Budgeting counts at home, but do government debts and deficits really matter? Phil Ruthven AM FAICD investigates.

Households have debt. However, they cannot run their affairs with deficits for long. Governments can do both for a very long time. The net worth of Australian households in 2018, according to the Australian Bureau of Statistics, exceeds $10 trillion and for our three tiers of government is approximately $1.5 trillion, despite the climbing debt, so both sectors are well and truly solvent.

In mid-2018, ABS and IBISWorld data show the average household in Australia has assets of $1.4 million with a debt of more than $250,000 and a net worth of $1.1 million-plus. Even the massive mortgage debt of more than $2 trillion is unlikely to lead to runaway default and misery, even though the nation has the highest household-debt-to-GDP ratio in the developed world.

In short, it is the ability to service debt repayments from income that matters — rather than level of debt — and Australia is managing this well. Interest rates are critical, with current rates the lowest in our history. Rising inflation and interest rates could make debt levels uncomfortable, but household incomes would rise as well to offset such extra outgoings.

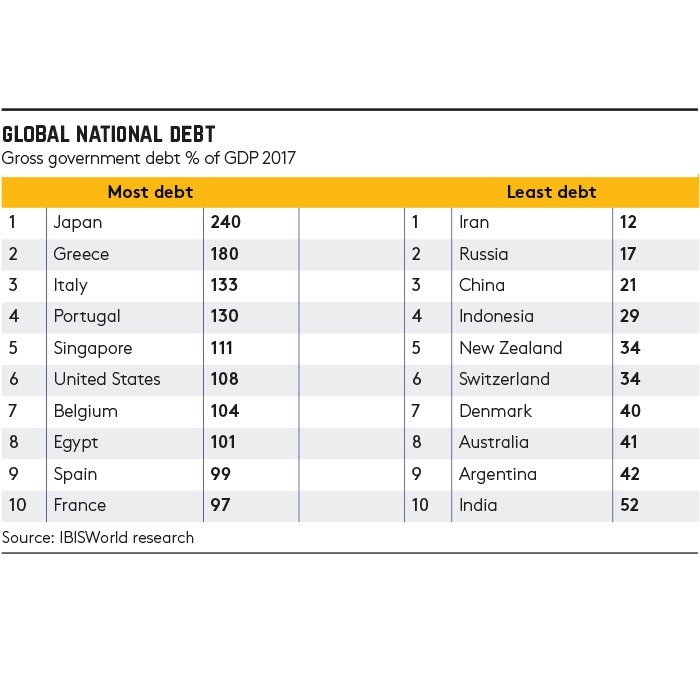

Are governments somehow safe, too, despite the huge debt built up over the past decade as a share of GDP? This includes countries such as Japan (which has the world’s highest government-debt-to-GDP ratio), Greece, Canada and the US (nearing a ratio of 110 per cent, last experienced at the end of WWII). No, they aren’t. The world has been at breaking point since WWII, with many nations at a ratio of 110 per cent or more (see below).

In the past, the solution to lowering the debt ratio was to have a longish period of high inflation with the debt level diluted by rapidly rising nominal GDP. Australia had one year at 25.25 per cent inflation in 1953 and reduced its debt-to-GDP ratio by a similar amount in 12 months flat. The US and other countries can, and may well, repeat this solution over the next decade.

Then there is deficit spending. What’s debilitating to an economy is the government’s failure to live within its means (except where excessive expenditure is directed towards infrastructure), especially when it becomes an unjustifiably chronic habit due to recession or an impending downturn. This is where the US has a serious problem.

It is damning to see only four years of surplus budgets in almost 50 years. Australia has had surpluses in 17 years over half a century — better, but not much to crow about.

The policies of the Trump administration are clearly leading to a worsening of the US’s situation. These actions include tax reductions, the attempted resuscitation of industrial-age industries — now the domain of developing economies with lower wages — a slowing of output if any trade war is expanded and a more inward focus than global outlook.

Governments can get away with a lot more financial imprudence than individuals and households; they can print money when they run short and/or raise taxes, while householders can’t. And they can do it for very long periods of time. But there is a price for that recalcitrance and the failure to continue reforming the economy, labour market and finance market.

The biggest losers this century are the powerful leaders of the 19th and 20th centuries: the US and European Union. Both now have either high taxes and/or debt and deficit problems.

The East is in the ascendancy, with GDP growth three times that of the West’s. But it, too, has nations that need to be careful. China is now the world’s largest economy and while it has a manageable government-debt-to-GDP ratio of under 50 per cent, its deficits are chronic and its business-debt-to-GDP ratio (about 250 per cent) is scary. India, the world’s third-largest economy, is in far better shape with total and government debt-to-GDP ratios among the lowest and safest in the world.

Fiscal rectitude, it would seem, is a global government challenge not just for yesterday’s powerful nations but also for today’s.

Latest news

Already a member?

Login to view this content