Overview

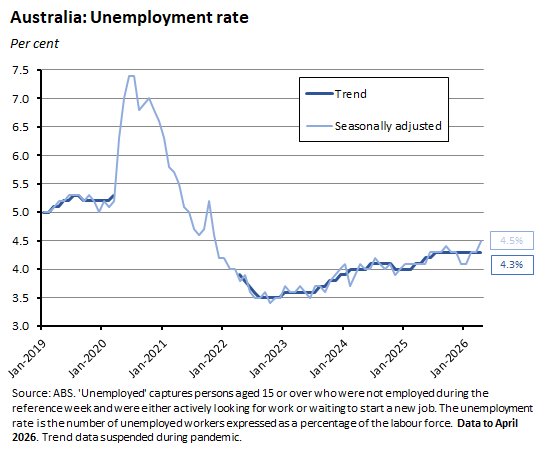

- The April 2026 Labour Force results printed weaker than the market had expected, with employment down and the unemployment rate up to 4.5%. Monetary policy tightening and the war in the Middle East may now be starting to hurt the labour market.

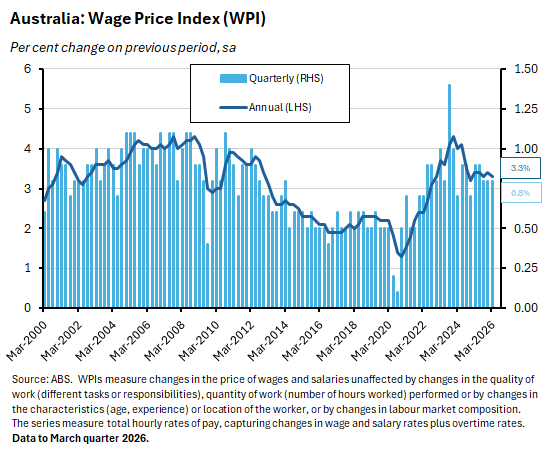

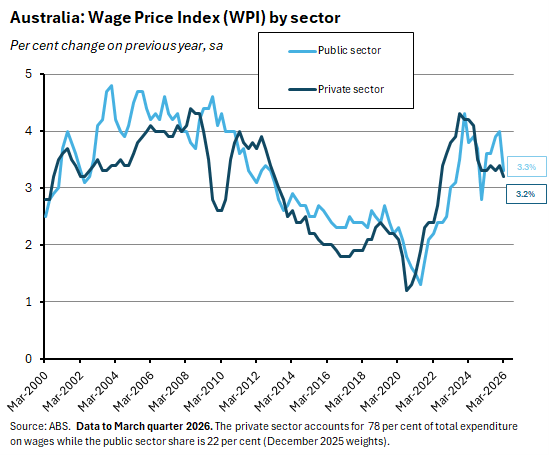

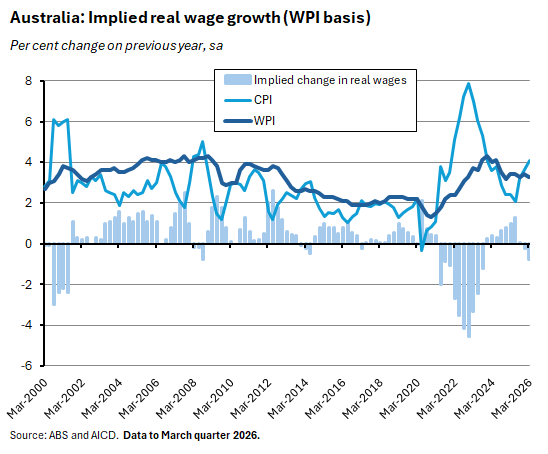

- The annual rate of nominal wage growth was little changed in the March quarter 2026, at 3.3%. That was not enough to keep pace with inflation, delivering a second consecutive fall in real wage growth. Private sector nominal wage growth edged down to an annual rate of 3.2%, the softest result since the June quarter 2022.

- Last week’s RBA Minutes rehearse the arguments behind the MPB’s recent 8-1 vote to increase the cash rate target by 25bp. The shift to a tighter policy stance should give the Board space to consider the impact of developments in the Persian Gulf and reduce the pressure for a June rate hike.

- Recent data on consumer sentiment suggests a mixed response to Budget 2026 while the latest business survey highlights a sharp jump in purchase costs last month.

