A relatively quiet week for Australian data ahead of next week’s GDP report. ‘Flash’ Purchasing Manager Index (PMI) estimates for November show Australian business activity rising at its fastest pace since July this year with both services and manufacturing expanding.

The ANZ-Roy Morgan weekly index of consumer confidence ended its record run of 11 consecutive weekly rises. Private capital expenditure fell again in Q3, further extending the downturn in business investment. Total construction work done also declined in the September quarter. Consensus growth forecasts for Australia have been upgraded again. Iron ore exports hit a new record high in October, proving immune to Australia-China trade tensions. Last week, preliminary retail sales numbers for October suggest that consumer spending got off to a decent start in Q4. ABS business survey results point to improving business optimism. Cross-country GDP readings paint a mixed picture for Q3 with varying degrees of recovery across the global economy. And world merchandise trade volumes have enjoyed a strong rebound.

This week’s readings include RBA analysis of the JobKeeper program, the latest Household, Income and Labour Dynamics in Australia (HILDA) Survey, insights on Australia’s long-run productivity performance, the economics of vaccines, lessons from Japan’s experience with low growth, low inflation and low interest rates, do ultra-low interest rates ‘unmoor’ political debate, and are we heading back to an Eighteenth Century style relationship between capitalism and politics?

What I’ve been following in Australia . . .

What happened:

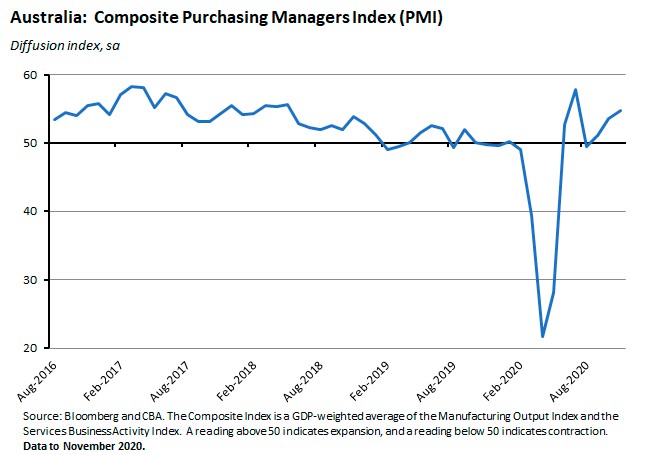

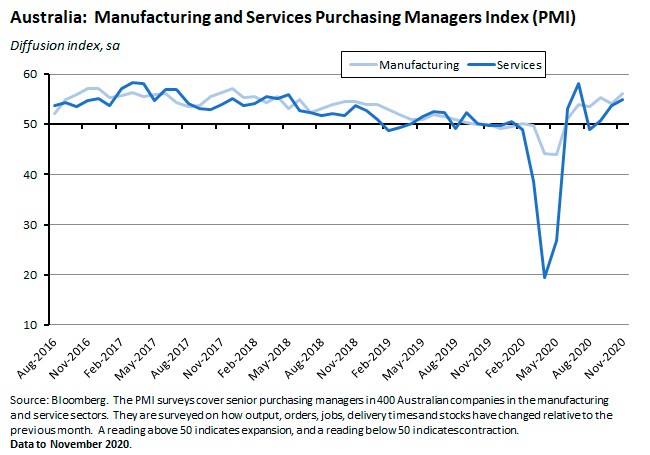

The IHS Markit Flash Australia Composite PMI rose (pdf) to 54.7 in November.

The Services PMI rose to 54.9 while the Manufacturing PMI increased to 56.1.

Why it matters:

The Composite and Services Flash PMIs both hit four-month highs in November while the Flash manufacturing PMI rose to a 35-month high. With both services and manufacturing indicators heading further into positive territory this month, the PMI readings are indicating a broad-based pick up in business activity in the final quarter of this year.

What happened:

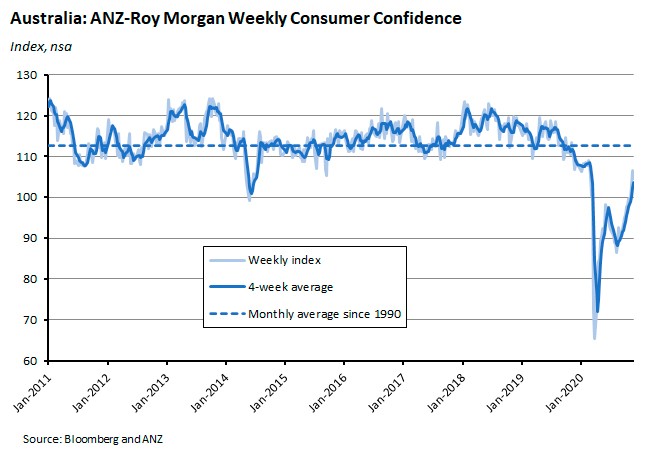

The ANZ-Roy Morgan weekly measure of consumer confidence fell two per cent to an index reading of 104.5 for the weekend of 21-22 November.

