Overview

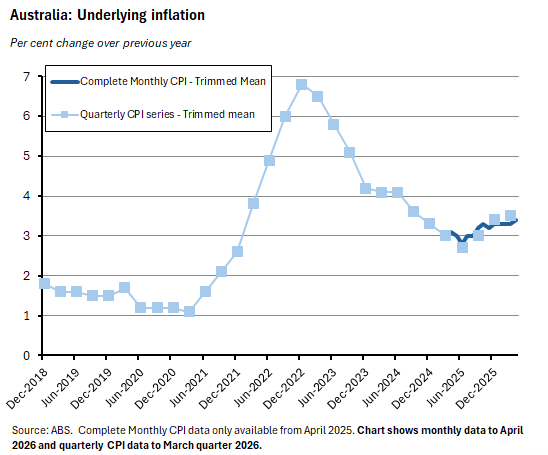

- April’s inflation reading reported a fall in the headline rate alongside a slight increase in underlying inflation as measured by the monthly version of the trimmed mean measure. The mixed messages haven’t changed market assessments that the RBA will likely keep monetary policy on hold next month.

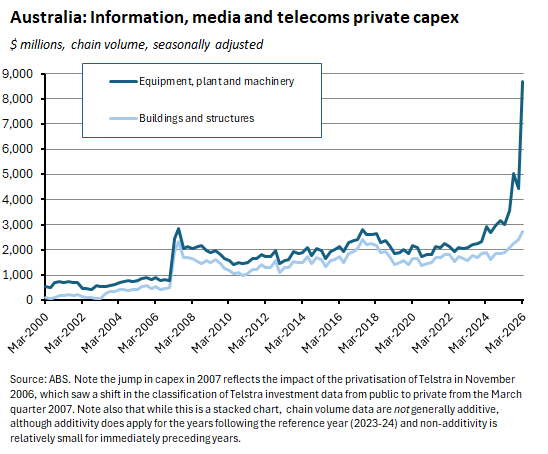

- The March quarter 2026 numbers on private capital expenditure highlight the increasingly significant role played by data centre investment.

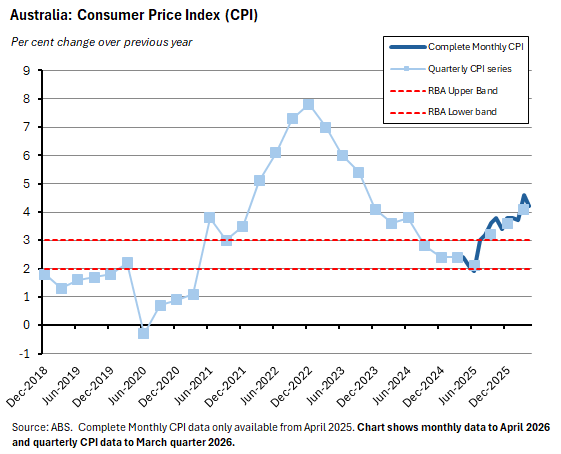

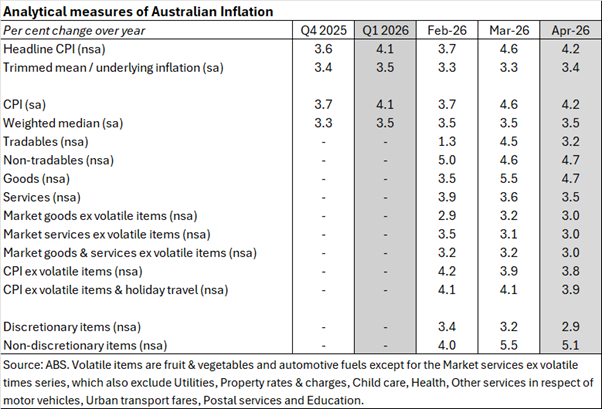

While global economy watchers continue to struggle to extract a signal from the ongoing noise around the war in the Middle East – talk of progress in negotiations alongside new US strikes on Iran dominated this week’s headlines – the main data drop on the domestic front was the April Consumer Price Index (CPI) reading. Headline CPI inflation surprised to the downside, with the annual rate falling from 4.6% in March to 4.2% last month. Underlying inflation printed in line with market expectations at 3.4%, however, which was up slightly from the March reading of 3.3%.

That set of numbers does little to change last week’s judgement that the Monetary Policy Board (MPB) is likely to vote to leave the cash rate target unchanged at 4.35% at its next meeting on 15-16 June. Consistent with this, market pricing continues to see only a very modest chance of a further dose of monetary policy tightening next month (although one further 25bp rate increase is still expected by year-end). Pausing will give the central bank time to assess the shifting balance of risks around inflation and activity, and – just perhaps – allow time for more clarity to emerge about developments in the Persian Gulf.

