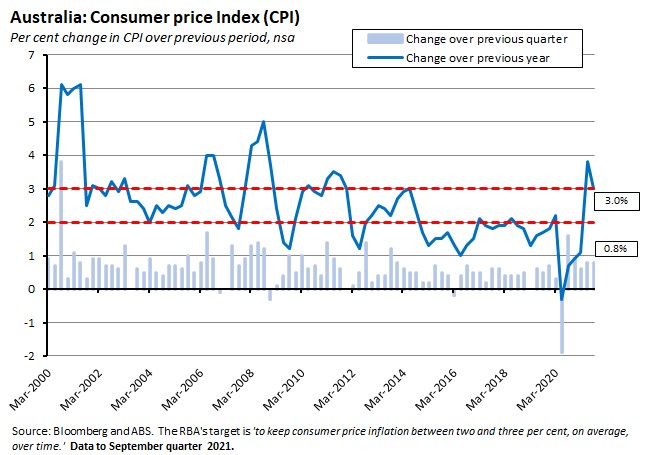

The key data release this week was the third quarter Consumer Price Index (CPI). Attention focused not on the headline rate of inflation – which eased to three per cent year-on-year in the September quarter from 3.8 per cent in the June quarter – but rather on a jump in underlying inflation. The trimmed mean, which is the RBA’s preferred measure of underlying inflation, beat market expectations by rising 0.7 per cent over the quarter and 2.1 per cent over the year.

This marks the first time that this measure has had a ‘two’ in front of it since 2015. Markets have taken this as another signal that inflationary pressures are rising faster than the RBA anticipated and that Martin Place will now have to adjust its timetable for increasing the cash rate accordingly. The RBA will get a chance to respond next week with Tuesday’s monetary policy meeting and Friday’s release of November’s Statement on Monetary Policy. But any radical shift in the central bank’s view seems unlikely.

For more background on inflation developments, please take a look at our new inflation chart pack.

The other big news this week was the government’s announcement that it would seek to deliver zero net carbon emissions by 2050. But while the Long-term Emissions Reduction Plan marks an important political moment, any economic impact seems strictly limited for now: there may perhaps be some modest decline in investor uncertainty as a result of this week’s commitment to a long-term target, but with no major new policies, no major new spending promises, and a continued aversion to pricing carbon, not much else has changed.

This week’s readings include a roundup of early reactions to the Government’s Long-term Emissions Reduction Plan, the latest state of the states, Australia’s experience with tax reform, the case for funding Australian foreign policy, COP26, inflation, the Great Resignation, the real-time revolution in economics and the dogged persistence of the five-year plan.

Listen and subscribe to Dismal Science podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

The ABS said that the Consumer Price Index (CPI) rose 0.8 per cent over the September quarter and was three per cent higher in year-on-year terms.

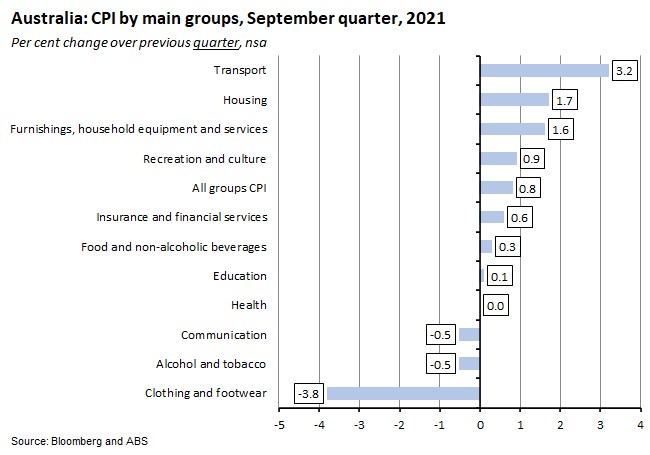

By group, the main price increases over the quarter were for transport (which jumped 3.2 per cent), housing (up a strong 1.7 per cent) and furnishings, household equipment and services (also up a robust 1.6 per cent).

The main drivers of the rise in the transport group were a 7.1 per cent surge in automotive fuel, which powered by rising global oil prices rose to its highest index level in the history of the series, and a 1.4 per cent hike in the price of motor vehicles due to continued strong demand and ongoing supply constraints reflecting the global semi-conductor shortage, COVID-related factory closures, and shipping costs.

