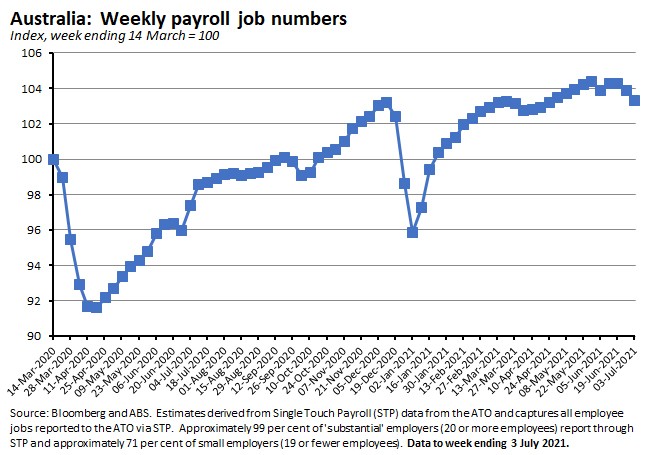

It was a relatively quiet week on the data front, but those releases we did receive largely confirmed that the Delta variant of COVID-19 and the state lockdowns led by New South Wales are now having a significant impact on the Australian economy. The ABS said that the number of payroll jobs fell one per cent over the latest fortnight of data, dragged down by job losses across every state and territory but led by a sharp drop in payroll numbers in Greater Sydney.

The Bureau also reported that the impact of coronavirus restrictions across multiple states saw the preliminary estimate for retail turnover in June suffer their biggest month-on-month decline since last December. Consumer sentiment is hurting, too: the ANZ Roy Morgan Weekly Consumer Confidence Index reported its largest drop since late March 2020 as the index slumped to its lowest level since November 2020 (although it’s also important to note that this still left it well above the lows plumbed in the first half of 2020). Given this rapidly changing backdrop, the minutes from the 6 July RBA monetary policy meeting that were published this week already feel dated. They did offer a bit more context for the central bank’s decisions earlier this month on yield curve control and quantitative easing but more importantly, RBA-watchers are increasingly convinced that the planned tapering of asset purchases that was announced on 6 July will now have be unwound in the face of the economic headwinds coming from extended lockdowns. Still, there was some good news on the data front this week: the preliminary estimate for June merchandise trade showed Australia’s goods exports continue to outperform, delivering new records for the monthly trade surplus, the value of total goods exports and the value of iron ore exports. Although it should be said that this strong export performance does come at the price of continued, substantial market and product concentration.

This week’s readings include an assessment of Australia’s economic weaknesses, updates on the housing market, how Australian policy should respond to the scourge of ransomware, how to improve our record on R&D, lots more on the global and US inflation debate, new growth forecasts for developing Asia, Biden’s China doctrine and an interesting case study of economic development in Haiti vs the Dominican Republic.

Finally, stay up to date on the economic front with our AICD Dismal Science podcast .

Listen and subscribe: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

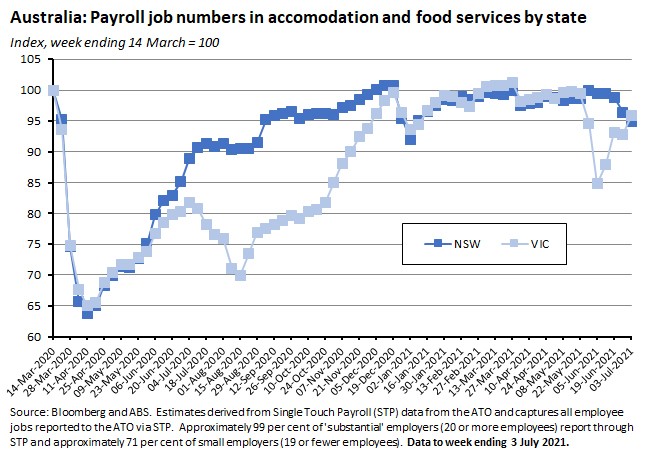

The ABS said that the number of weekly payroll jobs fell one per cent between the weeks ending 19 June 2021 and 3 July 2021, more than reversing an increase of 0.4 per cent over the previous fortnight. Over the past month, job numbers are down 0.6 per cent, although they are still up six per cent on their levels in the week ending 4 July 2020 and payroll job numbers are now 3.3 per cent higher than they were at the start of the pandemic. Note that the ABS did not report estimates for payroll wages in this release.

