February delivered another excellent result for the labour market with employment up by almost 89,000 people and the unemployment rate plunging by half a percentage point to 5.8 per cent. That left employment less than 0.1 per cent below where it had been in February 2020, pre-pandemic. The latest experimental payroll data were also consistent with ongoing recovery in the labour market, with job numbers by end February just 0.2 per cent below the index benchmark.

Consumer confidence slipped back a little in the week ending 13-14 March. The minutes from the 2 March meeting of the Reserve Bank Board confirmed that the RBA still doesn’t expect to change the cash rate until 2024. Overseas travel statistics show that travel to and from Australia remains at record lows.

This week’s readings include a new RBA Bulletin, the latest ABS COVID household survey, the rise of digital technology, what happens after JobKeeper ends, 17 reasons to be optimistic about economic recovery, how Europe and the United States ‘lost’ COVID, supercycle scepticism, the global baby bust, and the case for a strategic shiraz reserve.

I gave a webinar this week looking at some of the forces likely to drive the global and Australian economies this year, including vaccine rollout, the US$1.9 trillion American Recovery Plan, the clash between the everything rally and the reflation trade, the evolving shape of the Australian recovery and a quick overview of some of the known unknowns that will influence the structure of our post-pandemic economy.

And stay up to date on the economic front with our AICD Dismal Science podcast.

What I’ve been following in Australia:

What happened:

Employment rose by 88,700 people (a 0.7 per cent increase) in February, seasonally adjusted. Full-time employment rose by 89,100 while part-time employment fell by 500, leaving the part-time share of total employment unchanged relative to February 2020, at 31.6 per cent.

Monthly hours worked in all jobs rose by 102 million hours relative to January, reaching 1,767 million. That was 0.2 per cent above the hours worked in February 2020. That large (6.1 per cent) rise in seasonally adjusted hours worked in February represents payback following the outsized fall (a drop of 4.9 per cent) in January, when a larger than usual number of people took annual leave.

The unemployment rate plunged by half a percentage point from (a revised) 6.3 per cent in January to 5.8 per cent in February, while the underemployment rate rose by 0.4 percentage points to 8.5 per cent. The net impact was a 0.1 percentage point decline in the underutilisation rate to 14.4 per cent. Across the states and territories, the decline in the unemployment rate was led by falls of 0.8 percentage points in Queensland, 0.7 percentage points in Victoria and the Northern Territory and 0.4 percentage points in New South Wales.

The national participation rate was unchanged at 66.1 per cent in February while the employment to population ratio rose to 62.3 per cent.

Why it matters:

The run of consecutive months of strong employment results continued in February with the outcome substantially exceeding market expectations, with the consensus having predicted an employment increase of 30,000 and an unemployment rate of 6.3 per cent.

The number of employed Australians is now back above 13 million and is less than 0.1 per cent below the February 2020 pre-pandemic result.

The story is almost as positive in terms of unemployment. By last month, the number of unemployed had fallen to 805,200. That compares to a bit less than 696,000 unemployed in February 2020 – so that’s still more than 100,000 additional people without work. Even so, that compares favourably to a peak of more than one million unemployed in July 2020.

There was one small bit of disappointing news alongside all of the good results: the number of Australians working zero hours for economic reasons rose to more than 126,000, in part reflecting the impact of the Western Australia lockdown in the first week of last month.

At 5.8 per cent, February’s unemployment rate remains above the ‘comfortably below’ six per cent test set by the government for any shift in the focus of fiscal policy from sustaining the recovery to debt and deficits. Granted, ‘sustainably below’ leaves some wriggle room, but the Treasurer has suggested that this is likely to mean an unemployment rate of around 5.25 per to 5.5 per cent. It’s even further away from the kind of unemployment rate that the RBA thinks will be necessary to restore wage growth and push inflation into its target band – which is thought to be below the five per cent mark. All of which means that in terms of levels we still have a long way to go before the macro policy framework will start to adjust. At the same time, however, it’s important to recognise that the rate of progress towards both of these targets is running well ahead of the expectations earlier set out by the government, the RBA or private sector forecasters.

