The Westpac-Melbourne Institute Consumer Sentiment Index rose to close to a ten-year high in March. February saw NAB’s monthly index of business confidence reach its highest level since early 2010. RBA Governor Lowe explained in detail why he thinks financial markets have got it wrong about the likely future trajectory of monetary policy. The US Congress approved the Biden administration’s US$1.9 trillion fiscal package, effectively kicking off a major economic experiment.

The OECD upgraded its forecast for global growth this year by 1.4 percentage points to 5.6 per cent, partly on the back of that increased US fiscal stimulus. More than 326 million COVID-19 vaccines have now been administered worldwide as the daily vaccination rate continues to climb. The JP Morgan Global Composite PMI hit a four-month high in February. Bloomberg’s high frequency alternative data show Australia continues to perform well relative to our advanced economy peers but also suggest some levelling off in the pace of global economic recovery earlier this month.

This week’s readings include reflections on the Competition and Consumer Act, Garnaut on Reset, the role of the RBA, the national fiscal outlook, the reflation trade and the ‘big long’, the rise of the four-day work week, and how the pandemic has transformed the welfare state.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

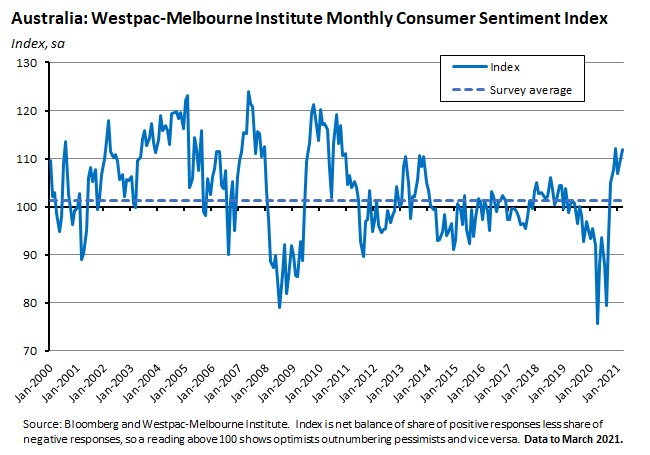

The Westpac-Melbourne Institute Index of Consumer Sentiment climbed (pdf) 2.6 per cent to reach an index level of 111.8 in March this year.

All five subcomponents of the index rose over the month: the smallest gain was for ‘family finances next 12 months’ which was up just 0.2 per cent, followed by ‘economic conditions next five years (up 2.3 per cent), ‘family finances vs a year ago’ (up 2.8 per cent), and ‘economic conditions next 12 months’ and ‘time to buy a major household item’ (both up 3.7 per cent month-on-month).

Survey results also showed more confidence in the labour market, with the Index of Unemployment Expectations falling by 2.2 per cent, suggesting that fewer respondents now expect unemployment to increase in the year ahead.

The House Price Expectations Index rose 3.1 per cent in March while the ‘time to buy a dwelling’ index fell 3.6 per cent.

Why it matters:

The Index is now only 0.2 points below the level it reached back in December, which marked a ten-year high, and is more than 21 per cent higher than the index level in March 2020. Positive health news, good economic news and ongoing policy support are all underpinning household sentiment. Similarly, the Index of Unemployment Expectations is reporting its best results in almost a decade (consistent with the recovering labour market), while the House Price Expectations Index has climbed to a seven-year high (although here rising prices do appear to be taking a toll on affordability, with the ‘time to buy’ index sliding for a fourth consecutive month).

What happened:

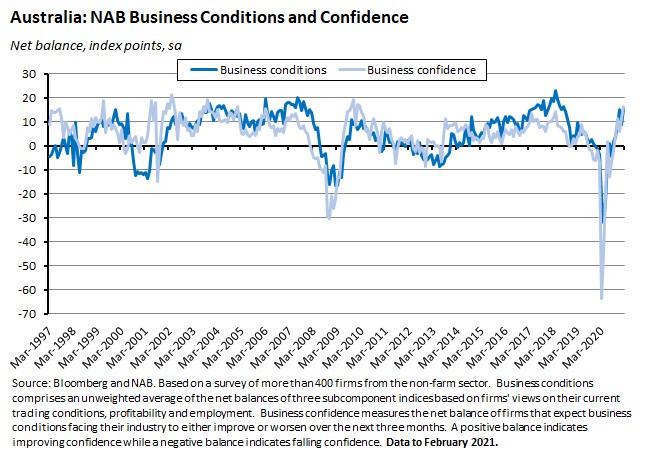

The NAB monthly index of Business Confidence rose four points in February to +16 index points. The gain in confidence was broad-based, with all states and all industries (except for retail) recording an increase. For the same month, the NAB monthly index of Business Conditions rose by more than six index points to a reading of +15 index points. Again, the rise over the month was broad-based across industries, with only three (retail, recreational & personal, and mining) not enjoying an increase and even then, conditions in all three remained at strong levels (in the range of 18 to 22 index points).

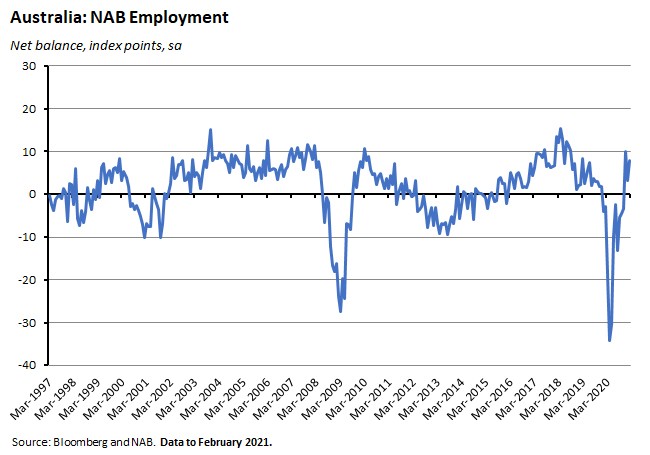

The employment index rose by five index points in February.

