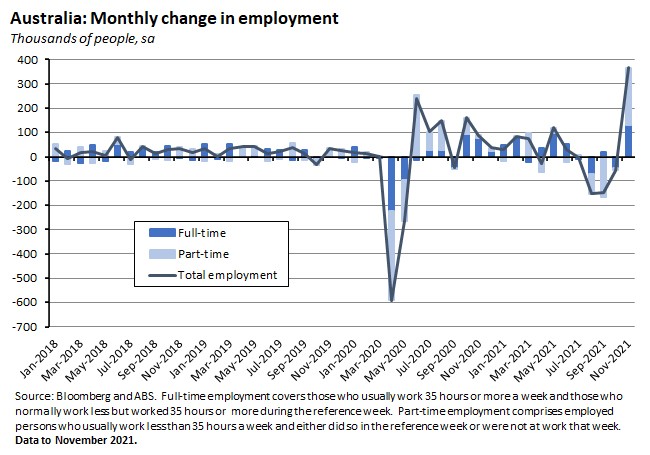

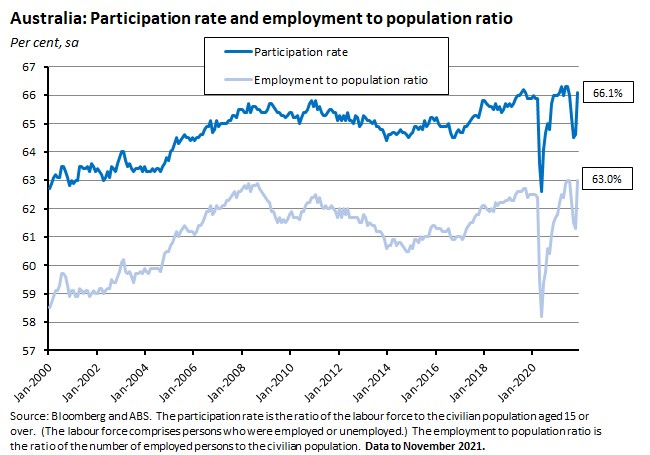

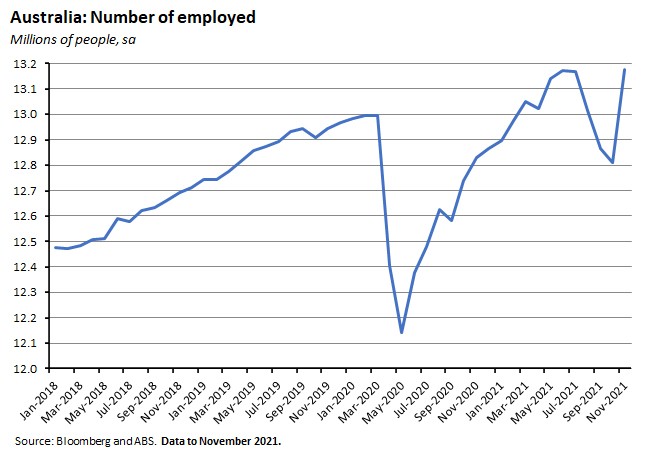

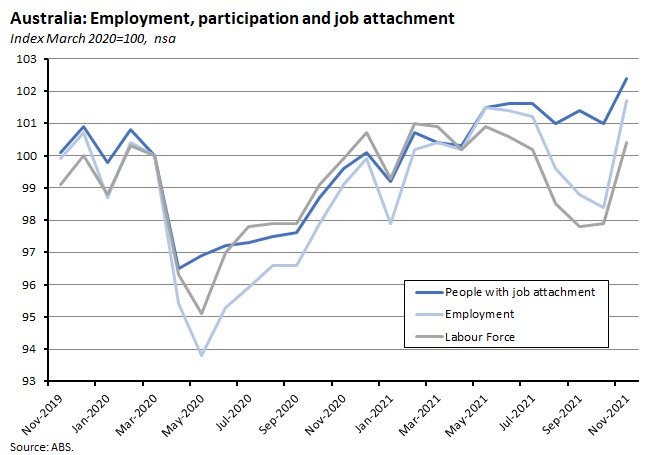

The number of employed people soared by a record 366,100 in November this year, smashing consensus expectations for an already-robust 200,000 increase. In an extremely strong labour force report, hours worked rose by 4.5 per cent, the participation rate jumped by 1.4 percentage points and the employment to population ratio climbed by an even larger 1.8 percentage points.

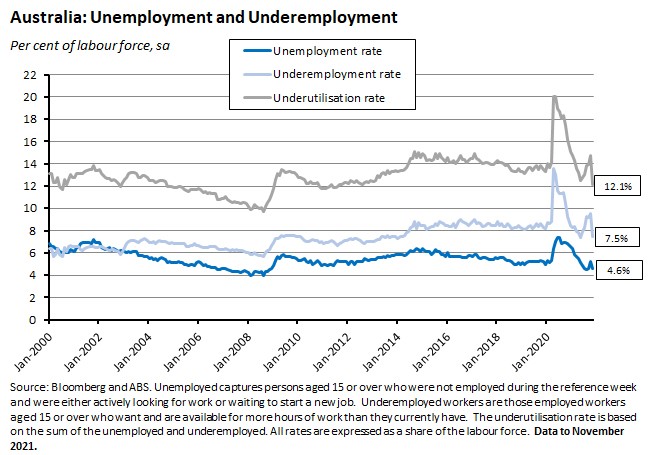

The unemployment rate fell from 5.2 per cent in October to 4.6 per cent last month, the underemployment rate dropped by two percentage points to 7.5 per cent, and the underutilisation rate tumbled to 12.1 per cent, its lowest rate since mid-2012. High levels of job attachment appear to have helped generate a super-charged labour market recovery in November after New South Wales (on 11 October 2021), the ACT (on 15 October 2021) and Victoria (on 22 October 2021) exited from lockdown over the course of the previous month. For more detail, see below and also take a look at the updated labour market chart pack which also includes new information from the Characteristics of Employment release that also appeared this week.

