Overview

- After a period of falling oil prices and rising traffic through the Strait of Hormuz, the resumption of conflict in the Middle East is a reminder of the volatility that currently characterises the international economic environment.

- That volatility is in part a product of two ruptures. The geopolitical rupture identified by Mark Carney, of which the Iran war is an exemplar, and the technological rupture that is the current AI boom.

- Despite recent turbulence, the global economy has remained remarkably resilient. In part, this reflects the way that the headwinds from one shock have been offset by the tailwinds from the other. But there is also a risk that some of the shocks could have compounding effects.

- The latest IMF World Economic Outlook Update and BIS Annual Economic Report provide useful overviews of the forces operating on the global economy and some of the associated risks.

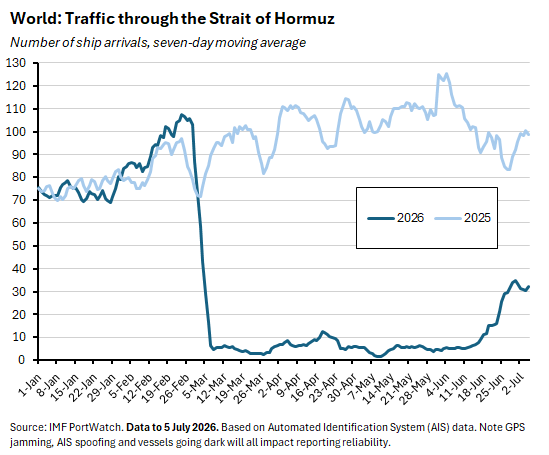

For a time, the 14-point Memorandum of Understanding signed between Washington and Tehran on 17 June and the 60-day US-Iran ceasefire looked to have meaningfully influenced the economic consequences of the war in the Middle East. Despite the obvious fragility of the deal, there had nevertheless been a significant pickup in traffic through the Strait of Hormuz. And oil prices had eased significantly, dropping to below pre-war levels towards the end of last month. Media headlines had even started to talk about a new oil glut. Now this week’s developments, including President Trump’s declaration that the ceasefire is over, have sent oil prices up while reminding everyone of the volatility that currently characterises our international economic environment, even as the duration of this latest phase in the conflict remains uncertain.

That volatility is one consequence of the ‘rupture’ to the global order called out by Canadian Prime Minister Mark Carney in his speech to the World Economic Forum in January this year. Carney’s rupture was about geopolitics, and the conflict in the Persian Gulf fits fairly comfortably into that story. Complicating the picture further, however, is another potential rupture in terms of the unfolding AI-led technological revolution.

Attempts to think about the current global economic outlook require grappling with the consequences of both ruptures. This week’s new IMF World Economic Outlook together with the earlier release of the BIS 2026 Annual Economic Report see forecasters from the official sector thinking through the interaction between the two shocks. To some extent, they have offset each other: the headwinds for confidence and activity created by the energy shock have run into tailwinds from AI-driven investment and trade booms and the associated financial market optimism. Yet in other areas, the shocks could be reinforcing as the inflationary impulse from higher commodity prices meets the demand pressures created by surging hyperscaler capex.

The offsetting effects of the two ruptures help explain another striking feature of the current international economic environment: the ongoing resilience of the global economy. Despite a series of large, adverse shocks, global economic (and financial) conditions have held up well. For all the talk of the fragility of complex systems such as the interlocking web of global supply chains, the market and business systems that underpin them have – so far – proved to be both adaptable and robust. Even if we have also been ‘lucky’ with the timing of the AI boom.

We dig into the new IMF and BIS reports in more detail below along with our usual roundups of Australia data and options for further reading and listening.

Finally, a belated thanks to those readers I got a chance to talk with at recent AICD events in Perth and Adelaide. It was lovely to meet you. The feedback, kind words and ongoing support are all much appreciated.