Four out of the five component subindices fell over the week, with declines for ‘current financial conditions’, ‘current economic conditions’, ‘future economic conditions’ and ‘time to buy a major item’ with the biggest decline suffered by ‘current financial conditions’ (down 4.5 per cent). The ‘future financial conditions’ subindex was unchanged.

Why it matters:

The record-breaking run of 11 consecutive weeks of rising confidence has now come to an end. The main culprit was likely the news of South Australia’s three-day lockdown, which saw the state index fall into negative territory even while the national index remained above the neutral reading of 100. But with the lockdown in SA being shorter than initially anticipated, the reversal in confidence may prove temporary.

What happened:

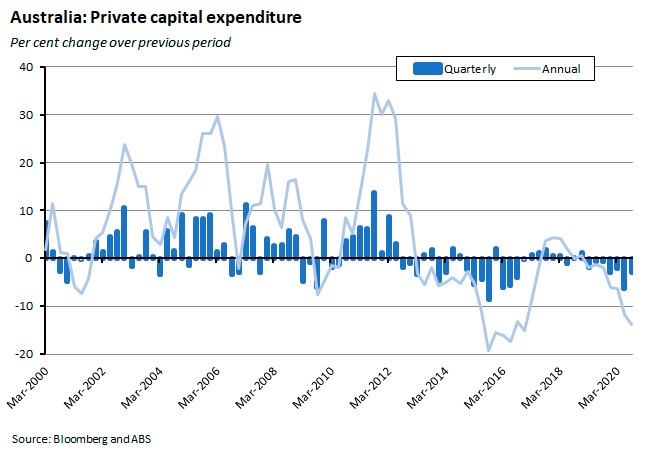

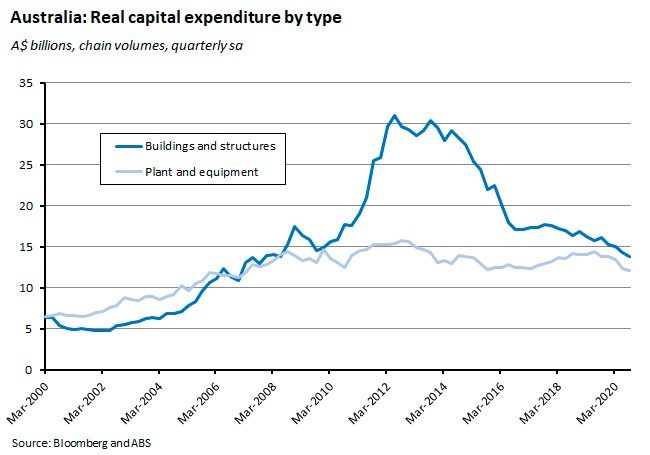

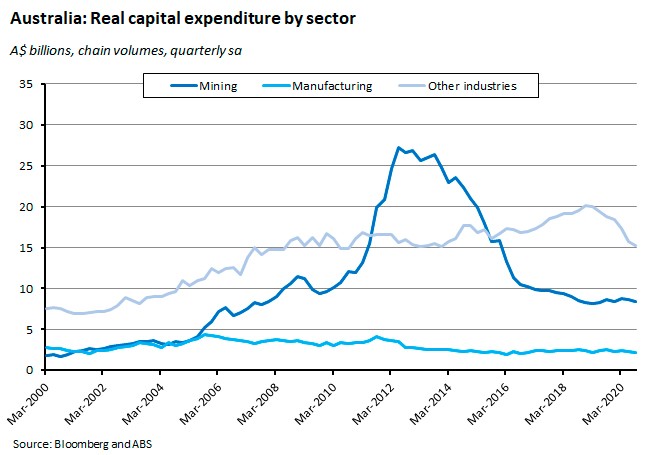

The ABS reported that total new private capital expenditure fell three per cent (seasonally adjusted) in the September quarter to be down 13.8 per cent relative to Q3:2019.

Spending on buildings and structures fell 3.7 per cent quarter-on-quarter and dropped 15 per cent year-on-year while spending on equipment, plant and machinery was down 2.2 per cent in quarterly terms and fell 12.3 per cent in annual terms.

By industry, mining capex fell 3.1 per cent over the quarter and 2.8 per cent over the year, manufacturing capex was down one per cent over the quarter and 12.9 per cent over the year, and capex in other industries was down 3.3 per cent over the quarter while slumping 18.9 per cent in annual terms. Within that latter category, there were particularly large drops in investment spending over the quarter in transport, postal and warehousing (down 19.1 per cent), construction (down 16.8 per cent) and information, media and telecommunications (down 15 per cent).

Capex fell across all states and territories over the September quarter, with the largest quarterly declines recorded in Victoria (down 7.7 per cent) and the ACT (down seven per cent) and the smallest decline in Queensland (down 0.7 per cent).