The Mid-Year Economic and Fiscal Outlook (MYEFO) provides an update on the fiscal position that combines the impact of events since May’s budget – the drag on activity from Delta lockdowns but also higher than forecast commodity prices and lower than forecast unemployment – and from revisions to Treasury’s forecasts of the economy. The new projections are relatively upbeat: they assume that national and international borders will continue to re-open, that large-scale lockdowns are now behind us, and that the Omicron variant won’t derail things the way that Delta did. The net impact of all this on the budget bottom line is surprisingly modest, however, as a big increase in projected receipts is largely offset by a rise in expected spending. As a result, the cumulative underlying cash balance over the forward estimates period is expected to be just $2.3 billion smaller than in the original budget projections. Debt is also projected to be somewhat lower although the associated interest burden is little changed thanks to a modest rise in the assumed yield on government bonds.

The AICD’s own Director Sentiment Index (DSI) for H2:2021 was also released this week, capturing the views of more than 1,600 directors. A summary report and the full research report are both available. The polling that supports the DSI was conducted between 28 October and 8 November this year, so it came after New South Wales, Victoria and the ACT had all exited from their lockdowns. It also took place during COP26 (which ran from 31 October to 12 November 2021) and after the government had announced its Long Term Emissions Reduction Plan on 26 October, but before the release on 12 November of the modelling underpinning that Plan. Importantly, it also preceded the announcement by the World Health Organisation on 26 November that Omicron was a variant of concern.

The DSI reports that (pre-Omicron at least) Directors were feeling optimistic about the next 12 months, with 67 per cent judging that the economic outlook for the coming year was strong and 64 per cent also expecting positive business conditions, although there were significant variations by state. Strikingly, our respondents cited labour shortages as the most important economic challenge now facing Australian businesses, ahead of COVID-19, climate change, the Australia-China relationship and global economic uncertainty. Climate change was identified as the issue that should be top of the government’s short-term (next three years) and long-term (next 10-20 years) priority list. Fifty per cent of directors said that climate change was a material risk for their organisation, and 49 per cent said that uncertainty around climate change policy settings was the most important barrier they faced with regard to climate governance. Cybersecurity is the issue that keeps the greatest number of DSI respondents awake at night. And directors have a nuanced view on the working from home revolution: a majority think it is positive for staff retention, attracting new staff and for staff health and wellbeing but also judge that it is negative for cybersecurity. And one last noteworthy result: 76 per cent of respondents agreed with the proposition that business should make COVID-19 vaccines mandatory for staff in their sector, with only 12 per cent disagreeing.

For a review of some of the other key data releases in what was a busy week, including flash PMI estimates for December, the NAB Business Survey for November, and the latest Westpac and ANZ-Roy Morgan consumer confidence readings, see below.

This week’s linkage comprises a roundup of yet more ABS data releases (overseas arrivals and departures, finance and wealth, population, and productivity, as well as tourism statistics from last Friday), two speeches from the RBA including an update on the likely future of the central bank’s bond-buying program (the central case scenario is for another taper in February 2022 followed by an exit in May), the Productivity Commission on pricing public transport after the pandemic, trust in scientists, some summer reading recommendations, lessons from Japan, the importance of inflationary expectations, green energy and a non-flat world, a dose of techno-optimism, and did 2021 change investing forever.

This will be the final update of 2021, and the weekly will now be off on an extended summer holiday until February. Many thanks to you all for following these updates over the past year and thanks also to those of you who listen to the Dismal Science podcast. Until next year, I wish you and yours a happy and peaceful holiday season. I’ll be back with a new webinar on 8 February when we’ll discuss what 2022 might have in store.

Listen and subscribe to our podcast: Apple Podcasts | Google Podcasts | Spotify

What I’ve been following in Australia . . .

What happened:

The ABS said that Australia’s employment surged by 366,100 people (seasonally adjusted) in November this year. Full-time employment increased by 128,300 and part-time employment rose by 237,800. The part-time share of employment was 31.3 per cent, up from 30.3 per cent in October.

Hours worked in all jobs last month rose by 4.5 per cent (76.7 million hours). The number of people working zero hours for economic reasons – that is, due to no work, not enough work available or being stood down – fell by more than 110,000, dropping to 78,500.

The unemployment rate declined from 5.2 per cent in October to 4.6 per cent in November, while the underemployment rate dropped by two percentage points, from 9.5 per cent to 7.5 per cent. As a result, the underutilisation rate fell by 2.6 percentage points to 12.1 per cent.

Both the participation rate and the employment to population ratio jumped in November, with the former rising from 64.6 per cent in October to 66.1 per cent and the latter up from 61.3 per cent to 63 per cent.

By state and territory, there were large gains in employment and hours worked, along with correspondingly large drops in unemployment and underemployment, in New South Wales, Victoria, and the ACT. All three geographies also saw significant increases in their participation rates and employment to population ratios.

For charts on the state results and for more on the labour market in general, see the latest version of our labour market chart pack.

