The anticipation of state re-openings, backed by rising vaccination rates, saw the NAB monthly measure of business confidence jump 19 points in September, propelled by a 42 point surge in New South Wales and a 16 point increase in Victoria.

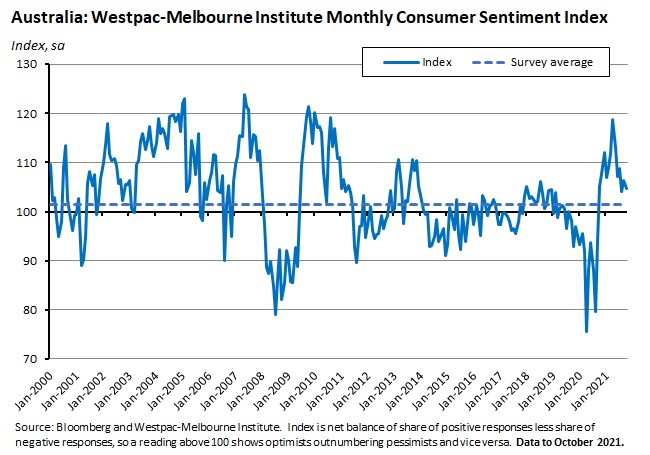

But while businesses judged that their future was looking brighter, current circumstances felt tougher: NAB’s measure of business conditions slumped by nine points last month, although that still left the index overall in positive territory. Meanwhile, consumer confidence retreated in October according to the latest release of the Westpac-Melbourne Institute Index of Consumer Sentiment, which dropped by 1.5 per cent. Even so, optimists continue to outnumber pessimists and sentiment remains quite high relative to the series average.

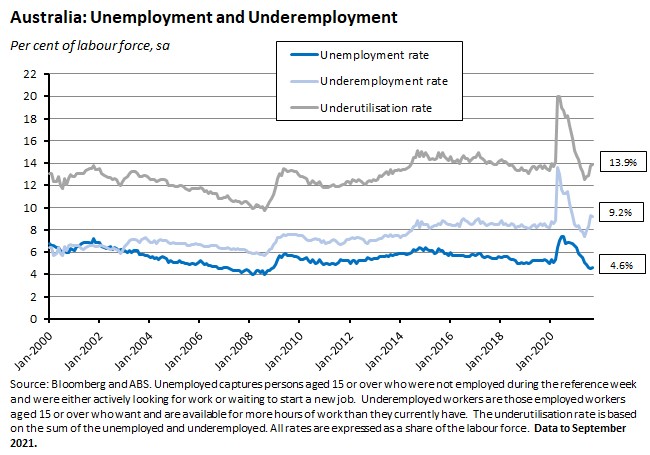

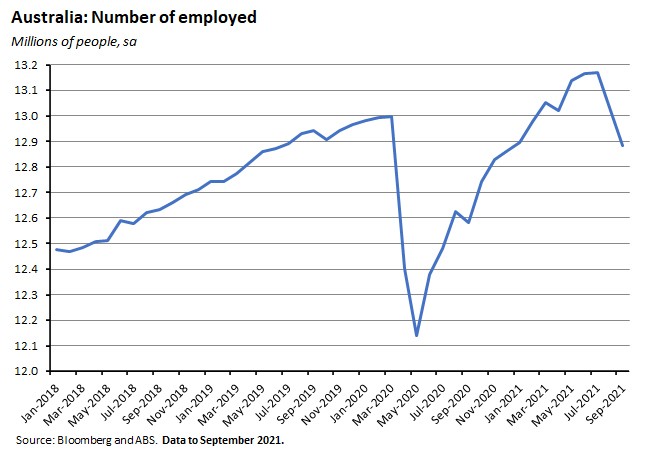

The other big Australian data release this week was September’s labour market report, which showed that employment has now fallen back below its March 2020 level, with large employment falls in Victoria, New South Wales and the ACT. There was also a marginal increase in the unemployment rate to 4.6 per cent – the first increase since September 2020 – although that number continues to paint a highly imperfect picture of labour market conditions as lockdowns continue to see a significant number of Australians exit the labour market altogether. More positively, hours worked actually increased last month in what might be an early sign of a labour market turnaround.