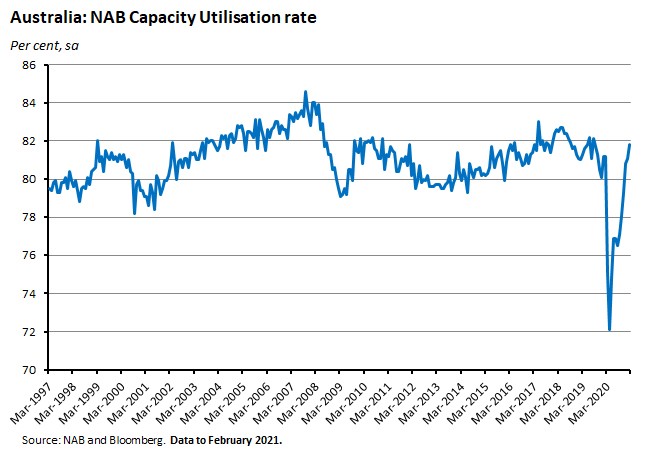

The reported rate of capacity utilisation moved higher, rising from 81.1 per cent in January to 81.8 per cent in February.

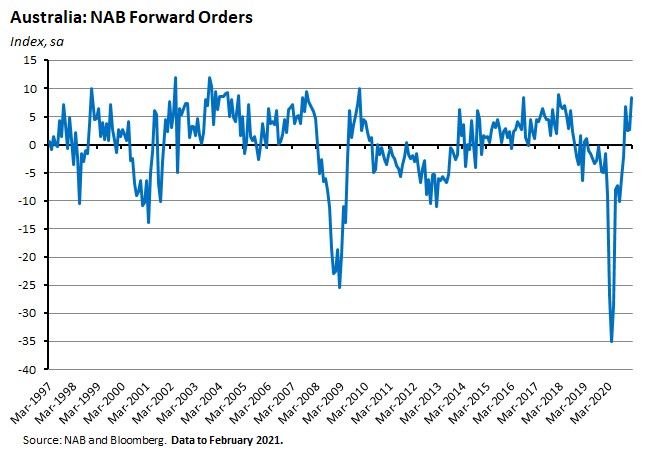

And forward orders also rose over the month.

Why it matters:

February’s survey results delivered a very positive message on business sentiment as the monthly confidence index rose to its highest level since early 2010 even as business conditions returned to close to multi-year highs.

The increase in the employment reading is good news for the labour market (see also this week’s readings and the link to the latest Manpower employment survey results, below), while the strong results for leading indicators - capacity utilisation is now at its highest level since mid/late-2019 and forward orders are running well above average – are consistent with further gains in business activity, with high rates of capacity utilisation in particular positive news for the outlook for future employment and investment decisions.

What happened:

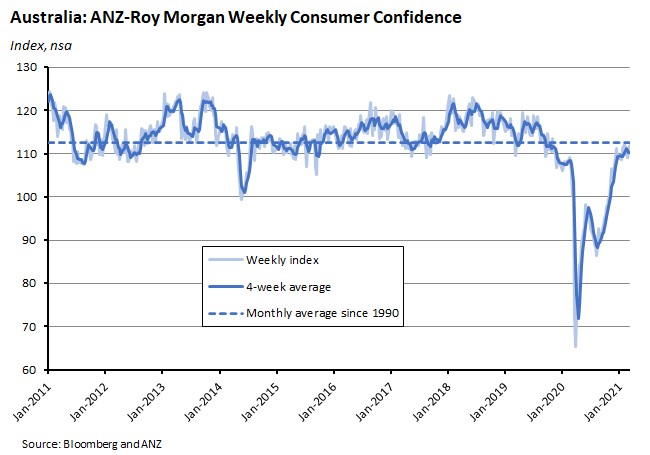

The ANZ-Roy Morgan weekly Index of Consumer Confidence jumped 1.5 per cent over the week ending 6-7 March, taking the index up to a level of 111.9.

Four out of five subindices rose over the week: ‘current financial conditions’ increased 1.5 per cent, ‘future financial conditions’ climbed 2.1 per cent, ‘current economic conditions’ bounced 3.6 per cent and ‘future economic conditions’ were also up by a healthy 2.1 per cent. The only softness came in the ‘time to buy a major household item’ subindex, which slipped 0.8 per cent.

Why it matters:

A second consecutive rise in the weekly confidence measure took the index up to its highest level since late 2019 and left it more than 11.5 points higher than in the same week in 2020. The improvement in financial and economic sentiment likely reflects last week’s positive economic data, with the Q4 GDP result in particular surprising on the upside.

What happened:

RBA Governor Philip Lowe gave a speech on The Recovery, Investment and Monetary Policy. On the recovery and investment, Lowe noted:

- The strong Q4 GDP outcome last week provided more evidence of the strength of Australia’s recovery.

- There has also been a V-shaped recovery in the labour market, although the approaching end of JobKeeper represents a short-term risk.

- Even so, there is still lots of spare capacity in the economy and an absence of inflationary or wage pressures.