The increase in the housing group reflected a large (3.3 per cent) increase in new dwelling purchases by owner-occupiers – the biggest increase since the September quarter of 2000. The ABS said that the rise was due to continued strong demand for housing construction which had enabled builders to pass through higher costs for both materials and labour. The Bureau also noted that government housing construction grants had a smaller impact on new dwelling prices this quarter as the number of grant payments was down on the June quarter.

The key drivers of the increase in the furnishings, household equipment and services group were furniture (up 3.8 per cent) due to the combined effect of strong demand and supply shortages, and childcare (up 2.1 per cent) due to higher fees.

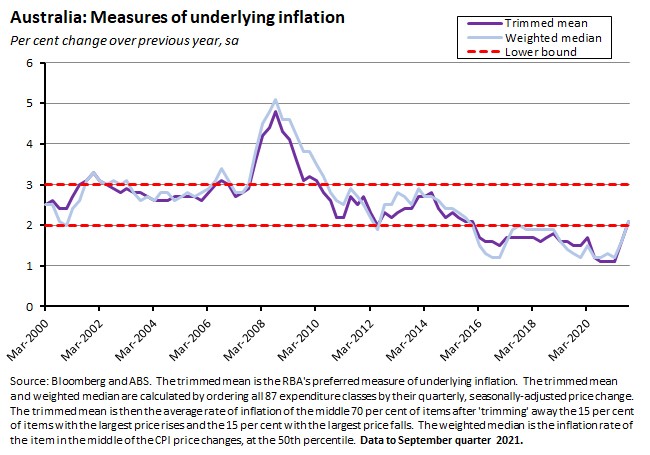

Two key measures of underlying inflation were markedly higher in the September quarter. Both the trimmed mean (the RBA’s preferred measure) and the weighted median rose by 0.7 per cent quarter-on-quarter and 2.1 per cent over the year.

By capital city, the quarterly rate of CPI inflation ranged from a low of 0.3 per cent in Hobart to a high of 1.5 per cent in Darwin, while in year-on-year terms the increases ranged from 2.5 per cent in Adelaide to 5.9 per cent in Darwin. The subdued quarterly price increase in Hobart was partly a function of a 20.8 per cent drop in electricity due to the annual price review and the introduction of a $125 winter energy bill supplement for concession customers, while the increase in Darwin reflected a 13 per cent jump in other financial services following the end of the ‘Territory Homeowner Discount on stamp duty paid’. All cities saw strong increases in automotive fuel (including record highs in Sydney and Melbourne and near-record levels in Brisbane) and in new dwelling purchases (except for Perth).

For more detail and background on recent developments in inflation, inflation expectations and related indicators, please take a look at our new inflation chart pack.

Why it matters:

The headline annual inflation rate of three per cent was exactly in line with market expectations and marked a retreat from the June quarter’s 3.8 per cent rate. But most attention was focused not on the decline in the headline rate but rather on the marked increase in the underlying rate of inflation as captured by the trimmed mean. Here the median forecast had called for a 0.5 per cent quarterly increase and a 1.8 per cent annual rate. Instead, we saw stronger gains of 0.7 per cent and 2.1 per cent, respectively. As a consequence, the annual rate of underlying inflation is now back inside the RBA’s target band (for the headline rate) of two-to-three per cent for the first time following 22 consecutive quarters of sub-two per cent readings, and is at its highest since the September quarter of 2015.

