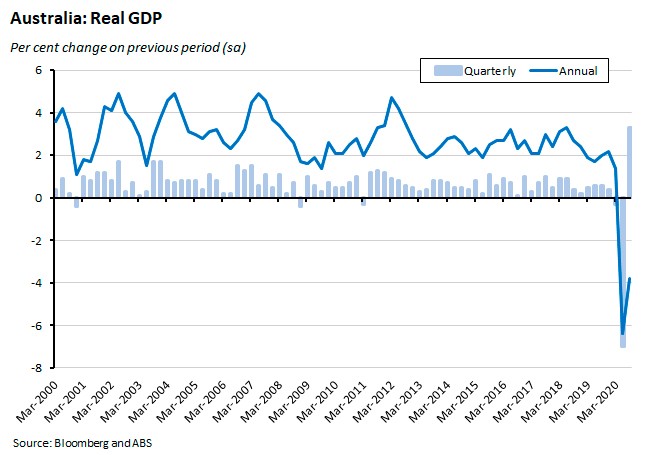

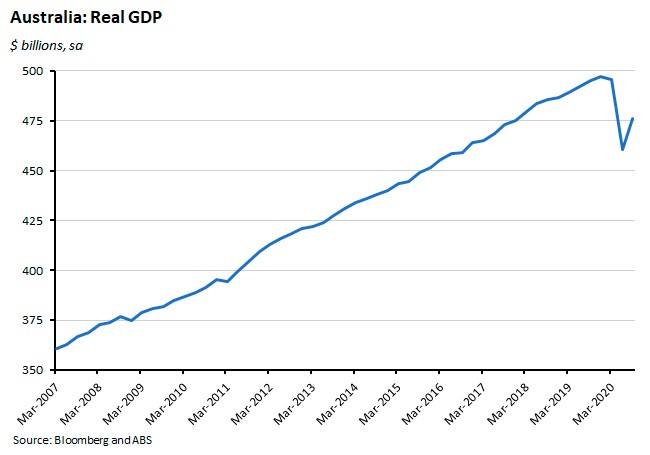

Real GDP rose by 3.3 per cent over the September quarter as the economy started to grow again, technically bringing the COVID-19 recession to an end but still leaving output more than four per cent below its pre-pandemic level.

The RBA left monetary policy unchanged at its 1 December meeting and is now scheduled to take a break with the next policy meeting scheduled for 2 February 2021. Australia recorded its sixth quarterly current account surplus in a row in Q3. And at the start of Q4, Australia recorded a trade surplus of almost $7.5 billion in October. The total value of new loan commitments for housing and the value of owner occupier home loan commitments both reached record highs in the same month. National payroll jobs numbers rose for a third consecutive fortnight, supported by continued recovery in Victoria. Building approvals for dwellings rose in October led by approvals for houses. House prices rose for a second consecutive month in November. After the previous week’s interruption, the weekly index of consumer confidence resumed its climb. Total credit in the economy in October was unchanged relative to September. Australia’s total general government net operating balance was in deficit by almost $94 billion in the September quarter of 2020.

This week’s readings include new JobKeeper statistics, explanations for the resilience of Australia’s housing market in the face of COVID-19, some guarded optimism from the RBA, trends in major energy and resource projects, Australia’s evolving strategic landscape, the OECD’s latest economic outlook, the ‘credit glut’, climate risk and response in Asia and a look at whether real estate booms are bad for national productivity performance.

What I’ve been following in Australia . . .

What happened:

The ABS said that real GDP rose 3.3 per cent (seasonally adjusted) in the September quarter although output was still down 3.8 per cent relative to Q3:2019.

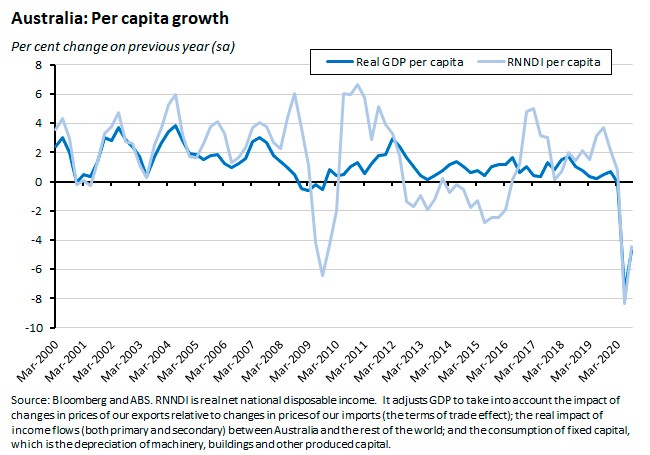

In per capita terms, real GDP rose 3.2 per cent over the quarter and was down 4.7 per cent over the year, while real net national disposable income per capita was up 4.8 per cent quarter-on-quarter and down 4.5 per cent year-on-year.

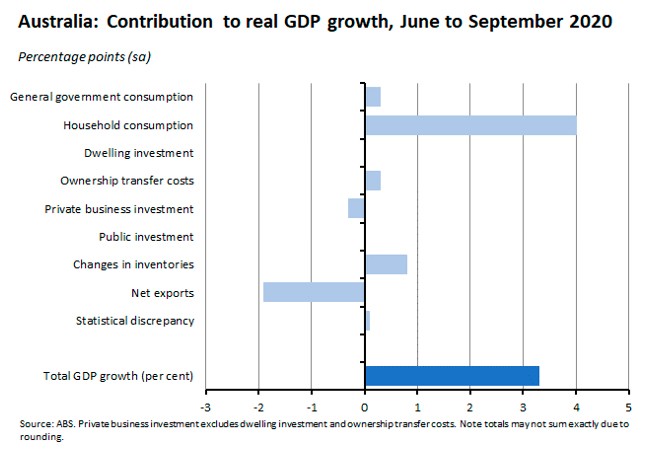

Real GDP growth in the third quarter was driven by domestic demand in general (which contributed 4.3 percentage points to overall growth) and by household consumption in particular (which alone contributed four percentage points). There were also modest positive contributions from general government consumption, ownership transfer costs and changes in inventories, while net trade (due to both falling exports and rising imports) and private business investment were both headwinds for activity.

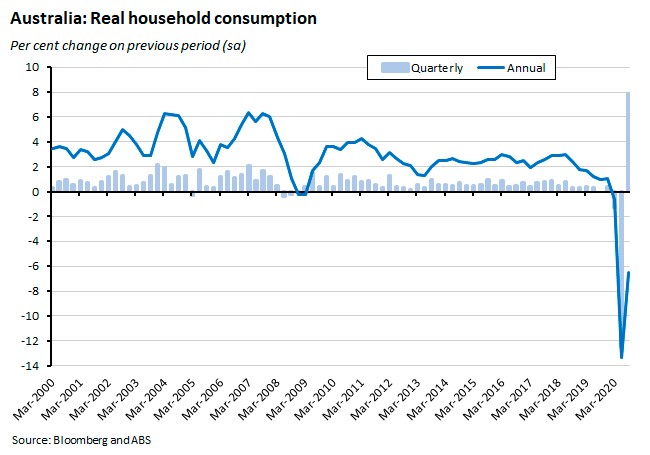

Household consumption expenditure rose 7.9 per cent over the quarter – marking the largest rise in the history of the quarterly national accounts following last quarter’s dramatic plunge in spending – although it was still down 6.5 per cent in annual terms. Household spending on services overall increased 9.8 per cent, with particularly strong growth for discretionary services, while goods consumption increased 5.2 per cent.

