The Reserve Bank of Australia has trimmed its forecast for GDP growth this year to 4 per cent from 4.75 per cent in the August Statement on Monetary Policy released today. The revised forecast followed confirmation earlier this week by the RBA of market consensus that September 2021 quarter GDP would be negative. (We will take a closer look at this next week.)

The implications of the Delta variant, the vaccine rollout and state lockdowns once again dominated the economic news this week. At its August meeting, the RBA made the predictable decision to leave key settings of monetary policy unchanged. Less predictably, it also decided to stick with last month’s announcement that it would start to taper its program of asset purchases from September. Markets had expected that a looming decline in GDP over the current quarter and the prospect of a rise in the unemployment rate would have prompted a rethink. Instead, the central bank is choosing to look through the near-term impact of tougher public health restrictions to what it still thinks will be a robust growth story in 2022. It has upgraded at least some forecasts for growth and the labour market relative to its May 2012 projections.

On the data front, new payroll numbers (down 2.4 per cent nationally over the fortnight to 17 July, but down 4.4 per cent in New South Wales and five per cent in Greater Sydney) and ANZ Job Ads for July (just slightly lower but suffering their first fall in 14 months) showed lockdowns starting to take a toll on labour conditions. The housing market, meanwhile, despite some modest loss of momentum continues to see rising prices. There were month-on-month increases in dwelling values in July for every capital city, including a two per cent increase for locked-down Sydney, while the national index rose at its fastest annual rate since 2004. New loan commitments for housing and the number of total dwellings approved did both retreat in June, as the winding down of government stimulus measures continues to influence the data. But that still left both readings significantly higher in annual terms and elevated relative to recent years. Consumer confidence edged up last week as stronger sentiment in the rest of Australia outweighed another fall in New South Wales. And June saw Australia set a new record goods and services trade surplus.

This week’s reading and listening roundup includes Grattan on accelerating the vaccine rollout and the riskiness of the Government’s transition plans, the ACCC’s advice to privatise for efficiency or not at all, an update on regional migration, scepticism about geo-economics, valuing the Olympics and soft power, Xi Jinping’s Capitalist Smackdown, the global housing boom, market fundamentalists vs economically illiterate humanists, and what might Milton Friedman make of contemporary monetary policy.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast .

Listen and subscribe: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

At its meeting on 3 August 2021, the RBA Board decided to leave the settings of monetary policy unchanged. The target for the cash rate remains at 10bp, the target for yield curve control (YCC) likewise stays at 10bp for the yield on the April 2024 Australian Government Bond, and the central bank’s quantitative easing (QE) program will continue to run at a weekly rate of asset purchases of $5 billion until early September, and then at $4 billion / week until at least mid-November.

With regard to the impact of the Delta variant and recent state lockdowns, the accompanying statement noted that:

‘The recent outbreaks of the virus are…interrupting the recovery and GDP is expected to decline in the September quarter. The experience to date has been that once virus outbreaks are contained, the economy bounces back quickly. Prior to the current virus outbreaks, the Australian economy had considerable momentum and it is still expected to grow strongly again next year. The economy is benefiting from significant additional policy support and the vaccination program will also assist with the recovery.’ [emphasis added]

The statement also provided a preview of the updated forecasts that will arrive with Friday’s publication of the August Statement on Monetary Policy:

‘The economic outlook for the coming months is uncertain and depends upon the evolution of the health situation and the containment measures. Beyond that, the Bank's central scenario is for the economy to grow by a little over four per cent over 2022 and by around 2½ per cent over 2023. This scenario is based on a significant share of the population being vaccinated by the end of this year and a gradual opening up of the international border from the middle of 2022. The Board also considered a range of other scenarios, with the main source of uncertainty being the health situation.’

Under that central scenario, the RBA reckons that the current lockdowns will generate a short-term increase in the headline unemployment rate, but that most of the adjustment in the labour market will take the form of falls in hours worked and in the participation rate. The unemployment rate is then projected to return to its trend decline, dropping to around 4.25 per cent at the end of 2022 and four per cent at the end of 2023. While this will eventually have implications for wage growth and inflation, the RBA’s view is that any changes will be gradual:

‘…it takes some years for the stronger economy to feed through into wage and price increases that are consistent with the inflation target. In underlying terms, inflation is expected to be 1.75 per cent over 2022 and 2.25 per cent over 2023.’

In terms of future monetary policy settings, the statement repeated its commitment that it ‘will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range,’ adding that the ‘central scenario for the economy is that this condition will not be met before 2024.’ And on QE, it said that the ‘Board will maintain its flexible approach to the rate of bond purchases. The program will continue to be reviewed in light of economic conditions and the health situation, and their implications for the expected progress towards full employment and the inflation target.’

Why it matters:

The most striking news from August’s meeting was the RBA’s decision to leave the planned taper of the QE program in place, despite the economic headwinds coming from lockdowns and the battle to contain the Delta variant. Heading into this week, markets and RBA-watchers had both been expecting that the central bank would reverse July’s decision to scale back the weekly rate of asset purchases in response to a widely anticipated contraction in GDP this quarter. Instead, the RBA has decided to look through the short-term impact of current lockdowns and focus on what it still judges will be a strong economic performance in 2022 and 2023, and moreover a somewhat stronger performance than it had been expecting earlier this year. That said, it did leave scope to revisit the QE decision, noting that it will ‘maintain its flexible approach’ towards asset purchases and continue to review the program in light of changing conditions.

Australia’s central bank does accept that recent developments will have some adverse economic consequences. It buys the consensus view that output will fall in Q3. And it acknowledges that there will likely be a short-term increase in unemployment, too. But it reckons that this will be temporary, and that the bulk of the labour market adjustment will take the form of some combination of lower hours worked and exits from the labour market, thereby limiting even that temporary rise in the measured number of unemployed. It also assumes that the current lockdown – despite its likely duration – will mirror its predecessors in that once restrictions are loosened activity will enjoy a relatively swift comeback.