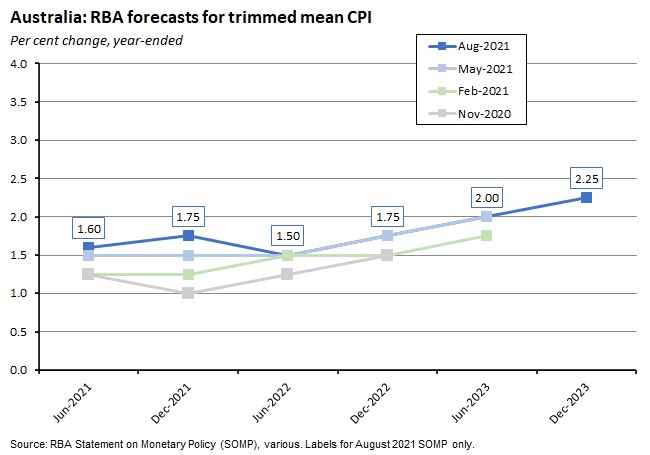

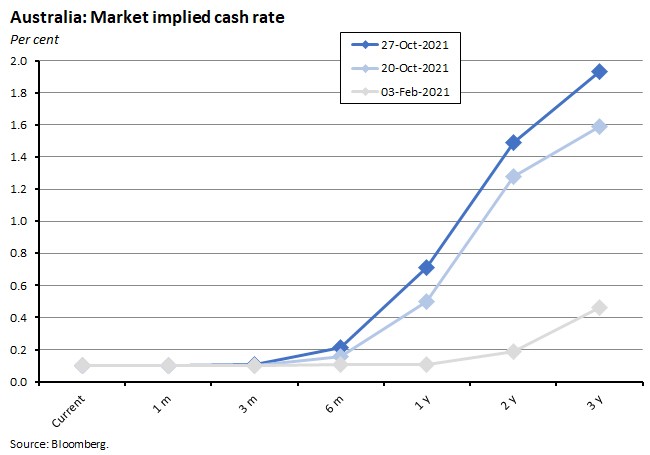

Last week’s note described the disagreement between the RBA and financial markets over the likely timing of any future increase in the cash rate. At the heart of that disagreement is a difference in the likely trajectory of inflation over the coming year. The RBA’s view has been that current price pressures are likely to be temporary, and that in the absence of any sustained response in the form of rising wages, inflation will remain relatively subdued: in August’s Statement on Monetary Policy (SOMP), for example, the baseline forecast had the annual rate of trimmed mean inflation running at 1.75 per cent in the December quarter of this year and only rising to 2.25 per cent by the December quarter of 2023. This forecast helps underpin the RBA’s repeated assertion that a rise in the cash rate will not happen ‘until actual inflation is sustainably within the two to three per cent target range’ and that the ‘central scenario for the economy is that this condition will not be met before 2024.’

In the August SOMP, the RBA predicted that underlying inflation ‘will likely remain subdued over the next few quarters, given the decline in activity in the September quarter and the absence of broad-based inflationary pressures.’ September’s actual result therefore fits somewhat uneasily with that narrative and the November SOMP now looks set to see at least some revision to the forecast inflation profile.

Markets meanwhile seem increasingly convinced that the RBA has got its inflation forecast – and therefore its projections for the cash rate – wrong. Aware that inflationary pressures are on the rise worldwide, they have been betting that inflation here in Australia will similarly surprise on the upside, and that as a result, the RBA will be forced to bring forward the timetable for a normalisation of the cash rate. The third quarter’s stronger-than-expected increase in the trimmed mean has reinforced that belief and one impact of this week’s data was a further increase in the expected profile for the cash rate relative to last week’s already (relatively) hawkish view.

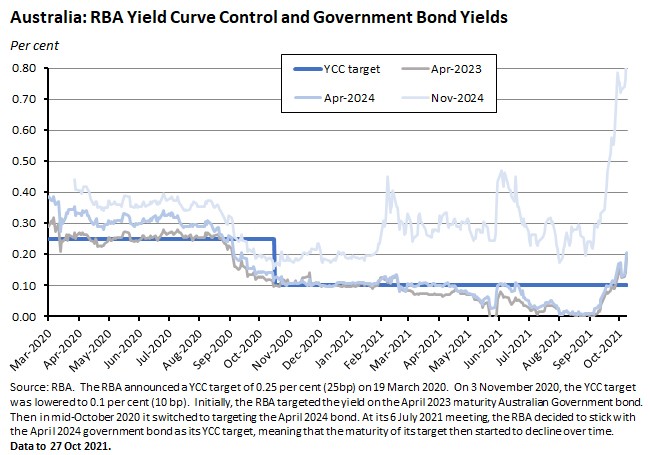

And in another repeat of last week’s developments, markets also again tested the RBA’s yield curve control (YCC) target, pushing the yield on the April 2024 government bond up above the 0.1 per cent target.