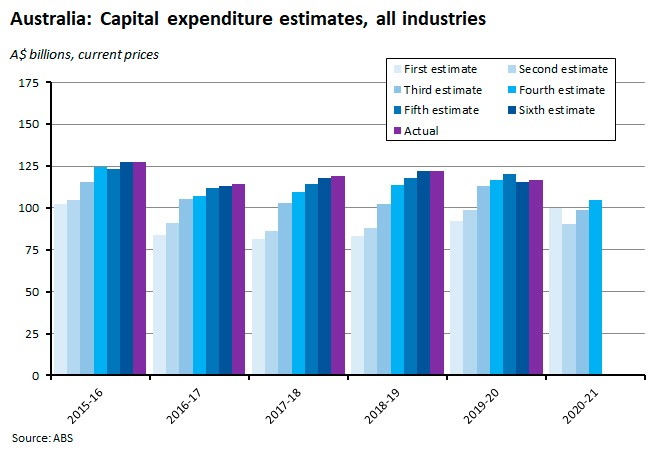

Looking ahead, the fourth estimate for capital expenditure in 2020-21 was just shy of $105 billion, which is 6.3 per cent higher than the third estimate for 2020-21 but 10.3 per lower than the fourth estimate for 2019-20. By industry, the fourth estimate for mining capex was down 5.8 per cent from the third estimate, while the fourth estimates for manufacturing and other industries were 13.9 per cent and 14.1 per cent higher than the previous estimates, respectively.

Why it matters:

The three per cent quarterly decline in private new capital expenditure was a deeper drop than the 1.5 per cent drop predicted by market consensus. It also marks seven consecutive quarters of falling investment – the longest run of negative quarters in the current century and also now ahead of the six consecutive quarters of falling investment spending seen between 1990 and 1992 during the early 1990s recession.

Business estimates of investment in 2020-21 have been upgraded overall relative to the third estimate, although it is notable that the mining sector has downgraded its expectations for capital spending. Most of the survey responses on investment expectations will predate the recent good news on vaccines, which might prompt some upgrade in investment intentions going forward.

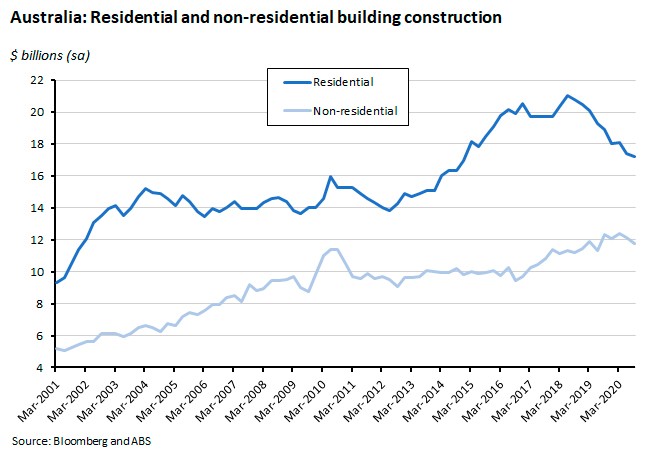

What happened:

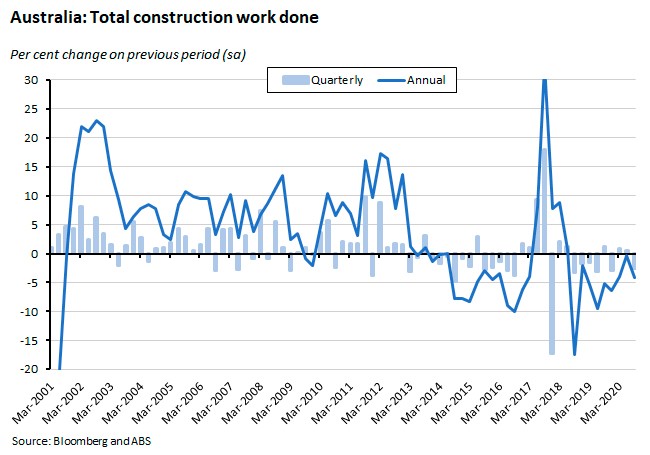

The ABS said total construction work done in the Australian economy fell 2.6 per cent over the September quarter (seasonally adjusted) to be 4.2 per cent lower across the year. Building work done fell two per cent in quarterly terms and 7.2 per cent in annual terms, while engineering work done fell 3.3 per cent in quarterly terms but was (just) up 0.1 per cent over the year.

Total construction work done in the September quarter fell in all states and territories, with the sole exception of the NT which saw a 3.9 per cent increase. The biggest quarterly declines were in the ACT (down 8.7 per cent), Victoria (down 5.7 per cent) and Tasmania (down 4.8 per cent).

Focusing on building work, non-residential building work done fell 3.4 per cent quarter-on-quarter and 4.5 per cent over the year, while residential building work done declined by one per cent over the September quarter to be 8.9 per cent lower than in Q3:2019.

Why it matters:

The market had expected a two per cent quarterly fall in construction work done in Q3, so the actual result was a bit weaker than anticipated. The big decline in activity in Victoria had been expected, however, given the impact of public health restrictions.

Despite the overall weakness, there were some spots of strength to be found in the data. Private new house construction was up 1.2 per cent over the quarter while private alterations and additions were up 4.6 per cent. The former is a sign that the federal government’s Homebuilder program along with state government support has had an impact on the market, while the latter is consistent with other data showing rising lending and rising approvals for innovations.