This week also brought the release of the IMF’s latest forecasts for the world economy. The Fund tweaked the headline number for growth this year with a small 0.1 percentage point downgrade but the real interest was in the accompanying commentary, which suggested that alongside its more longstanding concerns around the global distribution of vaccines, the IMF is increasingly worried about supply-side disruptions and rising inflationary pressures.

In this week’s Dismal Science podcast we talk about the implications of the latest US jobs and inflation data, the recent international agreement on setting a global minimum tax rate for multinational enterprises, the award of the economics ‘Nobel prize’, and the fallout at the IMF from the now-defunct World Bank Doing Business report.

This week’s readings include more IMF analysis, the latest world energy outlook from the IEA, more on the economics ‘Nobel’, the new order for world trade, and the death and birth of technological revolutions.

Listen and subscribe to Dismal Science podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

The ABS said that Australia’s unemployment rate increased to 4.6 per cent in September 2021 from 4.5 per cent in August (seasonally adjusted). The underemployment rate fell to 9.2 per cent from 9.3 per cent over the same period, and the underutilisation rate edged up by less than 0.1 percentage point to 13.9 per cent.

Employment fell by 138,000 people (1.1 per cent) to 12.9 million in September, as although full-time employment rose by 26,700 people over the month, part-time employment fell by a considerably larger 164,700. As a result, the part-time share of employment fell to 30.3 per cent.

In contrast to the fall in employment, monthly hours worked in all jobs rose by 0.9 per cent over the month in September.

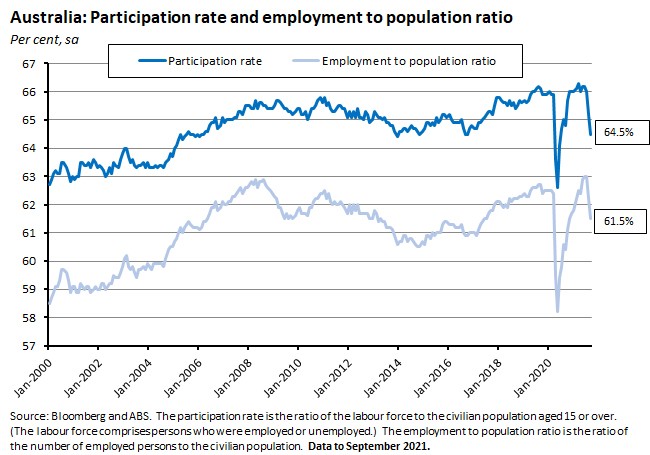

More Australians exited the labour force last month: the participation rate fell by 0.7 percentage points to 64.5 per cent. The employment to population ratio also fell by 0.7 percentage points to 61.5 per cent.

By state and territory, employment fell sharply in Victoria (down 3.5 per cent) and the ACT (down 3.2 per cent) and declined more modestly in New South Wales (down 0.6 per cent) between August and September. Queensland, however, enjoyed a 1.2 per cent gain in jobs.

The unemployment rate rose in Victoria (up 0.7 percentage points) and the ACT (up 0.5 percentage points) and both Victoria and the ACT also saw substantial falls in the participation rate (down 1.9 percentage points in each case) and the employment to population ratio (both down 2.2 percentage points).

Why it matters:

The fall in total employment of 138,000 last month was larger than the median forecast of a 120,000 drop and saw employment in the Australian economy slip to be 0.9 per cent lower than it was in March 2020. Lockdowns in New South Wales, Victoria and the ACT all weighed on the labour market again in September, with employment down by 123,000 in Victoria and 25,000 in New South Wales. There was also a big percentage decline in the ACT.