There is no doubt, then, that this week’s result has provided more ammunition for the inflation hawks.

Still, it will take more than one quarter’s worth of data to settle the matter. For a start, recall that Australia’s headline inflation rate did not accelerate in the third quarter and actually retreated in annual terms. Second, for now there’s still a reasonable argument to be made that a significant share of the price pressures seen in the latest data should be classified as transitory, driven as they were by supply side issues (increases in the cost of construction due to supply disruptions and shortages, increases in the cost of automobiles for similar reasons) along with higher energy prices. Third, and most importantly, the RBA will still want to see evidence of rising wage pressures before it changes its mind on the likely nature of future inflation dynamics. That makes the upcoming Q3 Wage Price Index (WPI) reading on 17 November of great interest. If wages start to surprise on the upside too, then the case for the inflation hawks will receive a considerable boost.

Before then, however, next Tuesday’s RBA monetary policy meeting and next Friday’s release of the November 2021 SOMP will show how the RBA has incorporated this latest inflation data into its forecasts for the Australian economy.

What happened:

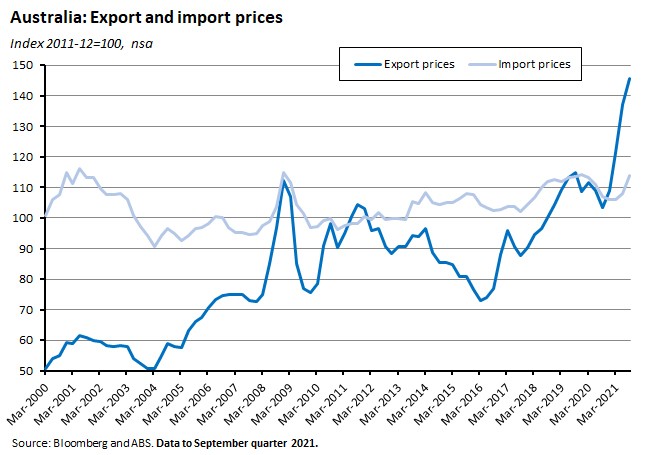

The ABS reported that Australia’s export price index rose 6.2 per cent in the September quarter to be up a hefty 41 per cent over the year. The import price index was up 5.4 per cent quarter-on-quarter and 6.4 per cent year-on-year.

Over the quarter, the rise in the export price index was driven by a 48.1 per cent jump for coal, coke and briquettes, driven by surging global demand; a 39.5 per cent increase for gas, due to the rise in oil-linked contracts capturing rising oil prices; and a 17.1 per cent rise for non-ferrous metals, powered by increased manufacturing demand. Metalliferous ores and metal scrap fell 12.8 per cent due to the fall in China’s demand for iron ore.

The drivers of the rise in the import price index over the quarter included a 12.2 per cent gain for petroleum and petroleum products; a 42.6 per cent surge for fertilisers due to rising energy costs of product, strong global demand, and supply constraints; and a 2.7 per cent increase for road vehicles.

Why it matters:

Australia has been benefiting from rising terms of trade (the ratio of export prices to import prices) over the past year as export prices have outpaced import prices – mainly thanks to surging resource prices – and this has allowed income growth to exceed growth in output boosting not only the government’s tax take but also our living standards (reflected for example in faster growth in real net national disposable income per capita than in GDP per capita). The Q3 export and import price numbers imply that this lift in the terms of trade continued into the third quarter of this year, although the combination of a pick-up in quarterly growth in import prices and a slowdown in quarterly growth in export prices also implies a moderation in this terms of trade effect.

The trade price indices also show the influence of the rise in energy prices that influenced Australia’s third quarter CPI reading (discussed above), with sharp increases in the prices for coal, gas and oil, along with signs of rising input costs more generally.