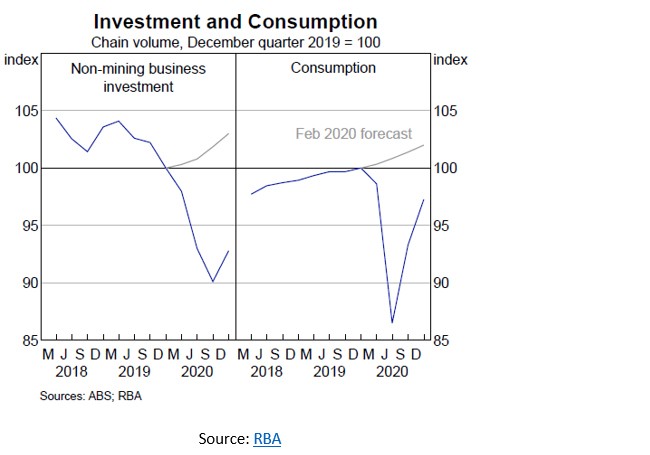

- While Australia has enjoyed a strong rebound in consumption spending, non-mining investment spending remains weak (see also last week’s brief discussion on this point in the GDP section of the Weekly).Investment is seven per cent below the level it reached last year and more than 10 per cent below where the RBA thought it would be at when the central bank made its projections at the start of 2020.

- Investment weakness is a long-running story: since 2020 non-mining business investment as a share of GDP has averaged just nine per cent, compared with 12 per cent over the previous three decades.This implies a smaller capital stock and slower future productivity growth.

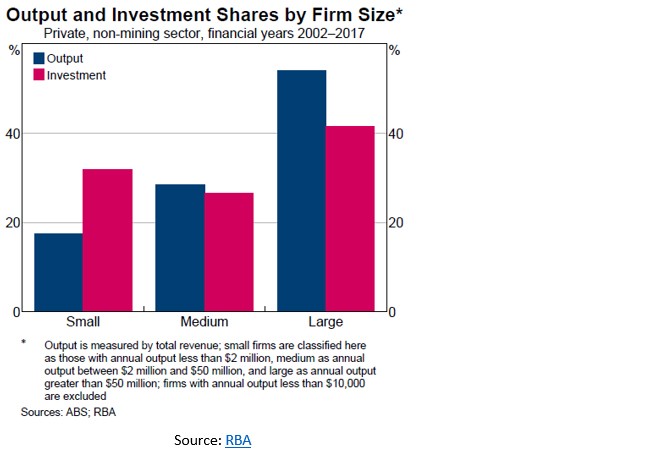

- Small businesses have in driving investment, with recent data showing that small firms are much more investment-intensive than their larger counterparts, which Lowe argued made the case for ‘ensuring a supportive environment for innovative small and medium-sized businesses.’

On monetary policy, key messages from the speech included:

- The RBA will leave the cash rate unchanged at 0.1 per cent ‘until inflation is sustainably within the two–three per cent range. It is not enough for inflation to be forecast to be in this range. Before we adjust the cash rate, we want to see actual inflation outcomes in the target range and be confident that they will stay there…we want to see actual inflation outcomes consistent with the target before moving the cash rate.’ [emphasis added]

- On the future of the cash rate: ‘market pricing has implied an expectation of possible increases…as early as late next year and then again in 2021.This is not an expectation that we share.’ [emphasis added]

- To meet the RBA’s inflation target, ‘it is likely that wages growth will need to be sustainably above three per cent…Currently, wages growth is running at just 1.4 per cent, the lowest rate on record…Even before the pandemic, wages were increasing at a rate that was not consistent with the inflation target being achieved. Then the pandemic resulted in a further step-down. This step-down means that we are a long way from a world in which wages growth is running at three per cent plus.’

- The target of higher wage growth will have to overcome some powerful headwinds, including increased competition in goods markets which had made firms very cost conscious, the internationalisation of services, the relative demand shifts prompted by technological change, and changes in the global supply of labour and the regulation of labour markets.

- The RBA will ‘look though’ any ‘transitory fluctuations in inflation’, including an expected temporary increase in the CPI to around three per cent in the June quarter of this year as pandemic-related price cuts are reversed.

- Monetary stimulus ‘is not just about achieving an inflation rate of two point something. It is just as much about achieving the maximum possible sustainable level of employment in Australia…There is, inevitably, some uncertainty about exactly what constitutes full employment in our modern economy… But…it is certainly possible that Australia can achieve and sustain an unemployment rate in the low fours, although only time will tell.’

- The RBA remains committed to its three-year yield target: ‘We are not considering removing the target or changing the target from 10 basis points.’That said, the central bank has yet to decide on ‘the question of whether to keep the April 2024 bond as the target bond, or to move to the next bond – that is the November 2024 bond – later this year.’

- On QE: ‘Later in the year, the Board will also consider the case for further extending the bond purchase program…Until then, we remain prepared to alter the timing of purchases under the current programs in response to market conditions.’

- Finally, on the housing market, Lowe said that he ‘would like to reiterate that the RBA does not target housing prices, nor would it make sense to do so.’Tools other than monetary policy would be deployed should the housing market become of greater concern, and here the RBA was ‘continuing to pay close attention to lending standards, especially given the combination of low interest rates and rising housing prices. Looser standards would increase medium-term risks and add to the upward pressure on prices, so would be of concern…We are not at this point, but we are watching carefully.’

Why it matters:

The governor’s speech was an elaboration of the position already staked out by last week’s monetary policy statement: the RBA thinks market expectations about an earlier (than presently flagged by the central bank) hike in the cash rate are misplaced, and that it will be quite some time before the necessary preconditions are in place for any such adjustment. Those preconditions are tied closely to the labour market, and in particular to the RBA’s desire to see faster wage growth – which the speech suggested would entail a rate of wage increases that was ‘sustainably’ in the ‘three per cent plus’ range. The governor also suggested that the ‘full-employment’ rate of unemployment that would support such growth, while uncertain, could possibly be ‘in the low fours’ and in the subsequent Q&A session conceded that the number could even have a ‘three’ in front of it. If so, with the unemployment rate still at 6.4 per cent, that means there’s still a fair distance to travel.

. . . and what I’ve been following in the global economy.

