Along with uncertainties around the implications of the new Omicron variant for the world economy, this week also brought Australia’s September quarter 2021 national accounts and a bunch of data on the Australian housing market. We have updated our GDP and Housing market chart packs to include the latest releases.

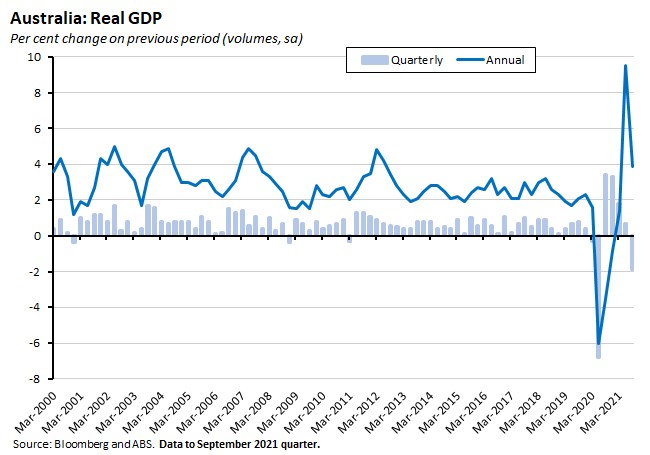

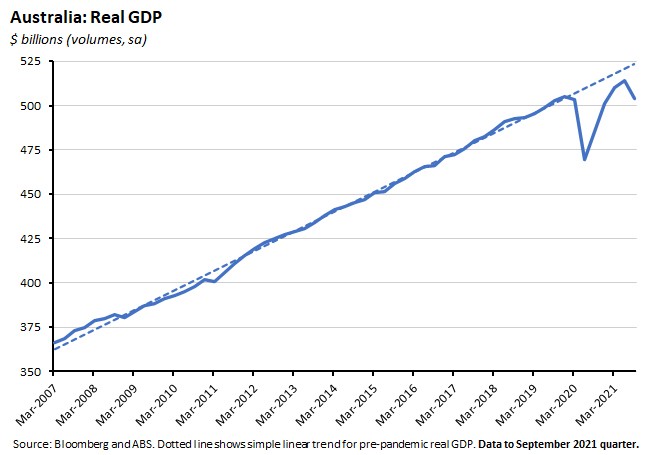

The main Australian data to land this week was the Q3:2021 national accounts. With the Delta variant having seen New South Wales, Victoria and the ACT placed under extended lockdowns for most of the September quarter of this year, real GDP was widely expected to have shrunk over the well below quarter, with the median forecast calling for a 2.7 per cent contraction. In the event, a milder than anticipated decline in household spending, plus offsetting support from government consumption and net exports, restricted the drop in output to a smaller 1.9 per cent decline. Even so, that was still the third largest fall in the history of the quarterly GDP series. It also leaves real GDP a little below its pre-pandemic level and well-below where it would have been in the absence of the COVID-19 shock.

The main message from this week’s national accounts data, then, was that the combination of the Delta variant and the subsequent state lockdowns has taken a significant toll on the Australian economy and pushed back the economic recovery. Even so, and significant as it was, the size of that toll was moderated by government and central bank policy, and – based on the economic releases seen to date for October and November – the September quarter’s contraction looks likely to be followed by a strong bounce back in the December quarter.

The GDP numbers are, of course, backward-looking and in terms of the future direction of the economy, this week’s GDP result perhaps best serves as a warning of the economic damage that COVID-19 can still wreak. The timing of that warning is important given the uncertainty surrounding the potential impact of the Omicron variant. On 26 November, the World Health Organisation (WHO) designated Omicron a variant of concern based on ‘a large number of mutations, some of which are concerning.’ The WHO noted that preliminary evidence ‘suggests an increased risk of reinfection with this variant’ although in a subsequent update it also noted the limited state of available knowledge, stating that it was ‘not yet clear whether Omicron is more transmissible…compared to other variants’ and similarly ‘not yet clear whether infection with Omicron causes more severe disease compared to infection with other variants.’ The implications for the efficacy of COVID-19 vaccines is likewise uncertain at this point, with contrasting opinions from the chief executive of Moderna (who warned that existing vaccines were likely to be much less effective against the new variant) and his counterpart at Pfizer (who claimed that fully vaccinated people would still have a high level of protection against severe disease).

With so much uncertainty around the nature of the Omicron variant itself, it’s hardly surprising that there is also a great deal of uncertainty around the potential economic implications, with any firm conclusions conditional on the nature of the answers to the questions over transmissibility, severity and vaccine efficacy. In the meantime, one early take was that the economic impact of Omicron was likely to be relatively limited, based on the hope that countries, governments and businesses are now more used to adapting to COVID-19 outbreaks and health restrictions and that the advanced stage of the vaccine rollout itself will offer at least some protection.