This relatively sanguine view of the short-term risks (suitably caveated with a note that the immediate outlook ‘is uncertain and depends upon the evolution of the health situation and the containment measures’) was combined with some modest upgrades to the prospects for the economy in 2022 and beyond. We will get more detail in the August Statement on Monetary Policy. But Tuesday’s commentary provided some early details. The RBA now expects real GDP growth next year to run at four per cent instead of the 3.5 per cent predicted in the May 2021 Statement on Monetary Policy, for example. Similarly, while back in May it forecast the unemployment rate to be 4.5 per cent at the end of 2022 and to still be there June 2023, it now thinks that the unemployment rate will fall to 4.25 per cent by the end of next year and drop again to four per cent by end-2023. There’s even what might be a modest upgrade to inflation prospects: May’s Statement had underlying inflation at two per cent by mid-2023 while the RBA now expects inflation to run at 2.25 per cent over the full year. Those changes to its forecasts haven’t been large enough to shift the central bank’s forward guidance that it doesn’t expect to change the cash rate until 2024, but – assuming things play out as Martin Place expects – they would seem to tip the balance of risks around that decision towards an earlier move to normalise monetary policy.

In the meantime, the merits of the RBA’s decision this month to stick with the plan will – along with the outlook for the economy overall – be hostage to Australia’s battle to contain the Delta variant while ramping up the national rate of vaccinations. As Tuesday’s statement notes, the RBA’s central scenario ‘is based on a significant share of the population being vaccinated by the end of this year and a gradual opening up of the international border from the middle of 2022.’

What happened:

The Prime Minister and Treasurer held a press conference on 3 August 2021 to announce the public release of the Doherty Report to the National Cabinet. That Report plus an Economic Impact Analysis produced by Treasury underpins the National Plan to Transition Australia’s National COVID-19 Response published last Friday

The National Plan set out a four-phase approach to ‘transition Australia’s COVID-19 response from its current pre-vaccination settings focused on continued suppression of community transmission, to post-vaccination settings focused on prevention of serious illness and fatalities.’ Phases B and C of the plan are triggered by reaching vaccination thresholds set at both the national and the individual state/territory level, with the target expressed as a percentage of the adult population (those aged 16 and over).

- Phase A. Vaccinate, Prepare and Pilot (Current Phase)

Focus is on suppressing the virus for the purpose of minimising community transmission via measures including accelerating vaccination rates, closing international borders, and early, stringent and short lockdowns if outbreaks occur.

- Phase B. Vaccination Transition Phase (c.70 per cent of adult population fully vaccinated)

Focus on minimising serious illness, hospitalisations and fatalities as a result of COVID-19 with low-level restrictions. Measures may include maintaining high vaccination rates, encouraging uptake through incentives and other measures, minimising cases in the community through ongoing low-level restrictions and effective track and trace, international border caps and low-level international arrivals, capped entry of student and economic visa holders, and preparation/implementation of a vaccine booster programme. Lockdowns unlikely but possible and targeted.

- Phase C. Vaccination Consolidation Phase (≥80 per cent of adult population fully vaccinated)

Focus on minimising serious illness, hospitalisations and fatalities as a result of COVID-19 with baseline restrictions. Measures may include maximising vaccination coverage, minimum ongoing baseline restrictions adjusted to minimise cases without lockdowns, exempting vaccinated residents from all domestic restrictions, abolishing all caps on returning Australians, lifting all restrictions on outbound travel for vaccinated Australians, increasing capped entry for student, economic and humanitarian visa holders, and if necessary use of highly targeted lockdowns only.

- Phase D. Final Post-Vaccination Phase.

Focus on managing COVID-19 in a way consistent with public health management of other infectious diseases such as influenza. Measures may include open borders with quarantine for high-risk inbound travel, uncapped inbound arrivals for all vaccinated persons without quarantine, and minimising community cases without lockdowns or restrictions.

The Doherty Report

The Doherty Report uses models of COVID-19 infection and vaccination to suggest a target rate of vaccine coverage for the transition to Phase B of the National Plan. It considers a range of targets (50/60/70/80 per cent vaccination rates) and two main vaccine allocation strategies: an ‘all adults’ scenario under which vaccinations are not prioritised in any particular order by age and an ‘oldest first scenario’ where vaccinations are prioritised from oldest to youngest.

The focus is on developments in Transmission Potential (TP), which is akin to the effective reproduction number (sometimes known as Re or Reff). If TP can be driven below one, no public health actions are needed to control an outbreak, as it will be self-limiting. On the other hand, the higher the TP is above one, the more rapidly case numbers will grow after an outbreak, and the harder it will be for the health authorities to bring the outbreak under control. A TP of less than one, therefore, is needed both to contain community transmission in our current Phase A and to prevent cases from exceeding the capacity of Australia’s health sector in Phase B.

Estimates of TP are influenced both by private decisions to change behaviour with regard to physical distancing and by imposed changes in behaviour arising from public health restrictions, or Public Health and Social Measures (PHSMs). The report considers four ‘bundles’ of PHSM restrictions. The first of these are baseline PHSMs where there are only minimal density restrictions in place. Then, in rising order of stringency, there are Low PHSMs, Medium PHSMs (such as the NSW measures introduced on 1 July this year) and High PHSMs (such as those deployed in Victora’s strict Stage Four lockdown last year). Each of these PHSMs also incorporates a set of test, trace, isolate and quarantine (TTIQ) measures. Importantly, the efficacy of TTIQ is assumed to decline as community transmission and case numbers increase, reflecting the constraints implied by limited public health capacity.

Using this framework, the report demonstrates that as vaccination coverage increases, less stringent levels of PHSMs are required to bring TP to below one. For example, as shown in the chart below, high PHSMs would still be needed to curb transmission at 50 per cent and 60 per cent vaccination coverage rates, as at these levels rapid rates of epidemic growth would still be expected. At 70 per cent rates, medium PHSMs might suffice, however, and at 80 per cent vaccination rates, low PHSMs might be enough.