The main news on the Australian data front this week was a weaker-than-expected labour market report for April 2026. The (seasonally adjusted) unemployment rate rose by 0.2 percentage points to 4.5% while employment dropped by 18,600 persons. Both results were softer than the market had expected. Last month’s surprisingly weak outcome should not be exaggerated: the monthly numbers can be volatile; measured on a trend basis the unemployment rate was unchanged at 4.3% in April; hours worked were still up over the month; and the underemployment rate was down a little. Still, it is not unreasonable to think that this week’s release could signal the first crack in what up until now has been an impressive display of labour market resilience.

Combined with the messaging in the Minutes from the Monetary Policy Board (MPB) meeting held earlier this month, the recent signs of labour market easing should push against any case for a fourth consecutive rate increase when the MPB meets again in June. If April’s result does indicate a more lasting shift, that would indicate risks to the RBA’s latest (May 2026) forecasts, which ‘only’ expect the unemployment rate to end this year at 4.3% before rising to 4.6% by the end of next year.

We dig into the labour market numbers and the MPB Minutes in a little more detail below, along with a look back to another labour market indicator in the form of last week’s wage data.

April’s labour market results were weaker than expected

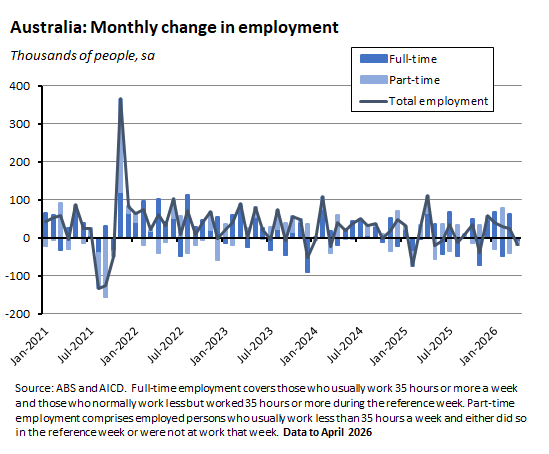

According to the April 2026 Labour Force report, seasonally adjusted employment in Australia fell by 18,600 people in April 2026. Full-time employment declined by 10,700 while part-time employment dropped by 7,900. In contrast, the market consensus forecast had expected employment to rise by 15,000.

The unemployment rate rose to 4.5% after the number of unemployed people increased by 33,000, with the ABS noting that ‘compared to what we usually see in April, more people remained unemployed.’ The market had expected an unchanged rate of 4.3% so again, the outcome was worse than anticipated. But note that on a trend basis, this was the result.

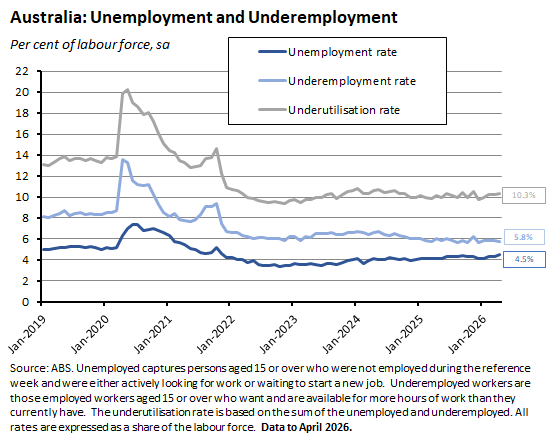

Although employment was down 0.1% over the month, hours worked still rose, up by 16 million hours or 0.8%. And the underemployment rate fell by 0.1 percentage points to 5.8%. As a result, the overall underutilisation rate edged up from 10.2% in March to 10.3% in April.

The participation rate ticked down from 66.8% in March to 66.7% in April while the employment-to-population ratio fell 0.2 percentage points from 63.9% to 63.7% over the same period.

Nominal wage growth was little changed last quarter

Last week, the ABS published the March quarter 2026 Wage Price Index (WPI). The seasonally adjusted WPI rose 0.8% over the quarter for a third consecutive time. This saw the annual rate of wage growth nudge down from 3.4% in the December quarter 2025 to 3.3% last quarter. Both results were in line with the market consensus forecast. Nominal wage growth has now oscillated between 3.3% and 3.4% for the past five quarters.

Private sector wages rose 0.8% over the quarter and 3.2% over the year while public sector wages were up 0.5% and 3.3%, respectively. The annual rate of private sector wage growth is now at its lowest since the June quarter 2022 while annual public sector wage growth is running at its lowest since the December quarter 2024. The sizeable gap between the two annual growth rates that had opened over recent quarters has now narrowed again.

