A speech on monetary policy and the Australian economy by RBA Deputy Governor Guy Debelle has prompted some central bank watchers to predict rate cuts and the introduction of quantitative easing before year-end and possibly as early as next month’s budget-day Board meeting.

The Treasurer has set out a new fiscal strategy for the government which pledges to avoid a premature fiscal tightening that would slow the recovery, recognises the fiscal space provided by record low borrowing costs and introduces a form of fiscal forward guidance linking the budgetary outlook to the unemployment rate. ‘Flash’ PMI estimates suggest that Australia’s business sector (just) returned to growth this month. The preliminary estimate for retail sales in August fell over the month, pulled down by a sharp contraction in Victoria and a small decline across the rest of Australia. In contrast to last week’s surprisingly strong August labour force report, the latest payroll numbers continue to suggest that the national recovery in employment has stalled, although there are large differences in performance across the states. The number of JobSeeker and Youth allowance recipients remained above 1.6 million in August. The weekly measure of consumer sentiment rose for a third consecutive week, but is still at levels last seen at the peak of the global financial crisis. The latest monthly survey of economic forecasters sees the median forecast for GDP in 2020 unchanged, with an anticipated contraction of 3.9 per cent for this year, while consensus expectations for growth next year have been trimmed to 2.7 per cent.

This week’s readings include the Productivity Commission on the importance of the supply side in any post-COVID recovery, new business survey results from the ABS, a spot of RBA-bashing, the global race for a vaccine, the new geopolitics of energy, research on the impact of higher unemployment benefits during the pandemic, more on the economics of WFH, and the perils of meritocracy. The weekly will take a break for the school holidays next week. The following week will see the release of the Federal Budget with an immediate take for AICD members on budget night followed by a webinar on 8 October.

What I’ve been following in Australia . . .

What happened:

RBA Deputy Governor Guy Debelle gave a speech on 22 September on the Australian economy and monetary policy.

In terms of the economic outlook, Debelle said that – despite the surprisingly low unemployment rate in August – the RBA still thinks ‘the recovery in the labour market is likely to be bumpy and uneven and we still expect the unemployment rate to rise from here.’ With regard to inflation, Debelle added that he did ‘not see there is any risk of a sustained rise in inflation while there remains considerable spare capacity in the economy. In particular, the high unemployment rate will mean that wage growth…will remain subdued. As wage costs are a major factor affecting prices, inflation will remain contained for some time.’ In terms of the overall trajectory of the economy, the speech characterised the recovery not as ‘a rapid bounce’ but rather ‘more of a slow grind’, arguing that ‘the shortfall in demand that occurs in recessionary conditions…will be a significant brake on the recovery. Until households and businesses are confident about future demand and income, they will be reluctant to spend and invest.’

The speech also reviewed the options for future monetary policy action, with the deputy governor conceding that since ‘the outlook for inflation and employment is not consistent with the Bank's objectives over the period ahead, the Board continues to assess other policy options.’ In this context, Debelle reviewed a list of options similar to those canvassed by RBA Governor Lowe in his speech of 21 July 2020:

- The RBA could buy additional bonds further out along the yield curve than required by the current three-year yield target, with the aim of further lowering government bond rates at longer maturities. Debelle explained that since ‘very few financial instruments in Australia price off these yields’ the RBA has to date instead focussed on the three-year yield, ‘because Australian financial instruments price predominantly off the shorter end of the curve.’ But he also acknowledged that buying longer-dated debt would still have some additional impact, via a portfolio balance effect. Because the RBA would be buying bonds for cash, it would be exchanging a shorter duration asset (cash) for longer duration assets (bonds). This should incentivise investors to switch into other assets, including potentially foreign assets, to secure their desired duration exposure. That portfolio rebalancing should then in turn lead to lower interest rates on other financial assets and possibly contribute to a lower exchange rate.

- The RBA could intervene in the foreign exchange (FX) market to drive down the value of the Australian dollar. Echoing previous comments by Governor Lowe, Debelle cautioned that ‘with the Australian dollar broadly aligned with its fundamentals, it is not clear this would be effective in the current circumstances.’ That said, he also added that ‘a lower exchange rate would definitely be beneficial for the Australian economy, so we are continuing to watch developments in the foreign exchange market carefully.’

- A third option is that the RBA could ‘lower the current structure of rates in the economy a little more without going into negative territory’. Debelle suggested it would be possible to lower rates on the RBA’s Exchange Settlement (ES) balances (currently at 10bp), the three-year yield target (currently 25 basis points) and the borrowing rate of the Term Fund Facility (TFF, also 25 basis points). Again, this was consistent with Governor Lowe stating back in July that ‘the various interest rates currently at 25 basis points could have been set lower, at say 10 basis points.’

- The final option considered in this week’s speech was the introduction of negative interest rates. Here, Debelle restricted himself to noting that the ‘empirical evidence on negative rates is mixed…In the short-term, they can contribute to a lower exchange rate. In the medium term, the effectiveness can wane including through the effect on the financial system. Negative rates can also encourage more saving as households look to preserve the value of their saving, particularly in an environment where they are already inclined to save rather than spend.’ So, far from a ringing endorsement, although Debelle didn’t repeat Lowe’s mantra that ‘negative interest rates in Australia are extraordinarily unlikely.’