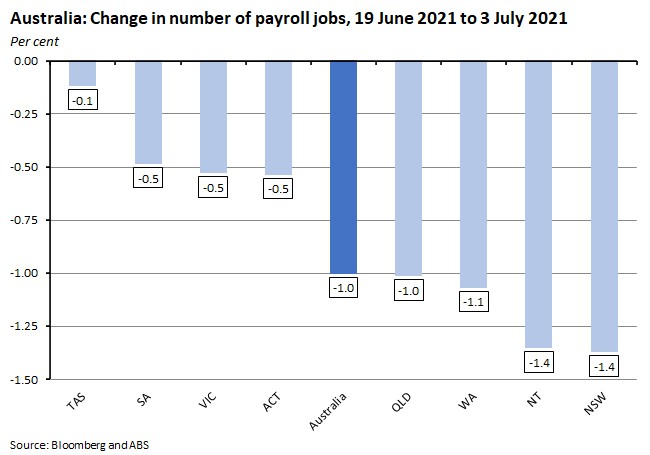

By state, job numbers fell in every geography over the past fortnight, with the declines ranging from 1.4 per cent in New South Wales and the Northern Territory to 0.1 per cent in Tasmania.

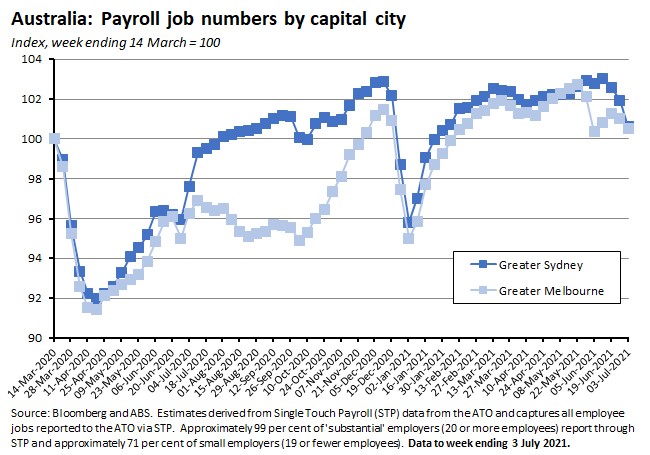

Across Australia’s capital cities, job numbers over the latest two weeks of data dropped by 1.9 per cent in Greater Sydney, by 1.3 per cent in Greater Brisbane and Greater Darwin, by 1.1 per cent in Greater Perth and by 0.8 per cent in Greater Melbourne.

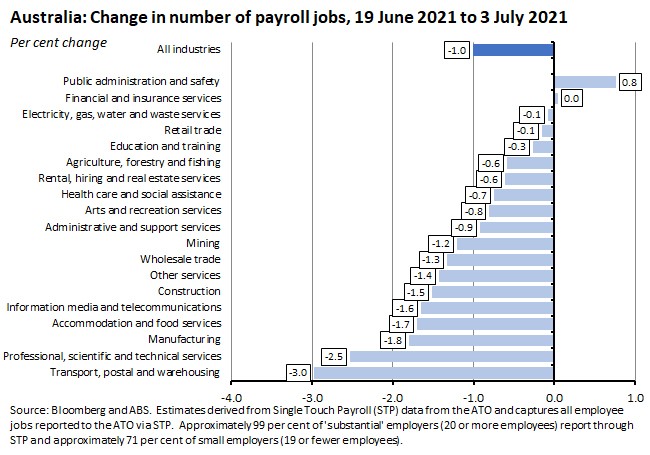

By industry, job numbers between the weeks ending 19 June and 3 July declined the most in transport, postal and warehousing (down three per cent), professional, scientific and technical services (down 2.5 per cent), manufacturing (down 1.8 per cent) and accommodation and food services (down 1.7 per cent). The only two industries where job numbers did not fall over this period were financial and insurance services (no change) and public administration and safety services (up 0.8 per cent).