In testimony to Congress this week, Fed Chair Jerome Powell warned that ‘The recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation. Greater concerns about the virus could reduce people's willingness to work in person, which would slow progress in the labour market and intensify supply-chain disruptions.’ The latest OECD Economic Outlook, published this week, warned that the ‘failure to ensure rapid and effective vaccination everywhere is proving costly with uncertainty remaining high due to the continued emergence of new variants of the virus.’

This week’s linkage includes a roundup of commentary on Omicron, as well as a summary of some of the ABS data releases that didn’t make it into the main note this week, new OECD forecasts for Australia, lessons from a year of ranking COVID-19 resilience and why directors should never ignore that ‘Enron feeling.’

Listen and subscribe to our podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

The ABS said that Australia’s real GDP fell 1.9 per cent quarter-on-quarter (seasonally adjusted) in the September quarter of this year, although real output was still 3.9 per cent higher than in the same quarter a year ago.

Per capita GDP fell two per cent over the quarter and was up 3.5 per cent in annual terms, while real net national disposable income per capita fell 3.8 per cent quarter-on-quarter but grew 7.8 per cent year-on-year.

Nominal GDP shrank by 0.6 per cent over the September quarter but was 11.2 per cent higher over the year. That strong nominal annual growth reflects Australia’s still-high terms of trade: although they were up only 0.4 per cent over the quarter, the ratio of export to import prices was more than 23 per cent higher than in the corresponding quarter in 2020.

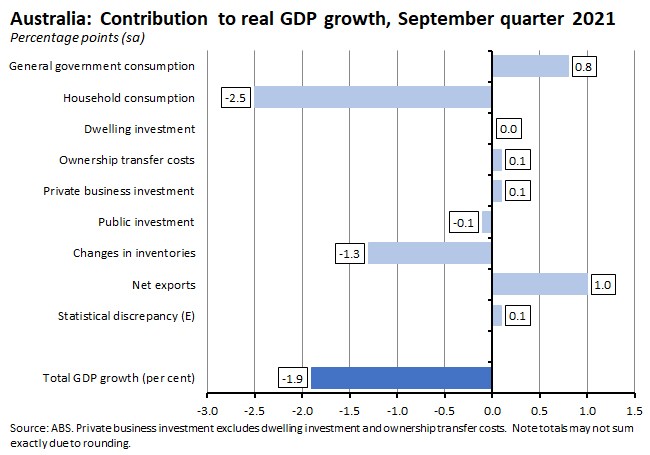

On an expenditure basis, the quarterly contraction in GDP reflected a sizeable decline in household consumption and a negative contribution from inventories as firms ran down their stocks. Those headwinds were partially offset by increases in general government consumption and a positive contribution from net exports.

Lockdowns and other restrictions saw household spending slump by 4.8 per cent over the quarter, with spending on services dropping by an even steeper 5.8 per cent. Services particularly exposed to lockdowns suffered from yet bigger declines in consumer spending, with a more than 40 per cent drop in spending on transport services, a greater than 20 per cent drop in spending on hotels, cafes and restaurants, and an almost 12 per cent drop in spending on recreation and culture. The household saving ratio also jumped from 11.8 per cent in the June quarter of this year to 19.8 per cent in the September quarter as the decline in spending met a rise in household gross disposable income.

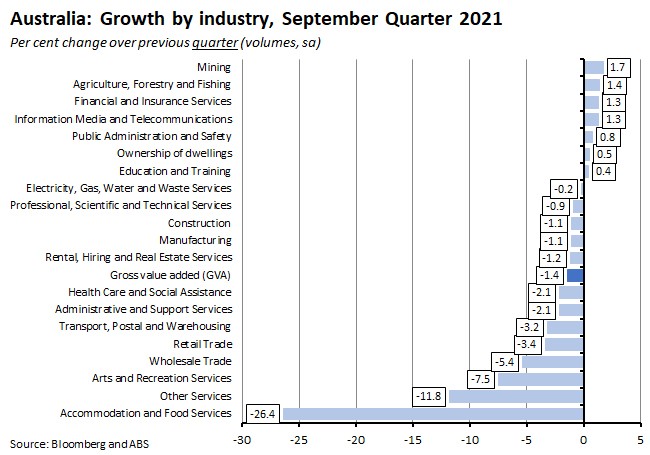

On the production side of the national accounts, gross value added (GVA) fell 1.4 per cent over the quarter. Again, the biggest declines were suffered by those industries most affected by lockdowns, with big quarterly falls for accommodation and food services, other services, and arts and recreation services.