Why it matters:

Debelle’s speech addressed the issue we’ve raised several times in previous editions of the Weekly and on the Dismal Science podcast: given that according to the RBA’s own forecasts it will fail to meet its targets for inflation and unemployment over the coming years, shouldn’t the central bank be doing more? The options set out in this week’s speech – buying more bonds in a form of conventional quantitative easing (QE) to supplement its yield curve control policy, intervention in the FX market, tweaking already-low interest rates, or applying negative interest rates – are not new, and as might be expected, the deputy governor’s assessment largely tracks the previous judgements delivered by the governor. Even so, a perceived change in tone in this week’s speech has prompted several respected central bank watchers to adjust their forecasts for monetary policy.

At the time of writing, both the Westpac and NAB economics teams (along with several other economists) had said that in the aftermath of the speech they now thought further monetary easing from the RBA was on its way, with Westpac predicting a change as early as the 6 October Board meeting (that is, the same day the government will deliver its budget) and NAB suggesting either that meeting or the following Board meeting in November. Both Westpac and NAB see the RBA adopting the kind of policy package that would be consistent with Debelle’s speech this week and Lowe’s earlier July presentation: cuts in the cash rate, the three-year government yield target and the TFF rate from 25 basis points to 10 basis points and the introduction of QE with bond purchases focussed on the five- to ten-year segment of the yield curve.

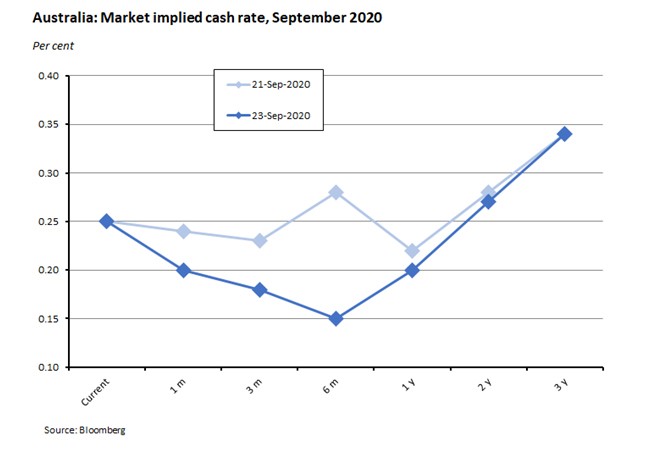

Movements in financial markets have reflected some of the shifting consensus on RBA policy as the profile for the market implied cash rate moved lower in the day following Debelle’s speech relative to the day preceding it.

It’s also worth noting here that Debelle emphasised in the discussion on QE that in his view the current level of government bond rates was ‘not a constraint on the fiscal decisions of the Australian and state governments. They all have strong balance sheets, with debt stocks that are low relative to other jurisdictions, even taking account of the current sizeable fiscal stimulus. The increase in debt is definitely manageable [emphasis added].’ This is important because this view presumably underpins the RBA’s rejection of the argument that it should be doing more to support fiscal policy. In this interpretation, more effort is not currently required, since neither the current level of government bond yields nor the level of government debt serve as a binding constraint on fiscal policy.

Finally, and also on fiscal policy constraints, in a footnote (#10) the deputy governor dismissed concerns over Australia’s sovereign rating arising from higher government debt, noting that ‘there is the possibility of a ratings downgrade from higher debt, but that really only has a political dimension not a financial dimension, as government bond rates would likely be little changed. In any case, a rating agency should not be the determinant of fiscal policy.’

What happened:

The Treasurer gave a fiscal strategy update in a speech to the Australian Chamber of Commerce and Industry.

Josh Frydenberg began by reminding his audience of the unprecedented scale of government intervention triggered by the pandemic, noting that to date the government has announced $314 billion (around 15.8 per cent of GDP) of fiscal support, which has been in addition to an estimated $55 billion (about 2.8 per cent of GDP) in support from the states and territories. He added that Australia had already ‘seen $106 billion in direct fiscal support go out the door in just five months.’ Government borrowing has increased to finance this fiscal largesse, resulting in the Australian Office of Financial Management (AOFM) ‘issuing bonds at a rate of around $4 billion to $5 billion per week’ with around $267 billion of issuance to date since the onset of the crisis.

The Treasurer then noted that the pandemic would lead to lower tax receipts and higher spending as a share of GDP ‘for many years to come’. This change in economic circumstances, he explained, warranted a change in the government’s fiscal strategy. Under the previous strategy, the ‘plan was to deliver budget surpluses of sufficient size to significantly reduce gross debt and eliminate net debt by the end of the medium term.’ But now: ‘in the face of this shock, this is no longer the prudent or appropriate course of action. It would now be damaging to the economy and unrealistic to target surpluses over the forward estimates — given what this would require us to do in terms of significant increases in taxes and large cuts to essential services. This would risk undermining the economic recovery we need to bring hundreds of thousands more Australians back to work and to underpin a stronger medium-term fiscal position.’

To replace the old fiscal strategy, the Treasurer said the government would ‘adopt a new two stage fiscal strategy that emphasises jobs and growth’.

In the first phase, the government will focus on ‘boosting business and consumer confidence and promoting jobs and growth throughout the economy.’ That will see Canberra (1) continuing to ‘allow the automatic stabilisers to work freely to support the economy’; (2) continuing ‘to provide temporary, proportionate and targeted fiscal support, including through tax measures, to leverage private sector jobs and investment’; and (3) continuing to ‘push ahead with structural reforms that position the economy for the jobs of the future and which improve the ease of doing business.’