Why it matters:

A run of relatively strong payroll data (until the most recent reading) along with other positive labour market indicators had seen the market consensus predict a robust gain of 200,000 jobs in November as the economies of New South Wales, Victoria and the ACT had all re-opened over the course of the previous month. The actual outcome was significantly better than that, setting a new record for monthly job gains. Of the outsized 366,100 gain, New South Wales accounted for 180,000 and Victoria for a further 141,000. Total employment is now 181,800 people (1.4 per cent) above its pre-pandemic (March 2020) level.

The unemployment rate, the underemployment rate and the underutilisation rate are all now considerably lower than they were pre-pandemic, and the underutilisation rate has fallen to its lowest rate since August 2012. What makes this achievement even more impressive is that it coincided with a large rebound in the participation rate. Last month’s analysis of October labour market data had cautioned that there could be something of a tug-of-war between the positive impact on the unemployment rate of the likely gains in employment arising from state reopening on the one hand and the expansion of the labour force due to rising participation rates on the other. In the event, the scale of the recovery in employment demand has allowed November to comfortably deliver increases in employment, in hours worked and in labour market participation all alongside falling unemployment and underemployment.

The dramatic nature of the labour market recovery from the September quarter 2021 Delta lockdowns is even more impressive than the one that followed the recovery from the 2020 lockdowns, which at the time was seen as unexpectedly rapid. An important part of the story likely relates to job attachment, which the ABS had highlighted in last month’s release. This term refers to whether someone has a job that they are connected to, and importantly it is possible for someone to have such an attachment without necessarily being classed as employed. Pre-pandemic, this status applied to a relatively small group of people – people with a job but who were on leave without pay for more than a month (e.g. unpaid parental leave) and people who had a job but hadn’t yet started or restarted work. During the pandemic, however, a large number of people worked reduced or no hours due to lockdowns but remained attached to their job. So, while in March 2020 there were 189,000 people who considered they had a job that they were attached to, but who weren’t classed as employed, by May 2020, the pandemic had seen this number jump to 592,000. It then dropped back to pre-pandemic levels during the first half of this year. During the Delta lockdowns, the Bureau reports that this number again rose sharply, peaking at 531,000 in October 2021.

The ABS estimates that job attachment was even higher in the Delta period than in the 2020 lockdowns. For example, between March and May 2020 the number of employed people fell 6.2 per cent and the number of people in the labour force (the sum of the employed and unemployed) fell 4.9 per cent, but the share of people who considered they were attached to a job ‘only’ fell by 3.1 per cent. The Delta period then shows a similar pattern but with an even larger gap: between May 2021 and October 2021, the number of employed people fell 3.1 per cent while the number of people in the labour force fell three per cent, but the number of people who considered they were attached to a job dropped by just 0.5 per cent.

The Bureau suggests that this high level of attachment looks to have been a key factor in the rapid recovery in both employment and participation in November, by allowing people who already had a job attachment to return to work very quickly.

What happened:

The Mid-Year Economic and Fiscal Outlook (MYEFO) 2021-22 set out the updated economic and fiscal outlook for the Australian economy relative to the 11 May 2021 budget.

The new economic projections underpinning the MYEFO see the Australian economy growing at 3.75 per cent in 2021-22 and at 3.5 per cent in 2022-23 before growth moderates in the final two years of the forward estimates. That means that real GDP growth will be lower than had been expected at the time of the budget in 2021-22 (the budget had predicted 4.25 per cent growth but that forecast was derailed by the economic hit from the Delta variant and the subsequent state shutdowns) and then considerably stronger in 2022-23 (up from 2.5 per cent in the budget forecasts).

There are also significant upgrades to the projections for the unemployment rate (from five per cent and 4.75 per cent for 2021-22 and 2022-23 in the budget forecasts to 4.5 per cent and 4.25 per cent in the MYEFO, respectively) and for the rate of growth of the Wage Price Index (up from 1.5 per cent and 2.25 per cent to 2.25 per cent and 2.75 per cent over the same period). Inflation forecasts have also been adjusted up, as have population growth projections. Australia’s terms of trade are now expected to plateau in 2021-22 before falling back by 18 per cent in 2022-23 as commodity prices retreat from their current elevated levels. The terms of trade hit a record high in the September quarter of this year – more than eight per cent higher than in the budget forecasts – reflecting high prices for iron ore, coal and LNG.

The overall result of these and other changes is that growth in nominal GDP – which reflects the size of the tax base – is now projected to grow by a much stronger 6.5 per cent in 2021-22 compared to a budget forecast of 3.5 per cent. The pace of growth is then expected to ease to 1.25 per cent in 2022-23 compared to the budget’s earlier projection of two per cent growth.

The assumptions underlying these economic projections include: that Australia’s vaccination program will have more than 90 per cent of the over 16 population vaccinated by year-end (the ratio was already at 89.9 per cent at the time of writing); that major lockdowns are no longer required to manage COVID-19 and that any temporary strengthening of activity restrictions will not materially impact the economic outlook; that all remaining state border restrictions are lifted by early 2022; that there is a gradual return of temporary and permanent migrants from early next year; and that the Omicron variant ‘is not assumed to significantly alter current reopening plans or require a reimposition of widespread health and activity restrictions.’

The combination of a stronger than expected labour market recovery, and higher than anticipated commodity prices and asset prices means that tax receipts are set to be exceed the levels assumed in the May budget (up by a hefty $95 billion over the four years to 2024-25 thanks largely to an extra $45 billion in personal income tax receipts and an additional $37 billion of company tax receipts) even as unemployment benefit payments are set to be lower (jobseeker payments are projected to be some $4 billion lower over the forward estimates compared to the original budget forecasts).