Moreover, if case numbers can be kept low enough to allow the maintenance of optimal (instead of partial) TTIQ effectiveness, then a combination of 70 per cent vaccine coverage and low PHSMs ‘would likely be sufficient for control.’ Likewise, ‘applying continuous low-level social restrictions makes the requirement for stringent lockdowns unlikely at 70 per cent population vaccine coverage.’ These are the results that help underpin the 70 per cent vaccination rate that is cited as a precondition for triggering Phase B in the National Plan.

Source: Doherty Institute

The report finds that the ‘all adults’ approach dominates the ‘oldest first’ approach. It also considers the case for extending the vaccine program to the 12-15 age group but argues that this ‘has minimal impact on transmission and clinical outcomes for any achieved level of vaccine update.’

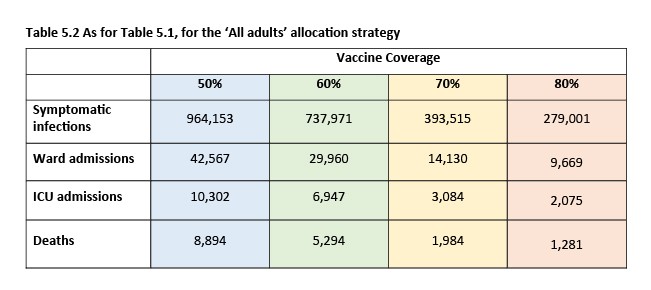

What are the potential health implications of a transition to Phase B? The report includes the results from a series of epidemic simulations, based around the assumption that a single outbreak involving 30 individuals initiates community transmission at the time of a national transition to Phase B, once a given target vaccine rate has been achieved. For example, the table below reports key cumulative health outcomes over the 180 days following an outbreak for the ‘all adults’ allocation strategy, assuming only baseline PHSM restrictions and partial TTIQ effectiveness. Here, hospital admissions range from more than 42,000 under a 50 per cent vaccination rate to less than 10,000 under an 80 per cent rate, while deaths range from almost 9,000 to closer to 1,000 under the corresponding vaccination rates.

Source: Doherty Institute

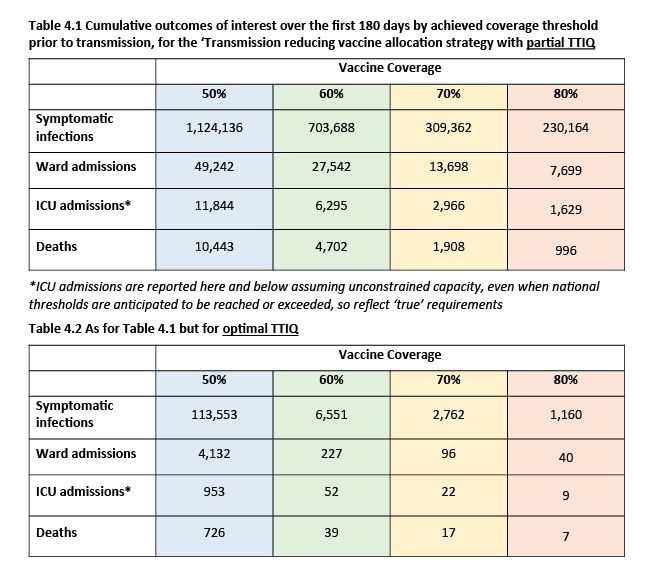

In an addendum to the main report, the Institute also considers a ‘transmission reducing strategy’ which builds on the ‘all adults strategy’ but adds a focus on achieving high vaccine coverage in the key transmitting population group of those aged 20-39. That adjustment delivers a further modest reduction in the TP rate and delivers lower death and case numbers under the same scenario as noted above. Then, as before with regard to reductions in TP, if the assumption of partial TTIQ effectiveness is replaced by an assumption of optimal TTIQ effectiveness, the results become considerably better at all vaccination rates.

Source: Doherty Institute

In summary, the key messages from the Doherty Report are that vaccine coverage rates of 70 per cent or above are a precondition for moving away from the need for extended and stringent PHSMs, that at these higher vaccination rates pandemic control should become easier and the need for tough lockdowns become much less likely, and that having case numbers low enough to deliver optimal TTIQ rather than partial TTIQ makes a very significant difference to health outcomes.

Treasury’s Economic Impact Analysis

In a separate piece of work, Treasury has estimated the direct economic costs of the different approaches identified by the Doherty Institute under the ‘All adults’ vaccination strategy. Treasury’s Economic Impact Analysis considers the 50 to 80 per cent range of vaccination rates as well as two strategies: a case minimisation strategy under which community transmission is limited, case numbers remain low and therefore optimal TTIQ is possible, and a managed transmission strategy, where there is ongoing community transition leading to only partially effective TTIQ. The analysis also considers the economic costs associated with Baseline, Low, Medium (or Moderate) and High (or Strict) PHSM ‘bundles’, which range from $0.1 billion per week for Baseline PHSMs up to $3.2 billion per week for Strict PHSMs.

Source: Treasury

These estimates only include the direct impact of restrictions on activity. They do not include a range of other costs including indirect confidence effects, labour market scarring, social costs, disruption to supply chains, the economic costs of illness and death, and any associated fiscal costs.

The Impact Analysis takes these cost estimates for the four PHSM Bundles and multiplies them by the expected duration and coverage of restrictions as estimated by the Doherty Institute, also taking into account how changing vaccination rates reduce the estimated total amount of time in lockdown. While the Institute’s modelling provides an estimate for how long restrictions will need to be applied to bring an outbreak under control for each bundle of PHSMs at each vaccination rate, this exercise also requires making an assumption about the frequency of outbreaks. Here, for the first set of scenarios Treasury assumes that there will be, on average, five separate outbreaks in the community each quarter, each affecting one large metropolitan area or around 20 per cent of the Australian economy. The results also assume that below vaccination rates of 60 per cent, these five outbreaks will each require Strict PHSMs to be applied for an of average two weeks to bring community transmission back to zero – giving a cumulative total of ten weeks per quarter.