Crucially, the Treasurer said this first phase ‘will remain in place until unemployment is on a clear path back to pre-crisis levels’ which likely means ‘until the unemployment rate is comfortably back under 6 per cent’.

The second phase of the new fiscal strategy will then focus on restoring Australia’s fiscal position and will also comprise three elements: (1) a ‘central focus on jobs and growth, combined with structural reforms that increase our economy’s potential’; (2) a’ deliberate shift from providing temporary and targeted support for the economy to stabilising gross and net debt as a share of the economy’; and (3) rebuilding the economy’s fiscal buffers. The government will also retain its 23.9 per cent cap on the tax to GDP ratio.

Why it matters:

The new fiscal strategy – particularly in its first phase – marks a decisive break from the government’s previous, over-riding focus on returning the budget to surplus. Instead, the new strategy accepts the constraints – and opportunities – represented by changed economic circumstances and makes several welcome and important adjustments.

First, the government has accepted the new consensus view that one big international macro lesson from the GFC was that many countries turned off the fiscal tap too soon and embarked on a premature and counter-productive swing to austerity. The Treasurer notes that an early move to ‘increase taxes or reduce spending on essential services’ would ‘slow the speed of our recovery.’

Second, the Treasurer also now buys the argument that the current configuration of interest rates means that there’s considerably more fiscal space for Canberra to play with than has been the case in the past, remarking that with ‘historically low interest rates, it is not necessary to run budget surpluses to stabilise and reduce debt as a share of GDP — provided the economy is growing steadily. And even though debt will be at much higher levels than we are accustomed to, it remains sustainable… And low interest rates make our debt servicing task easier.’

Third, in an important innovation, the new strategy appears to introduce a form of forward guidance for fiscal policy. The Treasurer said that Canberra would not switch to the second phase of its fiscal strategy with its focus on stabilising debt and restoring fiscal buffers ‘until unemployment is on a clear path back to pre-crisis levels’ which he said meant that he expected ‘Phase 1 to remain in place until the unemployment rate is comfortably back under six per cent.’ I’ve been making the case for a form of fiscal policy forward guidance on the

Dismal Science podcast and here in the Weekly, for a while now, so it was very positive to see this element introduced into the framework.

What happened:

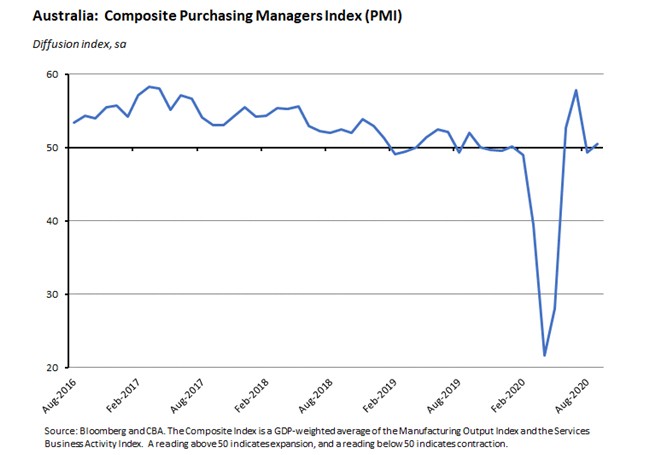

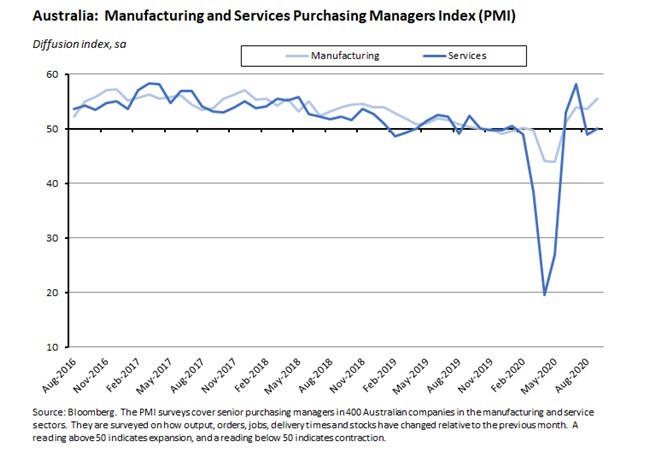

The September ‘flash’ Composite Purchasing Managers Index (PMI) report showed the index rising to 50.5 in September, up from a final reading of 49.4 in August. (Flash indices are based on around 85 per cent of final survey responses and are intended to provide an advance indication of the final PMI.)

The services business activity index rose to 50 this month from 49 in August, while the manufacturing PMI climbed to 55.5 from 53.6.

Why it matters:

With the PMI returning to positive territory this month, albeit only marginally, the index is signalling that Australian business started to expand again in September after having contracted in August. That overall shift was accompanied by a return to neutral for services activity – indicating no change on last month – and a 29-month high in manufacturing activity.

