The government has eased eligibility requirements for the JobKeeper program as intensified public health measures in Victoria have prompted Treasury to scale back its forecasts for Australian GDP growth this year and raise its projections for unemployment.

After a three-month break, the RBA has resumed its purchase of government bonds as it reinforces its yield curve control program. Consumer confidence fell for a sixth consecutive week. Retail trade volumes contracted in Q2. Australia enjoyed a record trade surplus in 2019-20, thanks to selling an even larger share of our exports to China, as well as a big swing in the services trade balance. House prices continue to slide, but the adjustment to date has been modest. Global PMIs indicate an upturn in world activity in July, while GDP results depict painfully large contractions in Europe and North America over the June quarter.

This week’s readings include planning regulations and the supply of Australian apartments, new data on tourism jobs, a ‘lost decade’ of income growth for young Australian workers, the US Fed as the world’s ‘backup lender’, how COVID-19 is changing the way we work and a symposium on place-based policies.

What I’ve been following in Australia . . .

What happened:

The government announced that it would ease the eligibility requirements for its JobKeeper 2.0 program, effectively unwinding the tightening in criteria it had introduced on 21 July when it had extended the existing program for an additional two quarters.

There are two sets of changes, the first to business eligibility and the second to employee eligibility.

Regarding business eligibility, from 28 September 2020, businesses and not-for-profits (NFPs) seeking to claim JobKeeper 2.0 will now be required to re-assess their eligibility with reference to their actual turnover in the September quarter 2020 to be eligible for JobKeeper from 28 September 2020 to 3 January 2021. Under the previously announced 21 July measures, the turnover test in this case would have applied not just to the September quarter but would also have had to be met for the June quarter too. Similarly, businesses and NFPs seeking to make a claim for the period from 4 January to 28 March 2022 now need to demonstrate that they have met the relevant decline in turnover test in the December quarter 2020. Under the old rules, they would have had to meet the turnover tests in the June, September and December 2020 quarters.

For employee eligibility, the new rules (which will apply from 3 August) say that the reference date for assessing which employees are eligible for JobKeeper is now 1 July 2020 instead of 1 March 2020. Full details are available here (pdf).

According to the government, about 530,000 extra Victorian employees will join the JobKeeper program over the September quarter, taking the total number of Victorian employees on the program up to 1.5 million or nearly half the state’s private sector workforce. The combined cost of JobKeeper 1.0 and 2.0 is now expected to rise by about $15.6 billion, with $4.5 billion of that increase reflecting an increase in the number of Victorians joining the existing JobKeeper 1.0 program and a further $11.1 billion associated with the new changes to JobKeeper 2.0.

The adjustments to JobKeeper came after Prime Minister Scott Morrison set out Treasury’s latest thinking on the impact of the increased number of COVID-19 cases and the intensified public health measures in Victoria, updating the forecasts presented in the July Economic and Fiscal Update from just a few weeks ago.

According to the PM, Treasury reckons that the new, stricter version of Victoria’s lockdown will subtract between $7 billion and $9 billion from GDP in the September quarter, with the direct hit to activity in Victoria estimated to account for around $6 billion to $7 billion, or about 80 per cent, of the total loss in national output. The balance reflects the damage to confidence in the rest of Australia and disruption to national supply chains. The combined effect on GDP of the stage three and the stage four Victorian restrictions through the September quarter is expected to be between $10 billion and $12 billion dollars which is anticipated to cut around 2.5 percentage points from quarterly real GDP growth.

The forecast official national unemployment rate is now expected to rise to around 10 per cent, up from the 9.25 per cent peak predicted in July’s Update. And the underlying ‘effective’ rate of unemployment (which adjusts for the impact of JobKeeper on the official rate) is now projected to climb to more than 13 per cent, up from its current estimated rate of around 11 per cent.

Why it matters:

The changes to JobKeeper 2.0 announced Friday August 7 mark a welcome recognition on the part of the government of the increased economic damage that will be inflicted by developments in Victoria and the consequent need for an enhanced policy response.

Just two weekly notes ago, we were commenting that private sector forecasters had become relatively more optimistic on Australia’s economic outlook. Like the Treasury, those same forecasters are now having to pare back their projections. The significant revisions to Treasury’s own forecasts in the space of just a few weeks, and the government’s rapid winding back of some of its recent adjustments to JobKeeper both serve as powerful examples of the vulnerability of any economic projections and policy choices to shifts in the trajectory of COVID-19.

When the government released its Economic and Financial Update on 23 July, one of the key assumptions (see Box 2.1 in Part 2) was that Victoria’s (then) stage three lockdown in Melbourne and the Mitchell Shire, which had taken effect from 9 July, would remain in place for six weeks before gradually easing. Instead, restrictions have been tightened to stage four in Melbourne and stage three across regional Victoria. We noted at the time that the assumptions around Victoria seemed optimistic and, very sadly, that has proved to be the case.

