Overview

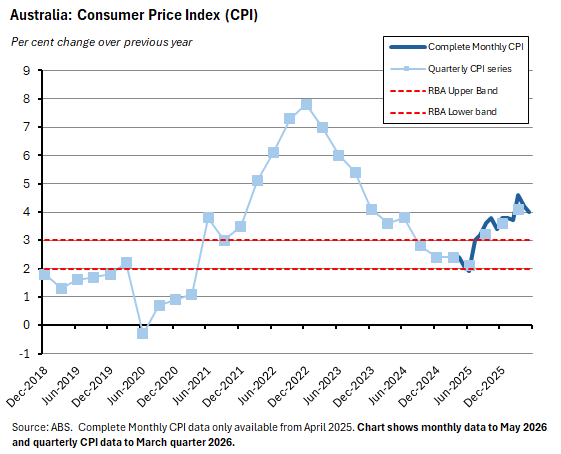

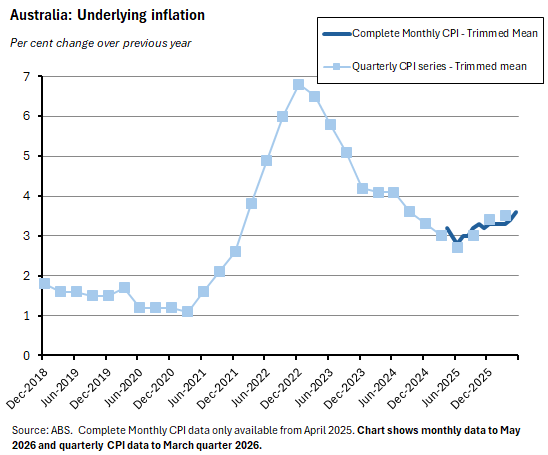

- The annual rate of headline CPI inflation slowed to 4% in May 2026 from 4.2% in April. But underlying inflation as measured by the trimmed mean moved in the opposite direction, increasing to 3.6% from 3.4%.

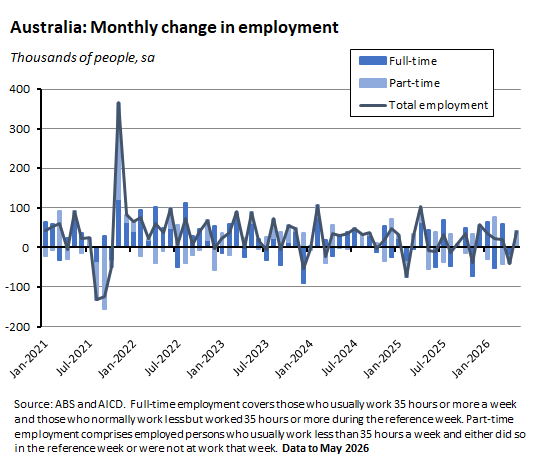

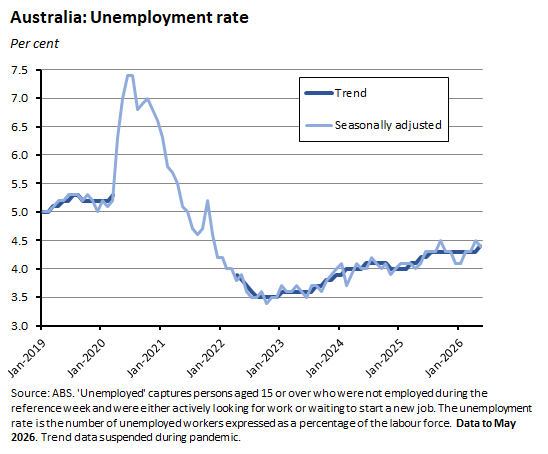

- Employment grew by a strong 40,300 over the month in May (seasonally adjusted) while the number of unemployed fell by 18,300. The unemployment rate fell to 4.4% from 4.5% in April (although on trend basis it nudged up from 4.3% to 4.4%).

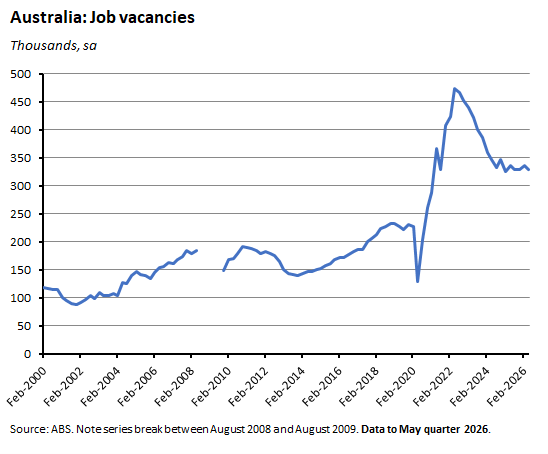

- The number of job vacancies fell by 2.1% in the three months to May, marking the first decline in vacancies since August last year.