What happened:

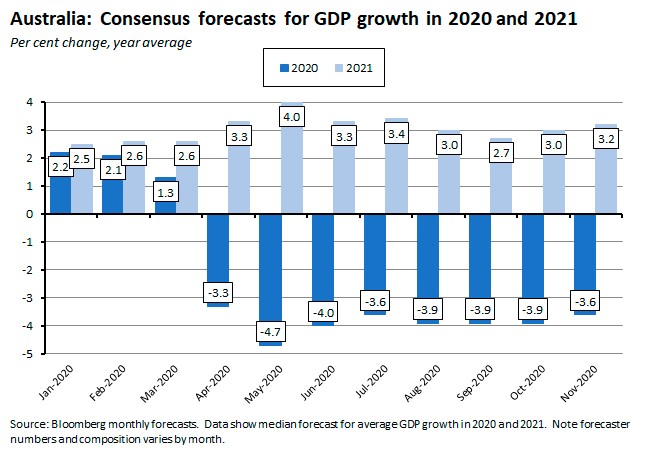

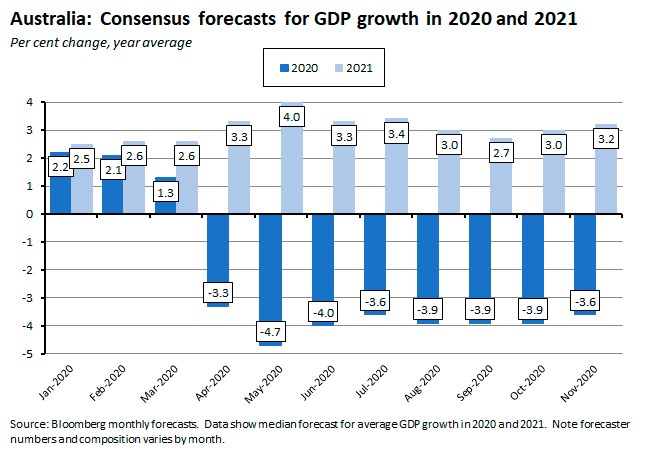

The November iteration of Bloomberg’s monthly survey of economists showed that respondents have become more optimistic on prospects for the Australian economy. Real GDP growth is now forecast to contract by 3.6 per cent this year, then rise by 3.2 per cent next year, before the pace of growth accelerates again, rising to 3.5 per cent in 2022.

Expectations regarding the labour market have also improved. The unemployment rate is now expected to dip below seven per cent this year and to be at 7.1 per cent in 2021, before falling further to 6.3 per cent in 2022.

Despite the anticipated improvement in activity, there is still little expectation of wage growth or inflationary pressures. The median forecast sees the rate of increase in the wage price index (WPI) slowing from 1.6 per cent this year to 1.1 per cent next year, then rising modestly again to 1.5 per cent in 2022. The rate of change in the consumer price index (CPI) is predicted to edge up from 0.7 per cent this year to 1.5 per cent in 2021 and 1.7 per cent in 2022, still below the bottom of the RBA’s target range.

Why it matters:

The stronger run of data in recent weeks, along with the easing of the lockdown in Victoria and positive news on a vaccine against COVID-19 have been reflected in modest upgrades to the median forecasts for growth and unemployment, but that hasn’t changed the market’s view that any meaningful increase in inflation remains a long way off.

What happened:

According to the ABS, preliminary data for merchandise trade in October showed goods exports up six per cent and goods imports up eight per cent. That produced a merchandise trade surplus of $4.8 billion (original terms).

Why it matters:

The ABS said Australia exported a record $13.5 billion of metalliferous ores in October. Iron ore accounted for 81 per cent of that, and at a value of $10.9 billion, iron ore exports also set a new record. With 80 per cent of all iron ore going to China last month, the trade numbers show that the bilateral iron ore trade remains insulated from the challenges that have afflicted other Australian exports in recent months as part of the deterioration in bilateral relations. That’s broadly in line with expectations since – unlike with the products apparently targeted by Beijing – there are no easy substitutes available to China for Australian iron ore.

Also notable in the preliminary data was an increase in the value of exports of natural gas – the first monthly rise since March this year and a sign that global demand is returning.