What happened:

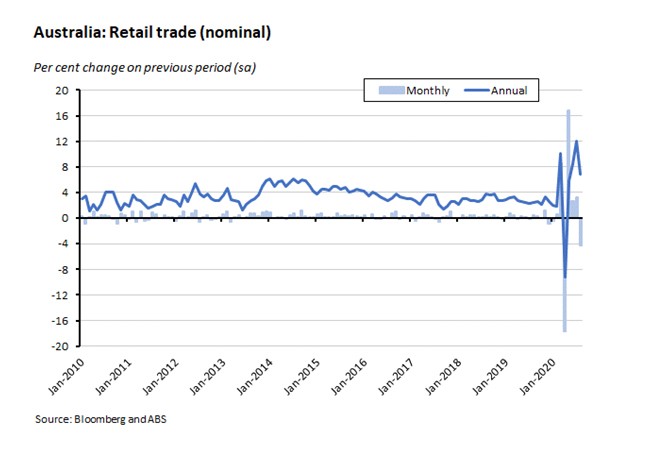

The ABS said the preliminary estimate for retail turnover in August fell 4.2 per cent over the month (seasonally adjusted), but was still 6.9 per cent higher compared with August 2019. (The estimate is based on preliminary data provided by businesses that make up approximately 80 per cent of total retail turnover and is subject to revision. The final monthly estimate is due on 2 October 2020.)

By state, Victoria led the decline with turnover down 12.6 per cent across the month. Excluding Victoria, the rest of Australia saw turnover fall by a more modest 1.5 per cent.

All industries fell, mainly reflecting the Victorian result, although there were falls in most states and territories. Household goods retailing led the falls, although the ABS notes that sales in this industry were still 20 per cent above the levels of August 2019. Clothing, footwear and personal accessory retailing, department stores, and cafes, restaurants and takeaway food services, also all saw large monthly falls in August, with the steepest declines suffered in Victoria.

Why it matters:

A sharp decline in retail spending in Victoria in August had been expected as Stage Four restrictions in Melbourne along with Stage Three restrictions in Regional Victoria had been widely predicted to take a heavy toll on retail businesses over the month. Spending also fell across the rest of Australia, however, with consumers in New South Wales in particular showing a large fall in turnover in Cafes, restaurants and takeaway food services.

What happened:

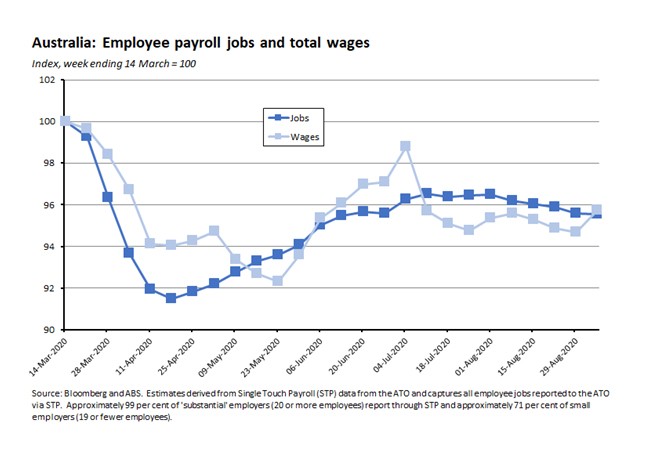

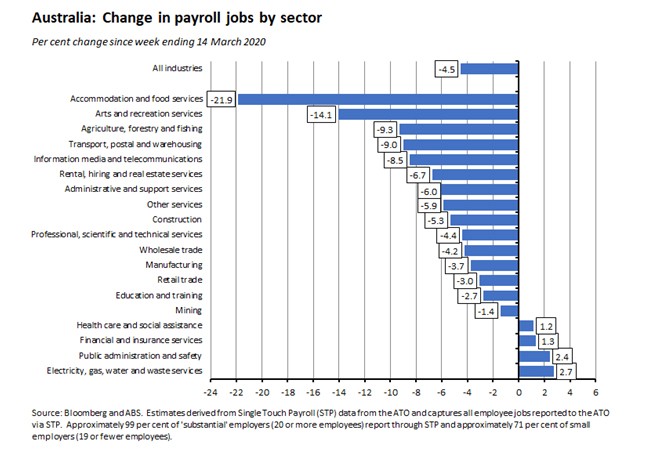

According to the ABS, between the week ending 14 March 2020 (the week Australia recorded its 100th confirmed COVID-19 case) and the week ending 5 September 2020, the number of payroll jobs decreased by 4.5 per cent, meaning that there were approximately 480,000 fewer payroll jobs on 5 September 2020 than on 14 March 2020. Over the same period, total wages paid fell by 4.3 per cent.

Over the most recent fortnight (from the week ending 22 August), payroll jobs have fallen 0.4 per cent, while over the past four weeks they are down 0.7 per cent.

