoreLogic reported that national house prices rose 1.9 per cent over the month in June 2021 to be 13.5 per cent higher over the past financial year. The latest Intergenerational Report (IGR 2021) suggests that the combined impact of the pandemic plus longer-running demographic trends could lead to an Australia in the future that is somewhat smaller (in terms of both population and GDP), older, poorer and more indebted than was projected to be the case at the time of IGR 2015.

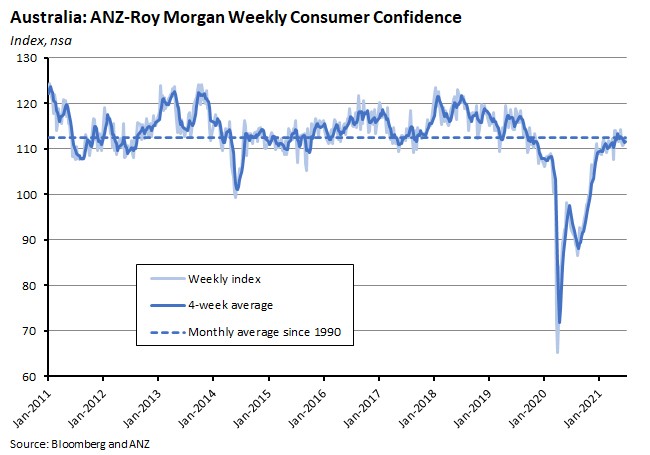

That also assumes that productivity growth performs considerably better than it has done in the recent past. Australia recorded a trade surplus of $9.7 billion in May this year, only a little below the record $9.9 billion surplus recorded in January 2021. According to the RBA, total credit to the private sector rose 0.4 per cent over the month (seasonally adjusted) in May 2021 to be up 1.9 per cent higher in year-on-year terms, as housing credit continues drive overall growth. The ANZ Roy Morgan Index of Consumer Confidence edged down 0.2 per cent over the week ending 26-27 June with a decline in confidence in NSW largely offset by a recovery in Victoria.

This week’s readings include market power and the Australian economy, new forecasts for Australia’s resource and energy exports, an update on household wealth and income, global productivity trends and prospects, the economics of deep trade agreements, the CCP at 100 and an appreciation of Albert O. Hirschman.

On the Dismal Science podcast this week, we look at the economic impact of this lockdown, at more on the intergenerational report, at how house prices keep going, at a boom in job vacancies and at the return of European tourism.

Listen and subscribe: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

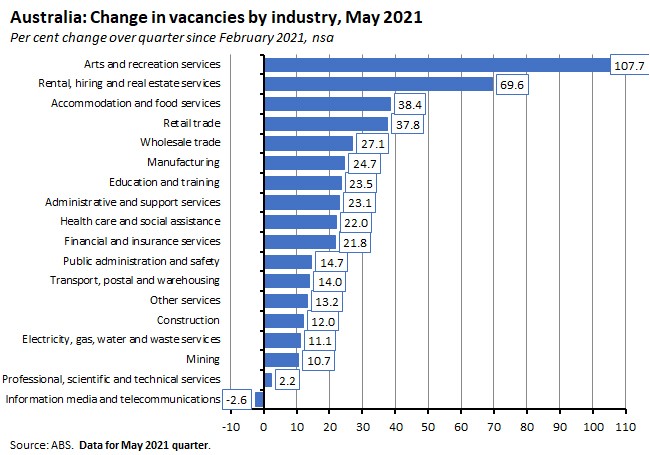

According to the quarterly Job Vacancies Survey, total job vacancies were 362,500 in May 2021, up 23.4 per cent (seasonally adjusted) from February 2021. Private sector vacancies were up 24.8 per cent to 331,900, while public sector vacancies rose 10 per cent to 30,600. Private sector vacancies accounted for about 96 per cent of the total increase.

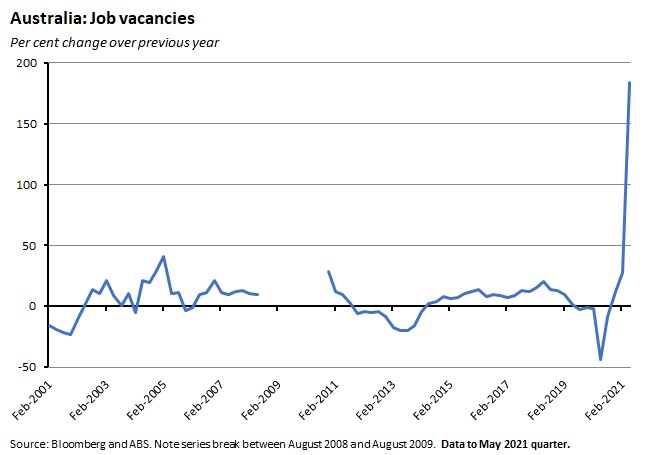

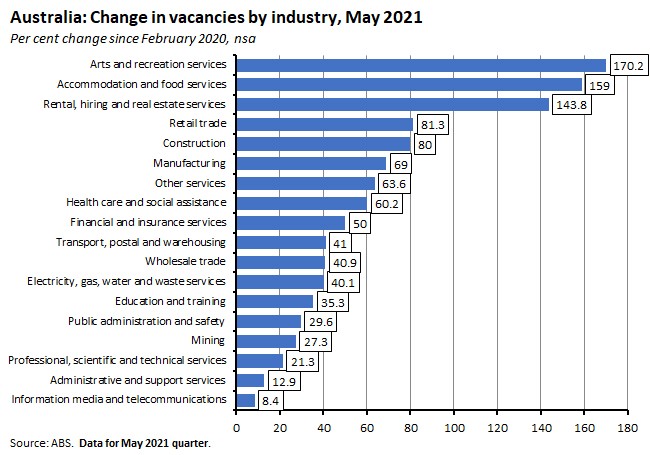

Relative to May 2020, when numbers were driven down by the impact of the pandemic, vacancies were up more than 180 per cent.

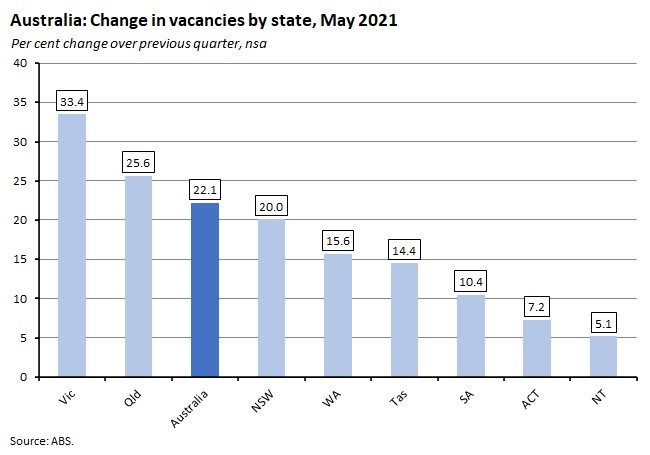

Vacancies were up in all states and territories over the quarter (original terms). The largest growth was in Victoria (33 per cent) but note that the mid-May survey reference period fell before that state’s most recent lockdown.