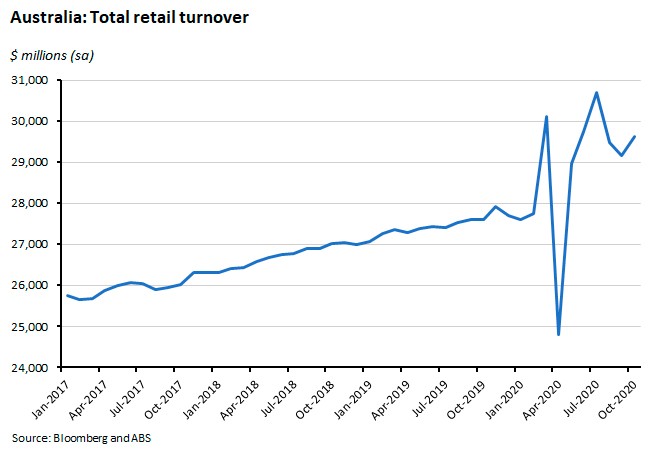

What happened:

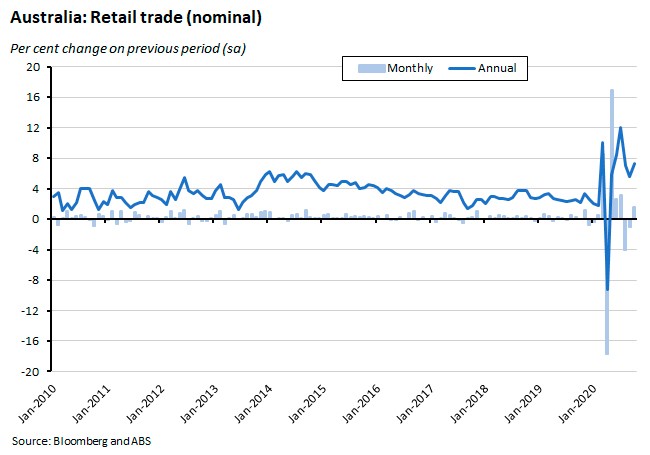

Last Friday, the ABS said its preliminary estimate of retail turnover in October rose 1.6 per cent over the month (seasonally adjusted) to be 7.3 per cent higher over the year.

In dollar terms, turnover was up $460.5million relative to September.

The ABS reported that cafes, restaurants and takeaway food services led the increase in October, although there were also rises for other retailing, and clothing, footwear and personal accessory retailing.

By state, the re-opening of stores in Victoria mean that the state led the monthly increases in all industries except for food retailing. Turnover in Victoria was up 5.2 per cent over the month but is still 5.7 per cent down on October 2019 levels.

Why it matters:

The re-opening in Victoria helped push up overall retail turnover in October and there was also a more modest increase in New South Wales following two months of falling numbers. With turnover running at more than seven per cent in annual terms, this preliminary data is a positive sign for overall household spending in the final quarter of the year and is consistent with the improvement in consumer sentiment that we’ve been tracking over the past couple of months.

What happened:

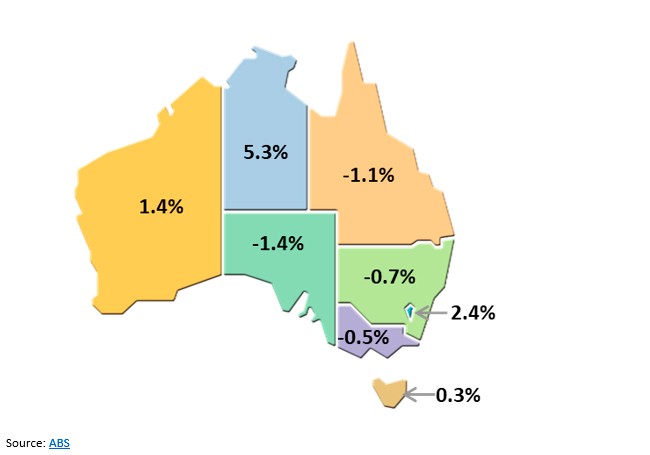

Last Friday, the ABS also published new data on annual economic growth across Australia’s states and territories.

In 2019-20, Real Gross State Product (GSP) shrank in South Australia (down 1.4 per cent), Queensland (down 1.1 per cent) New South Wales (down 0.7 per cent) and Victoria (down 0.5 per cent). GSP grew in the NT (up 5.3 per cent), the ACT (up 2.4 per cent), Western Australia (up 1.4 per cent) and Tasmania (up 0.3 per cent).

Why it matters:

The GSP figures for 2019-20 capture the initial impact of COVID-19 along with bushfires as well as drought conditions. The largest fall in GSP came in South Australia, while the biggest increase was in the NT, powered by a 39.7 per surge in mining gross value added, reflecting the transition from construction to production of LNG in the territory.

The falls in GSP in New South Wales and Queensland in 2019-20 were the first negative annual results recorded in the history of the two states.

What happened:

One final release from the end of last week saw the ABS report the latest set of findings from its Business Impacts of COVID-19 survey, this time covering the period 4 November to 11 November 2020. Findings included:

- 24 per cent of businesses reported an increase in revenue in November compared with 16 per cent in October.

- 22 per cent of businesses reported a revenue decrease in November. The proportion of businesses reporting a decrease in revenue has fallen each month since July.

- For the first time in this monthly survey, more businesses reported increased revenue than decreased revenue.

- 22 per cent of businesses said they had capital expenditure plans for the next three months.

- The share of businesses reporting economic uncertainty as a factor influencing their capital expenditure has halved since August, falling from 59 per cent to 29 per cent.

Why it matters:

The ABS said its last survey results showed signs of increasing confidence among businesses, although it also noted that some of the responses may have been driven by seasonal factors as well as an easing of COVID-related restrictions. Still, the survey results match the story being told by the PMIs and by the latest NAB monthly business survey in indicating more business optimism.