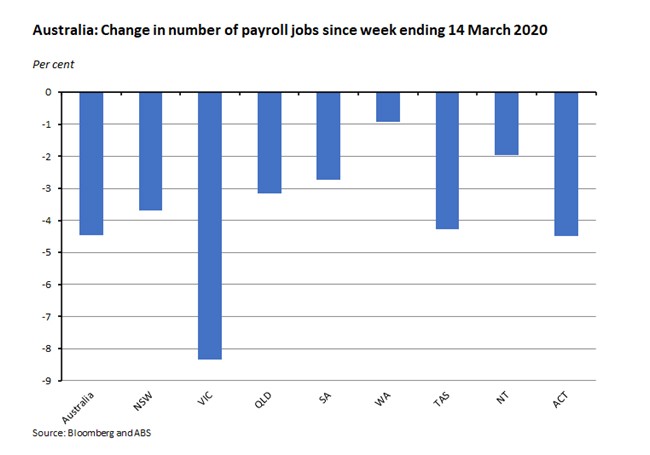

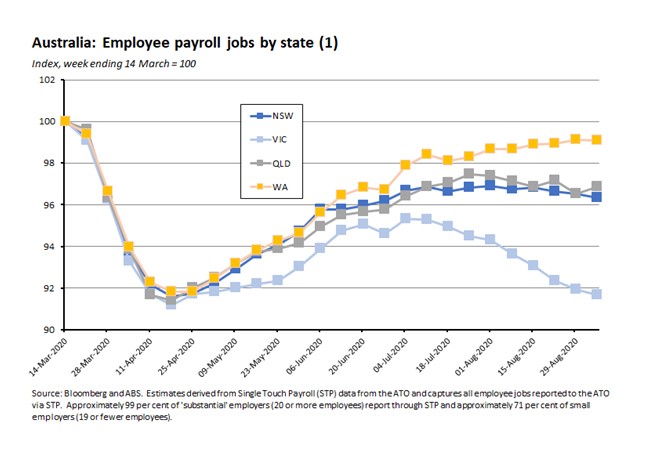

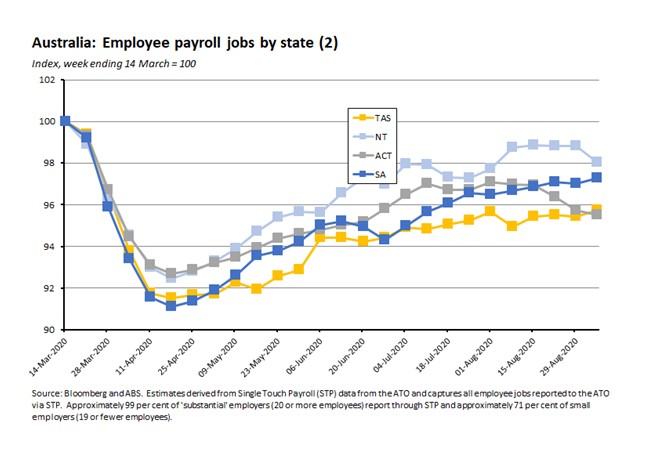

By state and territory, since the week ending 14 March 2020 the largest falls in payroll jobs numbers have been declines of 8.3 per cent in Victoria, 4.5 per cent in the Australian Capital Territory and 4.3 per cent in Tasmania. The smallest declines have been in Western Australia (down 0.9 per cent) and the Northern Territory (down two per cent).

Over the two weeks from the week ending 22 August, Western Australia, South Australia and Tasmania all added jobs, while the other states and territories saw job numbers decline, ranging from a 0.3 per cent fall in New South Wales to a 0.9 per cent decline in the Australian Capital Territory.

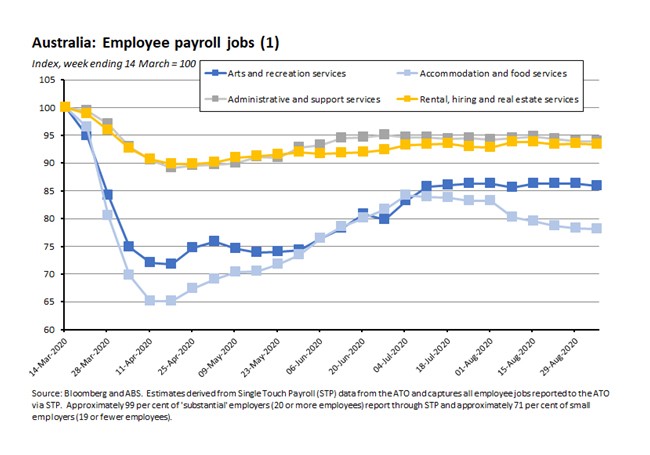

By industry, the largest job losses since 14 March have been in accommodation and food services (down 21.9 per cent) and arts and recreation services (down 14.1 per cent). Only four industries have added jobs over this period.

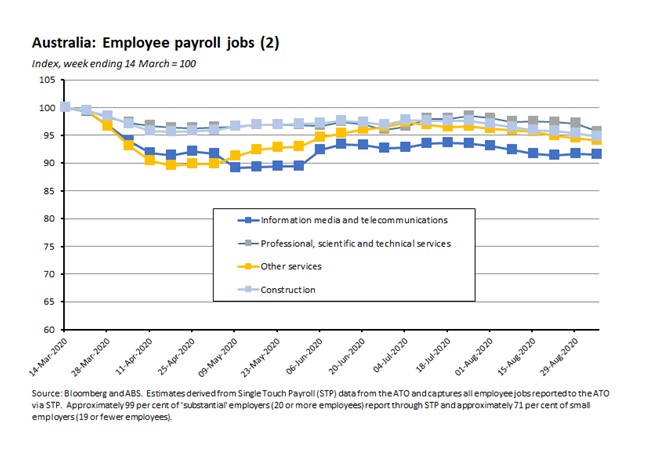

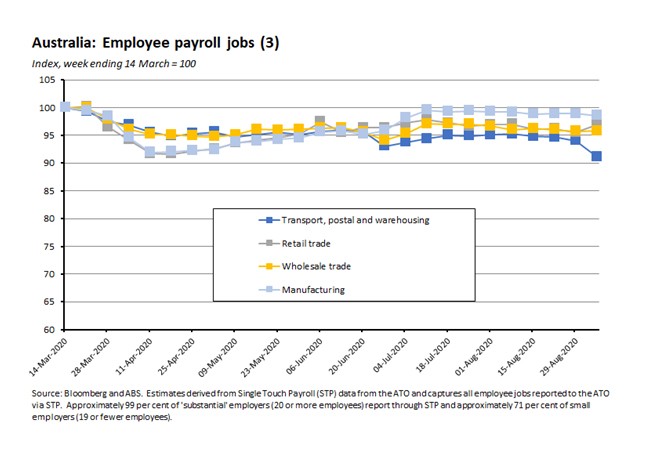

Over the most recent period, the largest declines in job numbers have been for transport, postal and warehousing (down 3.9 per cent) and professional, scientific and technical services (down 1.8 per cent).