The next big test for the labour market will be the end of the JobKeeper program later this month, where estimates of the size of potential job losses range from around 100,000 to 200,000 with a bias towards the lower end of that range.

What happened:

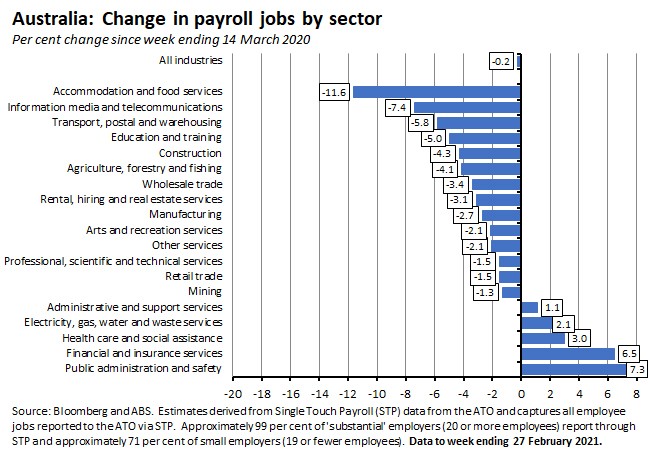

According to the ABS, between the weeks ending 14 March 2020 and 27 February 2021 the number of payroll jobs in Australia was down by just 0.2 per cent while total wages paid rose by one per cent. For the most recent fortnight of data, between the weeks ending 13 and 27 February 2021, the number of payroll jobs edged higher by 0.4 per cent, compared to an increase of 1.3 per cent in the previous fortnight. Total wages paid were unchanged over the most recent two weeks of data.

By state and territory, since the week ending 14 March 2020, the number of payroll jobs has increased in the Northern Territory (up 2.5 per cent), South Australia and Western Australia (both up 1.5 per cent). Elsewhere, however, numbers are still below their pre-pandemic levels, with the biggest shortfalls in Victoria (down 1.3 per cent) and Tasmania (down one per cent). Across the most recent fortnight of data, between the weeks ending 13 and 27 February 2021, job numbers rose in every state and territory except for Tasmania, with the largest gains of 0.6 per cent in both Western Australia and Queensland and a 0.5 per cent increase in the Northern Territory.

By industry, the biggest losses in payroll jobs since the week ending 13 March 2020 have been in accommodation and food services (where jobs are still almost 12 per cent down), information media and telecommunications (down by 7.4 per cent) and transport, postal and warehousing (down 5.8 per cent). The biggest gains have come in public administration and safety (where job numbers are more than seven per cent higher) and in financial and insurance services (up 6.5 per cent).

Across the latest fortnight of data, between the weeks ending 13 and 17 February 2021, the biggest changes in job numbers included 2.8 per cent increases for administrative and support services and for education and training and a 1.2 per cent gain for public administration and safety offset by a fall of 1.8 per cent in job numbers in agriculture, forestry and fishing and a one per cent decline in professional, scientific and technical services.

Why it matters:

This latest set of payroll jobs data shows the total number of jobs down just 0.2 per cent relative to job numbers in the week that Australia recorded its 100th confirmed COVID-19 case, while three states and territories (South Australia, Western Australia and the Northern Territory) have now more than recouped all job losses. The recovery remains uneven, however, with job numbers still well down in Tasmania and Victoria, and likewise in several industries including in particular accommodation and food services.

In terms of the momentum of the recovery, since the end of January, there has been a strong rise in payroll job numbers across Australia, with an overall gain of 1.7 per cent and rises in excess of one per cent across every state and territory.

Finally, as always we note that while the payroll data offer a useful additional source of (more frequent) insight on labour market conditions, they also come with several health warning attached: the series is still classified by the ABS as ‘experimental estimates’, the numbers are not seasonally adjusted, and recent data in particular are subject to quite substantial revisions.