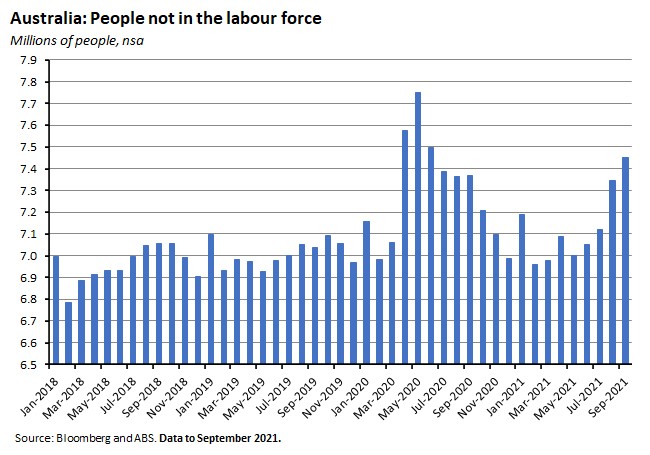

After having fallen for 10 consecutive months, Australia’s unemployment rate has now increased for the first time since September 2020. Once again, however, it’s important to note that the current level of the unemployment rate remains a poor indicator of the true state of the labour market during lockdowns. As we’ve explained before, in large part that’s because one impact of public health restrictions is that many people exit the labour market, and indeed September saw a third consecutive decline in the participation rate, further swelling the number of Australians not in the workforce. The number of the latter is now the highest reported since June 2020.

For a more detailed review of at this week’s labour market results, including charts showing results by state and territory, readers can take a look at our updated labour market chart pack.

What happened:

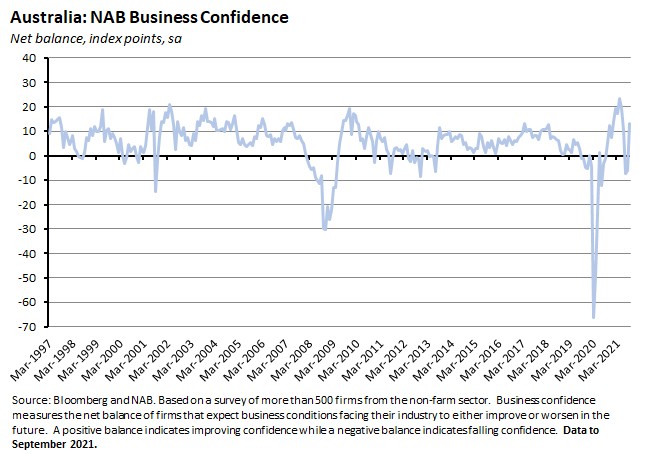

The NAB Monthly Business Survey: September 2021 reported that business confidence rose 19 points to a reading of +13 index points last month.

The surge in confidence reflected an extremely strong gain for New South Wales (jumping 42 points to +27) and a good result for Victoria (up 16 points to +5) although other states saw a modest decline. By industry, confidence rose strongly in wholesale (up 28 points), recreation and personal services (up 26 points) and construction (up 23 points).

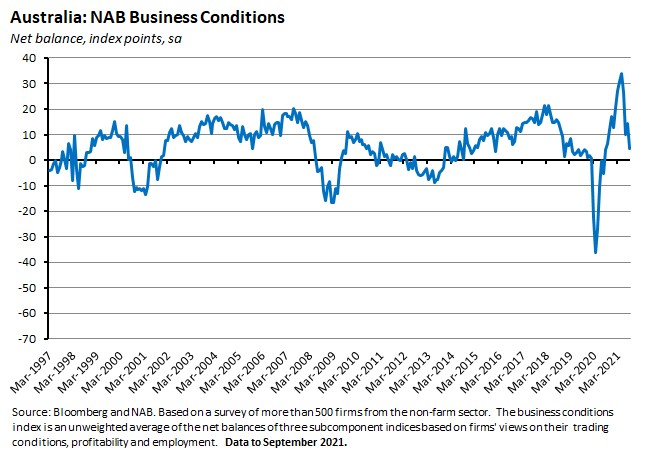

Moving in the opposite direction, current business conditions fell nine points to an index level of +5 points in September.