We provide a little more detail on the inflation numbers below and also highlight how the ongoing boom in data centre investment is shaping the capital expenditure statistics. This week’s reading and listening roundup includes some further reflections on Budget 2026 and the continuing, heated debate around tax settings.

Finally, just a quick mention that I will be delivering the AICD’s annual national economic update on 11 June.

Headline inflation down but underlying inflation up

The headline monthly Consumer Price Index (CPI) rose 0.4% over the month in April 2026 (original basis) to be up 4.2% over the year. That marked a slowdown from the March result, when the corresponding monthly and annual rates of increase were 1.1% and 4.6%, respectively. It was also a softer reading than the market had expected, with the consensus forecast having predicted 0.6% monthly and 4.4% annual outcomes.

The slowdown in inflation was in large part a product of government policy in the form of the three-month-long cut in the fuel excise tax from 56.2 cents/litre to 20.6 cents/litre, which took effect from 1 April. That policy change saw automotive fuel prices drop 7% over the month after having jumped by 32.8% in March. Their annual rate of increase also slowed, falling from 24.2% in March to 18.6% in April. Lower fuel prices meant that the Transport Group overall fell 2.7% over the month while the corresponding annual growth rate eased from 8.9% to 6.6%.

Lower fuel prices likewise contributed to a slowdown in the rate of goods price inflation (down from 5.5% the previous month to 4.7% in April) and in annual tradables inflation (down from 4.5% to 3.2%). Services inflation also edged lower last month, slipping from an annual rate of 3.6% to 3.5%. On the other hand, non-tradables inflation ticked up from 4.6% to 4.7%.

While the annual rate of headline inflation eased in April, underlying inflation as measured by the monthly version of the trimmed mean increased relative to the March result. The series was up 0.3% over the month (seasonally adjusted) and 3.4% over the year, compared to March monthly and annual readings of 0.2% (revised) and 3.3%, respectively. Those numbers were also in line with the consensus forecasts.

Other measures of underlying inflation painted a mixed picture. The weighted median series, for example, rose 3.5% over the year in April, unchanged from March, while the annual rate of increase in the CPI ex volatiles and holiday travel measure slowed to 3.9% in April from 4.1% in March.

Overall, the headline April numbers show that the government’s policy intervention has worked to limit the immediate increase in the headline rate and thereby delivered a better-than-expected result. At the same time, however, underlying inflation as measured by the monthly version of the trimmed mean did increase, moving slightly further away from the top of the RBA’s target band. On balance, none of this is likely to be enough to materially shift the central bank’s inflation assessments before next month’s MPB meeting. Financial markets seem to agree, with the implied market probability of a rate hike in June still at very low levels.

Australia’s data centre investment boom gathered pace last quarter

Total new private capital expenditure (capex) in Australia rose 6.5% (seasonally adjusted) over the March quarter 2026 to be up 14.6% over the year. By subcomponent, the ABS said the increase was driven by capex on equipment, plant, and machinery, which surged 18.1% quarter-on-quarter and jumped 31% year-on-year to reach a new record. In contrast, spending on buildings and structures fell 3.8% over the quarter and was up just 0.8% on an annual basis.

The Bureau attributed the March quarter’s robust growth in capex to investment in data centre equipment, specifically server racks and processing equipment. According to the ABS, investment in machinery and equipment by the Information, media and telecommunications sector soared by 196.1% last quarter, sending overall investment by the sector up 96.1% to hit a new record level.

The quarterly decline in total private capex on building and structures, on the other hand, was largely due to projects reaching completion, with the Bureau noting that investment in data centre building construction continued to grow.

Other Australian data points to note

The ABS Monthly Household Spending Indicator (HSI) fell 1.1% month-on-month (seasonally adjusted) in April 2026 but was still 4.9% higher than the April 2025 reading. The Bureau said the main driver of the fall in household spending was a 4.7% monthly decline in spending on transport costs. A drop in spending in air transport was the largest factor here along with a fall in spending on public transport in states offering free travel. The ABS also noted an increase in new vehicle sales with a significant rise in EV purchases.