What happened:

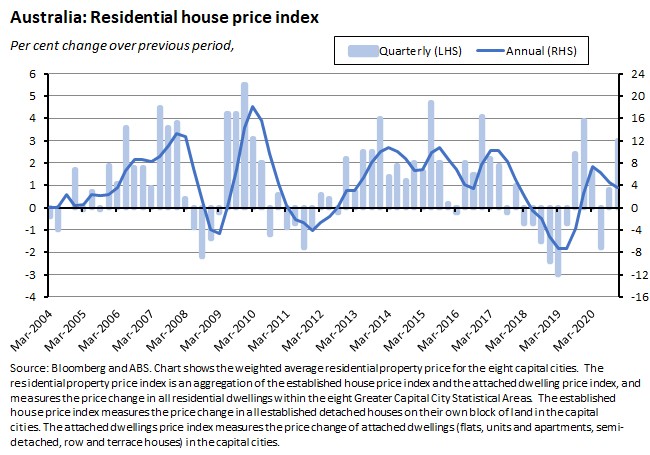

The ABS said that the weighted average of its eight capital cities Residential Property Price Index rose three per cent over the December 2020 quarter to be up 3.6 per cent in annual terms.

The total value of residential dwellings in Australia rose by $257.9 billion to $7,724.4 billion in Q4:2020 and the mean price of residential dwellings in Australia is now $728,500.

Prices increased over the quarter in all eight cities, with the rate of increase ranging from 2.2 per cent in Darwin to 3.4 per cent in Melbourne and Canberra. In annual terms, price gains were smallest in Darwin (up 2.3 per cent) and Melbourne (up 2.9 per cent) and largest in Canberra (up 5.2 per cent) and Hobart (up 6.4 per cent).

Why it matters:

The three per cent pace of quarterly price gains recorded in Q4 last year was the fastest rate of increase since the same quarter in 2019. According to the ABS, this was also the first time that all eight capital cities enjoyed an annual rise since the Q4:2014. All of which matches the current narrative of a booming housing market.

The quarterly release also included a special article on residential property sales activity which reports that the number of residential property transfers increased 7.2 per cent across Australia in 2020 with the count of transfers up 2.1 per cent for the combined capital cities and 16.4 per cent for the regions outside the capital cities. Transfer counts increased in all capital cities apart from Melbourne and Hobart last year, with the strongest increases in Perth (up 20.5 per cent), Canberra (up 12.9 per cent), Sydney (up 12.2 per cent), and Brisbane (up 10.7 per cent).

What happened:

The ANZ-Roy Morgan Index of Consumer Confidence slid 0.9 per cent to an index reading of 110.9 for the week ending 13-14 March 2021.

All but one of the subindices fell over the week: ‘current financial conditions’ slipped 2.5 per cent, ‘future financial conditions’ declined 0.6 per cent, ‘current economic conditions’ fell 0.6 per cent and ‘future economic conditions’ dropped 1.1 per cent. The only exception to the pattern was ‘time to buy a major household item’ which rose 0.1 per cent.

Why it matters:

ANZ economics suggested that the slight decline in the confidence index could reflect concerns over the upcoming end of JobKeeper. Or alternatively, the drop ‘could simply be a pure ‘noise’ in the data.’

What happened:

The RBA published the minutes from the 2 March 2021 meeting of the Reserve Bank Board. Points to note include:

- Members remained sceptical about global markets’ fears of ‘a sustained increase in consumer price inflation. This was considered unlikely for as long as substantial spare capacity remained in labour markets and wages growth remained subdued.’

- Turning to the domestic economy and the near-term outlook for the labour market, the minutes record that ‘the end of the JobKeeper program was seen as unlikely to result in a sustained increase in the unemployment rate…The number of people working zero hours in Australia had declined significantly in recent months to be close to pre-pandemic levels…some JobKeeper recipients, including the self-employed, were more likely to suffer a decline in income than lose employment at the end of the program. Information from liaison contacts had suggested that many firms in receipt of JobKeeper subsidies had already reduced the size of their workforces and were not planning on another large round of lay-offs...Members also took note of the increases in forward-looking indicators of labour demand, such as job advertisements and vacancies. These indicators had suggested that the ongoing recovery in labour market conditions could be broadly sufficient to offset the job losses arising after the end of the JobKeeper program.’

