An examination of history is useful when investigating any potential collapse in China’s economic performance.

China: no need to panic

China is an extraordinary nation. It had a population similar to today’s largest European nations more than two millennia ago in 1AD. It was the first nation with a billion people, a figure it reached in 1982. Its population is now 1.4 billion and expected to be 1.7 billion in 2050. It may have the first city of 100 million people before the end of this century. That city’s population will be far greater than Australia’s total population.

China’s population in 2016 is nearly 60 times our population of 24 million, on a land mass of 9.6 million square kilometres – similar to our land mass of 7.7 million square kilometres. But its arable land is only three times ours, and its annual water supply is only seven times ours. This data helps explain China’s growing food security fears that are fuelling interest in our land and our potential supply of foodstuffs to China. As the century unfolds, agricultural exports may yet again rival mineral exports.

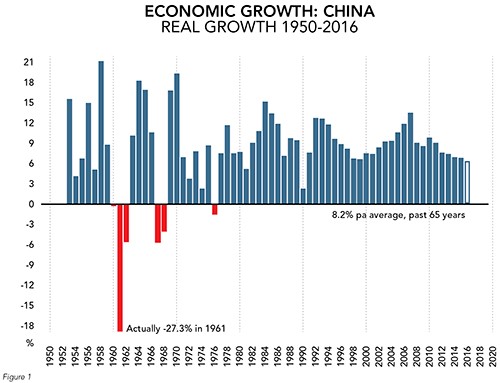

China’s average GDP growth of just more than 8 per cent a year for the past 65 years is not without precedent. Australia achieved that average in the 19th century, including through two depressions – in the 1840s and 1890s – and 10 recessions. China has done it with two depressions and one recession since the middle of the 20th century. Those setbacks happened under Mao Zedong’s reign; there have been none since he died in 1976, some 40 years ago. Figure 1 is illuminating in this regard.

Australia’s growth, which also averaged more than 8 per cent a year until Federation in 1901, took us to the highest standard of living in the world. However, Australia had a much higher population growth to boost economic growth over that period than China has had in its resurgence over the past half-century or more, given it was hobbled by the one-child policy, which has now been abandoned. No nation has ever grown at 8 per cent a year with a population of more than a billion people. The US achieved that growth starting with less than a tenth of that population and Australia did it with less than 1 per cent of that population.

Australia’s growth slowed to an average of 3.5 per cent per year in the 20th century with one depression in the 1930s and 14 recessions. It is now struggling to achieve growth of more than 3 per cent a year. This is despite the fact there has not been a recession for nearly a quarter of a century. Slow growth is largely due to an inadequate modern utility (fast broadband), overdue industrial relations reform, aborted taxation reform, aborted Senate reform and inadequate political leadership.

Hard or soft landing?

The question is whether China’s economic growth will also slow down and settle at around 3 per cent to 4 per cent a year, as Australia’s did. Of course it will, as did the US and other advanced economies. But not yet.

The slowing pace of China’s economic growth, if expected growth of 6.5 per cent in 2016 can be called slow, is a pause to restructure an overheated economy brought on by senseless investment in some provinces, leading to unoccupied new dwellings and other uneconomic investments. It is also due to imprudent bank lending in the form of shadow lending by state-owned banks, as well as other problems. China also needs to migrate its economy from one based on investment to one based on consumption.

Investment in the form of capital expenditure in China, on the back of extraordinary savings, reached more than 40 per cent of gross national expenditure (GNE) at its peak. Even now it is still more than 35 per cent – double the average of developed nations’ economies. Exports are about a fifth of GNE, double the level of the US and Japan.

That leaves consumption – by households and government – at a lowly 43 per cent of GNE, way below the developed world’s figure of 63 per cent, on average.

The Chinese government knows it must move to a more consumption-oriented economy. The booming outbound tourism market is a very visible example: 100 million-plus tourists a year. Australia has a paltry 1 per cent share of this trade. But if we get it right and achieve a much bigger share, we will earn more from inbound tourism than mineral exports by the end of the next decade.

China has been investigating service industries overseas for many years. But transitioning to a services-led economy is neither easy nor quick, as developed economies can attest. The Chinese economy is a difficult one to manage as this decade comes to a close.

As to how deep and long China’s slowdown will be, a depression or recession seems highly unlikely. The economy slowed to 2.4 per cent in 1990, the worst year for economic growth since the death of Mao. Present conditions are more likely to be a pause rather than a catastrophe, the end of one era and the beginning of another.

What next for China?

The country is now passing through the end of its industrial age and entry into the age of services and IT (and now digital disruption). The US, Australia and others entered this era 50 years ago.

In the post-industrial age, it’s not possible to get into the list of top 10 nations in terms of GDP per capita with a manufacturing or generally goods-based economy. The UK did in the late 1700s and Australia and the US did from the mid-1850s onwards in their industrial ages.

In 2016, China’s manufacturing sector will comprise less than 30 per cent of GDP. This figure was at 42 per cent seven years ago, reaching 45 per cent or more at its peak. Agriculture’s contribution to GDP, which not long ago accounted for a quarter of the economy, is now drifting into single figures.

China’s services industry now contributes more than 45 per cent to GDP, up from 40 per cent in 2009. This figure is well below Australia’s and other nations’, but China is on its way.

China already accounts for 40 per cent of our exports, and is poised to be our biggest single source of inbound tourism this year or next. Commodity prices will not regain their peaks, but will shortly come off the bottom. Export volumes, with a few hiccups, will grow until well into the second half of the 2020s. Service exports are in the wings, ready to take up any eventual slack from goods exports.

History shows we can’t write China off, or down. Nor should we sell short our fabulous opportunities for trade and investment in this exciting century. The best is yet to come. Patience helps.

In the meantime, Australia has some overdue reforms to tackle, as suggested earlier. It’s our time to bite the bullet too, not just China’s.

Latest news

Already a member?

Login to view this content