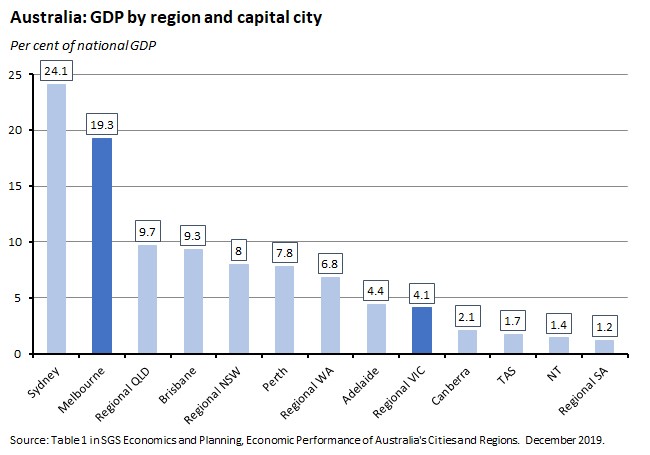

With Melbourne and regional Victoria together accounting for almost a quarter of national GDP, the direct impact of the lockdown on growth and employment will be substantial. Treasury’s assumption is that this will account for the bulk (about 80 per cent) of the hit to growth in the third quarter of this year, although there will also be some indirect impact via the drag on business and consumer confidence in the rest of the country. The hopeful base case is that this headwind, although significant, will be insufficient to fully undermine the recovery in the other states and therefore allow the national economy to eke out a positive growth result in the September quarter. But as we’re learning to our cost, COVID-19 continues to derail our expectations.

What happened:

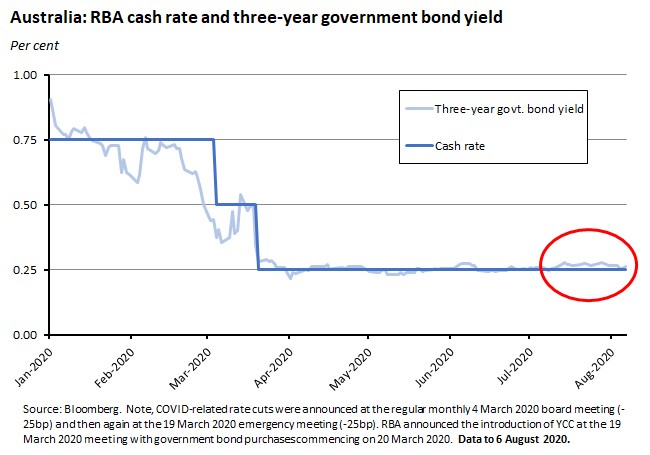

At its meeting on 4 August, the RBA Monetary Policy Board decided to maintain the central bank’s current policy settings, including targets for the cash rate and the yield on three-year Australian Government bonds of 25 basis points (bp).

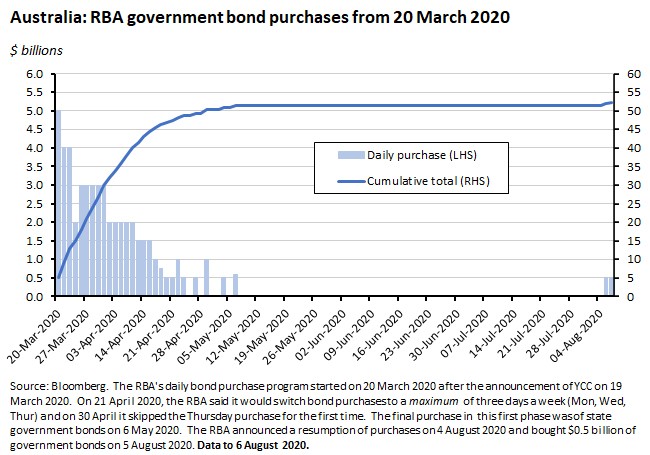

The Board did, however, announce one change. After noting that Australia’s government bond markets were ‘functioning normally alongside a significant increase in issuance’ and that the yield on three-year Australian Government Securities (AGS) had been consistent with the RBA’s target of around 25bp, the statement went on to acknowledge that the ‘yield has, however, been a little higher than 25 basis points over recent weeks. Given this, tomorrow the bank will purchase AGS in the secondary market to ensure that the yield on three-year bonds remains consistent with the target. Further purchases will be undertaken as necessary.’

The statement also noted the impact that the current COVID-19 outbreak in Victoria is having on the state and national economic outlooks and trailed some of the forecasts the RBA will release on Friday in the August Statement on Monetary Policy. First, beginning on a relatively positive note, the RBA said that although ‘the Australian economy is going through a very difficult period and is experiencing the biggest contraction since the 1930s’, nevertheless, ‘the downturn is not as severe as earlier expected and a recovery is now underway in most of Australia.’ But then came the more sombre assessment, with the statement continuing:

‘This recovery is, however, likely to be both uneven and bumpy, with the coronavirus outbreak in Victoria having a major effect on the Victorian economy. Given the uncertainties about the overall outlook, the Board considered a range of scenarios at its meeting. In the baseline scenario, output falls by six per cent over 2020 and then grows by five per cent over the following year. In this scenario, the unemployment rate rises to around 10 per cent later in 2020, due to further job losses in Victoria and more people elsewhere in Australia looking for jobs. Over the following couple of years, the unemployment rate is expected to decline gradually to around seven per cent.’

As well as this baseline scenario, the RBA is also considering alternatives, including the possibility of a stronger recovery ‘if progress is made in containing the virus in the near future’ along with the risk of more negative possibilities should Australia and other economies ‘experience further widespread lockdowns’, which would delay any recovery. In all the scenarios considered by the Board, inflation was expected to remain below two per cent over the next couple of years and therefore below the bottom of the RBA’s target band.

The statement concluded with pledges that the RBA Board was ‘committed to do what it can to support jobs, incomes and businesses in Australia’, that the current ‘accommodative approach will be maintained as long as it is required’ and that the RBA ‘will not increase the cash rate target until progress is being made towards full employment and it is confident that inflation will be sustainably within the two–three per cent target band.’