- Members could detect little sign of wage or inflationary pressure in the economy.Granted, the December quarter wage price index (WPI) had grown quite quickly over the quarter, but ‘[s]tripping out the effects of temporary pay cuts and their subsequent reversal in the December quarter, wages growth remained very subdued. Indeed, wages growth remained around historical lows in many industries, consistent with there being spare capacity across the labour market. The share of firms in the Bank's liaison program with wage freezes in place had remained high, and most firms had continued to report limited upward pressure on wages despite anecdotal reports of labour shortages in small segments of the labour market...Members agreed that a materially lower unemployment rate would be needed to generate wages growth in excess of 3 per cent, which in turn would be required to ensure inflation was sustainably in the 2 to 3 per cent target range.’

- Building on this assessment, ‘Members discussed the rate of wages growth that would be needed for inflation to be sustainably within the 2 to 3 per cent target range…it was likely that wages growth would need to be sustainably above 3 per cent, which was well above its current level…The Board's judgement was that wages growth would be unlikely to be consistent with the inflation target earlier than 2024.’

- ‘Members discussed the operation of the 3-year yield target, to which the Board remained committed. Later in the year, members would need to consider whether to maintain the April 2024 bond as the target bond or shift the focus of the yield target to the November 2024 bond. The Board agreed that it would not consider removing the target completely or changing the target yield of 10 basis points.’

- ‘Members…acknowledged the risks inherent in investors searching for yield in a low interest rate environment, including risks linked to higher leverage and asset prices, particularly in the housing market’ but the ‘Board concluded that there were greater benefits for financial stability from a stronger economy, while acknowledging the importance of closely monitoring risks in asset markets.’

- ‘Members affirmed that the cash rate would be maintained at 10 basis points for as long as necessary…until actual inflation is sustainably within the 2 to 3 per cent target range. For this to occur, wages growth would need to be materially higher than it is currently. This would require significant gains in employment and a return to a tight labour market. The Board does not expect these conditions to be met until 2024 at the earliest.’

Why it matters:

The minutes confirm the message sent by the central bank in both the statement following the 2 March meeting and in Governor Lowe’s speech last week, both of which have been discussed in detail previously: the RBA won’t move on rates until it sees actual inflation in the target range and moreover until it is convinced that it will stay there for some time. That in turn will require a tight labour market in order to deliver wage growth of more than three per cent. And the economy is unlikely to see that ‘until 2024 at the earliest.’

There was a little more detail around the specifics of the Yield Curve Control (YCC) policy, with the minutes repeating the point that the RBA would consider later this year whether it would maintain the April 2024 bond as the target bond or shift to the November 2024 bond, but adding that ‘it would not consider removing the target completely or changing the target yield of 10 basis points.’

What happened:

The ABS published provisional overseas travel statistics for February 2021. The numbers show that arrivals fell 18.5 per cent over the month to just 25,800, leaving them down 98.4 per cent over the year. In the same month, departures fell 23.6 per cent to 32,800 trips, which is 97.5 per cent year down on February 2021

Why it matters:

Travel to and from Australia remains at record lows. Pre-COVID, a typical month would see more than one million arrivals compared to the less than 26,000 trips recorded in February this year.

What I’ve been reading . . .

Three from the RBA this week.

- First RBA Governor Lowe’s remarks to the Melbourne Business Analytics conference.

- Next, Assistant Governor Chris Kent’s speech on small businesses finance in the pandemic, which notes that while small firms have generally been hit harder than larger ones (small businesses were around twice as likely as large businesses to have reported revenue declines of 50 per cent or more in June last year), there has been little change in overall lending to the SME sector during the pandemic – partly because firms have been reluctant to take on new debt at a time of high uncertainty, partly because of the alternative financing option provided by government support, partly because of tighter lending standards, and partly because ‘lending to SMEs in those industries most adversely affected by the pandemic has been low for some time.’

- Third, the March 2021 RBA Bulletin is now available.As always, there’s too much to cover in detail here, but my own reading list starts with the pieces on the determinants of the Australian dollar, developments in banks’ funding costs, and understanding the East Coast Gas Market.Note that there’s also more on SME financing and the economic recovery.