According to the Bureau, the Healthcare and social assistance industry made the largest contribution to wages growth last quarter, rising 0.7% in quarterly terms to be up 3.6% over the year. The ABS said this reflected the impact of a major Commonwealth funded initiative in the Early Childhood Education and Care workforce which saw private sector wage rises for the industry. At the same time, Queensland hospital health care workers were the main driver of public growth.

With headline inflation running at 4.1% in the March quarter of this year, annual real wage growth was negative for a second consecutive quarter.

RBA Minutes signal the central bank may now watch and wait

The Minutes of the 4-5 May Monetary Policy Board (MPB) meeting set out the background to this month’s 8 – 1 vote in favour of increasing the cash rate target by 25bp to 4.35%. According to the Minutes:

‘The case to raise the cash rate target…centred on the outlook for inflation. Members noted the staff’s assessment that capacity pressures remain tight and financial conditions may not be sufficiently restrictive to return inflation sustainably to target if the cash rate was held at its present level…an increase in the cash rate could provide greater confidence that underlying inflation would return to 2½% within the forecast period…Members agreed that monetary policy could not prevent a near-term increase in the price level as higher fuel prices worked their way through to final prices. However, monetary policy could limit the risk that this cost shock resulted in a broader and sustained lift in inflationary pressure, by bringing aggregate demand into closer alignment with aggregate supply and ensuring medium- to longer term inflation expectations remained anchored… the prolonged period over which underlying inflation had been above 3% may add to the risk that longer term expectations could become de-anchored…They agreed that the conflict in the Middle East was likely to see economic activity and labour demand soften somewhat, worsening the short-term trade-off between the Board’s inflation and employment objectives.’

On the other side of the policy debate:

‘Members noted that it would be appropriate to keep the cash rate target unchanged if they assessed that capacity pressures were not extensive or that financial conditions were already sufficiently restrictive to return inflation to target should there be a swift resolution of the conflict in the Middle East…An additional, or alternative, argument for leaving the cash rate target unchanged at this meeting would be if members judged that the impact on aggregate demand of a prolonged conflict in the Middle East would be sufficient to outweigh the inflationary impetus it would impart…this view could be strengthened if the sharp falls in consumer and business sentiment proved to be indicative of future spending...In light of this considerable uncertainty…and given monetary policy had already been tightened twice in 2026, waiting for a clearer assessment of how the conflict might affect economic activity could be an appropriate course of action.’

Of course, as we already know, it was the case for tightening that won over eight of the nine-member MPB:

‘…most members judged that the case to raise the cash rate target by 25 basis points at this meeting was the stronger one…underlying inflation was projected to be above target for an extended period across a range of scenarios for how the conflict in the Middle East might develop…these members determined that the risks to achieving the Board’s inflation objective had risen and…were not confident that, at 4.1%, the cash rate would be sufficient to mitigate these risks. Most members also judged that an increase in the cash rate target at this meeting would best balance the Board’s two objectives, accepting that the shorter term trade-off between these had worsened.’

While the single dissenter:

‘…placed more weight on the arguments for leaving the cash rate target unchanged, judging that capacity pressures prevailing before the conflict were somewhat less than the staff had assessed. This member also assessed the risk of a prolonged conflict that weighed more heavily on demand to be higher. Taken together, this led the member to expect inflation to be likely to return to target in an appropriate timeframe without additional tightening of monetary policy. Finally, the member in the minority judged that there was not yet sufficient evidence to be concerned about longer term inflation expectations becoming less anchored, particularly in view of the Board’s commitment to its inflation objective having been demonstrated by the 50 basis points of tightening already delivered this year.’

Finally, in terms of the outlook for policy post-meeting:

‘Members judged that, while it was still uncertain, financial conditions would probably be somewhat restrictive after this decision…the decision would give the Board space to see how the conflict in the Middle East develops and Australian households and businesses respond.’

The messaging here is consistent with our take at the time of the rate hike. The third of the RBA’s three 25bp rate hikes this year should allow the MPB a degree of breathing space to monitor the impact of the Iran war, the consequent global supply shock, and the implications for domestic activity and inflation. And as already discussed above, this week’s labour market numbers should also nudge Martin Place towards a wait-and-see position vs delivering a fourth consecutive rate hike at the upcoming 15-16 June MPB meeting.