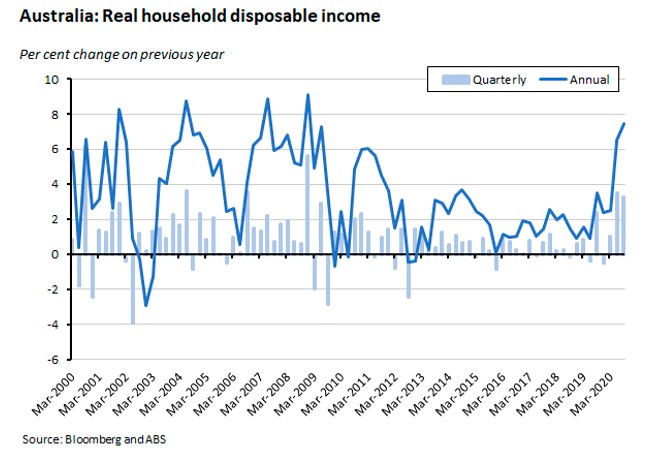

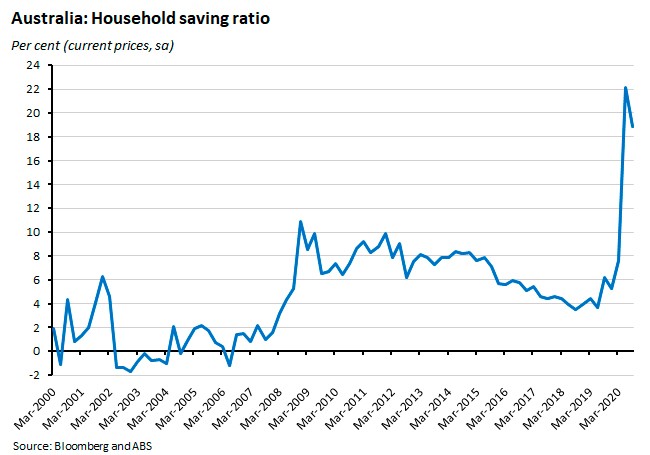

Real household disposable income rose strongly over the quarter and was also up in annual terms, boosted for a second successive quarter by fiscal stimulus measures.

As a result, although the household savings ratio fell back from its Q2 high of 22.1 per cent, it still remained elevated at 18.9 per cent.

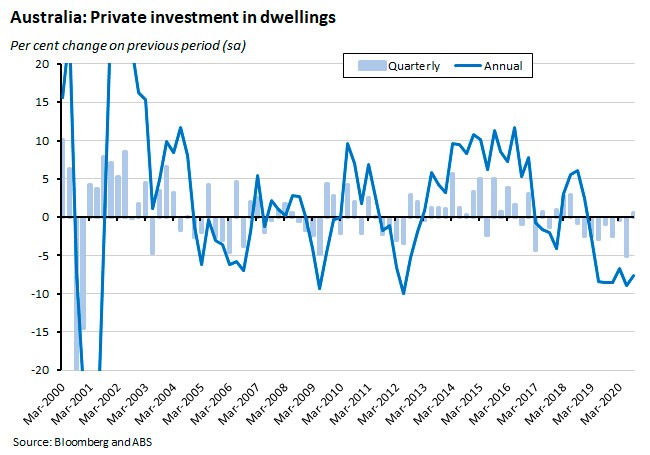

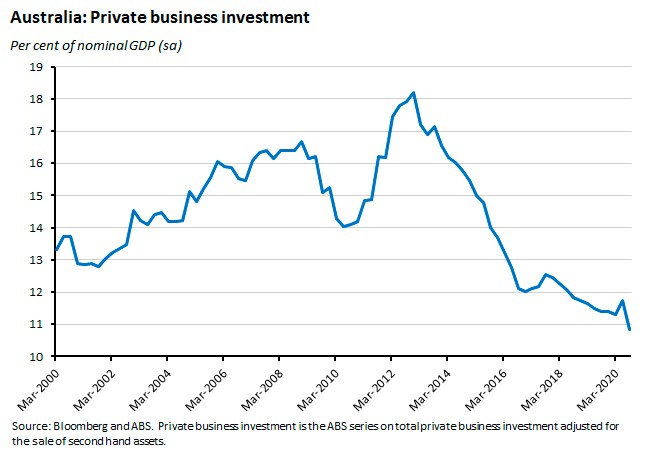

In contrast to household spending, total gross fixed capital formation (investment) fell over Q3, dropping by 0.1 per cent over the quarter and six per cent over the year as private investment overall made no contribution to GDP growth. Dwelling investment edged up 0.6 per cent in quarterly terms, making back a little ground from Q2:2020’s steep fall, but was still down 7.6 per cent relative to Q3:2019. (At the same time, ownership transfer costs which include legal and real estate fees surged by 21.4 per cent over the quarter to be up 8.6 per cent in annual terms as the housing market came back to life.)

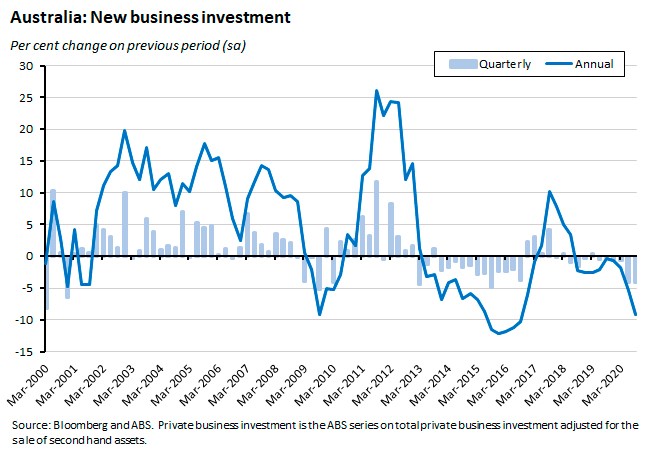

New private business investment fell for a fourth consecutive quarter, dropping 4.1 per cent, and was 9.2 per cent lower than in Q3:2019. By industry, mining investment was down 5.2 per cent over the quarter but up 4.5 per cent over the year. Non-mining investment dropped by 2.1 per cent in quarterly terms and 13.9 per cent in annual terms.

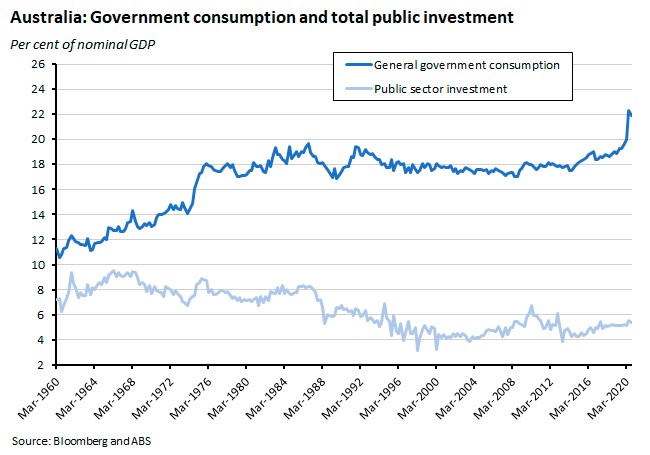

Public sector investment edged up 0.3 per cent over the quarter although it was down marginally (0.2 per cent) in annual terms. As noted above, public consumption made a more substantial contribution to overall growth this quarter, with general government consumption up 1.4 per cent quarter-on-quarter and a strong 7.8 per cent year-on-year.

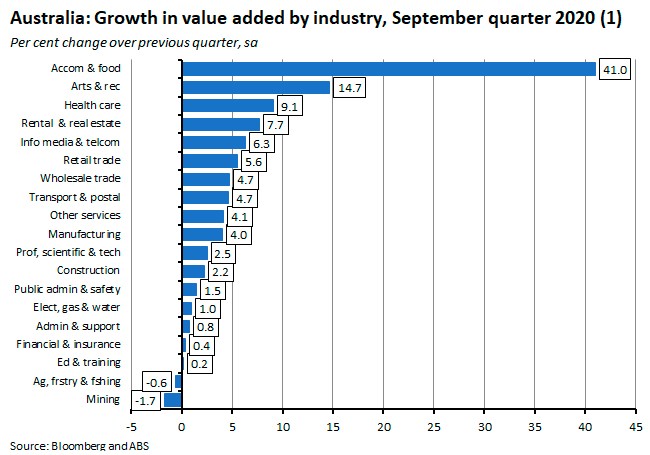

In terms of sectoral performance, 17 of 19 industries recorded positive growth across Q3 with the largest gains coming in accommodation and food services (where output soared by 41 per cent), arts and recreation (up 14.7 per cent) and health care and social assistance (up 9.1 per cent). The two exceptions were agriculture, forestry and fishing (down 0.6 per cent) and mining (down 1.7 per cent).