As discussed in last week’s post-MPB assessment, one key macro debate right now is between those who think the RBA’s next move will be to cut interest rates and those who judge that further tightening is likely to be required. The first camp (the doves) reckons that the economy is losing momentum and that the balance of risks is shifting from too-high inflation to too-low growth. The second camp (the hawks) thinks this judgement is premature and argues that activity is more resilient and inflation more stubborn. So, this week’s releases on inflation, the labour market, and household consumption gave both camps the opportunity to check their views against the latest data.

The doves can point to a bigger than expected fall in headline CPI inflation, which slowed to an annual rate of 4% in May. And they can also cite a first drop in the ABS vacancies series since August last year as signalling future labour market weakness. There was also a small uptick in the underemployment rate plus a slight rise in the trend unemployment rate. (Some might also want to point to news stories warning about falling property prices.)

For their part, the hawks can stress that the CPI inflation story was largely driven by lower global oil prices and emphasise that several measures of underlying inflation including the trimmed mean rose last month. In addition, May’s employment numbers bounced back sharply from April’s fall, the commonly cited seasonally adjusted unemployment rate fell to 4.4%, and the overall underutilisation rate also declined. Furthermore, household spending as measured by the ABS Monthly Household Spending Indicator surprised to the upside last month while signalling strength in some areas of discretionary spending.

Overall, there was nothing definitive either way here, which is consistent with last week’s argument about the case for ‘watch and wait.’ Still, if pushed, probably score this week’s data for the hawks.

Headline inflation eased last month but underlying inflation picked up

The ABS said that the Consumer Price Index (CPI) fell 0.7% over the month in May 2026 (original basis) taking the annual rate of increase down to 4% from April’s 4.2% result. The market consensus forecast had expected the headline CPI to fall 0.4% over the month and be up 4.3% over the year, so this was a weaker than anticipated result. The softer outcome in large part reflected the impact of lower fuel prices, with automotive fuel prices dropping 11.9% over the month after having fallen 7% in April. That in turn reflects lower world oil prices last month and before that the government’s halving of the fuel excise with effect from 1 April 2026. That measure expires at the end of June, although Canberra has announced that it will extend partial relief (which will make petrol and diesel 16 cents per litre cheaper instead of the previous 32 cent discount) through July.

In contrast to the decline in the headline rate, underlying inflation as measured by the trimmed mean – which excluded the impact of lower fuel prices – rose 0.4% over the month to be up 3.6% over the year. That was a higher result than the median forecast, which was for a 0.3% monthly increase and a 3.5% annual rise. In addition, the May annual rate was also up on the April outcome (3.4%).

Alternative annual measures of underlying inflation also increased, including the weighted median (also up from 3.4% in April to 3.6% in May) and the CPI excluding volatile items and holiday travel (up from 3.9% to 4%). That suggests that inflationary pressures remain in the economy and that at least some pass through from higher costs to higher prices is taking place: for example, in the context of new dwellings prices rising 5.6% over the year, the ABS noted that project home builders had increased base prices to pass through higher labour and materials costs and fuel surcharges.

Employment rebounded and the unemployment rate fell in May

According to the May 2026 Labour force report, the number of employed people rose by a seasonally adjusted 40,300 over the month, with full-time employment up by 5,200 and part-time employment rising by 35,200. That was a much stronger outcome than the consensus forecast’s prediction of total employment growth of 32,500 and represented a marked bounce back after April’s steep decline (revised down from a fall of 18,600 in the original April release to a much larger drop of 40,700). It saw the employment to population ratio rise by 0.1 percentage point to 63.8%. The participation rate also increased last month, rising from 66.6% in April to 66.7%.

The Bureau noted that over the past few months it had recorded higher proportions of unemployed people waiting to start jobs who had then remained unemployed in the following month. This backlog of people waiting to start a job eased in May, contributing to that 40,300 increase in employment as well as to an 18,300 fall in the number of unemployed.

That decline in unemployment saw the unemployment rate fall by 0.1 percentage points to 4.4%, a result that was in line with the median market forecast. Although note that on a trend basis, the unemployment rate edged upwards (the ABS described it as increasing ‘marginally’), climbing from 4.3% to 4.4%.

While the underemployment rate rose from 5.8% to 5.9% this was not enough to fully offset the fall in the unemployment rate, and as a result, the overall underutilisation rate eased from 10.3% to 10.2%.

Finally, monthly hours worked in all jobs fell 1.1% over the month after having risen 0.9% in April. According to the ABS, May’s drop in the number of hours worked likely reflected payback from the strong April result, which had seen fewer people than usual take leave during the Easter holiday period and thereby contributed to non-seasonal strength in hours worked.