The view from the IMF: War and technology

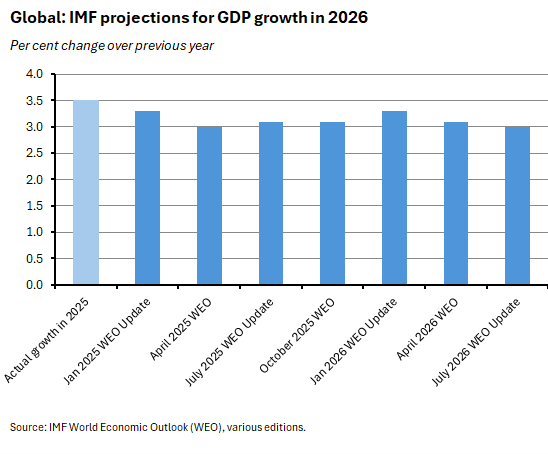

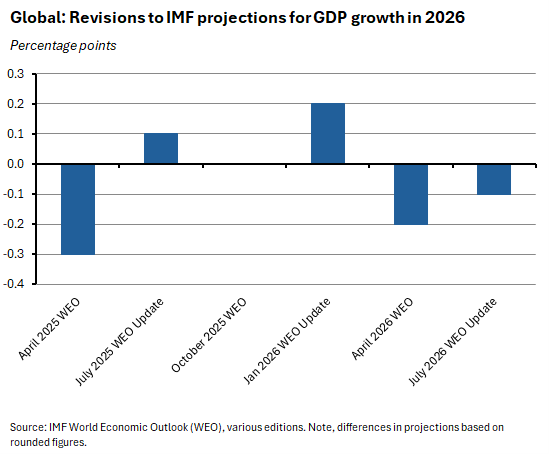

In its latest assessment of the world economy (which predates the latest flare-up in the Middle East conflict), the IMF has trimmed its forecast for global growth this year by 0.1 percentage point to 3% while boosting expected growth next year by 0.2 percentage points to 3.4%, relative to its April 2026 projections. The corresponding forecasts for Australia see a 0.1 percentage point downgrade to 1.9% for the Fund’s estimate for growth in 2026, while next year’s growth forecast was left unchanged at 1.7%.

Since last January, when the IMF started publishing growth projections for this year, the international economic environment has been characterised by a sequence of shocks including the April 2025 Liberation Day tariffs, the June 2025 12-day war, and the current Middle East conflict. Yet, in what has been a recurring theme in recent years, the toll on expected growth has – to date at least – proved relatively modest.

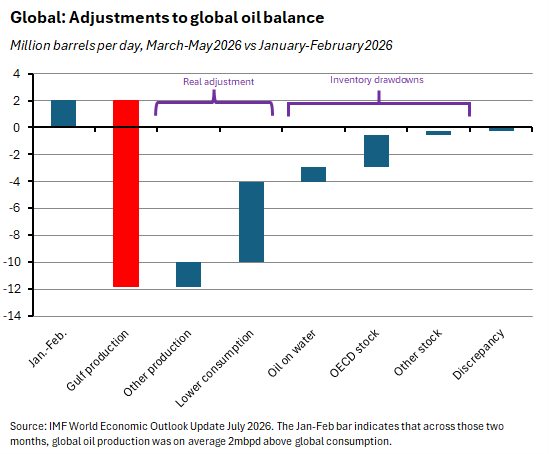

According to the July 2026 World Economic Outlook (WEO) Update, part of the reason that the global economy has been able to weather the storm of the Iran war is that the transmission process from the shocks already incurred remains in its early stages. At the same time, the loss of Persian Gulf oil production has been offset by a combination of lower consumption, the substitution of new production, and a significant drawdown of global commercial and strategic oil stocks. And the Fund also points to the declining energy intensity of GDP growth in many economies and the rise in the share of renewables in global energy production as additional shock absorbers.

In addition, global activity has also been supported by an AI-led acceleration in technology-related trade and investment, which has also contributed to easier global financial conditions and helped offset the war-driven headwinds for global growth.