Treasury’s first set of scenarios considers a strategy designed to minimise case numbers where the economy operates with an ongoing baseline level of PHSMs and with optimal TTIQ. Under this scenario, the assumption is that at a 50 per cent vaccination rate only strict lockdowns will suffice, with up to 70 days per quarter of strict lockdowns needed to manage the pandemic within the capacity of the health system. At 70 and 80 per cent rates, however, periodic low-level restrictions become a viable option. For example, at an 80 per cent rate, the response could be 18 days per quarter of periodic low-level restrictions, or 11 days per quarter of periodic moderate lockdowns, or seven days per quarter of periodic strict lockdowns. Estimates of the associated level of weekly costs for this scenario range from a high of $570 million / week (50 per cent vaccination rate, periodic strict lockdowns) to a low of $140 million / week (80 per cent or higher vaccination rate, periodic low-level restrictions only).

A second set of scenarios models the implications of applying Low PHSMs at all times rather than baseline restrictions. The trade-off here is that by applying a higher level of ongoing restrictions the need for strict and moderate lockdowns is reduced at each vaccination rate, but at a higher ongoing economic cost. At 50 and 60 per cent vaccination rates, periodic lockdowns are still required to minimise case numbers in addition to the Low PHSMs, but at 70 and 80 per cent rates lockdowns are no longer necessary at all. At each vaccination rate, however, the economic costs are larger than with baseline restrictions, ranging from a high of $1.1 billion / week (50 per cent vaccination rate, periodic strict lockdowns) to a low of $660 million / week (70 per cent or higher vaccination rate, no lockdowns required).

Finally, Treasury also considers a third set of scenarios where ongoing case numbers are higher and, as a result, TTIQ protocols are only partially effective. Here the focus shifts from the number of outbreaks per quarter to the amount of time different restrictions are required to be in place to cap transmission at a rate that keeps cases below health system capacity limits (that is, that are required to hold TP at around one). These range from 77 days per quarter under strict lockdown at a 50 per cent vaccination rate to 29 days per quarter under strict lockdowns or 81 days of low-level restrictions, both at an 80 per cent rate. This strategy is estimated to have direct costs ranging from a high of $2.7 billion / week while vaccination remains at 50 per cent and baseline restrictions are in place (almost five times the cost of managing COVID-19 under the strategy to minimise cases at the same vaccination rates) to a low of $590 million / week (80 per cent vaccination rate, periodic low-level restrictions). The intuition here is that, by acting later and allowing COVID to spread more widely, longer and more severe lockdowns are required to prevent the health system being overrun. As vaccination rates increase, lockdown requirements and the associated economic costs decline, but still remain substantial.

The chart below summarises the least cost combination of PHSM measures for each vaccination rate, for each scenario:

Source: Treasury

Comparing across results shows that the most cost-effective way to manage COVID-19 is by pursuing a strategy of minimising case numbers, aiming for optimal TTIQ and applying ongoing baseline restrictions. Strict, localised lockdowns for shorter durations are more cost effective than more moderate lockdowns for longer periods. And regardless of the strategy employed, rising vaccination rates significantly reduce the economic costs of managing the pandemic, with the ‘best case’ cost falling from $570 million a week at a 50 per cent vaccination rate to $140 million a week at an 80 per cent rate.

Why it matters:

The two reports released this week both provide useful frameworks for thinking through the challenges raised by the Delta variant. They also offer some numbers that are a helpful guide to the possible relative magnitudes involved in terms of health and economic outcomes: for example, while Treasury estimates that the strictest lockdown comes at a cost of $3.2 billion/week, a moderate lockdown still costs $2.35 billion/week. But what they mainly do is confirm what we already knew. That is, that the endgame for the pandemic remains conditional on achieving a high vaccination rate. And that in the meantime, the most effective way to deal with outbreaks is through applying strict lockdowns for shorter time spans, not more moderate ones that run for longer. That second point is reinforced by the message around the importance of ‘optimal’ TTIQ measures, given that these are only possible when case numbers are low enough that the system has sufficient capacity to cope.

What about the relationship between these analyses and the proposed National Plan? Here, it’s worth highlighting two key caveats presented in the Doherty report.

First, it stresses that any emergence of ‘vaccine escape variants’ would ‘require re-evaluation of targets and associated requirements for public health measures.’ In other words, just as previous plans have been thrown into disarray by the Delta variant, so current plans remain hostage to further COVID developments.

Second, the report is also clear that its focus is only on the transition to Phase B, emphasising that subsequent transitions to Phases C and D will be associated with a much greater level of uncertainty. That includes some significant risks to the downside such as the ‘likely emergence of new variants within Australia or internationally exhibiting one or more of heightened transmissibility, severity or immune escape’, the ‘waning of vaccine derived and natural immunity over time’, and ‘population fatigue and the potential for declining compliance with restrictions.’ It also includes the scope for some positive surprises such as the development of new vaccine products and the ‘potential for future development of readily bioavailable therapeutics that might be used for transmission reduction, prevention of disease progress and life-saving therapies.’ The modelling presented here is not directly designed to underpin any proposed shift from Phase B to Phase C.

One last point. The National Plan says that lockdowns during Phase B are ‘unlikely but possible and targeted.’ That roughly lines up with the findings discussed above, if we take the most favourable scenario described in the Treasury scenario (the one based on ongoing baseline restrictions and optimal TTIQ). Then, the Treasury numbers say that at a 70 per cent vaccination rate we might expect to be living either with periodic low-level restrictions (but not lockdowns) for about 82 days per quarter, or with periodic moderate lockdowns for 47 days a quarter, or with strict lockdowns for 29 days a quarter, with the first of those three options coming at the lowest economic cost to the economy of around $200 million/week.