What happened:

The US House and Senate both voted to pass President Biden’s US$1.9 trillion coronavirus aid package, the American Rescue Plan. The bill includes a US$1,400 direct payment (to individuals earning up to US$75,000 and couples earning up to $150,000), an extension of the US$300 per week supplement to unemployment benefits through to September (that would otherwise have started to expire this weekend), a one-year expansion of the child tax credit (increasing the benefit to US$3,000 per child from US$2,000 plus a US$600 bonus for children under six and making it refundable which will make the credit available to low income houses that currently don’t pay enough in taxes/earn enough income to take full advantage of it) as well as more money for vaccines, test and trace, schools and universities, the Affordable Care Act, and state and local governments. The spending comes on top of around US$4 trillion of fiscal support delivered last year.

A proposed staged increase in the US minimum wage was dropped from the legislation after the Senate parliamentarian ruled that the measure couldn’t be included as part of the reconciliation process (which allows a bill to be approved with a simple majority of votes in the Senate if it is linked to the budget, instead of the usual 60 votes required). The Senate voted for the bill 50-49 and the House 220 to 211. No Republicans voted for the bill in either the Senate or the House and all but one House Democrat voted in favour.

Why it matters:

This additional big dose of fiscal spending is expected to provide a substantial boost to US GDP growth – perhaps by as much as three percentage points this year – lift employment growth, and lower poverty rates. It will also provide a (possibly temporary) boost to inflation. In addition, there will also be significant spillovers to the rest of the global economy (see next story on OECD forecasts).

One way to the think about the implications of the American Rescue Plan is in terms of a giant economic experiment that will test several important propositions.

The first of these big tests relates to the macroeconomics of the stimulus package. These have been contentious, with some economists warning that it is too large and risks stoking inflation and others claiming such caution is misplaced. The US Federal Reserve has already said that it is expecting headline inflation to pick up over coming months although some of this will be a mechanical effect, as very weak results from 2020 drop out of the annual comparisons. But supply constraints, disruptions to global supply chains and rising commodity prices are also all adding to current price pressures (see story on global PMIs below) and pessimists worry that a big fiscal splurge risks converting these pressures into a more durable spike in inflation. On the other side of the argument, US Fed and Treasury officials argue that much of this price action will reflect transitory adjustment pressures, pointing to a still-large degree of slack in the US economy.

A second test relates to the impact on employment and unemployment, based around the case for ‘running the economy hot’ in order to drive down the unemployment rate. Further, the scale of the Biden administration’s fiscal response should be seen at least in part as a reaction to the perceived failure of the Obama administration’s fiscal measures in response to the global financial crisis (GFC). There is now a consensus among many economists that those measures were inadequate given the scale of the adverse shock, and that as a result, the US economic recovery from the GFC was much more subdued than it could have been, and that this in turn had unfortunate political and social consequences. The Biden administration is determined to avoid repeating this mistake. Better to run the risk of doing too much, the argument runs, than too little. And although voting for the bill split along predictably partisan lines, opinion polls (for whatever they’re worth) do suggest that the measures are popular across what is normally seen as a very politically divided voting population.

The third big test relates to social policy and the ambition to use government intervention to wind back poverty and inequality. With large-scale tax cuts and cash transfers targeted at low and middle income households, the bill can be viewed taking out insurance against the risk of a so-called K-shaped recovery that leaves a chunk of the population behind. On one estimate, measures in the bill including the extension to the tax credit for children could cut the projected US poverty rate in 2021 by more than one third while cutting the child poverty rate by more thana half. Another element here is that the bill also reflects an increased focus on the benefits of providing direct cash support to households.

Arguably, all three of these tests can be folded into one, bigger question: can a return to ‘big government’ deliver successful economic, political and social outcomes in the United States? With the Biden administration hoping to follow the American Rescue Plan with ambitious infrastructure spending proposals, this particular experiment has much more room to run.

One final point, relating to the idea of a political-economy regime shift. Some economists have argued that under the previous political-economy regime, Republicans tended to advocate for fiscal responsibility when their side did not hold the presidency before abandoning any budgetary restraint once in office, while at least some Democrats have been relatively more inclined to a degree of fiscal conservatism when in power. Under what looks to be the new regime, it seems that neither party may be keen to prioritise balancing the government’s books.

What happened:

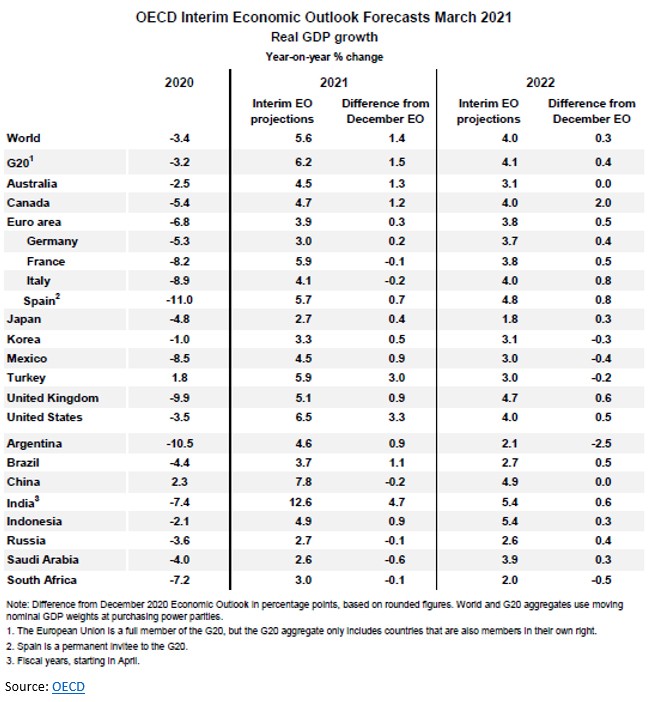

The OECD released the March 2021 update to its Economic Outlook. The new forecasts show the OECD becoming much more optimistic about the global growth outlook: after contracting by 3.4 per cent in 2020, it now thinks the world economy will grow by 5.6 per cent this year (up 1.4 percentage points from its December 2020 forecast) and four per cent next year (up a more modest 0.3 percentage points on December’s projections).