On the income side of the national accounts, the impact of the Delta variant was apparent in a strong 3.3 per cent rise in public compensation of employees (COE) – the fastest growth since the June quarter of 2010 – reflecting an increase in the provision of government services to manage the pandemic; in the large contribution made to quarterly growth in household disposable income by social assistance benefits (which contributed 2.6 percentage points of a 4.6 per cent growth rate); and in a boost to the gross operating surplus (GOS) of the non-mining sector delivered by government subsidies paid to Australian businesses affected by COVID-19 related restrictions.

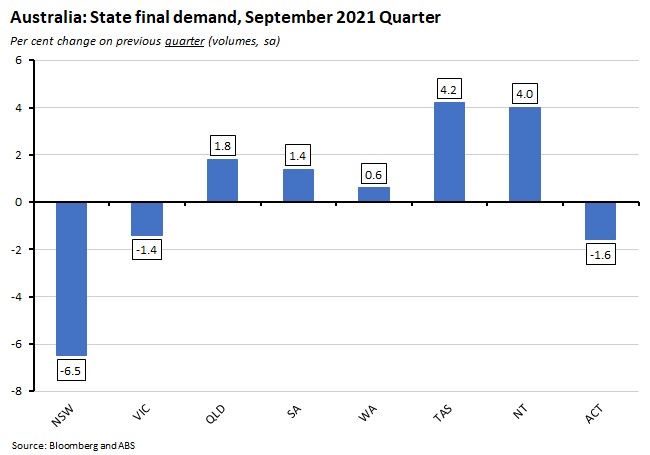

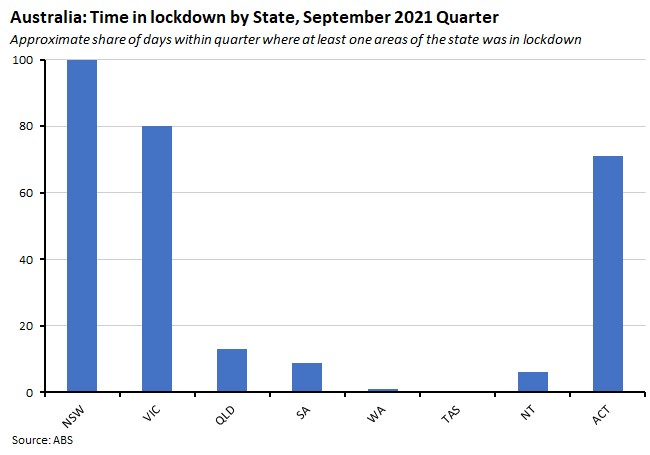

Data on State final demand was also dominated by pandemic-related effects. New South Wales, Victoria and the ACT all suffered extended lockdowns during the September quarter, while there were several short lockdowns in Queensland, South Australia and the Northern Territory. State final demand fell 6.5 per cent over the quarter in New South Wales, 1.4 per cent in Victoria and 1.6 per cent in the ACT, reflecting sharp drops in private consumption and investment spending as public health restrictions and Delta-concerns hit households and businesses.

For more detail on the September quarter GDP release, please take a look at our updated GDP chart pack.

The ABS release also included three articles on the national accounts this quarter, one on international and state economies during the September quarter 2021, one on insights from alternative data on lockdowns and consumption, and one on approaches by the Bureau to improve measures of household consumption.

Why it matters:

Judged against market expectations, the outcome for Q3:2021 GDP was better than expected. The median forecast had called for a 2.7 per cent contraction and official projections had previously suggested a three per cent decline could be on the cards. So, from that perspective, an actual decline of ‘just’ 1.9 per cent represented a positive surprise. On the other hand, this was still the third largest drop in GDP in the history of the quarterly series, beaten only by the pandemic-driven 6.8 per cent crash suffered in the June quarter of 2020 and a two per cent fall in the June quarter of 1974. As a result, GDP is back to being below its pre-pandemic level and well-below where it would have been in the absence of the COVID-19 crisis. Seen on that basis, this was powerful testimony to the ongoing ability of COVID-19 and the related public health measures to take a heavy toll on economic activity, and of the economic costs of the failure of the quarantine and test and trace systems to manage the Delta variant in New South Wales and beyond.