Overall, total budget receipts are now projected to be $50.1 billion higher in 2021-22 and $109.1 billion higher over the four years to 2024-25 relative to the assumptions made back in May. However, on the payments side of the government accounts, total payments have likewise been revised up, in this case by $42.7 billion in 2021-22 relative to the budget, and by $106.8 billion over the forward estimates as a whole.

With payments projected to increase by almost as much as receipts, those stronger than expected economic outcomes for nominal GDP and the labour market do not translate into substantial gains in the underlying cash deficit relative to the original budget projections. Granted, the projected deficit has narrowed by $7.4 billion in 2021-22 but it is then little changed over the remainder of the forward estimates, with a net improvement of just $2.3 billion over the entire four years – a cumulative shortfall of about $340 billion over the forward estimates instead of the $342.4 billion predicted in the budget papers. As result, the MYEFO sees the deficit at 4.5 per cent of GDP (instead of five per cent) in 2021-22, but by 2024-25 the MYEFO has the deficit at 2.3 per cent of GDP vs 2.4 per cent in the May 2021 budget numbers.

The implications of this changed deficit profile for government debt are that net debt is now projected to be $673.4 billion (30.6 per cent of GDP) in 2021-22, down from the budget’s assumption of $729 billion (34.2 per cent). By 2024-25, net debt to GDP is now expected to have risen to 37.4 per cent under the MYEFO instead of the 40.9 per cent budget estimate for that year.

That lower debt stock does not make much difference to projected interest payments, however, as the effects of less debt are broadly offset by a modest increase in the assumed yield on government bonds, which now assumes a weighted average cost of borrowing for future issuance of around 1.7 per cent compared with around 1.6 per cent in the budget. The overall effect is to leave net interest payments steady at 0.7 per cent of GDP over the forward estimates.

Why it matters:

The MYEFO update reflects a combination of the overall impact of economic developments since the May budget plus changes to Treasury’s forecasts for the next four years. The period between the budget and the MYEFO brought one big negative shock in the form of the hit to the economy from the Delta variant that saw Australia suffer the third largest quarterly fall in GDP on record. But it also saw a range of positive changes including higher than expected commodity prices and lower than expected unemployment rates. At the same time, the official forecasts for the economy overall have become more optimistic: unemployment will be lower, and population and wage growth higher than previously assumed. The MYEFO also assumes that the days of large lockdowns are behind us, and that the Omicron variant will not derail the economy. The net impact of all this on the new fiscal projections presented in the MYEFO is a big boost to projected revenues, although this has been almost entirely offset by a similarly sized boost to projected spending. That means the MYEFO leaves the budget bottom line little changed, with only a very modest decline in the cumulative underlying cash deficit predicted for the four years of forward estimates.

Where is the increased spending coming from? A sizeable chunk of it reflects COVID-19 related measures already taken in response to the Delta-shock, which are estimated to have reduced the underlying cash balance by $25 billion over the forward estimates. Another big chunk comes in the form of a large upward revision to payments relating to the NDIS, which are expected to rise by $26.4 billion over the forward estimates. And a third chunk relates to nearly $16 billion of spending under ‘Decisions taken but not yet announced and not for publication’, some of which reflects items such as pending vaccine purchases, but a fair bit of which likely relates to spending commitments that will be announced in the run-up to the pending election (the ‘election war chest’ of newspaper headlines).

What happened:

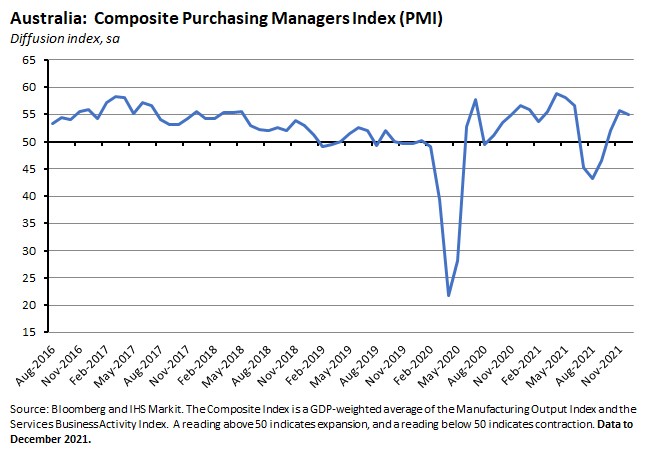

The IHS Markit Flash Australia Composite PMI edged down to 54.9 in December from 55.7 in November. (Flash responses are based on around 85 per cent of final survey responses and provide an advance indication of the final readings.)

According to the survey provider, private sector output and demand growth were both sustained at solid levels this month, albeit down slightly from November, while employment levels rose at a faster rate. Input cost and output price inflation both rose at record rates in December as supply issues persisted, with respondents saying lead times again lengthened while shortages continued. Faster input cost inflation reflected higher costs across materials, shipping and wages.

The IHS Markit Flash Australia Services PMI slipped from 55.7 in November to 55.1 in December while the Manufacturing PMI fell from 59.2 to 57.4 over the same period.

Why it matters:

After three large consecutive monthly rises, this was the first decline in the Composite PMI since August this year, although this month’s modest retreat still left the index firmly in positive territory. The Composite and Services PMIs have now been above neutral for the past three months.

Overall, the December result indicates that economic activity continues to increase at a robust pace, although momentum has eased relative to November. The PMI results are also still signalling that businesses are facing significant supply-side challenges, at least some of which are likely driven by the adjustment difficulties associated with re-opening.