Australia’s growth forecast for this year enjoyed a healthy 1.3 percentage point upgrade but even that big revision is put in the shade by upgrades of three percentage points for Turkey, 3.3 percentage points for the United States and 4.7 percentage points for India.

The OECD points to several drivers behind the acceleration in global activity: the gradual deployment and increasing evidence of the efficacy of vaccines, which are boosting confidence and allowing for a relaxation of lockdown measures; strong fiscal stimulus measures including the new Biden administration spending discussed above; and evidence that containment measures and the associated declines in mobility are now having a smaller negative impact on activity than they were in the earlier stages of the pandemic (possibly due to better targeting of both the measures themselves and of income support, but also due to adaptation by businesses and households). Global demand for goods has also picked up, leading to stronger industrial production and a return to pre-pandemic levels for world merchandise trade.

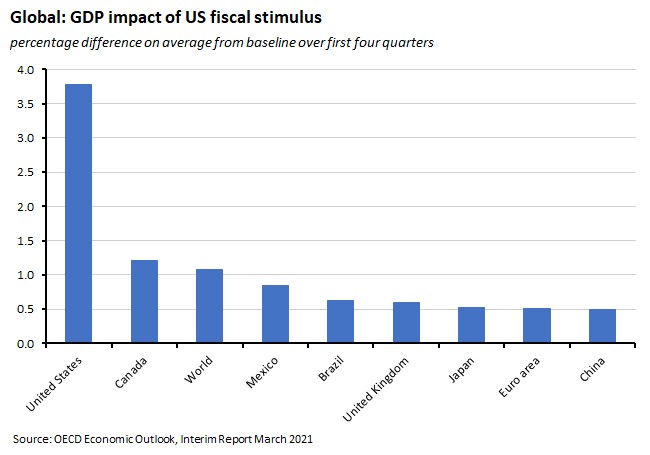

US fiscal measures play a prominent role in the OECD’s new forecasts. The December 2020 Consolidated Appropriations Act contained new temporary measures worth US$900 billion (about four per cent of GDP) and will now be supplemented by the US$1.9 trillion (about 8.5 per cent of GDP) American Rescue Plan. OECD modelling suggests that the latter could increase US output by around three to four percentage points on average in the first full-year of the package (2021:Q2 to 2022:Q1) with positive spillovers to the rest of the world, including a 0.5 to one percentage point boost to output in Canada and Mexico and a 0.25 to 0.5 percentage point increase for the eurozone and China.

Although the US fiscal stimulus is good news for the global economy overall – perhaps pushing up world output growth this year by a bit more than a full percentage point – the OECD warns that rising US bond yields could trigger a reversal of capital flows to some emerging economies along with higher currency volatility in a re-run of 2013’s ‘taper tantrum’.

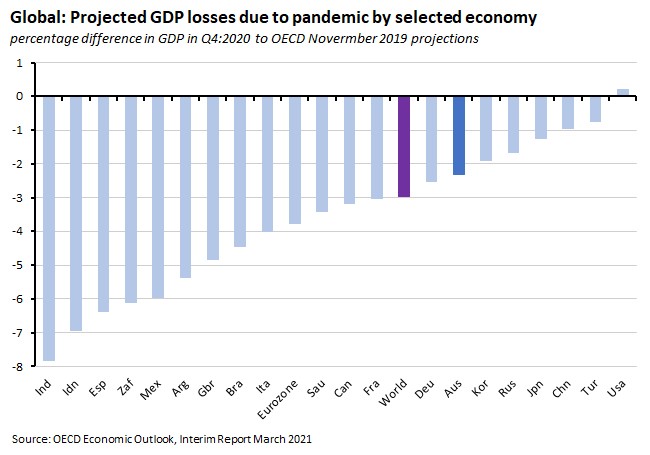

In addition, while the OECD is upbeat about the improvement in the overall economic outlook, indicating that it thinks global GDP should be back above pre-COVID levels by the middle of this year, it also cautions that there are substantial differences across countries. The Asia-Pacific (including Australia) has benefitted both from successful public health measures and the regional boost from the upturn in industrial activity and China’s economic recovery, for example, while fiscal largesse is helping power US activity. But other economies risk seeing lasting economic damage from the pandemic.

The March forecast update also notes that the improvement economic prospects has brought with it an increase in expectations of future inflation. Stronger demand from China in particular has helped push up commodity prices while temporary supply shortages in other sectors, including semiconductors and shipping, are contributing to the rising input prices now being reported in PMI surveys (see below). All that said, the OECD judges that underlying price pressures generally remain mild in most advanced economies given lots of spare capacity and that some current inflationary pressures are transitory, driven by one-off adjustments such as the re-opening of some sectors or changes to indirect taxes.

Why it matters:

The new OECD numbers are another sign of the growing optimism around the trajectory for the world economy this year. At the same time, the accompanying analysis also reminds us that a key risk to the economic rebound is the danger that the speed of vaccine production and deployment is not fast enough to put a halt to the transmission of the virus, particularly if new mutations that require new or modified vaccines were to become widespread. That argues for keeping a close eye on the global as well as domestic pace of vaccine rollouts.