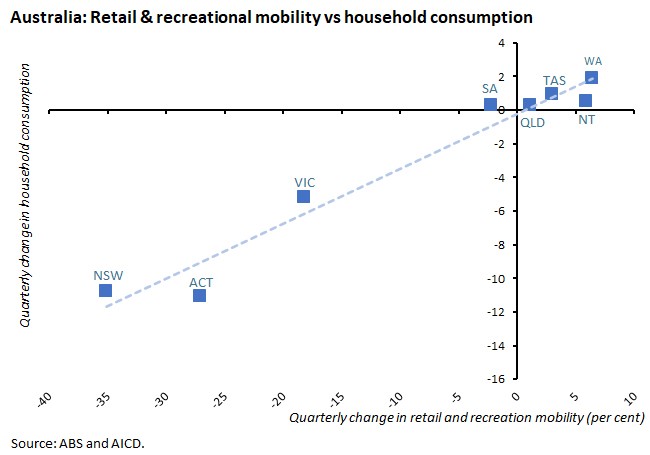

Evidence of the significant impact of lockdowns, other public health restrictions and voluntary shifts in economic behaviour was visible in the steep quarterly decline in overall private demand, in the big fall in household consumption (albeit not as big as the Q2:2020 slump in household spending), in the outsized decline in spending on services in particular, and in the state-level pattern of economic activity. With regard to the latter, for example, the Bureau noted that NSW, Victoria and the ACT were much more heavily impacted by lockdowns than the other states and territories.

No surprise, then, that ABS also noted that household spending in the three most impacted states and territories fell 8.4 per cent compared to a 0.7 per cent rise for the rest of Australia, as lower levels of retail and recreational mobility in those geographies subject to extended lockdowns coincided with large declines in consumption.

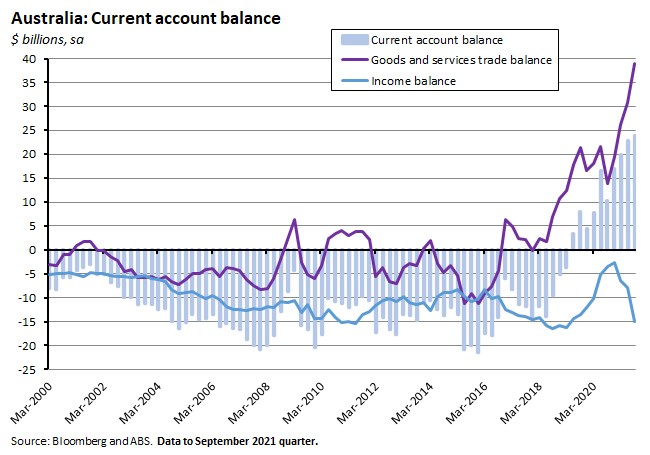

According to the ABS, Australia recorded a current account surplus of $23.9 billion (seasonally adjusted) in the September quarter of this year. That was an increase of $1 billion over the June quarter surplus. The balance on goods and services rose from a $30.1 billion surplus in the June quarter to a $38.9 billion surplus in the September quarter, while the deficit on the income account (primary and secondary) increased from $7.9 billion to $15 billion.

The corresponding deficit on the capital and financial account fell $2.6 billion to $21.8 billion in the September quarter, reflecting a financial deficit of $21.7 billion. The latter comprised a net outflow of equity of $14.8 billion and a net outflow of debt of $6.9 billion.

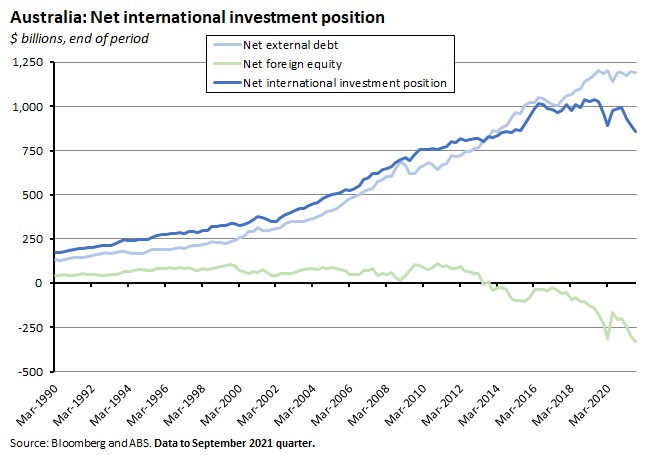

Australia’s net international investment position was a liability of $860.1 billion at 30 September 2021, a fall of $38.3 billion on the (revised) June quarter number, driven by a $3.8 billion decline in the net foreign debt liability position and a $34.5 billion increase in the net foreign equity asset position.