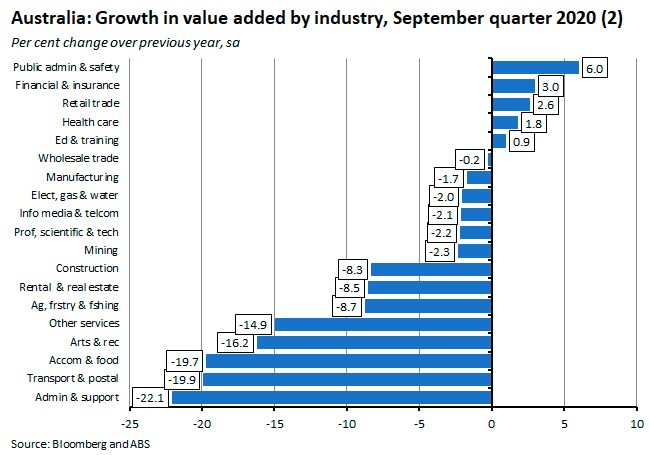

In terms of over the year comparisons, however, only five industries recorded positive growth: public administration and safety, financial and insurance services, retail trade, health care and education and training.

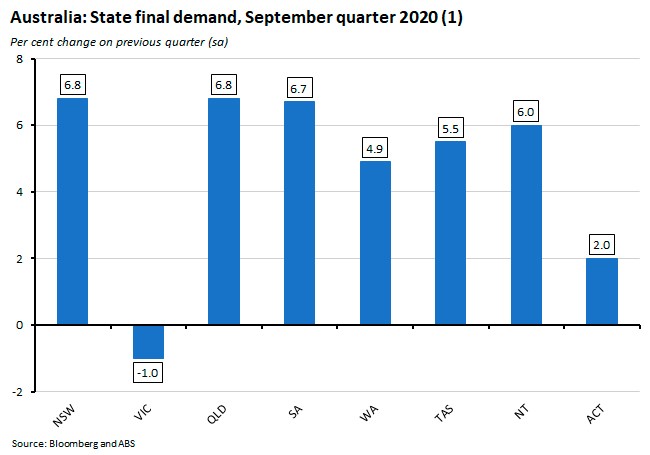

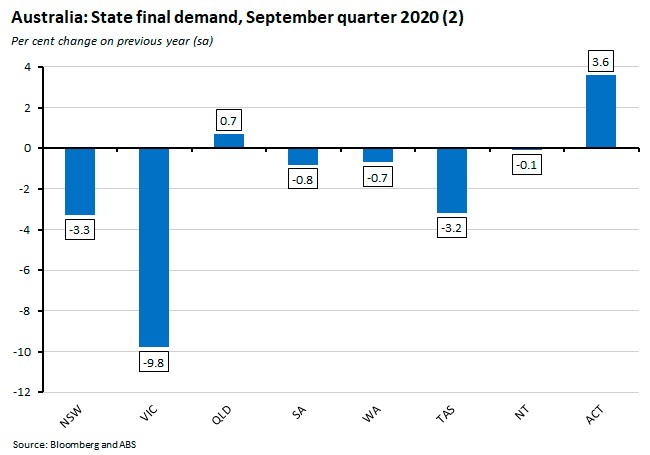

By state and territory, final demand grew everywhere over the quarter with the sole exception of Victoria. The strongest rises were in New South Wales, Queensland and South Australia.

In annual terms, final demand was still down in most states and territories, with only Queensland and ACT recording positive results.

Why it matters:

The Q3 GDP results comfortably beat market expectations for a 2.5 per cent quarterly rise and a 4.4 per cent annual fall. The resumption of real GDP growth also means that – in a technical sense, at least – the Australian economy has now exited the COVID-19 recession. Of course, that’s not the same thing as saying we’ve exited recession-like conditions. The level of GDP at the end of the September quarter is still more than four per cent below the level it had achieved by the end of 2019. And other indicators – in particular relating to the labour market – remain far from normal.

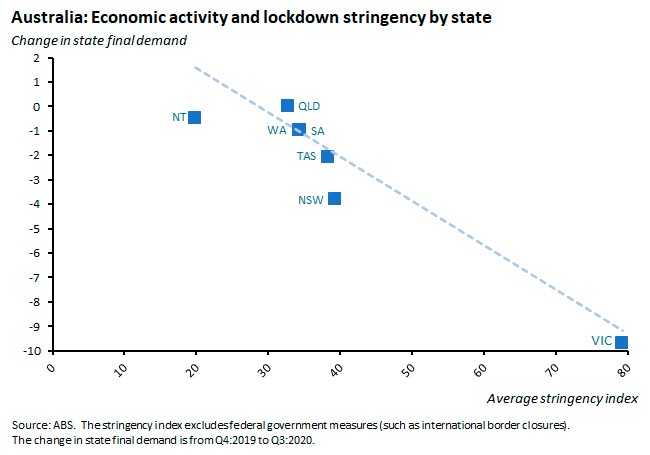

Still, even keeping all those qualifications in mind, this was a good GDP result, not least since it occurred despite the disruption to the September quarter created by Victoria’s public health lockdowns, which saw state final demand fall one per cent over the quarter. The important influence of variations in the level of public health restrictions on economic activity is visible in new data created by the ABS comparing lockdown stringency with growth outcomes by state.

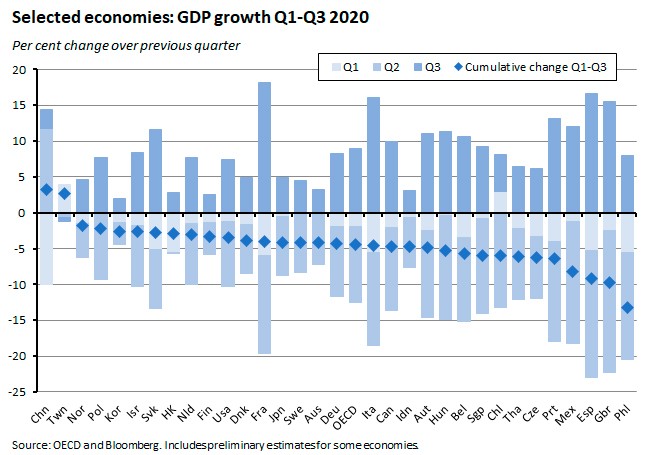

How does Australia’s GDP growth performance stack up in international terms? As noted above, over the first three quarters of this year, output is now down by about 4.2 per cent. That’s a bit better than the average OECD performance (a 4.4 per cent decline across the same period) and puts Australia alongside Japan, Sweden and Germany and only a little behind France in terms of cumulative output losses. And Australia has had significantly better public health outcomes (measured in terms of COVID-related deaths per million of population) than three of those four, with only Japan out-performing us. Moreover, while Australia also looks set for a decent Q4 growth performance, much of the Northern Hemisphere is facing more challenging public health conditions due to a resurgence in COVID-19 cases.

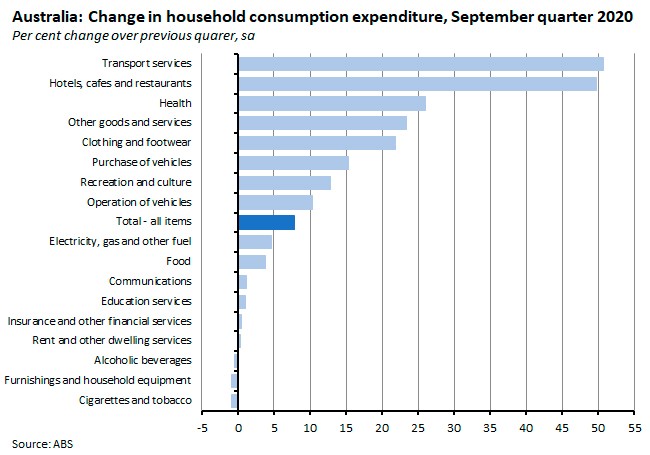

The details of this quarter’s national accounts emphasise how the recovery to date has been supported by the combined effects of the easing of government restrictions and better health news plus continued public policy support. The impact of the former is visible in the snapback in consumption spending on those products and services that had suffered most from lockdowns and voluntary social distancing, with large rises in spending hotels, cafes and restaurants (up almost 50 per cent), transport (up more than 50 per cent), recreation and culture (up 12.8 per cent), and other goods and services (up 23.4 per cent).

It is also apparent in the big recoveries in gross value added in the most severely impacted industries, especially accommodation and food services but also arts and recreational services, as reported in the previous section.