Job vacancies fell in May

The latest ABS Job Vacancies Survey estimates that the total number of vacancies in May 2026 was 329,500. That was down 2.1% (seasonally adjusted) from February this year and likewise down 2.1% from May 2025. It marked the first fall in vacancy numbers since August 2025.

Private sector vacancies fell 1.4% over the quarter while public sector vacancies dropped 7.9%. The Bureau also noted that as well as falling across both the private and public sectors, vacancies were down across most states and most industries.

Other Australian data points to note

This year’s Lowy Institute Poll reported that Australians registered ‘historical levels of distrust and unease in 2026.’ More than half of respondents (53%) reported feeling ‘unsafe’ in the world, setting a record high. It also found that almost six in ten Australians (59%) are pessimistic about Australia’s economic performance. That’s up 12 points from last year’s poll and marks another all-time high for the survey. On this measure, at least, Australians now feel worse about the economy than they did during the COVID pandemic and the Global Financial Crisis. The poll also reported that a majority of respondents (55%) reckon the total number of migrants coming to Australia is ‘too high’ (another poll record); a near-20 point drop (to 73%) from 2024’s poll in the share of respondents viewing cultural diversity as either ‘entirely positive’ or ‘mostly positive’; and a 12-point (to 64%) rise from the 2024 poll in the share saying the risks of AI outweigh the benefits.

The ABS Monthly Household Spending Indicator rose 1.3% over the month (seasonally adjusted, current prices) in May 2026 and grew 5.5% over the year. That was stronger than the consensus forecast, which had anticipated 0.5% month-on-month and 4.3% year-on-year increases. The Bureau notes that May’s increase largely reversed a 1.1% monthly decline recorded in the previous month and included strong rises in discretionary spending on hotels, cafes and restaurants and on clothing and footwear. Spending on fuel also remained elevated but according to the ABS continued to ease from the March 2026 peak because of the reduction in excise duty. Spending results were also influenced by travel-related refunds returning to normal after having been boosted in April due to flight cancellations triggered by the war in the Middle East.

New ABS data on Finance and Wealth shows that household wealth rose by $224.9 billion (up 1.2%) over the March quarter 2026 to $19,211.9 billion. The increase was driven by a $302 billion (2.5%) increase in the value of residential land and dwellings, which was partly offset by a decline in household superannuation assets and an increase in borrowing.

According to the latest ABS Characteristics of Australian Business, in 2024-25: 12% of businesses reported using AI in the workplace, up from just 1% in 2022-23, with the AI usage rate rising to 35% for large businesses; 59% of businesses reported disruptions to their supply chains; 21% reported experiencing a cyber security incident, a similar rate to 2021-22 (22%); 35% reported experiencing skills shortages; and 24% offered staff the ability to work from home, down from 31% in 2021-22.

The ABS said that the value of Engineering construction work done rose 7.1% over the March quarter 2026 (seasonally adjusted, chain volume measures) to be 5.3% higher over the year. Private sector engineering construction jumped 15.9% quarter-on-quarter and 14.5% year-on-year while public sector work done was down 3.5% in quarterly terms and 5.5% lower on an annual basis.

Further reading and listening

- A second chance for carbon pricing in Australia (inflection points)?

- Why taxing gas profits is harder than it looks (e61 Institute).

- Is Australia at risk of losing its ‘corporate brain’?

- RBA Deputy Governor Andrew Hauser’s speech to the Economic Society of Australia on the Phillips Curve and nonlinearity in the labour market.

- Since January this year, the rise in the US S&P 500 has been driven by AI and energy. Everything else is down.

- Marc Levinson considers the remaking of global trade.

- A look at China shock 2.0 and the eurozone from economists at the Bank of Italy.

- The Economist magazine analyses the United States’ plunging savings rate.

- The IMF examines how the energy shock has tested government budgets.

- This research finds that independent central banks take more financial risk than politically captured ones. The authors reckon that independence allows central bankers to focus on meeting their mandate without being constrained by potential losses or lower payments to treasuries.

- The WSJ’s Greg Ip remembers Alan Greenspan.

- Why AI and drones are the biggest revolution in the history of warfare.

- Why American data centres can’t plug in.

- The FT has been running a series on Brexit, 10 years on.

- I’ve now seen several links to this Apocalypse Early Warning System based on private jet flights.

- Related (kind of), how to survive a zombie apocalypse.

- The New Bazaar podcast on the AI shock vs the China shock.

- The Odd Lots podcast on what the world should know about Chinese AI.

- The Joe Walker podcast talks with Professor Patrick Weller about how prime ministers really govern.

Latest news

Already a member?

Login to view this content