Why it matters:

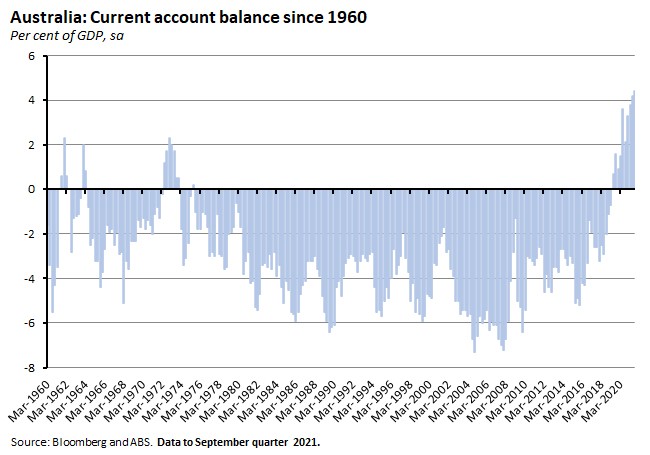

After having already delivered a record current account surplus record in the June quarter, Australia set another new record with the September quarter data. Once again, the key driver was a big goods trade surplus powered by a surge in the dollar value of exports.

Sitting behind that robust export performance were strong prices for exports of coal and other mineral fuels as well increased volumes of agricultural exports.

The transformation in Australia’s external accounts has now delivered ten consecutive quarters of current account surpluses. Prior to that, Australia had reported current account deficits for 175 quarters in a row, with the last time the current account was in surplus coming in the June quarter of 1975.

The shift in the structure of the balance of payments is also apparent in Australia’s net international investment position, where net liabilities are now equivalent to about 40.6 per cent of GDP. That’s the lowest ratio recorded since the September quarter of 1988.

What happened:

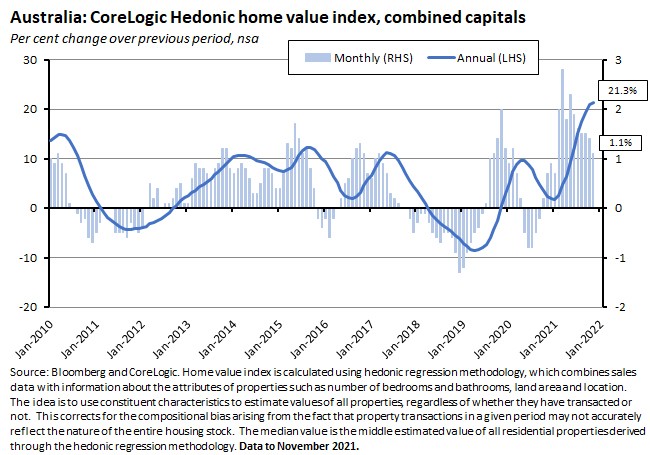

CoreLogic said Australian national housing values rose 1.3 per cent over the month in November this year to be 22.2 per cent higher in annual terms. Regional markets outperformed capital cities last month, with monthly prices rising at double the combined capital rate: the combined capitals index rose 1.1 per cent over the month and four per cent over the year, while the combined regional index was up 2.2 per cent in monthly terms and 5.9 per cent year-on-year.

Of the capital cities only Darwin (down 0.4 per cent) saw dwelling values fall in November with the strongest monthly growth in Brisbane (up 2.9 per cent) and Adelaide (up 2.5 per cent).

According to CoreLogic, houses have continued to outperform units, with capital city values up 1.2 per cent in the former and 0.7 per cent in the latter in November. While the gap between the two growth rates has now narrowed to its smallest since October last year, based on median values capital city houses are now almost 38 per cent more expensive than capital city units – the largest difference on record.

Why it matters:

November marked the 14th consecutive month of rising dwelling values in Australia, although it was also the softest monthly growth rate recorded since January of this year, continuing the trend of a gradual easing in momentum. CoreLogic pointed to a rise in the number of homes available for sale as a key factor behind the slowing in price growth, noting that on a national basis the number of new listings added to the market over the month to 28 November was tracking 15.7 per cent above the five year average, which is the highest level since late 2015. CoreLogic also pointed to a modest rise in the median number of days taken to sell a property and a decline in auction clearance rates, both of which are consistent with some limited softening in the market. Rising fixed term mortgage rates, declining housing affordability (the ratio of house values to household incomes reached a new record high in June, as did the time needed to save for a deposit), and tighter credit conditions are all now headwinds for the housing market, although if border opening remains on track (Omicron permitting – there has already been some tightening of border restrictions), that should be an offsetting future positive for housing demand.

What happened:

Along with the house price data discussed in the previous story, this week brought several other data releases on the state of the Australian housing market.

- ABS data on building approvals for October 2021 showed the number of dwellings approved fell 12.9 per cent over the month (seasonally adjusted) to be down 8.1 per cent over the year. Approvals for private sector houses were up 4.3 per cent month-on-month but down 3.7 per cent year-on-year, while approvals for private sector dwellings excluding housing slumped 37.5 per cent month-on-month and were also down 16.5 per cent in annual terms.

- According to the RBA, total credit for housing rose 0.6 per cent over the month in October this year (seasonally adjusted) to be up 6.7 per cent in annual terms. The pace of monthly growth was unchanged from September’s result but the pace of year-on-year growth has accelerated.