What happened:

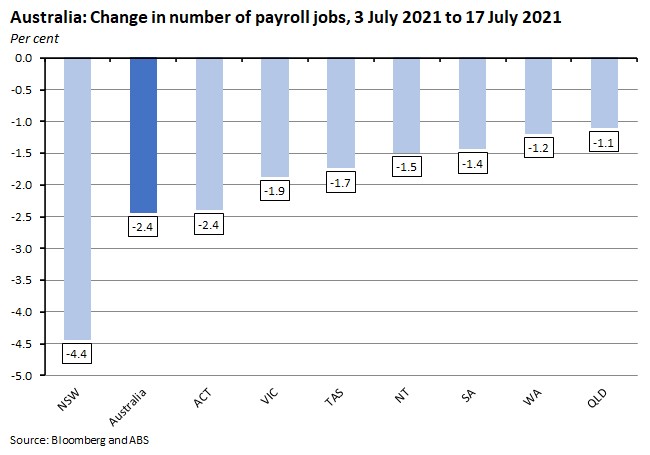

The ABS reported that the number of payroll jobs fell 2.4 per cent between the weeks ending 3 July and 17 July 2021, compared to a fall of 0.2 per cent over the previous fortnight. Job numbers were down 2.6 per cent over the past month but still up 3.3 per cent over the year. Every state and territory saw job numbers fall over the fortnight, with the decline ranging from a 4.4 per cent slump in New South Wales to a more modest 1.1 per cent decline in Queensland.

By industry, the biggest fortnightly drop in job numbers was in accommodation and food services (down 8.7 per cent) but there were also sizeable falls in agriculture (down 7.7 per cent), administrative and support services (down 5.9 per cent), other services (down 5.5 per cent) and arts and recreational services (down 4.5 per cent).

Why it matters:

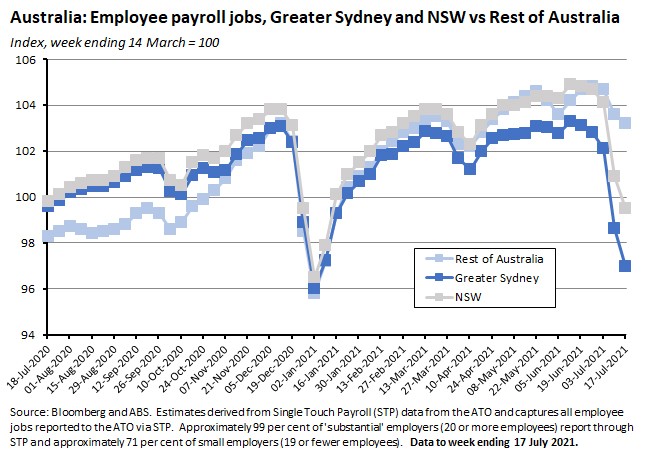

The latest fortnight of payroll jobs data captured the impact of school holidays in every state and territory, the second and third weeks of the Greater Sydney lockdown, increased COVID-19 restrictions in other parts of New South Wales and the first two days of lockdown in Victoria. No surprise, then, that a drop in job numbers was on the cards. Even so, the impact of the Sydney lockdown was particularly notable. As reported above, job numbers across New South Wales slumped 4.4 per cent over the fortnight. Job numbers in Greater Sydney fell by an even larger five per cent.

The ABS also highlighted job declines in the lockdown-sensitive accommodation and food services industry (down 19 per cent in New South Wales and 8.7 per cent nationally) and in arts and recreation services (down 18 per cent in New South Wales and 4.5 per cent nationally).

One important data issue to note. The Bureau said that the changing nature of government policy support could mean that the drop in payroll jobs numbers in July will overestimate the impact on reported unemployment in the labour force survey. That’s because current government support payments around COVID restrictions are paid directly to people or businesses, rather than through payrolls. As a result, employees who were only temporarily stood down (and therefore not paid by their employer) will show up as a fall in payroll jobs, even if the employee retains an attachment to their employer. And as highlighted by the RBA (see first story, above) the impact of lockdowns on the unemployment numbers will also be muted by the likelihood that a substantial share of labour market adjustment will instead take the form of declines in the participation rate and in hours worked.

What happened:

ANZ Job Ads edged down 0.5 per cent over the month (seasonally adjusted) to stand at 206,819 in July 2021.

The number of Job ads was up 35 per cent relative to pre-COVID (January 2020) levels.

Why it matters:

Although significant enough to produce the first fall in the number of ads in 14 months, July’s lockdowns appear to have had a relatively limited impact on firms’ demand for labour as reflected in job advertisements. Last month’s reaction was very different from the steep falls suffered in March (down 12.9 per cent) and April (a plummet of 53.1 per cent) last year. And as ANZ also noted, not only was this relative resilience the case for last month overall - the first full month of the Sydney lockdown - but it also held for the second half of the month, when Sydney tightened restrictions and when Victoria and South Australia also entered lockdown.

At current levels, Job ads are consistent with an unemployment rate of around five per cent, and it is possible that the adverse consequences from additional public health restrictions on employment and unemployment are being offset by the combination of government policy support (for example, JobSaver incentivises employers to maintain their payroll) plus a desire by businesses to hold onto their existing workforce as much as possible in order to limit search and hiring costs once activity resumes.

What happened:

CoreLogic said that Australian housing values rose 1.6 per cent in July, leaving national values 14.1 per cent higher over the first seven months of this year and 16.1 per cent higher over the past year. The combined capitals index was also up 1.6 per cent in monthly terms and 15.1 per cent higher year-on-year.

Prices were up in every capital city over the month, with the gains ranging from 0.3 per cent in Perth to 2.6 per cent in Canberra. Dwelling values in Sydney rose two per cent month-on-month and were 18.2 per cent higher in annual terms, while in Melbourne the corresponding increases were 1.3 per cent and 10.4 per cent, respectively.