The ABS said that total construction work done in the March quarter 2026 was $84.4 billion (chain volume, seasonally adjusted estimate). That was up 3.4% from the previous quarter and 6.3% higher than in the March quarter 2025. The market consensus had anticipated much more moderate quarterly growth at 0.8%. Within that total, building construction ($44.7 billion) was up 0.6% quarter-on-quarter and 7.8% higher year-on-year while engineering construction ($38.7 billion) grew by a strong 6.9% on a quarterly basis and 4.7% on an annual basis. Breaking down the building component, residential construction fell 0.6% over the quarter but rose 5.6% over the year, while non-residential construction rose 2.5% over the quarter to be up 11.2% over the year.

According to the newly restored ABS Business Conditions and Sentiments survey, some 72% of Australian businesses reported that current fuel prices or fuel availability negatively impacted their business in May this year; 60% reported making changes to operations due to fuel prices or availability; 28% reported changes to their workforce (including 9% making cuts to workforce numbers); and 17% reported delays or cancellations to capital investment plans. Half of all businesses reported a rise in operating costs and 36% reported a reduction in revenues. In addition, 16% of Australian businesses said they experienced supply chain disruptions, with the Agriculture, forestry and fishing (42% of affected businesses) and retail trade (31%) the two most impacted industries.

The ANZ-Roy Morgan weekly consumer confidence index was down 0.3 points to a reading of 66.1 for the week ending 24 May 2026. That means confidence remains around historical lows – the reading was the eighth lowest in the history of the series. Weekly inflation expectations rose by 0.1 percentage points to 6%.

Further reading and listening

- The Grattan Institute identifies some budget myths.

- A useful AFR explainer on Budget 2026’s changes to CGT.

- Related, the e61 Institute on the complexities of taxing capital income.

- Also related, the OECD says that empowering public understanding is now an essential part of modern budgeting.

- The May 2026 edition of the RBA Bulletin includes insights from new data on Australian housing investors (investors tend to be older with a median age of 51 and earn higher incomes) and a look at the theory, measurement and implications of margins, mark-ups and consumer prices (some sector-specific dynamics seem to have pushed down both margins and aggregate inflation in early 2025 but then unwound and accentuated the pick-up in inflation later that year, but overall changes in margins had only a modest impact on inflation dynamics).

- Why Australia can’t deliver megaprojects on time and on budget. Problems include prematurely announcing projects with no credible business case; a lack of independent scrutiny including the power to pause projects; and poor transparency. A fix requires dealing with all three.

- The Climate Council’s Clean Energy Australia 2026 report reckons that renewable energy generated 43% of Australia’s electricity last year, up from 39% the year before. Australia also became the third-largest utility-scale battery market in the world. At the same time, just 2.3GW of new renewable energy generation projects reached financial close in 2025, one of the lowest levels in a decade.

- Against ‘affordable’ housing.

- The WSJ’s Grep Ip casts a wary eye over the dangerous brew that’s rattling bond markets – out-of-control government borrowing, above-target inflation, heavy corporate borrowing to fund AI infrastructure, the rise of populism, and a series of adverse global supply shocks.

- The WHO on the Ebola outbreak in the Democratic Republic of the Congo.

- Related, research on estimating the size of the Ebola outbreak.

- China’s biotech giant: a look at the empire of Wuxi.

- From the LRB, John Lanchester on money laundering.

- The FT’s Martin Wolf on the infantilism of an ‘ungovernable’ Britain. According to Wolf, a bad economy creates bad politics and bad politics create a bad economy, making the collapse in UK growth ‘the most important fact about British economics and politics’ and creating ‘a nightmare of fiscal crises and “affordability crises” without end.’ Related, an earlier FT Big Read on Britain’s debt cage.

- The World Bank says carbon pricing now covers 29% of global greenhouse gas emissions and mobilised more than US$107 billion for public budgets last year. The average carbon price was around US$21/tCOE2e.

- According to the OECD, developed countries met their goal to mobilise US$100 billion annually for climate action in developing countries for the three consecutive years between 2022 and 2024. Climate finance support reached US$136.7 billion in 2024.

- The Economist magazine says China’s solar industry is in turmoil due to a combination of exhausted domestic demand, excess supply, and rising overseas protectionism.

- A look at the evidence on corporate net zero targets finds that headline net zero pledges alone should not be treated as reliable indicators of near-term emissions performance.

- Falling public listings and rising numbers of investment vehicles mean there are now more ways to trade the US market than there are stocks in that market.

- New IMF research on the post-COVID inflation shock.

- How to find AI in the (US) GDP statistics.

- How AIs see our world.

- The Ezra Klein podcast has a wide-ranging talk with Yuval Noah Harari.

- The Conversations with Tyler podcast asks Toby Wilkinson about Ptolemaic Egypt and the first great commercial civilisation.

Latest news

Already a member?

Login to view this content