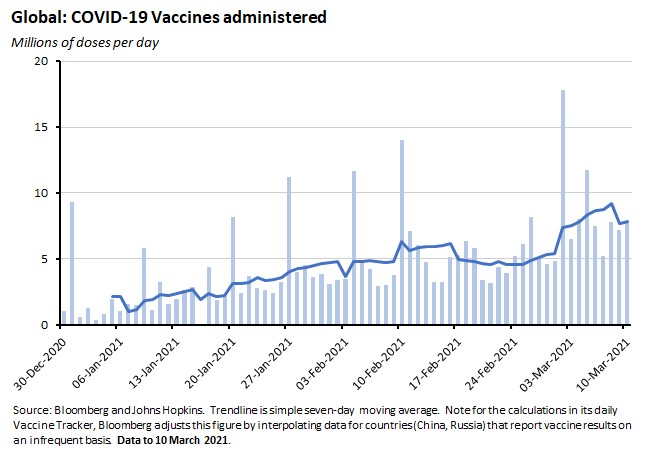

What happened:

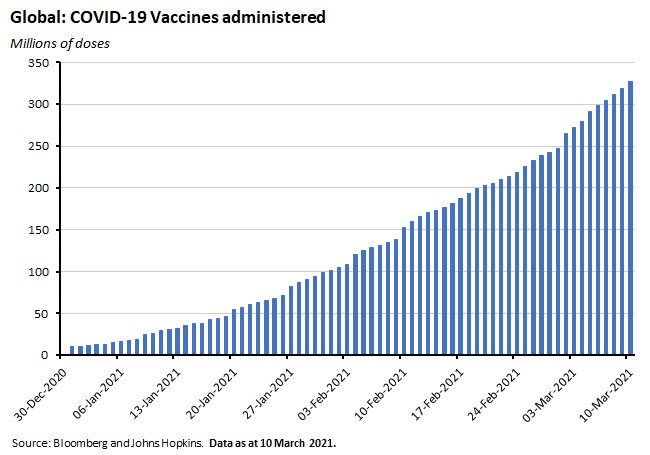

According to Bloomberg’s daily vaccine tracker, as of 10 March this year, more than 326 million vaccines had been administered worldwide.

At a crude average daily rate, vaccines are running at around 7.9 million a day. Adjust for slow reporting economies and the average daily rate rises to a little above 8.3 million. At this rate, it would take an estimated 3.6 years to cover 75 per cent of the world’s population with a two-dose vaccine.

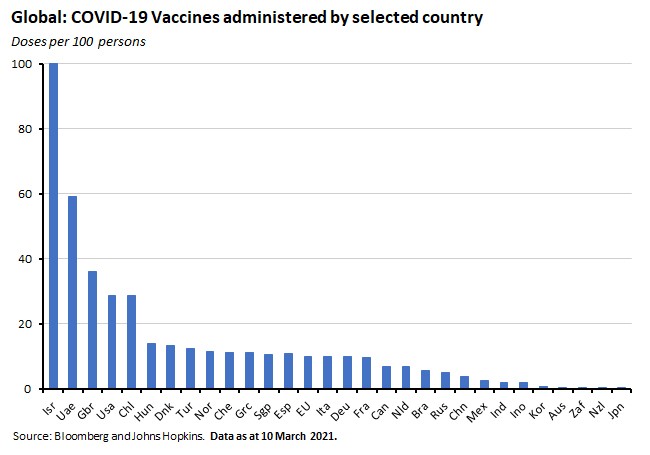

Differences in coverage by country remain substantial, ranging from more than 100 doses administered per hundred people in Israel to more than 28 per hundred in the United States, to less than ten per hundred across the EU, less than four per hundred in China and less than two per hundred in India.

Why it matters:

The global success of the vaccine rollout remains a critical input to forecasts of the global economy. In that context, the not-so-great news is that less than one per cent of the global population has been vaccinated to date and at current rates it will still take considerably longer than three years to cover 75 per cent of the world’s population with a two-dose vaccine. The better news, however, is that this daily rate is already up significantly from where it was just a few weeks ago and is continuing to rise, indicating that the expected time to vaccinate should continue to decline.

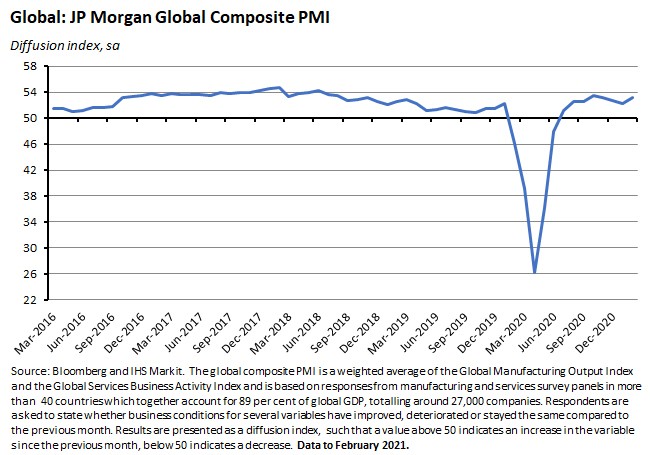

What happened:

The JP Morgan Global Composite PMI rose (pdf) to a four-month high of 53.2 in February.

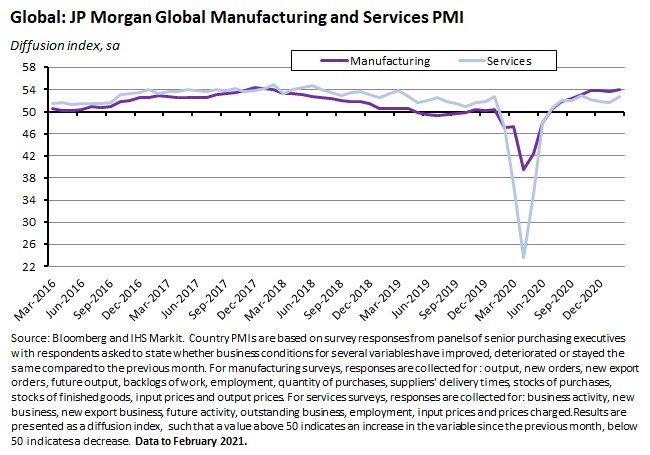

Manufacturing continues to lead the global economic recovery, with the Manufacturing PMI edging up to 53.9 in February, marking a three-month high, and with 23 of 29 reporting nations enjoying a PMI reading above 50. Manufacturing output was up across the investment, intermediate and consumer goods industries.