- The ABS said that in October 2021, new loan commitments for housing fell 2.5 per cent month-on-month (seasonally adjusted) but were still up more than 32 per cent in annual terms. Lending to owner-occupiers fell 4.1 per cent in monthly terms while rising 15.1 per cent over the year, while lending to investors rose 1.1 per cent over the month and jumped 89.6 per cent relative to October 2020.

For more detail on these releases, please see the updated Housing market chart pack.

Why it matters:

Signs of easing momentum in the pace of gain in home prices (see previous story) were also consistent with some weaker-than-expected readings for dwelling approvals and new lending.

In the case of the former, the market had expected a fall in dwelling approvals in October, but the actual monthly decline of 12.9 per cent significantly exceeded the median forecast of a 1.5 per cent fall. That larger than expected fall was the product of a substantial 37.5 per cent slump in approvals for private sector dwellings excluding houses. Note, however, that approvals are still comfortably up relative to pre-pandemic levels.

Similarly, while the median forecast for new lending in October was for a 1.5 per cent rise, the actual outcome of a 2.5 per cent decline was another surprise to the downside, reflecting a more than four per cent drop in lending to owner-occupiers. Lending to first-time buyers also fell again in October. On the other hand, new loan commitments to investors rose to near-record levels, climbing to their highest level since the record high hit in April 2015.

What happened:

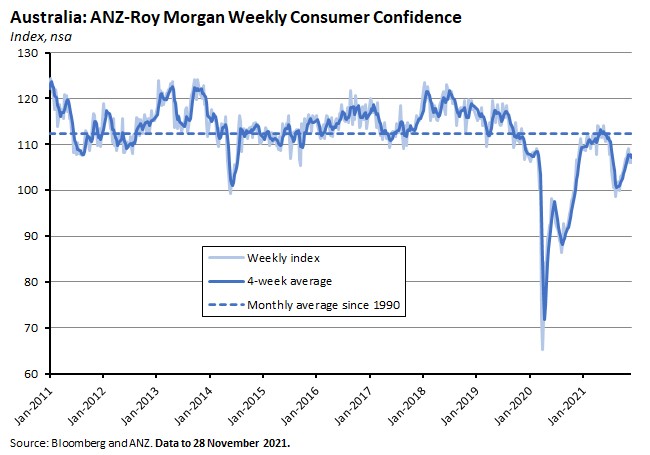

The ANZ-Roy Morgan Consumer Confidence index fell 1.3 per cent last week.

Four of the five subindices fell over the week, with a particularly large fall for ‘future economic conditions’, which slumped 5.9 per cent in its biggest drop since April 2020. The only increase was for ‘time to buy a major household item.’

Weekly inflation expectations rose to 4.8 per cent last week from 4.6 per cent the week before but remain below the five per cent rate reached earlier this month.

Why it matters:

The drop in the weekly measure of consumer sentiment likely reflects news of the Omicron variant and the subsequent imposition of some new restrictions on international travel.

What happened:

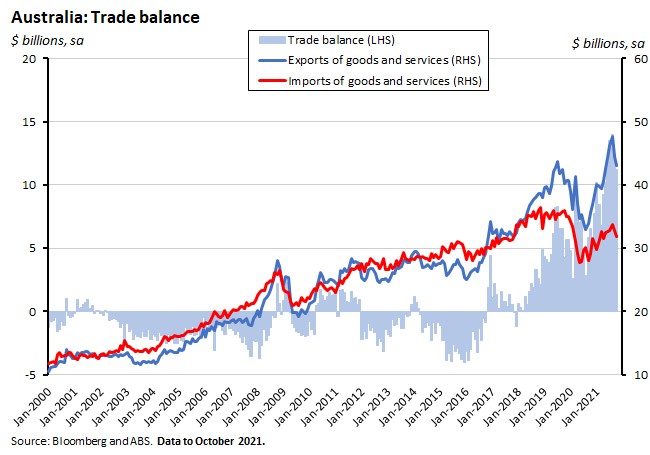

The ABS said that Australia recorded a goods and services trade surplus of $11.2 billion in October 2021, down $0.6 billion from September’s result. Exports of goods and services fell three per cent or by $1.5 billion over the month to $43.1 billion while imports of goods and services also fell three per cent, or by $0.9 billion, to $31.8 billion.