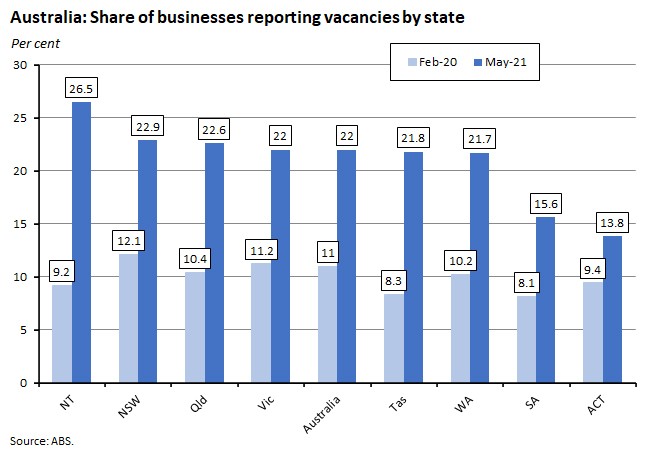

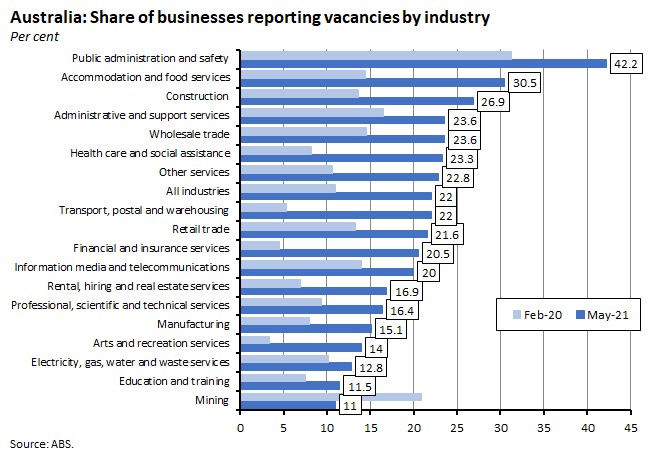

The ABS also reported that there has been a steady increase in the share of businesses reporting at least one vacancy. Pre-pandemic, that share was 11 per cent and it had fallen to just seven per cent as of May 2020. But by August last year it had increased to 12 per cent. Since then, it has continued to rise, climbing to 15 per cent in November 2020, 18 per cent in February 2021 and 22 per cent in this latest result. The share of businesses reporting vacancies by state in May 2021 ranged from a bit less than 14 per cent in the ACT to more than 26 per cent in the Northern Territory.

By industry, over the past quarter the biggest percentage increase in the number of vacancies was in arts and recreation services, followed by rental, hiring and real estate services.

The share of businesses reporting vacancies by industry in March 2021 ranged from a high of more than 42 per cent in public administration and safety to a low of 11 per cent in mining.

Why it matters:

At 362,500, job vacancies hit a record high in May 2021 and were 57 per cent higher (132,000) than in February 2020, before the start of the pandemic. Over that period, the growth in the number of vacancies has been strongest in arts and recreation services, accommodation and food services, and rental hiring and real estate services. The ABS also noted that the increase in reported labour shortages is particularly notable for lower paid jobs.

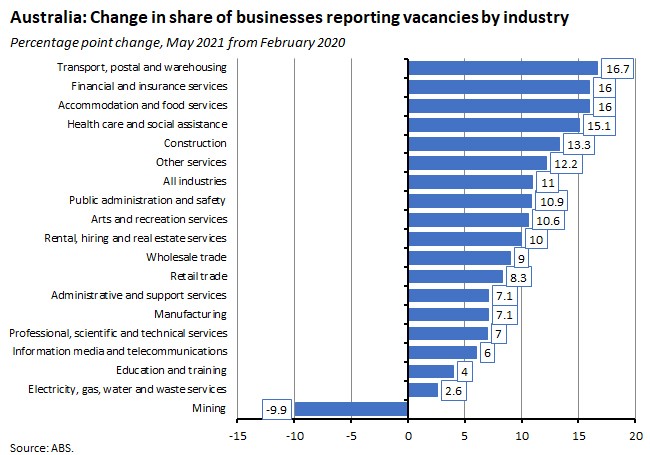

Measured in terms of the share of businesses in each industry reporting vacancies, the largest increases have been in transport, postal and warehousing services (up 16.7 percentage points) and financial and insurance services and accommodation and food services (up 16 percentage points).

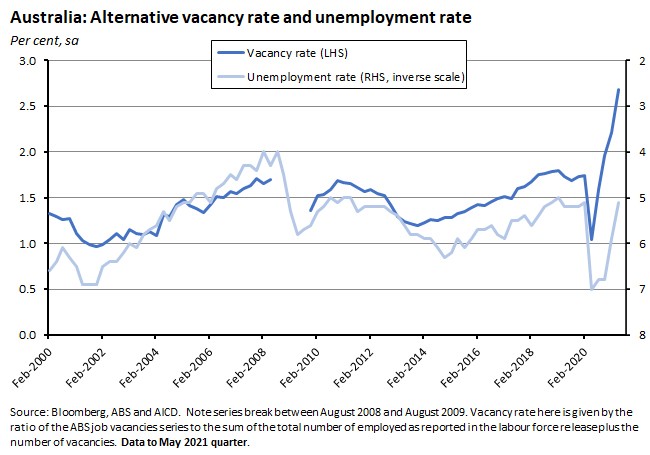

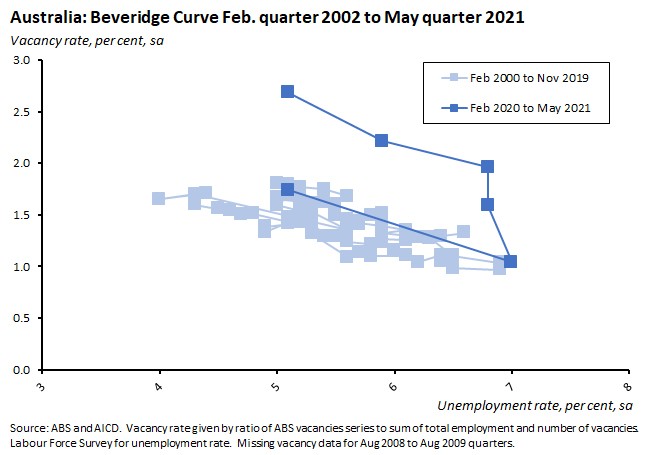

A few weeks ago, we took a detailed look at the relationship between vacancies (using the labour account measure) and unemployment as tracked by the Beveridge Curve. By combining the ABS vacancy data with employment data from the labour force, we can construct an alternative vacancy rate series to the one provided by the labour account and again compare with the unemployment rate.

As would be expected, the data deliver the same message as that earlier analysis: a given rate of unemployment is now associated with a higher rate of vacancies than has typically been the case.

The most likely explanation remains the story we told in that earlier piece about the lagged response of labour market matching following some very large swings in employment and unemployment. That story also implies that there is scope for significant further falls in the unemployment rate. But as we noted then, other explanations are also possible.