Why it matters:

After a run of several Board meetings which were pretty much ‘dead’ in terms of any expected policy change, the run-up to this week’s meeting had generated a bit more anticipation than has become usual. That’s because in the aftermath of the shift to a more intense version of lockdown in Victoria and the consequent adverse implications for growth and employment, some economists revisited Governor Lowe’s 21 July speech and speculated that the RBA might choose to push the cash rate down to just 0.1 per cent. Despite that speculation however, the clear consensus was still for no change in the policy framework and in the event no change was – largely – what we got.

The modest exception to that came in the form of the RBA’s announcement that it would resume its program of buying government bonds. This program had started on 20 March, the day after the RBA announced its yield curve control (YCC) program, with a $5 billion purchase, but the scale of central bank purchases was then wound back quite quickly, with the last coming on 6 May, producing a cumulative total of $51.35 billion. The initial purchase marking the RBA’s second phase of intervention in the secondary market for government securities was on a much smaller scale – just $0.5 billion on 5 August.

As noted above, according to this week’s statement, the trigger for the resumption of activity in the secondary market after a three-month hiatus was that the yield on three-year government securities had been higher than the RBA’s ‘about’ 25bp target.

The other point of note from this week’s meeting was a preview of the forecasts that will be presented in the August Statement on Monetary Policy, which included what appears to be a paring back of the RBA’s previous growth forecast for 2021 along with an increase in the forecast unemployment rate (which seems to be in line with the new Treasury projections noted in the previous story).

What happened:

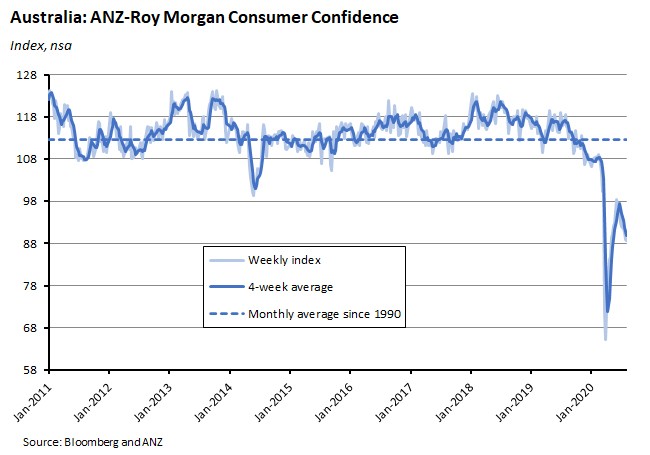

The ANZ-Roy Morgan Consumer confidence index fell 0.4 per cent to 88.6 this week.

Why it matters:

This was a sixth consecutive weekly fall which matches the run of declines back in March and April earlier this year (although the size of the drop in confidence is much lower now than it was back then). The index now at its lowest level for over three months, having returned to levels last seen at the end of April.

What happened:

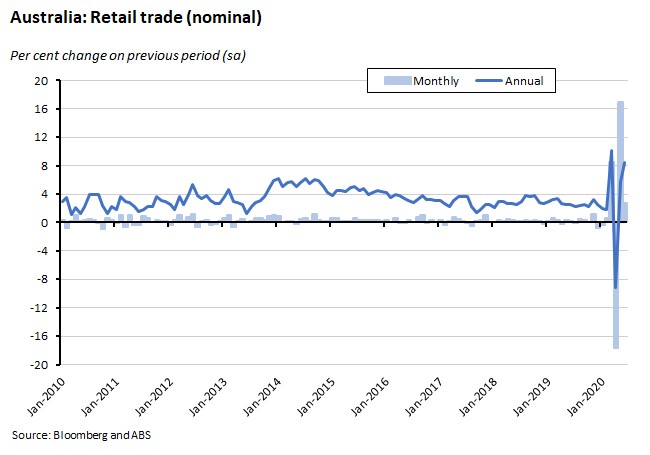

Finalised data from the ABS on retail trade showed turnover in June rising 2.7 per cent (seasonally adjusted) and increasing 8.5 per cent in annual terms. (A couple of weeks ago, preliminary data from the Bureau had suggested retail turnover for June rose by 2.4 per cent over the month and 8.2 per cent over the year.)

The ABS said that June saw the continued recovery of industries impacted by trading restrictions in April and early May, with large monthly increases in turnover for cafes, restaurants and takeaway food services (up 27.9 per cent), and for clothing, footwear and personal accessory retailing (up 20.5 per cent).

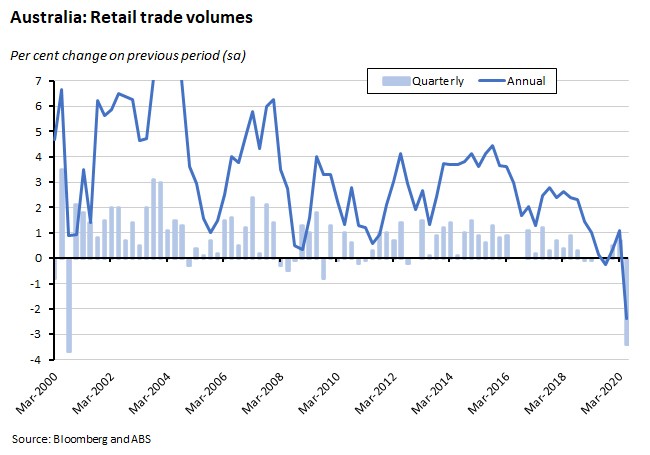

Along with monthly nominal retail turnover data for June, the ABS also published real (that is, inflation-adjusted) retail turnover data for the second quarter of this year. That showed turnover volumes falling 3.4 per cent over the quarter (seasonally adjusted) and dropping 2.4 per cent in annual terms.

