Stephen Walters GAICD warns that while there's good reason for board director optimism, we're not in the clear just yet.

What a difference a year makes. In last year’s Budget, Treasurer Scott Morrison was still hinting at fiscal emergencies and “debt and deficit disasters”. Battening down the hatches, he announced new taxes, including the contentious big banks’ levy, and an increase in the Medicare levy.

The 2017 Budget was Plan B for the Coalition government — the approach under previous treasurer Joe Hockey, had been one of even greater austerity, the ending of the “age of entitlement”, more “lifters” and fewer “leaners”. That fiscal experiment ended badly, with the government forced to adopt yet another approach.

This year, the economic sunshine has returned, albeit unexpectedly, so much so that the planned increase in the Medicare levy — aimed at funding the National Disability Insurance Scheme (NDIS) — has been jettisoned. The Budget now will return to black ink a year earlier, according to the Budget papers. Morrison has even promised to cease borrowing for recurrent purposes, the so-called “bad debt” he referred to last year.

So, what happened in between? Essentially, Treasury discovered an impressive wall of tax revenue they didn’t know existed a year ago. In fact, this is the first time in recent memory — at least a decade — that a Federal Treasurer has been pleasantly surprised, rather than shocked by a cavernous tax-collection shortfall.

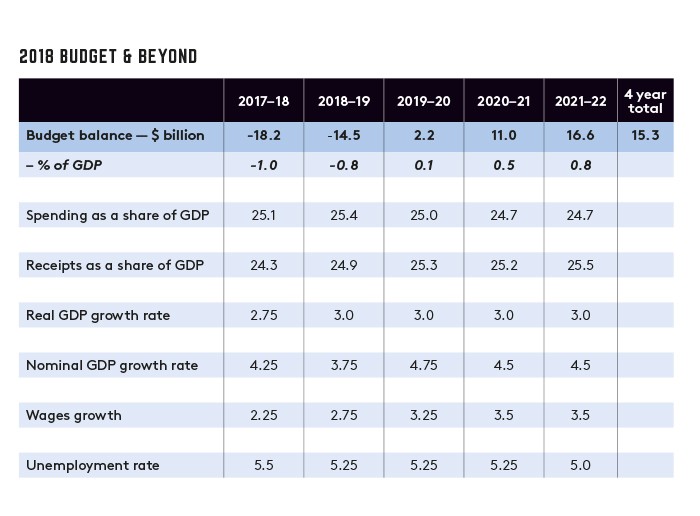

In the first nine months of 2017–18 alone, the Department of Finance reports that actual Commonwealth revenue collections are running more than $5 billion ahead of the midyear update forecast last December. Even better, Treasury now expects nearly $26b in additional tax to flow into government coffers over the next four years.

Company tax receipts have bounced back, partly because tax losses that many companies incurred in the aftermath of the GFC, in particular, and which they had written off against contemporary revenues, have been exhausted. There was also the boost to tax collections from the improving economy and stellar job market last year, when more jobs were created than ever before — more than 400,000 positions.

However, some of the revenue euphoria should be taken with a pinch of salt. Indeed, it’s not clear exactly how Treasury plans to squeeze so much additional tax from the same economic profile going forward. Treasury assumptions about the performance of the economy have not changed from the 2017 Budget, but the impact on revenue collection has — and materially.

Treasury’s implicit assumption must be that the “elasticity” of revenue to economic growth has improved. That is, more tax juice will be squeezed from the same economic lemon — more tax collection bang from the same economic buck. We’ll have to see how this plays out, but the track record is not great. Indeed, for the best part of the past decade, Treasury has consistently forecast that revenue growth would rebound, only for collections to fall well short of lofty expectations. This time, at least, the improving trend over the past nine months is running in Treasury’s favour.

Morrison has dragged forward the promised return to surplus to 2019–20, also pledging to spend more on health and education while simultaneously promising tax cuts for households and corporates. This trifecta sounds a little too good to be true, but the metrics add up — as long as the economy performs as expected. The economic assumptions, however, still stretch credulity. Treasury forecasts the economy will grow consistently by three per cent across the forward estimates, stretching Australia’s remarkable recession-free record to 31 years. This presupposes no global recession or domestic housing market meltdown, among other possible calamities.

Only once in the past decade has Australia’s economy grown by three per cent or more — in 2012, at the height of Australia’s biggest mining investment construction boom. The 3.5 per cent wages growth forecasts seem similarly optimistic. The last time wages rose that quickly was back in 2013, when that same resources boom had drained big city labour markets. It’s clear from the Budget papers that the lion’s share of the return to surplus will be borne by the revenue side of the accounts. The spending share is assumed to stay above 25 per cent of the economy, an elevated level usually associated with subdued economic conditions following recessions or other serious dislocations, not the economic sunshine apparently now shining down on us.

Spending as a share of GDP, for example, reached 25 per cent of the economy during the recessions of the early 1980s and 1990s, peaking at 26 per cent of GDP in 2009–10 during the darkest days of the GFC. Government attempts to rein in this ratio in the aftermath foundered in the Senate, so the onus is on the revenue side of the Budget. But now the Treasurer has effectively tied his own hands by capping the tax share at 23.9 per cent, without similarly capping spending. The promised surplus “circle” is squared by remembering that the government also collects significant non-tax revenue, like dividends from the Reserve Bank. These non-tax collections can amount to more than two per cent of GDP.

The adoption of a tax speed limit and the acceptance of an elevated spending share effectively manacles the promised wafer-thin surplus in two years’ time to the credibility of Treasury economists. An underperforming economy could see the government’s fiscal plan go pear-shaped, although there’s a chance the economic pointy-heads are being too pessimistic.

Longer-term, a key risk is that the government is promising to fund multi-decade structural spending commitments like the NDIS from recurrent revenue. This is the type of bold assumption that recent history has proven fallible. Cycle-high revenue during the commodity price boom of the 2000s was assumed to continue as spending was ramped up in the aftermath of the GFC. That failed experiment ended with record high debt and deficits.

In particular, by abandoning the planned rise in the Medicare levy, the government has placed the funding burden of the NDIS back on the vagaries of underlying tax collections. The government still claims that the NDIS is explicitly funded — not any more!

Finally, the Treasurer claims we are living within our means. We are not, at least not yet. By definition, running deficits means we’re still spending more than we’re raising in tax — and borrowing the shortfall. Such a strategy is not sustainable in the long term and leaves the economy without a fiscal buffer for the next, inevitable economic downturn.

Alarmingly, Commonwealth public debt is already nearing $600b. The interest bill alone is $40m a day. Not until we consistently run surpluses across the economic cycle can we reasonably expect to start paying down this unprecedented debt mountain.

Latest news

Already a member?

Login to view this content