What happened:

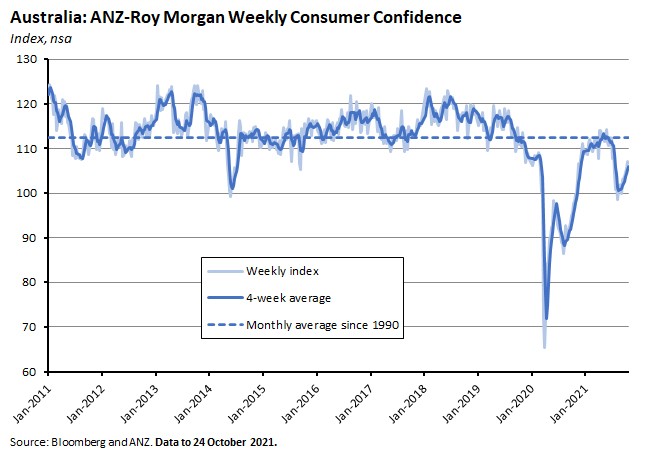

The weekly ANZ-Roy Morgan Consumer Confidence Index fell 0.2 per cent last week.

There was a mixed pattern of rises and falls across the five sub-indices: ‘current financial conditions’ (down 0.2 per cent), ‘future financial conditions’ (down 3.4 per cent) and ‘current economic conditions’ (down 0.3 per cent) all fell, while ‘future economic conditions’ (up 1.3 per cent) and ‘time to buy a major household item’ (up 2.4 per cent) moved in the opposite direction.

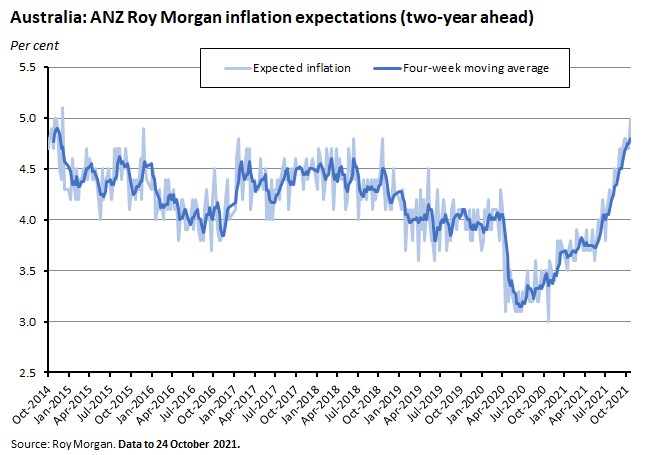

Weekly inflation expectations rose to five per cent, marking that index’s highest value since December 2014.

Why it matters:

Victoria’s exit from lockdown saw confidence in Melbourne lift by 1.2 per cent while sentiment across the state rose by 1.5 per cent. Confidence also edged higher in Queensland (0.7 per cent) and was up strongly in South Australia (10.4 per cent) but the impact of these gains on the national index was offset by drops in New South Wales (down 1.8 per cent) and Western Australia (down 5.9 per cent).

The jump in inflation expectations was notable last week, with ANZ suggesting that rising petrol prices may have influenced household perceptions regarding the rate of price increase.

What happened:

The Australian government said this week that it would seek to deliver net zero carbon emissions by 2050. It said that Australia’s Long Term Emissions Reduction Plan (‘the Plan’) will be based around five principles: (1) technology not taxes; (2) expand choices not mandates; (3) drive down the cost of a range of new low emissions technologies; (4) keep energy prices down with affordable and reliable power; and (5) be accountable for progress.

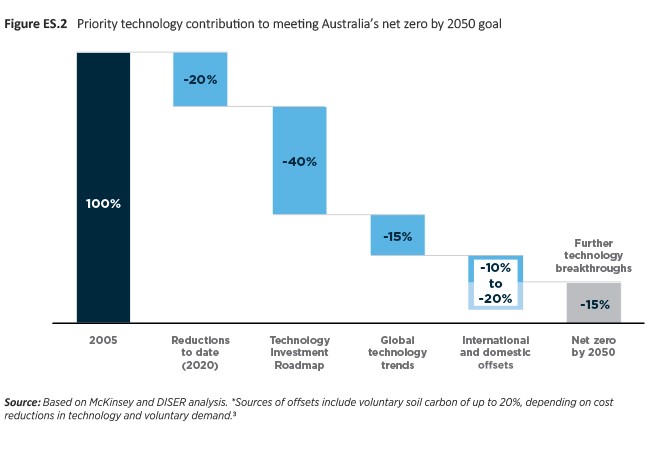

The overwhelming focus is on the role of technology in cutting emissions. Of the total reduction in emissions needed to meet a target of net zero by 2050, the Plan proposes that:

- 20 per cent of the fall required has already been achieved.