What happened:

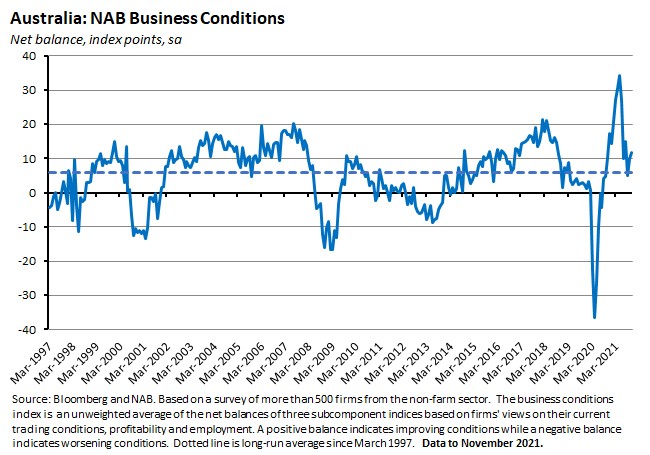

The November 2021 NAB Monthly Business Survey was released this week. Business Conditions rose two points to +12 index points last month after having jumped by five points in October.

By industry, business conditions were up strongly in retail (up 14 points), transport and utilities (up 12 points) and finance, property and business (up eight points) but fell in construction (down eight points).

By state, business conditions rose in Queensland (up six points), South Australia (up four points) and Victoria (up two points) but were unchanged in New South Wales and Western Australia and down in Tasmania (a six point drop).

Of the three components of the Conditions index, employment was the main driver of the overall increase, rising by five points to +11 index points. The trading conditions index was up one point and profitability unchanged.

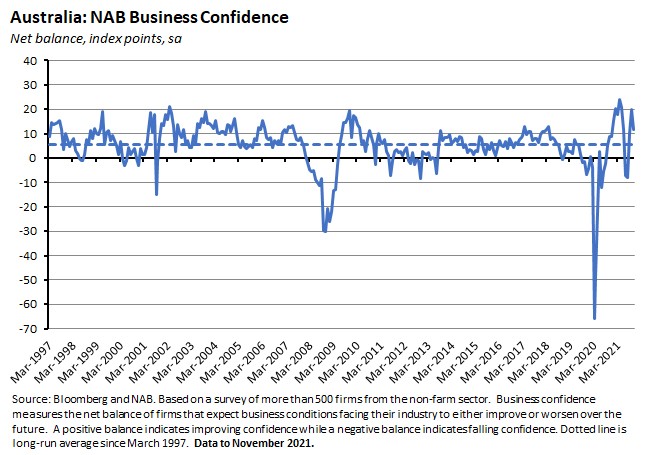

Business confidence retreated by eight index points last month, falling from +20 index points in October to +12 in November.

By industry, business confidence eased across most sectors in November and confidence also retreated from the very strong October readings across New South Wales, Victoria and South Australia, although it did rebound in Tasmania.

The capacity utilisation rate rose to 83.2 per cent in November from 81.2 per cent in October while the Forward Order index slipped one index point to +14 index points.

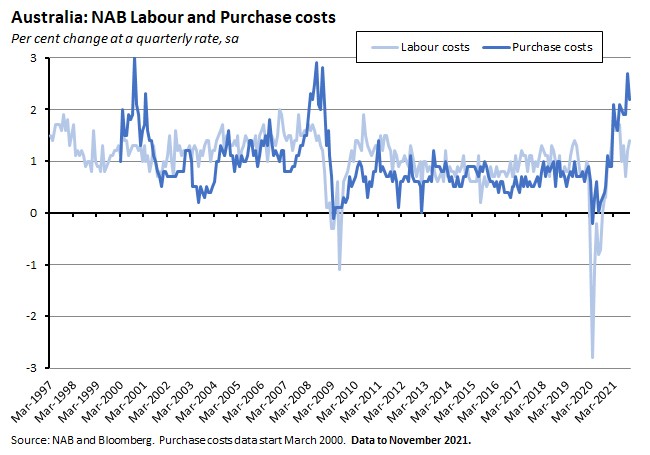

The quarterly pace of increase in labour costs accelerated again in November, rising to 1.4 per cent from 1.2 per cent in October, although the rate of increase in purchase costs eased to 2.2 per cent from a record 2.7 per cent in the previous month.

Why it matters:

After a very strong result in October, business conditions again strengthened in November albeit by a more modest amount, suggesting some levelling-off in the post-lockdown bounce. At the same time, although business confidence retreated from the previous month’s reading it still remained comfortably above the series average.

With the RBA focused on faster wage growth as a precondition for a sustainable return of inflation to the target range (and therefore for a normalisation of monetary policy), analysts are keeping a close eye on any signs of rising wage pressures. In this context, another monthly increase in the reported quarterly rate of growth in labour costs is worth noting. However, NAB pointed out that the growth in labour costs reflects the combined impact of increases in employment plus any rise in hourly wages, and added that in most sectors, the reported increase in labour costs was associated with a rise in employment (with the notable exception of construction where employment fell while costs still increased).