What happened:

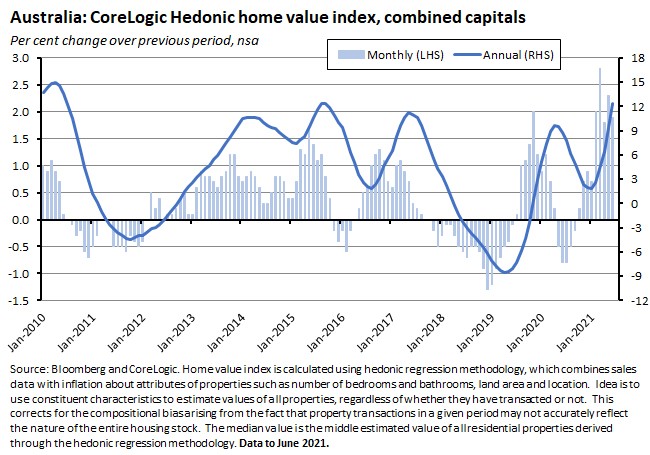

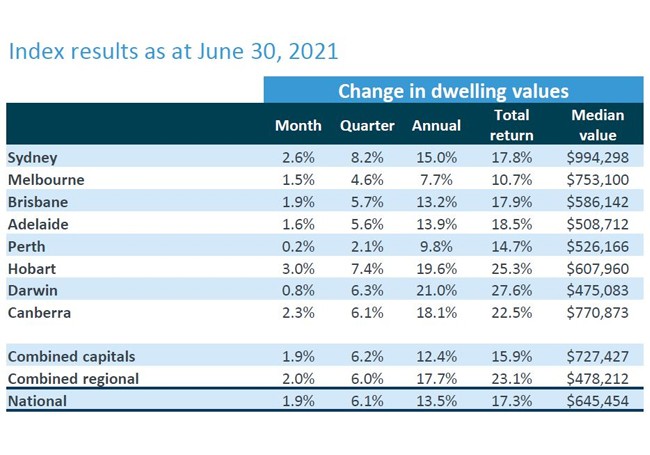

CoreLogic said that its index of national dwelling values rose 1.9 per cent over the month in June to be 13.5 per cent higher in annual terms. Combined capitals values rose 1.9 per cent month on month and 6.2 per cent year on year while the corresponding growth rates for combined regional values were two per cent and 17.7 per cent, respectively.

Dwelling values rose in every capital city across the month, with the pace of increase ranging from 0.2 per cent in Perth to three per cent in Hobart.

House values continue to outperform unit values, with the former up 15.6 per cent over the year compared to a 6.8 per cent gain for the latter.

Auction clearance rates remain elevated, although down from their February 2021 peak.

Sales volumes have also remained strong through to the end of the financial year. CoreLogic estimates that in the year to June, there were approximately 582,900 transactions nationally, the highest annual sales volume observed since February 2004.

Why it matters:

Despite COVID-19 (but driven by the policy response to the pandemic with state and federal government initiatives targeting the housing market, ample fiscal support for incomes and the RBA delivering record low interest rates) national dwelling values ended the financial year up more than 13 per cent with capital city values up more than 12 per cent.

CoreLogic reckons that there are some signs of easing momentum in the market, noting that while June’s monthly growth in national values of 1.9 per cent was significantly above the decade average of 0.4 per cent it was also down from May’s 2.3 per cent and March’s 2.8 per cent increases. Rising prices are themselves part of the story, as they squeeze affordability. State lockdowns will also have an impact on the market, although here CoreLogic notes that short (‘circuit-breaker’) lockdowns mainly impact transaction activity with short, sharp falls in sales and listings followed by swift rebounds but with little impact on prices. Longer lockdowns, however, would likely have a greater impact.

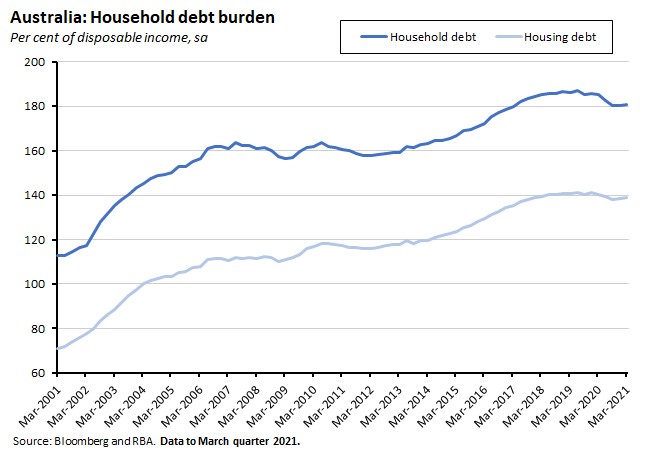

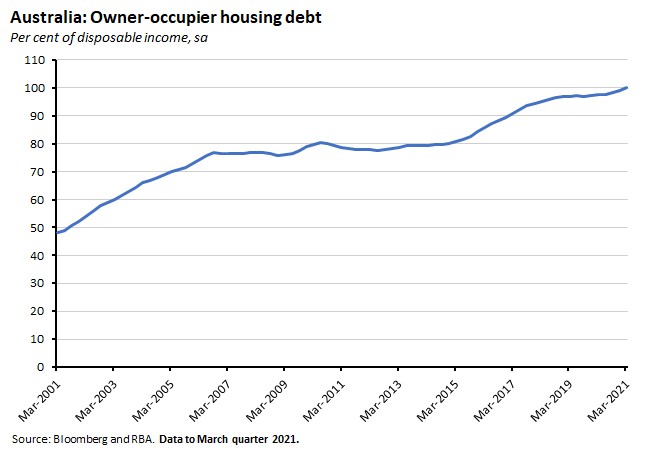

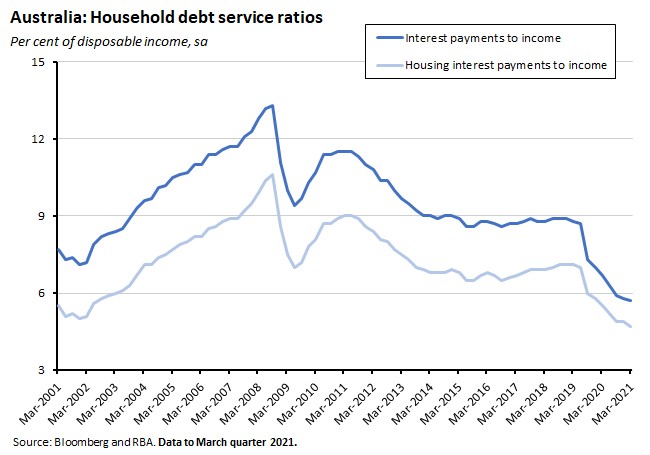

Last week’s data on household finance and wealth showed that while household debt burdens are still below their June quarter 2019 peaks, they did edge up in the March 2021 quarter of this year.

And in the case of owner-occupier housing debt, the sector that has led much of the current boom, the ratio of debt to disposable income hit a new record in the first quarter of this year.

Still, for now, low borrowing costs mean that debt service burdens remain subdued.

What happened:

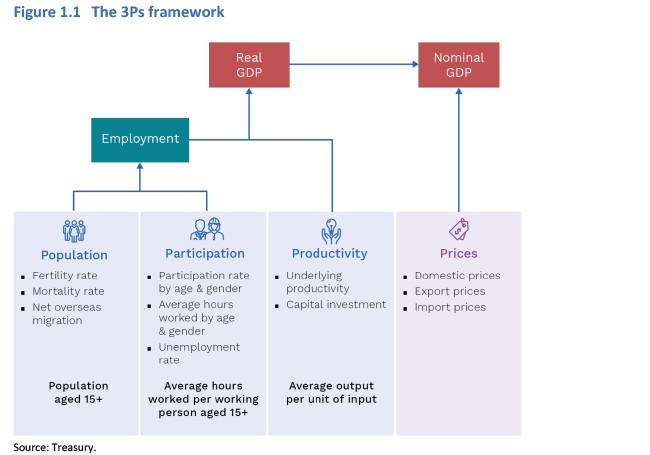

The Treasurer released Australia’s fifth intergenerational report (IGR 2021). The IGR series began in 2002 with subsequent reports released in 2007, 2010 and 2015. The latest report was originally due in 2020 but delayed by the pandemic. The IGR is intended to analyse ‘the long-term sustainability of current policies and how demographic, technological and other structural trends may affect the economy and the budget over the next 40 years.’ To do this, the projections take current policy settings and combine them with a range of demographic and economic projections based on some combination of historical averages and/or long-term trends. In the case of IGR 2021 that means combining the effects of pre-existing structural trends such as population ageing with what are judged to be the persistent effects of the pandemic, primarily the impact of sharply lower net overseas migration (NOM).