Why it matters:

The ABS commented that the latest fortnight of payrolls data overlapped with increased COVID-19 restrictions in most states and territories, including lockdowns in four of the eight capital cities, as well as coinciding with school holidays in most states and territories. And while job numbers were down across every state and territory over the two weeks, the largest falls were suffered in those geographies where lockdowns were in place, with the biggest decline coming in Greater Sydney.

The pattern of job losses by industry likewise reflect the impact of public health restrictions. Accommodation and food services saw marked declines in job numbers across those states and territories with lockdowns in place, with falls ranging from four per cent in New South Wales to 0.1 per cent in the Northern Territory. In contrast, in Victoria the number of jobs in the industry rose 2.9 per cent as restrictions were eased.

And as noted above, tighter restrictions on mobility and increased state border restrictions also helped drive a national decline in the number of transport, postal and warehousing jobs.

What happened:

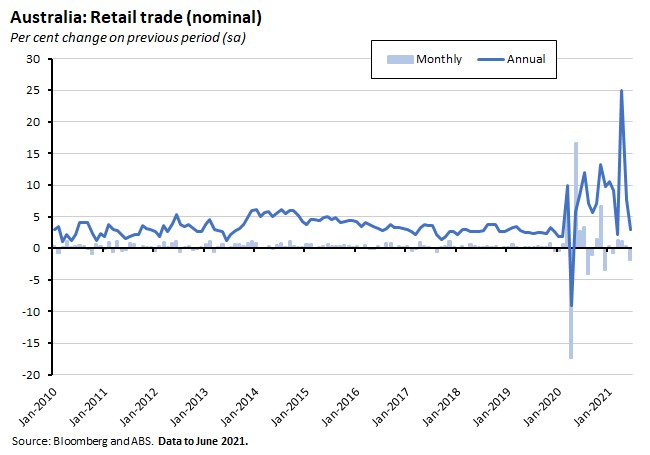

The ABS said that the preliminary estimate for retail turnover in June 2021 fell 1.8 per cent over the month (seasonally adjusted). That still left turnover 2.9 per cent higher than in June 2020.

By industry, food retailing (up 1.5 per cent) was the only industry to see turnover increase last month, with food retail in those states entering lockdown during the month driving the rise. All other industries saw sales fall as COVID-19 restrictions curtailed foot traffic and household movements. The ABS said that cafes, restaurants and takeaway food services, and clothing, footwear and personal accessory retailing suffered the largest monthly declines.

By state, Victoria (down 3.5 per cent), New South Wales (down two per cent) and Queensland (down 1.5 per cent) drove last month’s overall drop in turnover, with the first two states under stay-at-home orders for part of June. The ABS also noted that Victoria's fall was larger than the fall seen in May when it commenced Stage Four COVID-19 restrictions.

Why it matters:

The preliminary estimate of a 1.8 per cent drop in retail turnover in June was steeper than consensus expectations for a 0.7 per cent decline and was also the biggest month-on-month drop since last December. The ABS said the fall in turnover was due to the impact of coronavirus restrictions across multiple states, with Victoria under restrictions from the start of the month (gradually eased from the 11th of June), New South Wales issuing stay-at-home orders towards the end of the month, and with other states and territories also suffering from interrupted sales due to mini-lockdowns and reduced interstate mobility as border restrictions were tightened.

With the Sydney lockdown since extended and tightened, and with new lockdowns in Melbourne and South Australia now underway, retail turnover will be under further pressure this month.

Note that this was the final release of the preliminary release on retail trade, an innovation of the COVID-era, with the release schedule of the regular retail trade publication now having been revised. The ABS is discontinuing several of the publications it introduced during the pandemic and is also planning to introduce some new products. A short note on the changes to the ABS statistical work program released back in April this year provides some more detail.