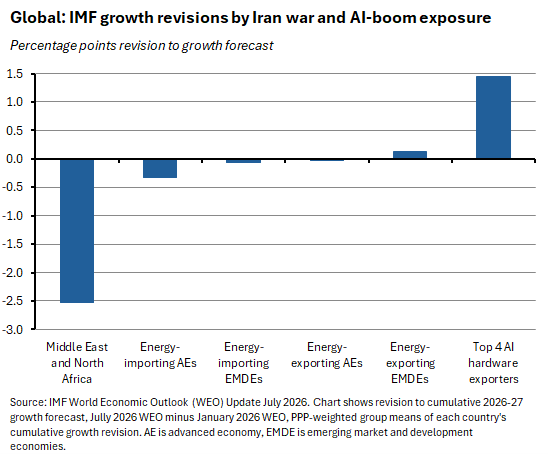

All of which means that sitting behind that modest 0.1 percentage point decline in the IMF’s growth forecast for this year is a more complex adjustment in relative growth prospects: countries in the Middle East directly exposed to the war have seen relatively large downgrades to growth forecasts; growth prospects for energy exporting economies outside the region have either been sheltered from (in the case of advanced economies) or modestly boosted by (for emerging market and developing economies) higher energy prices; countries heavily integrated into global technology value chains have enjoyed a large boost to projected activity; and energy importers that are not well-placed to benefit from the AI boom have seen growth downgrades.

In terms of the risks to the global outlook, the Fund reckons that these are more balanced than was the case back in April this year but still tilted to the downside. In this context, top of the Fund’s worry list is the war in the Middle East, with the WEO Update warning that any re-escalation of geopolitical tensions (at risk of being underway at the time of writing) would undermine growth while boosting inflationary pressures. With global oil inventories now approaching multiyear lows, further supply disruptions could trigger what the Fund calls ‘nonlinear dynamics’ in energy prices. Likewise, renewed disruption to fertilisers would risk a worsening in global food security, particularly in low-income countries in South Asia and Sub-Saharan Africa. On the other hand, a faster than expected resolution to the conflict would improve the outlook for growth and inflation.

In the case of the AI boom, the IMF’s judgment is that risks ‘are more distinctly two-sided.’ On the upside, if AI investment is sustained and then translated successfully into material gains in aggregate productivity, the prospects for medium-term growth will strengthen. On the downside, if expectations regarding AI-powered profitability and productivity outcomes were sharply downgraded, both physical investment plans and market valuations could suffer sharp and potentially destabilising corrections.

According to the Fund, other things to keep an eye on include the potential for renewed trade tensions, the Ebola public health emergency, the high probability of extreme weather events triggered by an ‘extraordinarily strong El Nino’, and AI-amplified cybersecurity risks.

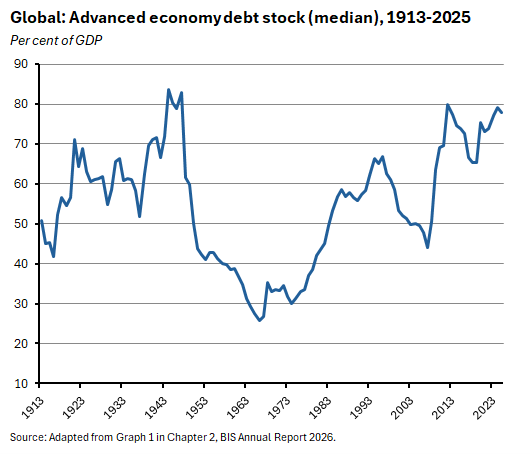

The view from the BIS: Resilience and pressure points

A second recent assessment of the global economic and financial situation comes from the latest BIS Annual Economic Report, where the main messages largely align with the IMF’s analysis. Published before the new WEO Update, the BIS Report begins on an optimistic note with a review of the global economy’s resilience through the second half of last year which it attributes to two main factors.