All three subcomponents of busines conditions fell over the month, with declines in trading (down 10 points), profitability (down 13 points) and employability (down eight points). All three components remain in positive territory, although employment (at +1) and profitability (at +2) are now at relatively low levels.

Business conditions fell across all states in September, with particularly large falls in New South Wales (down 16 points), South Australia (down 13 points), Victoria (down 11 points) and Tasmania (down nine points). NAB also reported that conditions fell across all industries with the exception of transport and utilities (which saw a 27-point rebound) and retail (which edged up by one point). The biggest fall came in mining (where conditions slumped by 52 points from record highs) and in recreation and personal services (down 26 points).

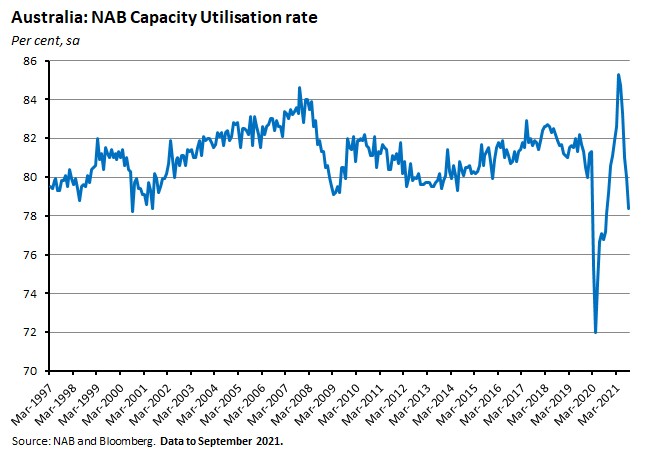

Capacity utilisation also fell sharply over the month, dropping from 80.1 per cent in August to 78.4 per cent in September, taking the utilisation rate to almost seven percentage points below its pre-lockdown peak. Forward orders also declined, slipping back into negative territory after having turned positive in August.

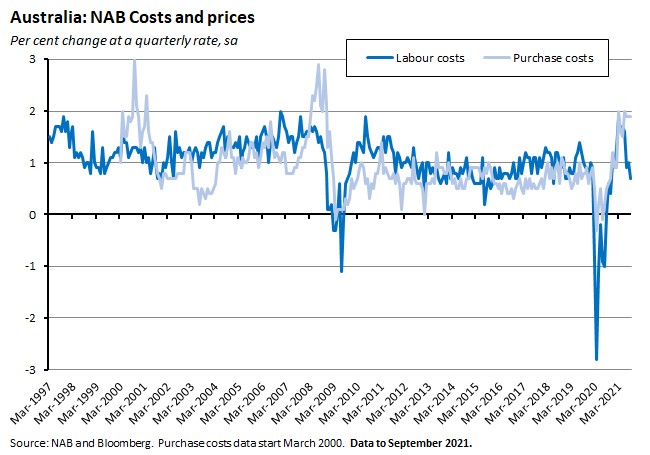

Finally, in terms of inflationary pressures, growth in purchase costs again edged higher over the month but growth in labour costs fell back quite significantly relative to August. The rate of final product price inflation was unchanged from August’s reading.

Why it matters:

Business confidence and business conditions sent opposing signals in September. The big rebound in confidence – powered by New South Wales and Victoria – suggests that last month businesses were looking to the re-opening plans of those two states and as a result feeling considerably more optimistic about future prospects than they had been in August. Rapid progress with the vaccine rollout is also likely to have been a contributory factor to that improvement in sentiment. At the same time, however, actual business conditions weakened markedly over the month. Although the business conditions index remains in positive territory, public health restrictions appear to be taking a mounting toll – a trend also visible in the declining rate of capacity utilisation.

What happened:

The Westpac-Melbourne Institute Index of Consumer Sentiment (pdf) fell by 1.5 per cent in October.

In terms of the five subcomponents, there were monthly declines for ‘economic conditions next 12 months’ (down 1.7 per cent), ‘family finances vs a year ago’ (down 1.3 per cent) and ‘economic conditions next five years’ (down 5.6 per cent). ‘Family finances next 12 months’ edged higher by 0.5 per cent and ‘time to buy a major household item’ rose 0.9 per cent.