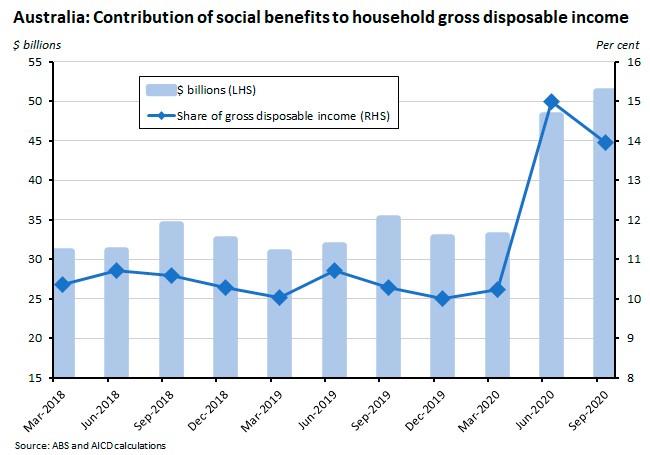

The impact of policy can be seen in the significant support provided to household gross disposable income by the payment of government social benefits such as the JobSeeker coronavirus supplement and the cash payments to households, which together delivered a significant lift to incomes over both the June and September quarters.

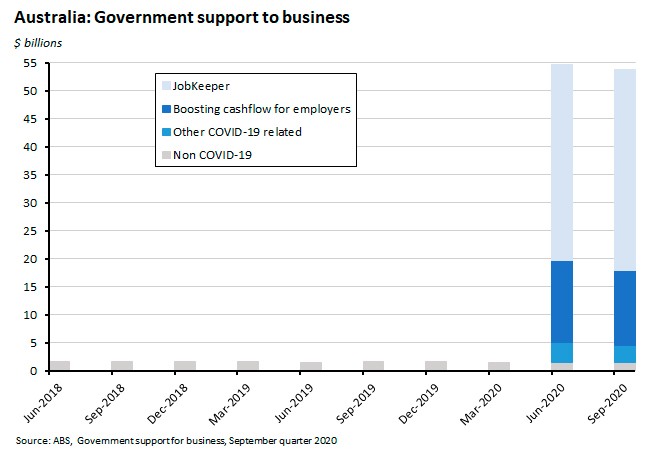

The role of policy is even more apparent in the substantial fiscal support provided to Australian businesses. JobKeeper payments alone delivered $35.8 billion in Q3, following $35.1 billion in Q2 while Boosting cash flow for employers contributed a further $13.5 billion on top of $14.6 billion in Q2. And other COVID-19 related subsidies, including those made by state governments, added an additional $2.9 billion to the total in the September quarter.

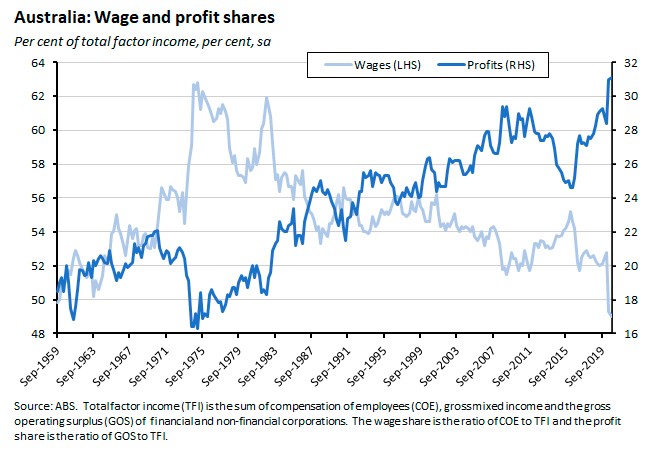

All that government largesse helped lift the profit share in total national income to a new record high in Q3 even as the wage share slipped to a new record low.

While generous policy support has translated into higher household spending, the same is not true for new private business investment, which has now slumped to less than 11 per cent of GDP. While hardly surprising given the high level of uncertainty and economic dislocation seen this year, this is still unwelcome news for future growth and productivity prospects and any sustained recovery will ultimately also require a recovery in business capex.

What happened:

The RBA left its current policy settings unchanged at the 1 December monetary policy meeting. The accompanying statement noted:

- ‘Mixed’ news on the global front, with rising infection rates and waning economic momentum in Europe and the United States set against positive news on vaccines.

- Ongoing economic recovery in Australia where ‘recent data have generally been better than expected’. Even so, ‘the recovery is still expected to be uneven and drawn out and it remains dependent on significant policy support. In the RBA's central scenario, it will not be until the end of 2021 that the level of GDP reaches the level attained at the end of 2019.’

- A further rise in [Australia’s] unemployment rate is still expected, as businesses restructure in response to the pandemic and more people rejoin the workforce.’ The RBA does think that the unemployment rate will fall next year, but only slowly, still leaving it around six per cent at the end of 2022.

- It follows that ‘high unemployment and excess capacity is expected to result in subdued increases in wages and prices over coming years…In underlying terms, inflation is forecast to be 1 per cent in 2021 and 1½ per cent in 2022.’

- Given this outlook, ‘monetary and fiscal support will be required for some time.’

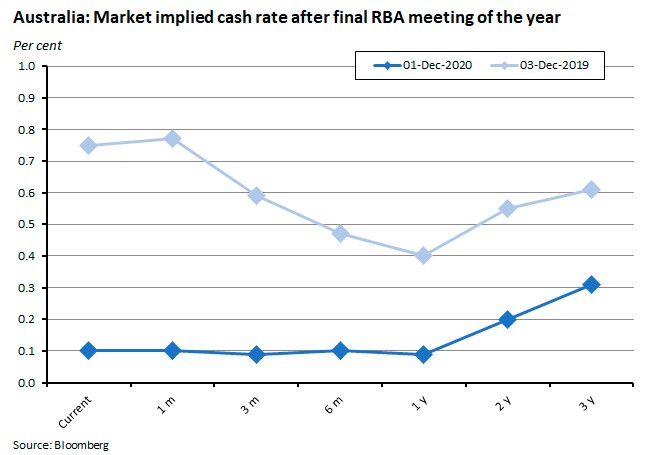

In the RBA’s view, all that means that ‘the Board is not expecting to increase the cash rate for at least 3 years.’ Moreover, it remains ‘prepared to do more if necessary.’

Why it matters:

Following the announcement of last month’s policy package, no action had been expected from the central bank in December and as anticipated, the RBA opted to leave its current policy settings unchanged. The next monetary policy meeting isn’t due until 2 February, which will give Martin Place time to assess the state of the recovery over the next couple of months and in particular, to see if outcomes continue to beat expectations. Meanwhile, markets are expecting to see little change in terms of the cash rate over the next three years, in line with the RBA’s forward guidance.

Interestingly, the statement made no mention of two of the big economic items in the news – mounting bilateral tensions with Australia’s largest trading partner and the return of rising house prices – suggesting that both issues have yet to feature as a major concern when it comes to rate-setting. The latter did, however, make an appearance in Governor Lowe’s testimony to the House Standing Committee on Economics (referenced in this week’s readings, below) where he noted that while the central bank was ‘paying close attention to asset prices and trends in household debt…in the current environment, the bigger stability risk is a protracted period of high unemployment, rather than excess borrowing.’