First, the impact of last year’s trade policy disruption turned out to be smaller than expected. Partly because final US effective tariff rates ended up much lower than the initially announced headline rates, while US trading partners largely refrained from retaliatory tariffs. And partly because of the adaptability of the international trading system and of individual firms. The former entailed the realignment of trade flows via a reconfiguration of supply chains. The latter saw US importers front-load purchases to get ahead of tariff changes as well as absorb higher prices through lower margins.

Second, the surge in AI optimism has supported global activity directly via increased investment spending and greater trade in AI-enabling products, and indirectly via the easier global financial conditions driven by investors’ AI-enhanced risk appetites.

Despite this resilience, however, the BIS too is mindful of the risks to the global outlook, highlighting ‘four pressure points’ to monitor:

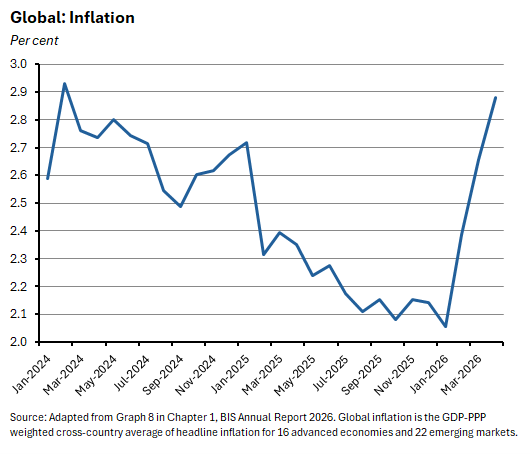

1. The risk of an inflation comeback. The BIS worries that the full inflationary impacts of the Iran war are yet to be fully felt, pointing to ongoing uncertainties over how long it will take for traffic through the Strait of Hormuz to fully resume and for the repair of damaged energy infrastructure in the region. The Report warns that there are already signs of rising inflationary pressures, with global inflation up by half a percentage point since the start of the conflict, several commodities including plastics and fertilisers experiencing double-digit price increases, and the danger of ‘cascading effects’ of previous price rises through supply chains.

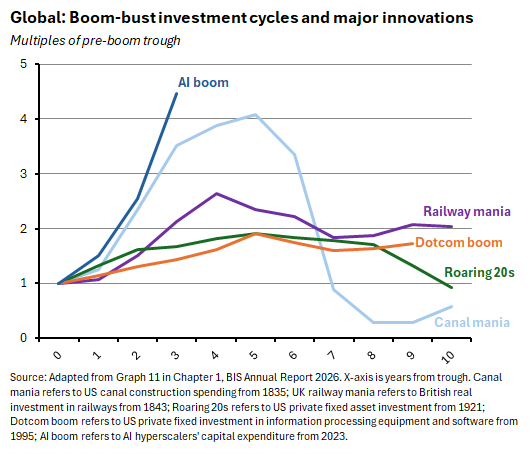

2. Pressure on the AI investment boom. While the BIS notes that ‘AI has the potential to raise productivity significantly over the coming decade’ it also cautions that in the near term, the speed and scale of the current investment boom raise questions about its sustainability, with one risk being that disappointing returns could trigger a sudden reduction in financing and turn boom into bust. A second risk is that the AI boom runs into supply-side constraints – with the Report highlighting the emergence of current bottlenecks in electricity, semiconductors, and grid equipment. The Report also points to current echoes of past investment booms from canal and railway mania to the dotcom boom and their pattern of boom followed by slump.