Why it matters:

The payroll data continue to tell a story of little progress in restoring lost jobs over the past couple of months. Indeed, over the four weeks to 5 September, total payroll jobs fell by 0.7 per cent. Victoria is, of course, a big part of that story with payroll jobs down 2.1 per cent over that period. That contrasts with a much stronger labour market performance in some other states. Even so, payroll jobs also fell over the same period – if only by a modest 0.2 per cent – across the rest of Australia excluding Victoria. As a result, the total number of payroll jobs remains around 4.5 per cent lower than mid-March, with numbers 8.3 per cent lower in Victoria and 3.1 per cent lower in the rest of Australia (but less than one per cent lower in Western Australia).

This relatively sombre take on the state of the labour market stands in marked contrast to last week’s more upbeat monthly labour force report. The latter showed a surprise fall in the unemployment rate in August, along with a 0.9 per cent monthly rise in the number of employed persons.

The difference between these two perspectives on the labour market is explained by the different nature of the two datasets. As we’re usually careful to note when discussing the payroll numbers, they come with several important limitations. They are not seasonally adjusted, they are typically subject to very large revisions (which tend to see the numbers revised up over time), and they measure the number of jobs and not the number of employed (about six per cent of employed people hold multiple jobs and we know from the data that job destruction during this period has been particularly high for secondary employment).

Finally, by definition, the payroll jobs numbers only capture payroll information reported to the ATO by businesses with Single Touch Payroll (STP). That means that the data exclude owner managers of unincorporated enterprises (the self-employed or sole traders). As we noted last week, that exclusion turns out to have been particularly important last month, as the labour force survey showed there was a sharp increase in the number of self-employed persons in August – something that the payroll numbers wouldn’t pick up.

What happened:

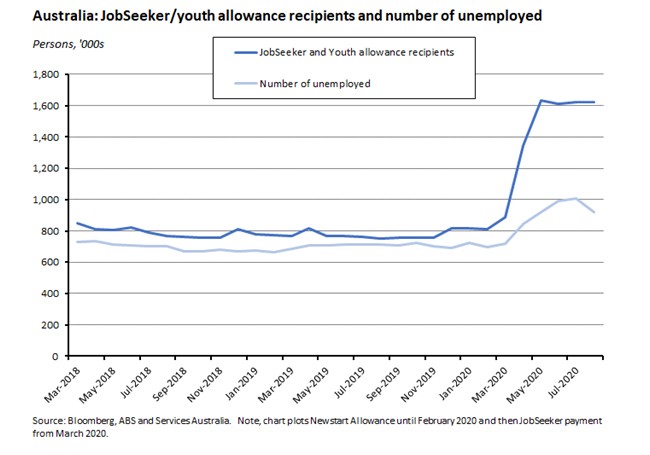

Last week, the Department of Social Services released the latest count of the number of Australians on JobSeeker and Youth Allowance. As of August, there were more than 1.6 million recipients.

Note that there is significant gap between the reported number of recipients and the ABS count of unemployed Australians. That’s because they measure two different things.

The ABS unemployment count refers to people aged 15 years and over who were not employed during the reference week, and had actively looked for full time or part time work at any time in the four weeks up to the end of the reference week and were available for work in the reference week; or were waiting to start a new job within four weeks from the end of the reference week and could have started in the reference week if the job had been available then.

The recipient count is based on eligibility for JobSeeker and the Youth Allowance. And the ABS reminds us that people who receive JobSeeker are not automatically classified as unemployed (and those classified as unemployed will not necessarily be in receipt of JobSeeker). Instead, how recipients are categorised depends on how they answer questions around their labour market activity. JobSeeker is paid to people who are looking for work or are sick or injured and cannot undertake their usual work or study for a short time, and who meet the eligibility requirements. Note, for example, that people can also receive the JobSeeker payment if they have a job, provided they meet a low-income test. Moreover, some of the government’s changes to JobSeeker in response to COVID-19 meant that recipients did not have to meet the usual mutual obligation requirements, such as looking for work (although some of these obligations have been gradually reinstated from June onwards).

Why it matters:

The JobSeeker numbers have been relatively stable over the past four months with the number of recipients exceeding 1.6 million Australians since May this year, following big jumps in March and April. The JobSeeker count, like the payroll numbers, does not show the improvement in labour market conditions reported in the August labour force report.

What happened:

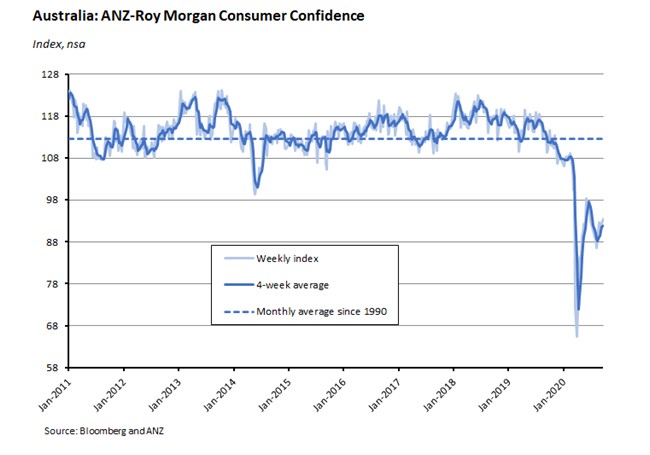

The ANZ-Roy Morgan weekly index of consumer confidence rose 1.2 per cent to an index reading of 93.5 for 19/20 September.