Why it matters:

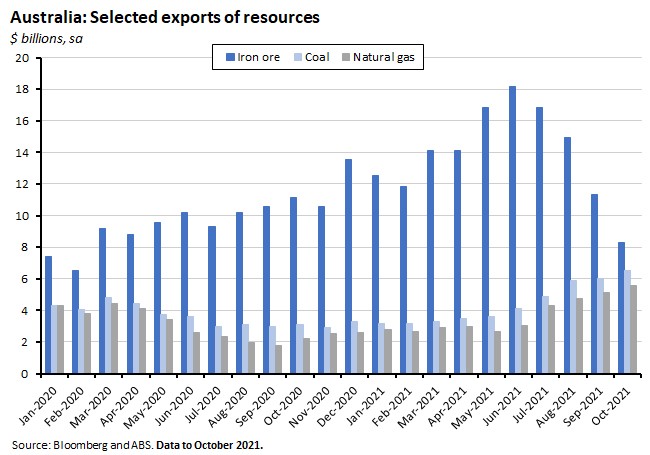

October’s actual trade surplus was close to the median forecast with the decline from the September reading largely reflecting another large fall in the value of iron ore exports that was only partially offset by rising values of coal and gas exports.

Also of note was a decline in imports of capital goods, which fell eight per cent over the month, and which may in part reflect ongoing disruption to global supply chains.

What happened:

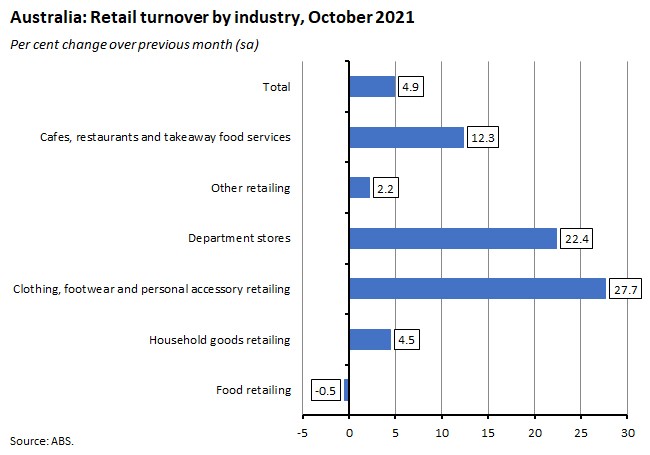

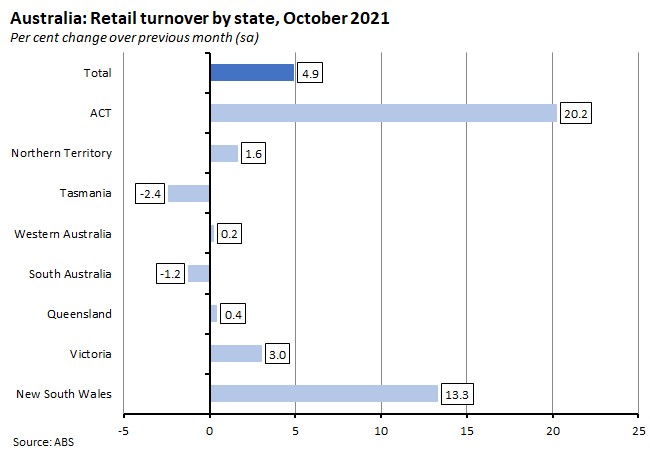

Last Friday, the ABS said that nominal retail turnover in October this year rose 4.9 per cent month-on-month (seasonally adjusted) to be up 5.2 per cent over the year.

By industry, growth in turnover was up sharply in clothing, footwear and personal accessory retailing and in department stores and there was also strong growth for cafes, restaurants and takeaway food services.

By state and territory, retail turnover jumped over the month in the ACT and New South Wales and also grew at a decent clip in Victoria.

Why it matters:

October’s 4.9 per cent monthly increase in retail turnover was the strongest result since Victoria’s first lockdown bounce in November 2020. Retail turnover is now back at its highest level since June 2021, before the onset of the Delta variant and consequent state lockdowns. That should be good news for prospects for a strong bounce back in growth in the December quarter.

The impact of the pattern of exit from lockdown shaped the monthly data, with strong rises in retail turnover in the ACT and New South Wales and a healthy increase in Victoria (New South Wales existed lockdown on 11 October, the ACT on 15 October and Victoria on 22 October). Similarly, turnover was up sharply in industries benefitting from increased mobility including clothing and footwear, department stores and cafes and restaurants.

A small selection of Omicron linkage . . .

- An article in Nature on the mutated Omicron variant.

- Noah Smith on the Omicron situation.

- The ABC on what we know about Omicron.

- And an FT explainer.

- A roundup of pieces on the new variant from the Economist magazine.

- And a guide to navigating the all the noise around Omicron from Bloomberg.

Regular linkage . . .