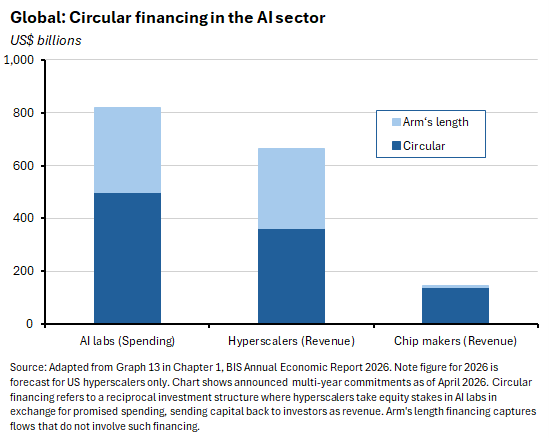

3. Financial vulnerabilities. Should one or both of the previous two risks materialise, the BIS is concerned that the macro fallout could be exacerbated by existing financial vulnerabilities, including elevated debt issuance by AI-related businesses, extended equity valuations, compressed risk premia, exuberant market sentiment, and the opacity of AI-sector financing (including the complex tangle of circular financing which involves chip makers and hyperscalers taking equity stakes in AI labs and neocloud providers – specialised cloud platforms purpose built for AI – that have committed to multi-year purchases from the former).

4. Fiscal strains. Finally, the Report reminds its readers that the Iran war energy shock has served to place further strain on already-stretched fiscal positions. Sovereign borrowers face large refinancing needs this year and that borrowing task will now be complicated by higher interest rates and slower growth.

Other Australian data points to note

ANZ-Indeed Australian Job Ads fell 0.2% over the month (seasonally adjusted) in June 2026 to be 0.5% higher than in the same month last year. ANZ noted that the series has now fallen by about 28% since late 2022 – in line with a similar decline in the ABS Job Vacancies data – but remains significantly higher than before the pandemic.

The ABS said that in the March quarter 2026, total dwellings commenced fell 11.2% quarter-on-quarter (seasonally adjusted) while edging higher 0.2% year-on-year to 48,012. The number of new private sector houses commenced fell 3.5% over the quarter and dropped 2.1% over the year to 27,658. The number of new private sector other dwellings dropped 20.7% over the quarter but was up 5.6% over the year, at 19,116.

While we were away last week, the RBA published the Minutes of the 15-16 June 2026 MPB Meeting, at which the Board had voted unanimously to leave the cash rate target unchanged. At the time we characterised that decision as a ‘hawkish hold’ and the Minutes are consistent with this interpretation. They report that ‘information received since the previous meeting had supported the view that the economy was operating with excess demand and widespread inflationary pressures. Inflation was still materially above the Board’s target and the staff’s expectation remained for underlying inflation to increase in the June quarter. Labour and non-labour cost pressures remained widespread.’ And again, later: ‘…members agreed that monetary policy needed to remain restrictive to unwind current excess demand through a period of below-trend growth. While the most recent data and forward-looking indicators suggested somewhat mixed signals about how quickly momentum in economic activity was slowing, members judged the easing in growth to be broadly in line with earlier expectations.’ The Minutes also report the MPB discussing two sets of risks, one related to developments in the Middle East where members acknowledged that the conflict ‘still posed material upside risks for inflation and downside risks for growth’ and one focused on the domestic economy, where members ‘expressed somewhat differing views about the extent of current capacity pressures…[but]…agreed that persistently weaker-than-expected productivity growth could impede progress on returning inflation to target’ and where they ‘also noted the risks associated with a potentially material weakening in housing markets, including if this were to inhibit growth in consumption.’

Further reading and listening

- The June 2026 edition of Resources and Energy Quarterly (REQ) – with publication pushed back by the Iran war – reckons that the near-term impact of the conflict in the Middle East will be to push up the value of Australian resource and energy exports. Relative to its previous (December 2025) forecasts, the new REQ estimates that exports will be $405 billion in 2025-26 and $416 billion in 2026-27, representing upward revisions of $22 billion and $42 billion, respectively. Exports are then forecast to fall to $371 billion by 2030-31 as commodity prices drift lower: the REQ sees iron ore prices softening due to rising Brazilian and African supply while energy prices are forecast to normalise in the aftermath of the war.