The Services Business Activity Index also rose to a four-month high of 52.8 in February, showing activity in services rising at the fastest pace since last October. The divergence in performance between financial and business service providers on the one hand and consumer service providers on the other continued, however, with the latter group suffering its thirteenth successive month of falling activity.

Why it matters:

The Composite PMI hit its highest index level in four months and its second-highest reading for two and a half years. The index has now been in positive territory – indicating rising economic activity – for eight consecutive months.

One other point of note: survey respondents report that inflationary pressures are rising, with the global manufacturing sector facing supply chain disruption, delivery delays and rising cost pressures. Overall, in February Input prices were rising at the fastest pace since September 2008 (a 149-month record) and output charges increasing to the greatest extent since that series began in October 2009.

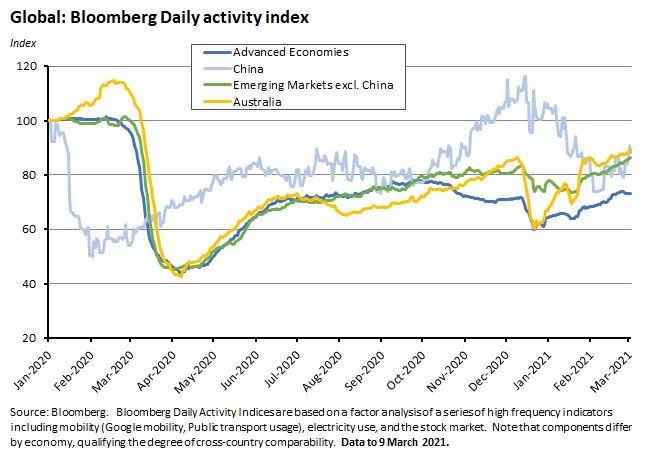

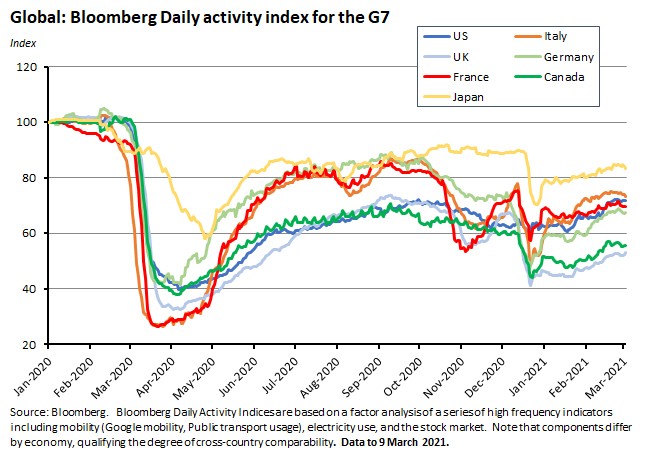

What happened:

The latest set of results from Bloomberg’s high frequency alternative data suggests that Australia continues to outperform most of its advanced economy peers in terms of the pace of its recovery. And we are now also looking good by emerging economy standards.

At the same time however, the numbers for the big G7 economies suggest that many have had a relatively subdued few weeks of activity and that the pace of the global economic recovery may have eased as we entered the beginning of this month.

Why it matters:

Bloomberg’s daily activity data offer an alternative, higher frequency perspective on developments in economic activity that complement more traditional data sources. As we’ve noted before, they are not without their drawbacks – overweighting mobility indicators, limited comparability across economies – but they still offer a useful insight into recent trends.

What I’ve been reading . . .

- Manpower Group’s Q2:2021 employment outlook survey reported the strongest national outlook for hiring in more than nine years, with job gains expected across all states and territories. South Australia leads the pack with that state’s strongest net employment outlook in a decade. All seven industries covered by the report also expect strong growth in payrolls, with finance, insurance and real estate the most positive and wholesale and retail trade the most cautious.

- ACCC Chair Rod Sims offers some reflections on the 10th anniversary of the 2010 Competition and Consumer Act (CCA). Sims argues that the CCA ‘heralded a new era in Australian consumer protection,’ putting consumers ‘in their rightful place at the centre of national competition and consumer laws.’ According to Sims, the Federal Court has imposed a total of almost $400 million in civil pecuniary penalties instituted by the ACCC in the last 10 years, compared to only around $5 million in criminal fines obtained for consumer law breaches prior to its introduction. Looking forward, he argues that Australia would benefit from an unfair trading practice prohibition, which in his view would ‘remove or avoid the need for some intrusive industry-specific regulation’ and thereby ‘help lessen the overall regulatory burden.’ Sims also canvassed potential reforms to merger law, where he argued that it ‘appears that insufficient weight is placed on the risks to competition, such as potential competition being lost, barriers to entry raised or competitors being foreclosed. As a result, our merger control regime is skewed towards clearance, which presents real challenges for our economy given the damage that can be done by anticompetitive mergers. We therefore consider that the approach to merger control needs to be rebalanced.’

- Peter Martin lauds the critical role played by the ABS. As long-term readers will know, I’m a big supporter of the importance of the Bureau.

- Ross Garnaut in conversation with Alan Kohler about the former’s new book, Reset. Topics covered include: modern monetary theory, targeting full employment and the level of the NAIRU, the case for a cash flow tax, and universal basic income (UBI).