What happened:

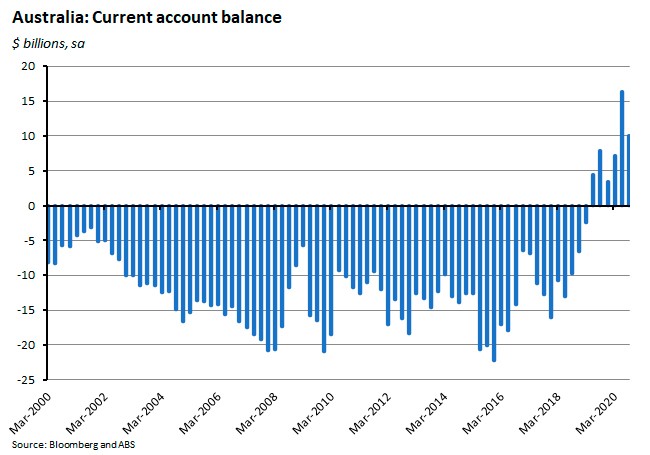

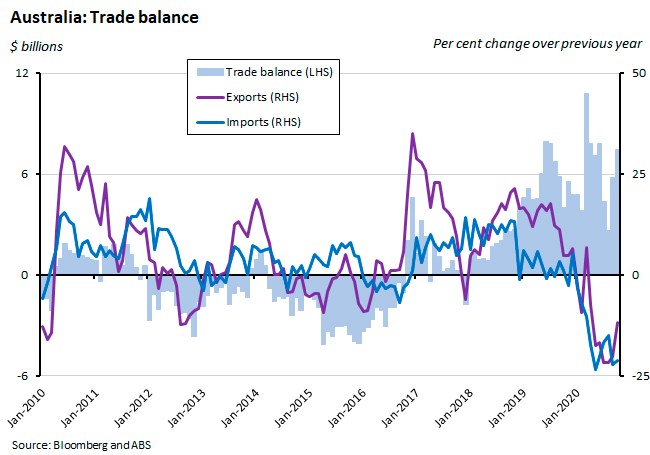

Australia’s current account surplus fell $6.3 billion to $10 billion or about 2.1 per cent of GDP in the September quarter (seasonally adjusted).

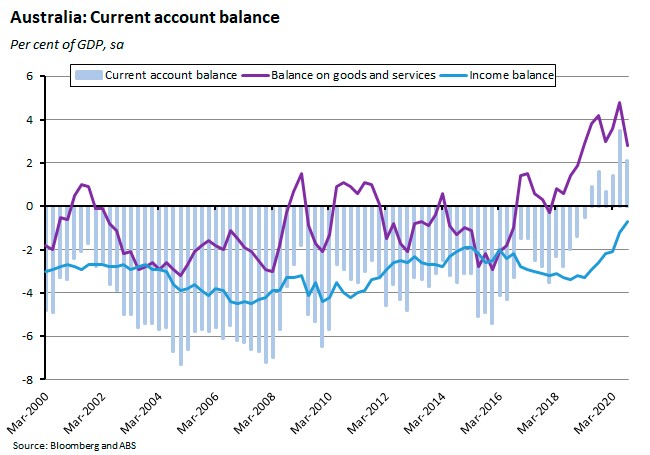

The ABS said that the fall in the current account surplus was largely the product of a decline in the surplus on goods and services, which dropped $8.7 billion to $12.8 billion. The deficit on the net primary income balance shrank to just $3.3 billion.

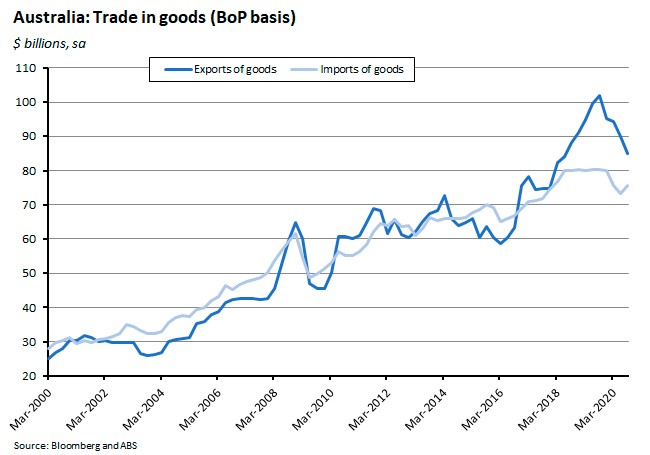

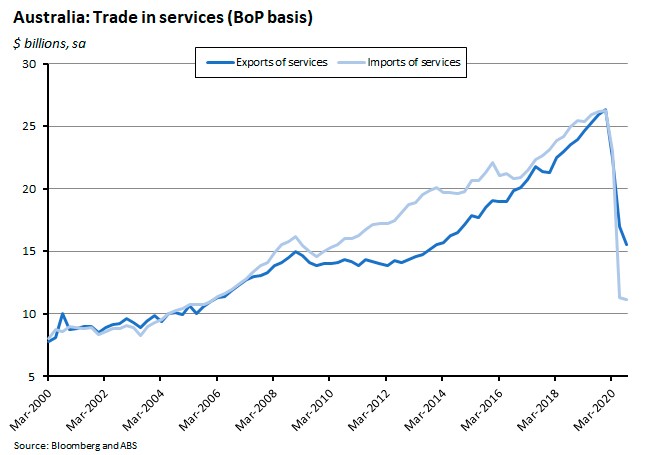

Exports of goods fell six per cent over the quarter while exports of services were down 8.7 per cent. Goods imports rose three per cent while imports of services fell 1.6 per cent.

The current account surplus was matched by a deficit of $9.3 billion on the capital and financial accounts, mainly driven by the financial account deficit of $9.1 billion. That in turn reflected a net outflow of equity of $43.3 billion and a net inflow of debt of $34.2 billion.

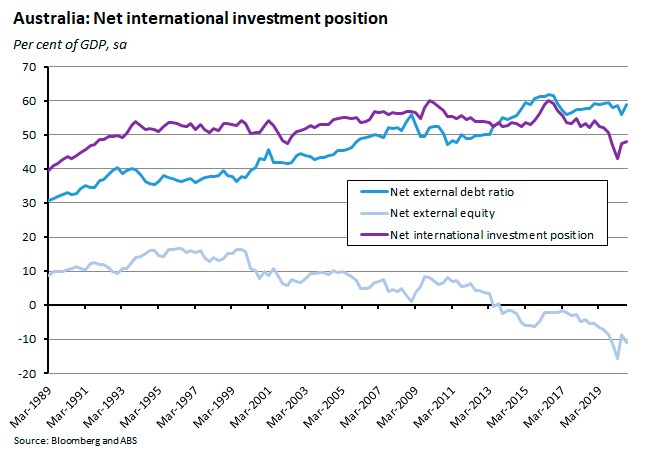

Australia's net international investment position (IIP) was a liability of $942.8 billion as of 30 September 2020, equivalent to about 48 per cent of GDP. Australia's net foreign debt liability position was $1,157.8 billion or 58.9 per cent of GDP while Australia's net foreign equity asset position was $215 billion or 10.9 per cent of GDP.

Why it matters:

Australia recorded a sixth consecutive current account surplus in the September quarter of this year, and although the surplus was down more than $6 billion on the June quarter result, it was still the second largest on record.

The ABS noted that the pandemic continues to shape Australia’s external position, with stronger activity both in Australia and overseas contributing to a recovery in imports, reflected in substantial increases in imports of non-industrial transport equipment, fuels and lubricant, and textiles clothing and footwear, while at the same time, more global competition and reduced demand sat behind lower commodity exports.

Meanwhile, international travel bans continue to impede services trade.

What happened:

Australia recorded a trade surplus of almost $7.5 billion in October (seasonally adjusted). The ABS reported that exports of goods and services rose five per cent over the month but were down 11.7 per cent over the year while imports were up one per cent in monthly terms but down 21.3 per cent relative to October 2019.

Why it matters:

After recording a sixth consecutive current account surplus in the third quarter of this year (see previous story), Australia began the final quarter of 2020 with another sizeable monthly trade surplus. After having risen by a softer 2.6 per cent over the month in September, export growth strengthened in October, driven by a six per cent rise in goods exports. The latter included a strong month for exports of iron ore, which continue to be immune from the tensions disrupting other elements of Australia’s trade with China, and to benefit from high iron ore prices. On the import side of the trade balance, imports of consumption, capital and intermediate goods all grew by two per cent in October as domestic demand continues its recovery.

