The global economy could suffer if the US Federal Reserve's signs continue to be misread. How will it affect your organisation?

The world economy will this year record its fastest growth rate since 2011, according to the most recent International Monetary Fund (IMF) forecasts. Across “advanced” economies, labour markets are tightening and unemployment is (on average) lower than at any time since the late 1970s. Although inflation remains low (in most countries) by historical standards, it is now more clearly on a gradual upward trend — at least insofar as consumer prices are concerned (wages are still a different story in most countries).

In these circumstances, it should be no surprise that the era of unprecedently “cheap money”, which has prevailed since the onset of the global financial crisis more than a decade ago, is drawing to a close. Already, the US Federal Reserve has raised its key funds rate seven times in the past three years and begun the process of shrinking its bloated balance sheet. The British and Canadian central banks have also started lifting their policy interest rates. And although it will likely be some time before the European Central Bank and the Bank of Japan do likewise, they are both likely to take a step back from their “quantitative easing” programs over the next 12–18 month period.

Financial market participants generally expect all of this to happen at a predictable, gradual pace. Indeed, central banks have themselves gone to considerable lengths to avoid surprising financial markets over the past decade, partly with a view to keeping long-term interest rates (over which they have less control than short-term rates) low and steady. However, the world’s major central banks, especially the US Federal Reserve, may be confronted by a less predictable environment over the remainder of this year and through 2019.

The Fed’s preferred measure of US “core” inflation is now back to its target level of two per cent for the first time since 2012. The odds are it will rise further. That’s partly because of the inflationary impact of the Trump administration’s tariff measures, which are already starting to show up in measures of “upstream” price pressures. The US is the one economy in the advanced world where there are some signs that labour market tightness is resulting in a gradual acceleration in wages.

Most important is the spectacularly mistimed US fiscal stimulus. IMF estimates suggest the US structural budget balance will widen by two percentage points of GDP between 2017 and 2019, at a time when the US economy will be operating at a bigger margin above its “potential” and the US unemployment rate will be further below its full employment level than at any time since the late 1960s. History suggests the chance of this ending well are not high. It therefore should not be surprising that the Fed is clearly signalling it will continue raising US interest rates — with its most recent set of forecasts centring on a federal funds rate of 3.25–3.5 per cent by 2020.

This raises two concerns. The first is the risk that the Fed becomes subject to sustained political criticism from the Trump administration and the Republican-controlled Congress. Although, as a presidential candidate, Trump accused the Fed under Janet Yellen of keeping interest rates artificially low, more recently as president, he has accused the central bank of “hurting all that we have done” by raising rates.

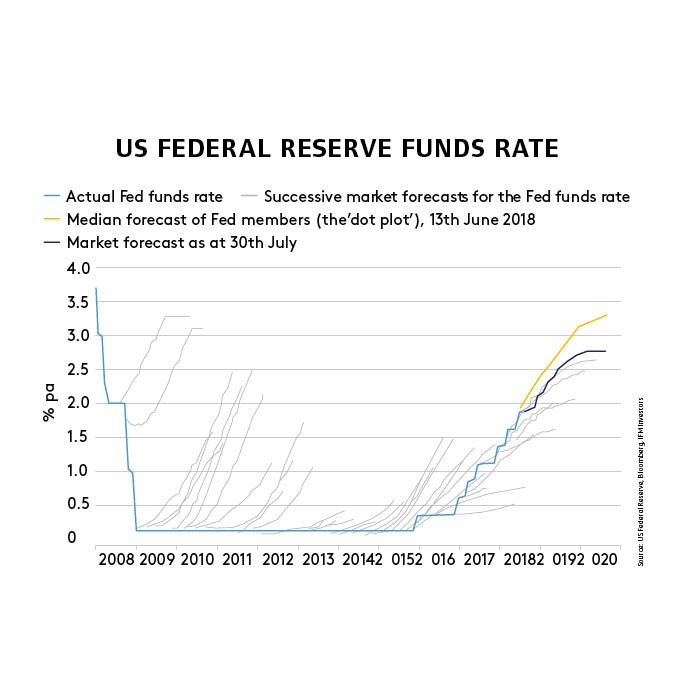

The second concern is that, although the Fed has, by and large, done exactly what it has said it would do in raising interest rates, thus far, financial markets have been unwilling to take it at its word in “pricing” future moves.

Markets were previously consistently wrong in their estimates of how long the Federal Reserve would keep interest rates at zero (see chart). But the consequences of those mistakes were relatively small.

By contrast, if interest rate markets end up being surprised by the pace at which the Federal Reserve tightens monetary policy — because they’ve been unwilling to believe what it has been saying — then the consequences could be more serious, not only for other financial markets (including equities), but also for the financial system and the broader economy.

Latest news

Already a member?

Login to view this content