The basic analytical framework for the IGR rests on the ‘three Ps’ of Population (the number of people in the working age population), Participation (the share of those who work and their working hours) and labour Productivity (output produced per hour worked) which together drive long-run trends in the economy’s potential output (GDP).

Population

Australia’s population has grown at an annual average rate of 1.4 per cent over the past 40 years, but the impact of pandemic-driven restrictions on NOM is expected to see population growth slump to a low of just 0.1 per cent in 2020-21, the slowest rate in more than a century. IGR 2021 then assumes that population growth will recover to 1.3 per cent a year by 2023-24 before gradually slowing, falling to 0.8 per cent a year by 2060-61 as the contribution from natural increase declines.

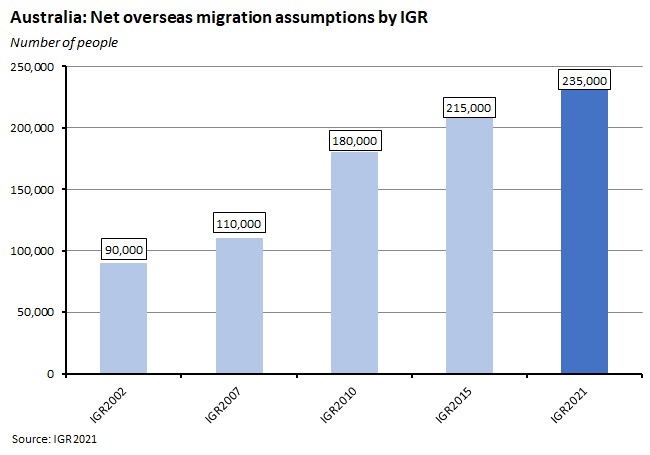

Post-pandemic, the IGR assumes that the level of NOM recovers and then remains fixed at 235,000 people per year from 2024-25. The level of permanent migration is assumed to be unchanged at 190,000 people per year from 2024-25, plus 13,750 people per year under the humanitarian program, with the balance made up by temporary migration. With no change in levels, the share of total population growth driven by NOM rises from around 60 per cent over the past decade to around 74 per cent by 2060-61.

That assumption of 235,000 people for NOM is in line with current policy settings, although a look back at previous IGRs shows that in practice the number of migrants has risen in each subsequent report.

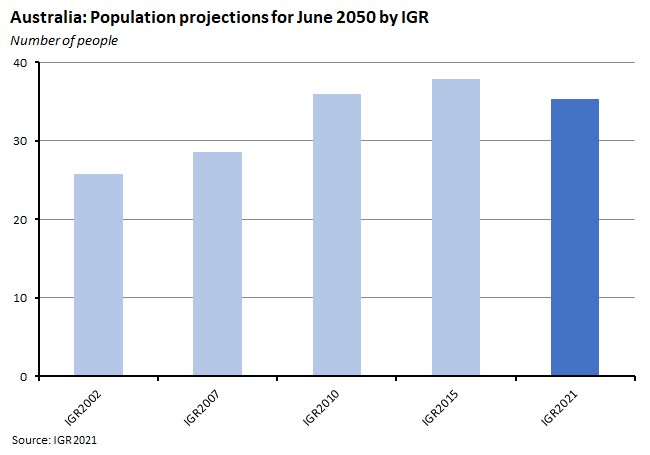

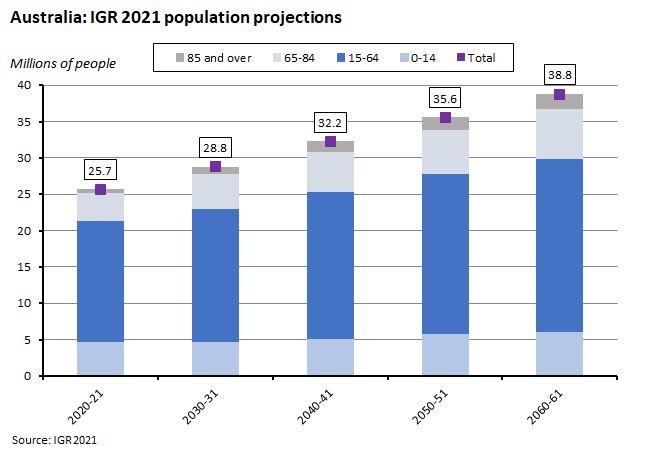

Based on these underlying assumptions, Australia’s total population is projected to reach 38.8 million by 2060-61. That puts the projected increase in population on a lower trajectory than in either IGR2010 or IGR2015 but still well above the forecasts in IGR2002 and IGR2007.

This marks the first downward revision to Australia’s forecast future population in an IGR and mostly reflects the COVID-19 impact on NOM along with the combined effects of a temporary decline in the total fertility rate (TFR) driven by the pandemic (the TFR is forecast to fall from 1.65 babies per woman in 2019-20 to 1.58 in 2021-22 before temporarily rising to 1.69 in 2023-24) together with a lower projected long-term TFR of 1.62 babies per woman, down from the 1.9 TFR rate assumed by IGR 2015.

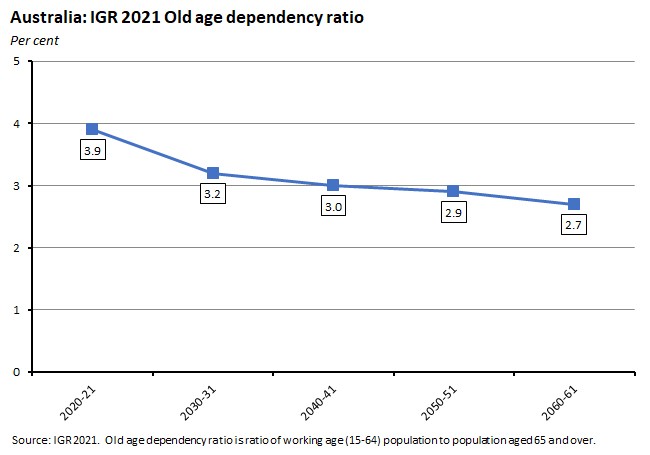

Rising life expectancy at birth plus falling fertility rates mean that from 2019-20 to 2060-61 the number of people aged 65 and older will double to 8.9 million and their share of the population will rise from 16 per cent to 23 per cent. The old age dependency ratio (the ratio of working age people to those over 65) is expected to fall from almost four in 2019-20 to 2.7 by 2060-61.

The IGR also offers an alternative population scenario under which NOM is held at a constant 0.82 per cent of the population, which would see the absolute number for NOM rise to 327,000 people by 2060-61. That in turn would see a total Australian population of 40.5 million by the end of the projection period, or 1.7 million more than the baseline projection. Given that migrants are on average younger than the overall population, that would also increase the size of the working age population and delay the impact of population ageing.