What happened:

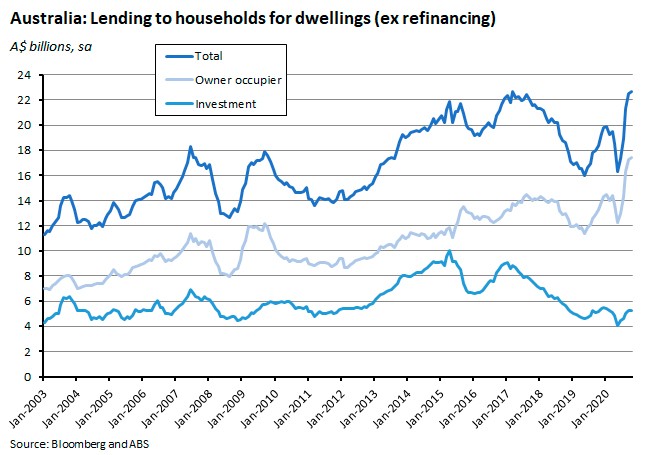

The ABS said that new loan commitments (excluding refinancing) for housing rose 0.7 per cent in October (seasonally adjusted) to be up 23.3 per cent over the year. Loan commitments for owner-occupiers rose 0.8 per cent month-on-month and 31.2 per cent year-on-year while commitments for investors were up 0.3 per cent and 2.8 per cent, respectively.

New commitments for personal fixed term loans rose 4.3 per cent over the month but were still down 7.9 per cent over the year. Commitments for business construction and purchase of property both fell over the month and over the year.

Why it matters:

The total value of new loan commitments for housing overall and the value of owner occupier home loan commitments both reached record highs in October as the housing market continues to strengthen.

The largest contributor to the rise in owner occupier housing loan commitments was commitments for the construction of new dwellings which were up 10.9 per cent. The ABS noted that the value of construction loan commitments has risen by 65.6 per cent since July, pointing out that this coincides with the June 2020 implementation of the Government’s HomeBuilder grant. The Bureau also said that the number of owner occupier first home buyer loan commitments increased by 3.4 per cent in October to reach 13,481 - more than 30 percent higher than in any pre-COVID month since 2009, when the first home owner grant was temporarily tripled as part of the then government’s stimulus package in response to the global financial crisis.

What happened:

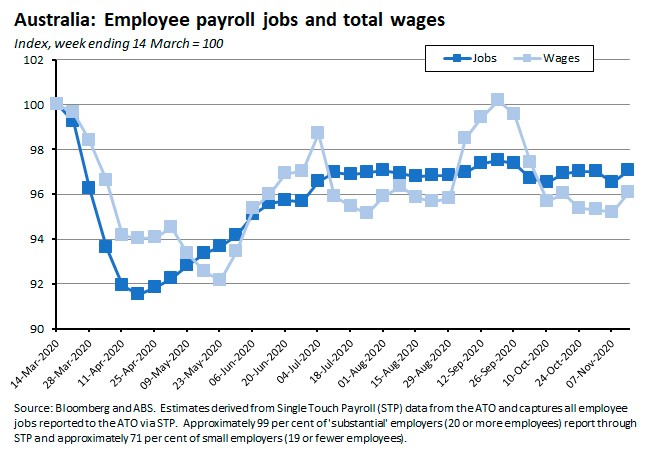

The latest ABS data on weekly payroll jobs showed that between the week ending 14 March 2020 and the week ending 14 November 2020, the number of payroll jobs fell 2.9 per cent while total wages declined by 3.9 per cent. As a result, by 14 November there were approximately 320,000 fewer payroll jobs than on 14 March.

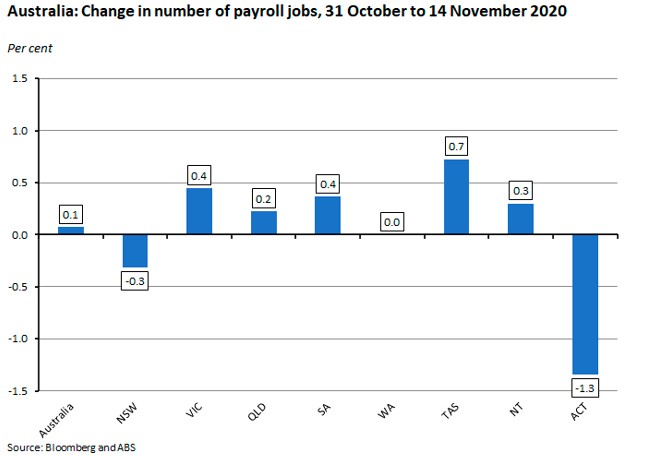

According to the most recent fortnight’s worth of data, between the week ending 31 October 2020 and the week ending 14 November 2020 the number of payroll jobs rose by 0.1 per cent.

By state, since the week ending 14 March the largest falls in payroll jobs have been suffered by Victoria (down 5.4 per cent), Tasmania (down 4.1 per cent) and the ACT (down 3.3 per cent). Only the NT added jobs over this period (up 0.3 per cent). Over the most recent fortnight of data, only NSW and the ACT saw declines in job numbers, with Victoria posting another gain as the state continued to emerge from the effects of public health restrictions.

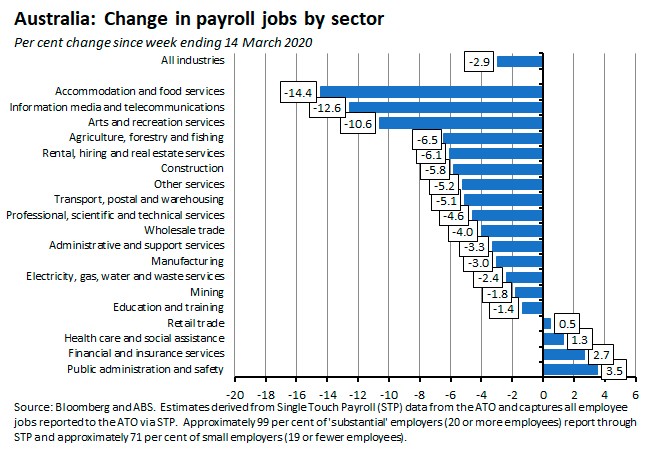

By industry, the largest falls in payroll jobs over the full period since the week ending 14 March are accommodation and food services (down 14.4 per cent), information media and telecommunications (down 12.6 per cent) and arts and recreational services (down 10.6 per cent).

Over the latest fortnight, the largest job falls were in Agriculture, forestry and fishing (down 2.8 per cent), other services (down 1.8 per cent) and rental, hiring and real estate services (down 1.4 per cent).

Why it matters:

Payroll jobs have now risen for three consecutive sets of fortnightly data releases, supported by the recovery in activity in Victoria (which has also enjoyed three consecutive sets or increases. Note, however, that the ABS also reminded us that ‘The end of the calendar year is a time of pronounced seasonal increases in employment, and [this] should be considered when interpreting changes in payroll jobs data over the period.’

Finally, there are two changes in the sectoral numbers worth pointing out. First, the scale of payroll job losses in information, media and telecommunications over the course of the pandemic now exceeds that suffered by arts and recreational services. And second, the retail services industry has joined the small subset of industries to have added payroll jobs over the period since 14 March.

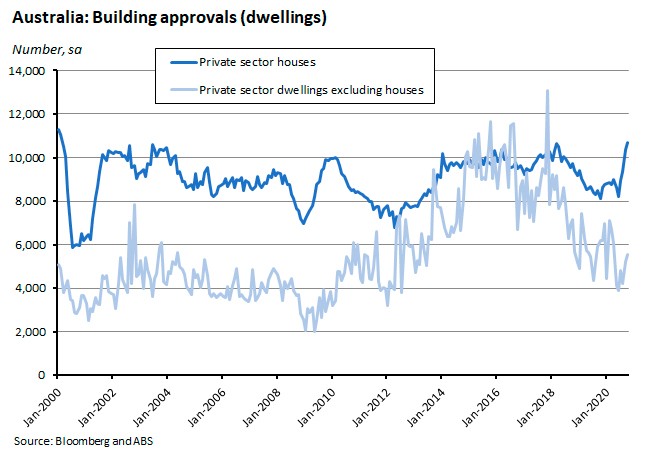

What happened:

According to the ABS, total approvals for dwellings rose by a seasonally adjusted 3.8 per cent over October to be up 14.3 per cent over the year. Approvals for private sector dwellings excluding houses rose 6.2 per cent month-on-month but fell 10.6 per cent in annual terms, while approvals for private sector houses rose 3.1 per cent over the month and jumped 31.7 per cent in annual terms.

By state, there were large increases in total approvals in New South Wales (up 32.1 per cent) and Western Australia (up 29.7 per cent). Approvals for private sector houses rose by 37.5 per cent in Western Australia over the month, while in New South Wales there was a large gain for private sector dwellings excluding houses.