- The ABS released the latest survey results on Household Impacts of COVID-19, based on a February 2021 reference period.This time the data included findings on Australians’ attitudes towards working from home (WFH), study and training, COVID-19 vaccines and testing, household finances and the use of government stimulus payments.On WFH, 41 per cent of Australians aged 18 years and over with a job at the time of the survey reported working from home one or more times a week in the four weeks in February 2021 compared with 24 per cent saying the same before COVID-19 restrictions began in March 2020.Over the next six months, 47 per cent of respondents expected the amount of work from home to remain the same with only 11 per cent expecting a decline and eight per cent an increase, while in terms of preferences, 42 per cent wanted the amount of work from home to stay the same, 14 per cent wanted an increase and eight per cent a decline.See below for readings on UK and Japanese views on the same issue.

- EY’s Jo Masters and Johnathan McMenamin set out the analysis behind the new EY Global COVID-19 Economic Index.The index ranks 25 countries by economic activity (measured by GDP and employment) and combined balance sheet strength across household, government, central banks, non-financial corporates and financial institutions.Benchmarked against COVID-19 mortality per capita and this index, Australia is ranked third (behind New Zealand and South Korea) with the lowest deaths per capita and also third (behind New Zealand and Ireland) on the Economic Index.The Index suggests that while good health outcomes are not a guarantee of good economic outcomes, they do help.Australia’s strong performance arguably sits awkwardly with disappointing private investment results, which Masters and McMenamin – echoing the RBA – explain by the persistence of high hurdle rates.

- Greg Earl’s latest economic diplomacy column for the Lowy Interpreter reviews the business to response to the coup in Myanmar and the implications of the Regional Comprehensive Economic Partnership (RCEP) as a kind of economic counterpart to the Quad.

- Roy Morgan provide an update on tracing the economic impact of COVID-19 on Australia, drawing on their survey data on employment, consumer confidence and business confidence.

- Two columns from the Conversation.Kevin Davis notes that the number of company external administrations and of personal bankruptcies dropped markedly over 2020 thanks to a range of policy initiatives including JobKeeper and JobSeeker as well as enhanced safe harbour protections.But, he argues, there is a risk that government support has only postponed the final reckoning, and that a surge in business failures and personal insolvencies may lie ahead.And Richard Holden argues that a key take away from the pending closure of the Yallourn coal-fired power plant is the missing economic signal that would be provided by government putting a price on carbon.

- For another view on some potential lessons from the Yallourn plant closure story, see also Grattan’s Tony Wood.

- The latest Melbourne Institute Tracking the Pulse of the Nation survey (pdf) shows a rise in the number of respondents reporting financial and mental stress, despite the ongoing economic recovery.

- Jeff Borland on what happens after JobKeeper ends.

- Productivity Commission Chair Michael Brennan gave a speech on the rise of digital technology.Brennan is ‘highly optimistic’ that technology and innovation will deliver higher productivity growth, arguing that there is reason to believe COVID has brought forward the adoption of new technologies - according to Infrastructure Australia, nine out of ten Australian firms adopted new technology during the pandemic, for example.Brennan sees the potential for technology to create new opportunities in remote working (‘the likelihood of going back to pre-existing levels of remote working is, well, remote’) and regtech (using technology to both improve the quality of regulation and to reduce compliance costs).

- Some praise for the New Zealand government’s decision to task the Reserve Bank of New Zealand with taking into account ‘the impact on housing when making monetary and financial policy decisions.’

- Neil Irwin in the NYT has 17 reasons to feel optimistic about the economic outlook.(AFR version here.)Those 17 reasons mostly explain why he thinks three negative mega-trends (a dearth of economy-altering innovation, a global labour supply glut and a persistent demand short-fall), may all have run their course, and include the hope that we may now be rounding the productivity J-curve, the passing of the China shock, the next phase of the demographic transition and a major shift in policy consensus in favour of running the economy hot and achieving something closer to ‘full employment’.