Why it matters:

Retail trade accounts for about a third of consumption spending, which in turn accounts for about 55 per cent of GDP. Hence the sharp fall in quarterly retail volumes confirms what we already knew: household consumption’s contribution to second quarter GDP growth will represent a significant headwind for the overall growth outcome.

The Bureau also highlighted the ongoing impact of COVID-19 on spending patterns, pointing to large annual rises for several food categories including flour (27.2 per cent), fresh seafood (25.5 per cent), and oil (22.8 per cent), which is consistent with the story that social distancing measures are still driving an increase in food being prepared and consumed at home. In contrast, spending at cafes and restaurants saw a large annual fall in June.

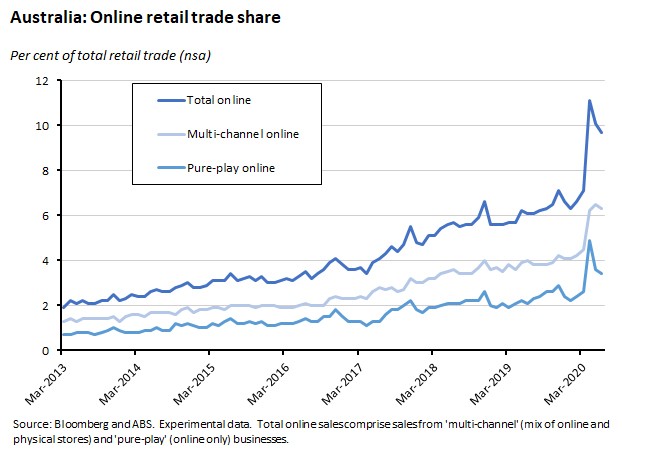

This month’s report also looked at recent developments in online retail spending (note that the ABS series discussed here excludes direct imports (for example, those purchased directly from an overseas website) and sales from households-to-households through third party websites). Online spending enjoyed large rises in March and April this year, as consumers turned to online shopping, but since then the series has seen comparatively small movements including a 3.9 per cent rise in May, and a fall of 4.2 per cent in June.

As a share of total sales, online sales in June were 9.7 per cent (original series) or 9.4 per cent (seasonally adjusted). This is down from the peak recorded in April but still well above pre-COVID-19 levels.

What happened:

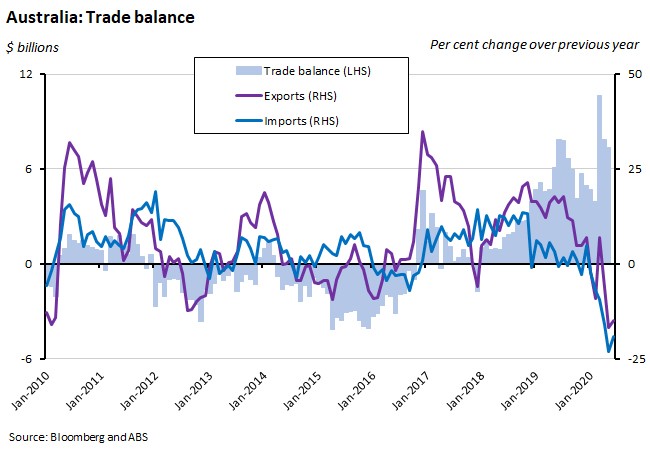

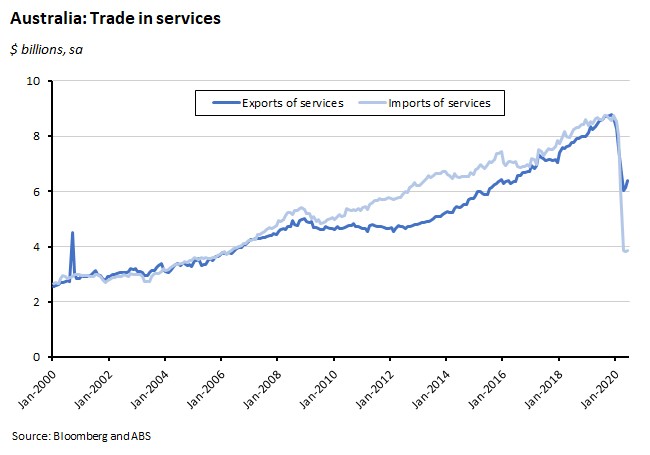

The ABS said that Australia recorded a trade surplus of $8.2 billion (seasonally adjusted) in June. Exports of goods and services rose three per cent over the month, but were still down almost 15 per cent relative to June 2019. Likewise, although imports were up one per cent relative to May this year, they were down more than 19 per cent relative to June 2019.

Trade in services continues to be hit hard by COVID-19, with exports of services rising four per cent over the month but still down about 25 per cent in annual terms, while imports of services were up one per cent over the month but around 50 per cent lower than in June 2019. As a result, Australia is now running a substantial surplus on services trade.

Why it matters:

For 2019-20, the balance on goods and services was a record surplus of $77.4 billion. That represents an increase of $28.3 billion on the surplus of $49.1 billion achieved in 2018-19. Relative to last financial year, imports of goods and services were $22.4 billion (five per cent) lower while exports were $5.9 billion (one per cent) higher.