What happened:

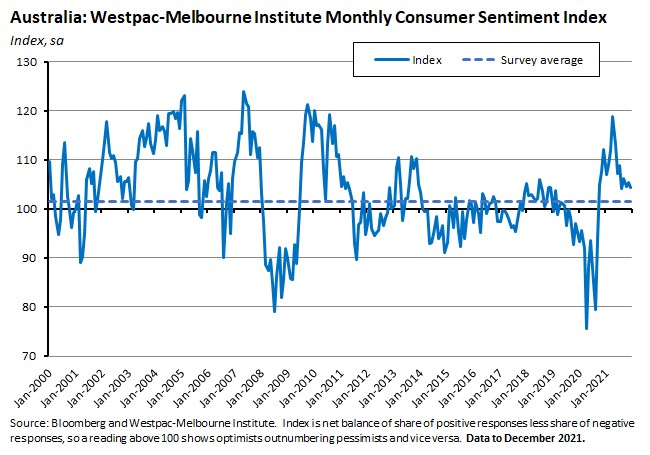

The December 2021 Westpac-Melbourne Institute Index of Consumer Sentiment (pdf) fell by one per cent.

Three of the five subindices fell this month: ‘time to buy a major item’ slumped 5.3 per cent over the month, while ‘economic outlook, next 12 months’ slipped 1.6 per cent and ‘economic conditions, next five years’ edged 0.5 per cent lower. In contrast, the ‘finances, next 12 months’ subindex rose 2.1 per cent while ‘finances vs a year ago’ rose one per cent.

Separately, the Unemployment Expectations Index jumped by 9.3 per cent, indicating a rise in the share of households expecting the unemployment rate to increase over the coming year.

The Index of House Price Expectations fell 1.3 per cent and the ‘Time to buy a dwelling’ index suffered a sharp 10.2 per cent fall.

Why it matters:

December’s fall in consumer sentiment still leaves the Index comfortably in positive territory, but it also suggests that households have become more cautious following news of the Omicron variant. Westpac notes that there was a clear difference this month in survey responses between those states hit hardest by the Delta outbreak and the rest. In particular, sentiment was down in New South Wales (a 3.6 per cent drop) and Victoria (a 3.5 per cent fall) but up in Queensland (a 3.4 per cent rise), Western Australia (3.2 per cent) and South Australia (7.1 per cent). It speculates that the ‘Delta states’ may be more sensitive to virus news than the rest of Australia.

Westpac also reported that consumers have become increasingly aware of developments around inflation and interest rates, and as noted above, the Unemployment Expectations index also indicated some cooling in earlier optimism regarding the labour market. That said, the index remains well below the series average, signalling a strong labour market overall.

Finally, housing affordability considerations appear to be influencing the appetite for dwelling purchases.

What happened:

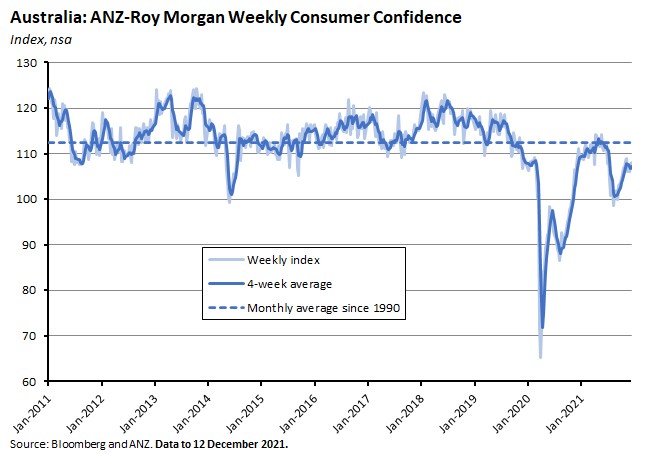

ANZ-Roy Morgan Consumer Confidence rose 0.5 per cent last week.

Four of the five subindices rose over the week, with the only decline registered for ‘future financial conditions’ which dropped 1.2 per cent.

Weekly inflation expectations fell 0.2 percentage points to 4.7 per cent.

Why it matters:

The small change in the overall index disguised some much larger moves at the state level, where there were gains in confidence for Queensland (up 5.2 per cent), South Australia (up 8.8 per cent) and Western Australia (up 4.1 per cent) that together only just offset a sharp fall in confidence in New South Wales (down 5.5 per cent). Confidence in Victoria was little changed (up just 0.1 per cent). ANZ said that the drop in sentiment in New South Wales likely reflected the marked increase in COVID case numbers at the weekend.

What happened:

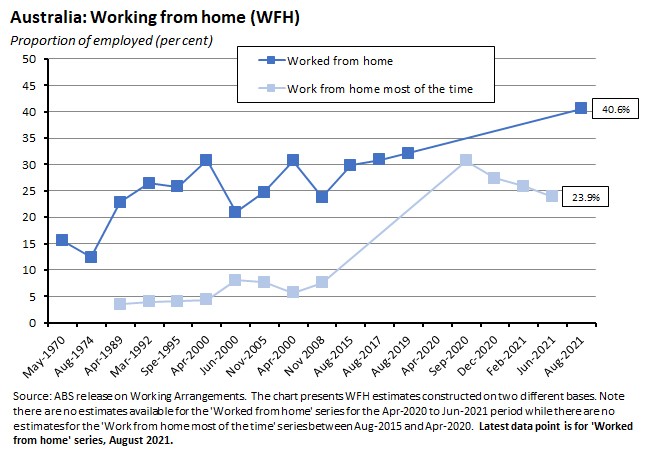

The ABS released Characteristics of Employment, Australia, with data up to August 2021. Notable results included:

- More than 40 per cent of employed people (40.6 per cent) were regularly working from home during the first half of August this year. That was up from 32.2 per cent in August 2019, before the pandemic.

- There were 2.4 million casual employees in August 2021, equivalent to 22.5 per cent of all employees and 19 per cent of all employed. That was down from 24.1 per cent of employees in February 2020, pre-pandemic.