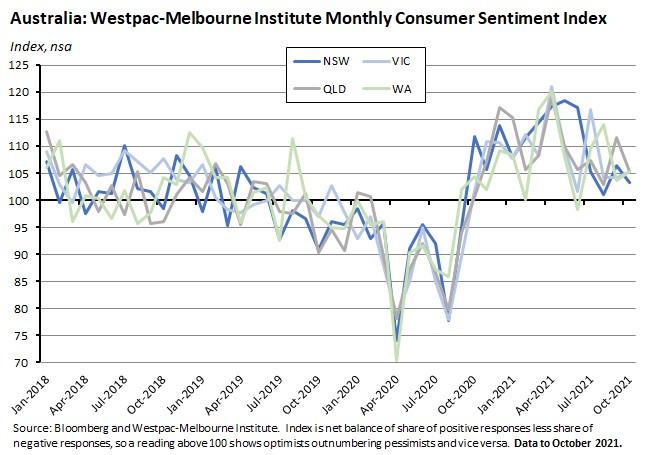

Westpac noted that there was little difference in confidence readings across states, with index readings of 103.4 in New South Wales, 105.4 in Victoria and Western Australia and 105.3 in Queensland.

It also noted that there were significant differences between metro and regional areas in New South Wales and Victoria, with sentiment increasing over the month in Sydney (up 1.2 per cent) and Melbourne (up 3.9 per cent) but down in regional New South Wales (a 10.6 per cent drop) and regional Victoria (down 8.2 per cent).

Confidence between those intending to get vaccinated (with an index reading of 122) and those who do not intend to do so (an index reading of just 84.8) has diverged further.

Households are feeling more optimistic about the labour market, with an 11.1 percent drop in October in the Index of Unemployment Expectations, signalling a rise in the share of respondents expecting unemployment to fall over the coming year.

The ‘time to buy a dwelling’ index fell 13.8 per cent in October while the Index of House Price Expectations remained close to eight-year highs, edging down only slightly (one per cent) from September’s reading.

Why it matters:

After having risen by 2.1 per cent last month, consumer sentiment retreated again in October. Still, at an index level of 104.6 sentiment remained comfortably in positive territory as optimists continued to outnumber pessimists. Sentiment also remains elevated relative to the series average. All of which is broadly consistent with the idea that the ongoing vaccination rollout, plus the prospects of state re-openings, are together helping sustain household as well as business confidence. That also seems to apply in the case of views on the labour market given this month’s sharp decline in unemployment expectations. In the case of New South Wales, for example, the state unemployment index dropped to a 16-year low in October.

Finally, there was more evidence that the rapid run-up in house prices is denting affordability: the ‘time to buy a dwelling’ index is now down 37 per cent from the peak it reached in November 2020.

. . . and what I’ve been following in the global economy

What happened:

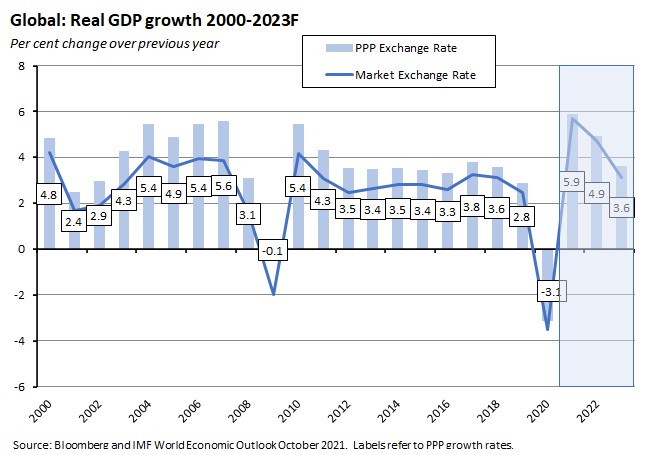

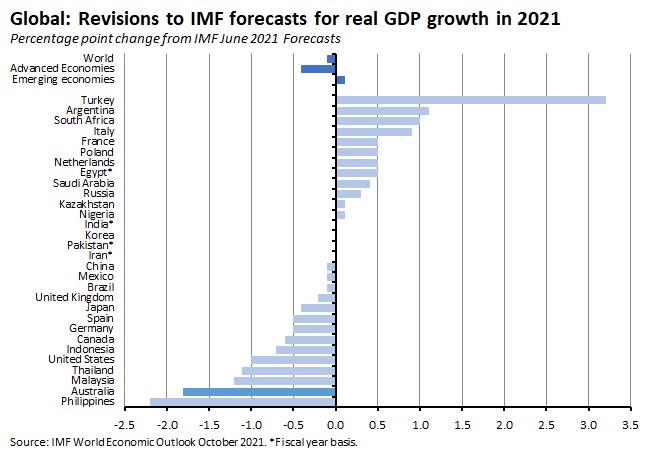

The IMF published the October 2021 World Economic Outlook (WEO). The Fund now thinks that the global economy will grow 5.9 per cent in 2021 and 4.9 per cent in 2022. The forecast for this year represents a modest 0.1 percentage point downgrade from the IMF’s July projections while the forecast for 2022 was left unchanged.

The IMF reckons that Australia will grow 3.5 per cent this year and 4.1 per cent in 2022. Back in the July, it was expecting that Australian growth would run at 5.3 per cent this year and three per cent in 2022 so the Delta variant and state lockdowns have led to a reshuffling of growth, with a 1.7 percentage point downgrade for 2021 followed by a 1.1 percentage upgrade in 2022. Australia suffered one of the larger downgrades seen in this forecast round.

Digging into the details for this year for the rest of the world economy, the Fund has downgraded its growth expectations for advanced economies by 0.4 percentage points, with sizeable cuts for the United States (down one percentage point), Canada (down 0.6 percentage points), Germany and Spain (both down 0.5 percentage points), and Japan (down 0.4 percentage points). Growth projections for emerging and developing economies have been upgraded by 0.1 percentage points, with increases for nearly every region including emerging and developing Europe (up one percentage point), Latin America and the Caribbean (up 0.5 percentage points), Sub-Saharan Africa (up 0.3 percentage points) and the Middle East and Central Asia (up 0.1 percentage points). The exception is emerging and developing Asia, where the Fund has cut its forecast 0.3 percentage points, with downgrades for China (0.1 percentage point) and the ASEAN-5 (1.4 percentage points).

Downgrades to growth in advanced economies tend to reflect supply disruptions and shortages although in some cases (Japan, Australia) the impact of higher COVID case numbers were also at work. Emerging and developing Asia similarly suffered from pandemic-related disruptions to growth while in other regions stronger commodity prices have boosted prospects for commodity exporters in Latin America, the Middle East and Sub-Saharan Africa.

Why it matters:

As usual, the latest WEO provides a good overview of the official take on the state of the global economy. Key elements of that official view include:

- The resurgence of the pandemic means that access to vaccines remains the main driver of fault lines in the global recovery: countries where vaccination strategies are advanced can look forward to what the IMF calls ‘further normalisation’ over the remainder of this year (likely to apply to almost all advanced economies and some emerging markets) while countries where vaccination roll outs are lagging will struggle with the ‘adverse health and economic impacts from resurgent infections.’

- The IMF sees one key downside risk to its baseline forecast as the emergence of more transmissible and deadlier COVID variants which would prolong the pandemic and trigger further disruption to economic activity.

- The IMF also assumes that financial conditions remain broadly supportive (healthy share markets, tight credit spreads and stable capital flows) over the forecast period.That leaves conditions vulnerable to any reassessment of policy stances by the world’s major central banks - particularly in response to changes in inflation prospects. Here, the Fund’s baseline view is still relatively sanguine: that the rising inflation currently visible in the world economy to a large extent reflects ‘a combination of pandemic-induced supply-demand mismatches, rising commodity prices, and policy related developments . . . rather than a sharp drop-off in spare capacity.’ Hence the WEO baseline forecast has inflation returning to pre-pandemic levels in 2022 in most of the world’s economies once those demand-supply imbalances have been resolved. In the meantime, however, the Fund does see some pass through from higher food and energy prices sustaining higher inflation rates.