Source: CoreLogic

Houses continue to see stronger price growth than units: national house values are up 18.4 per cent over the year while unit values have risen by a more modest 8.7 per cent over the same period. And regional prices once again outpaced capital prices, rising by 1.7 per cent over the month and 19.6 per cent over the year, although CoreLogic notes that this gap has narrowed over the course of 2021, with the past seven months showing a similar rate of growth in dwelling values across regional (up 14.5 per cent) and capital city (up 14 per cent) markets.

Auction clearance rates are still in the low- to mid-70 per cent range.

CoreLogic also reported that there had been some recent volatility in new inventory levels with sharp falls in the number of newly advertised properties in Sydney and Melbourne during lockdowns. In Sydney, for example, the number of new listings added to the market fell by about 30 per cent from the week ending 27 June, dragging total active listing numbers down almost 14 per cent below the fived-year average. Likewise, the number of new listings added to the Melbourne market fell 27 per cent between the weeks ending 11 July and 25 July.

Why it matters:

Australia’s home prices continued their upward journey in July, with the 16.1 per cent annual rate of growth recorded last month the fastest seen since February 2004. At the same time, however, the pace of monthly growth has continued to ease from its March 2021 peak (of 2.8 per cent). That decline in price momentum is likely the consequence of higher prices squeezing affordability plus the end of much of the previous pandemic-related support packages. It also seems probable that rising COVID-19 cases and new lockdowns have contributed to the loss in momentum, with falling listings in Sydney and Melbourne. Past experience with ‘snap’ lockdowns shows a pattern of falling buyer and vendor activity that is then followed by a rebound to pre-lockdown levels once restrictions have been eased, but CoreLogic remarks that the impact on the number of home sales and on listings has been larger in more recent lockdowns, and cautions that ‘it is reasonable to assume the uncertainty associated with the duration and severity of Sydney’s lockdown could see a greater level of disruption relative to previous shorter periods of restrictions.’

Despite the ongoing slowdown in the monthly rate of price increases, and despite the impact of the latest round of lockdowns, at 1.6 per cent July’s rate of monthly growth in housing values was still well above the 0.4 per cent average pace of monthly dwelling value appreciation recorded over the past ten years.

What happened:

The ABS said that new loan commitments for housing fell 1.6 per cent over the month (seasonally adjusted) in June 2021 but were up 82.7 per cent over the year.

The value of new loan commitments to owner occupiers fell 2.5 per cent over the month but was still up 75.9 per cent over the year. Lending to investor rose 0.7 per cent over the month and jumped 102 per cent in annual terms.

Why it matters:

June brought a drop in the value of new lending for housing that ended a run of seven consecutive monthly increases. But in absolute terms the series is down only slightly from May’s record high of $32.6 billion. Similarly, while the monthly decline in lending to owner-occupiers was the largest fall reported since May 2020, commitments were still up almost 76 per cent over the year and remain more than 64 per cent higher than their pre-COVID (February 2020) levels. Meanwhile, lending to investors in June rose to its second highest level in the history of the series.

Note that trends in lending figures continue to be influenced by the reduction in the size of the government’s HomeBuilder grant in January this year and the subsequent closing of that scheme in April. That impact was evident in a second consecutive monthly drop in the number of new loan commitments to owner-occupier first home buyers, which were down 7.8 per cent in June.

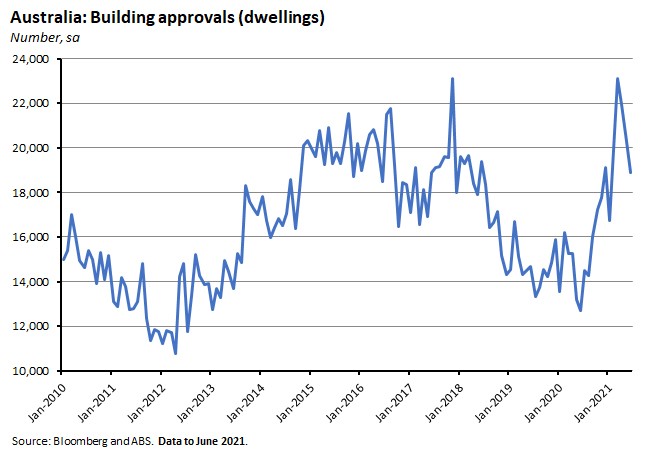

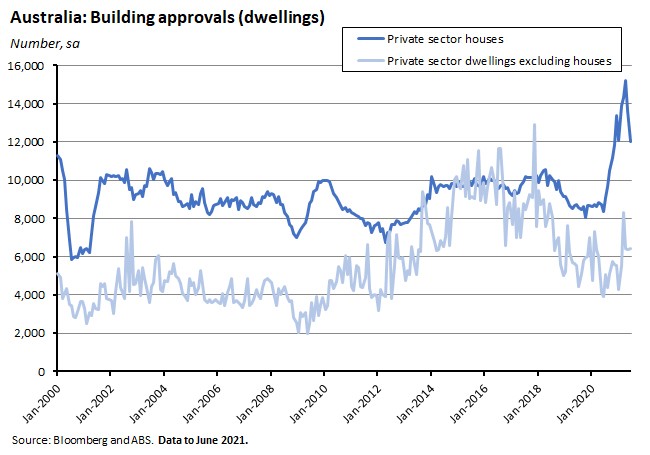

What happened:

According to the ABS, the number of total dwellings approved fell 6.7 per cent in June (seasonally adjusted) but was up 48.9 per cent over the year.

Approvals for private sector houses fell 11.8 per cent over the month but rose 44.3 per cent over the year while approvals for private sector dwellings excluding houses rose 0.8 per cent month-on-month and 63.7 per cent year-on-year.

