Real wages haven't been keeping pace with productivity for a while, which has put a constraint on overall sustainable economic growth.

One of the more important challenges confronting economic policymakers across almost all advanced economies, including Australia, is the persistently slow rate of growth in real wages — that is, after allowing for the impact of persistently low price inflation. The unusually slow (by historical standards) growth in Australian real wages in recent years can be attributed, at least in part, to the fact that, since the peak of the mining boom earlier this decade, the unemployment rate has remained above the level traditionally associated with full employment (and to the persistence of historically high levels of under-employment).

But the experience of other countries where unemployment has fallen to levels well below those conventionally regarded as consistent with full employment — including the US, Japan, Germany, UK and New Zealand — suggests that labour markets now need to be much tighter — and for longer than previously — before growth in wages begins to pick up.

And there’s no compelling reason to think that Australia’s experience will be any different, given the similarity between the factors that appear to have driven changes in the relationship between the state of the labour market and wages outcomes across advanced economies. These factors include globalisation, automation, slower productivity growth, changes in the composition of the workforce, changes in the way work is organised, and changes in the legal and regulatory frameworks within which wages and salaries are determined.

Since wages and salaries are a significant cost of production for most businesses, there might at first glance seem to be little reason for directors and executives to be particularly worried about wages growth being “too low”. But from a broader perspective, persistently slow growth in wages presents two problems for business leaders.

The first is that since household spending represents by far the largest component (almost 60 per cent) of GDP. The main driver of the household spending growth rate is the growth rate of household income, and wages represents the largest component of household income. So persistently slow growth in real wages imposes a constraint on overall economic growth — especially now that the scope for reductions in household saving is more limited than at any time since before the global financial crisis of a decade ago.

The second is that, as Reserve Bank Governor Philip Lowe noted in a speech in July, “slow wages growth is diminishing our sense of shared prosperity [and] if this persists, it can make needed economic reforms more difficult”.

One strand of conventional economic theory holds that, in the long run, the level and growth rate of real wages depends on the level and growth rate of labour productivity. Another theory suggests that labour productivity growth depends on (among other things) the level of capital investment, which is in turn importantly influenced by expected rates of return on investment.

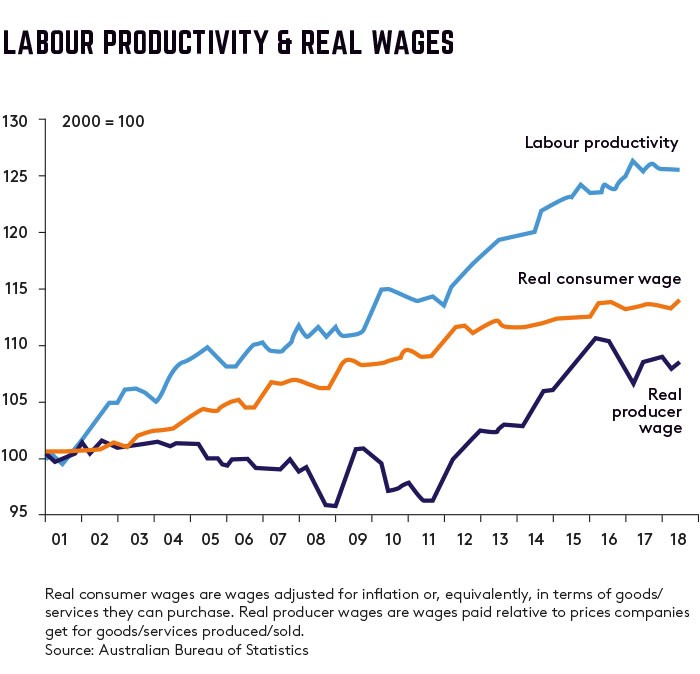

Together, these two propositions inform the widely held view that a prerequisite for faster growth in real wages is more rapid growth in profits. However, as is sometimes the case with economic theories, the available real world evidence suggests that the story isn’t quite that simple. In Australia, as in many other advanced economies, real wages have grown much less rapidly than labour productivity — irrespective of whether real wages are viewed from the perspective of employers (deflating nominal wages by a measure of the prices of goods and services produced) or employees (deflating nominal wages by a measure of the prices of goods and services consumed) — as shown in the top chart (left).

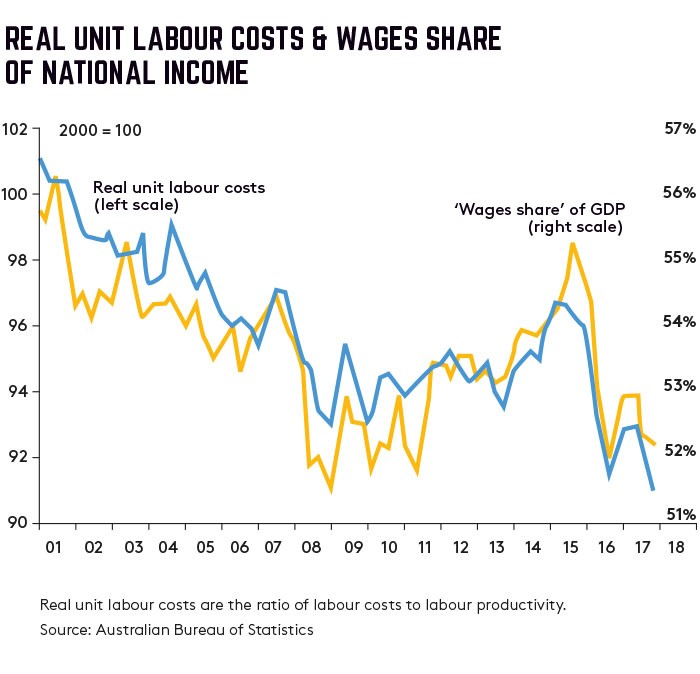

The corollary of the gap between real wages and labour productivity, which has opened up over the past two decades, is that real unit labour costs — that is, real wages (and other “on costs”) per dollar of goods and services produced — have declined by 10 per cent since the turn of the century. By encouraging the substitution of labour for capital, this decline in real unit labour costs has helped facilitate strong growth in employment — but, for precisely the same reason, it has also detracted from productivity growth. And, as the second chart illustrates, it directly parallels the decline in the wages share of Australia’s national income to near-record lows.

Put differently, the rise in the “profits share” of Australia’s national income (to near-record highs in recent years) reflects the fact that most of the benefits of what productivity growth Australia has experienced over the past two decades have accrued to employers, rather than employees. It’s in that sense that persistently slow growth in real wages risks “diminishing our sense of shared prosperity”, in Lowe’s words.

The problem that confronts Australia today is, arguably, the opposite of the one we faced some 35 years ago. After the “wages explosions” of the mid-1970s and early ’80s, Australia was burdened with what became known as a “real wage overhang”, a reference to the fact that real wages had grown much faster than productivity, resulting in stubbornly high unemployment and a much-diminished profit share of national income. In response, government policy — with the support of peak union and business organisations — sought to restrain growth in real wages to less than that of productivity, in order to correct the overhang. By and large, that objective was attained.

Today, by contrast, the country has what could be called a “real wage underhang”. Australia needs to find a way of allowing real wages to grow at a faster rate than productivity, for a while — and, desirably, at the same time fostering a faster rate of growth in productivity — in order to facilitate not only faster and more sustainable economic growth, but also to restore our communal sense of prosperity.

Latest news

Already a member?

Login to view this content