- Richard Holden argues that the RBA will win in any tussle over the direction of interest rates in the economy, given the unlimited firepower at its disposal, as long as it is up for the fight.

- Also on the RBA, Steve Grenville defends the central bank against accusations (like those of Garnaut, above) that excessively tight monetary policy caused the post-GFC slowdown in the Australian economy, arguing that it was fiscal austerity that took the greater toll on growth.

- Grattan released a new report on the impact of the pandemic on Australian women that says that women lost more jobs, shouldered more of the increase in unpaid work (e.g. supervising children learning remotely) and were less likely to get government support than men.

- The Parliamentary Budget Office (PBO’s) latest national fiscal outlook (pdf). Since the start of the pandemic the aggregated bottom line for state and federal governments – as measured by the national net operating balance – has worsened dramatically. In the PBO’s 2019-20 outlook it forecast the national net operating balance in 2020-21 would be in surplus by 1.7 per cent of GDP. Now it thinks it will record a deficit of 11.1 per cent of GDP. That compares to a peak deficit during the GFC of 3.2 per cent of GDP. Even so, the turnaround in the fiscal position is forecast to be quite quick, with the deficit down to 2.2 per cent of GDP by 2023-24. There will be a more lasting effect on national public debt, which is now forecast to triple from pre-COVID levels, rising from 20 per cent of GDP in 2018-19 to 59 per cent in 2023-24.

- The latest issue of Australian Foreign Affairs is available, themed around ‘the march of autocracy.’ You can listen to Allan Gyngell (who spoke at the AGS) discuss one of the essays – How to prepare for a China-led world – with the authors here.

- Related, Bates Gill in the Lowy Interpreter casts his eye over last week’s National People’s Congress in China and in particular the new ‘dual circulation strategy’ (dual for domestic and international) which he reckons will have ‘profound implications for global economics and geopolitics’ in the form of a greater focus on China’s own internal market alongside more emphasis on the technological underpinnings of the ‘Made in China 2025’ strategy.

- The March 2021 BIS Quarterly Review offers a deep dive into the reflation trade that has roiled financial markets in recent weeks. There are also interesting boxed discussions on how, in an environment of low interest rates, stock returns are particularly sensitive to news on monetary policy and on the growing influence of retail investors in financial markets.

- Related, Joshua Brown on the ‘big long’. His argument: when the risk-free rate is zero, money is almost free, which means that ‘if you’re borrowing it to earn a better return elsewhere, your hurdle rate to clear in terms of generating income is also almost zero. The investments you are making do not have to generate cash flow right now to support the cost of your borrowing, because you’re borrowing for nothing… So now you have trillions of dollars, owed with almost no interest, all chasing investments with the potential for massive capital appreciation – the cost of this money being so low as to render the need for current cash flows completely irrelevant to the global players of this game: Sovereign wealth funds, hedge funds, asset managers, index ETFs, mutual and closed-end funds, retirement savers, family offices, day traders, corporate treasuries and teenagers on TikTok.’

- The FT’s Martin Wolf analyses the economics of the UK’s latest budget plans, which saw a conservative government promise to increase the rate of corporation tax.

- Bloomberg Businessweek reckons that the four-day week is on its way.

- Cecchetti and Schoenholtz evaluate inflation worries with a particular focus on the implications of the dramatic growth seen in traditional broad monetary aggregates in the United States, such as M2. They cast doubt on the simple monetarist arithmetic that says that such a spike in board money will lead inevitably to higher inflation.

- A nice VoxEu column that relates to a pet hate of mine - struggling ‘heroically’ into work when sick, which the authors note can contribute significantly to the transmission of diseases. Here the focus is on the beneficial impact of sick pay, where their research draws on US state level data to show that over the last ten years states that introduced sick-pay mandates saw a decrease in seasonal flu activity by up to 30 per cent in the first years compared to states that didn’t introduce such mandates. Moreover, they reckon that this positive effect came without leading to significant falls in employment or wages. They also look at the impact of the introduction for the first time ever of a sick-leave mandate at the US federal government level, as part of the Families First Coronavirus Response Act (FFCRA) and estimate that this saw a significant reduction in COVID-19 infection rates, with an estimated decrease of 56 per cent in the weeks following the introduction of FFCRA emergency sick leave.

- An Economist briefing examines how COVID-19 has transformed the welfare state (‘Established principles such as means-testing…social insurance…and conditionality…went out of the window. Governments wrote near-blank cheques for everything from job guarantees to food. Some simply sent cash’) and asks what changes will endure (perhaps a renewed appreciation for governments’ role in pooling and underwriting risks). The same edition also looks at how the pandemic is influencing the debate around Universal Basic Income (UBI).

- This is an interesting blog post on how macro thinking in general and theories of the business cycle in particular have evolved over time, taking in the Phillips Curve, Real Business Cycle theory, and New Keynesian Macro.

- The WSJ’s Saturday Essay by Richard Florida and Adam Ozimek provides an engaging tour of how the pandemic and the rise in remote work it has sparked are reshaping the US urban landscape. Smaller urban areas, the authors argue, are becoming new ‘Zoom towns’ which, alongside the rise of ‘Cloud Commuting’, could lead to a reversal in what had been a ‘winner-take-all’ trend in US economic geography. But it would at most be only a partial reversal, as they argue that the ‘places that will compete the best are those that offer unique amenities—lakefronts like Michigan’s Upper Peninsula, ski slopes like Telluride, Colo., or Park City, Utah., college-town charms like Ann Arbor, Mich., or Madison, Wis., and cosmopolitan and creative rural communities like Woodstock, N.Y., that are close enough to big cities for occasional office visits. Many older, decaying cities, run-of-the mill suburbs with nothing to offer but tract houses, and depressed rural areas are likely to fall further behind.’

Latest news

Already a member?

Login to view this content