- The distribution of weekly earnings saw the number of employed people earning less than $1,000 / week fall by almost half a million relative to pre-pandemic levels, dropping from 4.5 million in August 2019 to a bit over four million in August 2021. That shift reflects the fact that lower paid workers and their roles were particularly hit by lockdowns.

Other data on employee earnings showed median employee earnings was $1,200 per week in August 2021, up 4.3 per cent ($50) since August 2020, although median hourly earnings were unchanged at $36 per hour over the same period.

For more detail, see the ‘selected other charts’ section in the labour market chart pack.

Why it matters:

This selection of ABS data updates shows how the pandemic has reshaped the labour market by leading to changes in working arrangements, in the distribution of earnings, and in the share of casual employment.

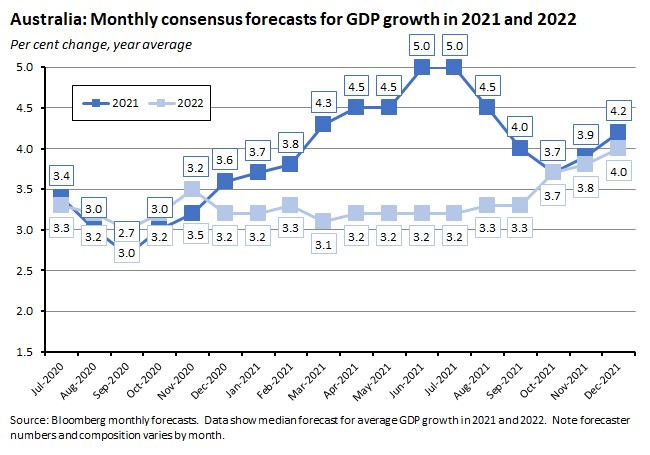

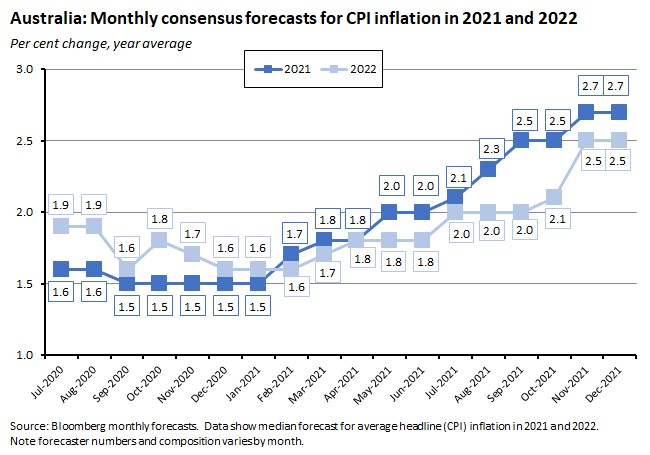

What happened:

The Bloomberg December 2021 roundup of market forecasts showed expectations for real GDP growth this year have increased in the aftermath of the smaller-than-expected decline in the third quarter, with the median forecast rising from 3.9 per cent in November to 4.2 per cent this month. Growth expectations for next year have also edged higher, rising from 3.8 per cent to four per cent.

On the inflation front, the median forecasts for this year and next were unchanged at 2.7 per cent and 2.5 per cent respectively.

That combination of stronger growth forecasts and no change on inflation expectations saw December’s median projection for the cash rate profile become somewhat more aggressive for 2023. In the November survey, the consensus had been that the cash rate would stay unchanged at 0.1 per cent through next year but then increase to 0.25 per cent in Q1:2023 before rising again to 0.5 per cent in Q3:2023, to 0.75 per cent in Q4:2023 and to one per cent by Q4:2024. December’s survey still sees a 0.25 per cent cash rate arriving in Q1:2023 but then brings the next projected 25bp increase in the cash rate forward to Q2:2023 and the one after that (taking the cash rate to 0.75 per cent) to Q3:2023.

Why it matters:

The Bloomberg survey of economists (which was conducted from 9 to 14 December) indicates that the consensus broadly shares the RBA’s assessment from last week and Treasury’s assessment in the MYEFO that the Omicron variant will not derail Australia’s economic recovery.

Linkage . . .

- As well as the releases discussed above, there were several other data drops from the ABS this week. For example, the Bureau released data on overseas arrivals and departures for October 2021, which showed total arrivals falling by 3,110 trips over the month to 15,730. Total departures rose by 6,490 trips to 36,820. By way of comparison, total arrivals in October 2019, pre-pandemic, exceeded 1.9 million and total departures were close to 1.7 million. Total visitors arriving in Australia in 2020-21 were down 97.8 per cent over the year while resident returns over the same period were down 97.4 per cent. Provisional data for November this year put arrivals at more than 73,000 and departures at almost 93,000.

- New national accounts data from the ABS on Finance and Wealth reported that household wealth rose $590 billion (4.4 per cent) to a record $13,918.5 billion in the September quarter of this year while wealth per capita also rose to a record high of $540,179. Residential property assets accounted for the bulk (3.5 percentage points) of the quarterly growth in household wealth, along with increases in currency and deposits. The Bureau said that the $72 billion increase in deposits in Q3:2021 was the largest on record, boosted by government support payments.

- ABS data on national, state and territory population showed Australia’s population was 25.7 million people at 30 June this year. Annual population growth was 0.2 per cent or 46,000 people which comprised 134,800 from natural increase and a fall of 88,000 from net overseas migration. The ABS also released a special article on 50 years of estimated resident population, noting that Australia’s population has almost doubled over the past half century, rising from almost 13.1 million in 1971 to 25.7 million in 2021.