The value of total building approved rose 26.1 per cent in October (seasonally adjusted), driven by a 58.6 per cent rise in the value of non-residential building. The value of total residential building increased 9.4 per cent over the month, reflecting a rise in the value of new residential building (up 11.5 per cent), while the value of residential alterations and additions fell 3.3 per cent.

Why it matters:

Building approvals for private sector houses rose for the fourth consecutive month in October and were at the highest recorded level since February 2000 (in seasonally adjusted terms). The ABS attributed the strong demand for detached housing in particular to the relaxation of COVID-19 restrictions, record low interest rates and federal and state-based incentives

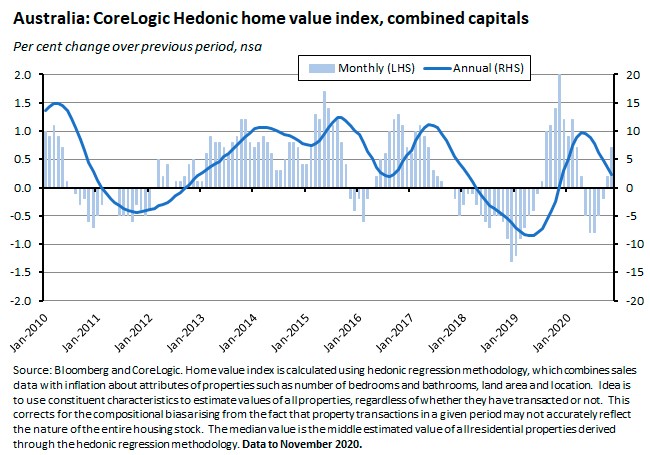

What happened:

CoreLogic’s national dwelling values index rose 0.8 per cent over November to be up 3.1 per cent over the year. The combined capitals index increased 0.7 per cent over the month and 5.7 per cent over the year.

Prices rose across the month in all capital cities in November, with the largest monthly increases in Canberra and Darwin (both up 1.9 per cent) and the smallest gains in Sydney (up 0.4 per cent) and Brisbane (up 0.6 per cent).

Regional areas continue to outperform capital cities, with the 1.4 per cent monthly rise in the combined regionals index double the gain recorded by the combined capitals index.

Why it matters:

This was the second consecutive monthly rise in housing values, indicating that the recovery in the housing market described last month is ongoing. At a national level, the index is still below per-COVID levels but CoreLogic notes that if current trends were to be sustained, then values would surpass their March 2020 levels early in 2021. Already, Brisbane, Adelaide, Hobart and Canberra have set new record highs last month, although other cities are still well-off past peaks. Other housing market indicators also point to further strength, with low levels of housing stock, steady sales growth (outside Victoria) and high auction clearance rates.

House and apartment results have continued to diverge as house values have driven gains in the combined capitals index over the past three months, rising 1.1 per cent, while capital city unit values fell by 0.6 per cent over the same period.

Finally, see this week’s readings for a CoreLogic piece on housing market resilience in the face of COVID-19.

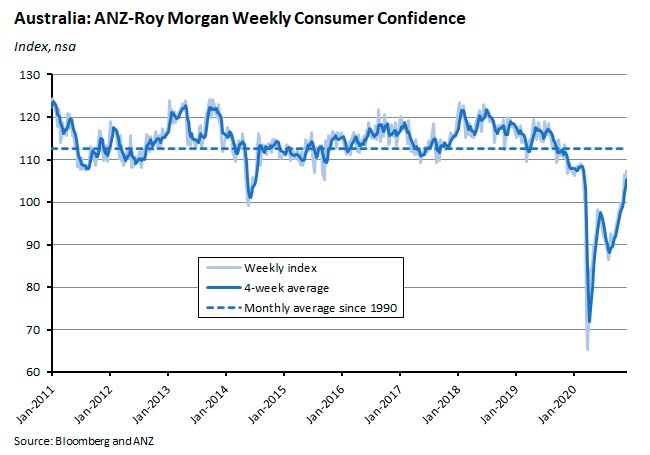

What happened:

The ANZ-Roy Morgan Weekly Consumer Confidence Index rose 2.9 per cent for the weekend of 28/29 November, taking the index up to 107.5.

All five subindices rose over the week, with the largest gain coming in the form of a big 7.6 per cent jump in the ‘current economic conditions’ result, followed in magnitude by a 4.2 per cent increase in ‘time to buy a major item’.

Why it matters:

Last week had brought an end to the run of 11 consecutive weeks of rising confidence, largely as a result of the introduction of lockdown restrictions in South Australia. Better news on that front saw confidence bounce back, with conditions in South Australia returning to positive territory after having fallen below the neural reading of 100 the previous week. Perceptions of current and future economic conditions are now at their highest levels in more than a year, while the ‘time to buy a major item’ subindex is at its highest level since 1 March 2020.

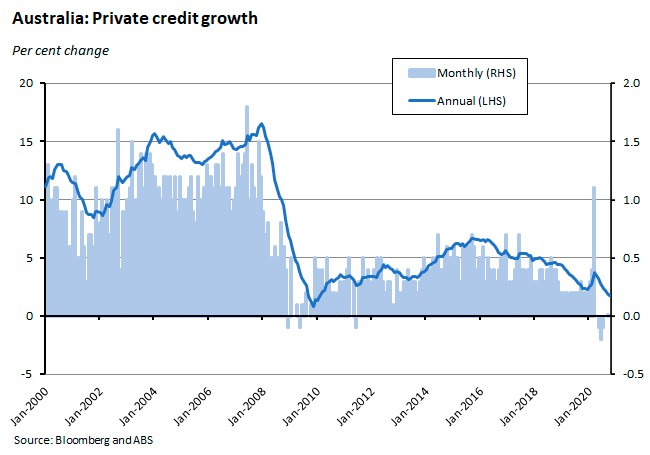

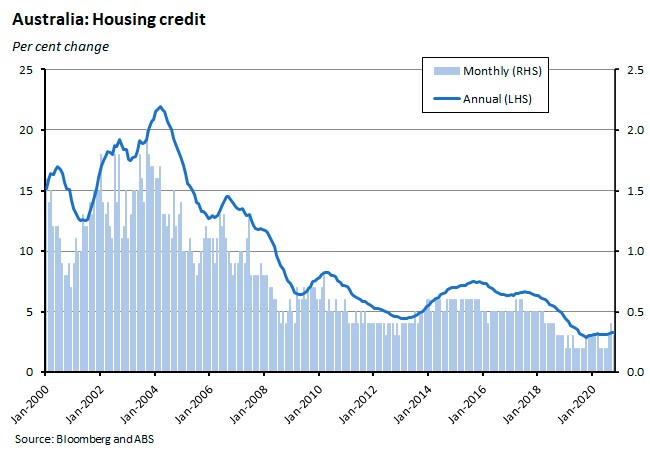

What happened:

The RBA reported that total credit in the economy in October was unchanged relative to September and up just 1.8 per cent over the year.

Housing credit was up 0.3 per cent over the month and 3.3 per cent over the year while personal credit shrank 0.7 per cent relative to September and fell 12.7 per cent in annual terms.

Business credit was down 0.3 per cent month-on-month but up 1.4 per cent year-on-year.

Why it matters:

The strength in the housing market noted earlier points to potential upside in future housing credit growth while CBA has pointed to bank data showing a collapse in borrowing for holidays as one important factor behind the decline in personal credit ex housing.

Business credit has now fallen for six consecutive months, suggesting that business borrowing, and business investment, remain weak.