- The Fund’s relative optimism that inflation will turn run permanently higher reflects three judgements: (1) that labour market slack remains relatively large with employment rates still typically below pre-COVID levels; (2) that inflation expectations are still well-anchored in large advanced economies; and (3) that the structural factors that previously lowered the sensitivity of inflation to labour market slack such as increasing automation continue to operate and in some cases are even intensifying.

- However, the WEO also cautions that the outlook for inflation is ‘highly uncertain.’ Hence another key downside risk to the IMF forecasts is that ‘more persistent supply-demand mismatches, price pressures, and faster-than-anticipated monetary policy normalisation’, produce tighter global financial conditions and the risk of a rapid re-pricing of financial assets.

- A related risk is that, in a context where many asset valuations are already stretched, investor sentiment looks vulnerable to sudden shifts in response to any negative shocks.

- Other downside risks include a smaller-than-expected US fiscal package, greater social unrest, more adverse climate shocks, cyberattacks, and intensified trade and technology tensions between the United States and China.

- While the Fund thinks risks to its forecasts are skewed to the downside, it does identify two potential upside risks as well. First, the possibility of faster vaccine production and distribution than is assumed in the baseline projections and second, the chances of a productivity growth spurt due to the impact of pandemic-induced changes in automation, workplace arrangements and changes to production, distribution and payment systems.

- The WEO also suggests that at the global level policymakers could increase the likelihood of positive economic outcomes by seeking to accelerate the global deployment of vaccines, by a more effective pursuit of policies designed to mitigate and adapt to climate change, by easing the financial constraints facing struggling economies, by defusing trade tensions and by finalising the agreement on a global minimum for corporate tax rates.

Much of this is familiar from the IMF’s previous assessments of the world economy earlier this year and the accompanying list of risks is little changed. What has shifted is the Fund’s relative emphasis on the threat posed by supply-side disruptions and inflationary pressures, with the WEO text warning that while central banks can ‘look through transitory inflationary pressures and avoid tightening until there is more clarity on underlying prices dynamics’, nevertheless ‘they should be prepared to act quickly if the recovery strengthens faster than expected…Early pre-emptive action will be required where there is a tangible risk of rising inflation expectations and more persistent price increases.’ Moreover, the WEO goes on to note that while ‘central banks with dual mandates in economies confronting rising inflation against the backdrop of still-subdued employment rates and labour market slack face particularly difficult choices’, any choice might now have to be resolved in favour of tightening monetary policy to get ahead of price pressures ‘even if that means the employment recovery is delayed.’

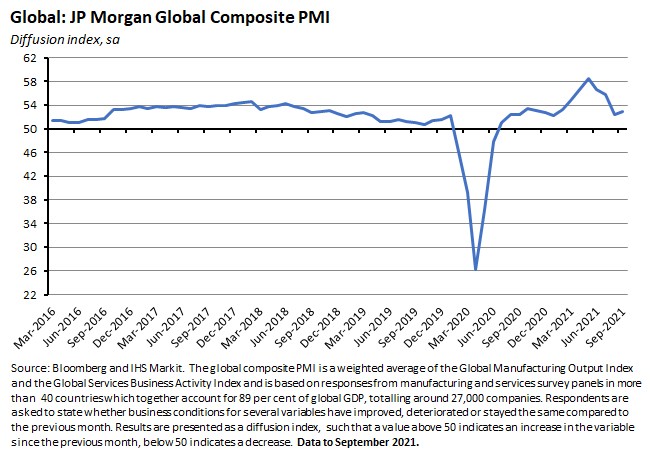

What happened:

According to data released last week, the J P Morgan Global Composite PMI (pdf) rose from 52.5 in August to 53 in September.