Why it matters:

June marked the third consecutive monthly fall in the number of dwellings approved, with total approvals pulled down by the fall for private sector houses (approvals for dwellings excluding houses rose over the month). In a similar story to lending developments, the ABS noted that following the unwinding of government stimulus measures, approvals for private houses have fallen 20.9 per cent from their record high in April, but that this still left private house approvals high relative to their levels for much of the past two decades.

What happened:

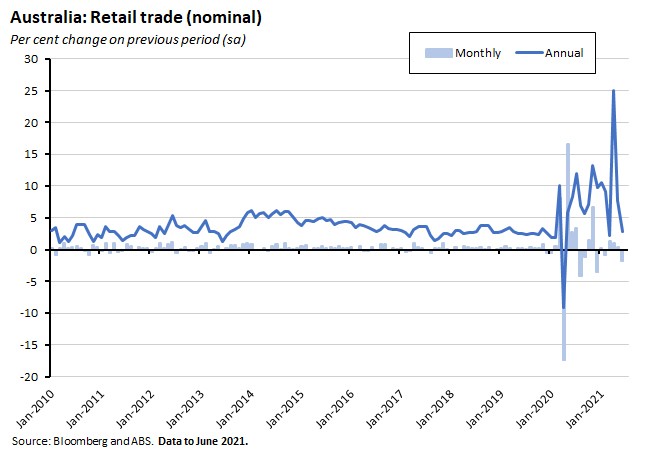

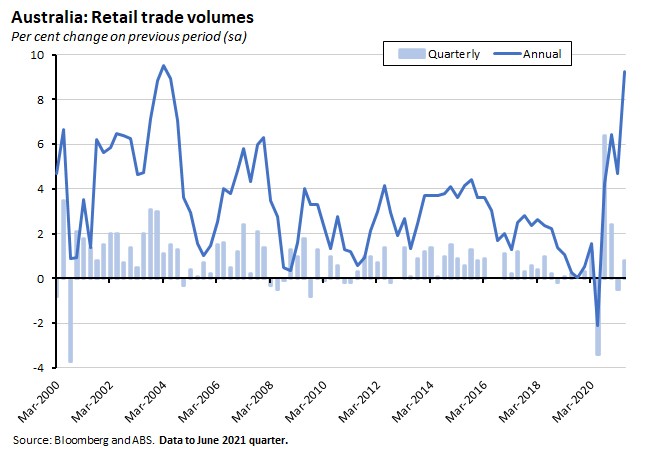

The ABS reported that the final figure for retail turnover in June 2021 was down 1.8 per cent over the month (seasonally adjusted) but up 2.9 per cent compared to June 2020.

In volume terms, the seasonally adjusted estimate rose 0.8 per cent over the June quarter 2021 and was up 9.2 per cent over the year.

Total online sales jumped 11.6 per cent in June, following falls of 4.5 per cent in May and 4.1 per cent in April, and were 11 per cent higher than in June last year.

Why it matters:

The final figure for the June monthly result was in line with the preliminary estimate reported here a couple of weeks ago as the value of turnover was dragged down by lockdowns across multiple states and territories. There were particularly large declines in retail sales for cafes, restaurants and takeaway food services (down six per cent), clothing, footwear and personal accessory retailing (down 9.5 per cent), and department stores (down seven per cent). Food retailing was the only industry to enjoy an increase over June as households substituted eating at home for dining out.

Reinforcing the centrality of the lockdown story for the monthly data, the ABS also noted that the largest falls in turnover came in those states that were under longer periods of restrictions during the month: Victoria (down four per cent), New South Wales (down two per cent), and Queensland (down 0.9 per cent). The influence of public health restrictions also appeared in online sales which rose to 10.5 per cent of total sales in June this year, up from 9.1 per cent the previous month and also higher than the 9.7 per cent share recorded in June last year.

Turning to the quarterly data, while the impact of lockdowns was felt from May onwards, retail volumes still managed to rise over Q2 as a whole, and were also up strongly in annual terms reflecting the significant spending momentum in the economy prior to the onset of the Delta strain.

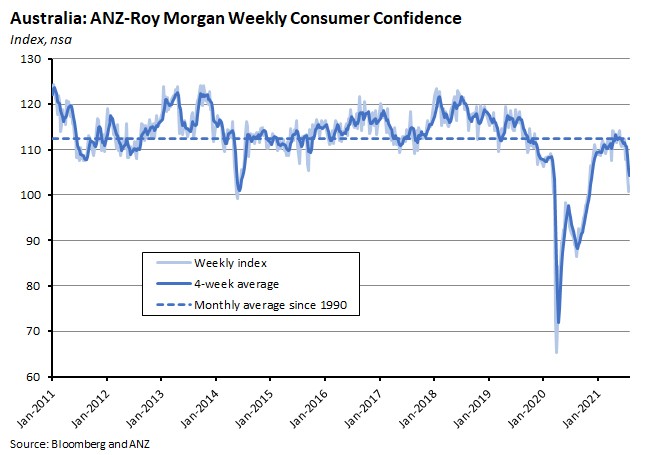

What happened:

The ANZ Roy Morgan Index of Consumer Confidence edged up 1.1 per cent last week.

Four of the five subindices rose over the week with the sole exception ‘current economic conditions’ which fell 4.7 per cent.

By geography, confidence dropped seven per cent in Sydney following the news that the NSW lockdown would be extended for a further month, but confidence rose in Melbourne (up two per cent) and Adelaide (up 2.9 per cent) as Victoria and South Australia exited their lockdowns. Confidence also rose 2.7 per cent in Brisbane, although the majority of the survey was completed before South East Queensland’s three-day lockdown was announced.

Why it matters:

After two consecutive weeks of lockdown-driven declines, sentiment rose this week as improving confidence outside New South Wales was enough to more than offset a sharp drop in Sydney. Although below its long-run average, the overall index is still up about 15 per cent over the year and is almost 56 per cent above the pandemic low it hit in late March last year.