- As well as the series of ABS publications covered in the main text, there were a range of other releases from the Bureau this week, including data on business indicators (company gross operating profits were up four per cent over the September quarter while wages and salaries fell 0.8 per cent, both series seasonally adjusted) and on mineral exploration expenditure. The ABS also published Government Finance Statistics for the September quarter of 2021, which showed the general government net operating balance swing from a small surplus of $2.3 billion in Q2:2021 to a deficit of $45.4 billion in Q3:2021, as total general government revenue fell by almost 14 per cent over the quarter while general government expenditures increased by more than nine per cent. See also an article on insights into government finance statistics.

- The week’s big data download from the ABS also included numbers on regional population for the 2019-20 financial year. These showed population rose by 1.4 per cent in Australia’s capital cities, outpacing growth in regional Australia of 1.1 per cent. Brisbane (up 1.9 per cent) and Perth (up 1.8 per cent) saw the highest growth rates out of the capital cities while Melbourne (up 80,100 people) and Sydney (up 57,100 people) experienced the largest absolute increases. The only capital city to see a fall in population was Darwin (down 180 people or a fall of 0.1 per cent).

- The ABS has also released experimental estimates on electric passenger vehicle use in Australia.

- Grattan’s Danielle Wood gave the John Button Oration on The Next Generation’s Australia.

- Also from Grattan, calls for a social housing future fund.

- Deputy Governor Guy Debelle with a speech on the Indigenous Economy in Australia and the RBA.

- Also from the RBA, a new Research Discussion Paper on the effect of Corporate Sentiment on Investment. Author Gianni La Cava constructs a new company level indicator of business sentiment based on Australian company disclosures (the net balance of positive and negative words used in their annual reports) and finds that company-level investment is very sensitive to this measure even after controlling for fundamentals such as expected profits and measures of company-level uncertainty: a company that uses more positive words / fewer negative words is higher in sentiment and more likely to invest, all else equal. The paper suggests that while a decline in sentiment and a rise in uncertainty both contributed to weak investment during the GFC, subsequently it has been demand side effects such as sales growth that have been more important drivers of subdued capex in Australia.

- From the Department of Industry, the latest quarterly update on Australia’s greenhouse gas emissions. Emissions in the year to June 2021 were down 2.1 per cent in annual terms and 20.4 per cent lower than in 2005 (the baseline year for the Paris Agreement).

- And from the Australian National Audit Office, a new report on the administration of Australia’s R&D Tax Incentive.

- The OECD published its December 2021 Economic Outlook. The forecast for Australia sees real GDP growth accelerating from 3.8 per cent this year to 4.1 per cent in 2022 before moderating to three per cent growth in 2023. The OECD also warns the RBA to be ‘vigilant about signs of rising inflation’ and says the central bank ‘may need to tighten monetary policy faster than it is currently anticipating.’ The forecasts have headline CPI inflation at 2.7 per cent next year before easing to 2.1 per cent in 2023.

- Also from the OECD, new work on COVID-19 and well-being.

- In the WSJ, Greg Ip looks at the different performances of US states on public health and economic activity during the pandemic, and argues that – contrary to some findings for elsewhere in the world economy – in the US there is evidence of an inverse relationship between infections and economic activity. Political partisanship also has an important influence on patterns in the data.

- Why metals may become the new oil. The new technologies needed to hit net zero emissions commitments – renewable energy, electric vehicles, hydrogen, carbon capture – are more metals-intensive than their fossil fuel counterparts. One potential implication is prices for copper, nickel, cobalt and lithium could reach historical peaks for a sustained period.

- The IMF on how domestic violence is a threat to economic development. And the IMF’s chart of the week on how the rich get richer, as for a given portfolio allocation, individuals who are wealthier are more likely to get higher risk-adjusted returns, possibly because they have access to exclusive investment opportunities or better wealth managers.

- The Economist on measuring the share of the property sector in China’s GDP. Depending on the source, estimates range from a high of 29 per cent of GDP to 23 per cent to as low as 15 per cent.

- Updated residential property prices from the BIS.

- Bloomberg looks back at a year of ranking COVID-19 resilience and finds that past performance has not been a great guide to future success. Early on, the top performers were countries that deployed tough containment strategies including quarantines and border restrictions (New Zealand, Singapore). Then it was those who could roll out vaccination programs at speed, although here early leaders (the US, Israel) were caught out by a subsequent flare up of the pandemic. Bloomberg’s top performers – defined as the group of countries that consistently scored above average throughout the history of the rankings to date – comprise seven countries: Norway, Denmark, Finland, the UAE, Canada, South Korea and Switzerland. On the narrower definition of preventing death (less than 100 deaths per million people), the top performers include China, New Zealand, Taiwan, South Korea and Australia.

- From the FT, the queasy ‘Enron feeling’ directors should never ignore.

- The Macro Musings podcast talks to Matt Klein on US inflation.

Latest news

Already a member?

Login to view this content