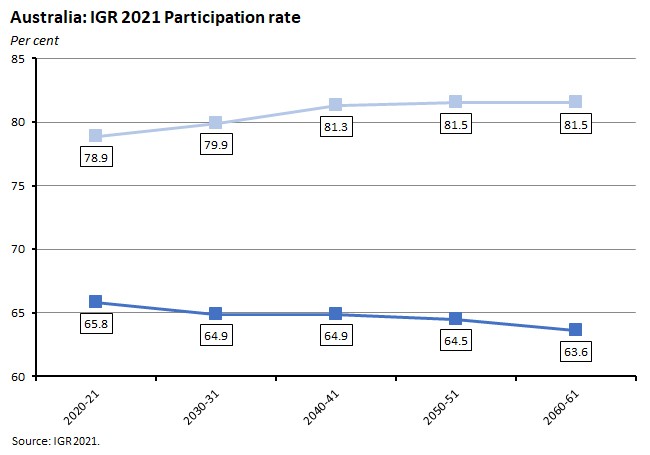

Participation

In March this year, the participation rate reached a record high of 66.3 per cent. IGR 2021 projects the participation rate to fall to 63.6 per cent by 2060-61 as a negative effect of ageing on participation is only partially offset by higher participation rates for some groups (particularly for women aged 40 years and over). Note, however, that projections for the participation rate have been revised upwards in every successive IGR including the current one.

Along with the participation rate, the unemployment rate also influences the supply of labour that is actually deployed by the economy. IGR 2021 assumes that the unemployment rate falls to 4.75 per cent – consistent with Treasury’s latest estimates for the non-accelerating inflation rate of unemployment (NAIRU) – and remains there.

Finally, potential GDP is not only a product of how many people work, but also of how much each person works on average. The average number of hours worked per week per workers fell significantly in 2019-20 due to the impact of the pandemic, but pre-pandemic (in 2018-19) was around 32. The IGR assumes that this rate falls to 31 by 2060-61 due to a continued rise in the share of part-time employment, an increase in the share of women in the labour force, and an increase in the share of older workers.

Productivity

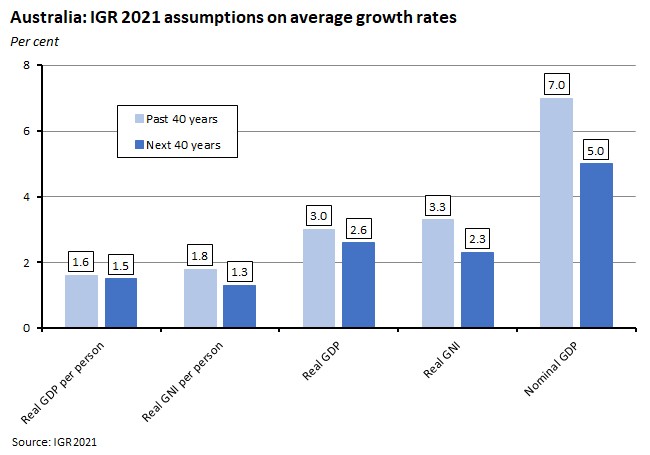

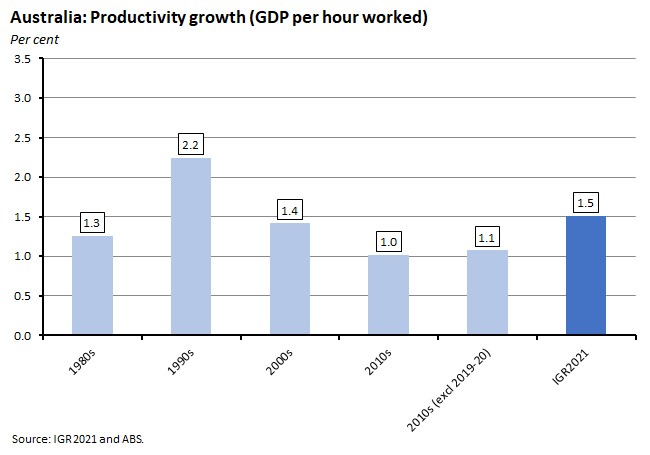

Labour productivity measures the amount of goods and services produced per hour of work. Over the past three decades it has been the source of more than 80 per cent of the growth in Australian living standards (measured as real gross national income per person). The IGR assumes that labour productivity growth will converge to the average rate of growth of labour productivity over the 30 years to 2018-19, which was 1.5 per cent. That convergence is assumed to take place over the next ten years.

IGR 2021’s assumption of 1.5 per cent productivity growth in the long term is faster than the average rate of productivity growth of 1.2 per cent recorded over the most recent complete productivity cycle, which ran from 2011-12 to 2017-18. The report includes a sensitivity analysis that looks at the impact of assuming productivity growth converges to 1.2 per cent instead of 1.5 per cent, and finds that real and nominal GDP are both about 9.5 per cent lower by 2060-61, nominal gross national income per person is $32,000 lower, the underlying cash deficit is swollen by an additional 2.2 percentage points of GDP and net debt is 22.7 percentage points of GDP higher.

Potential output

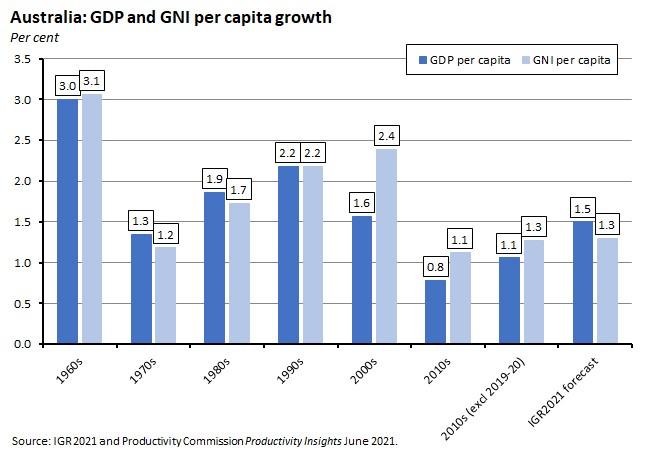

Based on the IGR’s assumptions about the three Ps, Australia’s real GDP is forecast to grow at an average annual rate of 2.6 per cent from 2020-21 to 2060-61, implying a 0.4 percentage point slowdown relative to GDP growth over the past 40 years. Most of that decline is driven by the assumed slowdown in population growth.

Real GDP per person is assumed to grow at 1.5 per cent per year on average over the next 40 years while average annual growth in real gross national income per person is expected to be a little lower, at 1.3 per cent, reflecting conservative assumptions about commodity prices and the terms of trade.

Nominal GDP (real GDP plus price changes) is expected to grow at an average of five per cent per annum over the 40 years covered by IGR2021, down from seven per cent over the past 40 years.

Implications for the Budget

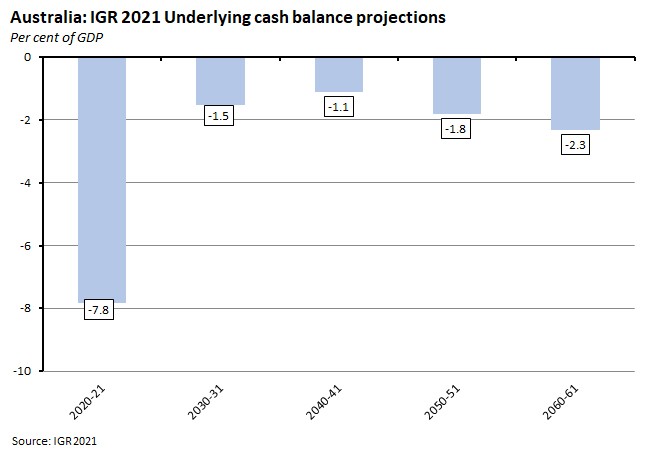

Based on these assumptions and current policy settings, Australia’s underlying cash balance is projected to be in deficit over the next 40 years. The fiscal trajectory first sees the budget moving from an estimated shortfall of 7.8 per cent of GDP in 2020-21 to a deficit of 0.7 per cent of GDP in 2036-37 as the deficit-expanding effects of the pandemic gradually fade. But then the underlying cash deficit is projected to widen again, rising to 2.3 per cent of GDP by 2060-61. That second phase of increase comes because while tax receipts are projected to hit the government’s tax to GDP cap of 23.9 per cent in 2035-36, government payments as a share of GDP are expected to continue to grow, driven by increases in health, aged care and interest payments.