. . . and what I’ve been following in the global economy

What happened:

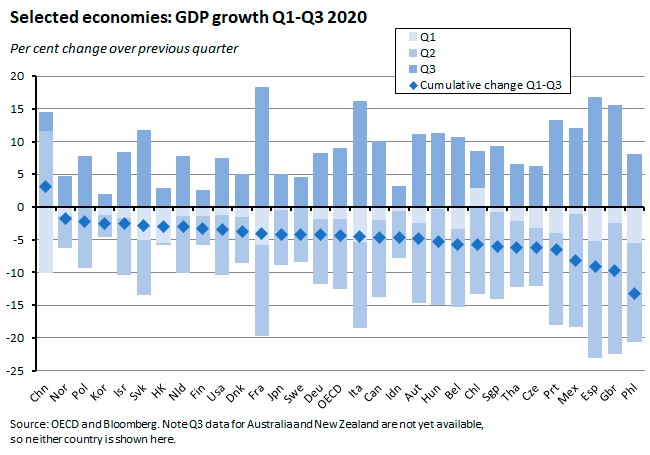

Third quarter GDP readings to date have painted a mixed picture of developments across the world economy. Some economies have enjoyed large bounce backs in activity that have gone a fair distance to reversing the steep declines in output suffered in Q2, while in other cases the recovery has been much more partial. Overall, however, the only major economy to date to report cumulative GDP growth over the first three quarters of 2020 is China.

Other economies to have performed relatively well in terms of real GDP during the pandemic include Norway, Poland, South Korea, Israel and Slovakia, all of which managed to keep the cumulative loss of output they endured over the first three quarters of 2020 below three per cent. At the other end of the economic pain spectrum, the Philippines, UK, Spain and Mexico have all suffered cumulative output losses of more than eight per cent.

Why it matters:

It’s tempting to use the ranking of output performance as a broad indicator of country competence in handling the twin economic and health challenges posed by the pandemic. Of course, simple cross-country comparisons of GDP performance only tell a partial story since a range of factors likely explain observed growth outcomes including the degree of relative economic exposure to the sectors most hurt by the pandemic (for example, countries with GDP more skewed towards tourism and face-to-face services more generally would be expected to suffer more), levels of social trust and trust in government (which will influence public compliance with health measures and hence the stringency of lockdown measures), the relative performance of key economic partners, and just plain luck. Another important caveat here is that, with the pandemic still running, it’s still too soon to draw any final conclusions about best practice.

All those caveats made, however, when the post-pandemic assessments do get underway, relative output performance will be one of the indicators used to judge both the relative effectiveness of the policy response and the competence of those who administered it.

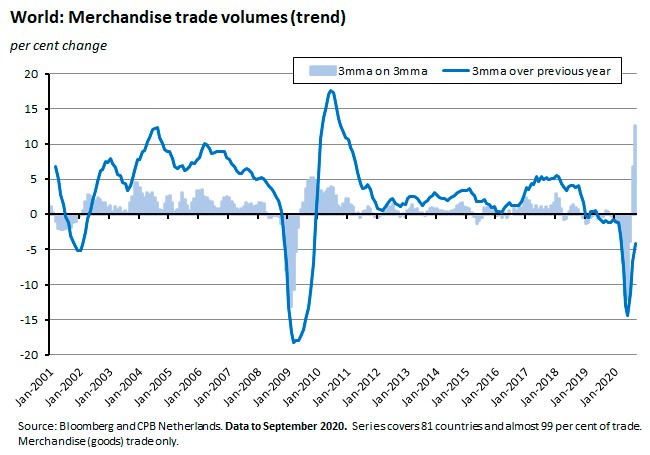

What happened:

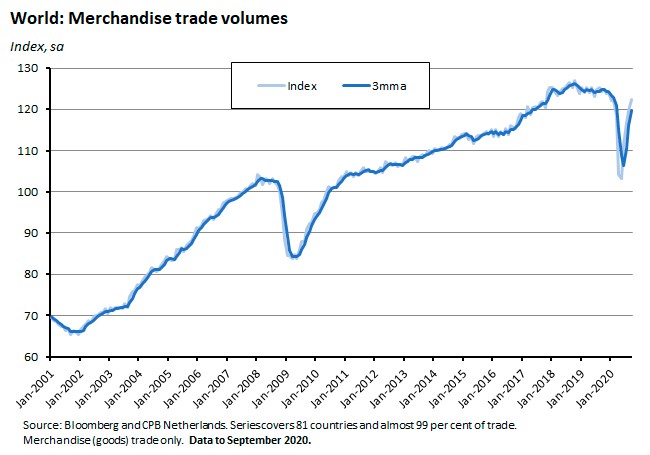

The CPB World Trade Monitor said that world trade volumes grew by 2.1 per cent in September 2020, marking a modest slowdown in monthly growth from the 2.4 per cent pace recorded in August and a bigger drop from the five per cent reached in July. On a quarterly basis, world trade volume growth was a strong 12.5 per cent in Q3 following a 12.2 per cent drop in Q2.