- 40 per cent will come from Australia’s Technology Investment Roadmap, which was introduced on 22 September 2020.This is now expected to guide ‘at least $20 billion of Australian Government investment in low emissions technologies over the decade to 2030.’

- 15 per cent from ‘global technology trends.’

- Between 10 and 20 per cent from the purchase of international and domestic offsets.

- 15 per cent from ‘further technological breakthroughs.’

In other words, the Plan assumes that about half the reductions still required will come from the already-existing Technology Investment Roadmap and the other half from a combination of carbon offsets and unspecified technological change.

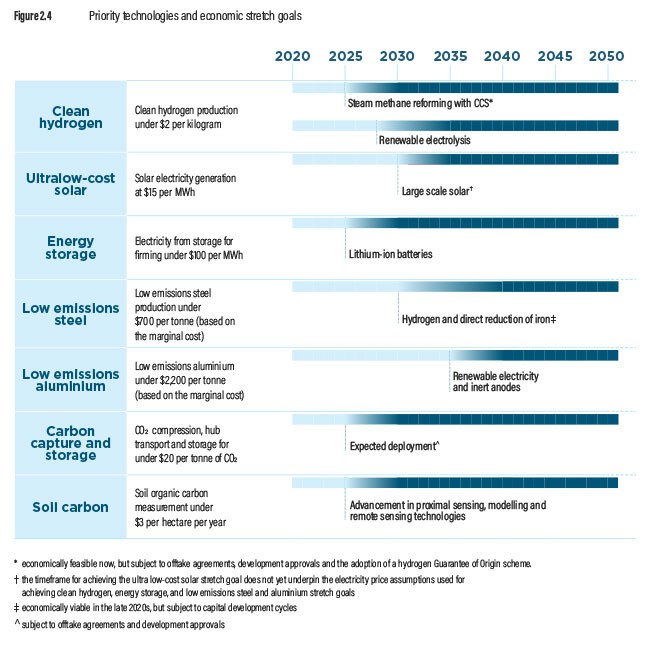

Of the ‘known’ part of the Plan, the Technology Investment Roadmap is ‘a strategy to accelerate development and commercialisation of low emissions technologies’ by making them economically competitive with established technologies. The original roadmap included the following ‘priority stretch goals’:

- Clean hydrogen production at under $2 per kilogram.

- Energy storage: electricity from storage for firming under $100 per MWh. This would enable firmed wind and solar at pricing at or below today's average wholesale electricity price.

- Low carbon materials: low emissions steel production under $900 per tonne (now cut to $700/t) and low emissions aluminium under $2,700 per tonne (now cut to $2,200/t).

- Carbon Capture and Storage (CCS) – CO2 compressions, hub transport and storage for under $20 per tonne of CO2.

- Sequestering carbon in soil or ‘soil carbon’ measurement for under $3 per hectare per year.

To this list, the Plan now adds:

- Ultra-low-cost solar electricity generation at $15 per MWh (that is, solar that produces electricity at about half the current cost).

The original September 2020 Technology Roadmap promised Government investment of around $18 billion in low emissions technologies over the decade to 2030 which was to ‘catalyse $3-$5 dollar of new investment for each dollar of commonwealth funding, to achieve $50 billion - $100 billion in new investment overall.’ Funding for the Roadmap comes from money already committed to existing initiatives including $10 billion for the Clean Energy Finance Corporation (CEFC), more than $1.4 billion for the Australian Renewable Energy Agency (ARENA) and $2.5 billion for projects through the Clean Energy Regulator (CER)’s Emissions Reduction Fund (Australia’s carbon offset fund) and $2 billion for further abatement through the CER’s Climate Solutions Fund.

Why it matters:

The main impact of the new Long-Term Emissions Reduction Plan is political: it marks a (partial?) end to the so-called carbon wars that have distorted Australian politics, forestalled the development of a sensible and durable suite of climate and energy policies, and undermined the investment climate. It – potentially – marks an end to the carbon wars in that there is now at least a degree of political and policy consensus around the long-term target of net zero carbon emissions by 2050. But it may prove to be only a partial end as there is as yet no accompanying consensus on the policies that will be needed to meet that target, no agreement on shorter-term or intermediate targets and trajectories, and still an opportunity for political discord to continue over some or all of those differences.