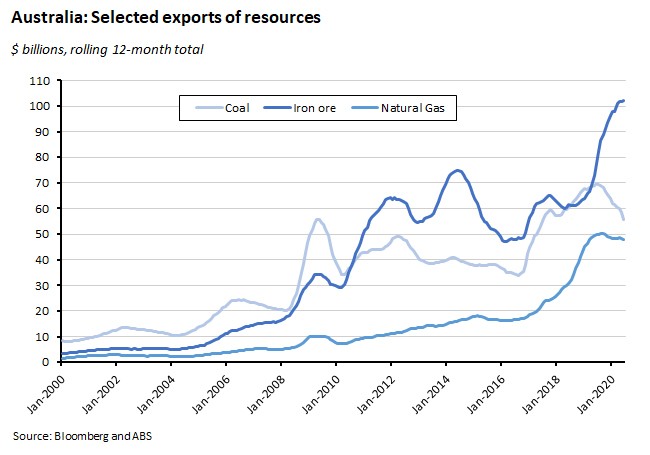

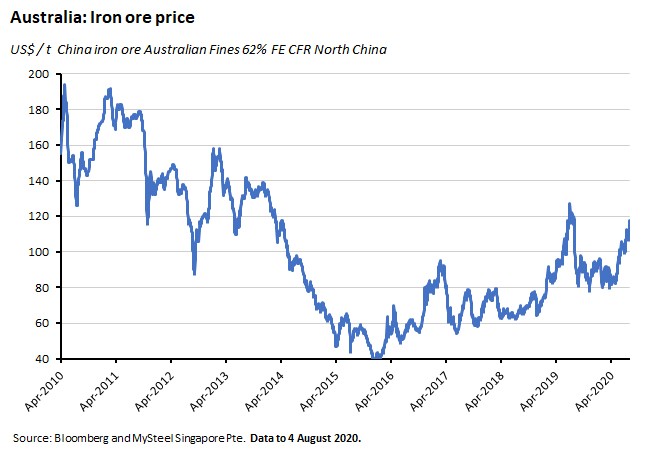

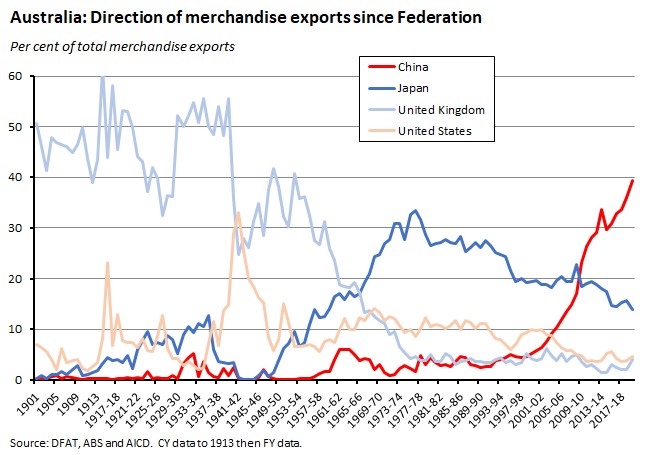

As we noted last week when we discussed the preliminary goods trade data, iron ore has continued to play a critical role in Australia’s export story this year, accounting for about $102 billion or more than a quarter of total goods exports, of which around $85 billion went to China alone.

The role of iron ore has been supported by strong prices over the current financial year, with the price currently well above US$100/t.

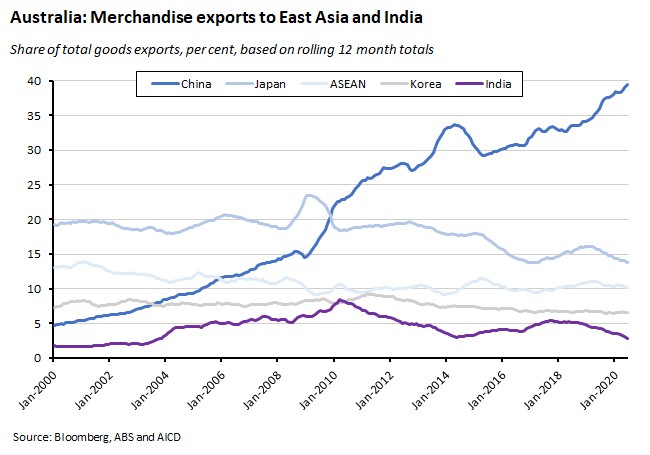

Thanks in part to that dominant role in our iron ore trade, China also remains by far the most important destination for Australian goods exports overall, accounting for about 39 per cent of merchandise export sales in 2019-20.

Not only is that far above the merchandise export share of markets like Japan (about 14 per cent), the EU (around seven per cent) and the United States (less than five per cent), it’s also much greater than the markets that are sometimes touted as potential diversification plays for Australian exporters like India (three per cent) and ASEAN (10 per cent). That’s not to say that those markets won’t become relatively more important in the future, of course. But for now, they’re a long way from approaching China’s significance as an export destination.

Taking a long-run perspective, China’s relative importance as a destination for merchandise exports is currently at the kind of levels last seen in the early 1950s, when Australia was still dependent on the UK as its key export market.

What happened:

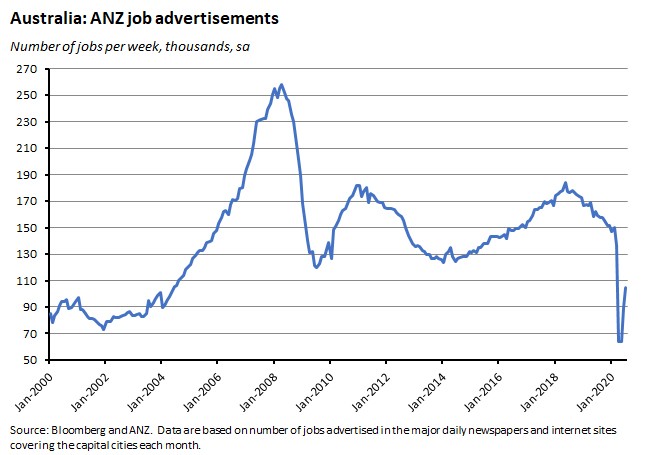

ANZ Australian Job Ads rose 16.7 per cent over the month in July, but were down 34 per cent over the year.

