The relative economic performance of Australian states is improving -- and board director confidence is on the rise.

Economists have long talked about the two-speed nature of Australia’s economy. During the recent resources boom, for example, mining states Western Australia and Queensland grew more quickly than the “rust belt” economies in the south-east. When the boom ended, the reverse was true, as the mining states underperformed. Indeed, WA and Queensland are often epicentres of stronger, then weaker, economic activity while other states like South Australia and Victoria are the traditional manufacturing hubs. Other states are more service-orientated, particularly New South Wales, so tend to have less pronounced economic cycles.

Over time, service industries are becoming more significant in most regions. This development is helping the national economy absorb job losses associated with the end of the mining investment boom and the slow decline of manufacturing. It also helps dampen regional disparities. Employers in education and healthcare, for example, have been the largest generators of jobs nationally in recent years, across all regions.

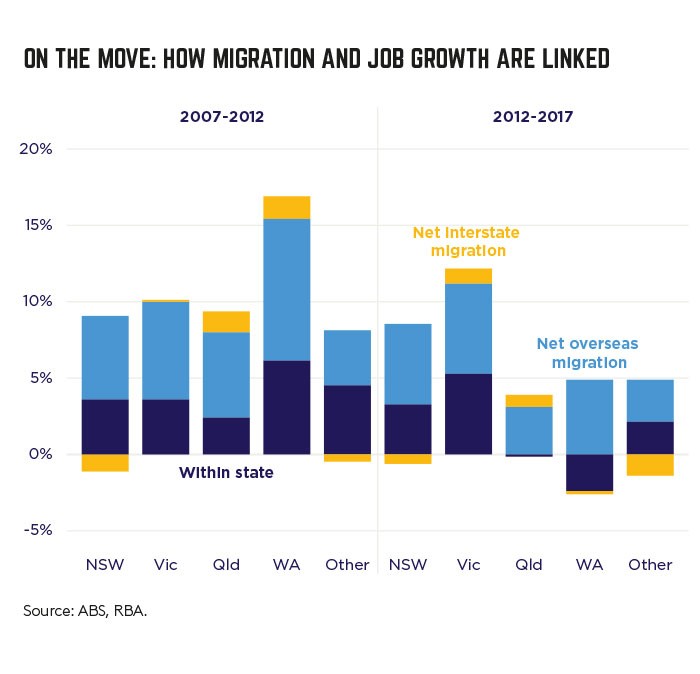

Migration flows have had a lot to do with the relative outperformance of some regions over others. Interstate migration typically ebbs and flows with economic activity as workers follow employment opportunities. These sometimes exaggerated movements of skilled workers, in turn, contribute to economic activity and price movements.

The perception of multi-speed economies is changing. A speech by Reserve Bank Governor Philip Lowe in April indicated that the notion of a two-speed economy is becoming harder to justify. Lowe highlighted that economic performance of the various states has become more similar over time, although there remain significant regional differences.

House prices have become more dissimilar, thanks to previously soaring prices in Sydney and Melbourne. Similarly, wage levels remain significantly higher in the capital cities than in regional areas, reflecting the concentration of higher-paying business services jobs in the central business districts of the major cities.

Prosperous mining-related activities in WA and Queensland drove up both incomes and house prices, but the downside of the booms has seen the opposite. House prices in parts of regional WA and Queensland have been in free fall, while many of the high-paying construction jobs simply disappeared when the resource facilities were completed.