Three of the subindices – current and future economic conditions and future finances – rose last week while the other two (current finances and time to buy a major household item) fell.

Why it matters:

Consumer confidence has now risen for three weeks in a row, with the latest reading bringing significant gains in Melbourne and the rest of Victoria – likely a reflection of improving public health news. Sentiment in Melbourne is still in negative territory but is now slightly above sentiment in Sydney. And sentiment in the rest of Victoria has now risen above the neutral 100 level for the first time since March.

Despite the improvement in sentiment over the past three weeks, however, current readings are still only comparable to those reached during the worst of the global financial crisis.

What happened:

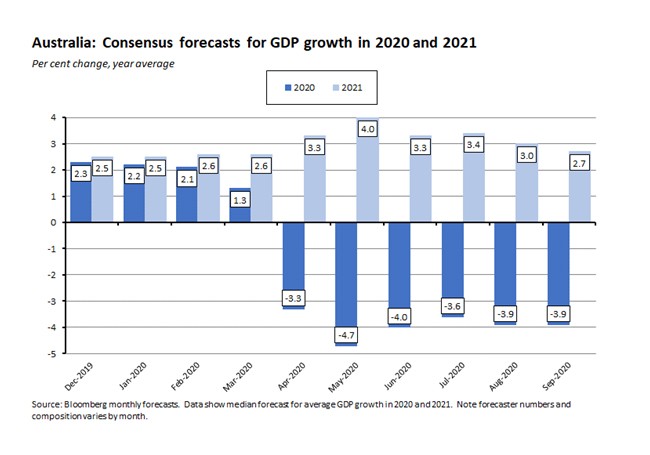

Bloomberg’s latest monthly survey of economic forecasters reported that the median forecast as of September is for the Australian economy to shrink by 3.9 per cent this year before growing by 2.7 per cent in 2021.

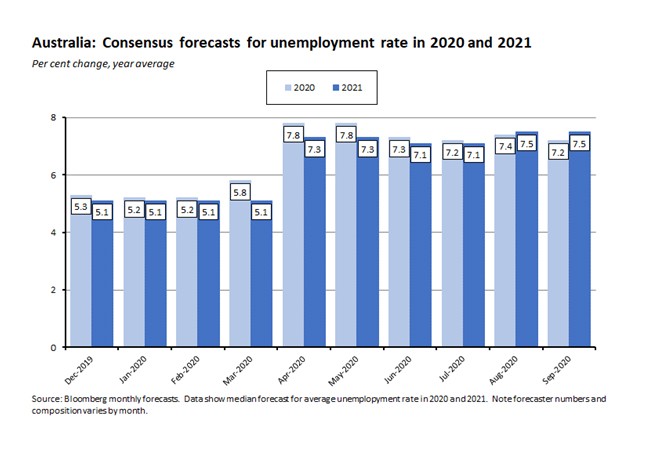

Following last week’s better than expected labour force report, the median forecast for the average unemployment rate this year has fallen by 0.2 percentage points to 7.4 per cent while the forecast for 2021 remains unchanged.

Why it matters:

After some big swings at the start of the year as forecasters struggled to come to grips with the economic implications of COVID-19, expectations about the economy have become more settled, with the consensus growth forecast for this year unchanged relative to August’s survey result, although the forecast for next year has slipped back from three per cent last month.

Australia is still expected to suffer its worst post-war recession on record in 2020 but the depth of the decline in GDP has been scaled back relative to some initial fears. At the same time, hopes of a sharp bounce back in growth next year have also receded, although to some extent that likely reflects the assumption that a smaller downturn will be followed by a shallower recovery.

What I’ve been reading:

Michael Brennan, Chair of the Productivity Commission, gave a speech looking at economic recovery from COVID-19 from a supply side perspective. Brennan’s staring point is James Tobin’s 1971 observation that ‘It takes a heap of Harberger triangles to fill an Okun gap’ – in other words, that the inefficiencies from resource misallocation are small when stacked against the consequences of a lack of aggregate demand, particularly during a recession. But while this might seem to argue that only demand and macro policies are important right now, Brennan instead sets out the case that ‘supply side policy is an important enabler of the recovery, without which demand-side stimulus is incomplete or compromised in its effectiveness.’ Partly, he suggests, that’s because COVID-19 is also a significant re-allocation shock (that is, capital and labour will have to be redeployed across the economy as some sectors shrink and others expand) and getting the microeconomics of that right will be vital in smoothing the adjustment. Partly it’s because supply-side measures can help offset the adverse consequences of ‘belief-scarring’ on risk appetite and new business formation. And partly it’s because microeconomic reforms can build ‘greater adaptability and resilience…especially in the face of shocks and disruptions.’

The government has published Australia’s first low emissions technology statement.

Grattan’s Tony Wood gives recent government initiatives on energy and climate a largely positive review.