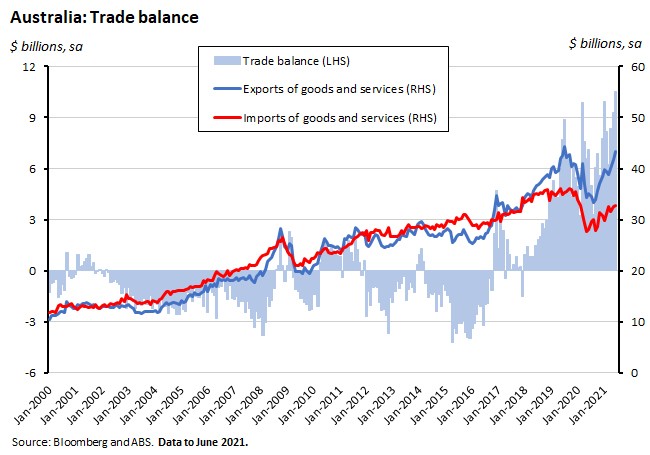

What happened:

Australia reported a record $10.5 billion goods and services trade surplus in June 2021. The ABS said that exports of goods and services rose $1.5 billion (four per cent) over the month to $43.3 billion while imports of goods and services rose $0.3 billion (one per cent) to $32.8 billion.

Why it matters:

June’s trade surplus set a new record, beating the previous record of almost $10 billion set in January this year. Strong export growth, powered by in particular by a surge in the value of exports of iron ore to China, was a key factor here, as discussed in our previous analysis of June’s merchandise trade results.

What I’ve been reading . . .

Grattan’s Race to 80 report argues that once 80 per cent of Australia’s population is vaccinated – and 95 per cent of the most vulnerable, including the over-70s – Australia can safely begin to ‘live with COVID’. It thinks that we can reach that target somewhere between the end of this year and March next year. Grattan is also critical of the Government’s National Plan.

The RBA’s August 2021 chart pack is now available.

ACCC Chair Rod Simms says Australian governments should privatise for efficiency, or not at all. According to Simms, ‘Privatisation can generate important benefits to the economy, such as improved incentives for cost control, investment and innovation to meet the needs of consumers’ but the ‘problem is that, in more recent years, many of Australia’s key economic assets have been privatised without regulation, and often with rules designed to prevent them ever facing competition. This makes us all poorer.’

Provisional data on regional migration from the ABS. In the March quarter of this year, 104,100 people moved interstate. This was 600 (0.6 per cent) less than the number who moved in the previous quarter but 16,400 (19 per cent) more than in the same quarter last year. The Bureau said that the number of interstate movers in the quarter was the highest for a March quarter since 1996. The first quarter of this year also saw a net loss of 11,800 people from Australia's greater capital cities through internal migration. This was the largest net loss on record since the series started in 2001, surpassing the previous record net loss set in the September 2020 quarter (a fall of 11,200).

Also from the ABS, updated cost of living indices. All five living indices rose over the June 2021 quarter, with transport (fuel prices) the main contributor for four out of the five. In annual terms, the rate of increase ranged from 2.3 per cent to 3.5 per cent vs the headline CPI increase of 3.8 per cent.

The Productivity Commission has published the first Annual Data Compilation Report to inform reporting on progress under the National Agreement on Closing the Gap. And Productivity Commission Chair Michael Brennan gave a speech on Reform and Sustainable Funding of Health Care.

Adam Triggs is sceptical about geoeconomics. My own view is that it’s fair enough to push back against some of the policy prescriptions that come from this approach, but that it’s hard to disagree that this way of viewing the world has become increasingly important. (Full disclosure: back in my days at the Lowy Institute I predicted the return of geoeconomics).

Greg Earl rounds up some research on the costs and benefits of hosting the Olympics with a focus on the soft power / diplomacy angle.

Also from the Lowy Interpreter, Hugh White argues that Cold War-style analogies comparing China to the Soviet Union are misplaced.

Xi Jinping’s Capitalist Smackdown. Tom Hancock and Tom Horlik describe how China’s leaders have ‘remembered they’re Communists’ and then wiped out more than US$1 trillion of the value of Chinese tech stocks. And here is Ray Dalio’s view.

John Gray: The West isn’t dying - its ideas live on in China.

The Economist on the growth slowdown in emerging markets.

The FT points out that the pandemic is creating the broadest global house price boom in two decades.

Should we blame central banks for fuelling inequality? Ken Rogoff says it’s a bit more complicated than that.

A cross-country comparison of COVID contact-tracing apps and why they appear to have failed to have had much impact on controlling the pandemic.

Charles Goodhart with a provocative take on the moral hazard of limited liability. He argues for the application of a distinction between a class of 'insiders', who would be subject to multiple liability, and 'outsiders', who would retain limited liability.

Two pieces from the IMF. First, this blog post looks at how the pandemic widened current account balances, as the collapse in travel flows, wild swings in oil prices, booming trade in medical products, surging government borrowing and spending and dramatic shifts in consumer spending patterns saw both deficits and surpluses expand. Second, the Fund has released a new policy paper on the arrival of a new era of public and private digital money and its implications for the IMF. It sees the good news as that innovation offers the prospect of easier, faster, cheaper and more accessible payments. The challenges on the other hand are around maintaining trust, protecting domestic economic and financial stability, and sustaining the stability of the international financial system.

Tyler Cowen: the future will be weirder than we think.

From the Q3:2021 Milken Review, an interesting perspective on what the authors see as a clash between market fundamentalism and economically illiterate humanism.

A couple of podcasts to finish. First, the Masters in Business podcast interviews Charity Dean on the lessons of COVID (Dean is one of the central characters in Michael Lewis’ recent book on the pandemic, The Premonition). Second, Macro Musings asks Scott Sumner to speculate on What Milton Friedman Would Think of Monetary Policy Today.

Latest news

Already a member?

Login to view this content