What happened:

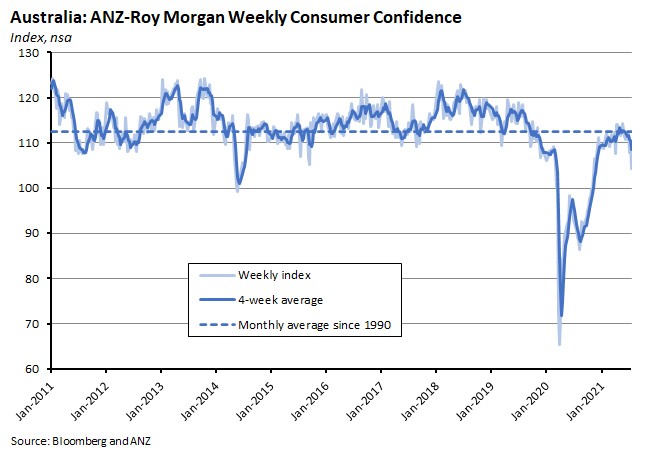

The ANZ Roy Morgan Consumer Confidence Index slumped 5.2 per cent last week.

Four out of the five subindices fell over the week: ‘time to buy a major household item’ dropped 10.5 per cent, ‘current economic conditions’ fell 7.9 per cent, ‘future economic conditions’ fell 4.5 per cent and ‘future financial conditions’ declined by 3.4 per cent. The only subindex to increase was ‘current financial conditions’ which rose 1.2 per cent.

Confidence plunged across the state capitals, with declines in Adelaide (down 9.5 per cent), Perth (down 8.2 per cent), Sydney (down 4.8 per cent) and Melbourne (down 3.7 per cent).

Weekly inflation expectations edged higher by 0.1 percentage points to 4.2 per cent.

Why it matters:

News of the extension and tightening of the Sydney lockdown and the introduction of Melbourne’s fifth lockdown helped deliver the largest drop in weekly consumer confidence seen since late March 2020 and took the index down to its lowest level since November 2020. The subindices for economic conditions and time to buy a major household item likewise reported their worst readings since November last year. Even so, the current level of the index still remains significantly above last year’s pandemic-lows.

What happened:

The RBA published the Minutes of the 6 July 2021 Monetary Policy Meeting of the RBA Board. That meeting took part during the initial phase of the Greater Sydney lockdown (before the subsequent extension and tightening of restrictions), with the minutes noting that:

‘Recent COVID-19 outbreaks in many parts of the country, and associated restrictions, were considered likely to weigh on household consumption through the middle of the year. However, as observed following earlier lockdowns, spending was expected to rebound when containment measures were eased, supported by highly accommodative policy settings, the strengthened balance sheets of many households and firms, and an increase in the pace of vaccinations.’

The 6 July meeting saw the RBA make decisions on yield curve control (YCC) and on asset purchases or quantitative easing (QE). On YCC, the minutes record that:

‘Members discussed the three-year yield target for government bonds. They noted that, when the three-year target was introduced in March 2020, the Board had judged that the probability of the cash rate increasing over the subsequent three years was extremely low. Since that time, the maturity date for the three-year bond had been extended from April 2023 to April 2024 and would soon move to November 2024. The Bank's central scenario implied that the conditions for an increase in the cash rate would not be met until 2024. Even so, the faster-than-expected recovery in economic conditions over the course of 2021 had widened the range of alternative plausible scenarios for the economic outlook and therefore the cash rate over the period to November 2024. In view of these considerations, the Board decided to retain the April 2024 bond as the target bond, rather than extend the horizon to the bond with a maturity date of November 2024.’