Relative to the August reading, momentum rose for output, new business, future output, outstanding business, input price and output prices but slowed for new export business and employment.

Survey respondents continued to report that supply chain issues remained a challenge, with shortages and delays for raw materials also feeding through into higher prices.

Why it matters:

After falling to a seven-month low in August, the Global Composite PMI rose slightly in September to deliver the first rise in the PMI in four months. It also saw the Index record its 15th consecutive month in positive territory, indicating that despite all of the disruption triggered by Delta, activity across the global economy has now been rising for well over a year.

Still, the September PMI does show that Delta continues to impact the global economy, particularly through the supply channel. Survey provider IHS Markit has noted that the latest results show that average suppliers’ delivery times ‘continued to lengthen globally at a rate unprecedented in almost a quarter century of survey data, exceeded only by the delays seen in the prior three months,’ going on to add that this is underscoring the ‘unparalleled supply chain delays being recorded in recent months as a result of the pandemic.’ Input price inflation is now running at the second highest rate recorded in 13 years, just a little below the peak reached in May of this year. There are also signs that the price increases that have been a feature of the manufacturing data are increasingly feeding through into services.

What I’ve been reading . . .

- The RBA’s October 2021 Financial Stability Review.

- A speech from RBA Deputy Governor Guy Debelle on Climate Risks and the Australian Financial System.

- Also from the RBA, a couple of handy snapshots of the Composition of the Australian economy and Key economic indicators.

- The BCA on achieving a net-zero economy.

- Grattan on practical policies to offset carbon emissions, the latest report in Grattan’s Towards net zero series. Podcast version.

- Treasury offers some insights from the first six months of JobKeeper.

- Peter Martin is another sceptic when it comes to the current housing affordability inquiry.

- The IEA’s World Energy Outlook 2021 says that although a new global energy economy is now emerging, the transformation still has a long way to go. In particular, the ‘rapid but uneven economic recovery from last year’s COVID-induced recession is putting major strains on parts of today’s energy system, sparking sharp price rises in natural gas, coal and electricity markets. For all the advances being made by renewables and electric mobility, 2021 is seeing a large rebound in coal and oil use…it is also seeing the largest annual increase in CO2 emissions in history.’

- As well as the World Economic Outlook, the IMF also released its Global Financial Stability Report and Fiscal Monitor this week.

- A couple of weeks back we included some links to the demise of the World Bank’s Doing Business Report and the Bank’s investigation into some data irregularities that triggered the decision to cease publication. This week the IMF Executive Board said that the information presented in the course of that Bank review ‘did not conclusively demonstrate’ that the IMF’s current Managing Director played an improper role regarding the Doing Business 2018 Report when she was CEO of the World Bank. For some more discussion, here is Lowy’s Steve Grenville on the political nature of the IMF and the Bank, here is Anne Krueger arguing that the affair has triggered a credibility crisis for both the IMF and the World Bank, and here is an interesting VoxEU column that links the demise of Doing Business to Goodhart’s Law – that when an index becomes a policy target, it stops being a good measure.

- A column on the economic geography of climate change.

- The Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2021 (more commonly if less accurately known as the Nobel Prize for Economics) was awarded to David Card ‘for his empirical contributions to labour economics’ and to Joshua Angrist and Guido Imbens ‘for their methodological contributions to the analysis of causal relationships.’ Here’s Marginal Revolution with a nice description of their contribution to the credibility revolution in economics, and here’s FT Undercover Economist Tim Harford on how they turned statistics into insight. For those who’d like to dig a little deeper, as well as the very useful material on the Nobel web site, I’d also recommend this essay in the Journal of Economic Perspectives by Angrist on the credibility revolution in empirical economics.

- The WSJ sets out some detailed background on the Evergrande story.

- Bloomberg Businessweek digs into Tether.

- The Economist magazine has a Special report on the new order for World Trade.

- Competition is for losers: David Runciman in the LRB on Peter Theil.

- Stratechery on the Death and Birth of Technological Revolutions.

Latest news

Already a member?

Login to view this content