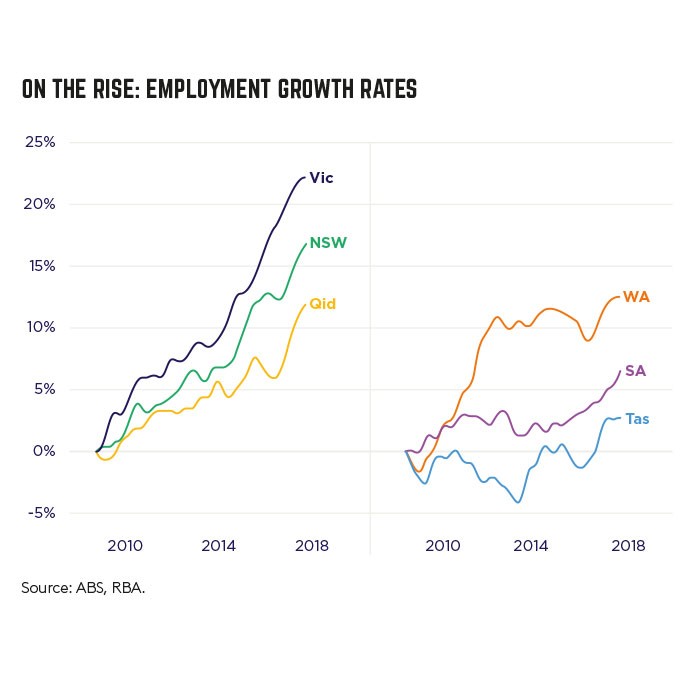

However, disparity in other key areas of regional economic performance is diminishing. Dispersion of the various state unemployment rates, for example, and growth in wages and employment, alongside trends in business confidence and investment, have fallen over the past couple of decades.

It’s a similar story with growth in state final demand. Back in 2012, as the resources euphoria was ending, the gap between growth in the best- and worst-performing state economies was a whopping 15.6 percentage points. Output in WA had expanded nearly 13 per cent that year, while Tasmania’s then-torpid economy had shrunk by almost three per cent.

Last year, however, the growth gap between the winning and losing states had narrowed to less than four percentage points. This smaller discrepancy was for the same rate of expansion in demand in the national economy (3.2 per cent).

Surprisingly, given its characteristics, South Australia (up 4.9 per cent) was the strongest economic performer in 2017; Western Australia was the worst (up only 1.2 per cent). SA benefited, in particular, from the ramping up of defence spending, which masked ongoing problems associated with soaring energy costs and the closure of the vehicle manufacturing sector. Unusually, all states reported positive growth last year — the WA economy had previously been contracting.

Regional differences in economic performance

It’s not surprising that the lingering regional differences in economic performance are reflected in the latest results from the AICD’s Director Sentiment Index. Directors in NSW and Victoria are the most optimistic about the outlook, while those in South Australia and WA are more downbeat. Optimism in Queensland also lags. However, nationally, this measure of the positive outlook among directors has reached the highest level since the Director Sentiment Index was first collected in 2011.

The RBA’s Lowe attributes this transition towards more uniformity across the states and territories to a combination of cyclical and structural factors. The cyclical forces are broad in nature, reflecting the underlying improvement in the performance of the national economy. In a way, the rising national economic tide is lifting all regional boats, albeit to varying degrees.

The structural forces are more difficult to identify, but include a more flexible labour market, changing migration flows, both interstate and overseas, and the rising level of education. Much of these are related to the growth in service industries mentioned above, and the relative decline of manufacturing.

The differing performances of the various state economies over time raise sometimes contentious complexities for policy setting. The complexity applies particularly to official interest rate settings by the central bank, and the carving up of revenue from the goods and services tax (GST) according to capacity and need.

On monetary policy, RBA officials were once accused of wearing “Sydney Harbour sunglasses” as they raised interest rates to cool buoyant activity in the premier state. The other regional economies dealt with the same degree of interest rate pain, without the underlying strength in economic activity. But the Reserve Bank has just a single interest rate instrument at its disposal to calibrate according to economic need. The same constraint applies to overseas jurisdictions, of course, including the pan-European Central Bank that presides over dozens of national economies.

The regional carve-up of GST revenue, all of which goes to the states, is the subject of review by the Productivity Commission.

The existing GST distribution causes considerable consternation, particularly in the west, where the state government receives only a fraction relative to the state’s population share, thanks to previous outperformance by the WA economy. Now, the sandgropers are facing the double whammy of weak activity and a punitive GST distribution.

Of course, the AICD has long argued that rather than squabble over division of the GST pie, we should take what would be the more productive step of growing the size of the pie.

Raising the rate of the GST and broadening the tax base would free up the federal and state governments’ hands to do so many more constructive things with the tax system, including abolishing the more damaging state-based taxes that can exaggerate regional weaknesses.

Latest news

Already a member?

Login to view this content