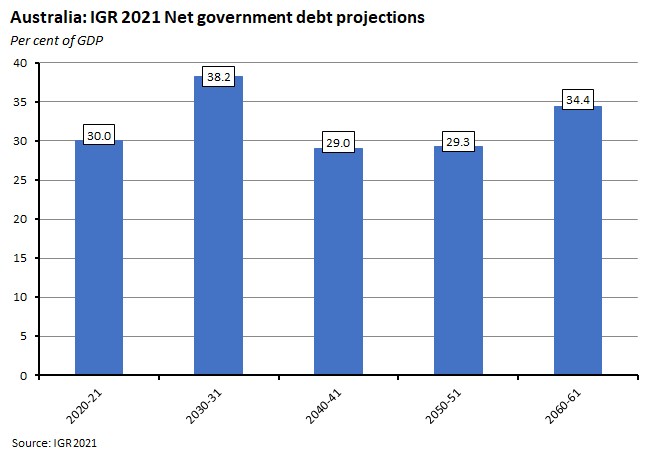

Net debt is projected to peak at 40.9 per cent of GDP in 2024-25 before falling to 28.2 per cent of GDP in 2044-45 and then increasing again to 34.4 per cent of GDP by 2060-61. Gross debt is projected to peak at 51.5 per cent of GDP in 2028-29 and be at 40.8 per cent of GDP by 2060-61.

Note that these debt projections assume that the yield on ten-year government debt remains at or below the rate of economic growth over the next 40 years. That’s broadly in line with past experience, with yields on Australian Government 10-year bonds having been lower than nominal GDP growth in 31 of the last 50 years, averaging 0.6 percentage points lower over the period.

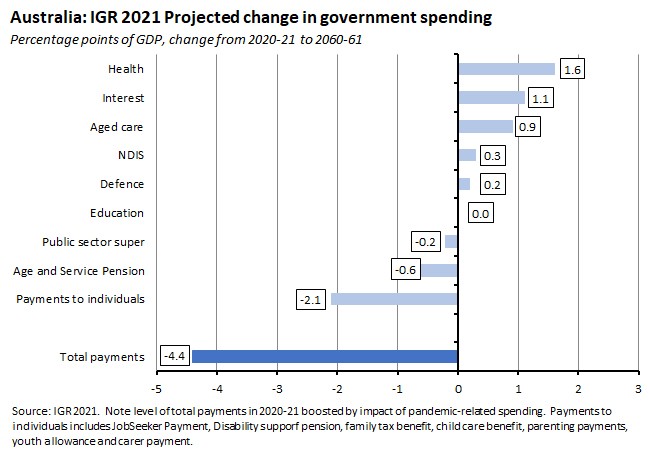

Government spending

Total government spending as a share of GDP is expected to be 32.1 per cent of GDP in 2020-21, reflecting the extensive fiscal response to the pandemic. It is then expected to fall to 26.2 per cent by 2024-25 as the economy recovers. Thereafter, rising payments see spending rise to 27.7 per cent of GDP by 2060-61.

Three main factors are behind the anticipated increase in payments: health care, aged care and debt service payments, with health care the most important. Health spending is projected to rise from 4.6 per cent of GDP in 2021-22 to 6.2 per cent by the end of the projection period, and from 19 per cent of total government spending to 26 per cent. The key drivers here are a mix of demographic (population growth, population ageing) and non-demographic (technology, changing consumer preferences and rising incomes) with the latter accounting for just over half the increase. Aged care payments are also expected to grow, rising from 1.2 per cent of GDP to 2.1 per cent over the same period. Both demographic factors (a doubling in the number of people aged 70 or over across the next 40 years) and non-demographic factors (changing consumer preferences, higher real incomes and the changing incidence of frailty and disease among users of the aged care system) are again at work. Finally, interest payments are expected to rise from 0.8 per cent to 1.9 per cent of GDP.

There will also be some (partially) offsetting falls in the share of government spending on age and service pensions, other payments to individuals, and education. The first of these reflects the impact of the superannuation system on reduced dependence on the age pension, which sees the share of older Australians receiving the age pension decline even as their numbers increase. At the same time, however, by around 2040 the cost of superannuation tax concessions will exceed the cost of age pension expenditure, and as a result, the total cost of age pension expenditure plus superannuation tax concessions will increase from around 4.5 per cent of GDP in 2020-21 to five per cent of GDP in 2060-61. The decrease in spending on education as a share of GDP is mainly a product of slowing population growth and demographic change, with real spending per person expected to rise.

Defence spending is projected to increase from 2.1 per cent of GDP in 2020-21 to around 2.3 per cent of GDP in 2031-31 and then to grow in line with the economy.

In real terms, total government payments are forecast to grow at an average annual rate of 2.5 per cent from 2021-22 to 2060-61, down from an average rate of 3.4 per cent over the past 40 years.

Government receipts

IGR 2021 assumes that the government’s tax to GDP cap of 23.9 per cent is maintained over the projection period. The pandemic triggered a sharp fall in the tax to GDP ratio, which is expected to fall to a low of 20.9 per cent in 2021-22, but then rise to hit the tax cap by 2035-36.

Why it matters:

The IGR is an interesting attempt to push the government of the day to think beyond the tyranny of Australia’s short electoral cycle and consider the medium-term. That has the obvious and important advantage that it encourages a focus on the longer-term implications of current policy settings. But it has the equally obvious and important shortcoming that our ability to say anything with confidence about the global and Australian economies four decades from now is incredibly limited. Consider, for example, just how much both have changed over the four decades between 1980-81 and 2020-21 and the impossibility of forecasting most of those changes. Which is why the report itself explains that it is not a forecast but rather ‘one possible picture of the future based on expected structural settings and existing policy settings…the report presents a world that could be, rather than will be.’

With that key caveat in mind, one main focus of the current IGR is the interaction between the long-running concerns that motivated the original 2002 edition of the report (primarily the challenges of an ageing population) with the impact of the pandemic on the trajectory of the economy. That interaction shows up in terms of changes to population and demographic projections that then have implications for growth and the budget. Most strikingly, and for the first time in an IGR, the population projection has been revised down in response to the pandemic’s hit to NOM. IGR 2021 also projects an older population than its predecessors. Long-run GDP growth has likewise been revised down while long-run debt and deficit projections have been increased. In summary, IGR 2021 now envisions a somewhat smaller, older, poorer and more indebted Australia than was projected by its predecessor (IGR 2015) and relative to what we might have expected pre-pandemic.