Other Australian data points to note

The Westpac-Melbourne Institute Consumer Sentiment Index rose 3.5% to an index reading of 83 in May. The modest uptick in sentiment after April’s war-induced drop likely reflects the positive impact of the government’s temporary halving of fuel excise tax. But that lift to sentiment has also been offset by the RBA’s May rate hike. Westpac also reported a ‘very mixed’ impact from the Federal budget. On the one hand, responses over the course of the survey week showed a slight improvement in sentiment following the announcement of the Budget. But on the other, the survey also found that few consumers expected to see a direct benefit, with only 15% expecting to be better off compared to 34% expecting to be worse off. History shows that post-budget polling typically finds a negative gap of this kind, but Westpac notes that the size of the gap in this case is considerably larger than the gap that appeared following the previous two budgets.

Last week’s release of the monthly NAB Business Survey reported that business confidence rose five points to -24 index points in April 2026 while business conditions dropped for a fourth consecutive month, falling three points to +3 index points. NAB highlighted the increase in the survey measures of price pressures: purchase cost growth surged to 4.5% (quarterly equivalent terms) in April, up from 2.9% in March and 1.5% in February this year. The increase in growth in labour costs was more moderate, rising from 1.5% in March to 1.7% in April. But product price growth rose from 1.1% to 1.8% over the same period and retail price growth jumped from 0.6% to 3.2%, hitting a multi-year high.

Further reading and listening

- A speech from Sarah Hunter, RBA Assistant Governor (Economic) on inflation and the impact of the Middle East Conflict. Hunter argues that the war in the Persian Gulf will drive up Australian inflation through several channels, including via the direct impact of higher fuel prices on headline inflation and their indirect impact on the cost of producing and transporting other goods and services (that is, through higher input costs). In addition, the RBA also reckons that the rate of pass through of higher costs into prices will be relatively fast, given that the central bank judges that Australian businesses in aggregate were already capacity constrained before the war. In the RBA’s baseline forecast, the shock to oil prices places upward pressure on inflation over the coming year and contributes around 0.4 percentage points to underlying inflation in the March quarter 2027.

- Related to this, new RBA research on shifts in Australian price-setting behaviour around large shocks considers the post-pandemic inflation experience and finds that businesses adjusted their prices more frequently during the inflation surge. Simple economic models that assume stable price-setting behaviour may therefore be a poor guide when economies are suffering a major inflation shock. Under those circumstances, inflation can increase quicker than the models would predict.

- Five ‘under the radar’ budget measures.

- Are Budget 2026’s tax measures an assault on aspiration?

- A new Productivity Commission inquiry into reducing barriers to business dynamism is now underway.

- The IEA’s May 2026 Oil Market Report reckons that total losses in global oil supply between February and April this year have risen to 12.8 million barrels per day (mb/d), with output from Gulf countries affected by the closure of the Strait of Hormuz dropping to 14.4mb/d below pre-war levels. The IEA says global oil inventories have been depleted at a record pace.

- Also from the IEA, global sales of EVs are expected to reach 23 million this year, accounting for close to 30% of all cars sold worldwide. Global EV sales rose 20% in 2025, exceeding 20 million vehicles and accounting for around a quarter of all new cars sold, with Chinese carmakers supplying 60% of all EVs sold.

- The 2026 edition of the OECD Economic Survey of Japan.

- How macro policy should respond to AI.

- In the FT, Martin Wolf warns the energy crisis may just be starting.

- In the WSJ, Grep Ip says that China’s ‘Industrial policy of everything’ is leaving the rest of the world in the dust.

- This BIS working paper takes a look back at the squeeze on global liquidity and 1805-06 financial crisis that followed the Battle of Trafalgar, in search of lessons about what happens in the absence of a global lender of last resort (the ‘Kindleberger gap’).

- Also from the BIS, a new Bulletin on the role of currency carry trades in shaping exchange rate responses to monetary policy.

- The Economist offers a very short history of the jobs apocalypse.

- On maritime China.

- The Joe Walker podcast is producing a three-part series on Australian immigration policy. Part one talks to Martin Parkinson (former head of Treasury and then Prime Minister & Cabinet) about the economics of migration policy, while part two talks to Mark Cully (inaugural chief economist at the Department of Immigration) about his new book on the history of immigration to Australia. Part three was not available at the time of writing but is due soon.

- The FT Story of Money podcast explains why money is the biggest shared hallucination in human history and discusses the deal that put the US dollar at the centre of the world.

Latest news

Already a member?

Login to view this content