World trade volumes are now about two per cent below their pre-pandemic level.

World trade momentum (measured here as the monthly change in the three-month moving average) rose to 12.5 per cent in September, up from 6.7 per cent in August.

Why it matters:

The sharp recovery in world (merchandise) trade volumes in Q3 is the strongest recorded since the start of the CPB series in January 2000. The recovery has been led by East Asia in general and China in particular, with the latter successfully increasing its share of world trade over the course of the pandemic. The recovery – at least to date – also looks quicker than that seen in the aftermath of the global financial crisis, reflecting the fact that this time around it is the service sector that has suffered the most economic damage.

Consistent with this positive news on world trade, last week the WTO said that its World Goods Trade barometer had risen sharply in September, climbing to an index reading of 100.7, which the WTO reckons indicates a strong Q3 rebound (readings above 100 suggest above-trend growth). The pervious reading of 84.5 for June had been the lowest in the history of the WTO barometer, which dates back to 2007.

What I’ve been reading . . .

RBA Deputy Governor Guy Debelle gave a speech on Monetary Policy in 2020. Mostly this covered what is by now well-trodden ground, although it did give the RBA an opportunity to stress that policymakers needed to careful not to remove macro stimulus too early. In theory, the central bank’s own changes to forward guidance plus the Treasurer’s own version of fiscal forward guidance (with its target for the unemployment rate to be ‘comfortably below’ six per cent) should preclude this, although arguably that fiscal target does leave some wriggle room around the definition of ‘comfortably below’ given that pre-crisis estimates of labour market equilibrium were based around a sub-five per cent unemployment rate while Treasury’s latest estimate (as reported in the Budget Papers) puts the NAIRU at five per cent.

A new RBA Research Discussion Paper estimates the number of jobs saved by the government’s JobKeeper program over the first four months of its operation (April to July 2020 which covers much of the operation of JobKeeper 1.0 which ran from 30 March to 27 September this year). It does so by comparing the employment outcomes for casual employees with between six and 10 months tenure with their employer in February 2020 (and who were therefore ineligible for the scheme) with employment outcomes for casual employees with between 12 and 23 months tenure in the same month (and who were therefore eligible for JobKeeper). The authors estimate that receiving JobKeeper increased a person’s probability of remaining employed by at least twenty percentage points. Since there were about 3.5 million Australians on the scheme over this period, that implies that JobKeeper saved at least 700,000 jobs relative to what would have been the case in its absence. As actual employment fell by about 650,000 over the first half of this year, that further suggests that without JobKeeper the fall in employment would have been more than twice as large as the one that actually occurred. With the cost for JobKeeper for its first six months put at $70 billion, that implies a cost of around $100,000 per job saved. Note that this estimate doesn’t include any additional jobs that might have been saved by the scheme’s positive impact on overall demand in the economy through its boost to income levels and reduction in uncertainty, suggesting that the likely impact on jobs would have been greater, and the cost per job smaller, than these estimates.

A new article from the ABS on measuring excess mortality during the pandemic. One interesting finding: Significantly lower than expected numbers of deaths were recorded from the end of May to mid-July 2020, with the shortfall in mortality mainly driven by lower numbers of deaths from respiratory conditions including influenza, pneumonia and chronic respiratory conditions.

Last Friday brought the release of the final report for the Retirement Income Review. Here are Grattan’s five key takeaways from the report and here is Robert Breunig explaining the findings of some of the research commissioned by the Review.

The latest release of the Household, Income and Labour Dynamics in Australia (HILDA) Survey. Some of the findings that caught my attention included: (1) Average Australian household disposable income has grown in real terms by $23,248 since 2001, while average household wealth has increased to $934,025; median household disposable income has grown by $18,938 over the same period while median household wealth has risen to $503,563; (2) both mean and median household disposable incomes grew particularly rapidly over the 2003-2009 period but between 2009 and 2018 growth has been much weaker – mean incomes grew by just 3.3 per cent while median income in 2018 was lower than it was in 2009; (3) Wealth inequality increased between 2002 and 2006 but has remained largely stable since then while income inequality has barely changed since 2001 – the Gini coefficient for equivalised household disposable income has remained between 0.29 and 0.31 over all eighteen years of the HILDA survey; (4) Income mobility appears to have declined over the period of the survey; (5) Australia’s middle class is stable or even slightly growing in size across a wide range of measures, although estimates of the size of the middle class vary significantly by measure: for example, defining the middle class as those with incomes between 50 per cent and 200 per cent of median income suggests that more than 80 per cent of Australians are middle class and have been for most of the survey. On the other hand, if the definition requires both income and wealth to between 75 per cent and 125 per cent of the median, the share of the middle class plummets to just six per cent; and (6) Men’s reported life satisfaction has been consistently lower than women’s while Australians over 65 years old report the highest levels of satisfaction.