A second focus of the report is the critical role played by productivity growth in driving future prosperity. Last year, the Productivity Commission reminded us that almost all of Australia’s growth in material living standards (GDP per capita) since Federation has been attributable to labour productivity growth. As noted above, the baseline projection in IGR 2021 assumes that, after ten years, the average annual rate of labour productivity growth will converge to its long-term average rate of 1.5 per cent, although there is also an alternative scenario where productivity growth instead converges to a 1.2 per cent. That slower productivity growth drags down projected economic growth and incomes and pushes up debt and deficits to a significant degree, highlighting the critical importance of this assumption. And as many responses to the report have noted already, that baseline assumption of 1.5 per cent productivity growth looks optimistic relative to recent experience. Productivity growth over the past decade has been closer to one per cent, and over the past five years it has run at just 0.5 per cent, all of which makes even the downside scenario o f 1.2 per cent appear optimistic.

Our recent weak productivity performance means that Australia’s economic growth performance has also disappointed. Earlier this year, the Productivity Commission noted that the most recent decade of Australian per capita economic growth has been the slowest in at least 60 years, even before taking the impact of the pandemic into account. Slow labour productivity growth has been the main factor here, exacerbated (until recently) by declining terms of trade and labour utilisation rates. Unless Australia can reverse that recent productivity performance, both the IGR baseline and even the weaker alternative productivity growth scenario will be out of reach, with adverse consequences for our future standard of living.

Moreover, even the ‘optimistic’ IGR baseline with its forecast of 1.5 per cent per capita GDP growth would still see us underperform all but the 1970s and the lacklustre 2010s.

Finally, a third feature of IGR2021 worth noting is that the report includes a dedicated chapter on the environment, noting that environmental challenges will affect the economy and budget over the next forty years. Unfortunately, however, it does not attempt to quantify the potential implications.

What happened:

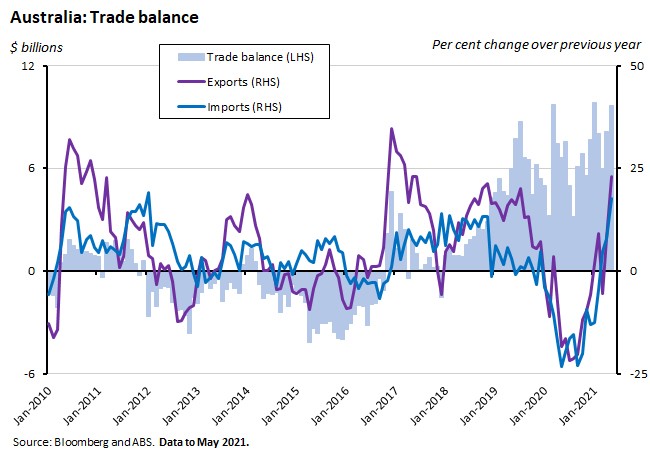

The ABS said that Australia recorded a $9.7 billion trade surplus in May 2021. Exports of goods and services rose six per cent over the month and 23 per cent over the year to $42.2 billion while imports of goods and services were up three per cent month-on-month and more than 17 per cent year-on-year at $32.6 billion.

As flagged by the preliminary merchandise trade results covered last week, metal ores and minerals largely explain the monthly increase in exports and the large trade surplus, with values rising by 11 per cent or $1.8 billion

Why it matters:

May’s results are yet more evidence of how a strong performance by resource exports in general and iron ore in particular continues to drive Australia’s trade position.

What happened:

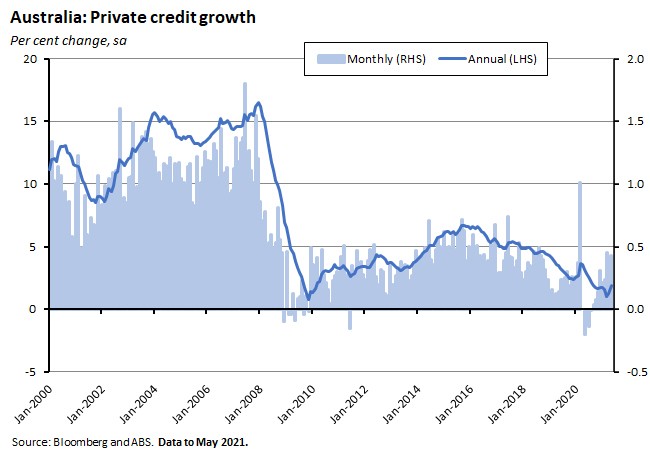

The RBA reported that Australia’s total credit to the private sector rose 0.4 per cent over the month (seasonally adjusted) in May 2021 to be 1.9 per cent higher in year-on-year terms.

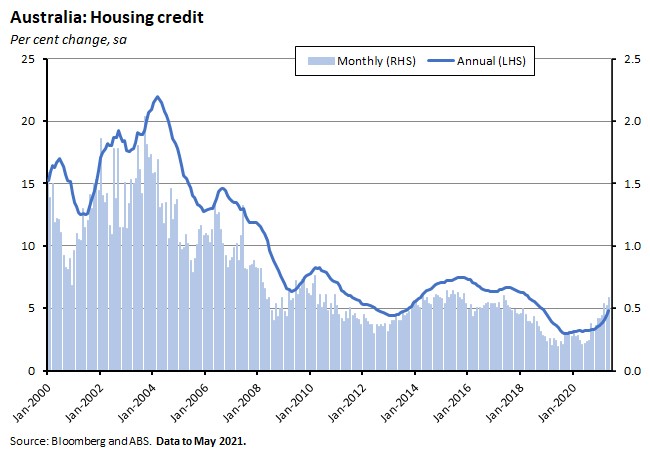

Housing credit rose 0.6 per cent over the month and 4.8 per cent over the year. Loans to owner occupiers were up 0.7 per cent month-on-month and 6.6 per cent year-on-year while loans to investors rose 0.4 per cent month-on-month and 1.6 per cent year-on-year.

Personal credit rose 0.2 per cent over the month but fell 6.4 per cent over the year while credit to business was also up 0.2 per cent in monthly terms and down two per cent on an annual basis.

Why it matters:

Credit growth overall remains relatively subdued in annual terms, with growth supported mainly by housing credit. We know from RBA speeches and the latest quarterly statement from Australia’s Council of Financial Regulators that regulators are keeping a close watch on housing credit developments, with a focus on lending standards and on the level of household debt. In that context, the mix between loans to owner-occupiers and loans to investors is a useful indicator to track alongside the overall growth numbers, with recent months indicating a return of investor interest.

What happened:

The ANZ Roy Morgan Index of Consumer Confidence edged down 0.2 per cent to an index value of 112.2 for the week ending 26-27 June.

Four of the five subindices fell over the week: ‘Current economic conditions’ dropped 3.4 per cent, ‘future economic conditions’ fell 1.7 per cent, ‘current financial conditions’ declined 1.3 per cent, and ‘future economic conditions’ fell 1.7 per cent. ‘Time to buy a major household item’ rose 3.5 per cent.

Why it matters:

The marginal fall in overall consumer confidence reflected diverging state experiences with COVID-19 and lockdowns, with confidence in Sydney down 4.6 per cent and in regional NSW down 6.6 per cent but confidence in Melbourne up 2.4 per cent.

What I’ve been reading . . .

The Treasurer introduces IGR 2021.

A new Treasury working paper looks at product market power and its implications for the Australian economy. The paper measures market power by looking at firms’ mark-ups (that is, the ratio of the firm’s price to its marginal cost – which has to be estimated – as market power will allow firms to set prices above marginal cost). It finds that mark-ups in Australia have increased by around five per cent on average since the mid-2000s, reflecting fairly broad-based rises across most firms. That scale of increase is slightly smaller than the average increase found in other advanced economies which the paper suggests could reflect Australia’s relatively high ranking in OECD measures of product market regulation. The paper’s conclusion is that firms’ mark-ups and market power have increased in Australia in the non-finance market sector since the mid-2000s, and that this in turn has had adverse implications for dynamism and labour productivity growth. This effect is estimated to explain at least one fifth of the observed slowdown in Australian labour productivity since 2012, with a caveat that the actual effect is likely larger, given that the estimate does not account for other potential negative effects of increased market power, such as decreased incentives for innovation and within-firm productivity growth.