- From Parliamentary Budget Officer Sam Reinhardt, Does the Budget get in the way of good policy? This is a very nice look at eight features of how budgets are currently constructed or presented. The eight are: The focus on forward estimates (which do not always capture the full implications of a policy); the assumption of no policy change (which can introduce a degree of ‘systematic optimism’ into budget numbers); the focus on the underlying cash balance (which offers an incomplete picture of fiscal costs and risks); the need to take a whole-of-government perspective (state and territory budgets are also central in driving the national fiscal position); the budget night focus on winners and losers (which can obscure longer-term and intergenerational effects of policy changes); the role of the contingency reserves and decisions taken but not yet announced (which creates transparency challenges); point estimates and estimate variations (which can lead to an under-appreciation of uncertainty in fiscal projections); and the relationship between marginal spend and the overall budget (the temptation to focus on new announcements rather than the full stock of spending already locked in).

- Jobs and Skills Australia’s Australian Jobs 2026 includes lots of interesting tables and graphics on the state of the Australian labour market.

- According to the latest Deloitte Access Economics Business Outlook, the Australian economy is facing its longest stretch of sub-2% growth since the early 1990s recession.

- RBA Assistant Governor (Economic) Sarah Hunter’s speech on Understanding supply shocks and their implications for monetary policy argues that the Iran war oil price shock has pushed the (empirical) Phillips curve outward, implying higher underlying inflation for a given level of unemployment.

- Also from the RBA, introducing Insights, a new series of short analytical notes by RBA staff. The first four notes include a review of the recent academic literature on non-linear Phillips Curves, an examination of how firms’ price-setting behaviour shifted in response to the pandemic (becoming more flexible), modelling work on the implications of greater price flexibility, and a look at the implications of shifts in price flexibility for monetary policy.

- The e61 Institute’s Gianni La Cava on knowledge capital and the Australia-US productivity gap.

- Views from ASPI analysts on China’s Pacific ballistic missile test.

- Grattan’s Tony Wood reckons the draft gas reservation scheme falls horribly short.

- Related, the AFR on how Grattan became Australia’s most influential public policy factory.

- EVs and China are reshaping the Australian automotive market.

- Related, fixing Australia’s EV charger rollout.

- Already discussed in detail above, but here for completeness: the July 2026 IMF World Economic Outlook Update and the BIS Annual Economic Report 2026.

- The OECD Employment Outlook 2026 reckons that members’ labour markets continue to be resilient, although it also finds that signs of weakening have started to emerge. The average OECD unemployment rate remains around 4.9% while employment and labour force participation rates are at or close to record levels. The report also notes that real wages are under pressure in many countries (with Australia ranking near the bottom of the list in terms of performance). And it points out that young university graduates are at an increasingly high risk of unemployment compared to other workers, although this rising trend began ‘well before’ the spread of generative AI. This edition of the Outlook includes chapters on a range of related issues, including geographic disparities in labour market outcomes, the impact of structural change on local labour markets, and the adverse effects of non-compete clauses and related agreements.

- Before this week’s developments, the WSJ was contemplating a sudden global oil glut.

- From the McKinsey Global Institute, a new report on competitiveness investigates where investment happens and why.

- Is the Economist magazine always wrong?

- An FT Big Read on how Europe would fight without America.

- Related, on the economic footprint of Europe’s defence buildup.

- The State of the AI Economy. A bottom-up assessment.

- The UBS Global Wealth Report 2026 (registration required to read).

- On skill nostalgia.

- The Conversations with Tyler podcast with Joel Mokyr on growth, clans, corporations, and China vs Europe.

- The Macro Musings podcast in conversation with Barry Eichengreen on the history of global currencies.

- The ChinaTalk podcast discusses the chemical supply chains of the semiconductor industry.

- The FT Unhedged podcast looks back at the AI-triggered fall in the market value of big software groups.

Latest news

Already a member?

Login to view this content