The Productivity Commission (PC) published another of its Productivity Insights. This one looks at Australia’s productivity performance over the longer term and provides some detailed historical accounting of past productivity developments. Looking forward, the PC notes that with 90 per cent of employment now found in services, a high productivity economy requires a high productivity service sector. Yet our knowledge of what drives service sector productivity is much less developed that in the case of manufacturing or natural resources. It may be the case, for example, that innovation in services requires less emphasis on traditional R&D and more on new business models and new business formation. It may be that it requires a greater emphasis on human capital formation (including the health and skills of the labour force). And it may be that it requires a more mobile and flexible workforce. But as the PC notes, there’s a lot of uncertainty here.

Also from the PC, Chair Michael Brennan gave a short speech on Productivity Reform in Australia and New Zealand: Barriers and opportunities.

ABC Business’s take on Victoria’s budget: an alternative set of priorities to the Federal approach. AFR reporting sees the approach as a government-led recovery versus what it characterises as a more business-friendly NSW approach.

John Freebairn is a fan of the NSW government’s ambition to get rid of stamp duty but is sceptical about the chosen path, given the big hole it could create in government revenues.

A thoughtful Unherd column on the economics of vaccines. It’s rather more complex than simplistic critiques of the profits made by ‘big pharma.’

Daniel Gros makes the case for subsidies over lockdowns.

Two COVID-related columns from VoxEU. The first examines how the prospect of access to a vaccine against COVID-19 could change public and private behaviour, suggesting that as a vaccine becomes more likely, some people may show increasing unwillingness to be socially active, share public spaces, eat out, or go to their workplace, some significant economic effects. The second reviews the cross-border trade during the time of the pandemic, noting that while 106 nations implemented a total of 240 reforms to ease the import of medical goods and medicines, at the same time there are 110 export curbs on medical goods and medicines currently still in force, of which 68 have no phase-out date.

Also from VoxEU, an assessment of the relative importance of policies affecting pre-tax vs post-tax income inequality (or pre-distribution vs redistribution) argues the case for paying more attention to the former.

Related, the Peterson Institute offers policy advice on how to fix economic inequality in the United States and other advanced economies (but note here the HILDA findings on inequality for Australia cited above).

The Guardian on accusations of COVID cronyism in the UK.

Martin Wolf on what the world can learn from the pandemic, in the FT and also the AFR. Wolf’s starting point is the apparent dislocation between what was a relatively mild pandemic (NB. Wolf means in historic terms when COVID-19’s toll is set against outbreaks such as the Spanish Flu as well as earlier calamities like the Black Death) and the huge economic cost incurred – a relationship that prior assessments of likely impact got badly wrong. Also worth a look is this INET piece that Wolf references in his column.

The FT has started a new series looking at lessons from Japan for other advanced economies. The proposition here is that Japan’s prolonged history of coping with very low growth, very low inflation and very low interest rates could be a useful guide to what’s in store for the rest of us (over the three decades since 1990, Japan has managed average annual real GDP growth of 0.8 per cent and annual inflation of 0.4 per cent). The first in the series suggests that those lessons include the importance of maintaining public confidence in central bank policy and avoiding any lock-in of zero inflation expectations along with the need for a strategy to drive economic growth. In the second, Adam Posen argues that after 2002, in per capita terms Japan actually performed in line with its peers as Tokyo successfully adopted new economic policies, and that ‘Japanification’ should be taken as shorthand for ‘failure to respond adequately to financial fragility, and being too timid with macroeconomic stimulus’ rather than as predetermined fate.

As more good news on vaccines and prospects for a synchronised global upturn next year (at least once the Northern hemisphere has got its COVID-winter out of the way) prompt another market rally and general increase in optimism, this essay from Harper’s Magazine offers a rather different kind of perspective with an ultra-bleak take on the long-term relationship between capitalism and democracy as a guide to where we might be heading: back to the Eighteenth Century?

Two from historian Adam Tooze. The first piece argues that the increased activism of leading central banks such as the Fed and ECB also pushes them into increasingly contentious political territory. The second starts from the observation that while the US electorate has now chosen to hand the White House to a Democrat at four moments of historic crisis (1916, 1932, 2008 and 2020), this is the first time it has done so without also giving the same party a clear majority in Congress.

The Economist profiles Janet Yellen, Joe Biden’s choice for US Treasury Secretary.

Matt Yglesias puts an interesting twist on the low interest rates story, claiming that they have pernicious political consequences by removing the need for fiscal discipline or hard budgetary choices. In his words, ‘Trump cut taxes, increased military spending, increased domestic spending, failed to repeal the Affordable Care Act, and watched as Social Security and Medicare spending continued their relentless upward march and it was…totally fine. The deficit exists as a purely abstract political football…And it’s left our politics a bit unglued.’

The IMF takes an in-depth look at reserve currencies against the backdrop of a transforming global monetary system. Continued US dollar dominance is the most likely scenario but ‘technological advances, particularly the emergence of digital currencies and advances in payment systems, could alter the importance of traditional drivers of reserve currencies, speed up the transition to alternative reserve configurations, result in the emergence of new reserve currencies, and even lessen the stability of future reserve currency configurations.’

Latest news

Already a member?

Login to view this content