The BCA’s new report, Living on borrowed time. It highlights eight ‘forces of change’ (the rise of Asia, advances in digital and technology, changing business models, the changing nature of work, exposure to climate risk, rising geopolitical volatility, debt and deficits and pressurised tax systems) and proposes economic diversification and the construction of a low carbon economy as responses.

More from Grattan on Australia’s vaccine rollout.

Resources and Energy Quarterly (REQ) June 2021 from the Department of Industry. According to the latest REQ, Australia’s export earnings are estimated to have hit a record $310 billion in 2020–21, and are expected to rise another eight per cent to $334 billion in 2021–22 before falling back to $304 billion in 2022–23. The 2021-22 and 2022-23 forecasts represent upgrades of $41 billion and $9 billion, respectively, to the forecasts presented in the March 2021 REQ. As noted above in the review of the May trade data, exports of iron ore are at the heart of the story: the June 2021 REQ estimates that earnings sin 2020-21 urged by almost 50 per cent to a record $149 billion, far above the previous high of $103 billion set in 2019–20. An easing in prices from the second half of this year is expected to push iron ore export earnings down to a still very healthy $137 billion in 2021–22, and then to $113 billion by 2022–23. The report also notes that Australia’s resource sector is set to capture the growth in demand for resources used in new and low emission technologies. The REQ does highlight several downside risks to its very strong export earnings forecasts, including the potential for a global inflation spike triggering a sharper than expected tightening of global monetary policies, risk of delays in vaccine rollouts, and the possibility of further disruption in bilateral trade with China.

NAB Economics investigates why the Australian dollar isn’t higher given the current strength in commodity prices, and whether the currency could repeat the big surge it experienced during the commodity cycle that peaked in 2011. Unlikely, is the judgment here, given that: a new ‘green’ commodity supercycle would not have the same implications for Australia given an export mix still dominated by iron ore, coal and gas; there’s little sign of a re-run of the mining investment boom; and likewise no equivalent to the fixed income investment shift that accompanied the previous period of AUD strength.

The latest Lowy poll. Inevitably, much of the media reporting has focussed on the China results, which show trust in China falling to a record low, with only 16 per cent of respondents saying that they trust China ‘a great deal’ or ‘somewhat’ to act responsibly in the world, a seven-point decline from last year and a third of the level in 2018 when a majority of Australians still said they trusted China. Similarly, only ten per cent said they had ‘some’ or ‘a lot’ of confidence in China’s President Xi Jinping to ‘do the right thing regarding world affairs’. And 63 per cent said they see China as ‘more of a security threat to Australia’ compared to the 34 per cent that said China was ‘more of an economic partner to Australia.’ The Lowy Interpreter also charts the Australia-China relationship over time as captured by successive Institute polling. On other topics, 95 per cent of respondents reckon Australia has handled the pandemic ‘very well’ or ‘fairly well,’ and the Federal Government is credited for its policy response with a strong score of 7.6 out of 10 vs a score of just 4.6 out of ten for the approach to climate change.

John Hawkins cautions against placing too much faith in estimates of indirect jobs, using recent claims about the mining industry as a case study.

The ABS on Household financial resources. Average Australian household wealth was $1.02 million in the December 2020 quarter while median household wealth was $632,200.

Results from the latest ABS General Social Survey.

An RBA research paper examines survey-based evidence on participation and diversity trends in the study of economics at the High School level.

A big (more than 400 pages) new World Bank publication on Global productivity: trends and drivers. The book examines productivity trends since the 1980s, suggesting that productivity growth has become more synchronised, with steeper declines and shallower recoveries, and that productivity growth began slowing long before the pandemic. Some of that slowdown reflects a weakening in some fundamental drivers, including a deceleration in the growth of the working age population, a stabilisation in the level of educational attainment, and a stalling in the growth of global value chains. In addition, adverse shocks such as natural disasters, wars, financial crises and epidemics have all led to weaker productivity growth. For example, during 2000-2018, four major epidemics: SARS (2002-03), MERS (2012), Ebola (2014-15) and Zika (2015-16) had ‘significant and persistent negative effects on productivity’, lowering it by four per cent after three years, mainly through their adverse impact on investment and the labour force due to increased uncertainty, but also by restricting mobility which slowed geographical and sectoral labour reallocation. The COVID-19 pandemic could likewise damage future productivity growth with potential channels including weaker investment and trade (although note that global goods trade has actually bounced back strongly), the erosion of human capital (disruptions to schooling have affected more than 90 per cent of the world’s children), a further slowdown in the rate of labour reallocation from low productivity to high productivity firms, and increased debt burdens for both governments and corporations. On the other hand, there is also scope for offsetting productivity gains including via organisational and technological changes, restructured supply chains, improved (online) education delivery, and digital-led financial development.

A new CEPR-World Bank e-book on the Economics of deep trade agreements (deep trade agreements or DTAs refer to bilateral and regional trade deals that are not focused exclusively or predominantly on trade but instead cover a broader range of policy areas including international investment, cross-border labour flows, intellectual property and environmental measures. One theme here is that because DTAs can provide additional underpinnings for market integration, they can have ‘positive effects on trade and welfare well beyond shallow trade agreements that lower preferential tariffs.’ For similar reasons, they are also less likely to be trade-diverting than trade-only preferential trade deals, since they often include policy areas that are non-discriminatory in nature (for example, rules that increase competition, limit domestic subsidies, and regulate state owned enterprises) and that can also help boost exports of non-members. Another theme is that DTAs could become even more important in a post-COVID world if the pandemic generates greater pressure for more activist trade policies. There is also a risk that these pressures could tilt towards a greater demand for more protectionism in future DTAs, leading to more trade fragmentation.

The Economist magazine has a special report on the Chinese Communist Party at 100.

The Boston Review has a long essay drawing on a new Intellectual Biography of Albert O. Hirschman: ‘If any life’s work could be summed up by the mantra “We don’t know, but let’s give it a try,” it was that of Albert O. Hirschman, one of the most prominent and original social scientists of the second half of the twentieth century…Hirschman theorized a uniquely pragmatic approach to economic management that took surprises for granted…In an era when “crisis” rather than “equilibrium” seems the more obvious tendency of the system, the fascinating experiments of both his life and work may yet have something to teach us.’

Noah Smith thinking about what Joe Studwell’s How Asia Works might have got wrong. If you’re not already familiar with Studwell’s (excellent) book, Smith recommends this recent review which serves as useful pre-reading for the previous link.

Bloomberg Businessweek looks back at the Ever Given saga and tells the story of The Ship that broke International Trade.

The 2021 BIS Annual Economic Report covers the world economy after COVID (‘pandexit’), the distributional impact of monetary policy and central bank digital currencies.

Related, the FT’s Martin Wolf is broadly supportive of the BIS position on monetary policy and inequality. AFR version.

How long-lasting are the economic effects of pandemics?(pdf). 220 years of Swedish data suggest that pandemics have had negative effects on birth rates, death rates and family formation. They have also had a negative short-term effect on the economy while the longer-term effects are less clear although there is some evidence that foreign trade, investment and sovereign debt have suffered from a persistent negative impact. (h/t Marginal Revolution).

Latest news

Already a member?

Login to view this content