- The ABS also published estimates of multifactor productivity (MFP) for the 2020-21 financial year. MFP is defined as the ratio of gross value added to the combined input of labour and capital. The Bureau said that market sector MFP rose just 0.2 per cent in 2020-21 as gross value added grew 0.6 per cent, inputs of capital rose 1.4 per cent and inputs of labour fell 0.5 per cent. Market sector labour productivity rose 1.1 per cent. (The market sector excludes the public administration and safety, education and training and health care and social assistance industries, where the majority of output is provided either free of charge or at non-market determined prices). By industry, the strongest growth in MFP was in agriculture, forestry and fishing and in wholesale trade while the biggest declines were in transport, postal and warehousing and arts and recreation services.

- Completing the roundup of ABS numbers, last Friday, the Bureau released the Tourism Satellite Account for 2020-21. Real tourism GDP plummeted by almost 38 per cent over the year while real gross value added tumbled by more than 39 per cent. The number of employed persons fell by more than 20 per cent, hours worked dropped by more than 19 per cent and gross value added per hour worked slumped by almost 25 per cent. The share of tourism in total employment fell to 3.9 per cent, the lowest recorded in the 17-year history of the published time series, and the ABS said that all tourism key statistics fell to their lowest level since at least 2005-06, reflecting the fact that tourism was disproportionately adversely affected by the pandemic.

- Two speeches from the RBA this week. First, Governor Philip Lowe gave an address on the RBA and the Australian economy. He suggested that when the RBA meets again in February to consider the future of its asset purchase program, it will likely choose from three options: (1) further taper bond purchases from the current $4 billion weekly rate with an expectation they would then cease altogether in May 2022; (2) further taper purchases and then review the program again in May; and (3) cease bond purchases altogether in February. Lowe noted that option (1) was ‘broadly consistent’ with the RBA’s baseline forecasts, with (2) and (3) relevant in the case of downside and upside surprises, respectively. The governor also reminded his listeners that in the RBA’s central scenario ‘the condition for an increase in the cash rate will not be met next year.’ Second, Jonathan Kearns, Head of Financial Stability, spoke on Evolving Bank and Systemic Risk. Kearns noted that alongside core banking risks such as market risk, credit risk (smaller than expected after the pandemic led to much smaller than anticipated losses), liquidity risk and operational risk (now rising in line with increasing size and complexity of some institutions) there are also important emerging risks, led by climate change and cyber risk.

- The ACCC says that the cost of supplying electricity to households has fallen to an eight-year low, although it also notes that real electricity costs today are still 32 per cent higher than they were in 2007-08. For small businesses, the costs are the lowest in five years, and for large businesses the lowest in four years.

- The Parliamentary Budget Office (PBO) provides an Explainer on the Contingency Reserve, which is an allowance within the government’s budget forecasts for items that either cannot or should not be allocated to specific programs at the time of publication. It includes a Conservative Bias Allowance (CBA) which provides for the historical tendency for the estimates of expenses for existing government policy to be under-estimated and a measure to capture the value of new policy decisions taken but not yet announced (DTBNYA). According to the PBO, DTBNYA have increased significantly in size since they started to be disclosed on a consistent basis from 2004-05. And see the MYEFO discussion above for another example of this trend.

- A new Productivity Commission research paper on public transport pricing. The starting point is that ‘COVID-19 has decimated public transport patronage and revenue in all Australian cities. The recovery period provides time for state and territory governments to re-think how they price and deliver sustainable public transport services.’ It argues that a better approach to pricing ‘would recognise that peak charges should be higher and timed to make improved use of transport assets, prices should better reflect that buses are less costly than trains, and longer distances travelled should come with higher prices’, and that ‘concessions are inadequately targeted.’ It also notes the case for road user charges and parking levies.

- Last week’s linkage included another Productivity Commission research paper, this one on wealth transfers. Richard Holden reckons that those findings mean that the case against death duties just got stronger while the AFR thinks it actually boosts the case for a modest inheritance tax as part of a broader package of tax reforms.

- Trust in scientists during the pandemic. The interaction with trust in government is interesting.

- Elon Musk is the FT’s person of the year.

- The Economist magazine’s best books of 2021. I’ve only read two of these, Empire of Pain and The World for Sale. Ishiguro’s Klara and the Sun is on my wish list for summer holiday reading.

- Also from the Economist, a special report on what the world can learn from Japan, a country that is ‘on the front line’ in terms of demographic change, US-China competition and natural catastrophes. Related, the Free Exchange column on why the demographic transition is accelerating: ‘demographic contagion.’

- From Wired: the office is an efficiency trap.

- A WSJ long read on the importance of inflationary expectations.

- From Brookings: a new report on the emerging global gas market and the 2021-22 energy crisis.

- Ricardo Hausmann argues that green energy sources do not lend themselves to a ‘flat’ world. Instead, energy-intensive activities will again have to take place near specific locations, with the winners from decarbonisation ‘those that combine geographic luck with smart action…countries that want to benefit from the relocation of energy-intensive industries will need to ensure that they can credibly offer access to green energy.’

- Noah Smith offers up some techno-optimism for 2022.

- Bloomberg Businessweek asks, has 2021 changed investing forever?

- Also from Bloomberg, the biggest risks for 2022: the list includes Omicron and more lockdowns, inflation risk, Fed rate hikes, emerging market vulnerability, a China slump, political turmoil in Europe, Food prices and unrest, geopolitical risks from Taiwan to Ukraine, and even the possibility of some nice surprises such as faster than expected Asian and global growth.

Latest news

Already a member?

Login to view this content