And on QE they state:

‘Members also discussed the future of the existing bond purchase program after the second $100 billion tranche of purchases is completed in early September…Given the high degree of uncertainty about the economic outlook, members agreed that there should be flexibility to increase or reduce weekly bond purchases in the future, as warranted by the state of the economy at the time, rather than a commitment to a specific rate of purchases over an extended period…Members then discussed the appropriate pace of future bond purchases. In particular, members considered whether to continue with the current pace of $5 billion per week or reduce purchases to $4 billion per week…Members acknowledged that an argument could be made to retain the pace of bond purchases at $5 billion per week, given that economic outcomes were still well short of the Bank's goals for inflation and employment. However, the economic outcomes had been materially better than earlier expected and the outlook had improved. In light of these improvements and the agreed decision-making framework, members decided to adjust the weekly purchases from $5 billion to $4 billion and agreed to review the rate of purchases at the November 2021 meeting.’

The discussion also covered the strong improvement in the labour market (the ABS data showing the most recent fall in the unemployment rate to just 4.9 per cent in June was released on 15 July, and so came after the RBA meeting), with members noting that some ‘industries where temporary visa holders had accounted for a sizeable share of employment in prior years, such as hospitality, had high levels of vacancies while employment remained below pre-pandemic levels. This suggested that the closure of Australia's international borders was contributing to the difficulties faced by some firms in attracting workers at prevailing wages.’

Near-record high participation rates, high levels of vacancies and other indicators of strong labour market demand are all consistent with a pickup in wage growth, but despite these developments the RBA has not changed its fundamental view that on wage dynamics, with the minutes reporting that although there were some ‘signs of wages growth picking up from the historically low levels recorded following the onset of the pandemic…In many cases, this reflected a recovery to the two–2.5 per cent average annual growth rate seen before the pandemic, rather than a shift to a materially faster pace.’ In addition, feedback from the RBA’s liaison program ‘suggested that firms were not expecting to make up for the period of wage freezes earlier in the pandemic’ while ‘the outlook for public sector wages, and rates of wages growth featuring in new enterprise bargaining agreements, suggested aggregate wage outcomes were unlikely to increase materially beyond pre-pandemic rates in coming quarters.’

Why it matters:

The minutes provided some additional context for the RBA’s decisions around YCC and QE as well as an interesting update on the central bank’s thinking around wage dynamics. But the economic assessments reported here have now been overshadowed by the subsequent expansion of the Greater Sydney lockdown in terms of both duration and range of restrictions as well as the spread of lockdowns beyond New South Wales to other states.

In this context, RBA-watchers have zeroed in on the discussion around QE and in particular on the point that:

‘Given the high degree of uncertainty about the economic outlook, members agreed that there should be flexibility to increase or reduce weekly bond purchases in the future, as warranted by the state of the economy at the time, rather than a commitment to a specific rate of purchases over an extended period.’

This is now being interpreted as implying that the changed economic conditions as a result of the intensification of lockdowns are likely to prompt the RBA to ramp up the rate of bond purchases in the future, delivering a rapid reversal of the July meeting’s decision to pare them back.

What happened:

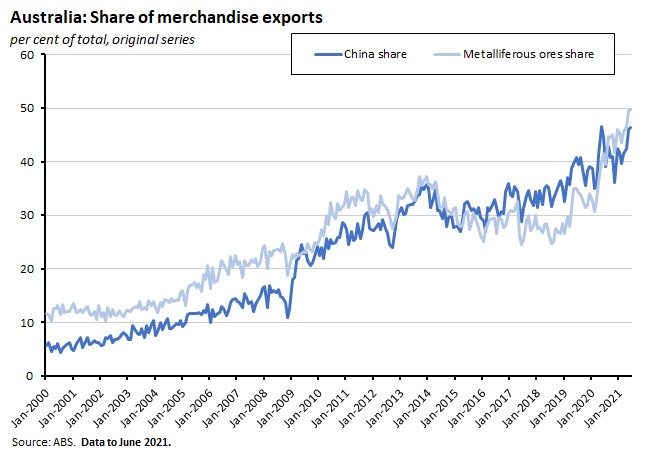

According to the ABS, preliminary estimates for merchandise trade in June 2021 show goods exports increasing by eight per cent or $2.9 billion over the month to $41.3 billion (original terms) while imports of goods also rose by eight per cent or $2.1 billion to $28 billion, giving a preliminary estimate for a June merchandise trade surplus of $13.3 billion.