The economic impact appears much more limited. Granted, an agreed commitment to that long-term goal by 2050 should bring some benefit in terms of lower uncertainty for investors and businesses. But any such fall is likely to be pretty modest, given that the continued uncertainty around the policy framework itself remains significant. That’s particularly the case since this week’s plan included no major new policies and no major new funding, resting instead on the assumption that a combination of existing programs, future technological developments, associated price falls in those technologies, and the resultant shift in incentives will deliver all of the heavy lifting required.

Completely unsurprisingly, it also persists with the aversion to adopting a market-based approach to climate policy based around an explicit carbon pricing framework, preferring instead to stick with the current command and control, picking winners model.

This week’s readings (below) contain a selection of initial responses to the Plan.

What I’ve been reading . . .

A selection of views and responses to the Government’s announcement of its net zero emissions by 2050 target:

- The Business Council of Australia welcomes the chance to ‘draw a line under the last decade of division and get on with the task of transitioning to a low emissions economy.’

- The Ai Group reckons that the ‘decision to adopt a formal economy-wide target of net zero emissions by 2050 will deliver an immediate boost to Australia’s transition, but a lot more work will be needed to flesh out the plan.’

- The Investor Group on Climate Change says the ‘commitment to net zero emissions is an important long-term signal to investors’, but warns that ‘the lack of a clear and ambitious 2030 target…will continue to hinder the orderly transition to net zero and frustrate investors’ ability to invest in climate solutions across Australia.’

- Stephen Hamilton in the AFR argues that that this isn’t really a plan at all, involving as it does an ‘explicit commitment to achieve net zero by 2050 without altering existing policy settings one iota.’

- Grattan’s Tony Wood judges that the commitment to net zero by 2050 is ‘a major breakthrough in Australia’s climate war, and…should be warmly welcomed’ but argues that it also comes with a credibility deficit, in part because of the combination of a heavy reliance on technology and the ‘idea the technologies will be cost-free and adopted by Australian households and businesses is dangerously close to magic pudding territory.’

- CommSec’s latest State of the States again ranks Tasmania in first place.

- A new FAQ from the ABS on the measurement of housing in the CPI and cost of living indices.

- Also from the ABS, Jobs in Australia. Details on the number and nature of filled jobs, the people who hold them and their employers for the period 2014-15 to 2018-19.

- The RBA Governor on Australia’s experience with central bank independence, mandates and policies.

- This working paper from the Tax and Transfer Policy Institute reviews Australia’s experience with tax reform over the past 20 years and concludes that it is best described as ‘lacklustre.’ It also warns that the challenges ahead are ‘daunting’.

- Peter Martin on the capital gains tax and house prices.

- The latest Australian Innovation System Monitor from the Department of Industry.

- In the AFR, Gyngell and McCarthy make the case for a greater investment in foreign policy.

- Bloomberg Green has a roundup on COP26.

- Another Martin Wolf column in the FT on COP26 to follow last week’s one, this time looking at what should be the minimum level of aspiration for the Glasgow summit. AFR version.

- The OECD on carbon pricing in the G20: almost half (49 per cent) of all energy related emissions in G20 economies are now covered by a carbon price.

- A WSJ long read examines how China’s ambitious climate goals are colliding with the reality of an economy that is still 56 per cent powered by coal.

- BIS research on labour markets and inflation after the pandemic.

- Goodhart and Pradhan explore what happens if inflation turns out to be persistently higher for longer.

- Related, why not to worry about hyperinflation (but still be concerned about inflation).

- Lawrence Katz Q&A on the Great Resignation: the US has ‘met a once-in-a-generation “take this job and shove it” moment’.

- INET interview with Jim Chanos on China’s ‘leveraged prosperity model.’

- Nice graphic: the biggest companies by market cap in 60 countries.

- The Economist magazine on the real-time revolution in economics.

- The persistence of the five-year plan.

Latest news

Already a member?

Login to view this content