Why it matters:

July’s rate of increase represented a marked slowdown from the 41.4 per cent jump recorded in June and left advertisements down 30 per cent from February this year. That’s consistent with other evidence (see for example last week’s look at the ABS payroll data) which suggests labour market conditions softened in July. Recent developments in Victoria will further weigh on labour market performance.

What happened:

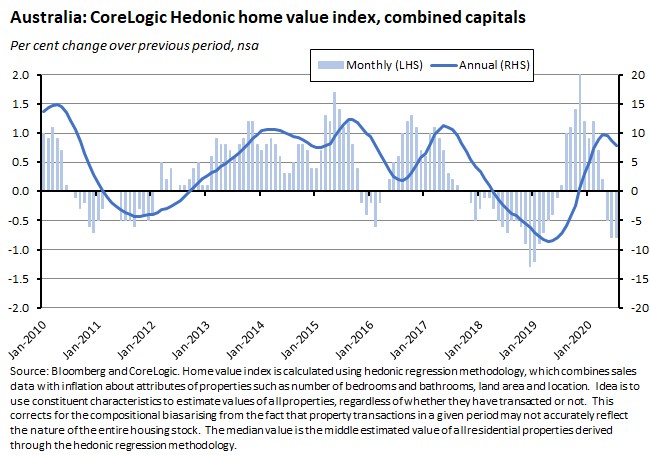

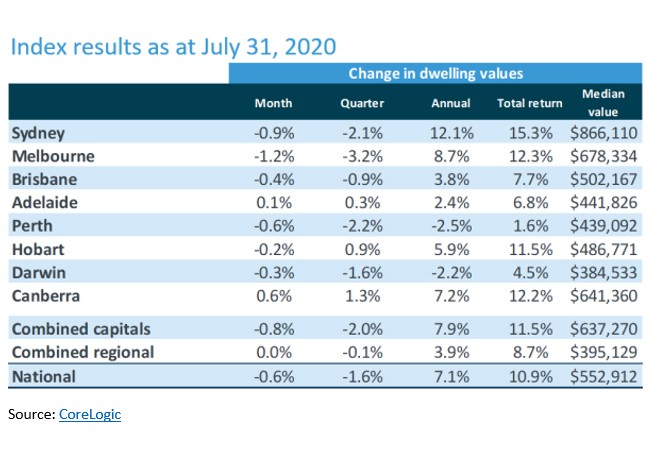

According to CoreLogic, Australian national dwelling values fell 0.6 per cent over the month in July, although they were still up 7.1 per cent over the year. Values for the combined capitals fell 0.8 per cent in monthly terms, but rose 7.9 per cent relative to July 2019.

July saw monthly price falls in every capital city bar Canberra and Adelaide, with the largest declines in Melbourne (down 1.2 per cent), Sydney (down 0.9 per cent) and Perth (down 0.6 per cent).

Source: CoreLogic

{kind=link}

CoreLogic also reports that several indicators of housing market activity continue to be relatively resilient, although other measures are less positive. For example, after slumping by around 60 per cent between mid-March and Easter, its measure of real estate agent activity is now tracking at similar levels to last year. Likewise, the number of newly advertised properties is up 46 per cent from recent lows of early May, with new capital city listings tracking 8.9 per cent above their 2019 results. But while new listings have increased, the total listing count remains 15.2 per cent below last year’s level nationally and 12.5 per cent lower across the combined capitals. (CoreLogic reckons that the diverging trend between new and total listing numbers reflects an underlying story whereby demand for established housing stock is outweighing advertised supply.) At the same time, auction markets – which had been recovering – are now showing renewed signs of weakness in response to the Melbourne lockdown.

Why it matters:

Dwelling values have now fallen for three consecutive months, although the pace of decline to date has been quite modest when set against the scale of economic disruption elsewhere in the economy. Analysts at CoreLogic put this relative resilience down to a combination of the unprecedented level of fiscal support from the federal and state governments, the provision of distressed borrower repayment holidays by lenders, and the impact of record low mortgage interest rates. New loan commitments (see next story) have also been holding up quite well, although this resilience will be tested further in coming months.

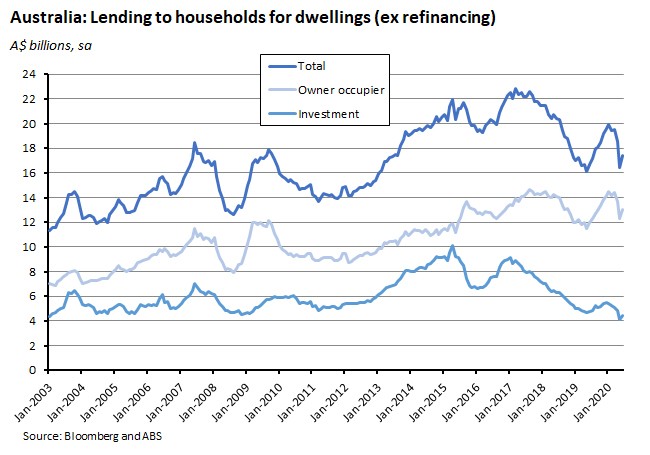

What happened:

The ABS said that new loan commitments for housing rose 6.2 per cent (seasonally adjusted) in June, to be up 4.5 per cent over the year. The value of new loan commitments for owner occupier housing rose 5.5 per cent over the month and 8.7 per cent over the year, while loan commitments for investor housing were up 8.1 per cent in monthly terms but down 6.1 per cent in annual terms.