Why it matters:

Even as the domestic economy suffers at the hands of the Delta variant of COVID-19, Australia’s international goods trade continues to break records. June this year looks to have delivered the largest merchandise trade surplus on record, a record high for goods exports after values pushed through the $40 billion mark for the first time, and a record high for exports of metalliferous ores (which hit $20.5 billion and accounted for almost half of total exports).

There was also another record high for iron ore exports, which hit $17.6 billion, and that in turn helped push up the value of goods exports to China to more than $19 billion. At 46.3 per cent, the share of goods exports to China also hit its second highest level on record, just below the 46.6 per cent peak share recorded in May last year.

Note that this is another of the COVID-ear ABS publications marking its final release this month, as discussed above.

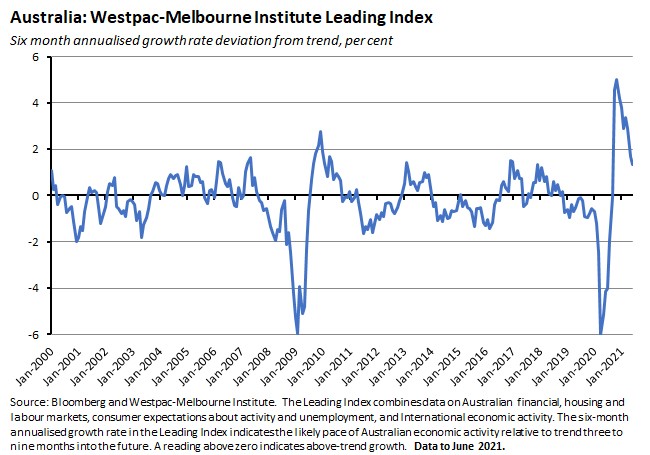

What happened:

The six-month annualised growth rate in the Westpac-Melbourne Institute Leading index (pdf) – which indicates the likely pace of Australian economic activity relative to trend three to nine months into the future – slowed from 1.7 per cent in May to 1.3 per cent in June.

Why it matters:

Despite the slowdown in growth indicated by the index over the past six months, growth remains in positive territory and continues to indicate an outlook of above-trend growth. Westpac commented that although recent lockdown measures have already had an impact on some index components (Victoria’s June lockdown hit total hours worked and consumer sentiment has weakened across both June and July), the full effect has yet to be felt, with the consequences of the further tightening of NSW restrictions and the introduction of a new lockdown in Victoria still to manifest in the index data.

What happened:

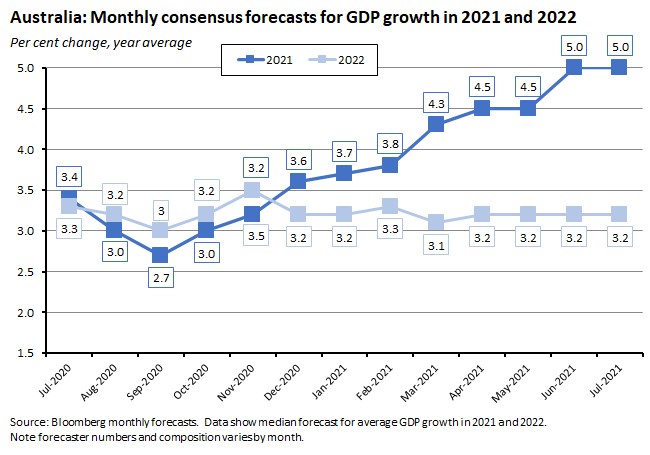

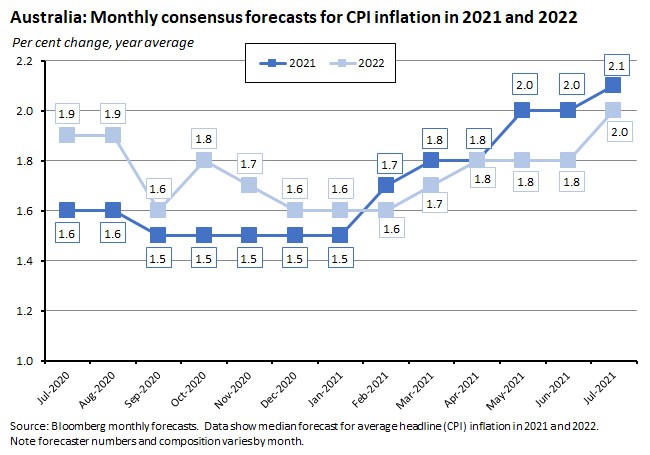

Bloomberg’s July roundup of economic forecasts showed no change from the June survey in the median forecast for GDP growth this year or next.

Forecasters have, however, become even more optimistic on the labour market, with the median forecast for the average unemployment rate for 2021 revised down from 5.4 per cent in June to 5.2 per cent this month. Forecast unemployment for next year has also edged lower from last month, dropping to 4.6 per cent from 4.7 per cent.

At the same time, consensus expectations for inflation have increased slightly, with the median forecast for the annual rate of increase in the CPI this year rising from two per cent in June to 2.1 per cent in July, while for next year the revision is from 1.8 per cent to two per cent.

Why it matters:

Despite recent COVID-19 developments, forecasts for Australia’s economic outlook remain relatively upbeat. Importantly, however, it’s likely that the roundup of July projections will not have fully considered the impact of extended lockdowns on growth projections for this year, and hence August’s numbers are likely to prove a superior test of their implications for growth expectations.

What I’ve been reading . . .

- Satyajit Das in the AFR is pretty scathing about what he sees as Australia’s economic weaknesses: an over-reliance on the free movement of people to drive growth and fill skills gaps; vulnerability to disruptions to global supply chains; too much dependence on ‘houses and holes’; a reluctance to try new policy solutions; and significant political deficiencies. And yet, for all of Das’s criticisms, it’s also that case that at least until recently, Australia had managed to deliver close to the best economic outcome to the COVID crisis of any OECD economy. Unfortunately, the slow vaccine rollout is now calling that initial success into question.

- Adam Triggs offers his take on the debate over the relationship between migration and wages. My own view here is that the story of the international impact on the labour market in general and on wages in particular is probably best seen not in terms of the migration debate but instead in terms of the impact of global competition more generally. It also seems likely that closed borders are one of the explanations for some recent labour market outcomes, including the rapid decline in the unemployment rate.

- Two new housing market reports from CoreLogic. The first is the June 2021 rental review, which shows that national rental rates are now 6.6 per cent higher over the year, marking the highest annual growth in dwelling rents since January 2009. Second, a review of the housing market during pandemic lockdowns finds that auction results across Sydney and Melbourne have tended to remain resilient in lockdowns, that although transaction activity typically slows markedly during lockdowns that is then followed by a ‘catch up’ phase in home purchases as restrictions are eased, and that the recent experience is that property values overall have remained resilient through lockdowns and then seen strong growth as social distancing restrictions eased.

- Some proposals to improve Australia’s record on Research and Development.

- A new Grattan report on policies to reduce carbon emissions from the transport sector. It starts from the propositions that (a) the transport sector is responsible for nearly 20 per cent of Australia’s emissions, and (b) more than 60 per cent of transport emissions are from light vehicles to argue that the ‘best way to cut transport emissions is to supercharge the switch to electric cars.’

- The Productivity Commission’s Trade and Assistance Review 2019-20 notes that while the pandemic has triggered ‘unprecedented industry assistance’, the bulk of that support was actually provided in 2020-21 and therefore is not captured in the 2019-20 statistics. Gross industry and sectoral assistance totalled about $13.7 billion in 2019-20, including $1.8 billion in the form of tariffs, $5.1 billion in budgetary outlays and $6.7 billion in tax concessions. Net industry assistance, which adjusts for the costs of tariffs to other sectors, was about $12.1 billion, implying an increase of about $0.4 billion on 2018-19 levels of assistance. Services received the most government support in absolute terms but only a small amount relative to their share in the economy, while primary production (mostly agriculture) and manufacturing each received a disproportionately large share of support: 20 per cent and 29 per cent of all direct assistance, despite only accounting for two per cent and six per cent of gross value added, respectively. Overall, however, and despite the increase, the Commission judges that effective rates of assistance (ERAs) remain at historic lows for most industries. For the first time, the Review also considered foreign investment into Australia.