The ABS has published the latest in its Business Impacts of COVID-19 Surveys. September’s survey reports that 64 per cent of all businesses were operating under modified conditions due to COVID-19, down from 73 per cent in June. Thirty-one per cent of all businesses reported they expect at least one of those modifications would remain in place long-term. Forty-three per cent of employing businesses reported that they had staff currently teleworking compared to 28 per cent prior to COVID-19, and 29 per cent expect staff to continue to telework once restrictions are lifted and conditions stabilise.

Paul Keating is critical of the RBA.

ANZ Bluenotes on tracking Australia’s Covid-recovery.

According to the ABS, Australia’s population was 25,649,985 people as of 31 March 2020. That was the product of annual growth of 357,000 people (1.4 per cent), of which roughly 38 per cent was due to natural increase and 62 per cent to net overseas migration. Net overseas migration was down 12 per cent compared to the same quarter last year, driven by a 20 per cent increase in overseas migration departures. All states and territories, except the Northern Territory, had positive population growth over the year ending 31 March 2020, with Victoria experiencing the highest growth rate (1.8 per cent) and the NT the lowest (-0.2 per cent).

The section on the RBA above referred to Exchange Settlement (ES) balances and we also touch on them in this week’s Dismal Science podcast. For those readers who’d like a better and (much) more detailed explanation of what they are and how they relate to the cash rate than my one minute podcast effort, see this useful RBA explainer.

Adam Tooze on how the world is both winning and losing the race for a vaccine. Tooze sees the race for a vaccine as a ‘test run for the political economy of the future’ and worries that while a vaccine would solve one set of economic and political problems it could also create another.

The Economist magazine has a briefing on the changing geopolitics of energy as what it means to be an energy superpower evolves alongside a shift from petrostates to ‘electrostates’. The piece highlights three big global changes and their implications: (1) concerns about a scarce supply of fossil fuels have shifted to a new focus on demand as the more pressing constraint – so peak oil now refers to peak oil demand rather than supply; (2) shifting policies in reaction to climate change; and (3) the rise of electrification.

Bloomberg’s Connor Sen applies the ‘K-shaped recession’ analogy to New York and Texas to argue that as well as capturing the differential performance across sectors post-pandemic, it also applies to geographies. In this case, Sen’s thesis is that ‘recovery is happening faster in those [US] states whose economies are less tied to in-person services, not states that have performed better in controlling the virus.’

Subramanian and Felman worry that deglobalisation will kill prospects for economic convergence for developing economies. They think it’s already happening, pointing out that while low- and middle-income countries were growing at three or four per cent per capita annually before the global financial crisis, they have since been averaging per capita growth of around one to two per cent.

The FT’s Gavyn Davies warns that the world economy faces significant economic scarring from the pandemic, consisting of more uncertainty, higher levels of precautionary saving, and lower business investment. While it’s very difficult to gauge the potential scale of these effects, one estimate is that scarring in 2022 could be three per cent of global GDP.

Some research from the San Francisco Fed examining whether the US decision to add a temporary US$600 weekly supplement to unemployment benefits discouraged workers from seeking employment. The implied nationwide median replacement rate—unemployment benefits as a fraction of earnings before job loss—with the supplement included, has been estimated at 134 per cent which implies that a substantial majority of recipients received benefits that exceeded lost earnings, often by a wide margin. (In contrast, US replacement rates under normal circumstances typically average about 50 per cent.) That in turn has led to arguments that this will have a negative impact on workers’ efforts to find new jobs. But this research finds that despite its relative generosity the extra payment ‘had little or no effect on the willingness of unemployed people to search for work or accept job offers. The researchers think that this likely reflects ‘the appeal of a sustained salary compared with even very generous unemployment benefits when labour market conditions are weak and virus containment measures prevent hiring.’ Which also implies that the main impact of the increased payment came in the form of stimulus to aggregate demand rather than in the form of any supply-side distortion.

Another piece of US research, this one looking at how Americans have used the time saved from not having to commute during the great WFH experiment. Barrero, Bloom and Davis estimate that the pandemic-induced shift to working from home has yielded 62.4 million fewer commuting hours per workday. Cumulating these daily savings from mid-March to mid-September gives an estimated aggregate time saving of more than nine billion hours. Drawing on survey data, they suggest that most of these time savings are devoted to non-leisure activities: ‘work for pay, but also chores, home improvement, and childcare.’ Together, these activities absorb about 60 per cent of the time savings with the single largest component – 35 per cent – devoted to the respondent’s primary job. But they also find substantial differences depending on education levels and between those with and without children at home.

From the WSJ, what US CEOs really think about remote working. Predictably (?), a pretty diverse set of views.

Another interesting (this time UK, Marxist) take on the economics of WFH.

Finally, a couple of podcasts from the LSE. The first is Paul Collier and John Kay discussing their new book Greed is Dead: politics after individualism and the second is Michael Sandel presenting the argument of his new book, The Tyranny of Merit: what's become of the common good? Both books/discussions push back against meritocratic and/or individualistic views of the world. To declare my own biases, since those are ideas that I tend to have a fair amount of sympathy for (and feel that I’ve personally benefitted from), I’m yet to be fully convinced by the current backlash against both, although I do buy some of the arguments being made here. I should also confess that I was intrigued by the Collier-Kay piece in part just because they cite the town and constituency in which I spent half my childhood as one of their examples. But if communitarianism isn’t your thing, then as an alternative LSE offering, here is Tim Harford on how to make the world add up.

Latest news

Already a member?

Login to view this content