Personal fixed term loans were also up 5.2 per cent over the month (led by a 20.4 per cent rise in the value of new loan commitments for road vehicles), but fell 10.9 per cent relative to June 2019.

Why it matters:

The Bureau reckons the rise in housing loan commitments in June this year reflects the easing of COVID-19 restrictions in May on auctions and open houses, as well as easier conditions in general, which together have supported activity by owner occupiers. In contrast, lending for investment purposes remains weak. And even after taking June’s bump in lending into account, the total value of housing loan commitments in the month was still more than 10 per cent below the levels recorded in March this year.

What I’ve been following in the global economy

What happened:

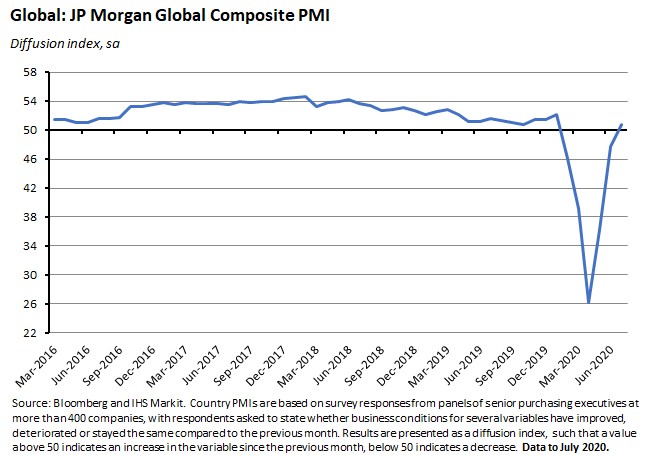

The J P Morgan Global Composite PMI rose to a six-month high of 50.8 in July, moving the indicator for the global economy back into expansionary territory for the first time since January this year.

For the 13 countries for which July composite data was available, nine countries reported PMIs in positive territory, while five of the six industry subsectors covered by the global survey reported positive output growth, with increases for consumer goods producers, business services, financial services, intermediate goods and investment goods. The exception was the consumer services category, which registered another monthly decline, although here the pace of contraction was the weakest recorded during the current downturn.

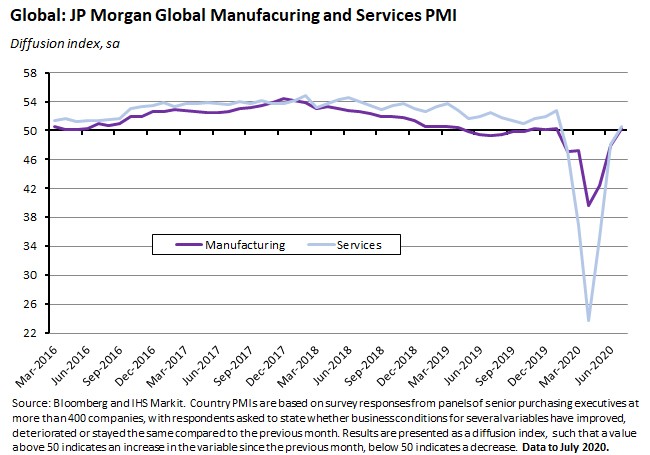

The Global Manufacturing PMI was also back in positive territory for the first time in six months, rising to 50.3 in July, with several of the index components reaching pre-pandemic levels including output and new orders.

Likewise, the Global Services Business Activity Index rose to 50.5 in July and it too was above a neutral reading of 50 for the first time since January.

Why it matters:

The PMI series suggest that, after a terrible second quarter (see next story) global manufacturing and services both started to grow again in July. Even so, the pace of recovery signalled here is very modest and will claw back only a little of the activity lost in the previous months. For example, survey provider IHS Markit estimates that at July's level, the manufacturing PMI survey's output index is consistent with an annual rate of growth of actual output of around 1.5 per cent. While that compares quite favourably to the survey readings in April which were consistent with a 17.7 per cent rate of decline in output, it hardly indicates a strong recovery.

What happened:

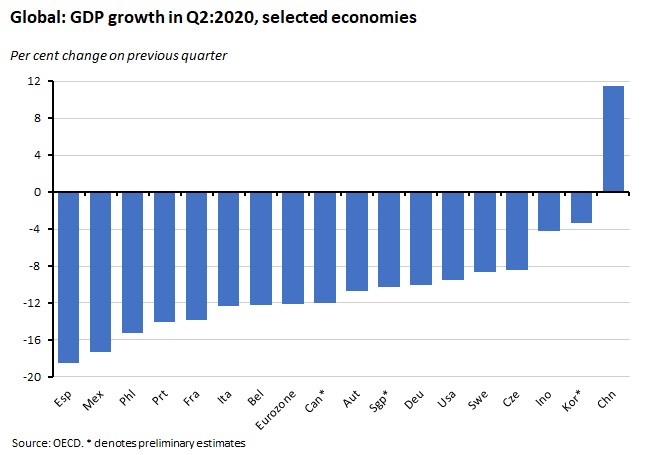

A few weeks ago, we flagged that China’s Q2:2020 GDP result had seen a strong 11.5 per cent quarter-on-quarter increase as the end of lockdowns and the deployment of some policy stimulus had helped the economy bounce back. But China’s GDP profile also benefitted from a ‘first in, first out’ effect. We’ve now had a sample of readings on second quarter GDP results from around the rest of the world economy that capture economies in very different stages of the COVID-19 experience, and they mostly make for pretty grim reading.