- Three interesting columns from VoxEu.org.First, a large survey in the UK points to a WFH Revolution for the UK labour market, with British workers hoping for two days a week WFH post-pandemic and self-estimating that they are (on average) about two per cent more efficient when they do so.In what makes for an interesting contrast, some Japanese research on WFH estimates based on survey data that suggests that WFH productivity on average was only about 68 per cent of workplace productivity and that taken overall, WFH far from being revolutionary was not a particularly big deal for the economy.Finally, on a separate subject, a column arguing that consumption behaviour can suffer from scarring effects, as consumers who have lived through times of high unemployment can subsequently stay pessimistic about their future financial situation, spend less in future years, and save more.

- BCG and The Network present a new set of rankings on working overseas and virtual mobility.Australia ranks highly as a preferred destination.

- A long essay from David Wallace-Wells on How Europe and the United States lost COVID: ‘In Europe, North America, and South America: nearly universal failure. In sub-Saharan Africa and South Asia: high caseloads and low death rates, owing largely to the age structure of populations. In East Asia, South-East Asia and Oceania: inarguable success.’The story Wallace-Wells tells is mostly a grim one of missed chances, poor choices, short-sightedness and indecision: ‘It wasn’t that these countries did nothing, because ultimately they did an enormous amount. It was that everything they did was late, unfocused, and poorly executed — at least as far as containing the actual disease was concerned.’ Yet it ends on a somewhat happy (if ambiguous) note with the technological breakthroughs of the vaccines and a striking reversal of fortune: ‘Never before in the history of medicine has the spread of an infectious disease been halted so early by the development of vaccines. And here, the U.S. and the U.K. are world-class…It’s the inverse of the story of pandemic containment, with two of the world’s most striking national failures delivering two of the most impressive vaccine programs.’

- The WSJ is sceptical about the commodities supercycle thesis, arguing that a sustained rise in commodity prices in the aggregate requires a major catalysing factor (think US or Chinese industrialisation/urbanisation) and that there is little sign of anything similar looming, although the ‘big unknown’ here is ‘how the drive to cut carbon emissions shifts supply and demand for different commodities.’

- Also from the WSJ, ‘everywhere you look, the global supply chain is a mess.’

- The Economist magazine asks a US$3 trillion question.Thanks to lockdowns and government stimulus, the world’s consumers have accumulated a lot of extra cash – it estimates about US$3 trillion in excess savings.Will global consumers spend or save?

- The IMF considers whether rising market power is a threat to the recovery, fretting that the pandemic will further entrench the market position of already-dominant firms as smaller competitors fall away, based on an estimate that the aftermath of the pandemic could see concentration increase in advanced economies by at least as much as it did in the fifteen years to end of 2015.A supporting paper with more data and background is also available.

- The Conversable Economist (Timothy Taylor) provides a helpful overview of a recent symposium on (US) antitrust law, which captures the growing arguments in favour of a more aggressive, pro-competition stance to policy in this area.The summarised papers include arguments about the role of nascent competitors (the risk that incumbents can successfully block future competition by pre-emptively buying small firms that could develop into future competitors – where a tricky complication is that it may well be that it is the prospect of being bought that encourages some start-ups in the first place), the potential mismatch between existing antirust rules and digital platforms, and the issues around horizontal mergers and trade-offs between increased efficiencies and greater market power on the impact on consumers.

- In the FT, Jeremy Grantham warns about the potential economic implications of a global baby bust.

- In October last year, Adam Tooze and Matt Klein had a great discussion on the global world order in the 1930s and today.There’s now a sequel available, which is once again a very stimulating listening – at least, it is if your thing is discussions that take in Hobson on imperialism, the road from Hamilton to Friedrich List to Stalin and socialism in one country, the possibility of the EU and China delivering a Eurasian agreement on carbon pricing and border adjustments, the case for revisiting Keynes on bancor, the idea of a strategic shiraz reserve, and even the proposition that tea-drinking helped rescue Britons from centuries of drunkenness and thereby encouraged the Industrial Revolution… great fun.

Latest news

Already a member?

Login to view this content