As Australia's economy continues to grapple with the impact of COVID-19, the government's outlook for debt and deficits will require a disciplined response, writes AICD chief economist Mark Thirlwell.

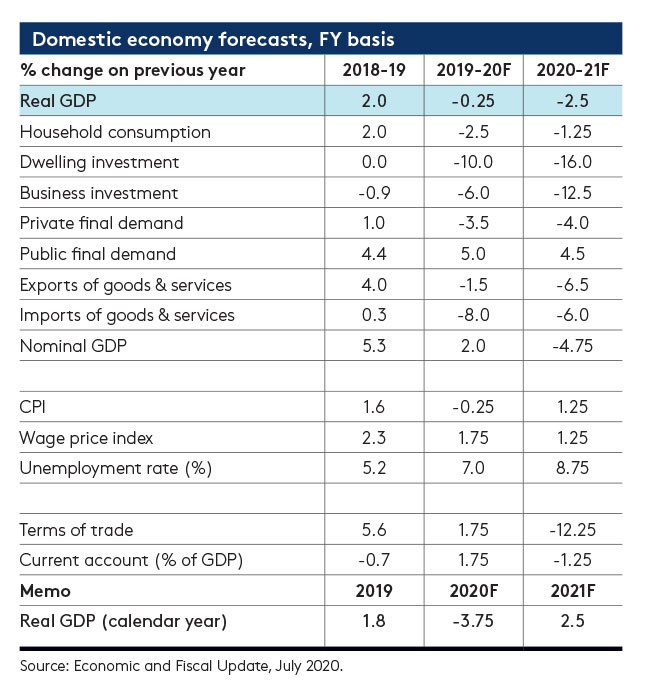

July’s Economic and Fiscal Update provided Canberra’s views on the post-COVID economic trajectory as well as estimates of the budgetary cost of the coronavirus. Set against the backdrop of Victoria’s new wave of cases, both sets of numbers made for a sobering read. In terms of the economic story, Treasury thinks real GDP will contract by 3.75 per cent in calendar year 2020, marking the largest annual decline in the post-World War II era, while in 2020–21 the decline is expected to be 2.5 per cent.

Nearly all the economy’s growth drivers are forecast to go backwards in 2020–21, with household consumption falling 1.25 per cent, dwelling investment 16 per cent and business investment 12.5 per cent. Net exports are also assumed to subtract from overall growth, with exports of services suffering a 32.5 per cent collapse. Although population growth is expected to remain positive, it is still predicted to drop to 0.6 per cent in what would be the weakest result since 1916–17.

The update predicts the official unemployment rate will continue to rise this year, peaking at around 9.25 per cent in the December quarter and only gradually declining over the first half of 2021, to be at 8.75 per cent by June next year. Moreover, this underestimates the true state of labour market distress — the Treasurer puts the current “effective” unemployment rate at above 11 per cent vs the official rate of 7.4 per cent — although the size of misdiagnosis should fall over time.

Treasury then expects the economy to recover next year, predicting growth of 2.5 per cent in calendar year 2021. But that modest expansion is critically dependent on the future trajectory of the coronavirus and the public health response allowing for continued easing in economic restrictions, as well as a reduction in economic and health-related uncertainty and a pickup in global economic activity. The update is appropriately explicit about the vulnerability of these projections to anything that could undermine its relatively optimistic assumptions about the pace of the economic emergence from lockdown that underpin what it describes as a relatively fast forecast recovery by historical standards.

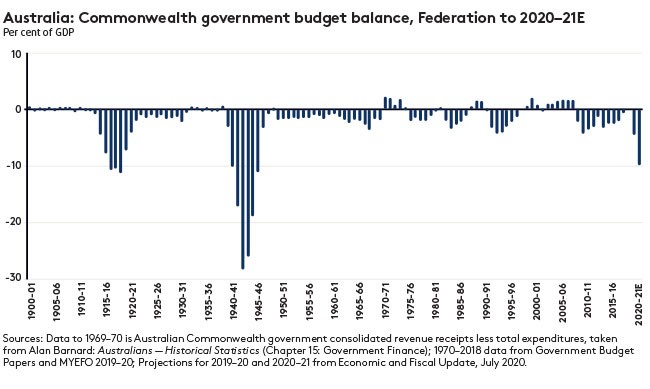

The update’s predicted post-WWII record contraction in GDP is matched by record forecast increases in debt and deficits. The pandemic has sent Australia’s fiscal accounts deep into the red, banishing the midyear economic and fiscal outlook (MYEFO) hopes of a “back in black” year. Instead, 2019–20 will have delivered an $85.8b deficit (4.3 per cent of GDP) while in 2020–21 the deficit is expected to blow out to $184.5b (9.7 per cent of GDP).

The transformation in the budget bottom line is the joint outcome of the so-called “automatic stabilisers” (falls in receipts as a result of lower economic activity and a parallel rise in automatic payments such as unemployment benefits) plus the impact of policy responses to COVID-19 (such as the JobKeeper and Boosting Cash Flow for Employers programs). The former accounts for roughly 38 per cent of the deterioration in the 2020–21 budget balance relative to MYEFO, policy measures for 62 per cent. From 1970–71 until now, the share of government payments in GDP has never been above 28 per cent. But in 2020–21, their share is expected to reach nearly 34 per cent due to the extraordinary measures Canberra has taken to protect the economy, not least JobKeeper, which has supported around 3.5 million workers — an incredible 30 per cent of the pre-COVID private sector workforce.

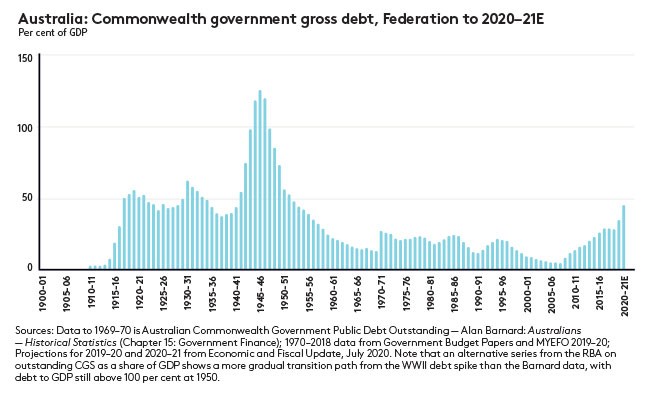

Big overshoots on the deficit imply big overshoots for government debt. Net debt is expected to have hit $488.2b (24.6 per cent of GDP) on 30 June this year and to increase to $677.1b (35.7 per cent of GDP) on 30 June 2021 — approaching double the MYEFO projections for that year. Indeed, the scale of debt and deficits predicted by the 2020–21 update is unprecedented in modern Australian economic history — we need to go back to WWII to find a larger explosion of red ink.

Still, that scale of fiscal response has been warranted by the sheer size of the economic challenge. Relative to no policy support, Treasury estimates Canberra’s budgetary largesse has increased the level of real GDP by around 0.75 per cent in 2019–20 and will bump it up by around 4.25 per cent in 2020–21. Likewise, fiscal measures are estimated to have lowered the peak of the measured unemployment rate by around five percentage points — about 700,000 jobs. The public health and economic wars against COVID-19 have to be fought. But like most wars, they come at a substantial fiscal cost.

Latest news

Already a member?

Login to view this content