European economies have been hit hard: Eurozone GDP fell 12.1 per cent between Q1 and Q2 of this year, marking the biggest decline since the eurozone was created. Spain suffered an 18.5 per cent contraction in output over the same period, Portugal saw output drop more than 14 per cent, France by 13.8 per cent, and Italy by 12.4 per cent. Belgium, Austria and Germany also all endured a double-digit decline in activity. Sweden did relatively better, with GDP ‘only’ declining by 8.6 per cent – although that was still that country’s biggest fall in output since the Second World War (we’ll have to wait a couple of weeks to compare Sweden’s result against the other Nordics).

In North America, the United States saw GDP fall by 9.5 per cent over the quarter (or at an annualised rate of contraction of 32.9 per cent, which is the way US GDP data is typically reported) according to an advance estimate from the Bureau of Economic Analysis. That marks the biggest drop in US post-war history, with the previous record set by a 10 per cent annualised decline in the March quarter of 1958. Preliminary data suggest the size of quarterly contraction in Canada was even larger, while Mexico suffered a dramatic 17.3 per cent collapse in output over the same quarter, leaving that economy on track for its worst recession in a century.

And despite China’s strong result, other Asian economies have suffered from falls in output. Granted the preliminary quarterly GDP declines of 3.3 per cent in Korea and 4.2 per cent in Indonesia look pretty modest relative to the drops in activity seen in Europe and North America, but both the Philippines and Singapore have also experienced double-digit declines in activity.

Why it matters:

While the PMI numbers described above are a more contemporary gauge of trends in economic activity, the Q2 data provide a look back at the damage that COVID-19 has already inflicted on the global economy, with the scale of the hit to output far exceeding that suffered during the global financial crisis.

What I’ve been reading

A new RBA research paper attempts to measure the impact of planning regulations on limiting the supply of apartments in Australia’s cities and hence the resulting excess demand. It does this by estimating the difference between the price paid for new apartments and the cost of their construction, finding that in 2018 home buyers paid an average of $873,000 for a new apartment in Sydney, although it only costs $519,000 to supply, a gap of $355,000 (68 per cent of costs). The authors find smaller gaps of $97,000 (20 per cent of costs) in Melbourne and $10,000 (2 per cent of costs) in Brisbane.

The RBA has also published its August chart pack.

The ABS has released new data on tourism employment and jobs which capture the impact of the summer bushfires and the initial effects of international travel restrictions in response to COVID-19. From March 2019 to March 2020, tourism filled jobs in Australia decreased by three per cent (a fall of 21,900) compared to an increase in jobs of 1.7 per cent (a rise of 243,900) for the whole economy over the same period. That decline in tourism employment is the largest yet seen in the time series, which goes back to September 2004.

Treasury Secretary Stephen Kennedy appeared before the Senate Select Committee on COVID-19 last week and we linked to his opening statement in last time’s note. Here is the testimony that followed.

And here is the opening statement of APRA Chair Wayne Byres to the House of Representatives Standing Committee on Economics, which also includes a helpful list of all APRA’s COVID-19-related initiatives.

Bloomberg’s Daniel Moss reckons that ‘extraordinary is the new vanilla’ for Australian policymakers, zeroing in on the RBA’s resumption of government bond purchases.

A summary of some of the key messages from the 2020 COVID-19 National Tax Summit.

New research from the Productivity Commission (PC) analyses trends in young people’s (defined here as those aged 15-34) incomes from 2001 to 2018. The focus is on the period between 2008 and 2018, which saw the average real incomes of young people decline while that of older Australians continued to increase. The PC describes the former development as a ‘lost decade’ of income growth, one which is mainly explained by a fall in wage income due to a combination of declines in both hours worked and in wage rates as firms offered lower starting wages and more young workers turned to part-time work. There were also declines in income over this period from government transfers and in income from business and investments.

The IMF on global imbalances and the COVID crisis, reflecting on the work set out in the Fund’s latest external sector report.

An FT Big Read on confidence and the US dollar after the greenback’s poorest monthly performance in a decade.

This new NBER working paper looks at how COVID-19 is changing the way some of us (or in this case, knowledge workers in 16 large metropolitan areas in North America, Europe and the Middle East) work, using meeting and email meta-data.

Do active fund managers outperform during market downturns? This research suggests maybe not, at least during COVID-19.

The Summer 2020 edition of the Journal of Economic Perspectives is now available. There’s a symposium on the productivity advantages of cities (particularly interesting in the time of COVID-19 and some of the speculation about what the pandemic might do to our appetite for dense urban spaces) and another on place-based policies.

The WSJ on the financial backing for Oxford’s search for a COVID-19 vaccine.

Also from the WSJ, how the US Fed became the ‘backup lender’ for the world.

The Atlantic has a long essay on how the pandemic defeated America.

A couple of podcasts to finish with. Back in June, I finished reading King and Kay on Radical Uncertainty. Here are the authors in conversation with Russ Roberts on the Econtalk podcast. And here is an Intelligence Squared podcast with Niall Ferguson on what history can teach us about COVID-19.

Latest news

Already a member?

Login to view this content