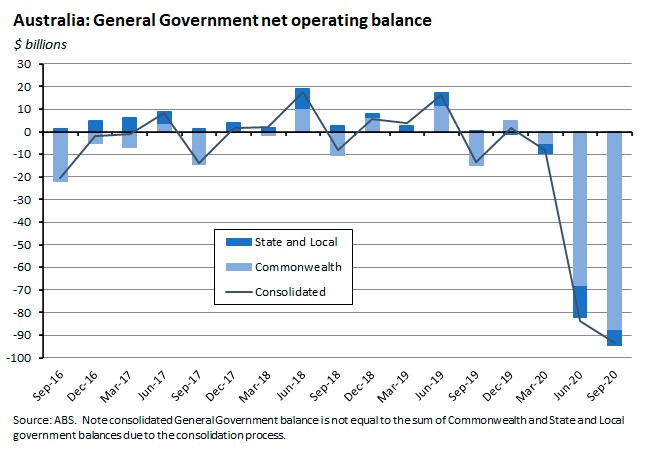

What happened:

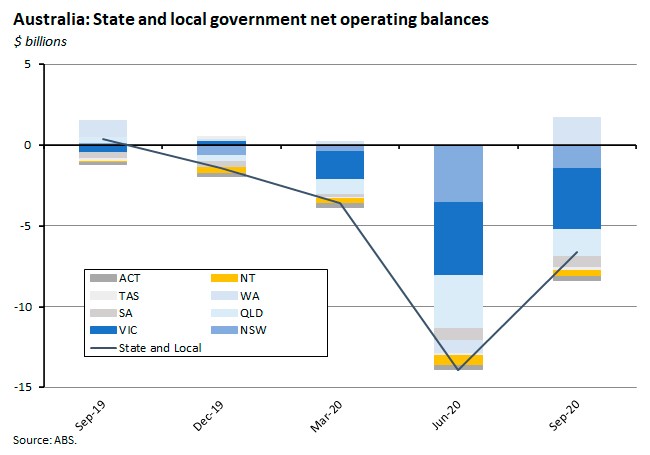

The ABS said that Australia’s total general government net operating balance was in deficit by almost $94 billion in the September quarter of 2020, a widening of the deficit by almost $10 billion relative to the June quarter. Most of that reflected more red ink at the Commonwealth level, where the deficit increased by almost $20 billion. In contrast, the state and local government deficit shrank by more than $7 billion in Q3.

Western Australia was the only state to return to a positive net operating balance in the September quarter, due in part to strong revenues from royalties and an increased GST allocation. Victoria reported the largest deficit in the quarter ($3.8 billion) followed by Queensland ($1.7 billion).

The increase in the consolidated general government deficit in Q3 was mainly driven by developments in revenue. Total revenues fell 6.5 per cent relative to the June quarter and were down 2.8 per cent over the year, largely reflecting lower tax receipts. At the federal level, that was mostly due to lower company tax receipts and excises on petroleum products while at the state and local level the main story was payroll tax waivers along with falling revenue from gambling taxes and other taxes on the provision of goods and services.

Total expenditures slipped 0.5 per cent relative to the June quarter thanks to a modest reduction in COVID-19 related subsidies although this was partially offset by increased payments related to the Medicare and Pharmaceutical Benefits Schemes. In annual terms, expenditure was up more than 42 per cent in Q3:2020, reflecting the continuing impact of a range of government programs including JobKeeper, boosting cash flow for employers and the Coronavirus Supplement.

Why it matters:

The Consolidated government finance statistics bring together Commonwealth and State and local government budget outcomes and therefore provide a more comprehensive picture of trends in public spending and taxation across all levels of government. Both the June and now September quarter results show the dramatic impact of the pandemic on government finances.

What I’ve been reading . . .

The Treasurer provided an update on the latest JobKeeper statistics. The preliminary data show that around 450,000 fewer businesses and around two million fewer employees qualified for JobKeeper in October than in September. Under JobKeeper 1.0, the scheme had supported more than 3.6 million workers and around 1 million businesses, with payments totalling nearly $70 billion over the March to September period. After new eligibility tests were introduced for JobKeeper 2.0, in October around 500,000 entities have had applications processed covering more than 1.5 million employees. The Treasurer notes that these preliminary results are an improvement on the 2020-21 Budget assumption of 2.2 million recipients for the December quarter, suggesting that there were around 700,000 fewer employees covered in October due to their employer no longer meeting the required decline in turnover test relative to the budget’s projections.

ANZ Bluneotes covers the bank’s latest Stateometer.

CoreLogic’s Eliza Owen analyses the resilience of the Australian housing market in the face of the pandemic. Earlier this year, the consensus was that COVID-19 would send prices down by around ten per cent, with worst case scenarios pointing to falls of around a third. Instead, home values fell less than two per cent between March and October and have now risen for two consecutive months. Extremely low interest rates, mortgage repayment deferrals, and the concentration of job and incomes losses due to COVID-19 in sectors where mortgage debt is less common are all part of the story.

RBA Governor Lowe’s Opening Statement to the House of Representatives Standing Committee on Economics. While the RBA now thinks there is some upside potential (‘It is certainly possible that the economy will do better than our central scenario. This scenario does not envisage a vaccine being widely available to most Australians until late next year at the earliest. It also assumes that significant restrictions on international travel are still in place at the end of 2021. Recent medical breakthroughs give us some hope that things will work out better than this. If so, confidence would lift and there would be a further easing of restrictions. The result would be an upside surprise to growth and jobs’) it also notes that some downside risks persist. The overall judgment remains that ‘Australia is likely to experience a run of years with unemployment too high and wage increases and inflation too low.’

The RBA’s December chart pack is also now available.

The ABC’s Gareth Hutchens adds up the various budgetary projections to estimate that total federal, state and territory debt will hit $1.4 trillion by 2023-24.

Peter Martin reports on his latest poll of Australian economists’ attitudes – this time towards the level of support offered by JobSeeker. And here is the Borland piece cited by Martin, which finds that an increase in the payment rate would have little impact on the incentive to work, in part because even a $125/week rise would leave JobSeeker at little more than half the national minimum wage.

The Department of Industry has released Resource and Major Energy Projects: 2020. The report argues that 2019 ‘represented an inflection point in the mining investment cycle. The value of ‘committed’ resource and energy projects — those where a final investment decision (FID) has been taken — increased by 30 per cent over the past year to $39 billion. This growth in value follows six years of decline — as a result of the completion of several large LNG projects — before levelling out last year.’ Over the year to the end of October 2020, the report says the number of resources and energy major development projects increased by 19 per cent to 335 projects, and the value of projects in the investment pipeline increased by four per cent to $334 billion. It also highlights that strong demand for gold and expectations of strong growth for electric vehicles saw the value of gold and battery/electric vehicle related projects rise by 33 per cent and 7 per cent, respectively. In contrast, there has been a slowdown in coal and gas projects. In the case of coal, there is ‘a growing preference for coal expansions over new project investments. There appears to be a growing reluctance to commit to greenfield coal projects, and an expanding list of lenders/investors have announced plans to no longer finance thermal coal projects. Some pension and equity funds are also divesting from, or limiting, their exposure to thermal coal, narrowing the range of investment financing options available to coal projects.’ While for gas, the ‘impact of COVID-19 on oil and LNG prices has occurred against a backdrop of an existing global LNG supply glut, which has led to the deferral of FIDs for several large offshore projects that were originally expected in 2020 or 2021.’

DFAT Secretary Frances Adamson’s speech to the ANU’s national security college on the evolving strategic landscape. According to Adamson, in the next ten years, ‘the key question for Australia will be how successful are we at pursuing our national interest in this tougher, riskier environment, defined by strategic competition’…and ‘The main challenge for Australia's foreign policy is one of shaping, with other countries, a regional and global order that responds to the new realities of power.’

China imposes ‘devastating’ tariffs on Australian wine.

Potential costs of an Australia-China trade war – perhaps six per cent of GDP in a worst case scenario, according to Rod Tyers and Yixiao.

Related, Hugh White on the ‘hard choices and compromises’ he thinks will be required to manage the relationship with Beijing, one that will have to be characterised by ‘the cold, hard calculus of advantage.’

The ABS has produced new estimates for Multifactor Productivity (MFP) for 2019-20, showing market sector MFP fell 0.7 per cent measured on a market hours basis, while gross value added (GVA) for the market sector fell 1.2 per cent. This marks the first decline in market sector MFP in the history of the series, which goes back to 1994-95. In contrast, labour productivity rose 0.6 per cent as the 1.7 per cent fall in hours worked outpaced the decline in GVA. Ten out of 16 market sector industries recorded a fall in MFP in 2019-20 with the largest falls coming in Agriculture, forestry and fishing (down 8.3 per cent reflecting drought conditions), and Administrative and support services (down 7.8 per cent due to the impact of the pandemic), while the largest growth in MFP was in Mining (up 3.7 per cent with strong output growth) and in Retail trade (up 3.6 per cent reflecting a large drop in hours worked). There is also an accompanying article on measuring productivity during a pandemic.

Latest news

Already a member?

Login to view this content