- Deloitte on the value of tourism to Australia.

- New data from CBA on household spending intentions.

- ASPI has some suggestions on how Australian policy should respond to the global rise of ransomware. Recommendations include ‘greater clarity about the legality of ransomware payments, increased transparency when attacks do occur, the adoption of a mandatory reporting regime, expanding the official alert system of the Australian Cyber Security Centre (ACSC), focused education programs to improve the public’s and the business community’s understanding and, finally, incentivising cybersecurity uplift measures through tax, procurement and subsidy measures.’

- Bloomberg explains why business brands have never been easier to destroy.

- The WSJ says the Olympics are turning into a US$20 billion bust for Japan.

- This BIS Bulletin piece examines global reflation and argues that concerns about a prolonged increase in inflation are overstated, since ‘the pickup in inflation can be ascribed largely to base effects, increases in the prices of a small number of pandemic-affected items and higher energy prices. A common thread through these causes is that their effect on inflation is likely to be temporary.’ As long as wage growth remains contained and inflation expectations anchored, the argument runs, medium-term inflation risks are limited. But the piece does hedge its bets somewhat, also conceding that ‘a more persistent pickup in inflation cannot be excluded. Intensifying supply-side disruptions, especially related to global supply chains, could lead to further price increases. COVID- and post-COVID adjustments, against the background of social tensions, may lead to higher wages or higher fiscal deficits which may in turn put pressure on inflation.’

- Related, Ken Rogoff in the FT says don’t stress about (US) inflation.

- For a different perspective, Otmar Issing sounds more worried about rising prices.

- And this VoxEU piece considers the evidence on the long-run effects of pandemics on inflation. It reports that a review of historical European data going back to the 14th century suggests that ‘following a pandemic event, trend inflation falls steadily below its initial level for nearly a decade.’ The authors do suggest that this time could be different, however. The unprecedented scale of the fiscal and monetary policy response to COVID-19, the rapid arrival of effective vaccines, the resilience of many busines sectors, pressures stemming from pandemic-related supply disruptions and rising transport and packaging costs could all lead to a divergent outcome.

- The NBER Business Cycle Dating Committee has announced that the US COVID-19 recession lasted just two months, finishing in April 2020. That makes it the shortest US recession on record – a record previously held by a six-month long recession in 1980.

- The July Supplement to the Asian Development Outlook provides updated forecasts for developing Asia, with the region now expected to grow at 7.2 per cent this year, down slightly from the April 2021 forecast of 7.3 per cent growth. The slight downgrade reflects the drag from new COVID-19 outbreaks.

- The IMF on the resilience of private sector balance sheets in Europe despite a dramatic collapse in output, largely thanks to the public sector taking the strain.

- The Economist’s Free Exchange column examines the strengths and shortcomings of the EU’s proposed carbon border adjustment mechanism (CBAM).

- Also from the Economist, a briefing on Biden’s China doctrine.

- Noah Smith looks at the dramatic economic divergence between Haiti and the Dominican Republic: in 1960 the two economies had roughly similar standards of living while now the Dominican Republic is perhaps eight times richer than Haiti. That’s a divergence story Smith reckons that is only surpassed by the tale of North and South Korea. But what does it tell us about development?

- The WEF has released a new white paper on navigating global value chain disruption in an age of uncertainty.

- Interesting FT opinion piece from Ruchir Sharma that pushes back against the consensus view of a global boom by arguing that there are risks that the two key engines of the global economy (the US and China) may be faltering.

- A couple of podcasts to finish with, both of which are a bit different from the usual economic focus. Ezra Klein talks to Annie Murphy Paul about how to think about thinking (including some implications for the modern workplace) while Econtalk digs into the Comfort Crisis.

Latest news

Already a member?

Login to view this content